EXERCISE 26-10

(a) 1. Cash payback period: $190,000 ÷ $50,000 = 3.8 years.

2. Annual rate of return: $12,000 ÷ [($190,000 + $0) ÷ 2] = 12.63%.

EXERCISE 26-11

(a)

Project

Capital

Investment

÷

Net Annual Cash

Flows*

=

Internal

Rate of

Return

Factor

Closest

Discount

Factor

Internal

Rate of

Return

22A

$240,000

÷

($15,500 + $40,000)

=

4.324

4.35526

10%

EXERCISE 26-12

(a) Project A: ($50,000 X 3.88965) – $200,000 = $(5,518)

Project B: ($65,000 X 5.03295) – $300,000 = $27,142

decision would change. Now both projects are acceptable.

SOLUTIONS TO PROBLEMS

PROBLEM 26–1A

(a)

Reject

Order

Accept

Order

Net Income

Increase

(Decrease)

Revenues (10,000 X $28)

$0

$280,000

$ 280,000

(1) Variable costs = $3,600,000 – $960,000 = $2,640,000;

$2,640,000 ÷ 120,000 units = $22.00 per unit;

10,000 X $22.00 = $220,000.

(b) Yes, the special order should be accepted because net income will

increase by $37,500.

PROBLEM 26–2A

(a)

