CHAPTER 26

CAPITAL BUDGETING

Brief Learning

Exercises Topic Objectives Skills

B. Ex. 26.1 Understanding payback period 26-3 Analysis

B. Ex. 26.2 Use of return on investment 26-3 Analysis

B. Ex. 26.3 Comparing NPV and required rate of return 26-3, 26-4 Analysis

B. Ex. 26.4 Net present value computations 26-3 Analysis

B. Ex. 26.5 Computations for payback period 26-3 Analysis

B. Ex. 26.6 Capital investment challenges 26-1, 26-2 Analysis, judgment

B. Ex. 26.7 Net present value and required rate of return 26-3, 26-4 Analysis, judgment

B. Ex. 26.8 Capital budgeting behaviors 26-5 Analysis, judgment

B. Ex. 26.9 Net present value analysis 26-3 Analysis

B. Ex. 26.10 Nonfinancial investment concerns 26-2

Analysis, communication,

judgment

Learning

Exercises Topic Objectives Skills

26.1 Accounting terminology 26-1–26-5 Analysis

26.2 Payback period 26-1–26-3

Analysis, communication,

judgment

26.3 Understanding return on average investment 26-1, 26-3 Analysis

26.4 Discounting cash flows 26-3 Analysis

26.5 Understanding net present value relationships 26-3 Analysis

26.6 Analyzing a capital investment proposal 26-1, 26-3 Analysis

26.7 Analyzing capital investment proposal 26-1–26-4

Analysis, communication,

judgment

26.8 Analyzing capital investment proposal 26-1, 26-3 Analysis

26.9 Competing investment proposals

26-1, 26-2,

26-5

Analysis, communication,

judgment

26.10 Replacing existing equipment

26-1–26-3,

26-5

Analysis, communication,

judgment

26.11 Gains and losses on sale of equipment 26-3 Analysis

26.12 Depreciation effects on cash flows 26-3 Analysis

OVERVIEW OF BRIEF EXERCISES, EXERCISES, PROBLEMS, AND CRITICAL

THINKING CASES

Learning

Exercises Topic Objectives Skills

26.13 Net present value in a not-for-profit 26-2, 26-3

Analysis, communication,

judgment

26.14 NPV of uneven cash flows 26-3 Analysis

26.15

Real World: Home Depot’s present value of

store closing costs

26-1–26–3

Analysis, communication,

judgment , research

Problems Learning

Sets A, B

Topic Objectives Skills

26.1 A,B

Capital budgeting and determination of

annual net cash flow

26-1–26–4 Analysis

26.2 A,B Analyzing capital investment proposals 26-1–26–4

Analysis, communication,

judgment

26.3 A,B Analyzing capital investment proposals 26-1–26–4

Analysis, communication,

judgment

26.4 A,B Capital budgeting using multiple models 26-1–26–4

Analysis, communication,

judgment

26.5 A,B Capital budgeting using multiple models 26-1–26–4

Analysis, communication,

judgment

26.6 A,B Analyzing a capital investment proposal 26-3 Analysis

26.7 A,B

Considering financial and nonfinancial

factors

26-1–26-4

Analysis, communication,

judgment

26.8 A,B

Analyzing competing capital investment

proposals

26-1–26-4

Analysis, communication,

judgment

26.9 A,B

Analyzing competing capital investment

proposals

26-1–26-5

Analysis, communication,

judgment

Critical Thinking Cases

26.1 How much is that laser in the window? 26-2–26-4

Analysis, communication,

judgment

26.2 Dollars and cents versus a sense of ethics 26-1–26-5

Analysis, communication,

research

26.3 International investments in outsourcing

26-1, 26-2,

26-5

Analysis, communication,

judgment

26.4 Real World: Red Robin Gourmet 26-5 Analysis, communication

Burgers judgment

(Ethics, fraud and corporate governance)

DESCRIPTIONS OF PROBLEMS AND CRITICAL THINKING CASES

Problems (Sets A and B)

26.1 A,B

Toying with Nature/Monster Toys 30 Strong

Covers incremental analysis and three basic capital budgeting

techniques in a single problem.

26.2 A,B

Hibbing Technology/Virginia Technology 25 Medium

Basic capital budgeting. Compute the payback period, return on average

investment, and net present value of two investment alternatives.

Student must decide which investment to select.

26.3 A,B

Welsh Industries/Jason Equipment Co. 25 Medium

Basic capital budgeting. Compute the payback period, return on average

investment, and net present value of two investment alternatives.

