1. a. Differential revenue is the amount of increase or decrease in revenue expected from a

p

articular course of action compared to an alternative.

b. Differential cost is the amount of increase or decrease in cost expected from a particular

course of action compared to an alternative.

c. Differential profit is the difference between differential revenue and differential cost.

3. If there is demand for the premium-grade product, the differential revenue (premium less commodity)

may exceed the differential cost to process the product to premium grade.

4. A business should only accept business at a special price if the lower price will not contaminate the

regular pricing for other customers or induce other customers to demand the special price. In

addition, the business must be careful not to violate the Robinson-Patman Act, which prohibits

uncompetitive price differences across different markets for the same product. Finally, the business

must consider the longer-term ramifications of offering discount business to a customer that may

want to order in the future.

5. It is reasonable to purchase from the supplier if the fixed cost per unit is less than 50 cents.

That is, if the fixed cost is less than 50 cents per unit, then the variable cost per unit will exceed

the supplier’s price, making the supplier price more attractive.

b

7. In the long run, the normal selling price must be set high enough to cover all costs (both fixed an

d

variable) and provide a reasonable amount for profit.

8. In setting prices, managers should consider such factors as the prices of competing products

and the general economic conditions of the marketplace.

CHAPTER 25

DIFFERENTIAL ANALYSIS, PRODUCT PRICING,

DISCUSSION QUESTIONS

AND ACTIVITY-BASED COSTING

p

CHAPTER 25 Differential Analysis, Product Pricing, and Activity-Based Costing

DISCUSSION QUESTIONS (Continued)

9. The target cost concept begins with a price that can be sustained in the marketplace, then

subtracts a target profit, thus determining the target cost. The cost is made to conform to the

p

rice required in the market. In contrast, under cost-plus, a markup is added to the cost. The

resulting price is assumed to be acceptable in the market.

10. The proper measure of product value in a bottlenecked process is the contribution margin per

b

ottleneck hour.

CHAPTER 25 Differential Analysis, Product Pricing, and Activity-Based Costing

PE 25-1A

Lease Sell Differential

Machine Machine Effects

PE 25-1B

Lease Sell Differential

Equipment Equipment Effects

(Alternative 1) (Alternative 2) (Alternative 2)

*

$113,000 × 6%

Ferrigno Company should sell the equipment.

Differential Analysis

Lease Equipment (Alt. 1) or Sell Equipment (Alt. 2)

March 23

PRACTICE EXERCISES

Differential Analysis

Lease Machine (Alt. 1) or Sell Machine (Alt. 2)

February 21

CHAPTER 25 Differential Analysis, Product Pricing, and Activity-Based Costing

PE 25-2A

Continue Discontinue Differential

Product Sigma Product Sigma Effects

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues $ 436,000 $ 0 $(436,000)

Product Sigma should be continued.

PE 25-2B

Continue Discontinue Differential

Product X Product X Effects

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues $ 94,800 $ 0 $(94,800)

Costs:

Variable cost of goods sold (61,200) 0 61,200

Product X should be discontinued.

Differential Analysis

Continue Product X (Alt. 1) or Discontinue Product X (Alt. 2)

May 9

Differential Analysis

Continue Product Sigma (Alt. 1) or Discontinue Product Sigma (Alt. 2)

Decembe

r

10

CHAPTER 25 Differential Analysis, Product Pricing, and Activity-Based Costing

PE 25-3A

Make Buy Differential

Bread Bread Effects

(Alternative 1) (Alternative 2) (Alternative 2)

Unit costs:

Purchase price $ 0 $(148) $(148)

The company should make the bread.

PE 25-3B

Make Buy Differential

Bottles Bottles Effects

(Alternative 1) (Alternative 2) (Alternative 2)

Unit costs:

Purchase price $ 0 $(29) $(29)

The company should buy the bottles.

Differential Analysis

Make Bottles (Alt. 1) or Buy Bottles (Alt. 2)

March 30

Differential Analysis

Make Bread (Alt. 1) or Buy Bread (Alt. 2)

