COMPREHENSIVE PROBLEM (Continued)

(j) Estimated number of helmets sold in December 2017 = 8,000 helmets

(good Christmas sales!)

Projected wholesale selling price = $40 per helmet

(k) Breakeven point in dollars: Sales dollars at the breakeven point =

Variable costs as a percentage of unit selling price X Sales dollars at

the breakeven point) + Total fixed costs

0.5475X = 0.4525*X + $48,400

0.5475X = $48,400

0.5475X = $88,402

(l) BICYCLE HELMET COMPANY

Sales Budget

For the Month Ended December 31, 2017

Expected unit sales …………………………………………………….. 8,000

COMPREHENSIVE PROBLEM (Continued)

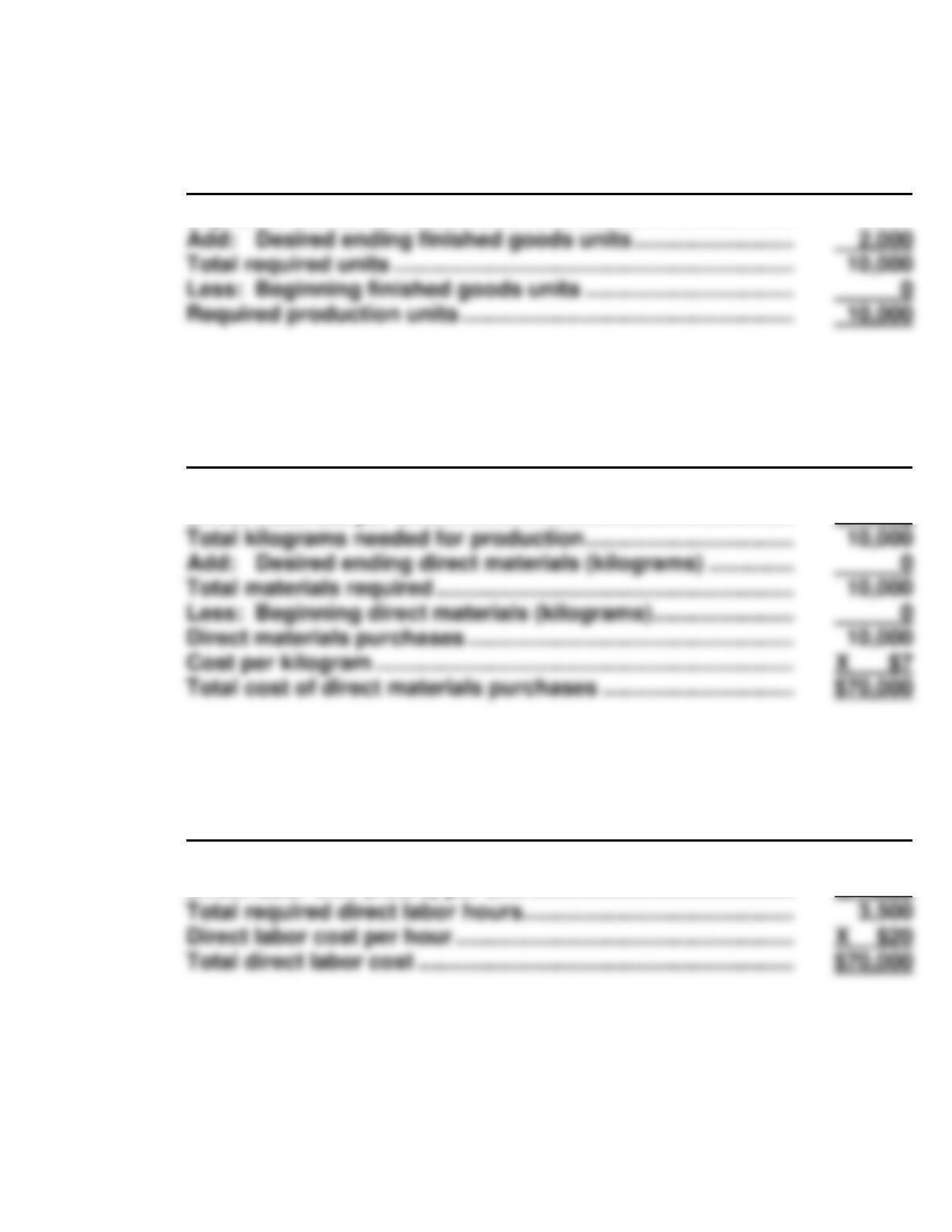

BICYCLE HELMET COMPANY

Production Budget

For the Month Ended December 31, 2017

Expected unit sales ……………………………………………………….. 8,000

BICYCLE HELMET COMPANY

Direct Materials Budget

For the Month Ended December 31, 2017

Units to be produced ……………………………………………………… 10,000

Direct materials per unit …………………………………………………. X 1kg

Total kilograms needed for production ……………………………. 10,000

Add: Desired ending direct materials (kilograms) ………….. 0

BICYCLE HELMET COMPANY

Direct Labor Budget

For the Month Ended December 31, 2017

Units to be produced ……………………………………………………… 10,000

Direct labor time (hours) per unit ……………………………………. X 0.35

COMPREHENSIVE PROBLEM (Continued)

