CHAPTER 25

Standard Costs and Balanced Scorecard

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

1. Describe standard costs.

1, 2, 3, 4, 5, 6,

7, 8

1, 2, 3

1

1, 2, 3, 4, 17

2. Determine direct materials

variances.

9, 10

4, 5

2

5, 7, 8, 9, 13,

14

1A, 2A, 3A,

4A, 5A, 6A

3. Determine direct labor and

total manufacturing

overhead variances.

11, 12

6

3

4, 6, 10, 11,

12

1A, 2A, 3A,

4A, 5A, 6A

4. Prepare variance reports

and balanced scorecards.

13, 14, 15, 16,

17, 18

7

4

10, 14, 15, 16,

17, 18, 19

2A, 3A, 5A,

6A

*5. Identify the features of a

standard cost accounting

system.

19

8, 9

20, 21, 22

6A

*6. Compute overhead

controllable and volume

variances.

20, 21, 22, 23

10, 11

23, 24, 25

7A, 8A, 9A,

10A

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Compute variances.

Simple

20–30

2A

Compute variances, and prepare income statement.

Simple

30–40

3A

Compute and identify significant variances.

Moderate

20–30

4A

Answer questions about variances.

Complex

30–0

5A

Compute variances, prepare an income statement, and

explain unfavorable variances.

Moderate

30–40

*6A

Journalize and post standard cost entries, and prepare

income statement.

Moderate

40–50

*7A

Compute overhead controllable and volume variances.

Simple

10–15

*8A

Compute overhead controllable and volume variances.

Simple

10–15

*9A

Compute overhead controllable and volume variances.

Moderate

10–15

*10A

Compute overhead controllable and volume variances.

Moderate

10–15

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End-of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

1. Describe standard costs.

Q25-3

Q25-8

Q25-1 Q25-7

Q25-2

Q25-4

Q25-5

Q25-6

BE25-1 E25-2

BE25-2 E25-3

BE25-3 E25-4

DI25-1 E25-17

E25-1

2. Determine direct

materials variances.

Q25-10

Q25-9

BE25-4

BE25-5

DI25-2

E25-5

E25-7

E25-9

E25-13

E25-14

P25-1A

P25-2A

P25-5A

P25-6A

E25-8

E25-19

P25-3A

P25-4A

3. Determine direct labor and

total manufacturing overhead

variances.

Q25-11

Q25-12

BE25-6

DI25-3

E25-4

E25-6

E25-10

E25-11

E25-12

E25-19

P25-1A

P25-2A

P25-5A

P25-6A

E25-11

E25-12

E25-21

P25-3A

P25-4A

4. Prepare variance reports and

balanced scorecard.

Q25-13

Q25-14

Q25-15

Q25-16

Q25-17

Q25-18

DI25-4

E25-19

BE25-7 P25-6A

E25-10

E25-14

E25-15

E25-16

E25-17

P25-2A

P25-5A

P25-3A

*5. Identify the features of a

standard cost accounting

system.

Q25-19

BE25-8

BE25-9

E25-20

E25-22

P25–6A

E25-21

*6. Compute overhead

controllable and

volume variances.

Q25-20

Q25-21

Q25-22

Q25-23

BE25-10

BE25-11

E25-23

E25-24

E25-25

P25-7A

P25-8A

P25-9A

P25-10A

E25-22

E25-23

E25-24

Broadening Your Perspective

BYP25-4

BYP25-6

BYP25-2

BYP25-1

BYP25-3

BYP25-5

BYP25-7

BYP25-8

BYP25-9

ANSWERS TO QUESTIONS

1. (a) This is incorrect. Standard costs are predetermined unit costs.

(b) Agree. Examples of governmental regulations that establish standards for a business are

the Fair Labor Standards Act, the Equal Employment Opportunity Act, and a multitude of

environmental laws.

2. (a) Standards and budgets are similar in that both are predetermined costs and both contribute

significantly to management planning and control. The two terms differ in that a standard is

a unit amount and a budget is a total amount.

3. In addition to facilitating management planning, standard costs offer the following advantages to

an organization:

(1) They promote greater economy by making employees more “cost–conscious.”

4. The management accountant provides input to the setting of standards through the accumulation

of historical cost data and knowledge of the behavior of costs in response to changes in activity

levels. Management has the responsibility for setting the standards.

