g.

651,504

h.

498

140

To close overhead variances to Cost of Goods Sold.

Overhead Volume Variance (favorable)

Cost of Goods Sold

PROBLEM 24.4A

SVEN ENTERPRISES (concluded)

Overhead Spending Variance (favorable)

Entry to close overapplied overhead to cost of goods sold:

Entry to transfer the 147 batches of puppy meal produced in April to finished goods:

Finished Goods Inventory (at standard cost)

Work in Process Inventory (at standard cost)

To transfer 147 batches of puppy meal to finished goods in April.

a. =

b. =

$16 per hour × (3,750 hours* – 4,200 hours)

$4,200 Favorable

Standard Hourly Rate × (Standard Hours – Actual Hours)

-$7,200 (or $7,200 Unfavorable)

45 Minutes, Strong

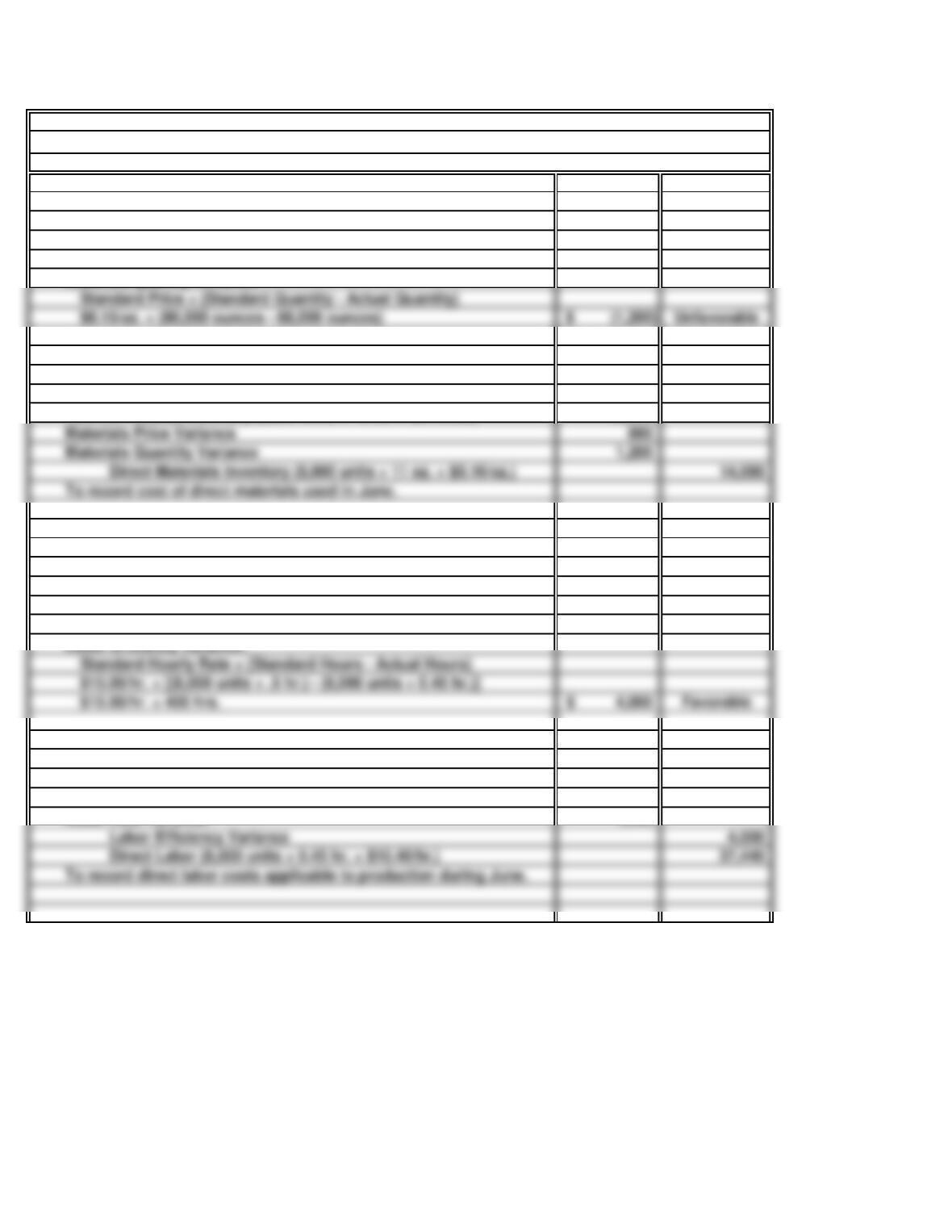

Materials Price Variance

PROBLEM 24.5A

SLICK CORPORATION

Actual Quantity Used × (Standard Price – Actual Price)

