1503

Exercise 25-11 (25 minutes)

a.

Project X1

Net Cash

Flows

Present

Value of

1 at 4%

Present

Value of

Net Cash

Flows

Year 1 ……………………………………………………….

$ 25,000

0.9615

$ 24,038

Year 2 ……………………………………………………….

0.9246

Year 3 ……………………………………………………….

$121,000

Net present value ………………………………………….

$ 30,646

Project X2

Net Cash

Flows

Present

Value of

1 at 4%

Present

Value of

Net Cash

Flows

Year 1 ……………………………………………………….

$ 60,000

0.9615

$ 57,690

Year 2 ……………………………………………………….

0.9246

Year 3 ……………………………………………………….

Net present value ………………………………………….

$ 19,480

b.

1504

Exercise 25-12 (25 minutes)

a.

Project X1

Net Cash

Flows

Present

Value of

1 at 12%

Present

Value of

Net Cash

Flows

Year 1 ……………………………………………………….

$ 25,000

0.8929

$ 22,323

Year 2 ……………………………………………………….

0.7972

Year 3 ……………………………………………………….

0.7118

Project X2

Net Cash

Flows

Present

Value of

1 at 4%

Present

Value of

Net Cash

Flows

Year 1 ……………………………………………………….

$ 60,000

0.8929

$ 53,574

Year 2 ……………………………………………………….

0.7972

Year 3 ……………………………………………………….

0.7118

b.

1505

Exercise 25-13 (20 minutes)