5. Ideal standards represent optimum levels of performance under perfect operating conditions. Normal

standards represent efficient levels of performance that are attainable under expected operating

conditions.

Questions Chapter 25 (Continued)

10. (a) (1) actual price. (2) standard price.

13. Variances should be reported to appropriate levels of management as soon as possible. The principle

of “management by exception” may be used with variance reports.

14. The purchasing department would be responsible for an unfavorable materials price variance

when it paid more than the standard price for the materials. The purchasing department would

also be responsible for an unfavorable materials quantity variance if it purchased materials of

inferior quality which caused an excess use of materials.

15. The four perspectives of the balanced scorecard are: financial, customer, internal process, and

learning and growth. The financial perspective employs financial measures of performance used

by most firms. The customer perspective evaluates the company from the viewpoint of those

people who buy its product in terms of price, quality, product innovation, customer service, and other

Questions Chapter 25 (Continued)

*19. (a) A standard cost accounting system is a double-entry system of accounting in which

standard costs are used in making entries and standard cost variances are formally

recognized in the accounts.

(b) The variance account will have: (1) a debit balance when the materials price variance is

unfavorable and (2) a credit balance when the labor quantity variance is favorable.

*20. Overhead controllable variance = actual overhead costs ($248,000) – overhead budgeted. Overhead

budgeted is based on standard hours allowed as follows: variable costs (27,000 X $5 = $135,000) +

fixed costs (28,000 X $4 = $112,000) = total overhead budgeted ($247,000). Thus, the controllable

variance is $1,000 unfavorable.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 25-1

(a) Standards are stated as a per unit amount. Thus, the standards are

materials $2.80 ($1,400,000 ÷ 500,000) and labor $3.40 ($1,700,000 ÷

500,000).

BRIEF EXERCISE 25-2

(a) Standard direct materials price per gallon = $2.60 ($2.30 + $.20 + $.10).

(b) Standard direct materials quantity per gallon = 4 pounds (3.6 + .4).

(c) Standard materials cost per gallon = $10.40 ($2.60 X 4).

BRIEF EXERCISE 25-3

BRIEF EXERCISE 25-6

The formula is:

Actual

Overhead

BRIEF EXERCISE 25-7

1.

financial ………………………………..

(c)

return on assets

*BRIEF EXERCISE 25-8

(a) Raw Materials Inventory ……………………………………… 12,000

*BRIEF EXERCISE 25-9

(a) Factory Labor …………………………………………………….. 24,900

Labor Price Variance ……………………………………. 1,500

*BRIEF EXERCISE 25–10

The formula is:

Overhead

Overhead

*BRIEF EXERCISE 25–11

The formula is:

Fixed

Overhead

Rate

X

(Normal Capacity Hours – Standard Hours Allowed)

=

Overhead

Volume

Variance

(25,000 – 20,600)

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 25-1

Manufacturing Cost

Elements

Standard Quantity

X

Standard Price

=

Standard

Direct materials

Direct labor

0.2 hours

Total

DO IT! 25-2

The variances are:

Total materials variance = (29,000 X $6.30) – (32,000* X $6.00) = $9,300 favorable

DO IT! 25-3

The variances are:

Total labor variance = (4,000 X $14.30) – (3,800* X $14.00) = $4,000 unfavorable

Labor price variance = (4,000 X $14.30) – (4,000 X $14.00) = $1,200 unfavorable

DO IT! 25-4

Sales revenue $82,700

Cost of goods sold (at standard) 51,600

Standard gross profit 31,100

SOLUTIONS TO EXERCISES

EXERCISE 25-1

(a) Direct materials: (2,000 X 3) X $5 = $30,000

Direct labor: (2,000 X 1/2) X $16 = $16,000

Overhead: $16,000 X 70% = $11,200

EXERCISE 25-2

Ingredient

Amount

Per

Gallon

Standard

Waste

Standard

Usage

Standard

Price

Standard

Cost Per

Gallon

Grape concentrate

Sugar (54 ÷ 50)

60* oz.

1.08 lb.

4%

10%

(a)

(b)

62.5 oz.

1.20 lb.