Labor Rate Variance

Actual Labor Hours × (Standard Rate – Actual Rate)

$1.30 per gallon × (16,250 gallons* – 16,500 gallons)

$825 Favorable

*Actual Price per Pound = $20,625 ÷ 16,500 gallons = $1.25/gallon

Standard Price × (Standard Quantity – Actual Quantity)

-$325 (or $325 Unfavorable)

*Standard Quantity Allowed = 5,000 cases × 3.25 gallons/case = 16,250 gallons

c.

$2,600

d. (1) 21,125 *

325

(2) 60,000 *

(3) 10,000

100

To apply overhead to production.

Manufacturing Overhead (at actual cost) ………………………………………

Overhead Spending Variance (favorable) ………………………………………

Overhead Volume Variance (unfavorable) ……………………………

Labor Rate Variance (favorable) ……………………………………………….

To record the cost of direct labor charged to production.

Work in Process Inventory (at standard cost) ………………….

*5,000 actual cases x 0.75 hours allowed per case x $16 per hour = $60,000

Direct Labor (at actual cost) ………………………………………………….

Labor Efficiency Variance (unfavorable) …………………………….

(4) 91,125

To close overhead variances to Cost of Goods Sold.

Cost of Goods Sold …………………………………………………….

Overhead Spending Variance (favorable) ……………………………….

Overhead Volume Variance (unfavorable) ……………………………

To transfer 5,000 cases to finished goods in May.

91,125*

Finished Goods Inventory (at standard cost) ………………………….

$2,200

Work in Process Inventory (at standard cost) ………………………………

To record the cost of direct materials charged to production.

Direct Materials Inventory (at actual cost) ………………………………………..

*5,000 actual cases x 3.25 gallons allowed per case x $1.30 per gallon = $21,125

Materials Price Variance (favorable) ……………………………………………….

Work in Process Inventory (at standard cost) ……………………………

Work in Process Inventory (at standard cost) …………………………

Materials Quantity Variance (unfavorable) ………………………..

Fixed

Fixed

Costs Applied

Overhead

Problem 24.5A

SLICK CORPORATION (concluded)

Overhead variances:

Actual Overhead

Costs Incurred

Standard Overhead

Costs Allowed

*Standard Variable Overhead Allowed = $1.50/case × 5,000 cases = $7,500

7,750

$9,950

40 Minutes, Strong PROBLEM 24.6A

POLYGLAZE, INC.

a. Materials price variance:

Actual Quantity × (Standard Price – Actual Price)

(8,000 units × 11 ounces) × ($0.15/oz. – $0.16/oz.) (880)$ Unfavorable

Materials quantity variance:

Journal entry to record direct materials used in June:

Work in Process Inventory (8,000 units × 10 oz. × $0.15/oz.) 12,000

b. Labor rate variance:

Actual Hours × (Standard Hourly Rate – Actual Hourly Rate)

(8,000 units × .45 hr.) × ($10.00/hr. – $10.40/hr.) (1,440)$ Unfavorable

Labor efficiency variance:

Journal entry to record direct labor cost for June:

Work in Process Inventory (8,000 units × 0.5 hr. × $10/hr.) 40,000

Labor Rate Variance 1,440

PROBLEM 24.6A

POLYGLAZE, INC. (concluded)