BICYCLE HELMET COMPANY

Selling and Administrative Expense Budget

For the Month Ended December 31, 2017

Variable (sales commissions) ………………………………………. $40,000

BICYCLE HELMET COMPANY

Budgeted Income Statement

For the Month Ended December 31, 2017

Sales revenue (8,000 X $40) ………………………………………….. $320,000

Cost of goods sold [8,000 X $15.13 (from part (e)] ………….. 121,040

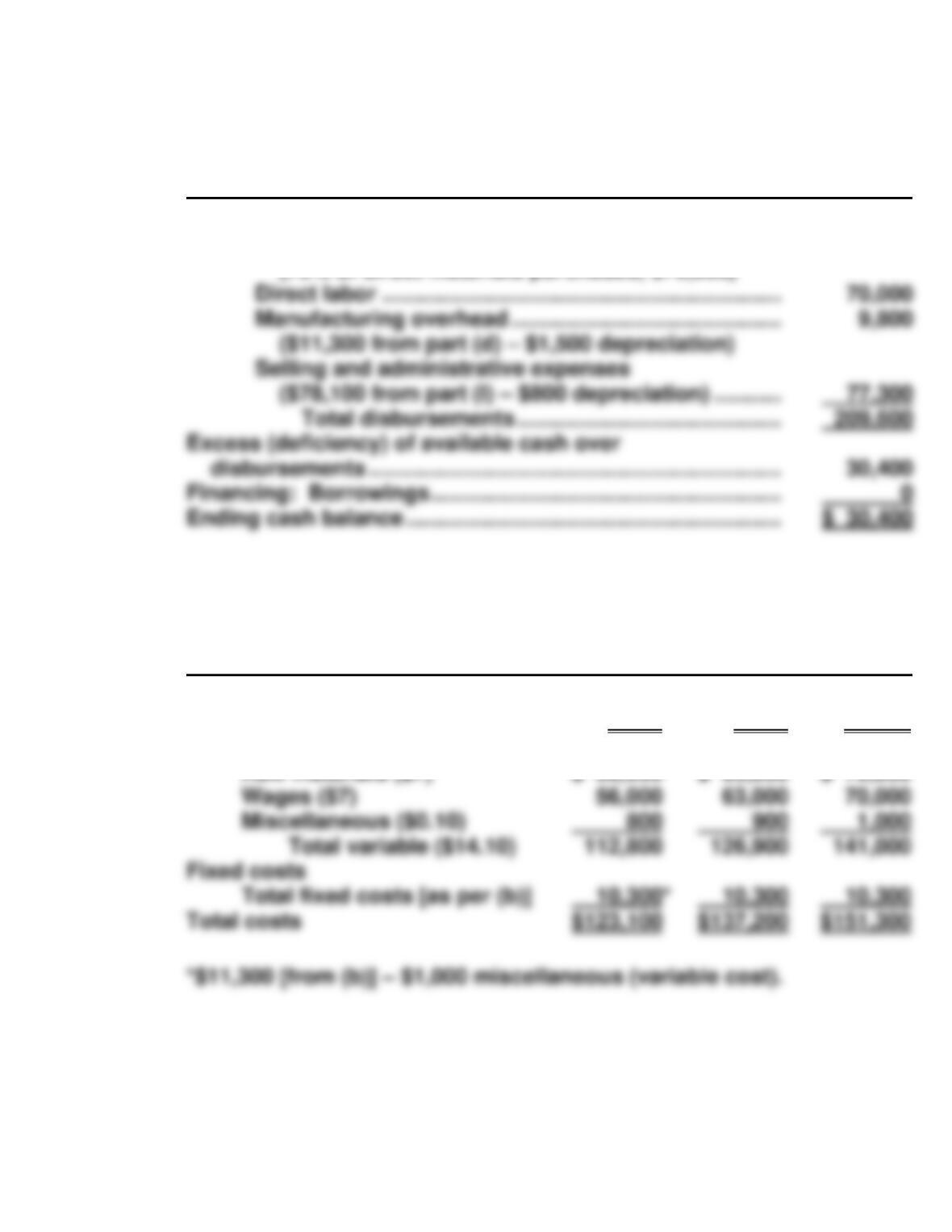

(m) BICYCLE HELMET COMPANY

Cash Budget

For the Month Ended December 31, 2017

Beginning cash balance ……………………………………………….. $ 0

Add: Receipts

Collections from customers

COMPREHENSIVE PROBLEM (Continued)

