Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 25

Short-Term Business Decisions

Review Questions

1. List the four steps in short-term decision making. At which step are managerial accountants most

involved?

The four steps in short-term decision making are: (1) Define business goals; (2) Identify alternative

2. What makes information relevant to decision making?

3. What makes information irrelevant to decision making?

4. What are sunk costs? Give an example.

5. When is nonfinancial information relevant?

6. What is differential analysis?

7. What are the two keys in short-term decision making?

The two keys in short-term decision making are (1) focusing on relevant revenues, costs, and profits,

8. What questions should managers answer when setting regular prices?

The three questions managers should answer when setting regular prices are:

9. Explain the difference between price-takers and price-setters.

A company is a price-taker when it has little control over the prices of its products and services

10. What is target pricing? Who uses it?

11. What does the target full product cost include?

12. What is cost-plus pricing? Who uses it?

13. What questions should managers answer when considering special pricing orders?

Managers should answer the following three questions when considering special pricing orders:

14. When completing a differential analysis, when are the differences shown as positive amounts? As

negative amounts?

15. When should special pricing orders be accepted?

16. What questions should managers answer when considering dropping a product or segment?

Some of the questions managers must consider when deciding whether to drop a product or a

business segment, include the following:

• Does the product or segment provide a positive contribution margin?

• Will fixed costs continue to exist, even if the company drops the product or segment?

17. Explain why a segment with an operating loss can cause the company to have a decrease in total

operating income if the segment is dropped.

18. What is a constraint?

19. What questions should managers answer when facing constraints?

Managers should answer the following questions when facing constraints:

20. What is the decision rule concerning products to emphasize when facing a constraint?

21. What is the most common constraint faced by merchandisers?

22. What is outsourcing?

23. What questions should managers answer when considering outsourcing?

24. What questions should managers answer when considering selling a product as is or processing

further?

25. What are joint costs? How do they affect the sell or process further decision?

26. What is the decision rule for selling a product as is or processing it further?

Short Exercises

S25-1 Describing and identifying information relevant to business decisions

Learning Objective 1

You are trying to decide whether to trade in your inkjet printer for a more recent model. Your usage

pattern will remain unchanged, but the old and new printers use different ink cartridges.

Indicate if the following items are relevant or irrelevant to your decision:

a. The price of the new printer

b. The price paid for the old printer

c. The trade-in value of the old printer

d. Paper cost

e. The difference between ink cartridges’ costs

SOLUTION

(a)

relevant

S25-2 Making pricing decisions

Learning Objective 2

Mountain Run operates a Rocky Mountain ski resort. The company is planning its lift ticket pricing for

the coming ski season. Investors would like to earn a 12% return on investment on the company’s

$111,000,000 of assets. The company primarily incurs fixed costs to groom the runs and operate the

lifts. Mountain Run projects fixed costs to be $37,000,000 for the ski season. The resort serves about

680,000 skiers and snowboarders each season. Variable costs are about $8 per guest. Currently, the

resort has such a favorable reputation among skiers and snowboarders that it has some control over the

lift ticket prices.

Requirements

1. Would Mountain Run emphasize target pricing or cost-plus pricing? Why?

2. If other resorts in the area charge $80 per day, what price should Mountain Run charge?

SOLUTION

Requirement 1

Mountain Run would emphasize cost-plus pricing because it is a price-setter. Mountain Run would be

Requirement 2

Current variable costs

($8 per guest × 680,000 guests)

$ 5,440,000

Plus: Fixed costs

37,000,000

Note: Short Exercise S25-2 must be completed before attempting Short Exercise S25-3.

S25-3 Making pricing decisions

Learning Objective 2

Refer to details about Mountain Run from Short Exercise S25-2. Assume that Mountain Run’s

reputation has diminished and other resorts in the vicinity are charging only $80 per lift ticket. Mountain

Run has become a price-taker and will not be able to charge more than its competitors. At the market

price, Mountain Run managers believe they will still serve 680,000 skiers and snowboarders each

season.

Requirements

1. If Mountain Run cannot reduce its costs, what profit will it earn? State your answer in dollars and as

a percent of assets. Will investors be happy with the profit level?

2. Assume Mountain Run has found ways to cut its fixed costs to $36,320,000. What is its new target

variable cost per skier/snowboarder?