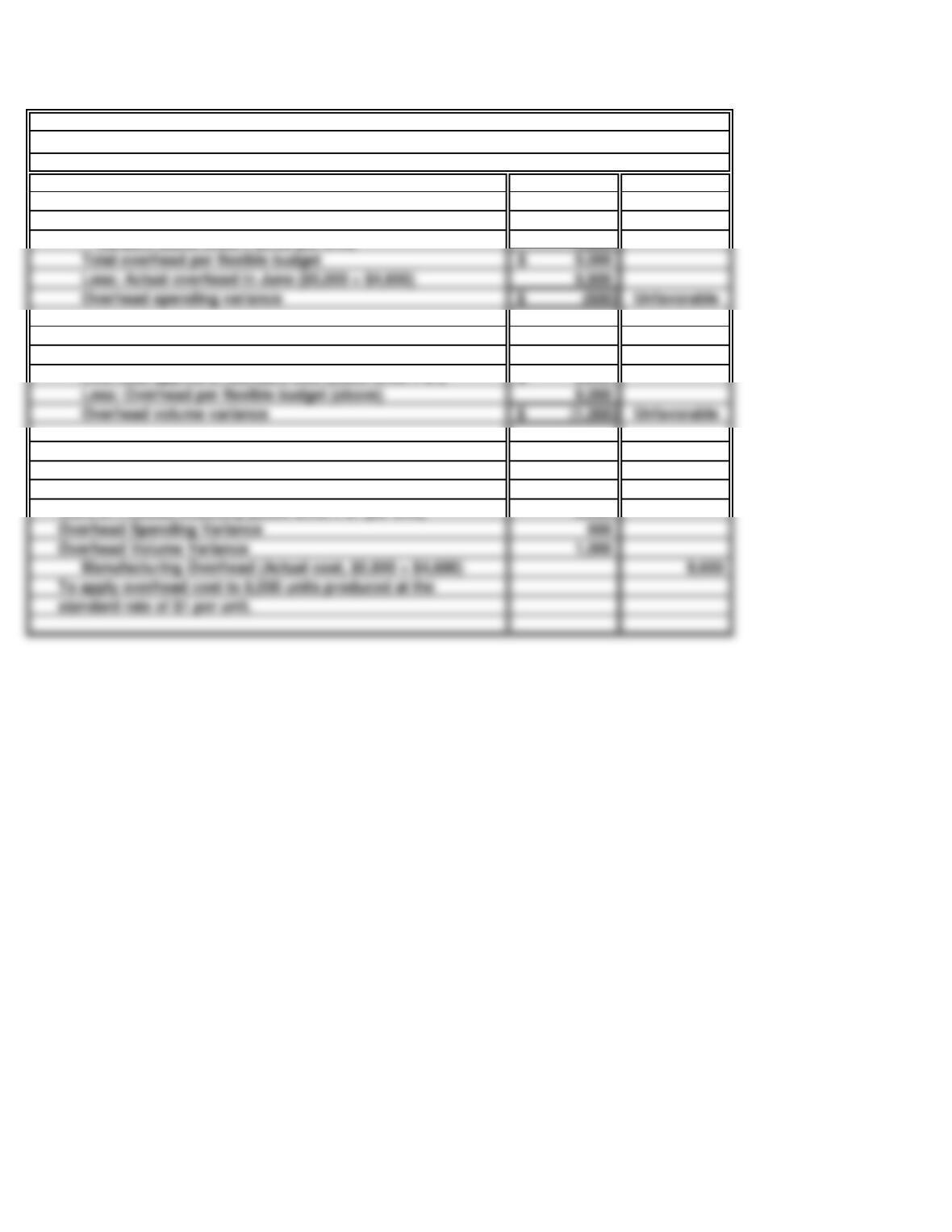

c. Overhead spending variance:

Overhead per flexible budget—8,000 units:

Fixed 5,000$

Variable (8,000 units × $0.50 per unit) 4,000

Overhead volume variance:

Overhead applied at standard cost (8,000 units × $1) 8,000$

Journal entry to record overhead applied to work in process:

Work in Process Inventory (8,000 units × $1 per unit) 8,000

PROBLEM 24.7A

HERITAGE FURNITURE CO.

a. (1)

(2)

$1.30/ft. × [(800 units × 100 ft.) – (88,000 ft.)]

$1.30/ft. × -8,000 ft.

-$10,400 (or $10,400 Unfavorable)

Standard Price × (Standard Quantity – Actual Quantity)

(3)

Actual Hours × (Standard Hourly Rate – Actual Hourly Rate)

(800 units × 5.5 hrs.) × ($8.00/hr. – $7.80/hr.)

4,400 hrs. × $0.20

$880 Favorable

(4)

Overhead variances are computed on the following page.

-$3,200 (or $3,200 Unfavorable)

Standard Hourly Rate × (Standard Hours – Actual Hours)

$8.00/hr. × [(800 units × 5 hrs.) – (800 units × 5.5 hrs.)]

