1. In a centralized operation, all major planning and operating decisions are made by top management

.

In a decentralized operation, managers of separate divisions or units are delegated operating

responsibility. The division (unit) managers are responsible for planning and controlling the

operations of their divisions. Divisions are often structured around products, customers, or

regions.

2. The department manager of a profit center has responsibility for and authority over costs and

revenues, while the manager of an investment center has responsibility for and authority over

controlling investments in assets as well as costs and revenues.

3. Payroll: Number of checks issued. Accounts payable: Number of invoices paid. Accounts

receivable: Number of sales invoice payments collected. Database administration: Number of

reports generated.

4. The major shortcoming of using income from operations as a measure of investment center

p

erformance is that it ignores the amount of investment committed to each center. Because

investment center managers also control the amount of assets invested in their centers, they

should be held accountable for the use of invested assets.

5. A division of a decentralized company could be considered the least profitable, even though

it earned the largest amount of income from operations, when its rate of return on investment

is the lowest. In this situation, the division would be considered the least profitable per dollar

invested in the division because it generated less profit out of each dollar of assets invested.

6. By dividing income from operations by the amount of invested assets, each division is placed

on a comparable basis of income from operations per dollar invested.

7. The balanced scorecard attempts to identify the underlying nonfinancial drivers, or causes, of

financial performance related to innovation and learning, customer service, and internal processes.

In this way, the financial performance may be improved. For example, customer satisfaction is

often measured by the number of repeat customers. By increasing the number of repeat customers,

sales and income from operations can be increased.

8. The objective of transfer pricing is to encourage each division manager to work in the best

interests of the company. Thus, transfer prices should encourage managers to transfer goods

b

etween divisions if the overall company income can be increased.

9. When unused capacity exists in the supplying division, the negotiated price approach is

p

referred over the market price approach.

10. When using the negotiated price approach to transfer pricing, the transfer price should be less

than the market price but greater than the supplying division’s variable cost per unit.

CHAPTER 24

PERFORMANCE EVALUATION

DISCUSSION QUESTIONS

FOR DECENTRALIZED OPERATIONS

24-1

CHAPTER 24 Performance Evaluation for Decentralized Operations

PE 24–1A

PE 24–2A

Southeast Division Service Charge for Travel Department:

PE 24–2B

Retail Division Service Charge for Computer Technology Department:

PE 24–3A

Northeast Pacific

Division Division

Sales……………………………………………………

…

$1,155,000 $1,204,000

Cost of goods sold…………………………………… 590,800 658,000

PRACTICE EXERCISES

24-2

CHAPTER 24 Performance Evaluation for Decentralized Operations

PE 24–3B

Retail Commercial

Division Division

Sales…………………………………………………

…

$945,000 $966,000

Cost of goods sold………………………………

…

504,000 559,300

PE 24–4A

PE 24–4B

a. Profit Margin = $36,000 ÷ $720,000 = 5.0%

PE 24–5A

Income from operations………………………………………………………………

…

$90,000

PE 24–5B

Income from operations………………………………………………………………

…

$420,000

24-3

PE 24–6A

PE 24–6B

Increase in South (Supplying)

Division’s Income from Operations =(Transfer Price – Variable Cost per Unit)

× Units Transferred

Increase in Pembroke (Supplying)

Division’s Income from Operations =(Transfer Price – Variable Cost per Unit)