SOLUTION

Requirement 1

Revenues

(680,000 guests @ $80 per lift ticket)

$ 54,400,000

Less: Costs

[37,000,000 + ($8 per guest × 680,000 guests)]

42,440,000

Profits

11,960,000

Requirement 2

Revenue at market price

(calculated above)

$ 54,400,000

Less: Desired profit

(12% × $111,000,000 assets)

13,320,000

Target full product cost

41,080,000

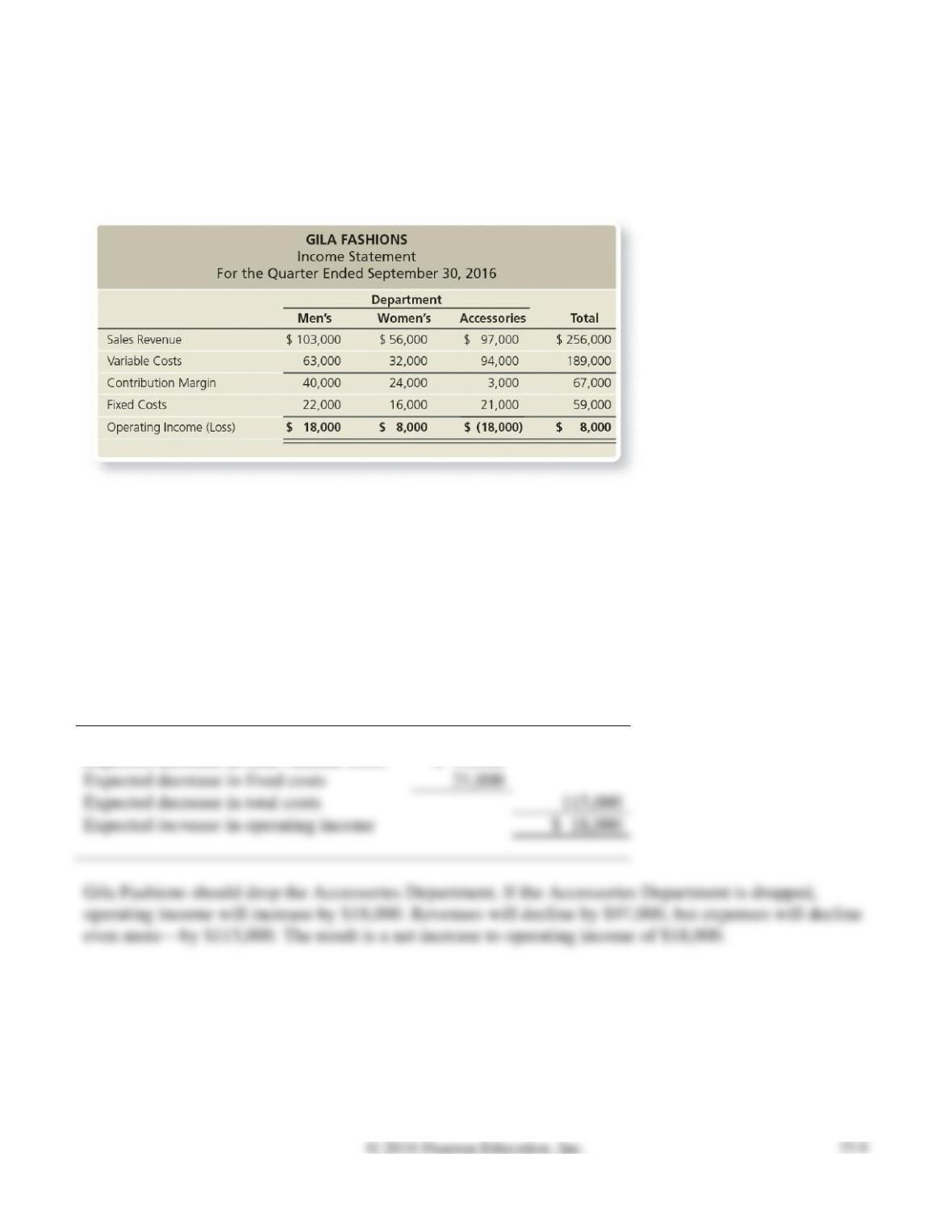

S25-4 Making dropping a product or segment decisions

Learning Objective 3

Gila Fashions operates three departments: Men’s, Women’s, and Accessories. Departmental operating

income data for the third quarter of 2016 are as follows:

Assume that the fixed costs assigned to each department include only direct fixed costs of the

department:

• Salary of the department’s manager

• Cost of advertising directly related to that department

If Gila Fashions drops a department, it will not incur these fixed costs. Under these circumstances,

should Gila Fashions drop any of the departments? Give your reasoning.