July 7

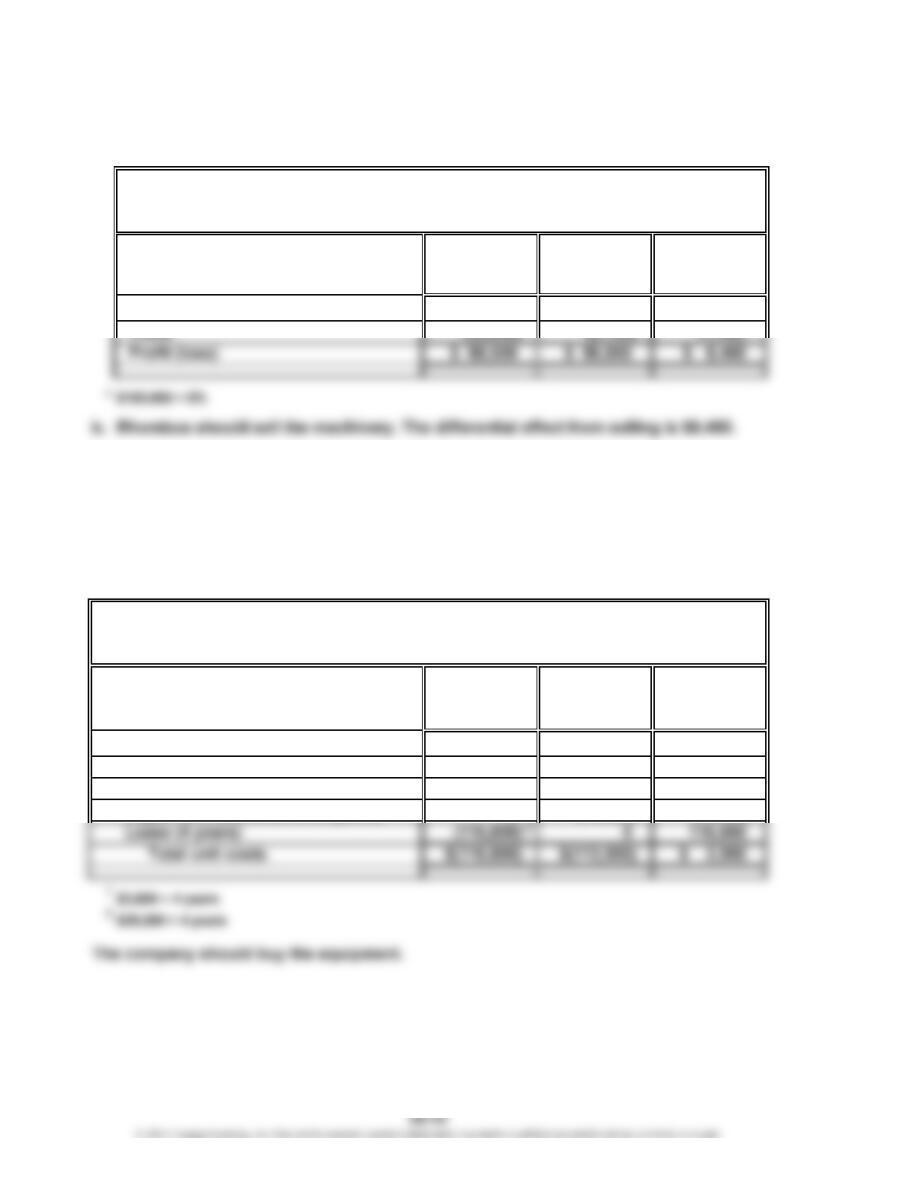

PE 25-4A

Continue Replace

with Old Old Differential

Machine Machine Effects

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues:

Proceeds from sale of old machine $ 0 $ 390,000 $ 390,000

Costs:

PE 25-4B

Continue Replace

with Old Old Differential

Machine Machine Effects

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues:

Proceeds from sale of old machine $ 0 $ 39,400 $ 39,400

Costs:

Purchase price 0 (58,500) (58,500)

Direct labor (5 years) (43,500) (29,500) 14,000

Profit (loss) $(43,500) $(48,600) $ (5,100)

Differential Analysis

Continue with Old Machine (Alt. 1) or Replace Old Machine (Alt. 2)

April 11

Differential Analysis

Continue with Old Machine (Alt. 1) or Replace Old Machine (Alt. 2)

