Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CHAPTER 26

SOLUTIONS TO PROBLEMS: SET B

PROBLEM 26-1B

(a)

Reject

Order

Accept

Order

Net Income

Increase

(Decrease)

Revenues (10,000 X $30)

Cost of goods sold

Selling and administrative

expenses

Net income

$0

0

0

$0

$300,000

240,000

25,000

$ 35,000

(1)

(2)

$ 300,000

( (240,000)

( (25,000)

$ 35,000

PROBLEM 26-2B

(a)

Make FIZBE

Buy FIZBE

Net Income

Increase

(Decrease)

Direct materials (5,000 X $4.75)

Direct labor (5,000 X $4.60)

Indirect labor (5,000 X $.45)

$23,750

23,000

2,250

$ 0

0

0

($ 23,750

( 23,000

( 2,250

(b) The company should continue to make FIZBE because net income

(c) The decision would be different. Because of the opportunity cost of

$6,000, net income will be $1,250 higher if FIZBE is purchased as shown

below:

Make FIZBE

Buy FIZBE

Net Income

Increase

(Decrease)

(d) Nonfinancial factors include: (1) the adverse effect on employees

if FIZBE is purchased, (2) how long the supplier will be able to satisfy

PROBLEM 26-3B

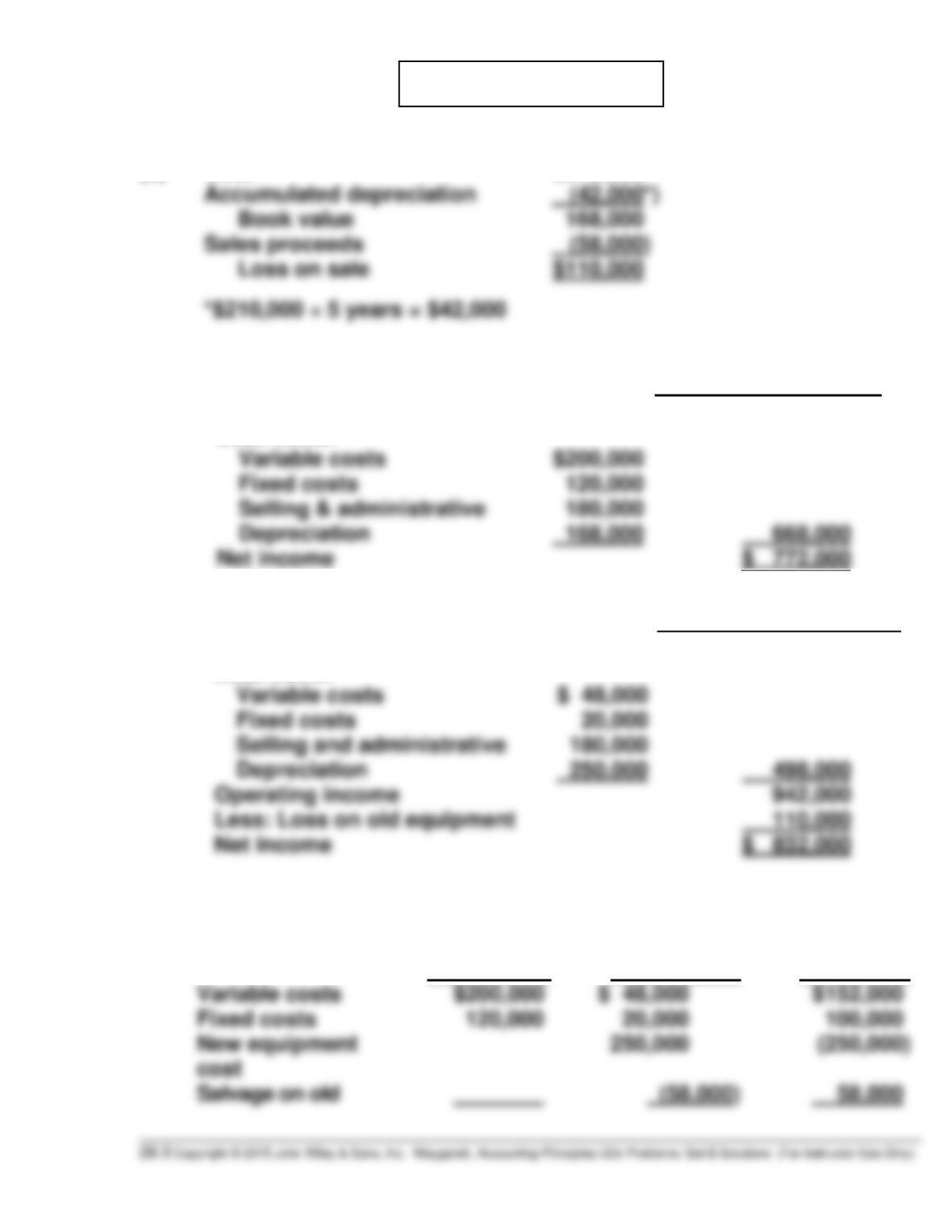

(a)

Cost

$210,000

Accumulated depreciation

(42,000*)

(b) (1)

Retain Old Equipment

Revenues ($360,000 X 4 yrs.)

$1,440,000

Less costs:

Variable costs

$200,000

(2)

Replace Old Equipment

Revenues

$1,440,000

Less costs:

Variable costs

$ 48,000

Fixed costs

20,000

(c)

Retain Old

Equipment

Replace Old

Equipment

Net

Income

Increase

(Decrease)

Variable costs

$200,000

$ 48,000

$152,000

equipment

PROBLEM 26-3B (Continued)