BICYCLE HELMET COMPANY

Cash Budget (Continued)

For the Month Ended December 31, 2017

Less: Disbursements

Direct materials …………………………………………………. 52,500

(75% of direct materials purchases, $70,000)

Direct labor …………………………..…………………………... 70,000

Manufacturing overhead …………………………………….. 9,800

($11,300 from part (d) – $1,500 depreciation)

(n) BICYCLE HELMET COMPANY

Monthly Flexible Manufacturing Costs Budget

For the Month Ended December 31, 2017

Activity level

Production in units

Variable costs

Raw materials ($7)

8,000

$ 56,000

9,000

$ 63,000

10,000

$ 70,000

COMPREHENSIVE PROBLEM (Continued)

(o) Potential causes of a materials variance: price paid for plastics or any

other raw materials included in helmet; new employees; faulty equipment

(p) Cash payback period: Cost of capital investment ÷ Annual cash inflow

$720,000 ÷ [$30,400 (from part (m) X 12 months)] = 2 years (1.97 years).

CD26-1 CURRENT DESIGNS

(a) Current Designs should accept the special order based on the following

calculations:

Reject Order

Accept Order

Net Income

Increase (Decrease)

Revenues

$0

$25,000*

$25,000

(b) Assuming that Current Designs is currently operating with excess

capacity, it should accept the order based on the calculations shown

in part (a). If Current Designs is currently operating at full capacity, it

Costs

(19,000)

CD26-2 CURRENT DESIGNS

(a) Average investment = ($256,000 + 0) ÷ 2 = $128,000

Annual rate of return = $15,200 ÷ $128,000 = 11.88%

(c)

Event

Time

Period

Cash

Flows

9% Discount

Factor

Present

Value

Net annual cash flow

1-8

$ 47,200

5.53482

$ 261,244

Oven purchase

0

(256,000)

1.00000

(256,000)

(d)

Time

Cash

Present

Net annual cash flow

1-8

$ 47,200

4.48732

$ 211,802

BYP 26-1 DECISION-MAKING ACROSS THE ORGANIZATION

Retain

Old Machine

Purchase

New Machine

Net Income

Increase

(Decrease)

Sales

Costs and expenses

Cost of goods sold

Selling expenses

$6,000,000

4,500,000

900,000

(1)

(3)

$6,600,000

4,620,000

990,000

(2)

(4)

($ 600,000

( (120,000)

( (90,000)

(1) 12,000 X $100 X 5 years = $6,000,000.

BYP 26-2 MANAGERIAL ANALYSIS

(a)

Make

Buy—

Trans-

Tech

Buy—

Omega

Sales Revenue

Variable Manufacturing Cost:

Circuit Board

Plastic Case

Alarms (4 @ $.15 each)

$ 14.50

2.00

0.80

0.60

$ 14.50

0

0

0

$ 14.50

0

0

0

(b) There are several important nonfinancial factors described in the case.

Other factors might be identified as well. The factors described are:

The company is having serious difficulty manufacturing the clocks.

Therefore, it would probably be willing to have someone else manu–

BYP 26–2 (Continued)

(c) Many answers are possible, depending upon each student’s assessment

of the seriousness of the issues mentioned in (b). One answer would

BYP 26-3 REAL-WORLD FOCUS

(a) Before building the special-order new ceiling fans, company manage-

ment must consider the effect of the new lines on current production

capacity, existing and available channels of distribution, the effect on

BYP 26-4 REAL-WORLD FOCUS

The following solution is provided for the year ended July 29, 2012.

(a) The statement of cash flows indicates that capital expenditures

(purchase of plant assets) were $323 million in 2012, an increase of $51

million from the prior year.

BYP 26-5 COMMUNICATION ACTIVITY

To: Maria Fierro, Supervisor

From: , Assistant Chief Accountant

Subject: Recommendation for New Asset

The quantitative analysis pertaining to this management decision is as

follows:

1. Cash payback period: $190,000 ÷ $50,000 = 3.8 years.

2. Annual rate of return: $12,000 ÷ [($190,000 + $0) ÷ 2] = 12.63%.

BYP 26-6 ETHICS CASE

(a) The stakeholders are:

• Yourself.

(b) The ethical issue is:

• An employee’s personal interests and those of his co-workers

and the town versus the best interests of the company and its

stockholders.

BYP 26-7 ALL ABOUT YOU

(a) Chronic homelessness is defined as being on the streets for a year

or more.

(b) Homelessness costs cities money because the chronic homeless have

frequent jail time, shelter costs, emergency room visits and hospital stays.

Some costs per city per homeless person are: New York $40,000; Dallas

$50,000; San Diego $150,000.