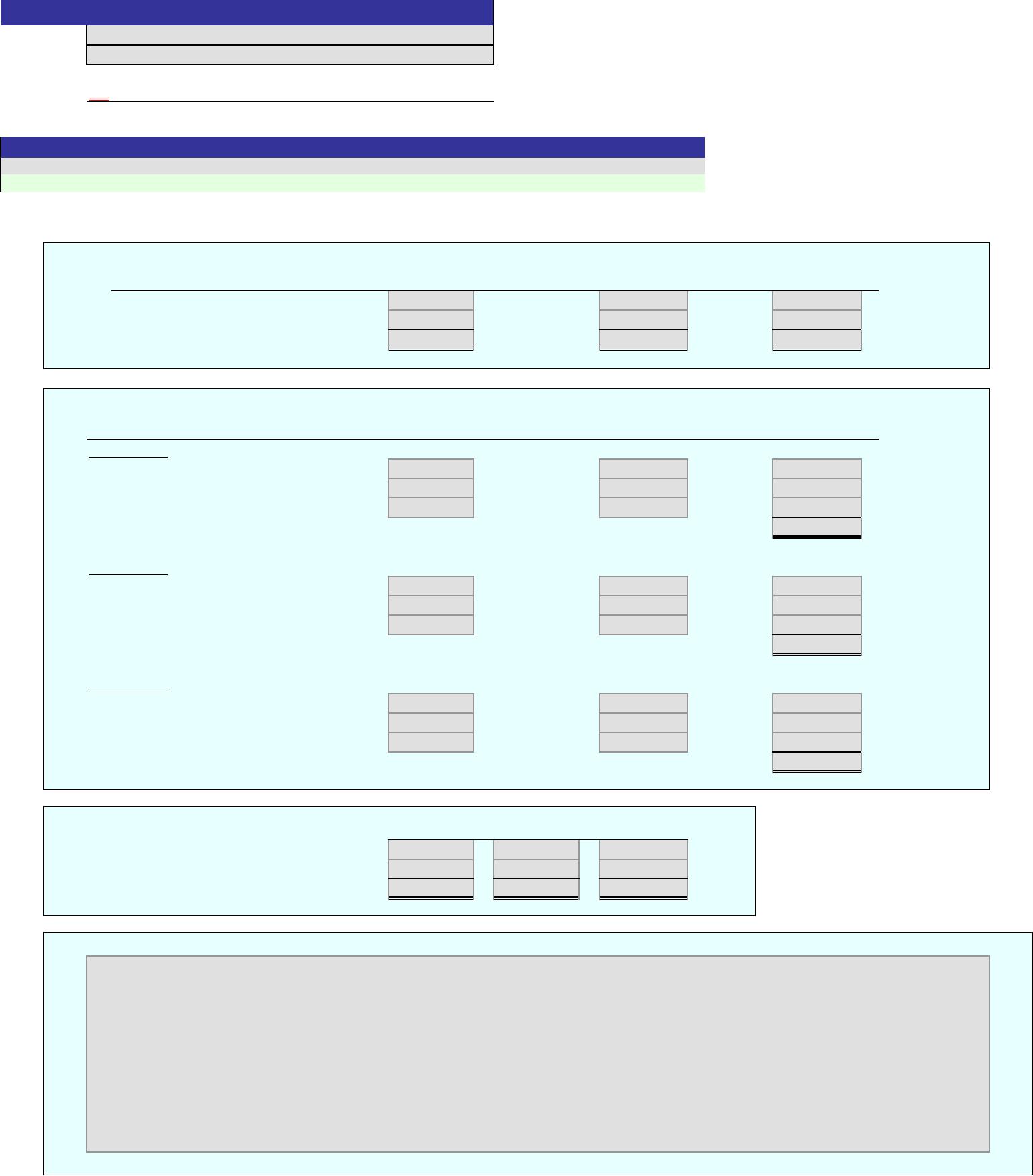

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

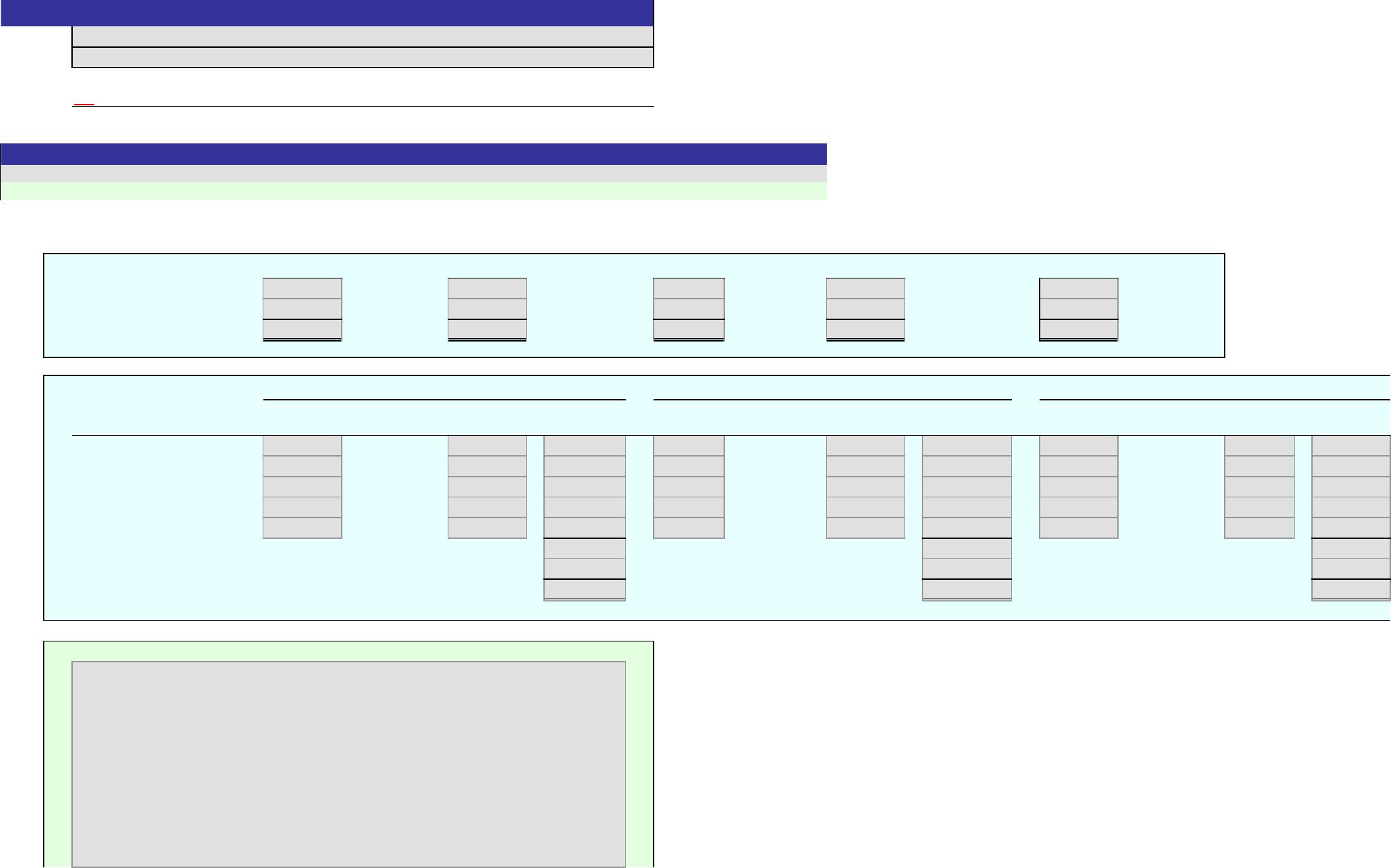

1.

Production department rates:

Cutting Finishing

Department Department

Factory overhead

Direct labor hours

Production department rate

/dlh /dlh

2.

Direct Labor Production Factory

Hours Department Rate = Overhead

Snowboards:

Cutting Department /dlh =

Finishing Department /dlh =

Total factory overhead

Number of units

Factory overhead per unit

Skis:

Cutting Department /dlh =

Finishing Department /dlh =

Total factory overhead

Number of units

Factory overhead per unit

3.

Activity-based rates:

Factory overhead

Activity base prod. runs

moves

dlh dlh

Activity rate /prod. run /move /dlh /dlh

4.

Activity Usage Activity Rate =Activity Cost Activity Usage Activity Rate =Activity Cost

Production Control runs /run = runs /run =

Materials Handling

moves

/move =

moves

/move =

Cutting Department dlh /dlh = dlh /dlh =

Finishing Department dlh /dlh = dlh /dlh =

Total

Number of units

Activity cost per unit

5.

Snowboards

Skis

Activity

[Key essay answer here]

Finishing

Control

Handling

Department

Department

Production

Materials

Cells with non-gray backgrounds are protected and cannot be edited.