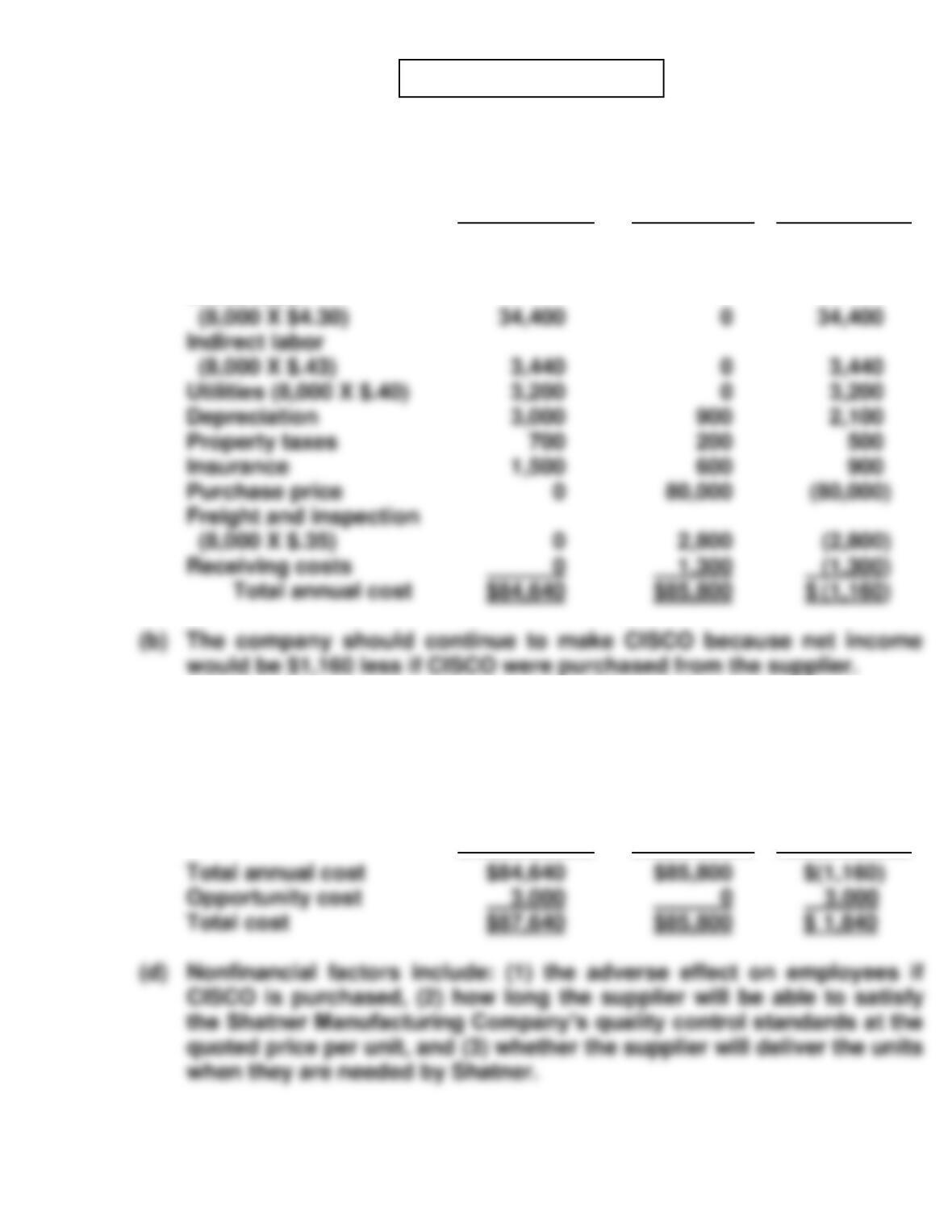

Make CISCO

Buy CISCO

Net Income

Increase

(Decrease)

Direct materials

(8,000 X $4.80)

Direct labor

(8,000 X $4.30)

$38,400

34,400

$ 0

0

($38,400)

( 34,400)

(b) The company should continue to make CISCO because net income

would be $1,160 less if CISCO were purchased from the supplier.

(c) The decision would be different. Because of the opportunity cost of

$3,000, net income will be $1,840 higher if CISCO is purchased as

shown below:

Make CISCO

Buy CISCO

(Decrease)