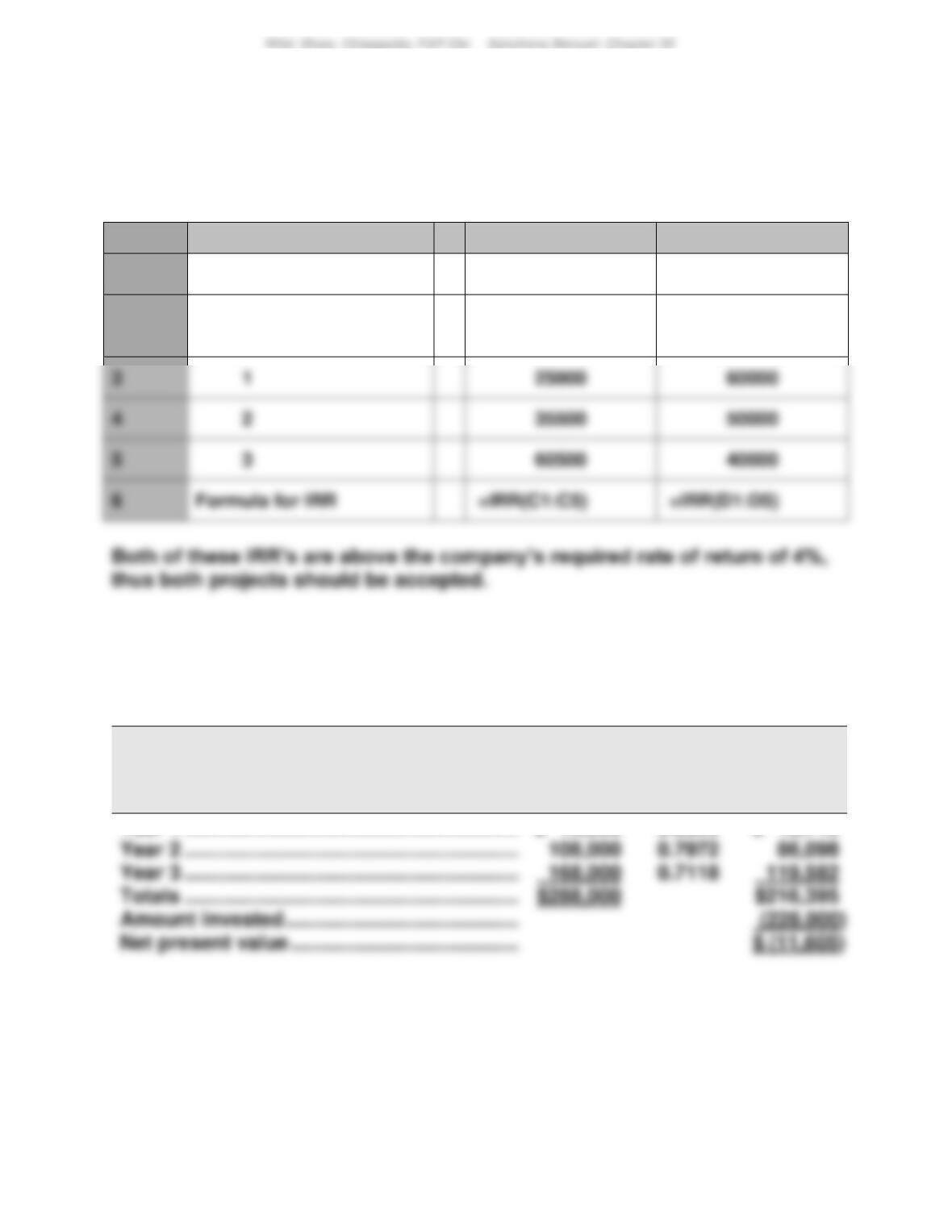

Using Excel, Project X1 (X2) has an internal rate of return of 20.34% (12.99%).

Project X1 Project X2

A

B

C

D

1

Initial investment

-80000

–120000

2

Annual cash flows,

end of period

4

2

5

3

6

Formula for IRR

Exercise 25-14 (35 minutes)

1.

PROJECT C1

Net Cash

Flows

Present

Value of

1 at 12%

Present

Value of

Net Cash

Flows

Year 1 ……………………………………………………….

$ 12,000

0.8929

$ 10,715

Year 2 ……………………………………………………….

0.7972

Year 3 ……………………………………………………….

0.7118

1506

Exercise 25-14 (continued)

PROJECT C2

Net Cash

Flows

Present

Value of

1 at 12%

Present

Value of

Net Cash

Flows

Year 1 ……………………………………………………….

$ 96,000

0.8929

$ 85,718

Year 2 ……………………………………………………….

0.7972

Year 3 ……………………………………………………….

0.7118

$288,000

PROJECT C3

Net Cash

Flows

Present

Value of

1 at 12%

Present

Value of

Net Cash

Flows

Year 1 ……………………………………………………….

$180,000

0.8929

$160,722

Year 2 ……………………………………………………….

0.7972

Year 3 ……………………………………………………….

0.7118

$288,000

$242,720

2. INTERNAL RATE OF RETURN VS. NET PRESENT VALUE FOR C2

Project C2 will have an internal rate of return higher than 12%.

1507

Exercise 25-15A (20 minutes)