October 3

12

CHAPTER 25 Differential Analysis, Product Pricing, and Activity-Based Costing

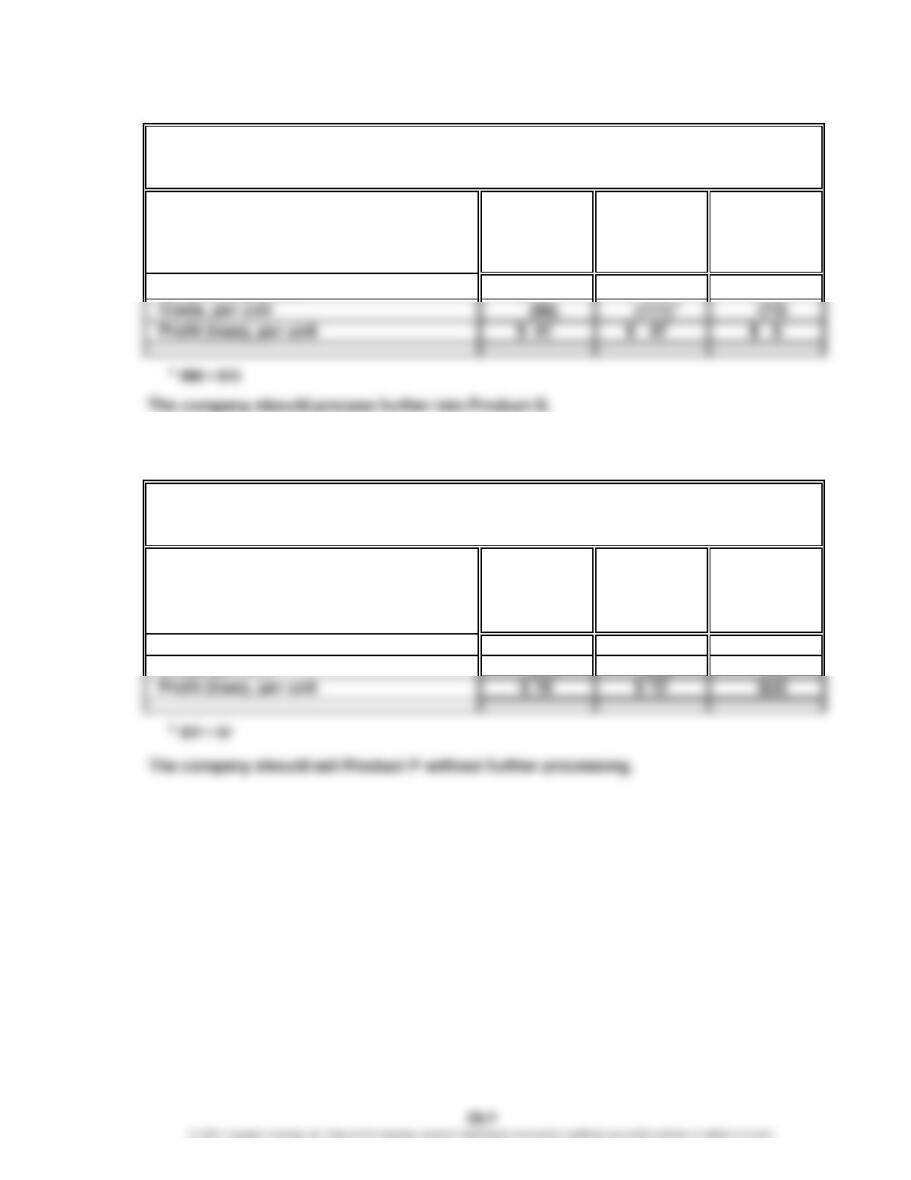

PE 25-5A

Process

Sell Further into Differential

Product F Product G Effects

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues, per unit $139 $ 158 $ 19

PE 25-5B

Process

Sell Further into Differential

Product P Product Q Effects

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues, per unit $ 47 $ 50 $ 3

Differential Analysis

Sell Product P (Alt. 1) or Process Further into Product Q (Alt. 2)

February 26

Differential Analysis

Sell Product F (Alt. 1) or Process Further into Product G (Alt. 2)