SOLUTION

Accessories Department:

Expected decrease in revenue

$ (97,000)

Expected decrease in total variable costs

$ 94,000

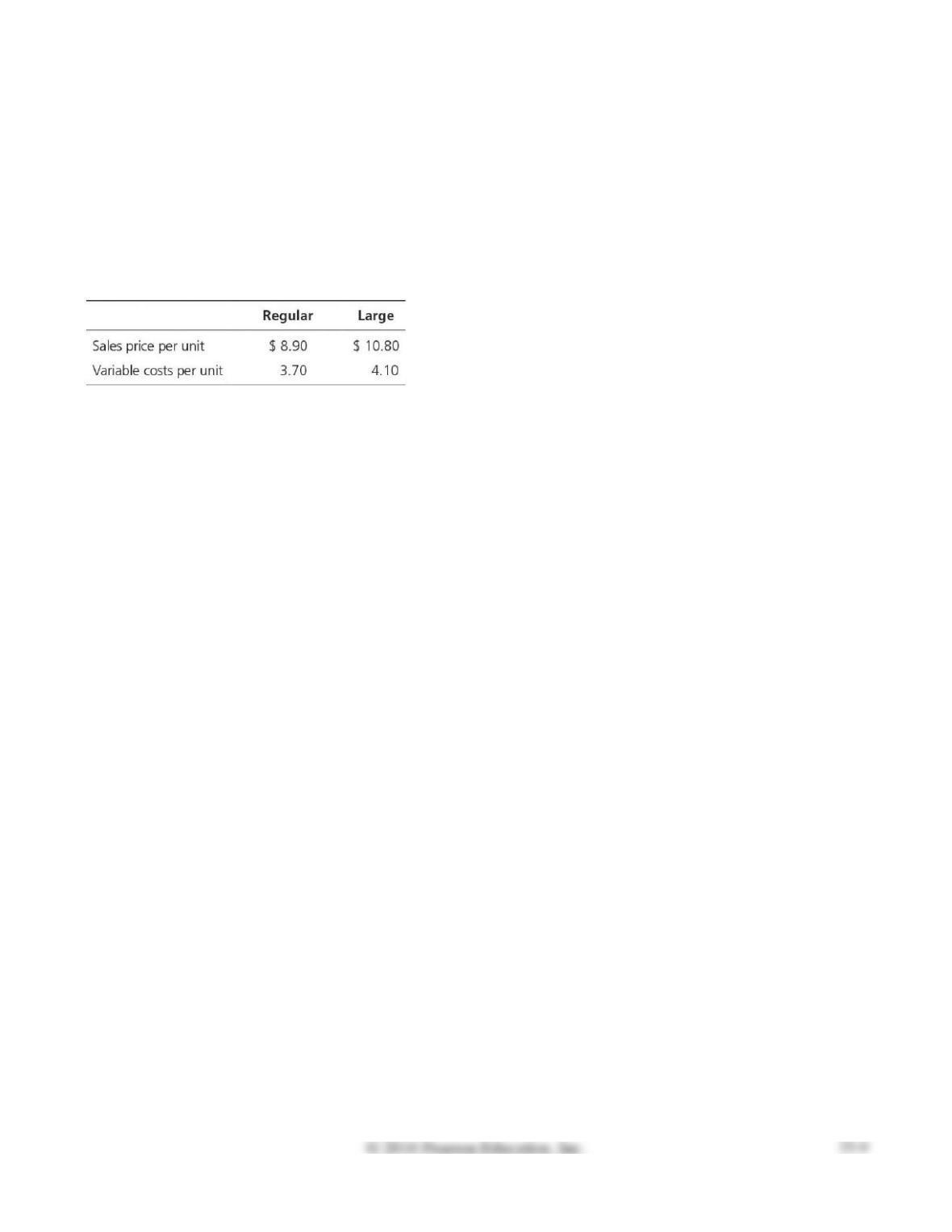

S25-5 Making product mix decisions

Learning Objective 3

ContainAll produces plastic storage bins for household storage needs. The company makes two sizes of

bins: large (50 gallon) and regular (35 gallon). Demand for the products is so high that ContainAll can

sell as many of each size as it can produce. The company uses the same machinery to produce both

sizes. The machinery can be run for only 2,800 hours per period. ContainAll can produce 11 large bins

every hour, whereas it can produce 17 regular bins in the same amount of time. Fixed costs amount to

$130,000 per period. Sales prices and variable costs are as follows:

Requirements

1. Which product should ContainAll emphasize? Why?

2. To maximize profits, how many of each size bin should ContainAll produce?

3. Given this product mix, what will the company’s operating income be?

SOLUTION

Requirement 1

Contribution Margin per Product:

Regular

Bin

Large

Bin

Sales price per bin

$ 8.90

$ 10.80

Contribution Margin per Machine Hour:

Regular

Bin

Large

Bin

(1) Bins produced per hour

17

11

When facing a constraint concerning which products to emphasize, the decision rule is to emphasize the

Requirement 2

Requirement 3

Regular

Bins

Sales Revenue

(47,600 bins × $8.90 per bin)

$ 423,640

S25-6 Making outsourcing decisions

Learning Objective 4

Suppose Brady House restaurant is considering whether to (1) bake bread for its restaurant in-house or

(2) buy the bread from a local bakery. The chef estimates that variable costs of making each loaf include

$0.54 of ingredients, $0.25 of variable overhead (electricity to run the oven), and $0.72 of direct labor

for kneading and forming the loaves. Allocating fixed overhead (depreciation on the kitchen equipment

and building) based on direct labor, Brady House assigns $1.05 of fixed overhead per loaf. None of the

fixed costs are avoidable. The local bakery would charge $1.70 per loaf.