$8.00/hr. × -400 hours

40 Minutes, Strong

Computation of materials price variance (MPV):

Computation of labor efficiency variance (LEV):

Computation of labor rate variance (LRV)

Computation of materials quantity variance (MQV):

Actual Quantity Used × (Standard Price – Actual Price)

(800 units × 110 ft.) × ($1.30/ft. – $1.20/ft.)

88,000 ft. × $0.10

$8,800 Favorable

PROBLEM 24.7A

HERITAGE FURNITURE CO. (continued)

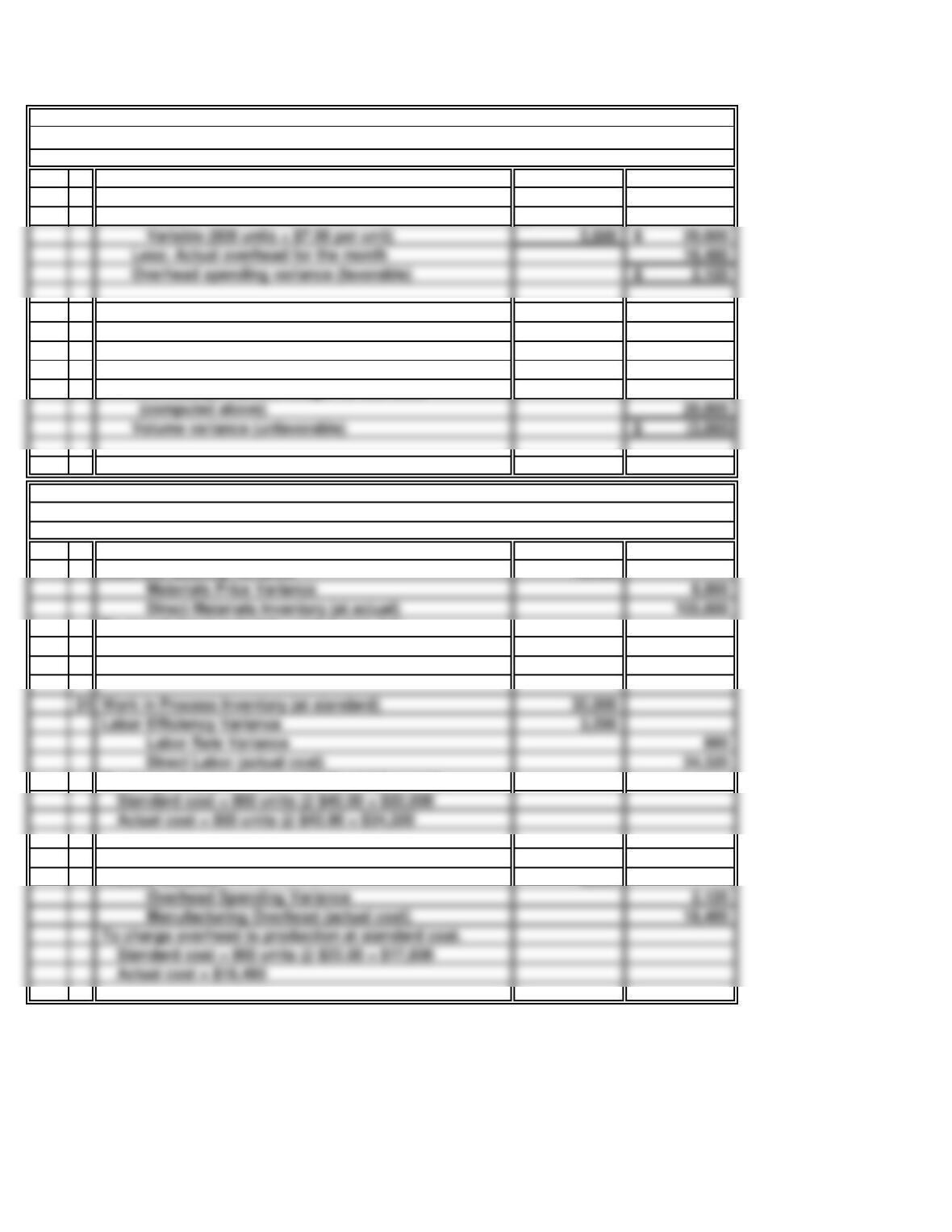

(5) Computation of overhead spending variance:

Overhead per flexible budget for 800 units:

Fixed 15,000$

(6) Computation of volume variance:

Overhead applied using standard cost

($800 units × $22 per unit) 17,600$

Overhead per flexible budget for 800 units

b.