November 15

*

CHAPTER 25 Differential Analysis, Product Pricing, and Activity-Based Costing

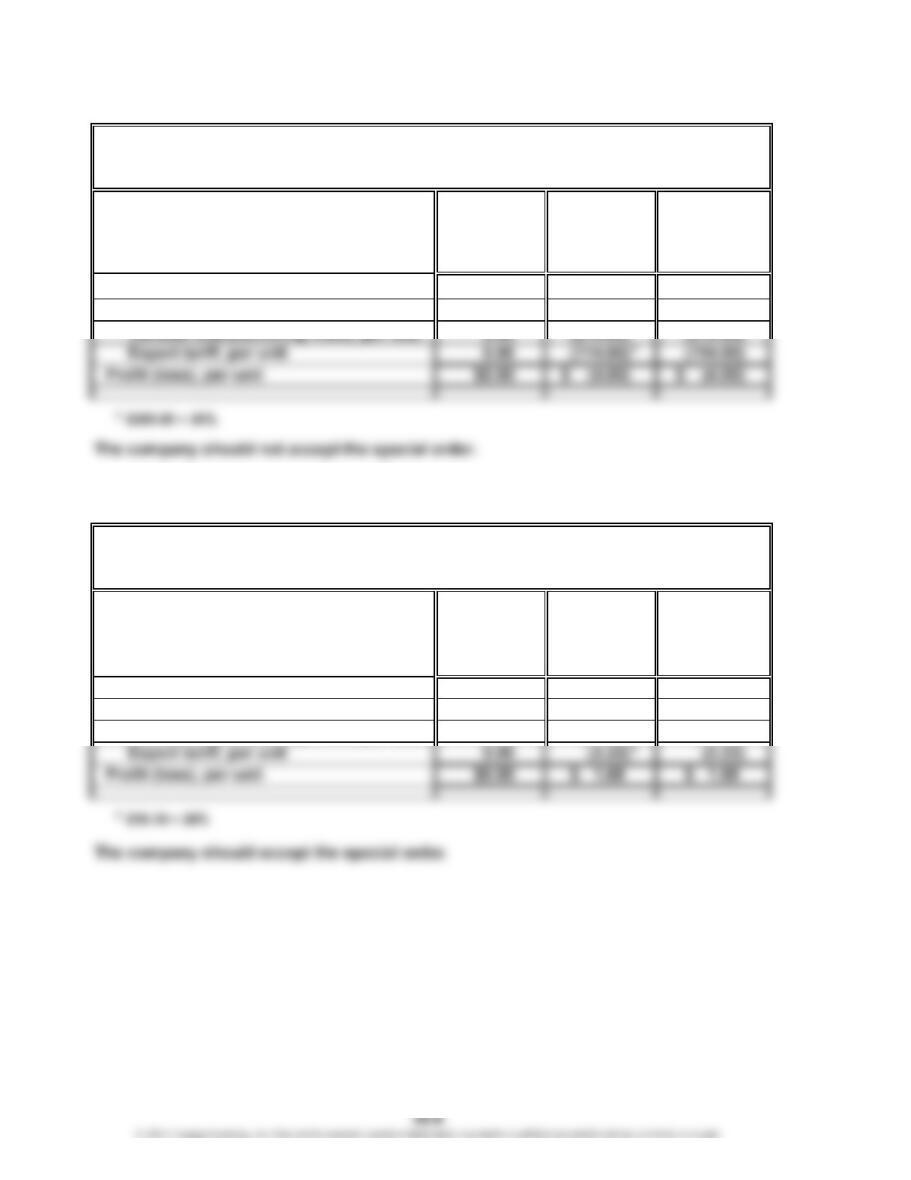

PE 25-6A

Reject Accept Differential

Order Order Effects

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues, per unit $0.00 $ 380.00 $ 380.00

Costs:

PE 25-6B

Reject Accept Differential

Order Order Effects

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues, per unit $0.00 $ 16.10 $ 16.10

Costs:

Variable manufacturing costs, per unit 0.00 (11.20) (11.20)

Differential Analysis

Reject Order (Alt. 1) or Accept Order (Alt. 2)

March 16

Differential Analysis

Reject Order (Alt. 1) or Accept Order (Alt. 2)

March 5

CHAPTER 25 Differential Analysis, Product Pricing, and Activity-Based Costing

PE 25-7A

PE 25-7B

$75 + $90

$220

PE 25-8A

Product R Product S

…

…

PE 25-8B

Product K Product L

Unit contribution margin……………………………………………

…

$360 $300

÷

Furnace hours per unit……………………………………………

…

5 4

Unit contribution margin per production bottleneck hour……

…

$72 $75

Product L is the most profitable in using bottleneck resources.

Markup percentage on product cost: Desired Profit + Selling and Admin. Exp.

Total Product Cost

= 75%

CHAPTER 25 Differential Analysis, Product Pricing, and Activity-Based Costing

PE 25-9A

a. Fabrication: $825,000 ÷ 3,000 direct labor hours = $275 per dlh

Assembly: $270,000 ÷ 3,000 direct labor hours = $90 per dlh

Setup: $536,000 ÷ 160 setups = $3,350 per setup

Inspection: $424,000 ÷ 800 inspections = $530 per inspection

b.

Activity Activity

Activity Cost Cost

Fabrication 1,200 dlh /dlh 1,800 dlh /dlh

Assembly 1,800 dlh /dlh 1,200 dlh /dlh

Speedboat

Activity-

Base

Usage

Activity Base

Usage

Bass Boat

×= ×=Rate

Activity

Rate

Activity-

$275

$90

$ 330,000

162,000

$275 $ 495,000

$90 108,000

CHAPTER 25 Differential Analysis, Product Pricing, and Activity-Based Costing

PE 25-9B

a. Cutting: $81,000 ÷ 1,500 direct labor hours = $54 per dlh

Sewing: $25,500 ÷ 1,500 direct labor hours = $17 per dlh

Setup: $60,000 ÷ 1,000 setups = $60 per setup

Inspection: $37,500 ÷ 500 inspections = $75 per inspection

b.