(d) MEMO

TO: Gene Simmons

FROM: Student

SUBJECT: Relevant Data for Decision to Replace Old Equipment

When deciding whether or not to replace any old equipment, the analysis

should only include cost data relevant to the replacement decision. The

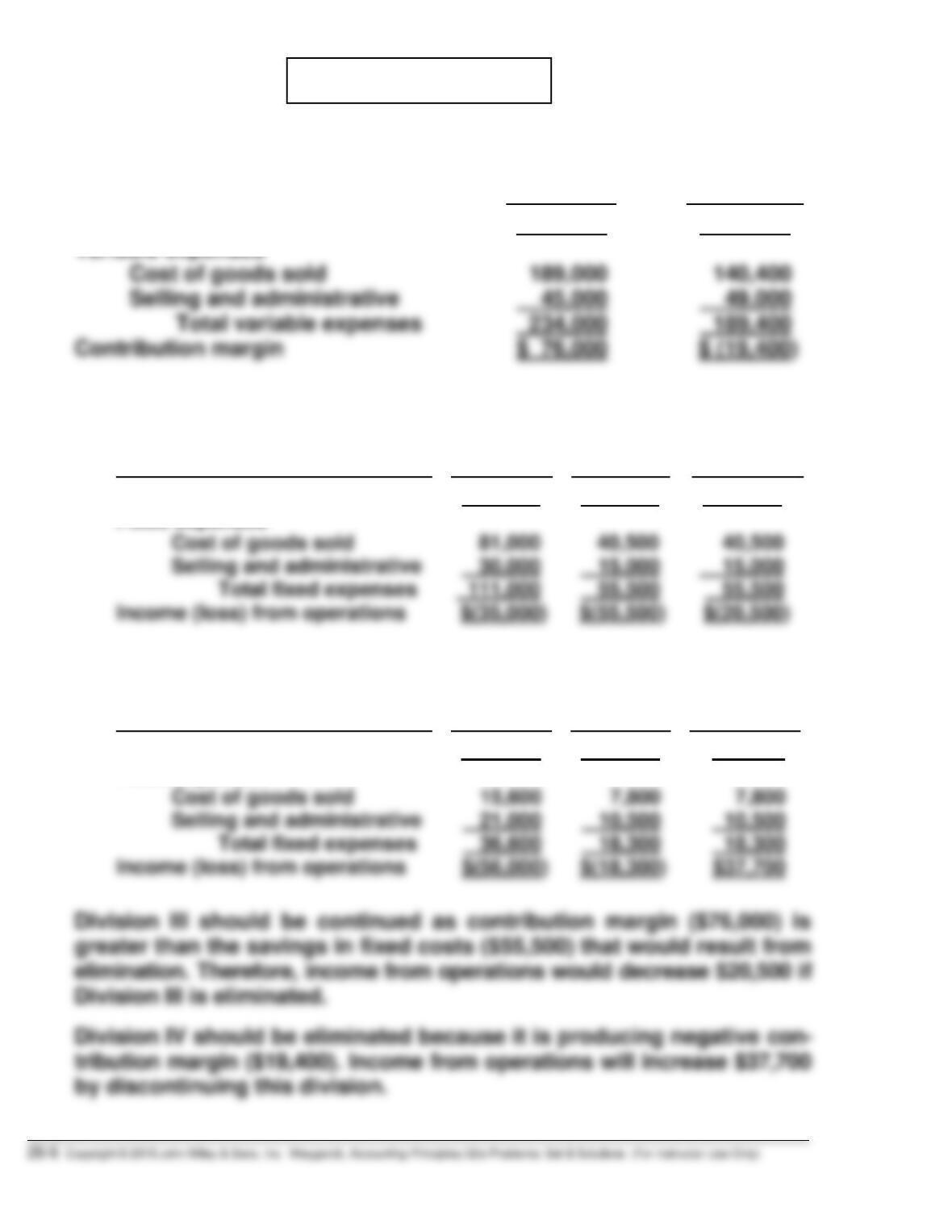

PROBLEM 26-4B

(a)

Division

III

Division

IV

Sales

$310,000

$170,000

(b)

(1)

Division III

Continue

Eliminate

Net Income

Increase

(Decrease)

Contribution margin (above)

Fixed expenses

Cost of goods sold

$ 76,000

81,000

$ 0

(40,500

$(76,000)

40,500

(2)

Division IV

Continue

Eliminate

Net Income

Increase

(Decrease)

Contribution margin (above)

Fixed expenses

Cost of goods sold

$(19,400)

(15,600)

$ 0

7,800

$19,400

7,800

PROBLEM 26-4B (Continued)

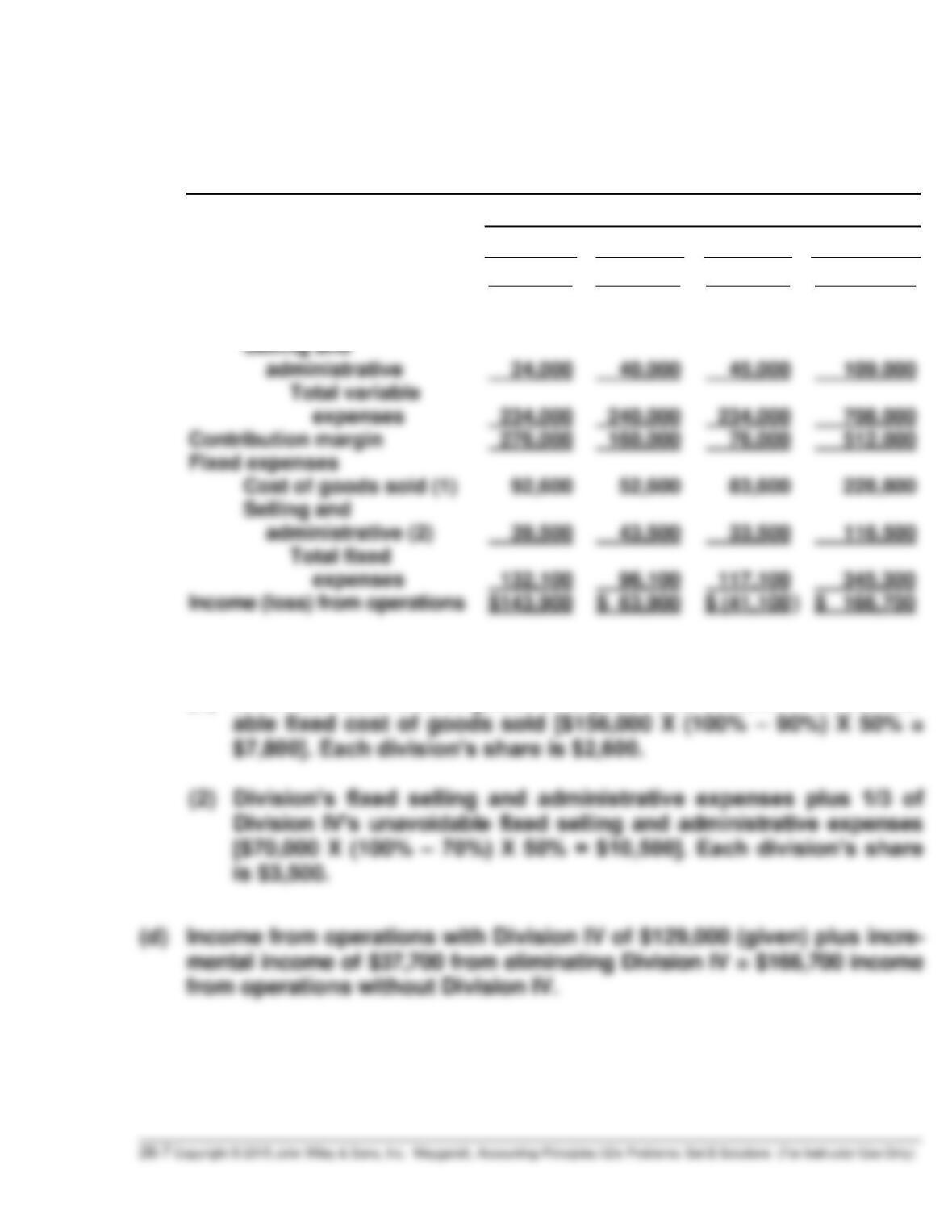

(c) PANDA COMPANY

CVP Income Statement

For the Quarter Ended March 31, 2017

Divisions

I

II

III

Total

Sales

Variable expenses

Cost of goods sold

Selling and

$510,000

210,000

$400,000

200,000

$310,000

189,000

$1,220,000

599,000

(1) Division’s fixed cost of goods sold plus 1/3 of Division IV’s unavoid-

able fixed cost of goods sold [$156,000 X (100% – 90%) X 50% =

$7,800]. Each division’s share is $2,600.