General Journal

July 31 Work in Process Inventory (at standard) 104,000

Materials Quantity Variance 10,400

To record direct materials used during July.

Standard cost = 800 units @ $130 = $104,000

Actual cost = 800 units @ $132 = $105,600

To charge July production with direct labor cost.

31 Work in Process Inventory (at standard) 17,600

Volume Variance 3,000

PROBLEM 24.7A

HERITAGE FURNITURE CO. (concluded)

c.

The company appears to be having significant problems in two areas. First, the large

unfavorable materials quantity variance ($10,400) indicates that far more material is being

used in the production process than is provided for in the cost standards. Assuming that

The favorable materials price variance may mean that the purchasing department is

purchasing lower-grade materials than normal and perhaps contributing to the large

Comments on cost variances:

a.

b.

c.

d.

60 Minutes, Strong

PROBLEM 24.8A

RIPLEY COPRORATION

Based on the journal entry to charge direct material costs to work in process, the standard

quantity of material allowed for the actual level of output achieved in June is determined as

follows:

Based on the journal entry to charge direct materials costs to work in process, the actual

quantity of material purchased and used during June is determined as follows:

Based on the journal entry to charge direct labor costs to work in process, the standard direct

labor hours allowed during June is determined as follows:

Based on the journal entry to charge direct labor costs to work in process, the average per

hour labor cost incurred in June is determined as follows:

e.

f. 154,000

g. 5,000

8,200

1,200

4,500

2,000

4,550

To close the cost variance accounts.

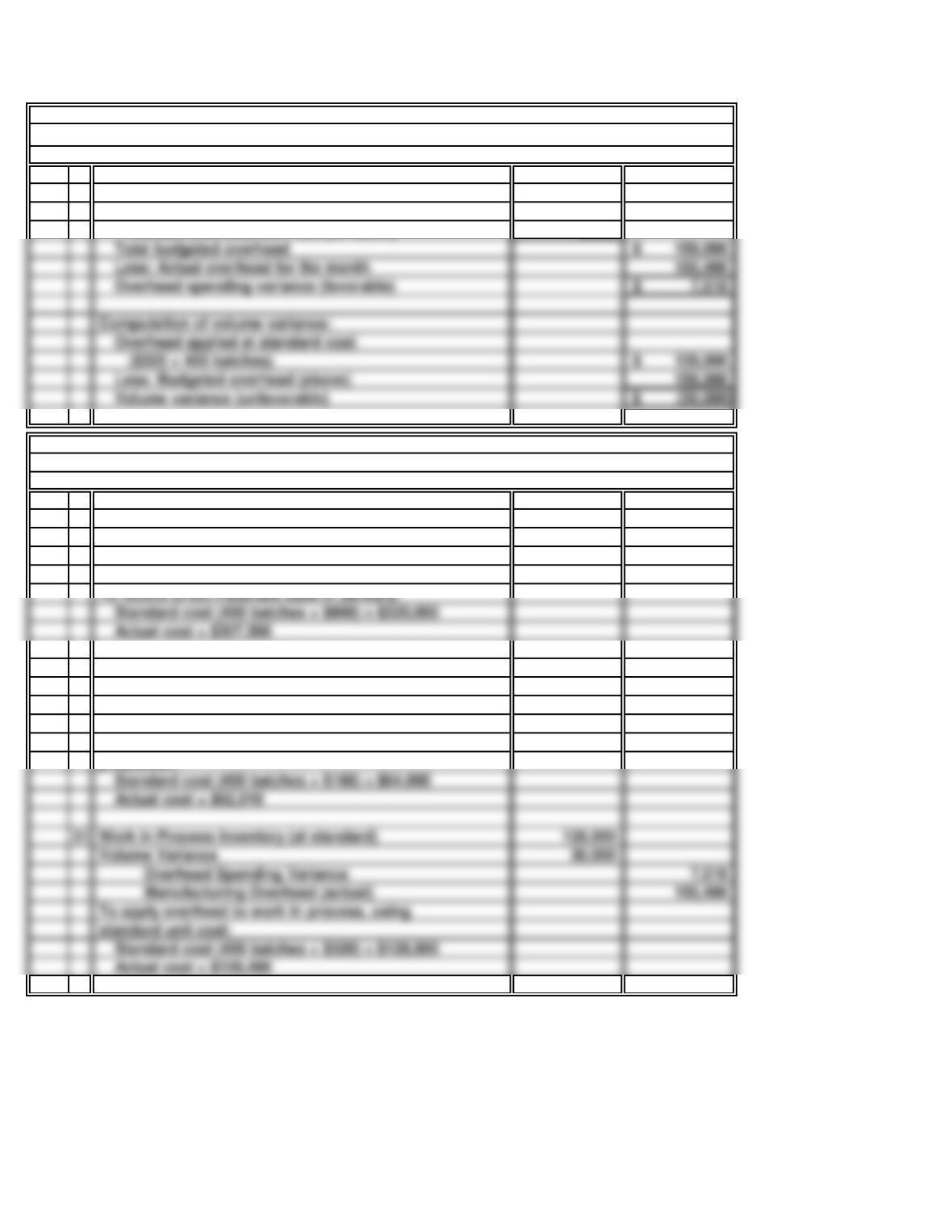

Overhead Spending Variance (unfavorable) ………………………………………….

Cost of Goods Sold ………………………………………………………………………

Direct Labor Rate Variance (unfavorable) …………………………………………

Direct Labor Efficiency Variance (unfavorable) ………………………………………….

Overhead Volume Variance (favorable) ………………………………

Materials Quantity Variance (unfavorable) …………………………………………

Materials Price Variance (favorable) ………………………………….

$22,000

Finished Goods Inventory (at standard cost)

Problem 24.8A

RILEY CORPORATION (concluded)

Based on the journal entry to charge overhead costs to work in process, the following

relationships exist:

To transfer cost of completed units to finished goods.

Work in Process Inventory (at standard cost)

a.

c. =

$ 600

Fixed overhead allowed ($3 × 200 units) …………………………………………………………..

Standard Overhead Allowed at Actual Production Level

440

$ 1,040

Total overhead allowed …………………………………………………………………………….

Variable overhead allowed ($2 × 220 units) …………………………………………………………….

Labor Rate Variance

Actual Labor Hours × (Standard Rate – Actual Rate)

PROBLEM 24.9A

ANTON COMPANY

45 Minutes, Medium

Since the direct materials quantity variance is $0, the actual quantity of materials used per

stand must equal the budgeted quantity per stand. Thus, the total quantity purchased and

used is:

$10 × (.5 hours per unit – actual hours per unit) × 220

b.

c. 30,400

1,600

3,200

Direct Materials Inventory (1,600 pounds × $22 per pound) ……..

Materials Price Variance (unfavorable) …………………………………………

SOLUTIONS TO PROBLEMS SET B

25 Minutes, Strong

PROBLEM 24.1B

UNDEM

The materials quantity variance (MQV) is first used to find the standard quantity of material

allowed for producing 950 units (MQV is half MPV):

Materials Quantity Variance (unfavorable) …………………………………….

Work in Process Inventory (1,520 pounds × $20 per pound) …………………………..

PROBLEM 24.2B

DYELOT INDUSTRIES

a.

-$8,000 (or $8,000 Unfavorable)

Standard Price × (Standard Quantity – Actual Quantity)

$0.80/lb. × [(1,000 lbs. × 400 batches) – 410,000 lbs.]

$0.80/lb. × -10,000 lbs.

$1,590 Favorable

Actual Hours × (Standard Hourly Rate – Actual Hourly Rate)

7,950 hrs. × ($8.00/hr. – $7.80/hr.)

7,950 hrs. × $0.20/hr.

Overhead variances are computed on the following page.

$8.00/hr. × [(20 hrs. × 400 batches) – 7,950 hrs.]

$8.00/hr. × 50 hrs.

$400 Favorable

Standard Hourly Rate × (Standard Hours – Actual Hours)

30 Minutes, Medium

Computation of materials price variance (MPV):

Computation of materials quantity variance (MQV):

Computation of labor rate variance (LRV):

Computation of labor efficiency variance (LEV):

Actual Quantity Used × (Standard Price – Actual Price)

410,000 lbs. × ($0.80/lb. – $0.75/lb.)

410,000 lbs. × $0.05/lb.

$20,500 Favorable

PROBLEM 24.2B

DYELOT INDUSTRIES (concluded)

a. (continued)

Computation of overhead spending variance:

Overhead budgeted for 400 batches:

Fixed 150,000$

Variable (400 batches × $20 per batch) 8,000

b.