Student must decide which investment to select.

26.4 A,B

Marengo/Samba 25 Medium

Basic capital budgeting. Compute the payback period, return on average

investment, and net present value of two investment alternatives.

Student must decide which investment to select.

26.5 A,B

V.S. Yogurt/I.C. Cream 25 Medium

Basic capital budgeting. Compute the payback period, return on average

investment, and net present value of two investment alternatives.

Student must decide which investment to select.

26.6 A,B

Pathways Appliance Company/Cafield Appliance Company 30 Strong

Prepare a schedule showing the estimated incremental net income from

proposed introduction of a new product. Compute annual cash flow,

payback period, return on average investment, and net present value of

the investment proposal.

26.7 A,B

Doctors 40 Strong

Students must determine whether it is profitable for several doctors to

invest their money in an expensive piece of testing equipment. Requires

financial analysis and consideration of nonfinancial aspects of their

decision.

Below are brief descriptions of each problem and case. These descriptions are accompanied by the

estimated time (in minutes) required for completion and by a difficulty rating. The time estimates assume

use of the partially filled-in working papers.

26.8 A,B

Jefferson Mountain/Jackson Mountain 50 Strong

A small ski resort must decide between alternative investment

proposals. Students are asked to analyze financial and nonfinancial

considerations relevant to the decision.

26.9 A,B Sonic, Inc./Boom, Inc. 45 Strong

A software company is trying to decide how to market their software.

Students are asked to analyze financial and nonfinancial

considerations relevant to the decision.

Critical Thinking Cases

26.1

The Case of the Costly Laser

Compute the net present value of a proposal to replace existing

equipment with new, more efficient equipment. The sale of the

existing equipment will involve a large loss. Students are asked to

comment on the relevance of this sunk cost.

26.2

Grizzly Community Hospital 60 Strong

A small community hospital considers a major capital investment in

a regional kidney center. Students are asked to analyze financial and

nonfinancial information relevant to the decision, explore

alternative uses of resources, and help the hospital define its role.

26.3 International Investments in Outsourcing 20 Medium

The cash flows associated with offshore investments are identified.

Ethical considerations of asking domestic employees to train their

international replacements are considered.

26.4 Red Robin Gourmet Burgers 30 Medium

Ethics, Fraud & Corporate Governance

Governance violations at Red Robin Gourmet Burgers leads to

capital budgeting conflicts of interest.

SUGGESTED ANSWERS TO DISCUSSION QUESTIONS

1.

2.

3.

4.

5.

6.

7.

8.

Capital budgeting is the process of planning and evaluating investments in plant assets. Capital

Corporate management would allow a lower rate of return for newly developing divisions, when

The major shortcoming in using the payback period as the sole criterion in capital budgeting

Timing differences are very important in present value computations and projects that have more

significant cash inflows after several years will inevitably have lower present values than projects

The present value of a future amount is the amount of money which, if invested today to earn a

Factors to consider in establishing a minimum required return on an investment proposal may

Discounting cash flows takes into consideration the timing of the earnings stream. The return on

Nonfinancial considerations associated with the installation of a fire sprinkler system may include

9.

10.

13.

14.

15.

If a company is replacing an asset, the first income tax consequence to be considered is

t

If an investment with no salvage value has a payback period that exceeds its estimated life, the

An investment’s contribution to income is not the same as its incremental cash flow because

One way to ensure that employee estimates of the costs and benefits of capital investments are

not overly optimistic or pessimistic is to implement a system for auditing capital budget

decisions. With an audit system in place, employees will be aware that their estimates will be

checked against actual results, and any biases discovered. Another step firms can take is to

Some capital investment proposals which may favor nonfinancial factors include a pollution

B. Ex. 26.1 The payback period is computed as follows:

B. Ex. 26.2 Proposal 1:

Proposal 2:

B. Ex. 26.3

B. Ex. 26.4 134,080$

B. Ex. 26.6

SOLUTIONS TO BRIEF EXERCISES

The estimated cash flows of replacement equipment often is relatively easy to estimate

because the company has experience with similar of assets. Thus, replacing a fleet of

If the investment proposal has a positive net present value of $20 when an 8% discount

Present value of expected annual cash flows ($40,000 × 3.352)

B. Ex. 26.6

(continued)

B. Ex. 26.7

B. Ex. 26.8

B. Ex. 26.9

Present value of expected annual cash savings ( X × 4.623) …………………….