Cutting

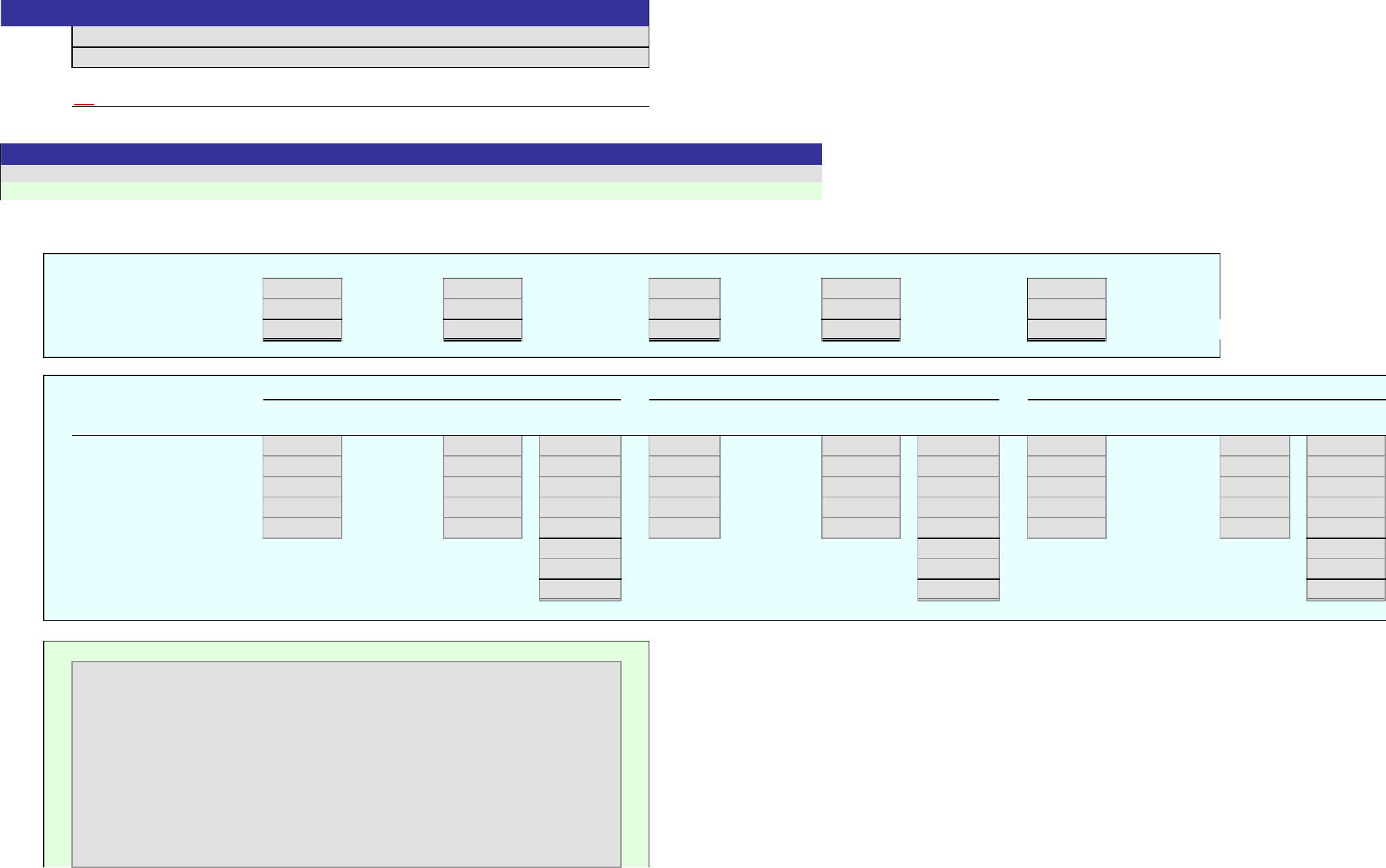

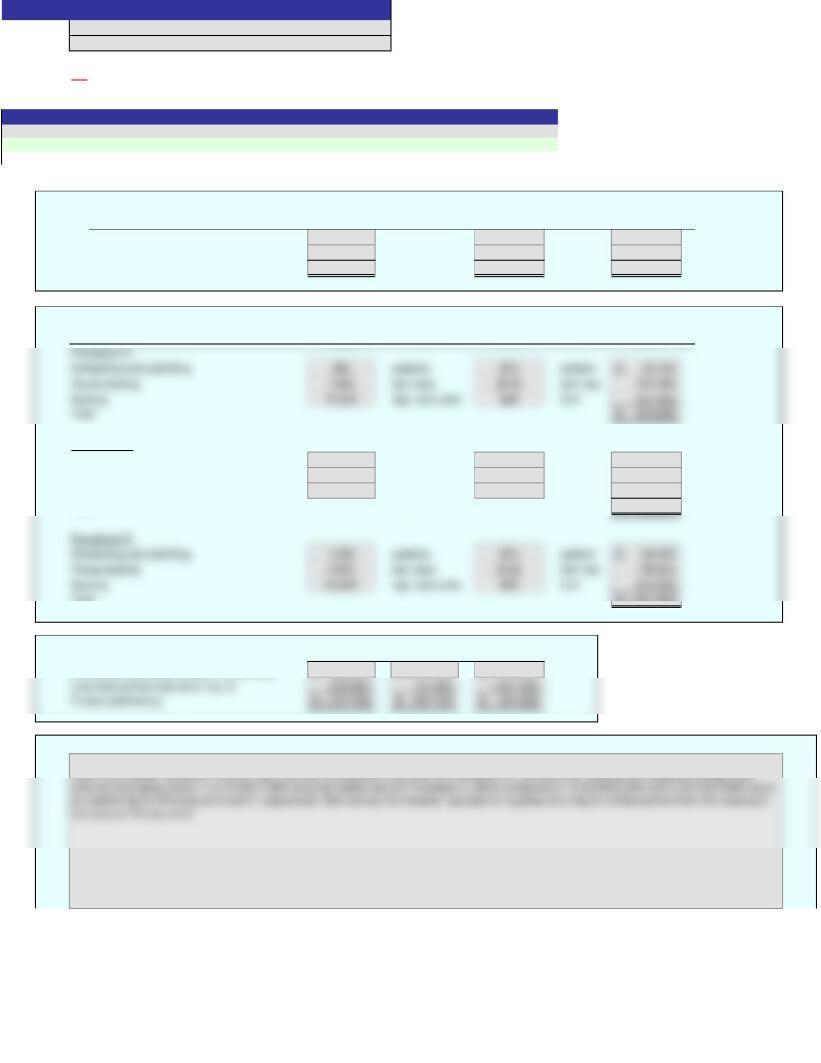

Problem 26(11)-3A

Name:

Section:

0%

[Key code here]

Answers are entered in the cells with gray backgrounds.

Score:

Key Code:

Instructions

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

1.

Production department rates:

Cutting Finishing

Department Department

Factory overhead $315,000 $540,000

2.

Direct Labor Production Factory

Hours

Department Rate

= Overhead

moves

Snowboards:

Cutting Department 4,000 $52.50 /dlh = 210,000$

Finishing Department 2,000 $90.00 /dlh = 180,000

Skis:

Cutting Department 2,000 $52.50 /dlh = 105,000$

3.

Activity-based rates:

Factory overhead $237,000 $270,000 $156,000 $192,000

4.

Activity Usage Activity Rate =Activity Cost Activity Usage Activity Rate =Activity Cost

Production Control 430 runs $474.00 /run = 203,820$ 70 runs $474.00 /run = 33,180$

Materials Handling 5,000

moves

$36.00 /move = 180,000 2,500

moves

$36.00 /move = 90,000

5.

The activity-based overhead allocation reveals that snowboards consume more factory overhead on a per-unit basis than

do skis. The multiple production department factory overhead rate method does not show this because all factory

Snowboards

Skis

Activity

Control

Handling

Department

Department

Production

Materials

Cutting

Finishing

Problem 26(11)-3A

Name:

Solution

Section:

Cells with non-gray backgrounds are protected and cannot be edited.

Score:

Instructions

Answers are entered in the cells with gray backgrounds.