General Journal

Jan. 31 Work in Process Inventory (at standard) 320,000

Materials Quantity Variance 8,000

Materials Price Variance 20,500

Materials Inventory (actual) 307,500

To record direct materials used in January.

Standard cost (400 batches × $800) = $320,000

Actual cost = $307,500

31 Work in Process Inventory (at standard) 64,000

Labor Rate Variance 1,590

Labor Efficiency Variance 400

Direct Labor (actual) 62,010

To record direct labor cost applicable to January

production:

Standard cost (400 batches × $160) = $64,000

Actual cost = $62,010

31 Work in Process Inventory (at standard) 128,000

Volume Variance 30,000

Overhead Spending Variance 7,510

Manufacturing Overhead (actual) 150,490

To apply overhead to work in process, using

Standard cost (400 batches × $320) = $128,000

Actual cost = $150,490

Total budgeted overhead 158,000$

Less: Actual overhead for the month 150,490

Overhead spending variance (favorable) 7,510$

Computation of volume variance:

Overhead applied at standard cost

($320 × 400 batches) 128,000$

Less: Budgeted overhead (above) 158,000

Volume variance (unfavorable) (30,000)$

25 Minutes, Medium PROBLEM 24.3B

LATIN SILK PRODUCTS

a.

General Journal

(1) Work in Process (standard cost) 50,000

Materials Quantity Variance 5,000

Materials Price Variance 1,000

Direct Materials Inventory (actual cost) 54,000

To record materials used.

(2) Work in Process (standard cost) 47,000

Labor Efficiency Variance 4,000

(3) Work in Process (standard cost) 56,400

Overhead Spending Variance 600

Overhead Volume Variance 3,000

Manufacturing Overhead (actual cost) 60,000

To record manufacturing overhead assigned to

production, and to record overhead variances.

b. (1) Finished Goods Inventory (at standard cost) 80,000

(2) Cost of Goods Sold (at standard cost) 72,000

Finished Goods Inventory (at standard cost) 72,000

To record cost of units sold, 9,000 units at $8 per unit.

a. =

b. =

=

=

*Actual Rate per Hour = $20,000/2,500 hours = $8.00/hour

-$825 Unfavorable

*Standard Hours Allowed = 160 batches × 15 hours/batch = 2,400 hours

$8.25 per hour × (2,400 hours* – 2,500 hours)

$625 Favorable

Labor Rate Variance

Actual Labor Hours × (Standard Rate – Actual Rate)

2,500 hours × ($8.25 – $8.00*)

45 Minutes, Strong

Materials Price Variance

Actual Quantity Used × (Standard Price – Actual Price)

PROBLEM 24.4B

HANS ENTERPRISES

=

=

$30,000 Unfavorable

*Standard Quantity Allowed = 160 batches × 1,025 pounds/batch = 164,000 pounds

$34,000 Favorable

*Actual Price per Pound = $816,000/170,000 pounds = $4.80/pound

170,000 pounds × ($5.00 – $4.80*)

c.

Overhead

Costs Applied

d.

30,000

Direct Materials Inventory (at actual cost) ……………………………………………………

Material Price Variance (favorable) ……………………………………………………………..

*160 actual batches × 1,025 pounds allowed per batch × $5.00 per pound = $820,000

To record the cost of direct materials charged to production.

Work in Process Inventory (at standard cost) ……………………………….

Materials Quantity Variance (unfavorable) …………………………………….

e.

19,800 *

Labor Rate Variance (favorable) ………………………………………………………………

Direct Labor (at actual cost) …………………………………………………………………..

Labor Efficiency Variance (unfavorable) ……………………………………………

To record the cost of direct labor charged to production.

*160 actual batches × 15 hours allowed per batch × $8.25 per hour = $19,800

f.

5,120

700

220

To apply overhead to production.

Manufacturing Overhead (at actual cost) ………………………………………………………..

Overhead Volume Variance (favorable) ……………………………………………………….

PROBLEM 24.4B

HANS ENTERPRISES (continued)

Overhead variances:

Actual Overhead

Costs Incurred

Costs Allowed

Standard Overhead

Entry to charge direct labor to production:

Work in Process Inventory (at standard cost) …………………………………

Entry to charge materials to production:

Entry to charge overhead to production:

Work in Process Inventory (at standard cost) …………………………………..

Overhead Spending Variance (favorable) …………………………………………………….

$3,100

1,100

*Standard Variable Overhead Allowed = $10.00/batch × 160 batches = $1,600