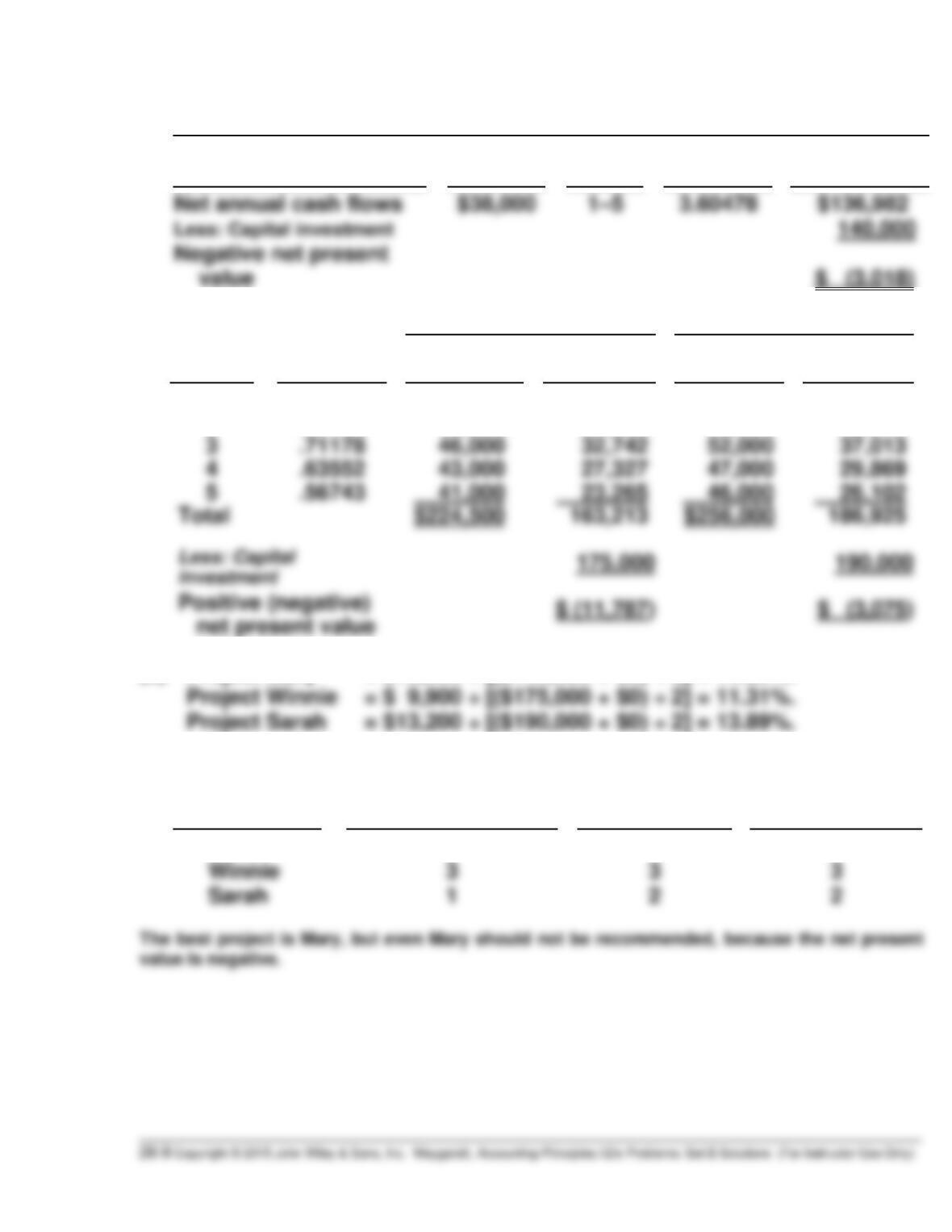

PROBLEM 26-5B

(a) Project Mary $140,000 ÷ [($10,000 + $28,000)] = 3.68 years

Project Winnie

Cash Flow

Cumulative Cash Flow

$47,500 ($12,500 + $35,000)

$47,000 ($12,000 + $35,000)

$ 47,500

$ 94,500

Project Sarah

Year

Cash Flow

Cumulative Cash Flow

1

2

$57,000 ($19,000 + $38,000)

$54,000 ($16,000 + $38,000)

$ 57,000

$111,000

PROBLEM 26-5B (Continued)

(b) Project Mary

Item

Amount

Years

PV Factor

Present

Value

Net annual cash flows

Less: Capital investment

Negative net present

value

$38,000

1–5

3.60478

$136,982

140,000

$ (3,018)

Project Winnie

Project Sarah

Year

Discount

Factor

Cash

Flow

PV

Cash

Flow

PV

1

2

.89286

.79719

$ 47,500

47,000

$ 42,411

37,468

$ 57,000

54,000

$ 50,893

43,048

(c) Project Mary = $10,000 ÷ [($140,000 + $0) ÷ 2] = 14.29%.

(d)

Project

Cash Payback

Net

Present Value

Annual

Rate of Return

Mary

2

1

1

PROBLEM 26-6B

(a)

(1)

Annual

Net Income

(2)

Annual

Cash Inflow

Sales

Expenses

Drivers’ salaries

Out-of-pocket expenses

*$144,000*

43,000

* 42,000***

$144,000

43,000

42,000

(b) 1. Cash payback period = $90,000 ÷ $59,000 = 1.53 years.

(c) Present value of annual cash inflows ($59,000 X 2.28323*) = $134,711

Capital investment = (90,000)

Net present value = $ 44,711

PROBLEM 26-7B

(a)