ON

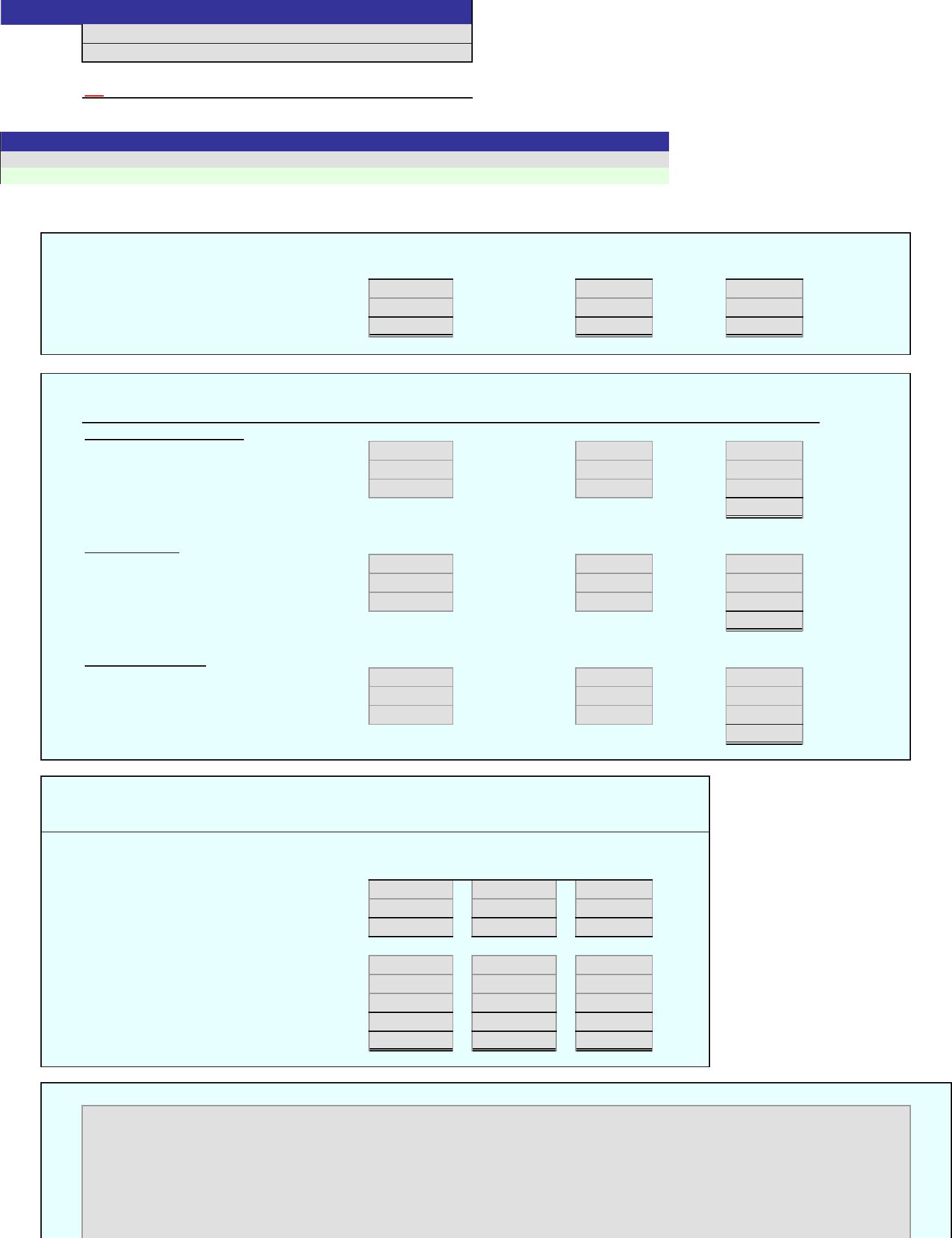

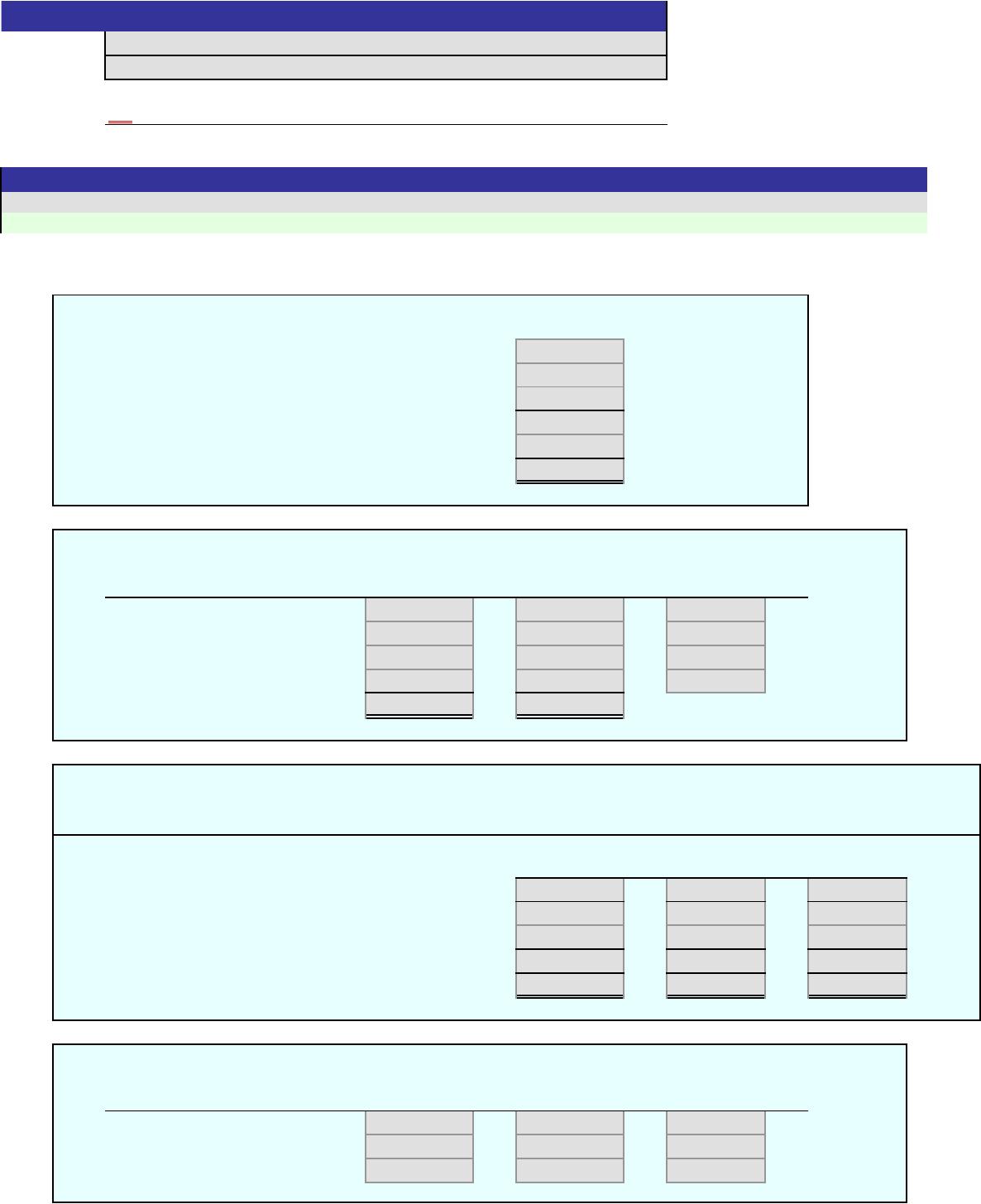

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

1.

Production department rates:

Subassembly Final Assembly

Department Department

Factory overhead

Direct labor hours

Production department rate

/dlh /dlh

2.

Direct Labor Production Factory

Hours Department Rate = Overhead

Receivers:

Subassembly Department /dlh =

Final Assembly Department /dlh =

Total factory overhead

Number of units

Factory overhead per unit

Loudspeakers:

Subassembly Department /dlh =

Final Assembly Department /dlh =

Total factory overhead

Number of units

Factory overhead per unit

3.

Activity-based rates:

Factory overhead

Activity base setups insp. dlh dlh

Activity rate /setup /insp. /dlh /dlh

4.

Activity Usage Activity Rate =Activity Cost Activity Usage Activity Rate =Activity Cost

Setup setups /setup =

setups

/setup =

Quality Control insp. /insp. = insp. /insp. =

Subassembly Department dlh /dlh = dlh /dlh =

Final Assembly Department dlh /dlh = dlh /dlh =

Total

Number of units