$.06

.30

$3.75

.36

EXERCISE 25-3

Direct materials

Cost per pound [$5 – (2% X $5) + $0.25] $5.15

Pounds per unit (4.5 + 0.5) X 5 $25.75

EXERCISE 25-4

(a)

Actual service time

1.0 hours

EXERCISE 25-5

(a) Total materials variance:

( AQ X AP )

(29,000 X $4.70)

–

( SQ X SP )

(28,200* X $5.00)

Materials price variance:

( AQ X AP )

(29,000 X $4.70)

$136,300

–

–

( AQ X SP )

(29,000 X $5.00)

$145,000

=

$8,700 F

(29,000 X $5.00)

–

( SQ X SP )

–

( SQ X SP )

Materials price variance:

$144,200

$140,000

=

( AQ X SP )

(28,000 X $5.00)

–

( SQ X SP )

( AQ X AP )

–

( AQ X SP )

EXERCISE 25-6

(a) Total labor variance:

( AH X AR )

(40,600 X $12.15)

$493,290

–

–

( SH X SR )

(40,000* X $12.00)

$480,000

=

$13,290 U

*10,000 X 4

( AH X AR )

–

–

( AH X SR )

=

$6,090 U

( AH X SR )

(40,600 X $12.00)

–

–

( SH X SR )

$480,000

=

$7,200 U

(c) Labor price variance:

( AH X AR )

(40,600 X $12.15)

$493,290

–

–

( AH X SR )

(40,600 X $12.25)

$497,350

=

$4,060 F

( AH X SR )

$497,350

–

–

( SH X SR )

$502,250

=

$4,900 F

EXERCISE 25-7

Total materials variance:

( AQ X AP )

(1,900 X $2.65*)

$5,035

–

–

( SQ X SP )

(1,840** X $2.50)

$4,600

=

$435 U

–

–

=

EXERCISE 25-7 (Continued)

Materials quantity variance:

( AQ X SP )

(1,900 X $2.50)

$4,750

–

–

( SQ X SP )

(1,840 X $2.50)

$4,600

=

$150 U

( AH X AR )

$8,280

=

$160 F

–

EXERCISE 25-7 (Continued)

(Not Required)

Materials Variance Matrix

(1)

(2)

(3)

Actual Quantity

X Actual Price

Actual Quantity

X Standard Price

Standard Quantity

X Standard Price

1,900 X $2.65 = $5,035

1,900 X $2.50 = $4,750

1,840 X $2.50 = $4,600

Labor Variance Matrix

(1)

(2)

(3)

Actual Hours

X Actual Rate

Actual Hours

X Standard Rate

Standard Hours

X Standard Rate

700 X $11.60 = $8,120

700 X $12.00 = $8,400

690 X $12.00 = $8,280

EXERCISE 25-8

(a) Total materials variance:

( AQ X AP )

(1,220 X $128)

$156,160

–

–

( SQ X SP )

(1,200 X $130)

$156,000

=

$160 U

Materials price variance:

( AQ X AP )

(1,220 X $128)

$156,160

–

–

( AQ X SP )

(1,220 X $130)

$158,600

=

$2,440 F

( AH X AR )

–

–

=

$200 U

–

–

=

(b) The unfavorable materials quantity variance may be caused by the

carelessness or inefficiency of production workers. Alternatively, the

excess quantities may be caused by inferior quality materials acquired

by the purchasing department.