Requirements

1. What is the full product unit cost of making the bread in-house?

2. Should Brady House bake the bread in-house or buy from the local bakery? Why?

3. In addition to the financial analysis, what else should Brady House consider when making this

decision?

SOLUTION

Requirement 1

Direct materials

$ 0.54

Direct labor

0.72

Requirement 2

Bread Costs

Make

Outsource

Difference

(Make – Outsource)

Variable costs:

Direct materials

$ 0.54

$ 0.54

Requirement 3

In addition to the financial analysis, Brady House should consider what else it could do with the freed

S25-7 Making outsourcing decisions

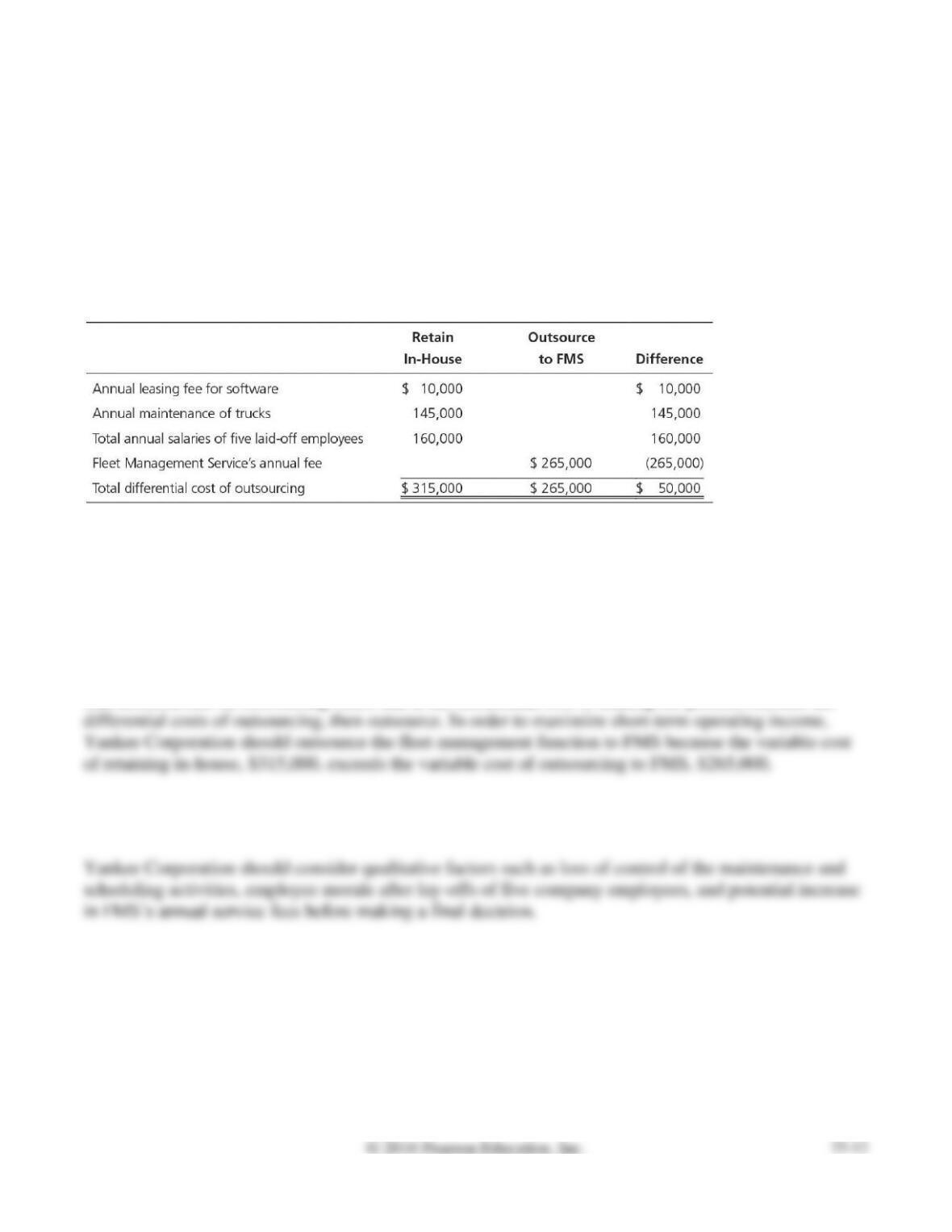

Learning Objective 4

Delila Nailey manages a fleet of 325 delivery trucks for Yankee Corporation. Nailey must decide

whether the company should outsource the fleet management function. If she outsources to Fleet

Management Services (FMS), FMS will be responsible for maintenance and scheduling activities. This

alternative would require Nailey to lay off her five employees. However, her own job would be secure;

she would be Yankee’s liaison with FMS. If she continues to manage the fleet, she will need fleet-

management software that costs $10,000 per year to lease. FMS offers to manage this fleet for an annual

fee of $265,000. Nailey performed the following analysis:

Requirements

1. Which alternative will maximize Yankee’s short-term operating income?

2. What qualitative factors should Yankee consider before making a final decision?

SOLUTION

Requirement 1

The decision rule on outsourcing states that if the differential cost of making the product exceeds the

Requirement 2

S25-8 Making sell or process further decisions

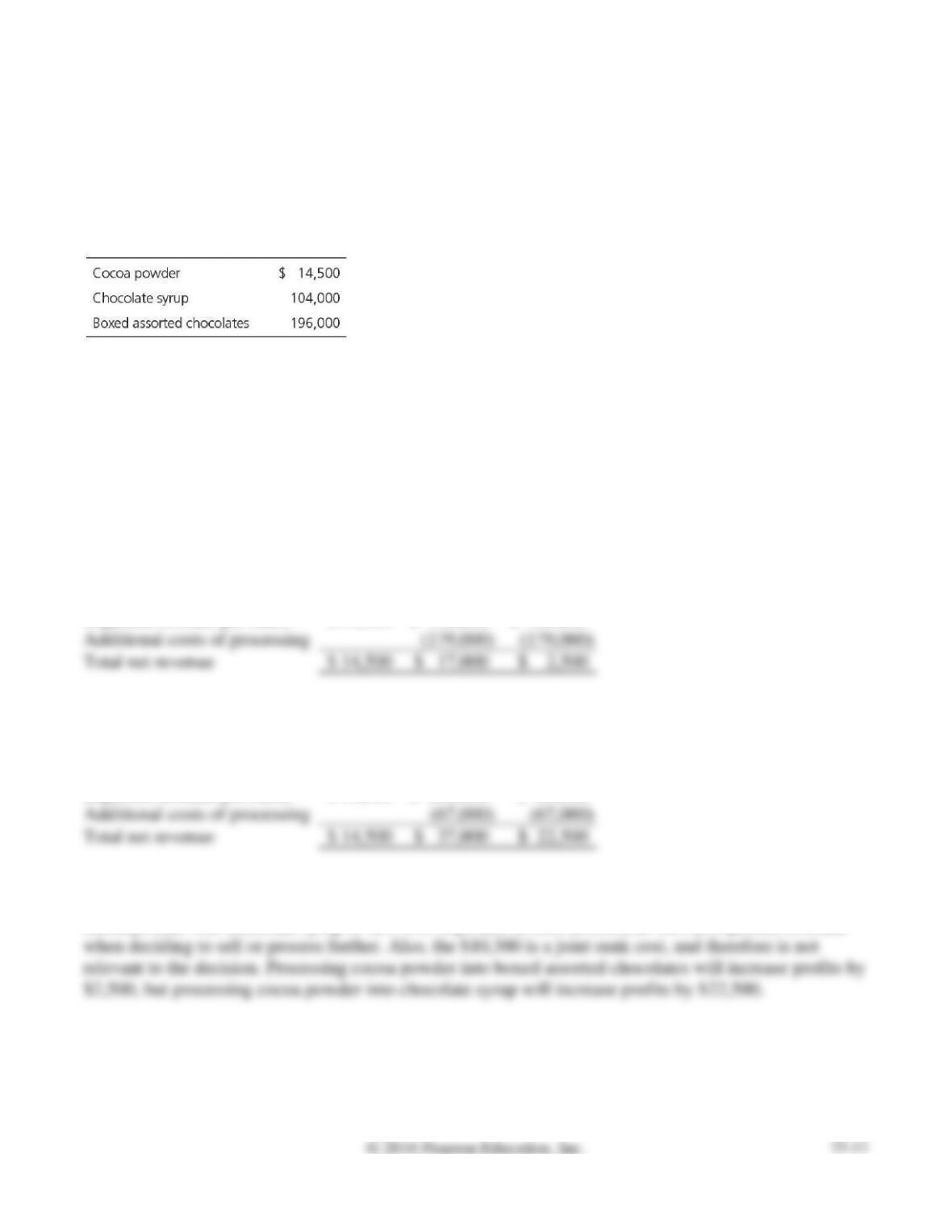

Learning Objective 4

Chocolicious processes cocoa beans into cocoa powder at a processing cost of $10,300 per batch.

Chocolicious can sell the cocoa powder as is, or it can process the cocoa powder further into either

chocolate syrup or boxed assorted chocolates. Once processed, each batch of cocoa beans would result

in the following sales revenue:

The cost of transforming the cocoa powder into chocolate syrup would be $67,000. Likewise, the

company would incur a cost of $179,000 to transform the cocoa powder into boxed assorted chocolates.

The company president has decided to make boxed assorted chocolates due to their high sales value and

to the fact that the cocoa bean processing cost of $10,300 eats up most of the cocoa powder profits.

Has the president made the right or wrong decision? Explain your answer. Be sure to include the

correct financial analysis in your response.

SOLUTION

Process into boxed assorted chocolates:

Costs

Sell

Process

Further

Difference

Expected revenue per batch

$ 14,500

$ 196,000

$ 181,500

Process into chocolate syrup:

Costs

Sell

Process

Further

Difference

Expected revenue per batch

$ 14,500

$ 104,000

$ 89,500

The President of Chocolicious has not made the best decision. The best decision would be to process the

cocoa powder into chocolate syrup to sell. It is important to look at costs, as well as expected revenue,

Exercises

E25-9 Describing and identifying information relevant to business decisions

Learning Objective 1

Dan Jacobs, production manager for GreenLife, invested in computer-controlled production machinery

last year. He purchased the machinery from Superior Design at a cost of $3,000,000. A representative

from Superior Design has recently contacted Dan because the company has designed an even more

efficient piece of machinery. The new design would double the production output of the year-old

machinery but would cost GreenLife another $4,500,000. Jacobs is afraid to bring this new equipment

to the company president’s attention because he convinced the president to invest $3,000,000 in the

machinery last year.

Explain what is relevant and irrelevant to Jacobs’s dilemma. What should he do?

SOLUTION

The cost and doubled production output of the new machine would be relevant information. The

E25-10 Making special pricing decisions

Learning Objective 2

1. $2,750

Suppose the Baseball Hall of Fame in Cooperstown, New York, has approached Hungry-Cardz with a

special order. The Hall of Fame wishes to purchase 55,000 baseball card packs for a special promotional

campaign and offers $0.33 per pack, a total of $18,150. Hungry-Cardz’s total production cost is $0.53

per pack, as follows:

Hungry-Cardz has enough excess capacity to handle the special order.

Requirements

1. Prepare a differential analysis to determine whether Hungry-Cardz should accept the special sales

order.

2. Now assume that the Hall of Fame wants special hologram baseball cards. Hungry- Cardz will spend

$5,000 to develop this hologram, which will be useless after the special order is completed. Should

Hungry-Cardz accept the special order under these circumstances, assuming no change in the special

pricing of $0.33 per pack?

SOLUTION

Requirement 1

Expected increase in revenue

(55,000 packs × $0.33 per pack)

$ 18,150

Requirement 2

Expected increase in revenue

(55,000 packs × $0.33 per pack)

$ 18,150

E25-11 Making special pricing decisions

Learning Objective 2

1. $475,000

Tolman Sunglasses sell for about $154 per pair. Suppose that the company incurs the following average

costs per pair:

*$2,250,000 Total fixed manufacturing overhead / 90,000 Pairs of sunglasses

Tolman has enough idle capacity to accept a one-time-only special order from Alaska Shades for 25,000

pairs of sunglasses at $83 per pair. Tolman will not incur any variable selling expenses for the order.