Activity cost per unit

5.

Loudspeakers

Activity

[Key essay answer here]

Final Assembly

Setup

Control

Department

Department

Quality

Problem 26(11)-3B

Name:

Section:

Receivers

Cells with non-gray backgrounds are protected and cannot be edited.

Subassembly

0%

[Key code here]

Answers are entered in the cells with gray backgrounds.

Score:

Key Code:

Instructions

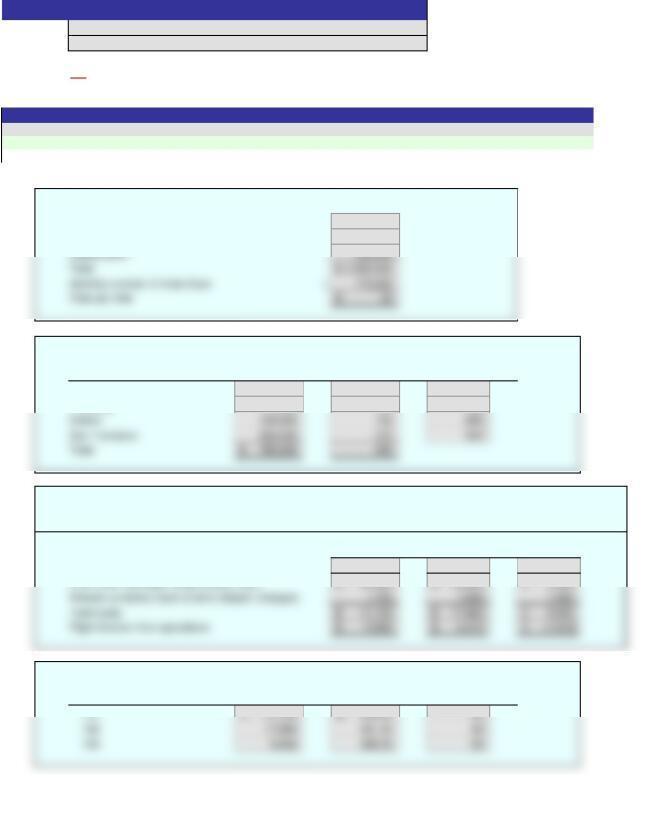

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

1.

Production department rates:

Subassembly Final Assembly

Department Department

Factory overhead $420,000 $294,000

2.

Direct Labor Production Factory

Hours Department Rate = Overhead

Receivers:

Subassembly Department 875 $300 /dlh = 262,500$

Final Assembly Department 525 $210 /dlh = 110,250

Loudspeakers:

Subassembly Department 525 $300 /dlh = 157,500$

Final Assembly Department 875 $210 /dlh = 183,750

3.

Activity-based rates:

4.

Activity Usage Activity Rate =Activity Cost Activity Usage Activity Rate =Activity Cost

Setup 80 setups $346.50 /setup = 27,720$ 320 setups $346.50 /setup = 110,880$

5.