Activity Activity

Activity Cost Cost

Cutting 500 dlh /dlh 1,000 dlh /dlh

Sewing 1,000 dlh /dlh 500 dlh /dlh

$ 54,000

Activity

Rate×

$54$54

$17

Activity Base

×

17,000

$17 8,500

Activity-

Jeans

Activity-

Base

Usage

Khakis

==Rate Usage

$27,000

CHAPTER 25 Differential Analysis, Product Pricing, and Activity-Based Costing

Ex. 25-1

a.

Lease Sell Differential

Machinery Machinery Effects

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues $125,000 $102,000 $(23,000)

Ex. 25-2

Note to Instructors: This differential analysis is a lease-or-buy decision, which is from

the user perspective. A lease-or-sell decision is from the perspective of the equipment

owner. Thus, the analysis is similar to the text examples but must be set up from the

user’s, rather than the owner’s, perspective.

Lease Buy Differential

Equipment Equipment Effects

(Alternative 1) (Alternative 2) (Alternative 2)

Unit costs:

Purchase price $ 0 $ (95,000) $ (95,000)

Freight and installation 0 (4,500) (4,500)

Repair and maintenance (4 years) 0 (14,400) (14,400)

EXERCISES

Differential Analysis

Lease Equipment (Alt. 1) or Buy Equipment (Alt. 2)

Decembe

r

11

Differential Analysis

Lease Machinery (Alt. 1) or Sell Machinery (Alt. 2)

May 25

1

CHAPTER 25 Differential Analysis, Product Pricing, and Activity-Based Costing

Ex. 25-3

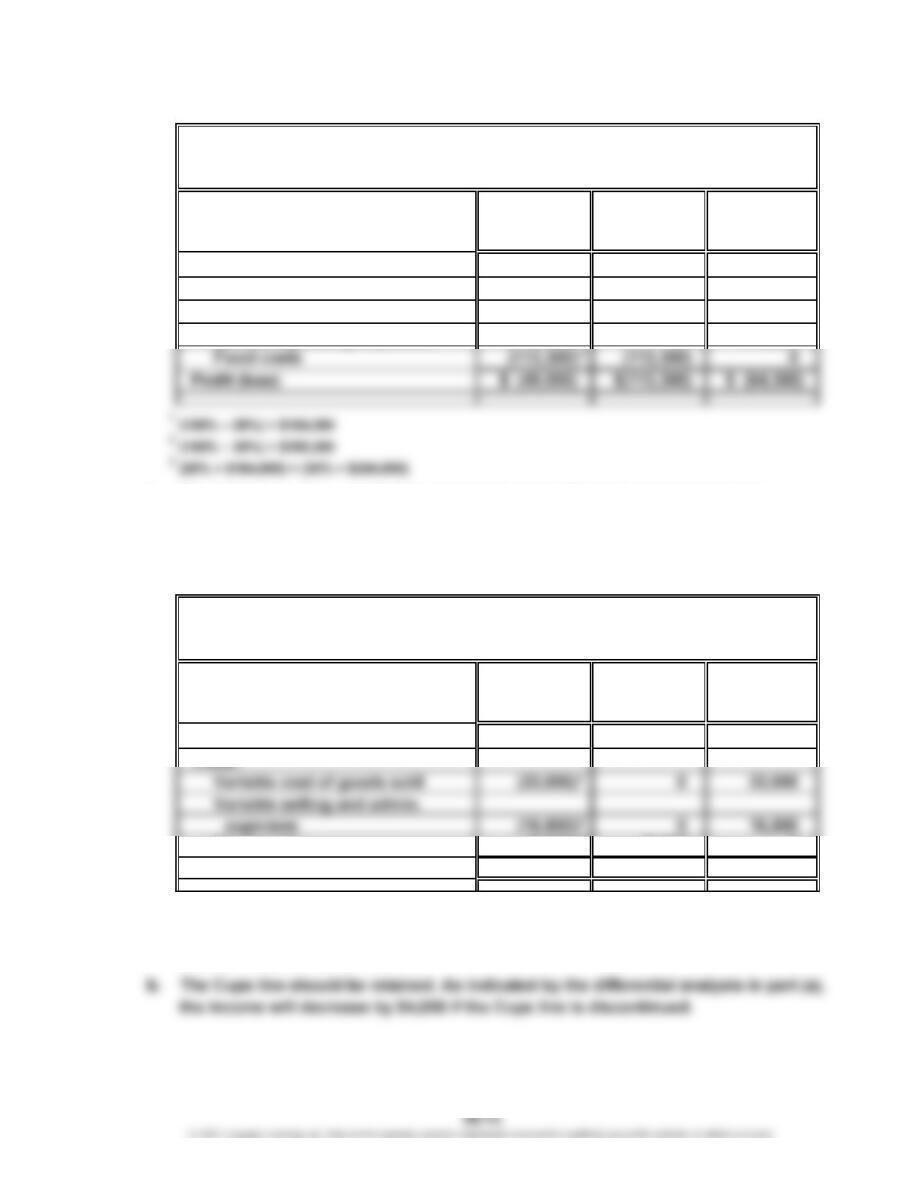

a.