Requirements

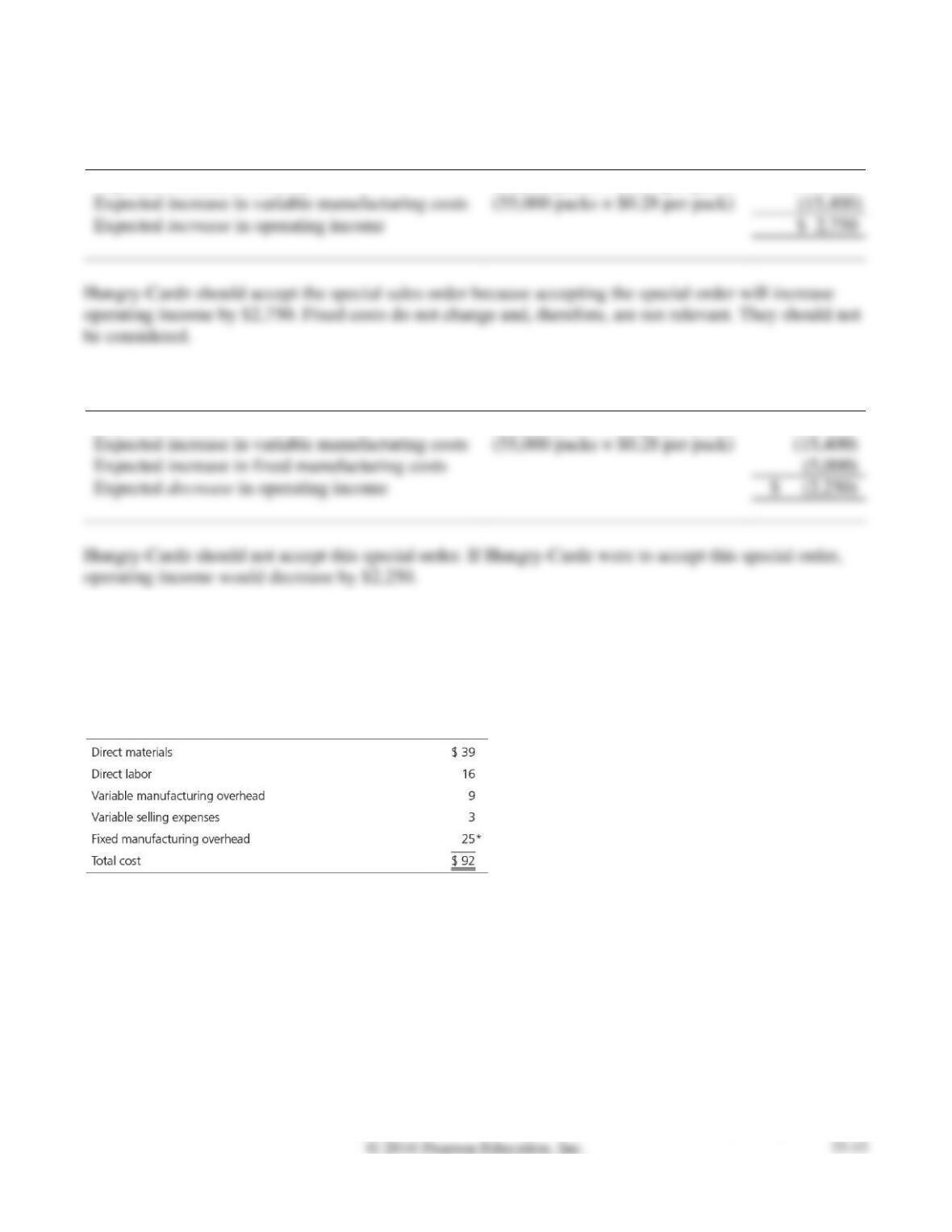

1. How would accepting the order affect Tolman’s operating income? In addition to the special order’s

effect on profits, what other (longer-term qualitative) factors should Tolman’s managers consider in

deciding whether to accept the order?

2. Tolman’s marketing manager, Peter Kyler, argues against accepting the special order because the

offer price of $83 is less than Tolman’s $92 cost to make the sunglasses. Kyler asks you, as one of

Tolman’s staff accountants, to explain whether his analysis is correct. What would you say?

SOLUTION

Requirement 1

Relevant variable costs:

Direct materials

$ 39

Direct labor

16

Requirement 2

As a staff accountant you need to explain that Peter Kyler’s analysis is not correct. The $92

E25-12 Making pricing decisions

Learning Objective 2

3. Desired profit $32,480

Rouse Builders builds 1,500-square-foot starter tract homes in the fast-growing suburbs of Atlanta. Land

and labor are cheap, and competition among developers is fierce. The homes are a standard model, with

any upgrades added by the buyer after the sale. Rouse Builders’s costs per developed sublot are as

follows:

Rouse Builders would like to earn a profit of 16% of the variable cost of each home sold. Similar homes

offered by competing builders sell for $202,000 each. Assume the company has no fixed costs.

Requirements

1. Which approach to pricing should Rouse Builders emphasize? Why?

2. Will Rouse Builders be able to achieve its target profit levels?

3. Bathrooms and kitchens are typically the most important selling features of a home. Rouse Builders

could differentiate the homes by upgrading the bathrooms and kitchens. The upgrades would cost

$22,000 per home but would enable Rouse Builders to increase the selling prices by $38,500 per

home. (Kitchen and bathroom upgrades typically add about 175% of their cost to the value of any

home.) If Rouse Builders makes the upgrades, what will the new cost-plus price per home be?

Should the company differentiate its product in this manner?