× Units Transferred

24-4

CHAPTER 24 Performance Evaluation for Decentralized Operations

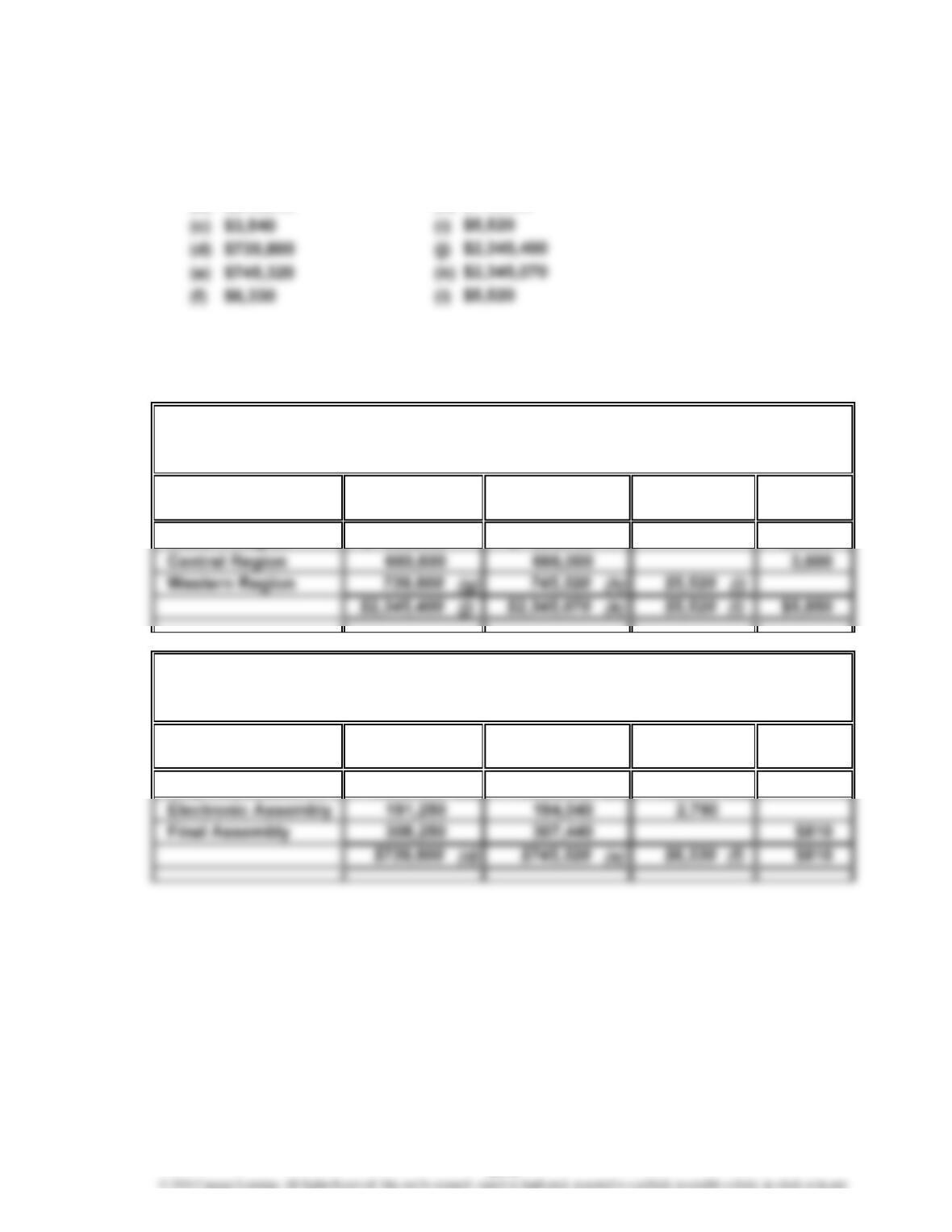

Ex. 24–1

a. (a) $240,300 (g

)

(b) $243,840 (h

)

Schedules of supporting calculations (answers in italics; the solution requires

working from the department level, up to the plant level, then to the vice president

of production level):

Under

Budget

Eastern Region $ 933,750 $2,250

Under

Budget

Chip Fabrication (a) $243,840 (b) $3,540 (c)