Loudspeakers

Activity

Subassembly

Final Assembly

Setup

Control

Department

Department

Quality

Problem 26(11)-3B

Name:

Solution

Section:

The activity-based overhead allocation reveals that loudspeakers are more costly on a per-unit basis than are the

receivers. The multiple production department rate method determined that the per-unit factory overhead was nearly the

same for the two products. The multiple production department factory overhead rate method distorts the unit costs

Receivers

Cells with non-gray backgrounds are protected and cannot be edited.

Score:

Instructions

Answers are entered in the cells with gray backgrounds.

ON

An asterisk (*) will appear to the right of an incorrect entry.

1. Production Setup Materials Handling Inspection Engineering

Total activity cost

Divided by total activity base mh setups no. parts insp. hours eng. hours

Activity rate /mh /setup /part /hour /hour

2.

Activity Activity Activity Activity Activity Activity

Activity

Activity Base Usage Rate =Cost Activity Base Usage Rate =Cost Activity Base Usage Rate =Cost

Production mh mh mh

Setup setups setups setups

Material handling parts parts parts

Inspection insp. hours insp. hours insp. hours

Engineering eng. hours eng. hours eng. hours

Total

Number of units

Activity cost per unit

3.

Answers are entered in the cells with gray backgrounds.

I8

[Key essay answer here]

Score:

Key Code:

Instructions

Cells with non-gray backgrounds are protected and cannot be edited.

M5

Z4

0%

[Key code here]

Problem 26(11)-4A

Name:

Section:

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

1. Production Setup Materials Handling Inspection Engineering

Total activity cost 264,000$ 96,000$ 9,600$ 50,000$ 150,000$

Divided by total activity base 2,200 mh 400 setups 480 no. parts 1,000 insp. hours 500 eng. hours

Activity rate 120$ /mh 240$ /setup 20$ /part 50$ /hour 300$ /hour

2.

Activity Activity Activity Activity Activity Activity

Activity

Activity Base Usage Rate =Cost Activity Base Usage Rate =Cost Activity Base Usage Rate =Cost

Production 1,000 mh $120 120,000$ 800 mh $120 96,000$ 400 mh $120 48,000$

Setup 60 setups $240 14,400 120 setups $240 28,800 220 setups $240 52,800

Material handling 80 parts $20 1,600 150 parts $20 3,000 250 parts $20 5,000

3.

The unit costs are different even though each product requires 0.8 machine hour because

the products consume many activities in ratios different from the volume. For example, the

Cells with non-gray backgrounds are protected and cannot be edited.

Score:

Instructions

Answers are entered in the cells with gray backgrounds.

M5

Z4

ON

Problem 26(11)-4A

Name:

Solution

Section:

I8

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

1. Production Setup Inspection Shipping Cust. Serv.

Total activity cost

Divided by total activity base mh setups inspections cust. orders requests

Activity rate /mh /setup /inspect. /cust. ord. /request

2.

Activity Activity Activity Activity Activity Activity

Activity

Activity Base Usage Rate =Cost Activity Base Usage Rate =Cost Activity Base Usage Rate =Cost

Production mh mh mh

Setup setups setups setups

Inspection insp. insp. insp.

Shipping cust. orders cust. orders cust. orders

Customer service requests requests requests

Total

Number of units

Activity cost per unit

3.

Answers are entered in the cells with gray backgrounds.

Powdered Sugar

[Key essay answer here]

Score:

Key Code:

Instructions

Cells with non-gray backgrounds are protected and cannot be edited.

White Sugar

Brown Sugar

0%

[Key code here]

Problem 26(11)-4B

Name:

Section:

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

1. Production Setup Inspection Shipping Cust. Serv.

Total activity cost 500,000$ 144,000$ 44,000$ 115,000$ 84,000$

Divided by total activity base 10,000 mh 450 setups 1,100 inspections 5,750 cust. orders 600 requests

Activity rate 50$ /mh 320$ /setup 40$ /inspect. 20$ /cust. ord. 140$ /request

2.

Activity Activity Activity Activity Activity Activity

Activity

Activity Base Usage Rate =Cost Activity Base Usage Rate =Cost Activity Base Usage Rate =Cost

Production 5,000 mh $50 250,000$ 2,500 mh $50 125,000$ 2,500 mh $50 125,000$

Setup 85 setups $320 27,200 170 setups $320 54,400 195 setups $320 62,400

Inspection 220 insp. $40 8,800 330 insp. $40 13,200 550 insp. $40 22,000

3.

The unit costs are different even though each product requires 0.5 machine hour because

Cells with non-gray backgrounds are protected and cannot be edited.

Score:

Instructions

Answers are entered in the cells with gray backgrounds.

White Sugar

Brown Sugar

ON

Problem 26(11)-4B

Name:

Solution

Section:

Powdered Sugar

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

1.

Customer Project Engineering

Service Bidding Support

Activity cost

Activity base

serv. reqs. bids desgn. chngs.

Activity rate

/serv. req. /bid /change

2.

Number Activity

of Activities Rate = Total

Good Knowledge University

Customer service serv. reqs. /req.

Project bidding bids /bid

Engineering support desgn. chngs. /chng.

Total nonmanufacturing activity costs

Hot Shotz Arena

Customer service serv. reqs. /req.

Project bidding bids /bid

Engineering support desgn. chngs. /chng.

Total nonmanufacturing activity costs

Break-a-Leg Hospital

Customer service serv. reqs. /req.

Project bidding bids /bid

Engineering support desgn. chngs. /chng.

Total nonmanufacturing activity costs

3.

Good Hot Break-

Knowledge Shotz a-Leg

University Arena Hospital

Revenues

Less cost of goods sold

Gross profit

Less selling and administrative activities:

Customer service

Project bidding

Engineering support

Total selling and admin. activities

Income from operations

4.

Key Code:

Instructions

Cells with non-gray backgrounds are protected and cannot be edited.