Net Income

Increase

PROBLEM 26–3A

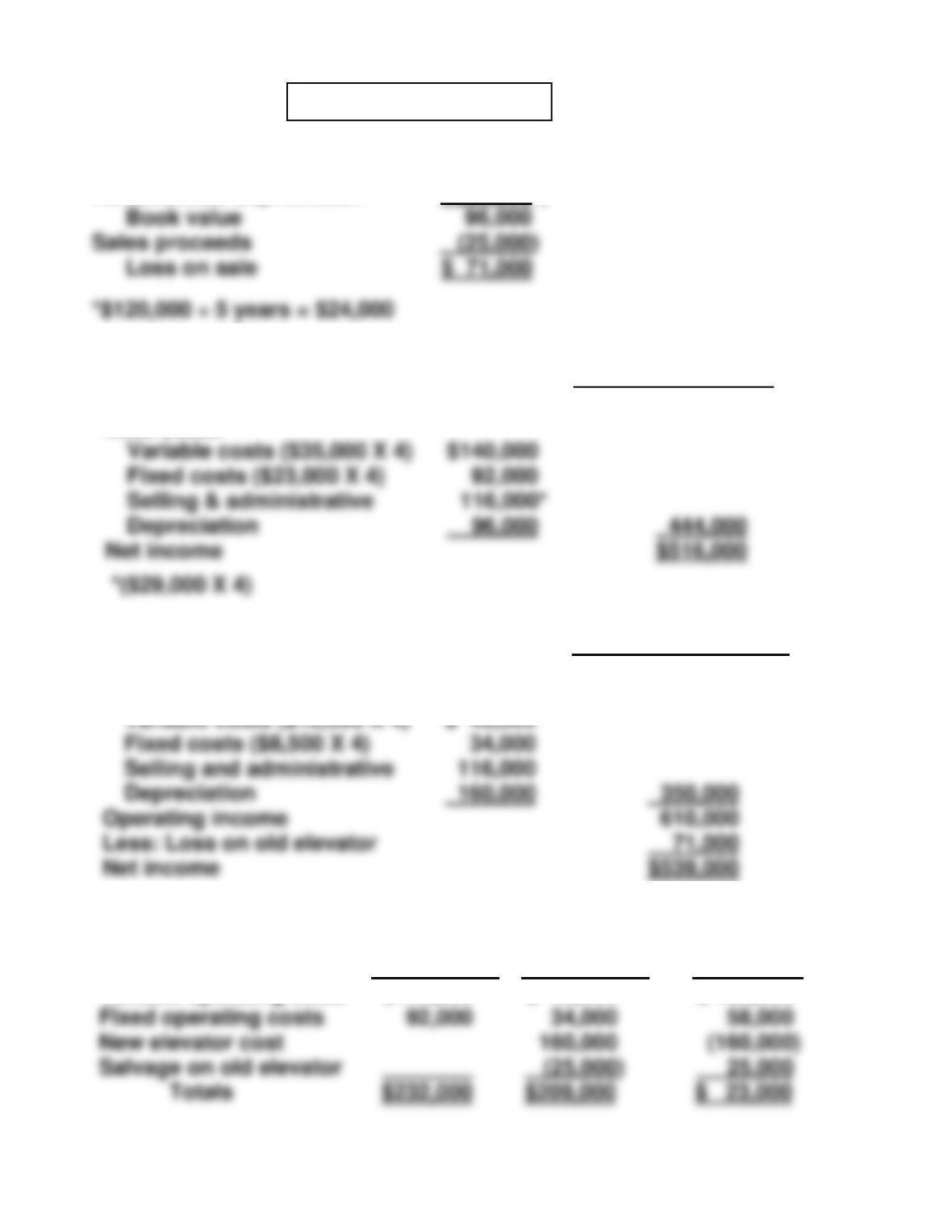

(a)

Cost

$120,000

Accumulated depreciation

(24,000*)

Book value

96,000

(b) (1)

Retain Old Elevator

Revenues ($240,000 X 4 yrs.)

$960,000

Less costs:

Variable costs ($35,000 X 4)

$140,000

Fixed costs ($23,000 X 4)

Selling & administrative

Depreciation

96,000

Net income

$516,000

(2)

Replace Old Elevator

Revenues

$960,000

Less costs:

Variable costs ($10,000 X 4)

$ 40,000

Fixed costs ($8,500 X 4)

34,000

Selling and administrative

Depreciation

Operating income

Less: Loss on old elevator

71,000

Net income

92,000

Sales proceeds

Loss on sale

$ 71,000

PROBLEM 26-3A (Continued)