BudgetPlant

$240,300

Department

Actual

Over

Over

SASKATOON COMPANY

Budget Performance Report—Manager, Western Region Plant

For the Month Ended June 30, 2016

Budget

Budget Actual

$745,320

Budget

$ 936,000

EXERCISES

SASKATOON COMPANY

Budget Performance Report—Vice President, Production

For the Month Ended June 30, 2016

$739,800

24-5

CHAPTER 24 Performance Evaluation for Decentralized Operations

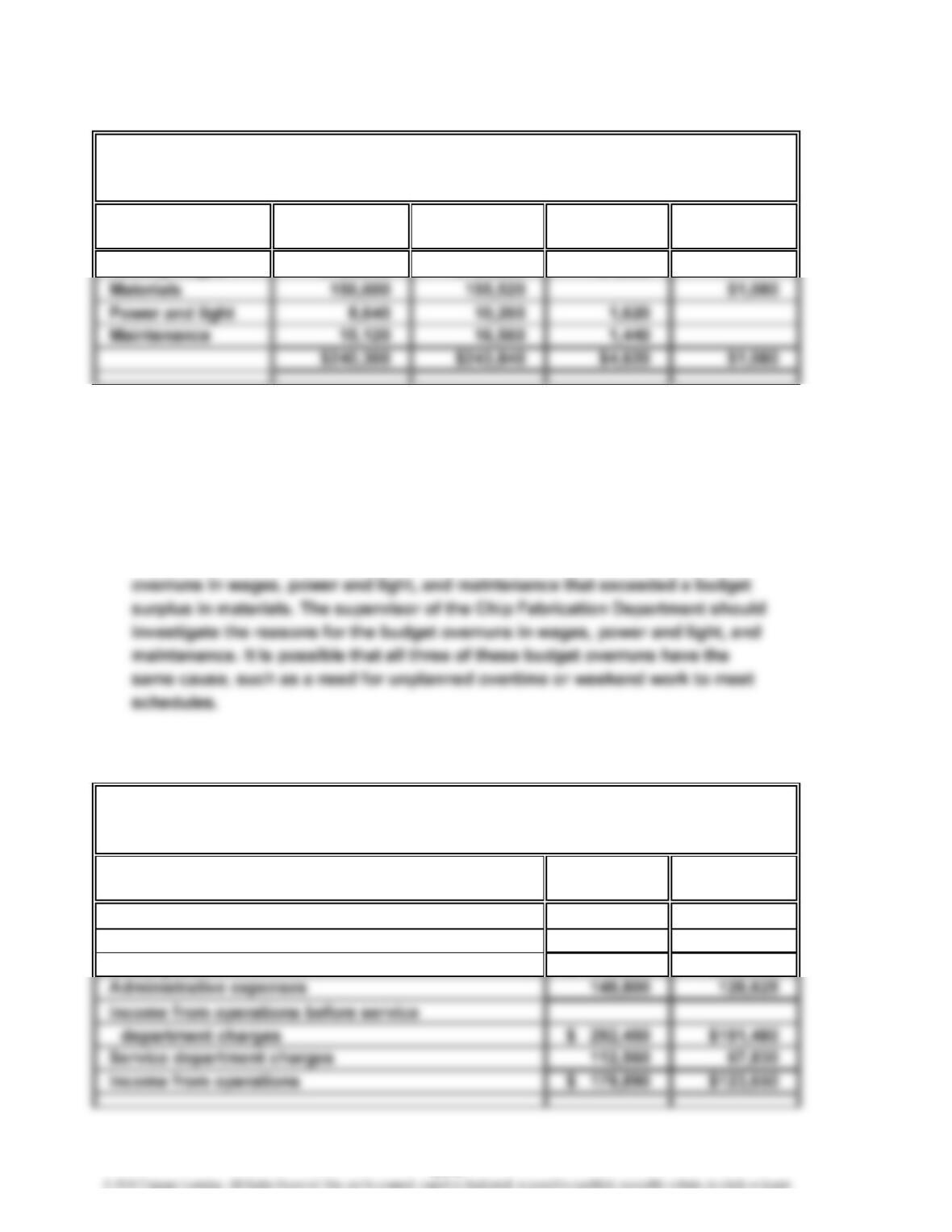

Ex. 24–1 (Concluded)