[Key essay answer here]

COLD ZONE MECHANICAL INC.

Customer Profitability Report

For the Year Ended December 31

0%

[Key code here]

Answers are entered in the cells with gray backgrounds.

Problem 26(11)-5A

Name:

Section:

Score:

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

1.

Customer Project Engineering

Service Bidding Support

Activity cost

$83,720 $61,360 $86,800

Activity base

322 serv. reqs. 104 bids 217 desgn. chngs.

Activity rate

$260 /serv. req. $590 /bid $400 /change

2.

Number Activity

of Activities Rate = Total

Good Knowledge University

Customer service 60 serv. reqs. $260 /req. 15,600$

Project bidding 36 bids $590 /bid 21,240

Hot Shotz Arena

Customer service 52 serv. reqs. $260 /req. 13,520$

Project bidding 18 bids $590 /bid 10,620

Engineering support 30 desgn. chngs. $400 /chng. 12,000

3.

Good Hot Break-

Knowledge Shotz a-Leg

University Arena Hospital

Revenues 1,650,000$ 1,050,000$ 450,000$

4.

Break-a-Leg Hospital is unprofitable, while the other two customers have acceptable margins. This is because Break-a-Leg Hospital requires

many customer service, project bidding, and design change activities. For example, Break-a-Leg Hospital awards contracts on only 12% of the

bid efforts (6 contracts/50 bids); it requests a large amount of service; and it requires extensive design change effort. The company‘s options

b. Reprice Break-a-Leg Hospital work. Charge Break-a-Leg Hospital a higher price to compensate for the higher activities required to serve it.

However, the customer may not accept the price increase required to move it to a profitable relationship.

c. Encourage Break-a-Leg Hospital to reduce the amount of design changes and customer service requests. The design changes are probably

driving the customer service requests. This may be appealing, but there may be no incentive for Break-a-Leg Hospital to change its behavior.

d. Charge a price for customer service and design change separately. That is, unbundle the pricing of goods from the

support services. This is a good long-term solution. In addition, improve the bidding process in order to improve the

“hit rate” or the percentage of awarded contracts to bids.

COLD ZONE MECHANICAL INC.

Customer Profitability Report

For the Year Ended December 31

Problem 26(11)-5A

Name:

Solution

Section:

Cells with non-gray backgrounds are protected and cannot be edited.

Score:

Instructions

Answers are entered in the cells with gray backgrounds.

ON

Break-a-Leg Hospital is unprofitable, while the other two customers have acceptable margins. This is because Break-a-Leg Hospital requires

many customer service, project bidding, and design change activities. For example, Break-a-Leg Hospital awards contracts on only 12% of the

bid efforts (6 contracts/50 bids); it requests a large amount of service; and it requires extensive design change effort. The company‘s options

include:

a. Stop bidding Break-a-Leg Hospital projects: This does not necessarily mean that all the costs can be avoided. The costs will only be

eliminated if the reduced activity translates into lower headcount (dismissals). Thus, the company should evaluate the contribution margin of this

customer relationship before making this decision.

b. Reprice Break-a-Leg Hospital work. Charge Break-a-Leg Hospital a higher price to compensate for the higher activities required to serve it.

However, the customer may not accept the price increase required to move it to a profitable relationship.

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

1.

Customer Sales Order Advertising

Service Processing Support

Activity cost pool

Activity base

serv. reqs. orders ads placed

Activity rate

/serv. req. /order /ad

2.

Number Activity

of Activities Rate = Total

Office Warehouse

Customer service serv. reqs. /req.

Sales order processing orders /order

Advertising support

ads placed /ad

Total nonmanufacturing activity costs

Office To-Go

Customer service serv. reqs. /req.

Sales order processing orders /order

Advertising support

ads placed /ad

Total nonmanufacturing activity costs

Office Universe

Customer service serv. reqs. /req.

Sales order processing orders /order

Advertising support

ads placed /ad

Total nonmanufacturing activity costs

3.

The Kosmo Supply

Warehouse Co. Universe

Revenues

Less cost of goods sold

Gross profit

Less selling and administrative activities:

Customer service cost

Sales order processing cost

Advertising support cost

Total selling and admin. activities

Income from operations

4.

Instructions

Problem 26(11)-5B

Name:

Section:

0%

Score:

Cells with non-gray backgrounds are protected and cannot be edited.

[Key essay answer here]

SHRUTE INC.

Customer Profitability Report

For the Year Ended December 31

[Key code here]

Answers are entered in the cells with gray backgrounds.

Key Code:

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

1.

Customer Sales Order Advertising

Service Processing Support

2.

Number Activity

of Activities Rate = Total

The Warehouse

Customer service 62 serv. reqs. $180 /req. 11,160$

Sales order processing 300 orders $24 /order 7,200

Advertising support

25 ads placed $1,250 /ad 31,250

Total nonmanufacturing activity costs 49,610$

Supply Universe

Customer service 25 serv. reqs. $180 /req. 4,500$

Sales order processing 140 orders $24 /order 3,360

Advertising support

3.

The Kosmo Supply

Warehouse Co. Universe

Revenues 899,100$ 899,100$ 899,100$

4.

Instructions

Answers are entered in the cells with gray backgrounds.

ON

Key Code:

Problem 26(11)-5B

Name:

Solution

Section:

Score:

Cells with non-gray backgrounds are protected and cannot be edited.