= X

B. Ex. 26.10

If the initial outlay for the project is $125,000 and the net present value of the

future cash flows is $120,000, then the present value (based on the 12% required

The net present value cash flows could be optimistic because the outside sales

Sam’s should also consider the potential cannibalization of in-store sales, the

Alternatively, new technology is inherently difficult to estimate. For example, when

VCRs, DVD players, or I-Pods were first introduced to the market, the prices were

set fairly high because manufacturers could not estimate demand. As demand grew

Present value of proceeds from disposal ($100,000 × .630) ……………………

Total Present Value of investment’s future cash flows……………………

Cost of investment …………………………………………………………

SOLUTIONS TO EXERCISES

Ex. 26.1 a.

Ex. 26.2 a.

b.

c.

Incremental analysis

Based strictly on payback periods, the Akron Industries machine is more

attractive because its cost will be recovered one year sooner than the cost of the

If the Akron Industries machine has a payback period of 60 months (or 5 years),

its cost can be computed as follows:

Cost = $5,000 x 5 years = $25,000

A 6-year payback period for the Toledo Tools machine is computed as follows:

Sunk cost

Capital budgeting

Return on average investment

Salvage value

Payback period

cost in determining its net present value.)

Present value

Discount rate

Ex. 26.3

Thus, the average estimated net income of Investment B is:

Average Estimated Net Income =18% x $45,000 = $8,100

The average investment of Investment C is:

The missing data for each investment proposal are solved for as follows:

Investment A

Thus, the return on average investment of Investment A is:

Investment B

Investment C

Average Investment = $6,000 ÷ 25% = $24,000

Thus, the estimated salvage value of Investment C is:

d.

Ex. 26.5

Present value of annual net cash flows discounted at 10% for 10 years

Present value of annual net cash flows discounted at 12% for 10 years

Thus, the original investment cost of Investment D is:

Investment Cost = ($40,000 × 2) – $2,000 = $78,000

Average Investment = $8,000 ÷ 20% = $40,000

Investment A

($20,000 × 3.352) + ($10,000 × 2.283) = $67,040 + $22,830 = $89,870

There are several ways to approach this problem. Shown below is the present value

of $20,000 received annually for 5 years plus the present value of the additional

Investment B

The missing information for each investment is solved for as follows:

Ex. 26.3

(continued)

Investment D

The average investment of Investment D is:

Ex. 26.4 a.

$40,000 × .061 = $2,440

($16,000 × 3.352) + ($20,000 × .497) = $53,632 + $9,940 = $63,572

Ex. 26.5

(continued)

b.

$500,000 ÷ 2

c.

Return on average investment:

Net present value of proposal, discounted 5 years at an annual rate of 10%:

Total present value of annual net cash flows

Average Investment

Given a net present value of zero, we can conclude that the discounted present value of the

future cash flows associated with Investment B must equal the investment’s original cost of

$141,250.

Investment C

Thus, the annual cash outflows associated with the investment can be computed as follows:

($37,000 – Cash Outflows) × 5.650 = $141,250

($37,000 × 5.650) – (5.650 × Cash Outflows) = $141,250

$209,050 – (5.650 × Cash Outflows) = $141,250

Cash Outflows = $67,800 ÷ 5.650 = $12,000

$209,050 – $141,250 = (5.650 × Cash Outflows)

$67,800 = (5.650 × Cash Outflows)

($19,000 – $7,000) × PV Factor = $80,520

$12,000 × PV Factor = $80,520

PV Factor = $80,520 ÷ $12,000 = 6.71

Thus, the discount rate associated with the investment that yields a net present value of zero

can be computed as follows:

Present value of annual net cash flows discounted at ?% for 10 years

Ex. 26.7 a.

b.

c.

Ex. 26.9 a.

This is a very complex question with no single correct answer. If all division

managers commonly overstate cash flow projections in order to obtain funding

There are several nonfinancial issues that Northwest Records should consider.

First, musical tastes often change very quickly. As such, an estimate that the

Present value of net cash flows of $250,000 per year for 4

The payback period of the Seattle Sound investment is computed as follows:

The net present value of the Seattle Sound investment is computed as follows:

Ex. 26.9

b.

Ex. 26.10

a. Net present value:

Calculate depreciation expense under each alternative:

New machine ($120,000 ÷ 5 years) 24,000$

Old machine ($100,000 ÷ 5 years) 20,000

Increase in depreciation of new machine 4,000$

Calculate the incremental increase in annual income taxes resulting

from the purchase of the new machine:

Cost savings of new machine 34,000$

Calculate the incremental increase in annual cash flow resulting from

the purchase of the new machine:

Cost savings of new machine 34,000$

Less: Increase in income taxes (see above) 12,000

Increase in annual cash flow 22,000$

Calculate the tax savings resulting from the loss on the sale of the

old machine:

Book value of old machine 100,000$

Proceeds from sale 20,000

Loss on sale of disposal 80,000$

Income tax rate 40%

Tax savings resulting from loss on disposal 32,000$

The net present value of the new machine can now be computed as follows:

Present value of incremental annual cash flows discounted at 12%

for five years is $22,000 × 3.605 (from Exhibit 26.4) 79,310$

Present value of tax savings from loss on disposal of the old machine

discounted at 12% for 1 year is $32,000 × .893 (from Exhibit 26.3) 28,576

Present value of proceeds from sale of old equipment 20,000

Total present value 127,886$

Less: Cost of new machine 120,000

Net present value 7,886$

(Continued on the following page)

There are numerous controls that might be implemented to discourage the

overstatement of capital budgeting estimates. First, whenever possible, assumptions and

Less: Increase in depreciation (see above) 4,000

Increase in pretax income 30,000$

Income tax rate 40%

Increase in income taxes 12,000$

Ex. 26.10 b.

c.

Ex. 26.11

a. b.

$ 80,000 $ 20,000

Ex. 26.12

$ 150,000

c.

Perhaps the most important nonfinancial consideration for EnterTech to

consider is the future demand for portable CD players. If demand for the

product is less than five years, the investment in the new machine is far less

Because the decision of whether or not to invest in the new machine is highly

dependent on the cost savings estimate, EnterTech may want to obtain a second

Cash proceeds of sale

The hospital should consider how many MRIs currently used by competing

hospitals in the surrounding area, a consideration that could influence the

Sales

$ 18,000 $ (42,000)

$ 72,800

Tax Savings at 40%

Net cash effect of sale:

($80,000 – $7,200)

Taxes Paid at 40%

Gain (Loss) on Sale

Ex. 26.14

5% rate 5% NPV 8% rate 8% NPV

Year 1 0.952 $142,800 0.926 $138,900

Ex. 26.15

Note to instructor: To generate class discussion, have students identify any nonfinancial

factors that pertain to store closings. For instance, a primary nonfinancial factor is how

Home Depot bases its store closing decisions by comparing the related

undiscounted cash flows with carrying values of the stores targeted for closure.

Amount

$150,000

Year 2 0.907 199,540 0.857 188,540

Year 3 0.864 216,000 0.794 198,500

$220,000

$250,000

SOLUTIONS TO PROBLEMS SET A

30 Minutes, Strong PROBLEM 26.1A

TOYING WITH NATURE

a.

Estimated sales (80,000 units @ $6) 480,000$

Less estimated incremental costs:

Variable manufacturing costs (80,000 units @ $2.50) 200,000$

Fixed manufacturing costs (except depreciation) 45,000

b. Computation of annual net cash flow:

Cash receipts 480,000$

Less cash outlays:

Variable manufacturing costs 200,000$

Fixed costs (other than depreciation) 45,000

Selling and general expenses 55,000

Income taxes expense 28,000 328,000

Annual net cash flow from sale of new product 152,000$

c. (1)

(3) Net present value of project, discounted at 15%:

Total present value of annual net cash flows ($152,000 × 2.283) 347,016$

Present value of salvage, due in three years ($20,000 × .658) 13,160

Total present value 360,176$

Less: Amount to be invested 350,000

Net present value of this project 10,176$

TOYING WITH NATURE

Schedule of Estimated Net Income

Payback period:

Depreciation expense [($350,000 – $20,000) ÷ 3] 110,000

Selling and general expenses 55,000 410,000

Income before income taxes 70,000$

Income taxes expense ($70,000 × 40%) 28,000

Estimated increase in annual net income 42,000$

PROBLEM 26.2A

HIBBING TECHNOLOGY

a.

(1)

(3) Net present value, discounted at 12%:

Total present value of eight annual net cash flows ($112,000 × 4.968) 556,416$

Less: Amount to be invested 560,000

(1)

(2)

Return on average investment:

(3) Net present value, discounted at 12%:

Total present value of seven annual net cash flows ($122,500 × 4.564) 559,090$

Present value of salvage value due in seven years ($70,000 × .452) 31,640

Total present value 590,730$

Less: Amount to be invested 490,000

Net present value of proposal 100,730$

b.

25 Minutes, Medium

Proposal B

Proposal A

Payback period:

From the information above, Proposal B clearly appears to be the better investment.

Payback period:

(2)

Return on average investment:

25 Minutes, Medium

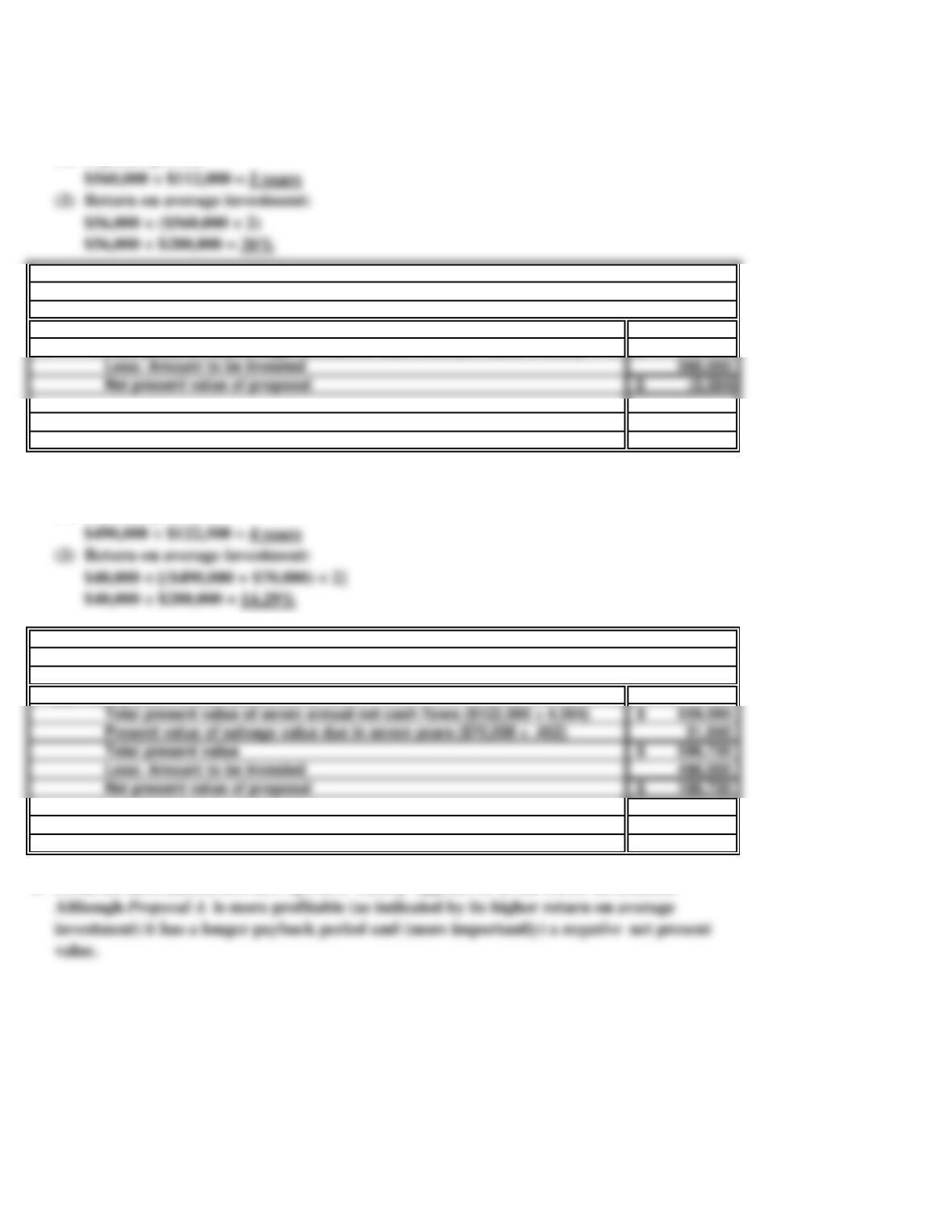

PROBLEM 26.3A

WELSH INDUSTRIES

a.