Under

Budget

Factory wages

b. MEMO

To: Robin Mooney, Vice President of Production

The Western Region plant has experienced a budget overrun, while the Eastern

and Central Region plants have experienced a budget surplus. The budget of the

Western Region plant reveals that the Chip Fabrication Department causes the

majority of the budget overrun. The budget for the Chip Fabrication Department

indicates that the budget overrun was caused by a combination of budget

Ex. 24–2

Residential

Division

Net sales $743,780

Cost of goods sold 423,675

Gross profit $320,105

Division

$1,354,500

912,250

$ 442,250

For the Year Ended June 30, 2016

JERSEY COAST CONSTRUCTION COMPANY

Commercial

Divisional Income Statements

Cost

$ 59,940 $1,560

Budget

Budget Actual

$ 61,500

SASKATOON COMPANY

Budget Performance Report—Supervisor, Chip Fabrication

For the Month Ended June 30, 2016

Over

24-6

CHAPTER 24 Performance Evaluation for Decentralized Operations

Ex. 24–3

Expense Activity Bases

a. Legal Number of hours of legal service

b. Duplication services Number of pages copied

c. Electronic data processing Central processing unit (CPU) time, number of

printed pages, amount of memory usage

24-7

CHAPTER 24 Performance Evaluation for Decentralized Operations

Ex. 24–5

Government

a. Residential Commercial Contract Total

Number of payroll checks:

Weekly payroll × 52………

…

15,600 7,800 10,400

Service Activity Charge

b. Dept. Cost ÷ Base = Rate

Service department charge rates:

Government

Residential Commercial Contract Total

Service department charges:

1

16,500 checks × $2.00 per distribution

2

9,720 checks × $2.00 per distribution

3

11,480 checks × $2.00 per distribution

c. Residential’s service department charge is higher than the other two divisions

because Residential is a heavy user of service department services. Residential

3

21

24-8

CHAPTER 24 Performance Evaluation for Decentralized Operations

Ex. 24–6

$160,000

3,200 calls

b. October charges to the COMM sector:

Help desk charge:

(5,200 employees × 25% × 96% × 1.5) × $50/call = $93,600

Network center charge:

a. Help desk:

= $50 per call

24-9

CHAPTER 24 Performance Evaluation for Decentralized Operations

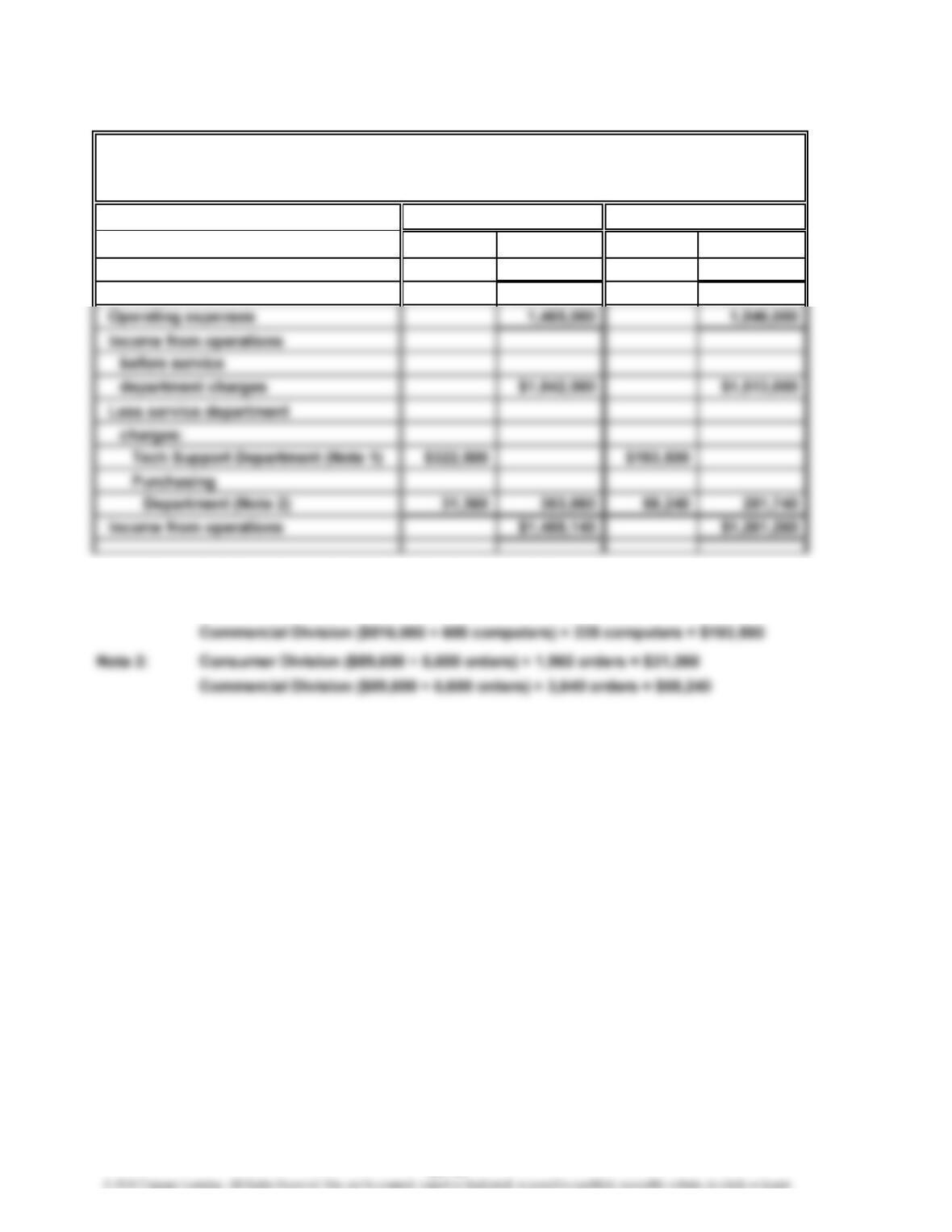

Ex. 24–7

Revenues $7,430,000 $6,184,000

Cost of goods sold 4,123,000 3,125,000

Gross profit $3,307,000 $3,059,000

Supporting calculations for controllable service department charges:

Note 1: Consumer Division ($516,000 ÷ 600 computers) × 375 computers = $322,500

YOZAMBA TECHNOLOGY

Divisional Income Statements

For the Year Ended December 31, 2016

Consumer Division Commercial Division

24-10

CHAPTER 24 Performance Evaluation for Decentralized Operations

Ex. 24–8

a. The reported income from operations does not accurately measure performance

because the service department charges are based on revenues. Revenues are

not associated with the profit center manager’s use of the service department

services. For example, the Reservations Department serves only the Passenger

b.

Revenues $3,025,000 $3,025,000

Operating expenses 2,450,000 2,736,000

Income from operations

before service department

Supporting calculations for controllable service department charges:

Training: Passenger Division, ($250,000 ÷ 500 personnel trained) × 350

personnel trained

WILD SUN AIRLINES INC.

Divisional Income Statements

For the Year Ended December 31, 2016

Passenger Division Cargo Division

24-11

CHAPTER 24 Performance Evaluation for Decentralized Operations

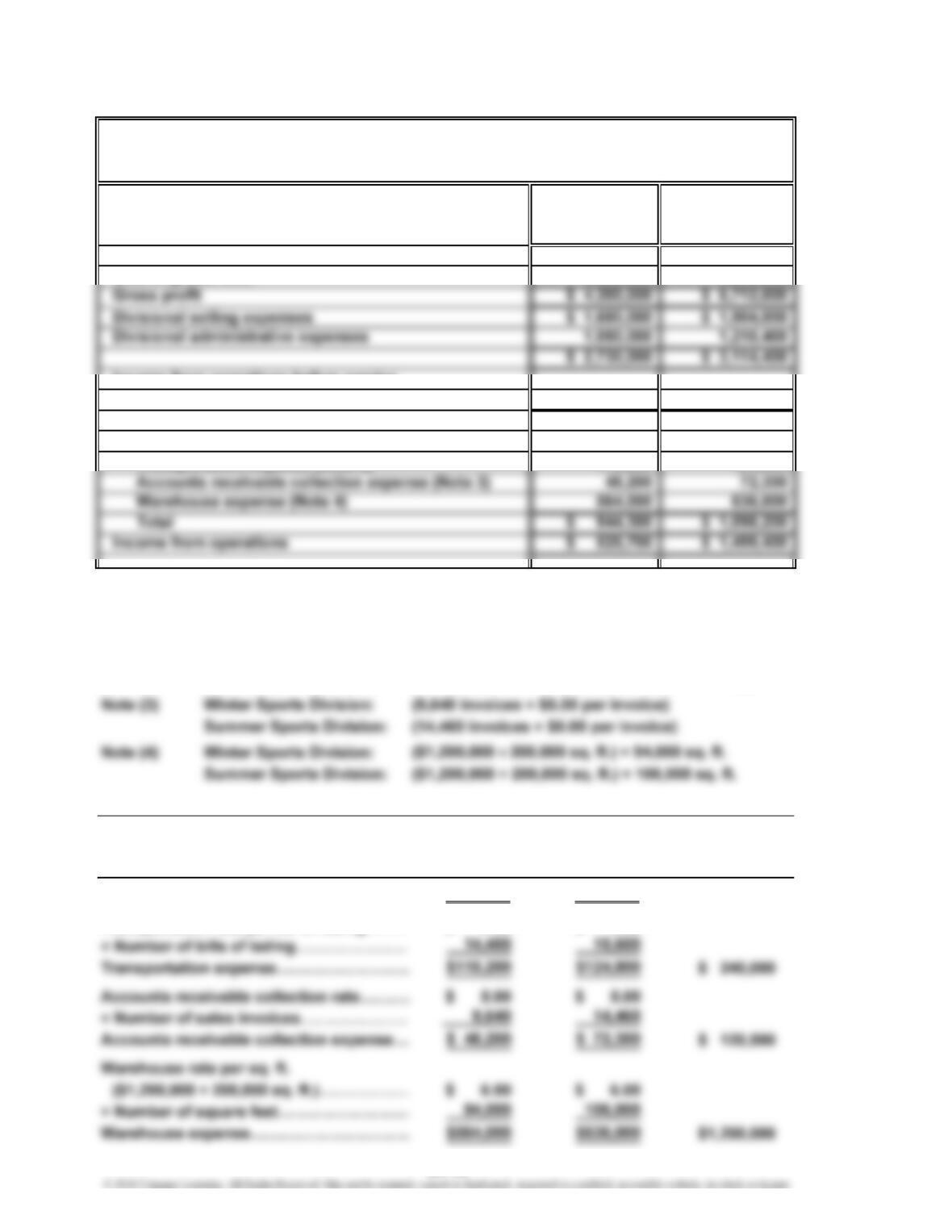

Ex. 24–9

Winter Summer

Sports Sports

Division Division

Sales $10,500,000 $13,600,000

Cost of goods sold 6,300,000 7,888,000

Income from operations before service

department charges $ 1,470,000 $ 2,597,600

Less service department charges:

Advertising expense (Note 1) $ 216,900 $ 265,100

Transportation expense (Note 2) 115,200 124,800

Supporting Schedule:

Note (1) Winter Sports Division: $216,900

Summer Sports Division: $265,100

Note (2) Winter Sports Division: (14,400 bills of lading × $8.00 per bill of lading)

Summer Sports Division: (15,600 bills of lading × $8.00 per bill of lading)

Winter Summer

Sports Sports

Division Division Total

Advertising expense…………………………

…

$216,900 $265,100 $ 482,000

Transportation rate per bill of lading……

…

$ 8.00 $ 8.00

…

Service Department Charges

XSPORT SPORTING GOODS CO.

Divisional Income Statements

For the Year Ended December 31, 2016

24-12

CHAPTER 24 Performance Evaluation for Decentralized Operations

Ex. 24–10

a. Retail Division: 26% ($343,200 ÷ $1,320,000)

Ex. 24–11

a. Retail Commercial Internet

Division Division Division

Income from operations………………………

…

$343,200 $320,000 $176,000

Minimum amount of income from

operations:

Ex. 24–12

a. 2.20 = 13.2% ÷ 6%

d. 3.00 = 15.0% ÷ 5%

24-13

CHAPTER 24 Performance Evaluation for Decentralized Operations

Ex. 24–13

Sales

Invested Assets

b. The profit margin would increase from 14% to 16%, the investment turnover

would remain unchanged, and the rate of return on investment would increase

from 28% to 32%, as shown below.