Continue Discontinue Differential

Star Cola Star Cola Effects

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues $ 390,000 $ 0 $(390,000)

Costs:

Variable cost of goods sold (147,200) 0 147,200

Variable operating expenses (178,500) 0 178,500

b. Star Cola should be retained. As indicated by the differential analysis in part

(a), the income would decrease by $64,300 if the product was discontinued.

Ex. 25-4

a.

Continue Discontinue Differential

Cups Cups Effects

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues $ 43,500 $ 0 $(43,500)

Fixed costs (9,605) (9,605) 0

Profit (loss) $ (5,600) $(9,605) $ (4,005)

1

$26,700 × (100% – 15%)

2

$22,400 × (100% – 25%)

3

($26,700 × 15%) + ($22,400 × 25%)

For the Month Ended May 31

Differential Analysis

Continue Star Cola (Alt. 1) or Discontinue Star Cola (Alt. 2)

January 21

Differential Analysis

Continue Cups (Alt. 1) or Discontinue Cups (Alt. 2)

1

2

3

CHAPTER 25 Differential Analysis, Product Pricing, and Activity-Based Costing

Ex. 25-5

Note to Instructors: Many students may be unfamiliar with the financial services

industry. This exercise provides an opportunity to introduce students to some

basic terms and concepts used in the industry.

b. Variable costs in the Investor Services segment include:

1. Commissions to brokers

2. Fees paid to exchanges for executing trades

3. Transaction fees incurred by Schwab mutual funds to purchase and sell

shares

4. Advertising

c. Investor Advisor

Services Services

(in millions) (in millions)

Income from operations……………………………………

…

$3,176 $1,386

Plus depreciation……………………………………………… 186 120

Estimated contribution margin……………………………

…

$3,362 $1,506

d. If one assumes that the fixed costs that serve the Advisor Services business

CHAPTER 25 Differential Analysis, Product Pricing, and Activity-Based Costing

Ex. 25-6

The flaw in the decision is the failure to focus on the differential revenues and

costs, which indicate that operating income would be reduced by $39,000 if

Children’s Shoes were discontinued. This differential income from sales of

Children’s Shoes can be determined from the following differential analysis:

Continue Discontinue

Children’s Children’s Differential

Shoes Shoes Effects

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues $ 165,000 $ 0 $(165,000)

* $32,000 + $17,000

Ex. 25-7

a.

Make Buy

Carrying Carrying Differential

Case Case Effects

(Alternative 1) (Alternative 2) (Alternative 2)

Unit costs:

Purchase price $ 0.00 $(89.00) $(89.00)

1

$26.00 × 15%

2

$10.40 – $3.90

b. Assuming that there were no better alternative uses for the spare capacity, it would

be advisable to manufacture the carrying cases because the cost savings would

Differential Analysis

Make Carrying Case (Alt. 1) or Buy Carrying Case (Alt. 2)

February 24

Differential Analysis

Continue Children’s Shoes (Alt. 1) or Discontinue Children’s Shoes (Alt. 2)

CHAPTER 25 Differential Analysis, Product Pricing, and Activity-Based Costing

Ex. 25-8

a.

Lay Out Purchase

Pages Layout Differential

Internally Services Effects

(Alternative 1) (Alternative 2) (Alternative 2)

Unit costs:

Purchase price of layout work $ 0 $(312,000) $(312,000)

Salaries (224,000) 0 224,000

Benefits (36,000) 0 36,000

Supplies (21,000) 0 21,000

*

24,000 pages × $13 per page

b. The benefit from using an outside service is shown to be $8,000 greater

than performing the layout work internally. The fixed costs (depreciation

expenses) in the budget are irrelevant to the decision. Thus, the work should

be purchased from the outside on a strictly financial basis.

c. Before electing to lay off the five employees, the guild should consider

Differential Analysis

Lay Out Pages Internally (Alt. 1) or Purchase Layout Services (Alt. 2)

February 22

*

CHAPTER 25 Differential Analysis, Product Pricing, and Activity-Based Costing

Ex. 25-9

a.

Continue Replace

with Old Old Differential

Machine Machine Effects

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues:

Proceeds from sale of old

machine $ 0 $ 90,100 $ 90,100

1

$11,200 × 8 years

2

$8,000 × 8 years

The company should replace the old machine.

Differential Analysis

Continue with Old Machine (Alt. 1) or Replace Old Machine (Alt. 2)

April 29

CHAPTER 25 Differential Analysis, Product Pricing, and Activity-Based Costing

Ex. 25-10

a.

Continue Replace

with Old Old Differential

Machine Machine Effects

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues:

Sales (5 years)* $1,025,000 $1,025,000 $ 0

Costs:

Purchase price 0 (180,000) (180,000)

Direct materials (5 years)* (360,000) (360,000) 0

Direct labor (5 years)* (255,000) 0 255,000

*

Each annual revenue and cost is multiplied by 5 years.

b. The proposal should not be accepted.

c. In addition to the factors given, consideration should be given to factors such as

Differential Analysis

Continue with Old Machine (Alt. 1) or Replace Old Machine (Alt. 2)

May 4

CHAPTER 25 Differential Analysis, Product Pricing, and Activity-Based Costing

Ex. 25-11

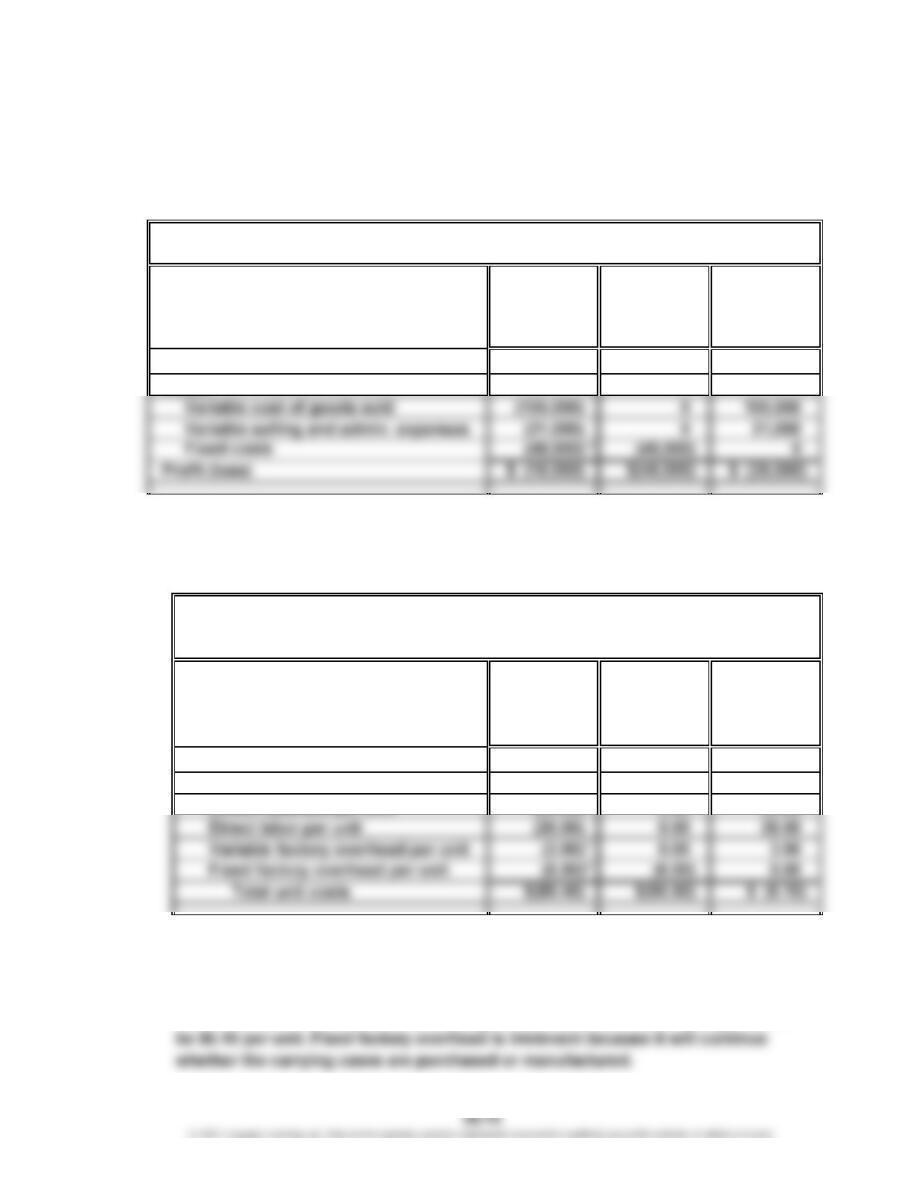

Process

Sell Further into Differential

Rough Cut Finished Cut Effects

(Alternative 1) (Alternative 2) (Alternative 2)

Ex. 25-12

a.