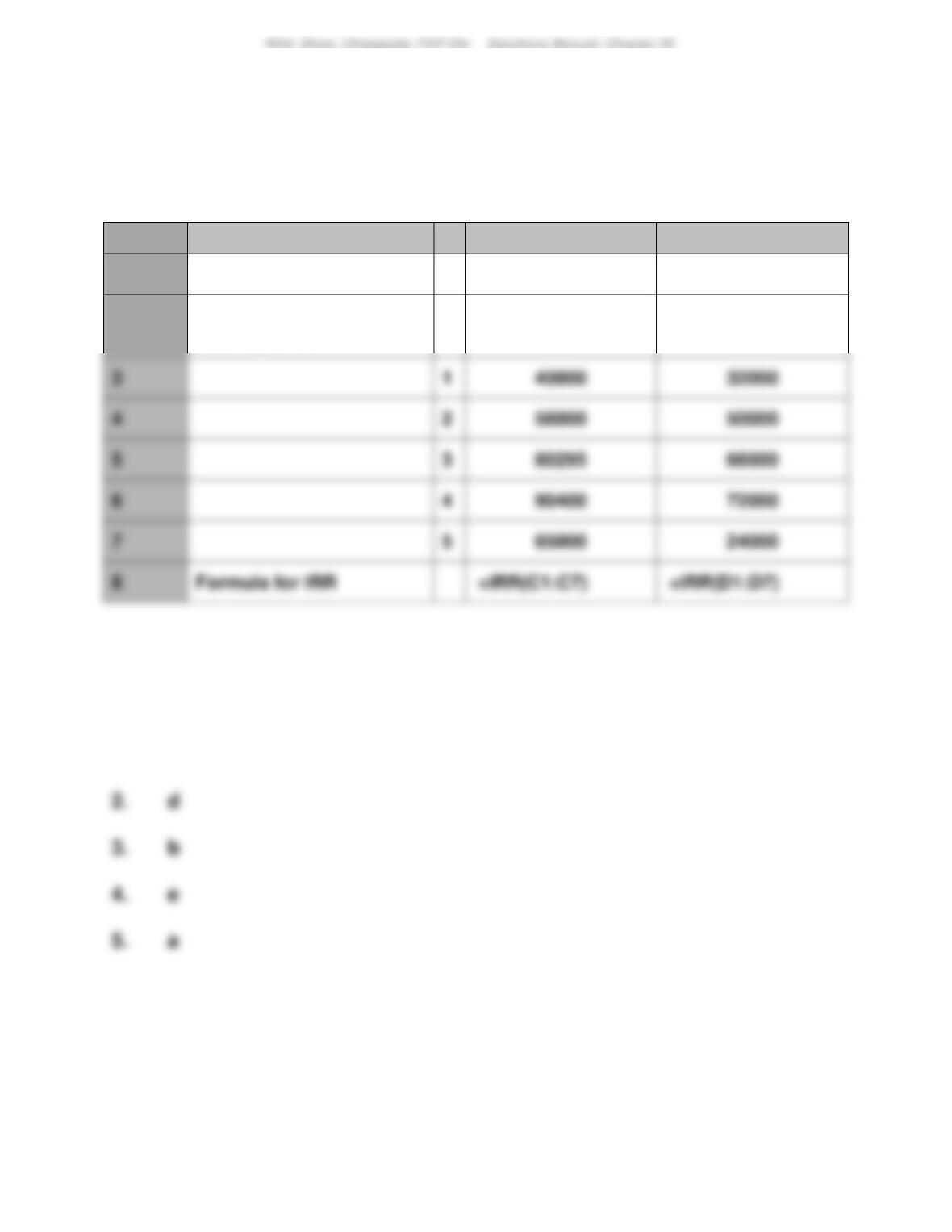

Using Excel, Project A (B) has an internal rate of return of 26.96 (35.00%).

Project A Project B

A

B

C

D

1

Initial investment

-160000

-105000

2

Annual cash flows,

end of period

4

2

5

3

6

4

7

5

8

Formula for IRR

Exercise 25-16 (10 minutes)

1. c

1508

Exercise 25-17 (25 minutes)

Normal

Additional

Combined

Volume

Volume*

Total

Sales …………………………………………..

$2,250,000

$180,000

$2,430,000

Costs and expenses

Exercise 25-18 (20 minutes)

Part 1

Normal

Additional

Combined

Volume

Volume

Total

Sales …………………………………………..

$8,000,000

$1,500,000

$9,500,000

Costs and expenses

1,200,000

1,400,000

0

Based on this analysis, Goshford should accept the new business.

Part 2

Other factors that Goshford should consider before deciding whether to

accept the new business are:

• Will regular customers demand a reduction in their selling price if they

hear of the sale to the new customer?

• Will the new customer expect to receive the special price for future sales?

• If Goshford accepts the new business, it will be operating at full capacity.

Can they maintain that full capacity without any defects?

• What will happen to regular sales if they cannot meet current customers’

expectations because of this order?

1510

Exercise 25-19 (20 minutes)

Make

Buy

Variable costs (65,000 x $1.95) ………………………

$126,750

—-

RECOMMENDATION: Note that the allocated fixed costs of $62,000 are not

relevant to this managerial decision because they will continue whether the

Exercise 25–20 (20 minutes)

Make

Buy

Variable costs (40,000 x $1.95) ………………………

$ 78,000

—-

1511

Exercise 25–21 (15 minutes)

Scrap

Rework

Sale of scrapped/reworked units …………………..