Sales

Invested Assets

a. Rate of Return

on Investment = Profit Margin × Investment Turnover

×

=

Rate of Return

on Investment Sales

Income from Operations

Rate of Return

on Investment = Profit Margin × Investment Turnover

Rate of Return

on Investment =Income from Operations ×

Sales

24-14

CHAPTER 24 Performance Evaluation for Decentralized Operations

Ex. 24–14

Revenues

Invested Assets

$2,220 $14,087

$14,087 $22,056

$661 $5,979

$5,979 $14,750

$1,112 $3,811

$3,811 $7,506

b. The four sectors are different from each other. Media Networks combines a good

at 15.8% with an average investment turnover. The combination produces a

respectable ROI of 10.1%. Studio Entertainment has a weak profit margin and a

× Parks and Resorts:

=

Rate of Return

on Investment

Studio Entertainment: ×

Consumer Products:

Revenues

Income from Operations

×

a. ×

24-15

CHAPTER 24 Performance Evaluation for Decentralized Operations

Ex. 24–15

a. 20.0% ($185,000 ÷ $925,000) g. $81,000 ($450,000 × 18%)

b. $138,750 ($925,000 × 15%) h. 13.0% ($58,500 ÷ $450,000)

Ex. 24–16

a. (a) $60,200 ($860,000 × 7%)

(b) $344,000 ($60,200 ÷ 17.5%)

b. North Division: $18,920 [$60,200 – ($344,000 × 12%)]

c. (1) The North Division has the highest return on investment (17.5%).

24-16

CHAPTER 24 Performance Evaluation for Decentralized Operations

Ex. 24–17

Revenues

Invested Assets

$105 $688

$688 $2,139

b.

Vacation

Ownership

Income from operations……………………………

…

$105

c. The Vacation Ownership (VO) segment has the weakest return on investment,

which is mainly the result of a weak investment turnover. The VO segment earns

profit margins that are higher than the profit margins in the Hotel Ownership (HO)

Revenues

$571

Ownership

Hotel

Income from Operations

a.

Vacation Ownership: ×

× =

Rate of Return

on Investment

24-17

CHAPTER 24 Performance Evaluation for Decentralized Operations

Ex. 24–18

Although there is some judgment in classifying each of these measures, the following

represents the author’s assessment with explanations:

Average card member spending Customer—demonstrates the usefulness of

the card to the customer.

Cards in force Customer—if customers did not value the

card, they would not have one.

24-18

CHAPTER 24 Performance Evaluation for Decentralized Operations

Ex. 24–19

This exercise is intended to spark discussion around using the balanced scorecard

in an emerging business. Some possible metrics are included below.

Innovation and Learning

Number of training hours

Employee turnover

Customer Service

Number of new customers

Retaining existing customers

Quality of food

Internal Processes

Order delivery time

Consistency of portion size

Financial

Number of meals served per shift (Note: Shift might be considered breakfast, lunch,

dinner, late night)

24-19

CHAPTER 24 Performance Evaluation for Decentralized Operations

Ex. 24–20

a. Increase in XPort Industries’ Market Variable Cost Unit

Income from Operations = Price – per Unit × Transferred

$3,000,000 =($210 –$160) × 60,000

Ex. 24–21

a. Increase in XPort Industries’ Market Variable Cost Units

Income from Operations = Price – per Unit × Transferred

b. Increase in the Instrument Division’s Market Transfer Units

Income from Operations = Price – Price × Transferred

c. Increase in the Components Division’s Transfer Variable Cost Units

Income from Operations = Price – per Unit × Transferred

d. Any transfer price will cause the total income of the company to increase, as long

as the supplier division capacity is used toward making materials for products that

are ultimately sold to the outside. However, transfer prices should be set between

variable cost and the market price in order to give the division managers proper

24-20