(d) MEMO

TO: Ron Richter

FROM: Student

SUBJECT: Relevant Data for Decision to Replace Old Elevator

When deciding whether or not to replace any old equipment, the analysis

should only include cost data relevant to the replacement decision. The

$71,000 loss that would be experienced if we replace the old elevator with

PROBLEM 26–4A

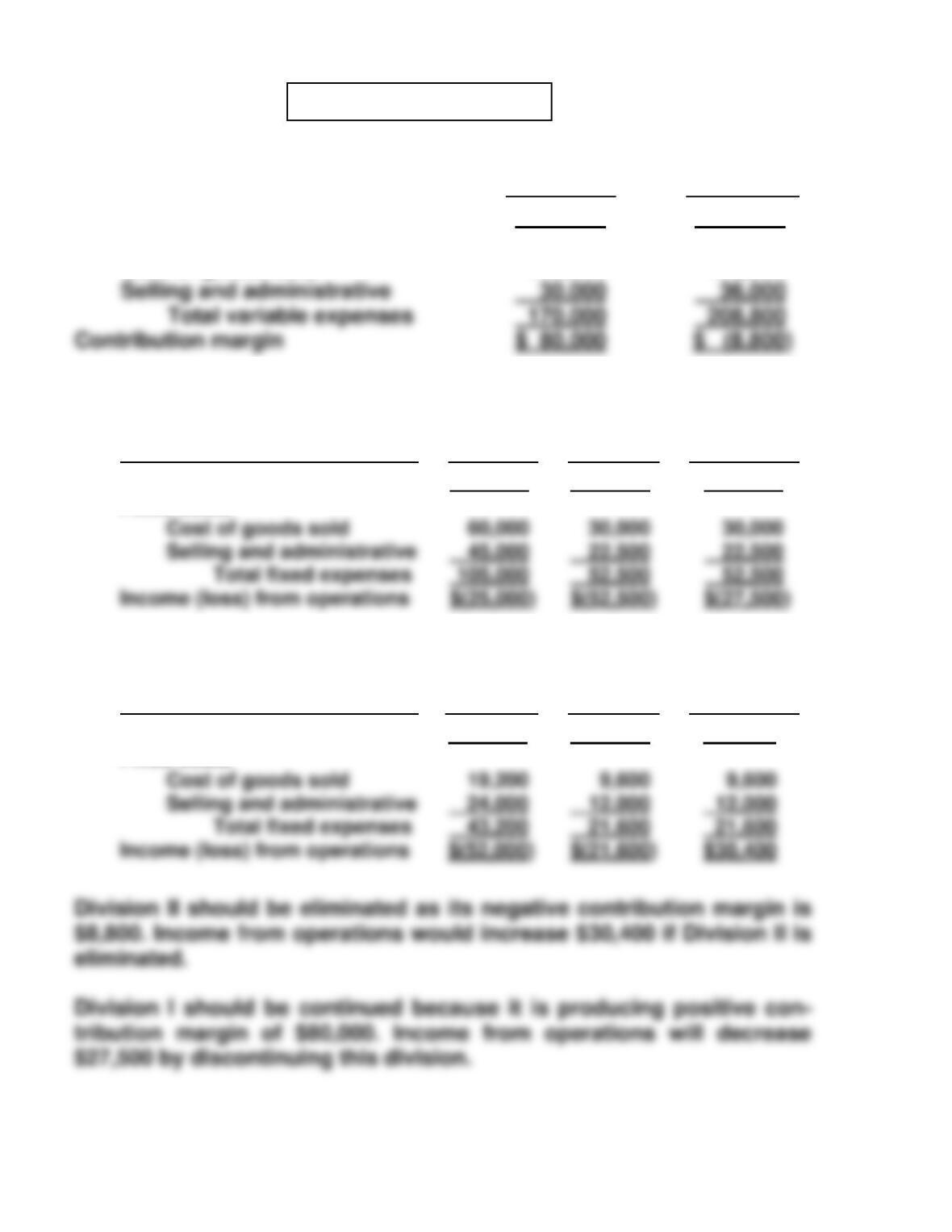

(a)

Division I

Division II

Sales

Variable costs

Cost of goods sold

$250,000

140,000

$200,000

172,800

(b)

(1)

Division I

Continue

Eliminate

Net Income

Increase

(Decrease)

Contribution margin (above)

Fixed costs

Cost of goods sold

$(80,000)

(60,000)

$( 0)

(30,000)

$(80,000)

30,000

(2)

Division II

Continue

Eliminate

Net Income

Increase

(Decrease)

Contribution margin (above)

Fixed costs

Cost of goods sold

$ (8,800)

(19,200

$( 0)

( 9,600)

$ 8,800

( 9,600

PROBLEM 26-4A (Continued)

(c) BRISLIN COMPANY

CVP Income Statement

For the Quarter Ended March 31, 2017

Divisions

I

III

IV

Total

Sales

Variable costs

Cost of goods sold

$250,000

140,000

$500,000

240,000

$450,000

187,500

$1,200,000

567,500

(1) Division’s fixed cost of goods sold plus 1/3 of Division II’s

unavoidable fixed cost of goods sold [$192,000 X (100% – 90%) X

50% = $9,600]. Each division’s share is $3,200.

PROBLEM 26-5A

(a) Project Bono $160,000 ÷ ($14,000 + $32,000) = 3.48 years

Project Edge

Year

Cash Flow

Cumulative Cash Flow

1

2

$53,000 ($18,000 + $35,000)

$52,000 ($17,000 + $35,000)

$ 53,000

$105,000

Project Clayton

Year

Cash Flow

Cumulative Cash Flow

1

2

$67,000 ($27,000 + $40,000)

$63,000 ($23,000 + $40,000)

$ 67,000

$130,000

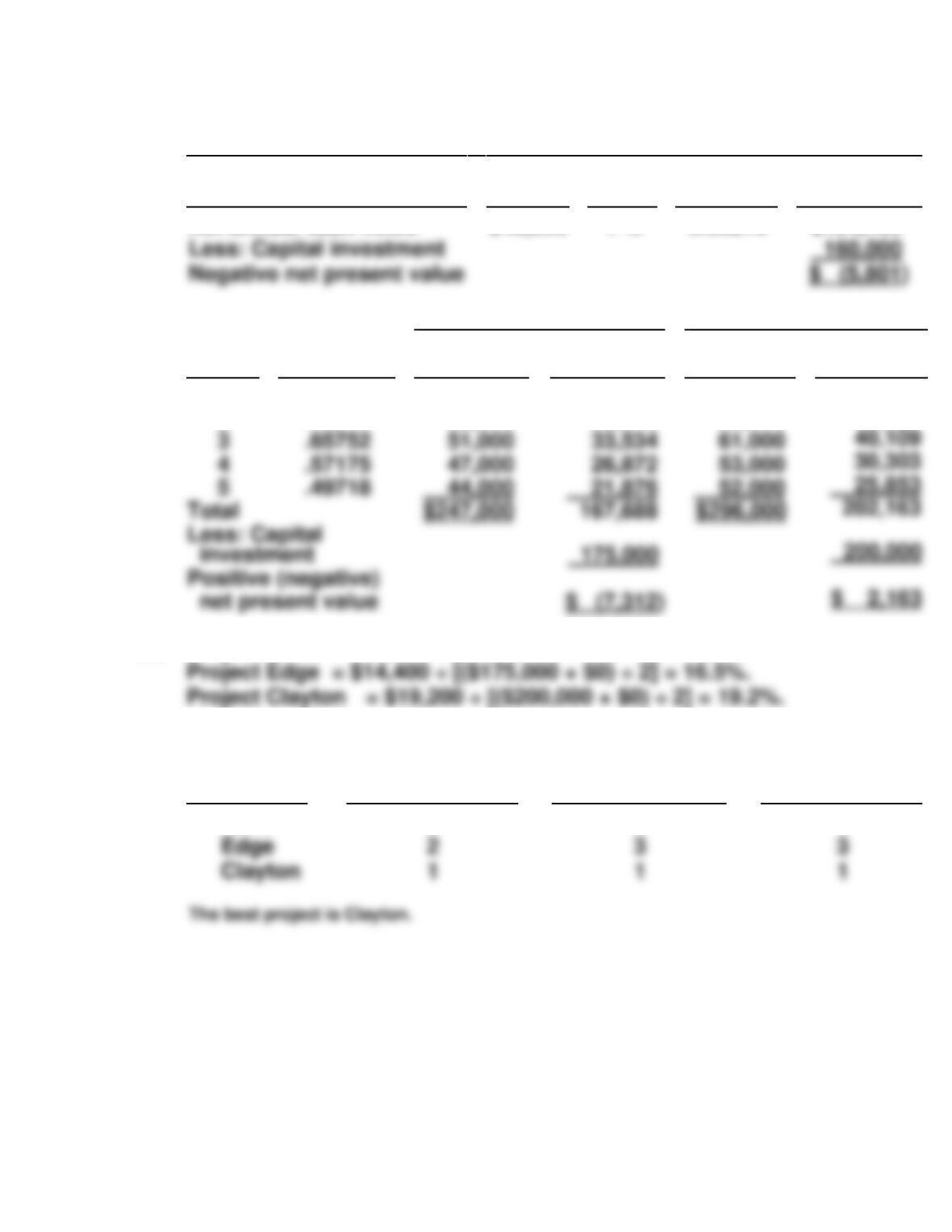

PROBLEM 26-5A (Continued)

(b) Project Bono

Item

Amount

Years

PV Factor

Present

Value

Net annual cash flows

Less: Capital investment

Negative net present value

$46,000

1–5

3.35216

$154,199

160,000

$ (5,801)

Project Edge

Project Clayton

Year

Discount

Factor

Cash

Flow

PV

Cash

Flow

PV

1

2

.86957

.75614

$ 53,000

52,000

$ 46,087

39,319

$ 67,000

63,000

$ 58,261

47,637

(c) Project Bono = $14,000 ÷ [($160,000 + $0) ÷ 2] = 17.5%.

(d)

Project

Cash Payback

Net

Present Value

Annual

Rate of Return

Bono

3

2

2

5

44,000

PROBLEM 26-6A

(a)

(1)

Annual

Net Income

(2)

Annual

Cash Inflow

Sales

Expenses

Drivers’ salaries

*$108,000*

* 48,000*

$108,000

48,000

(b) 1. Cash payback period = $75,000 ÷ $30,000 = 2.50 years.

(c) Present value of annual cash inflows ($30,000 X 2.28323*) = $68,497

Less: Capital investment = 75,000

Net present value = $ (6,503 )

(d) The computations show that the commuter service is not a wise

investment for these reasons: (1) annual net income will only be

Total expenses

PROBLEM 26-7A

(a)

(1) Option A

Cash

Flows

X

8% Discount

Factor

=

Present

Value

Present value of net annual cash flows

Present value of cost to rebuild

a$41,000a

( (50,000)

X

X

5.20637

.73503

=

=

($213,461)

( (36,752)

(2) The internal rate of return can be approximated by finding the discount

rate that results in a net present value of approximately zero. This is

accomplished with a 11% discount rate.

Cash

Flows

X

11% Discount

Factor

=

Present

Value

a$41,000a

(1) Option B

Cash

Flows

X

8% Discount

Factor

=

Present

Value

Present value of net annual cash flows

Present value of cost to rebuild

b$49,000b

0

X

X

5.20637

.73503

=

=

$255,112

0

PROBLEM 26-7A (Continued)

(2) Internal rate of return on Option B is 12%, as calculated below:

Cash

Flows

X

12% Discount

Factor

=

Present

Value

Present value of net annual cash flows

Present value of cost to rebuild

b$49,000b

0

X

X

4.56376

.63552

=

=

$223,624

0

COMPREHENSIVE PROBLEM: CHAPTERS 19 TO 26

Note to instructor: Solutions will vary by student. This is an extensive,

comprehensive problem whose solution will depend on the assumptions

and computations in previous parts. While the variety of assumptions that

may be made by students are valuable in themselves, requiring students to

Product Costs

Item

Direct

Materials

Direct

Labor

Manufacturing

Overhead

Period

Costs

Totals

10,000

Rent on production

equipment

Insurance on building

Raw materials (plastics,

$ 6,000

1,500

COMPREHENSIVE PROBLEM (Continued)

(d) Assume first month of operations is December 2017.

BICYCLE HELMET COMPANY

Cost of Goods Manufactured Schedule

For the Month Ended December 31, 2017

Work in process, December 1 $ 0

Direct materials

Raw materials inventory $ 0

(Dec. 1)

Manufacturing overhead

Rent on production equipment $ 6,000

Insurance on building 1,500

Utility costs 900

(e) Assume 10,000 helmets will be produced the first month of operations.

COMPREHENSIVE PROBLEM (Continued)

find it useful, using a process costing system, to identify the cost of

(g) In a process cost system, manufacturing costs (direct materials, direct

labor, and manufacturing overhead) are assigned to Work in Process

accounts for each department or process. As helmets are completed,

the cost of the work in process is transferred out to Finished Goods

(h)

Item

Variable

Costs

Fixed

Costs

Total

Costs

Rent on production equipment

Insurance on building

Raw materials (plastics,

polystyrene, etc.)

Utility costs

Office supplies

$ 70,000

$ 6,000

1,500

900

300

$ 6,000

1,500

70,000

900

300