(1) Option A

Cash

Flows

X

11% Discount

Factor

=

Present

Value

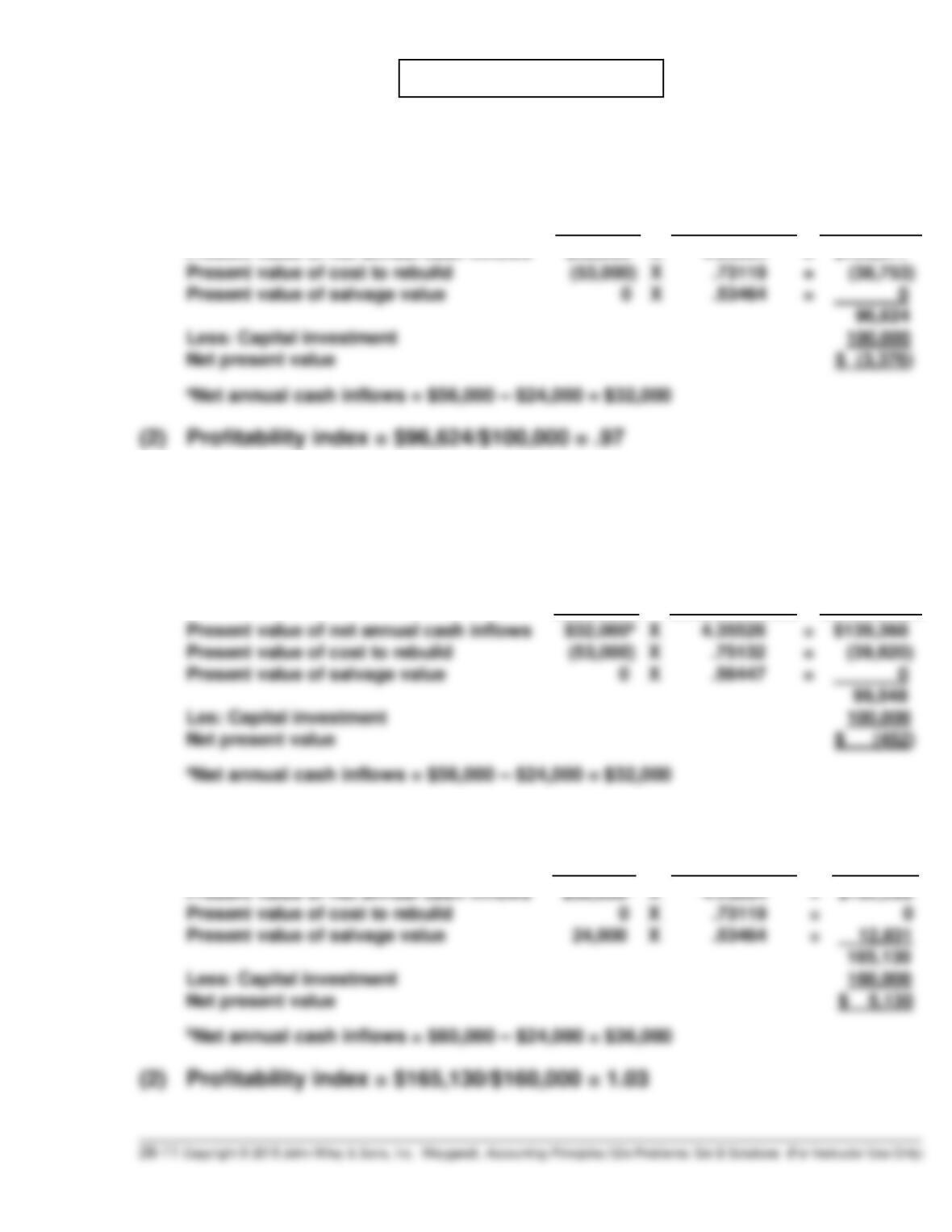

Present value of net annual cash inflows

Present value of cost to rebuild

Present value of salvage value

a$32,000a

( (53,000)

( 0)

X

X

X

4.23054

.73119

.53464

=

=

=

($135,377)

( (38,753)

( 0)

(3) The internal rate of return can be approximated by finding the discount

rate that results in a net present value of approximately zero. This is

accomplished with a 10% discount rate.

Cash

Flows

X

10% Discount

Factor

=

Present

Value

(1) Option B

Cash

Flows

X

11% Discount

Factor

=

Present

Value

Present value of net annual cash inflows

b$36,000b

X

4.23054

=

$152,299

PROBLEM 26-7B (Continued)

(3) Internal rate of return on Option B is 12%, as calculated below:

Cash

Flows

X

12% Discount

Factor

=

Present

Value

Present value of net annual cash inflows

Present value of cost to rebuild

b$36,000b

0

X

X

4.11141

.71178

=

=

$148,011

0