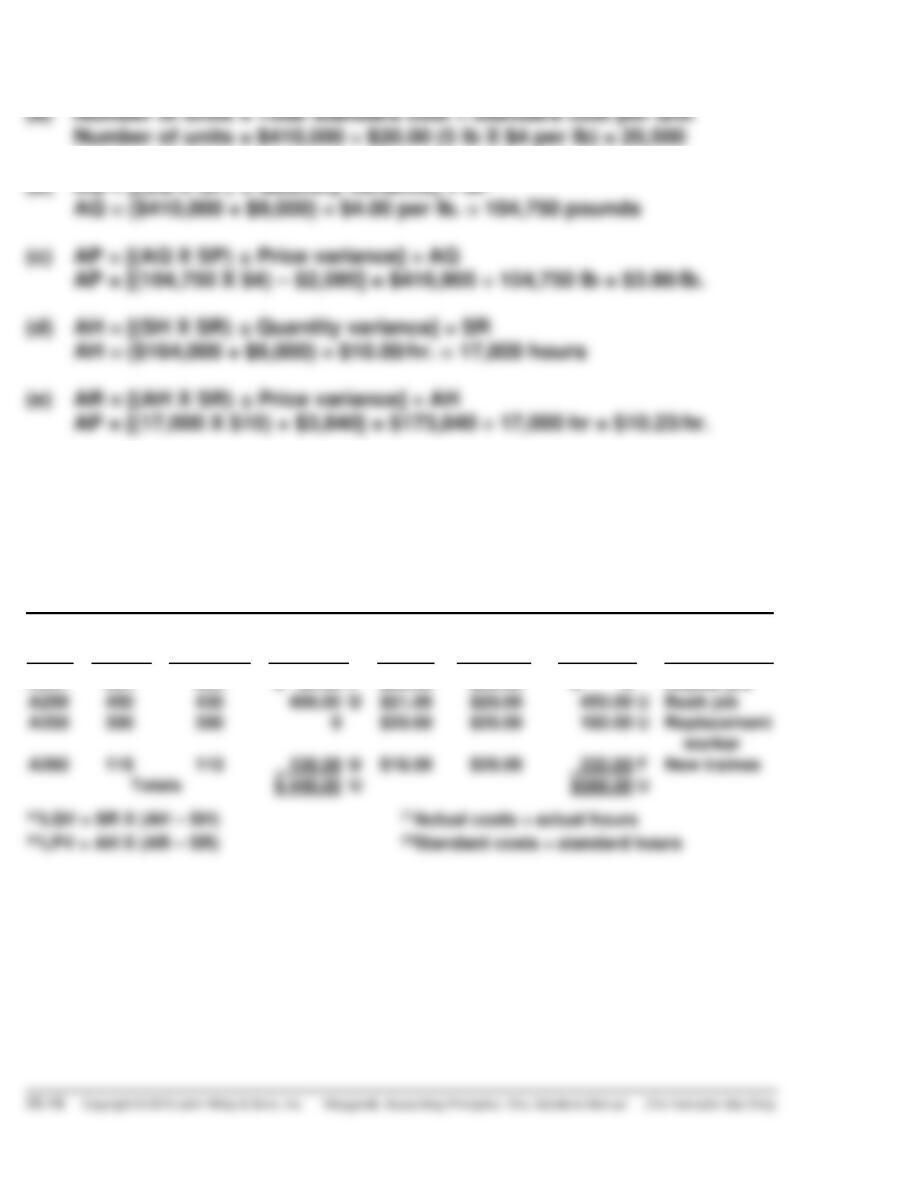

EXERCISE 25-9

(a) Number of units = Total standard cost ÷ Standard cost per unit

Number of units = $410,000 ÷ $20.00 (5 lb X $4 per lb) = 20,500

(b) AQ = [(SQ X SP)

±

Quantity variance] ÷ SP

AQ = ($410,000 + $9,000) ÷ $4.00 per lb. = 104,750 pounds

±

±

±

AP = [(17,000 X $10) + $3,840] = $173,840 ÷ 17,000 hr = $10.23/hr.

EXERCISE 25–10

TOBY TOOL & DIE COMPANY

Direct Labor Variance Report

For the Month Ended March 31, 2017

Job

No.

Actual

Hours

Standard

Hours

Quantity

Variance

(a)

Actual

Rate

(1)

Standard

Rate

(2)

Price

Variance

(b)

Explanation

A257

A258

221

450

225

430

$ 80.00

400.00

F

U

$20.00

$21.00

$20.00

$20.00

$ 0

450.00

U

Repeat job

Rush job

EXERCISE 25–11

Total overhead variance:

Actual Overhead

$263,000

–

–

Overhead Applied

$260,000

(52,000 X $5)

=

$3,000 U

EXERCISE 25–12

(a)

Overhead Budget

(at normal capacity)

÷

Direct Labor Hours

(at normal capacity)

=

Predetermined

Overhead Rate

Variable

$250,000

100,000

$2.50

Fixed

600,000

100,000

$6.00

(b)

X

=

(c)

=

$856,000

EXERCISE 25–13

(a)

(AQ X AP)

( $10,200)

–

–

( SQ X SP)

(2,100* X $5)

=

=

Total Materials Variance

$300 F

(AQ X AP)

( $10,200)

–

–

( AQ X SP)

(2,400 X $5)

=

=

Materials Price Variance

$1,800 F

–

–

( SQ X SP)

(2,100* X $5)

=

=

Materials Quantity Variance

$1,500 U

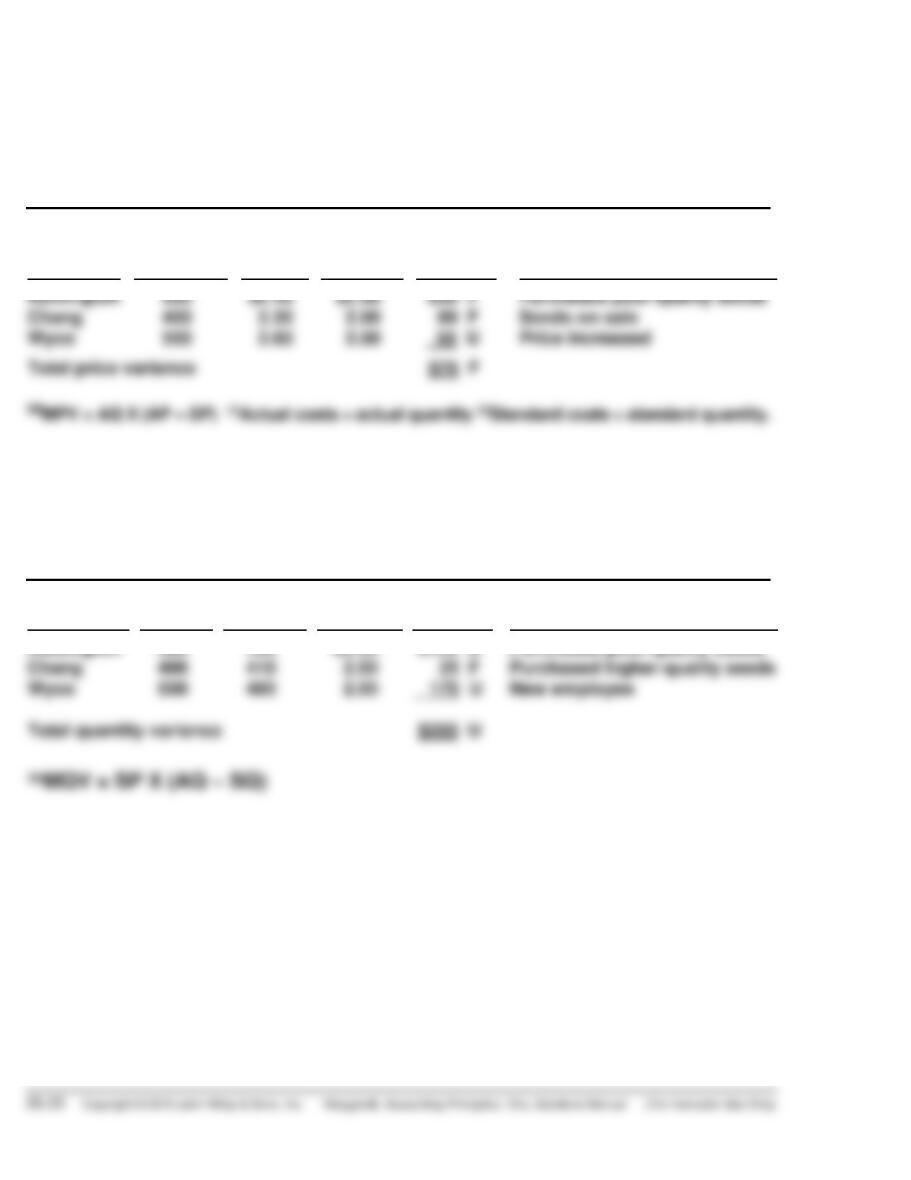

EXERCISE 25–14

(a)

PICARD LANDSCAPING

Variance Report – Purchasing Department

For the Current Month

Project

Actual

Pounds

Purchased

(1)

Actual

Price

(2)

Standard

Price

Price

Variance

(a)

Explanation

Remington

500

$2.40

$2.50

$50 F

Purchased poor–quality seeds

(b)

PICARD LANDSCAPING

Variance Report – Production Department

For the Current Month

Project

Actual

Pounds

Standard

Pounds

Standard

Price

Quantity

Variance

(b)

Explanation

Remington

Chang

500

400

460

410

$2.50

2.50

$100 U

25 F

Purchased poor-quality seeds

Purchased higher-quality seeds