(1)

(3) Net present value, discounted at 10%:

Total present value of five annual net cash flows ($100,000 × 3.791) 379,100$

Present value of salvage value due in five years ($80,000 × .621) 49,680

Less: Amount to be invested 400,000

Net present value of proposal 28,780$

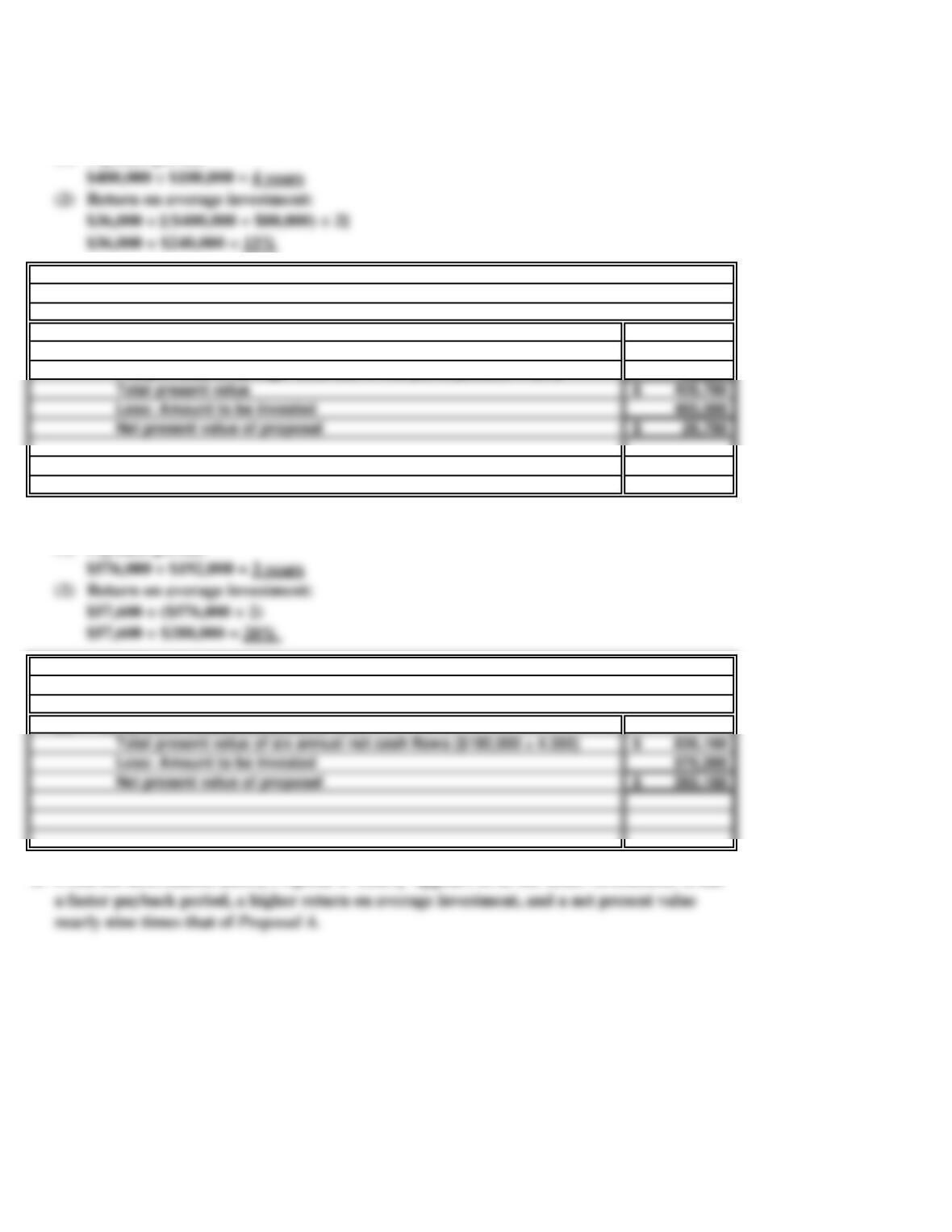

(1)

(2)

$576,000 ÷ $192,000 = 3 years

Return on average investment:

$57,600 ÷ ($576,000 ÷ 2)

$57,600 ÷ $288,000 = 20%

(3) Net present value, discounted at 10%:

Less: Amount to be invested 576,000

Net present value of proposal 260,160$

b.

From the information above, Proposal B clearly appears to be the better investment. It has

Proposal A

Payback period:

Proposal B

Payback period:

(2)

$400,000 ÷ $100,000 = 4 years

Return on average investment:

$36,000 ÷ $240,000 = 15%