$44,000

$187,000

(1) The incremental income from selling as scrap is $44,000 (22,000 x $2.00).

Exercise 25-22 (15 minutes)

INCREMENTAL REVENUE AND COST OF ADDITIONAL PROCESSING

Revenue if processed further (7,000 x $25) ………………………………………..

$175,000

Incremental revenue …………………………………………………………………………

1512

Exercise 25-23 (25 minutes)

Sell as is

Process

further

Incremental revenue ……………………………………..

$700,000

$1,372,000*

Product B ……………………………………………………………………

$105

Product C ……………………………………………………………………

ALTERNATE SOLUTION FORMAT

Net income (loss) from processed products

Revenue if processed further…………………………………………

$1,372,000

Less: Additional costs of processing…………………………...

RECOMMENDATION: This analysis shows that the company will be better off by

Exercise 25-24 (30 minutes)

Preliminary computations

Contribution margin per hour

Product TLX

Product MTV

Selling price per unit ………………………………………….

$15.00

$ 9.50

Variable costs per unit ……………………………………….

Machine-hours to produce 1 unit ………………………..

0.50

Contribution margin per machine-hour

1513

Exercise 25-24 (continued)

1. FOR PRODUCT TLX

Maximum sales ……………………………………………………….

4,700

units

Hours needed per unit ……………………………………………………

0.50

hours

Hours needed per unit ……………………………………………………

0.20

2. CONTRIBUTION MARGIN FROM THE RECOMMENDED SALES MIX

Units

Contribution

per Unit

Total

Total ……………………………………………

1514

Exercise 25-25 (30 minutes)