SOLUTION

Requirement 1

Requirement 2

Relevant variable costs:

Land

$ 51,000

Construction

121,000

Requirement 3

Upgraded variable costs per home

($181,000 original + $22,000 upgrades)

$ 203,000

Plus: Fixed costs

0

E25-13 Making dropping a product decisions

Learning Objective 3

1. $(33,000)

(Requirement 1 only)

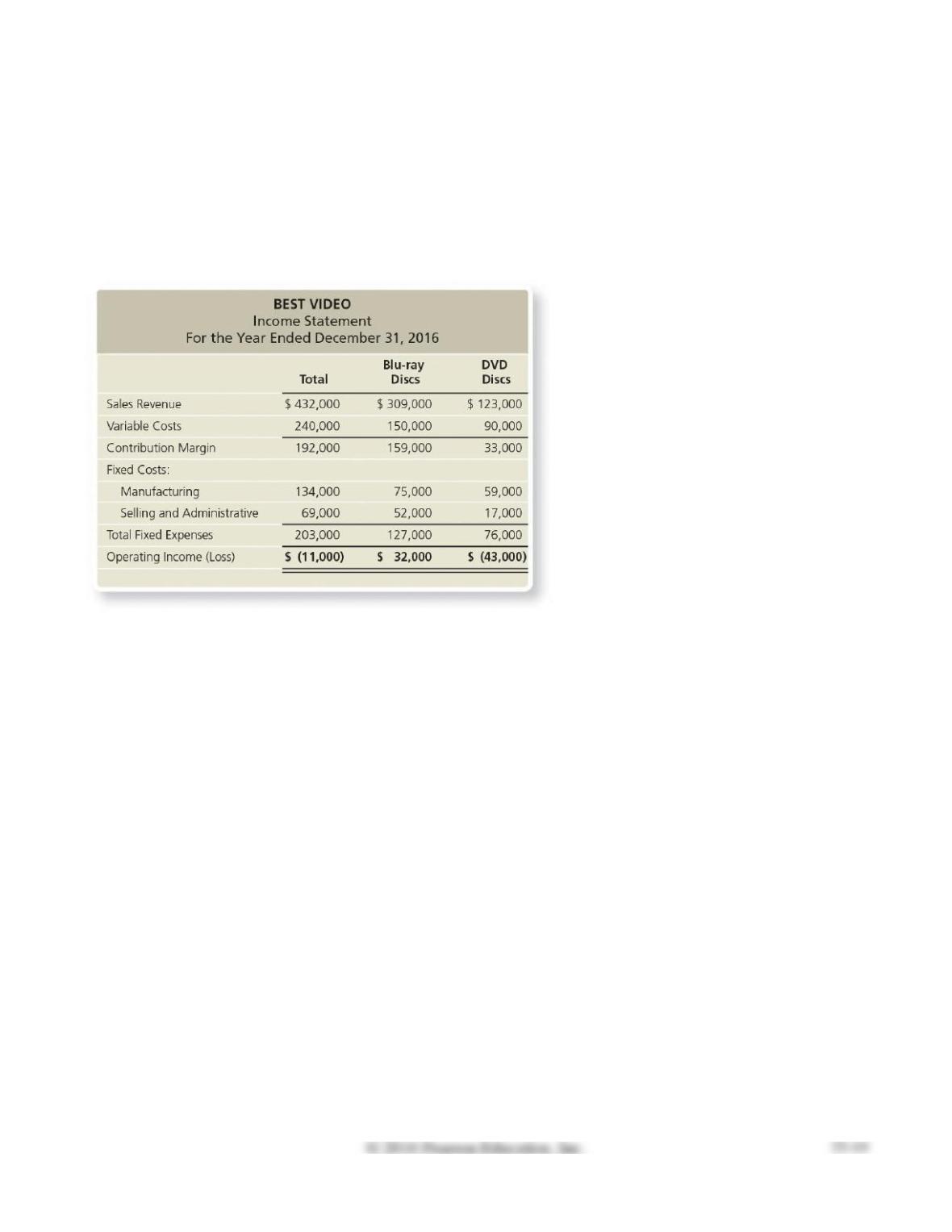

Top managers of Best Video are alarmed by their operating losses. They are considering dropping the

DVD product line. Company accountants have prepared the following analysis to help make this

decision:

Total fixed costs will not change if the company stops selling DVDs.

Requirements

1. Prepare a differential analysis to show whether Best Video should drop the DVD product line.

2. Will dropping DVDs add $43,000 to operating income? Explain.

SOLUTION

Requirement 1

Expected decrease in revenue

$ (123,000)

Requirement 2

Dropping the DVD product line will not add $43,000 to operating income. Dropping the DVD product

Note: Exercise E25-13 must be completed before attempting Exercise E25-14.

E25-14 Making dropping a product decisions

Learning Objective 3

1. $12,000

Refer to Exercise E25-13. Assume that Best Video can avoid $45,000 of fixed costs by dropping the

DVD product line (these costs are direct fixed costs of the DVD product line).

Prepare a differential analysis to show whether Best Video should stop selling DVDs.

SOLUTION

Expected decrease in revenue

$ (123,000)