Process

Sell Further into

Regular Decaf Differential

Columbian Columbian Effects

(Alternative 1) (Alternative 2) (Alternative 2)

b. The differential revenue from processing further to Decaf Columbian is more

than the differential cost of selling regular by $2,166. Thus, Rise N’ Shine

Coffee Company should process further to Decaf Columbian.

Sell Regular Columbian (Alt. 1) or Process Further into Decaf Columbian (Alt. 2)

October 6

Differential Analysis

Sell Rough Cut (Alt. 1) or Process Further into Finished Cut (Alt. 2)

August 9

Differential Analysis

12

CHAPTER 25 Differential Analysis, Product Pricing, and Activity-Based Costing

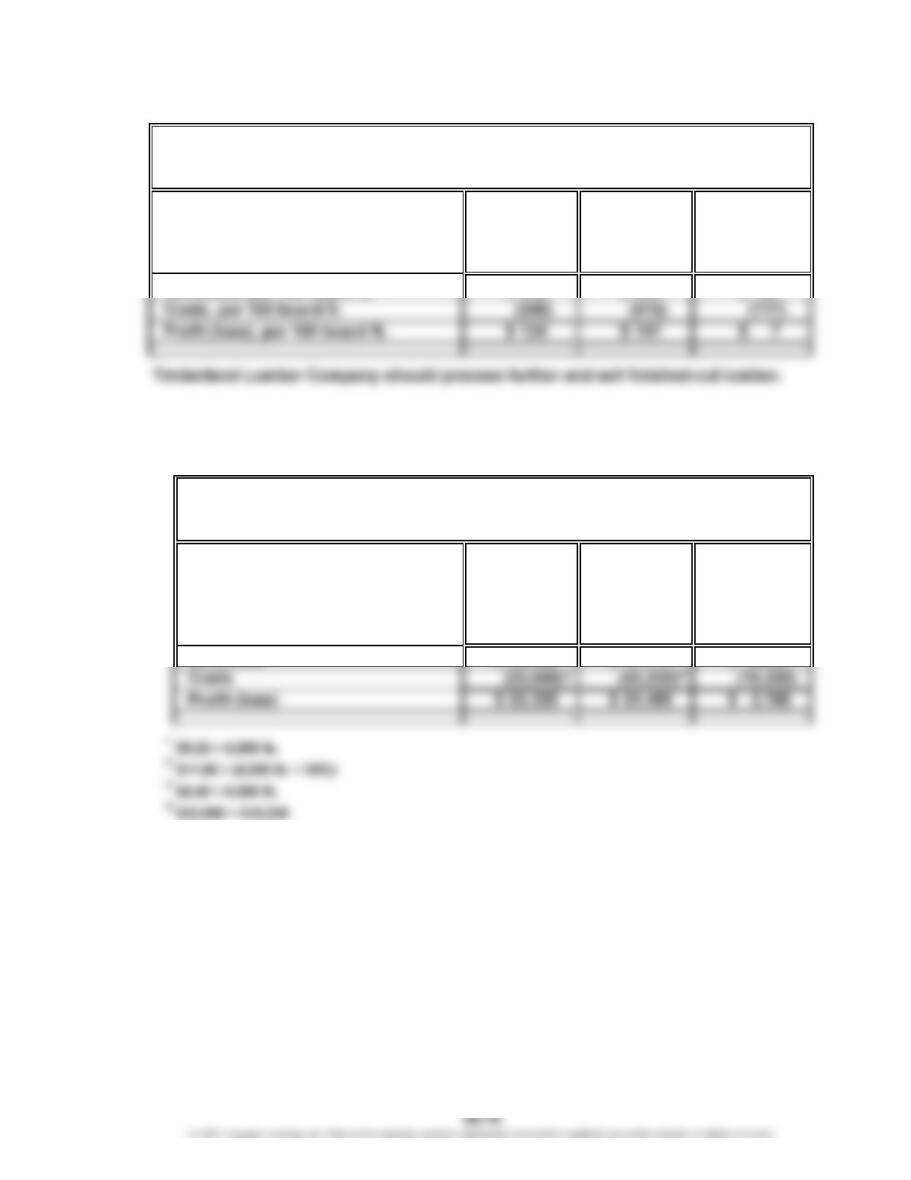

Ex. 25-12 (Concluded)

c. The price of Decaf Columbian would need to decrease to $11.50 per pound in order

for the differential analysis to yield neither an advantage nor a disadvantage

The price of Decaf Columbian would need to be $0.38 lower, or $11.50, to yield no

net differential income or loss. This is verified by the following differential analysis:

Sell

Regular Differential

Columbian Effects

(Alternative 1) (Alternative 2)

Further into

Process

October 6

Differential Analysis

Sell Regular Columbian (Alt. 1) or Process Further into Decaf Columbian (Alt. 2)

(Alternative 2)

Decaf Columbian