Kosmo Co. has low profitability, while the other two customers have acceptable margins. This is because Kosmo Co. requires many customer

services, sales order processing, and advertising support activities. For example, Kosmo Co. orders frequently in small order sizes, which

increases the sales order processing costs; it requests a large amount of service; and it requires extensive promotional support. The

company‘s options include:

b. Reprice Kosmo Co. Charge Office To-Go a higher price to compensate for the higher activities required to serve it. The customer may not

accept the price increase required to move this to a profitable relationship.

c. Encourage Kosmo Co. to order in larger quantities. This may be appealing. However, if Kosmo Co. wishes to keep its inventories low, it will

avoid making large infrequent orders but instead will prefer smaller frequent orders.

d. Improve the internal operations of Shrute Inc. to reduce the impact of the sales order-related activities. Reduce the cost of sales

order processing.

e. Unbundle pricing. Price customer service and advertising support as separate services. In other words, unbundle the pricing of

goods from the support services. This is a good long-term solution.

SHRUTE INC.

Customer Profitability Report

For the Year Ended December 31

Kosmo Co. has low profitability, while the other two customers have acceptable margins. This is because Kosmo Co. requires many customer

services, sales order processing, and advertising support activities. For example, Kosmo Co. orders frequently in small order sizes, which

increases the sales order processing costs; it requests a large amount of service; and it requires extensive promotional support. The

company‘s options include:

a. Drop Kosmo Co. This does not necessarily mean that all the costs can be avoided. The costs will only be eliminated if the reduced activity

translates into lower spending. Thus, the company should evaluate the contribution margin of this customer relationship before making this

decision.

b. Reprice Kosmo Co. Charge Office To-Go a higher price to compensate for the higher activities required to serve it. The customer may not

accept the price increase required to move this to a profitable relationship.

c. Encourage Kosmo Co. to order in larger quantities. This may be appealing. However, if Kosmo Co. wishes to keep its inventories low, it will

avoid making large infrequent orders but instead will prefer smaller frequent orders.

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

1.

Scheduling

& Admitting Housekeeping Nursing

Activity cost

Activity base

patients days wgt. care units

Activity rate

/patient /day /unit

2.

Activity Activity

Usage Rate = Total

Procedure A:

Scheduling and admitting patients /patient

Housekeeping pat. days /pat. day

Nursing wgt. care units /unit

Total

Procedure B:

Scheduling and admitting patients /patient

Housekeeping pat. days /pat. day

Nursing wgt. care units /unit

Total

Procedure C:

Scheduling and admitting patients /patient

Housekeeping pat. days /pat. day

Nursing wgt. care units /unit

Total

3.

Procedure A Procedure B Procedure B

Reimbursement (patient days x reimb. rate)

Less total activity cost (from req. 2)

Excess (deficiency)

4.

Answers are entered in the cells with gray backgrounds.

Score:

Key Code:

Instructions

Cells with non-gray backgrounds are protected and cannot be edited.

[Key essay answer here]

Problem 26(11)-6A

Name:

Section:

0%

[Key code here]

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

1.

Scheduling

& Admitting Housekeeping Nursing

Activity cost

$432,000 $4,212,000 $5,376,000

Activity base

6,000 patients 27,000 days 192,000 wgt. care units

Activity rate

$72 /patient $156 /day $28 /unit

2.

Activity Activity

Usage Rate = Total

Procedure B:

Scheduling and admitting 650 patients $72 /patient 46,800$

Housekeeping 3,250 pat. days $156 /pat. day 507,000

Nursing 6,000 wgt. care units $28 /unit 168,000

Total 721,800$

Total 1,507,200$

3.

Procedure A Procedure B Procedure B

Reimbursement (patient days x reimb. rate) 682,080$ 1,319,500$ 1,948,800$

4.

Answers are entered in the cells with gray backgrounds.

ON

Procedure A requires more activity cost than is being reimbursed by the insurance company. As a result, the hospital may wish to determine if the

Cells with non-gray backgrounds are protected and cannot be edited.

Score:

Problem 26(11)-6A

Name:

Solution

Section:

Instructions

An asterisk (*) will appear to the right of an incorrect entry.

1.

Depreciation and maintenance cost per mile:

Fuel

Crew salaries

Depreciation

Total

Monthly number of miles flown

Rate per mile

2. Monthly Ground Number of Arriv./Depart.

Personnel Arrivals/ Rate per

Terminal City Cost per City Departures =City

Charlotte

Pittsburgh

Detroit

San Francisco

Total

3.

Flight 101 Flight 102 Flight 103

Passenger revenue (passengers x ticket price)

Fuel, crew, and depr. costs (miles x rate)

Ground personnel (sum of arriv./depart. charges)

Total costs

Flight income from operations

4. Ticket Price

Break-Even

Fixed Costs less Var. Cost Number of

Flight of Flight per Seat =Passengers

101

102

103

0%

[Key code here]

BLUE STAR AIRLINE

Flight Profitability Report

Cells with non-gray backgrounds are protected and cannot be edited.

For Three Representative Flights

Answers are entered in the cells with gray backgrounds.

Score:

Key Code:

Instructions

Problem 26(11)-6B

Name:

Section:

An asterisk (*) will appear to the right of an incorrect entry.

1.

Depreciation and maintenance cost per mile:

Fuel 2,120,000$

Crew salaries 850,000

2. Monthly Ground Number of Arriv./Depart.

Personnel Arrivals/ Rate per

Terminal City Cost per City Departures =City

Charlotte 256,000$ 320 800$

Pittsburgh 97,500 130 750

3.

Flight 101 Flight 102 Flight 103

Passenger revenue (passengetrs x ticket price) 55,600$ 22,075$ 7,640$

Fuel, crew, and depr. costs (miles x rate) 40,000$ 16,000$ 8,000$

4. Ticket Price Break-Even

Fixed Costs less Var. Cost Number of

Flight of Flight per Seat =Passengers

Cells with non-gray backgrounds are protected and cannot be edited.

BLUE STAR AIRLINE

Flight Profitability Report

For Three Representative Flights

Score:

Instructions

Answers are entered in the cells with gray backgrounds.

ON

Problem 26(11)-6B

Name:

Solution

Section: