EXERCISE 25–15

URBAN CORPORATION

Variance Report – Purchasing Department

For Week Ended January 9, 2017

Type of

Materials

Quantity

Purchased

Actual

Price

Standard

Price

Price

Variance

Explanation

Rogue 11

Storm 17

Beast 29

27,500 lbs.

7,000 oz.

22,000 units.

$5.20

$3.45

$0.40

$5.00

$3.30

$0.43

$5,500 U

$1,050 U

$ 660 F

Price increase

Rush order

Bought larger quantity

EXERCISE 25–16

FISK COMPANY

Income Statement

For the Month Ended January 31, 2017

Sales revenue (8,000 X $8) ……………………………………… $64,000

Cost of goods sold (8,000 X $5) ……………………………… 40,000

Gross profit (at standard) ………………………………………. 24,000

Variances

EXERCISE 25–17

1. Balanced scorecard—(c) An approach that incorporates financial and

nonfinancial measures in an integrated system that links performance

measurement and a company’s strategic goals.

2. Variance—(a) The difference between total actual costs and total stan-

EXERCISE 25–18

1. Customer perspective.

EXERCISE 25–19

1.

Learning and growth perspective.

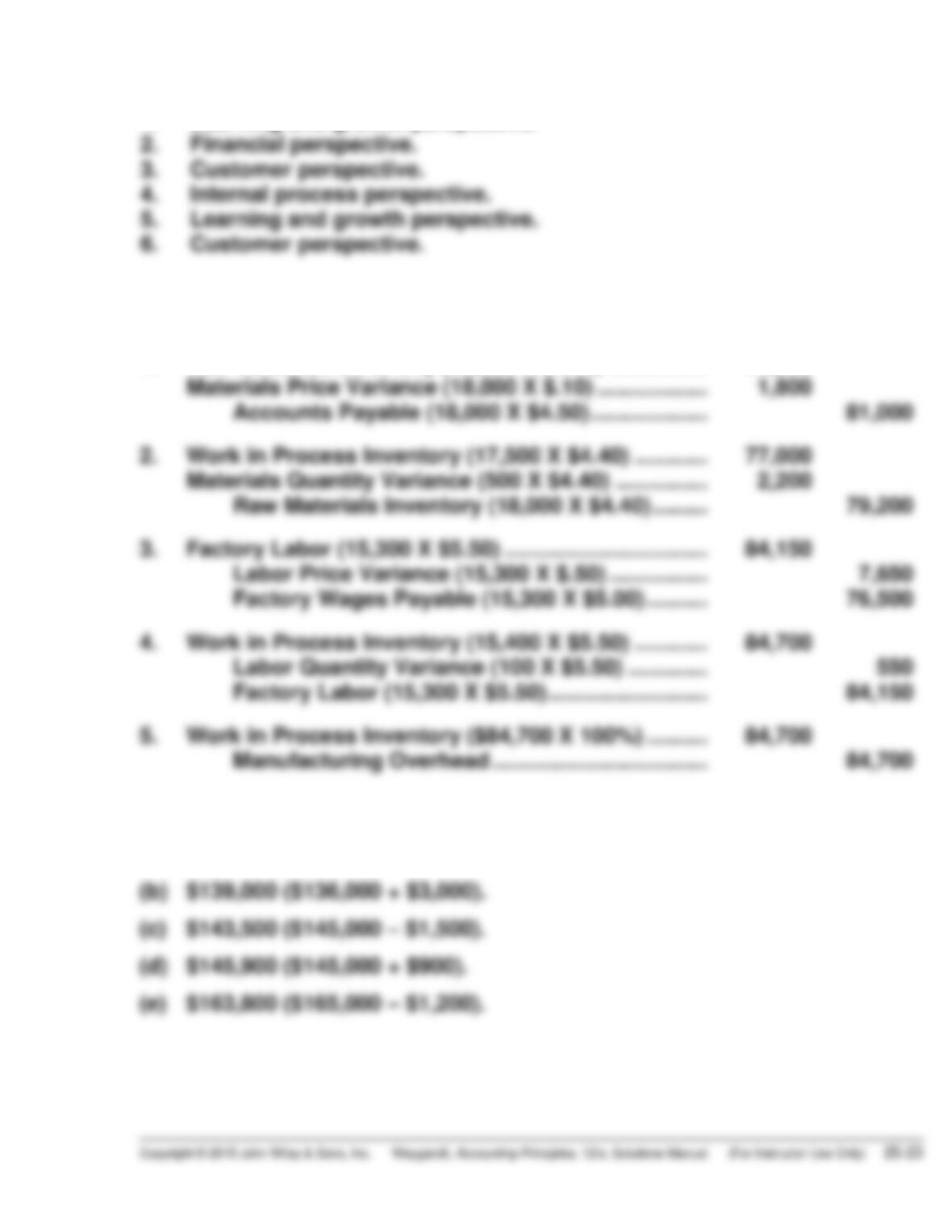

*EXERCISE 25–20

1. Raw Materials Inventory (18,000 X $4.40) ……………. 79,200

Materials Price Variance (18,000 X $.10) ……………… 1,800

Accounts Payable (18,000 X $4.50) ………………. 81,000

*EXERCISE 25-21

(a) $136,000 ($138,000 – $2,000).

*EXERCISE 25-22

Raw Materials Inventory (1,900 X $2.50) ……………………… 4,750

Materials Price Variance (1,900 X $0.15) ……………………… 285

Accounts Payable (1,900 X $2.65) ………………………… 5,035

*230 X 3

*EXERCISE 25-23

(a)

Item

Amount

Hours

Rate

$54,450

Variable overhead ……………………………..

$34,650

16,500

$2.10

EXERCISE 25-23 (Continued)

Overhead volume variance:

Fixed Overhead

Rate

X

Normal Capacity

Hours

–

Standard Hours

Allowed

*EXERCISE 25-24

(a)

1.

Total actual overhead cost

=

Overhead

Budgeted +

Overhead

Controllable

Variance

=

($18,000 + $12,600) + $1,200

=

$31,800

=

=

=

=

=

2,000 hours X $6 = $12,000

=

=

*EXERCISE 25-25

(a)

(Actual)

($19,500)

–

–

(Applied)

(1,800 X $10*)

=

=

Total Overhead Variance

$1,500 U

(Actual)

($19,500)

–

–

(Budgeted)

($17,600)

=

=

Overhead Controllable Variance

$1,900 U

SOLUTIONS TO PROBLEMS

PROBLEM 25–1A

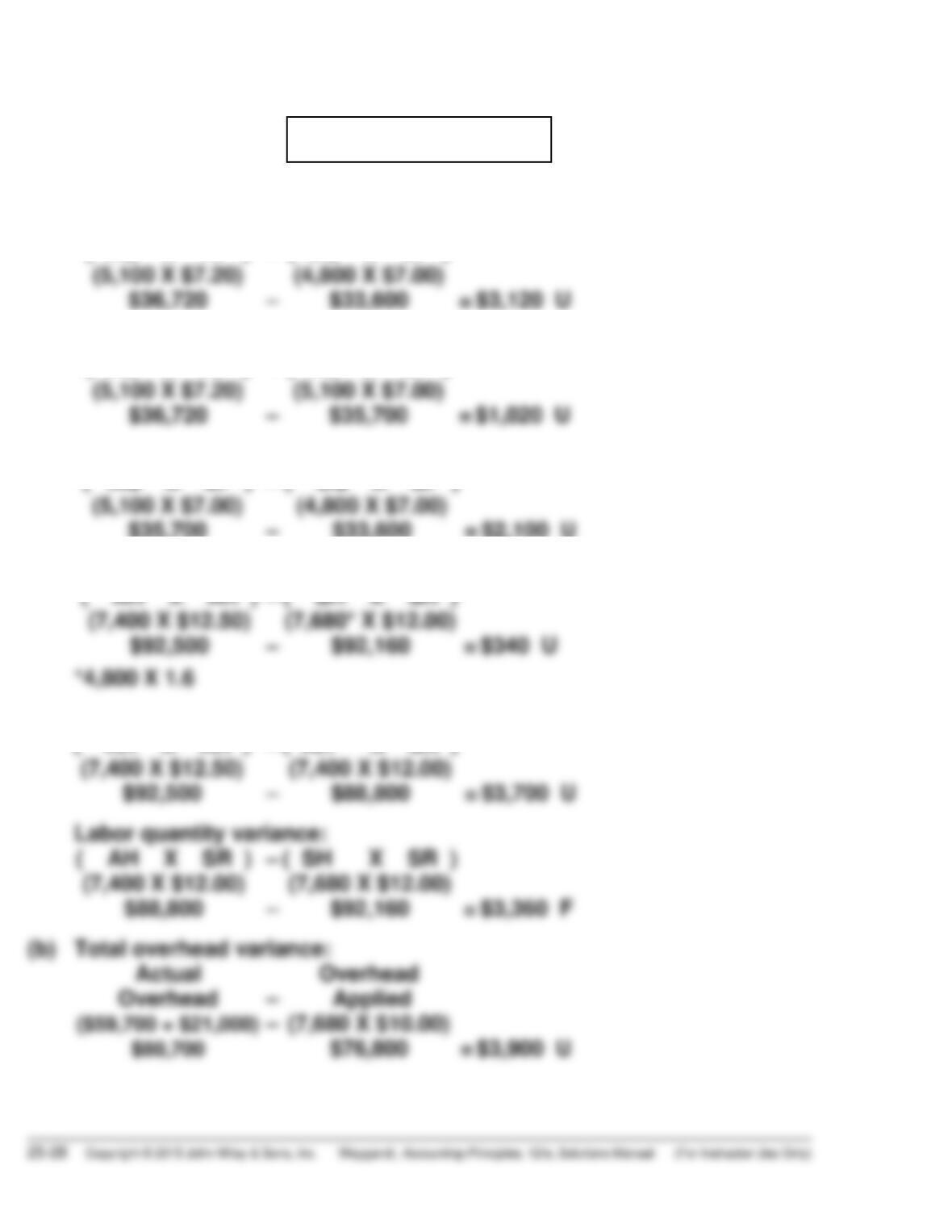

(a) Total materials variance:

( AQ X AP )

(5,100 X $7.20)

$36,720

–

–

( SQ X SP )

(4,800 X $7.00)

$33,600

=

$3,120 U

Materials price variance:

( AQ X AP )

(5,100 X $7.20)

$36,720

–

–

( AQ X SP )

(5,100 X $7.00)

$35,700

=

$1,020 U

( AQ X SP )

–

Labor price variance:

( AH X AR )

(7,400 X $12.50)

$92,500

–

–

( AH X SR )

(7,400 X $12.00)

$88,800

=

$3,700 U

Labor quantity variance:

–

PROBLEM 25–2A

(a) 1. Total materials variance:

( AQ X AP )

(10,600 X $2.25)

$23,850

–

–

( SQ X SP )

(10,000 X $2.10)

$21,000

=

$2,850 U

( AQ X AP )

( AQ X SP )

( AQ X SP )

–

( SQ X SP )

2. Total labor variance:

( AH X AR )

(14,400 X $8.40*)

$120,960

–

–

( SH X SR )

(15,000 X $8.00**)

$120,000

=

$960 U

*$120,960 ÷ 14,400 **$120,000 ÷ 15,000

( AH X AR )

$120,960

–

–

( AH X SR )

=

$5,760 U

–

(b) Total overhead variance:

Actual

Overhead

–

Overhead

Applied

PROBLEM 25-2A (Continued)

(c) AYALA CORPORATION

Income Statement

For the Month Ended June 30, 2017

Sales revenue …………………………………………….. $400,000

Cost of goods sold (at standard) …………………. 334,500*

Gross profit (at standard) ……………………………. 65,500

Variances

PROBLEM 25–3A

(a) 1. Total materials variance:

( AQ X AP )

(90,500 X $4.15)

$375,575

–

–

( SQ X SP )

(90,000* X $4.40)

$396,000

=

$20,425 F

*11,250 X 8

Materials price variance:

( AQ X AP )

(90,500 X $4.15)

$375,575

–

–

( AQ X SP )

(90,500 X $4.40)

$398,200

=

$22,625 F

( AQ X SP )

–

–

( AH X SR )

=

PROBLEM 25-3A (Continued)

(c) The materials price variance is more than 4% from standard. The actual

price for materials of $4.15 is $.25 below the standard price of $4.40 or

5.7% ($.25 ÷ $4.40). The same result can be obtained by dividing the

total price variance by the total standard price for the quantities purchased

($22,625 ÷ $398,200).

PROBLEM 25–4A

(a) $3,510 ÷ 117,000 = $.03; $.92 + $.03 = $.95 standard materials price per

pound. OR

117,000 X $.92 = $107,640; $107,640 + $3,510 = $111,150; $111,150 ÷

117,000 = $.95 per pound.

(b) $4,750 ÷ $.95 = 5,000 pounds; 117,000 – 5,000 = 112,000 standard

quantity for 28,000 units or 4.0 pounds (112,000 ÷ 28,000) per unit. OR

$111,150 – $4,750 = $106,400; $106,400 ÷ $.95 = 112,000; 112,000 ÷

28,000 = 4.0 pounds per unit.

PROBLEM 25–5A

(a) Materials price variance:

( AQ X AP )

(3,050 X $1.40*)

$4,270

–

–

( AQ X SP )

(3,050 X $1.46)

$4,453

=

$183 F

=

$146 U

(b) Total Overhead variance:

Actual

Overhead

PROBLEM 25-5A (Continued)

(c)

HART LABS, INC.

Income Statement

For the Month Ended November 30, 2017

Service revenue ……………………………………………… $75,000

Cost of service provided (at standard)

(1,500 X $42.92) …………………………………………… 64,380

(d) The unfavorable materials quantity variance could be caused by poor

quality materials or inexperienced workers or faulty test procedures.

*PROBLEM 25–6A

(a) 1. Raw Materials Inventory (6,200 X $1.00) ………… 6,200

3. Factory Labor (2,000 X $8) ……………………………. 16,000

Labor Price Variance

[2,000 X ($8.00 – $7.80)] ……………………… 400

Factory Wages Payable (2,000 X $7.80) ….. 15,600

4. Work in Process Inventory

(1,900 X $8.00) …………………………………………. 15,200

Labor Quantity Variance

[(2,000 – 1,900) X $8.00] ……………………………. 800

Factory Labor …………………………..………….. 16,000

*PROBLEM 25-6A (Continued)

(b)

Raw Materials Inventory

Materials Price Variance

Work in Process Inventory

(1) 6,200

(2) 6,200

(1) 310

(2) 5,700

(4) 15,200

(6) 23,750

(7) 44,650

(c) Overhead Variance ($25,000 – $23,750) …………… 1,250

Manufacturing Overhead …………………………. 1,250

(d) JORGENSEN CORPORATION

Income Statement

For the Month Ended January 31, 2017

Sales revenue ……………………………………………….. $65,000

Cost of goods sold (at standard)

(1,900 X $23.50) ………………………………………….. 44,650

Gross profit (at standard) ……………………………….. 20,350

Variances