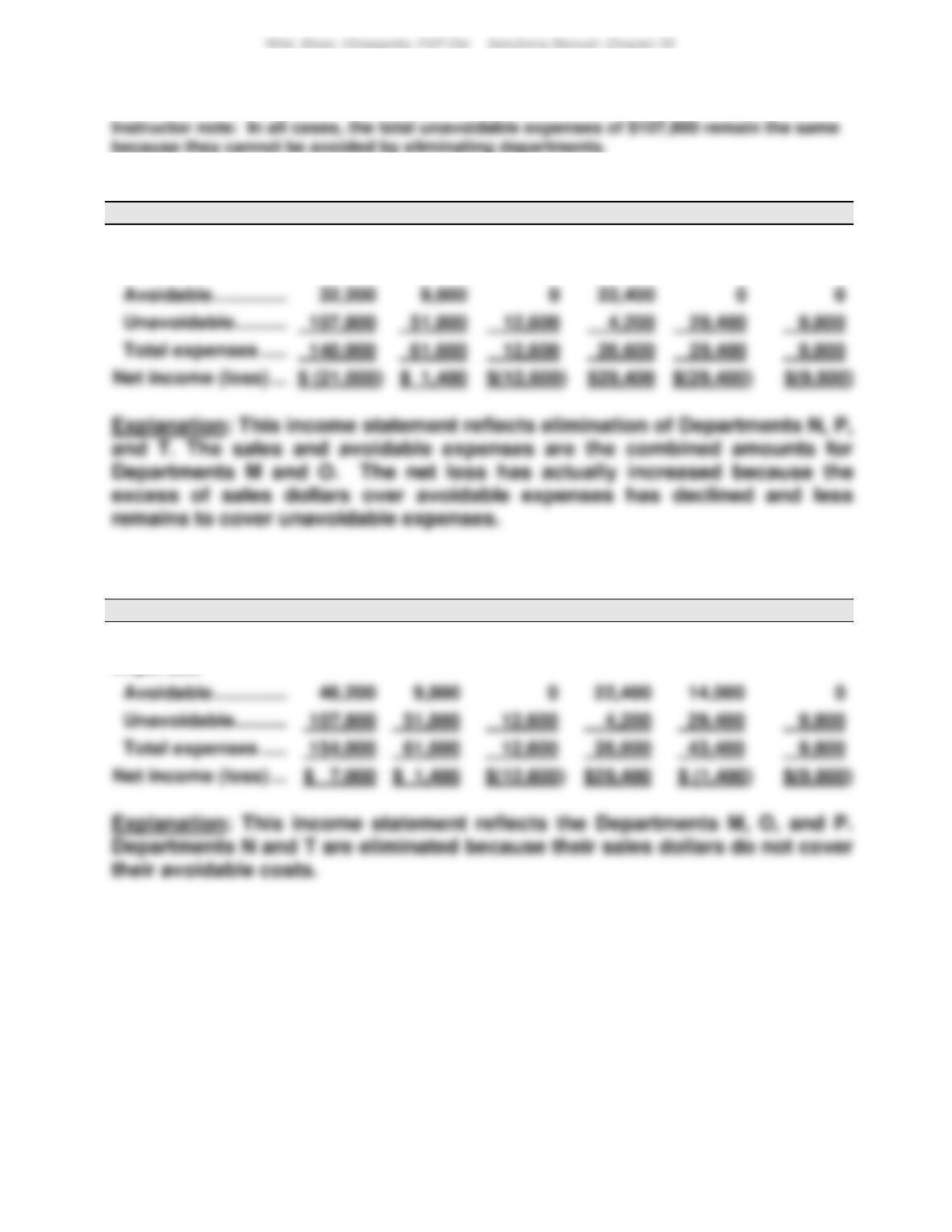

1. DEPARTMENTS WITH EXPECTED NET LOSSES ELIMINATED

Total

M

N

O

P

T

Sales…………………………..

$119,000

$63,000

$ 0

$56,000

$ 0

$ 0

Expenses

2. DEPARTMENTS WITH LESS SALES THAN AVOIDABLE EXPENSES ELIMINATED

Total

M

N

O

P

T

Sales…………………………..

$161,000

$63,000

$ 0

$56,000

$42,000

$ 0

Expenses

0

1515

Exercise 25–26 (20 minutes)

ALTERNATIVE A: INCREASE OR (DECREASE) IN NET INCOME

Cost to buy new machine ……………………………………………………….

$(115,000)

Reduction in variable manufacturing costs* …………………………..

ALTERNATIVE B: INCREASE OR (DECREASE) IN NET INCOME

Cost to buy new machine ……………………………………………………….

$(125,000)

Reduction in variable manufacturing costs** …………………………..

Exercise 25-27 (15 minutes)

1. Recovery time computation

2. The advantage of break-even time is that it considers the time value of

3. When (1) the interest rate is very low, 1% for example, and (2) the

Exercise 25-28 (20 minutes)

1516

(1)

Total

Costs

Direct materials ($100 x 10,000) …………………….

$ 1,000,000

(2) Markup percentage = Target profit/Total cost

(3)

Per Unit

Total cost ……………………………………………………..

Total variable cost ………………………………………..

Exercise 25-29 (20 minutes)

(1) Variable cost per unit

Variable Cost

Per Unit

Direct materials …………………………………………….

$ 70

(3) Selling price using variable cost method

Per Unit

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 25

1518

PROBLEM SET A

Problem 25-1A (50 minutes)

Part 1

Part 2

Net

Net Cash

Income

Flow

Expected annual sales of new product ………………

$1,840,000

$1,840,000

Expected costs of new product

Income before taxes ………………………………………….

Part 3

1519

Problem 25-1A (Continued)

Part 4

Part 5

Present Value of Net Cash Flows

Present

Present

Net Cash

Value of

Value of Net

Flows

1 at 7%

Cash Flows

Year 1 ………………………………………………….

$168,900

0.9346

$ 157,853.94

Year 2 ………………………………………………….

0.8734

Year 3 ………………………………………………….

0.8163

Year 4* …………………………………………………

0.7629

1520

Problem 25-2A (55 minutes)

Part 1

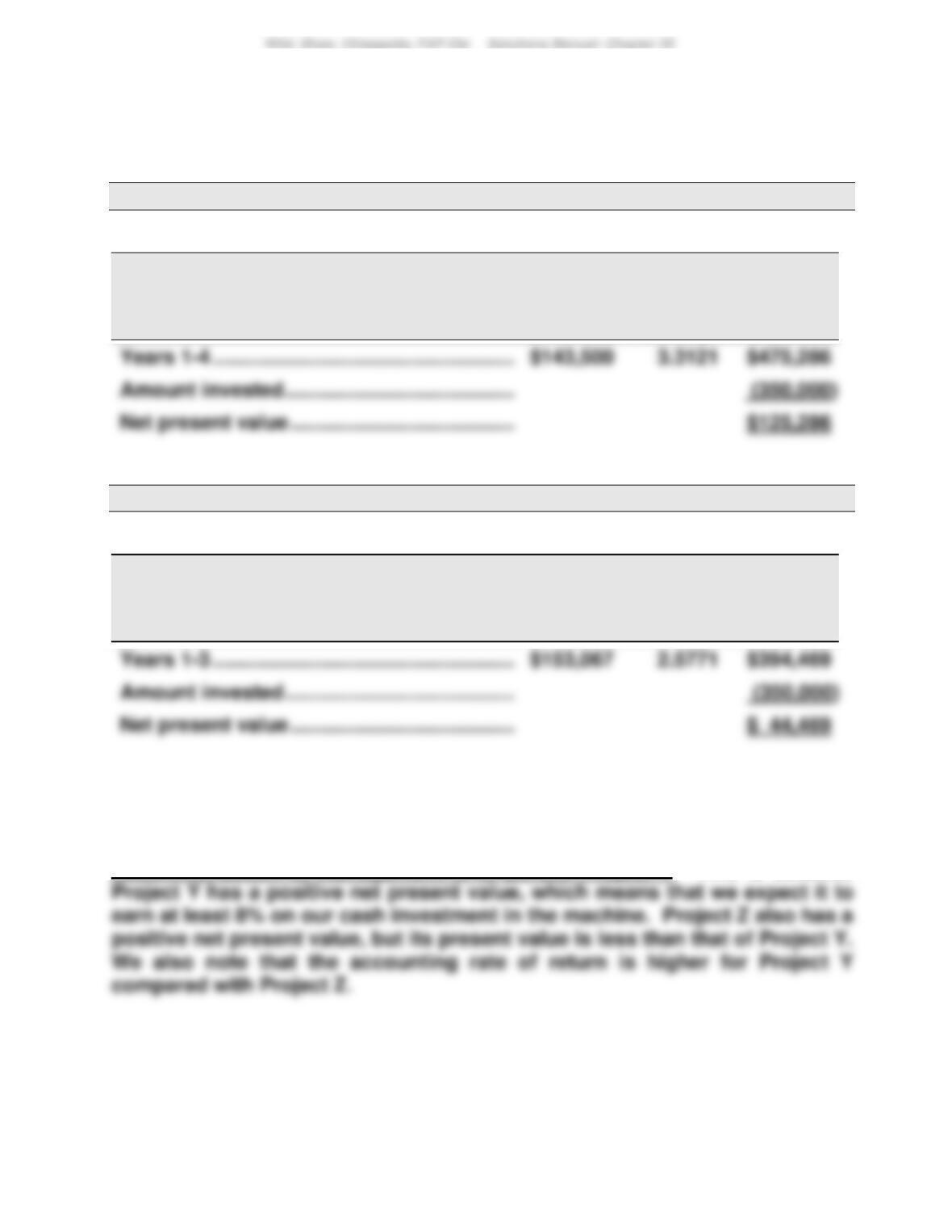

PROJECT Y

Net income ……………………………………………………….……………………..

$ 56,000

$143,500

PROJECT Z

Net income ……………………………………………………….……………………..

$ 36,400

$153,067

Part 2

PROJECT Y

PROJECT Z

1521

Problem 25-2A (Continued)

Part 3

PROJECT Y

PROJECT Z

1522

Problem 25-2A (Continued)

Part 4

PROJECT Y

Present Value of Net Cash Flows

Present

Present

Value of

Value of

Net Cash

Flows

1 at 8%

Annuity

Net Cash

Flows

PROJECT Z

Present Value of Net Cash Flows

Present

Present

Value of

Value of

Net Cash

Flows

1 at 8%

Annuity

Net Cash

Flows

Part 5

Recommendation to management is to pursue Project Y. This is because