PROBLEM 24–5A

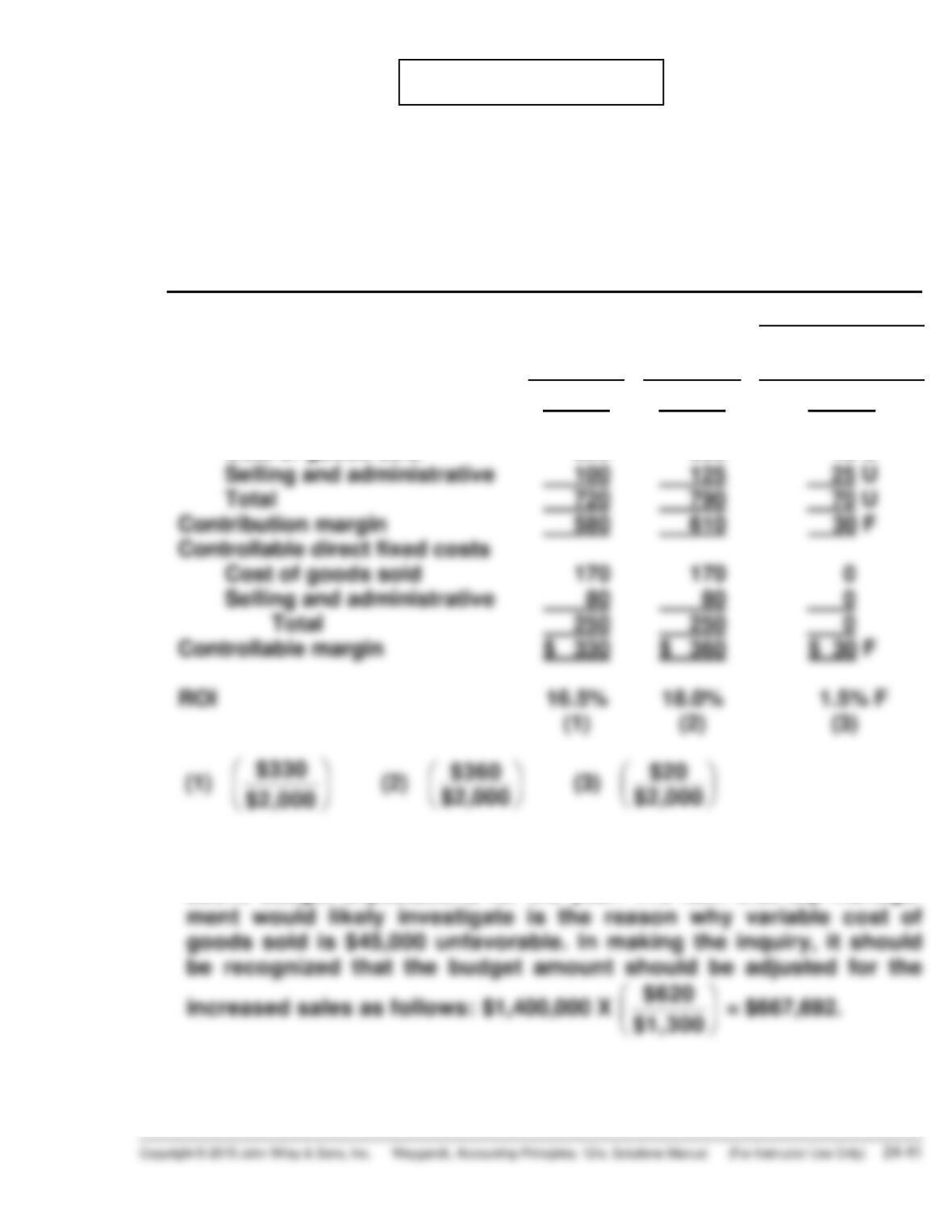

(a) OPTIMUS COMPANY

Home Division

Responsibility Report

For the Year Ended December 31, 2017

(in thousands of dollars)

Difference

Budget

Actual

Favorable F

Unfavorable U

(3)

Sales

Variable costs

Cost of goods sold

Selling and administrative

Total

$1,300

620

100

720

$1,400

665

125

790

$100 F

45 U

25 U

70 U

(b) The performance of the manager of the Home Division was slightly

above budget expectations for the year. The item that top manage-

ment would likely investigate is the reason why variable cost of

PROBLEM 24-5A (Continued)

(c) 1.

$360,000 + ($665,000 X 5%)

$2,000,000

= 19.7%.

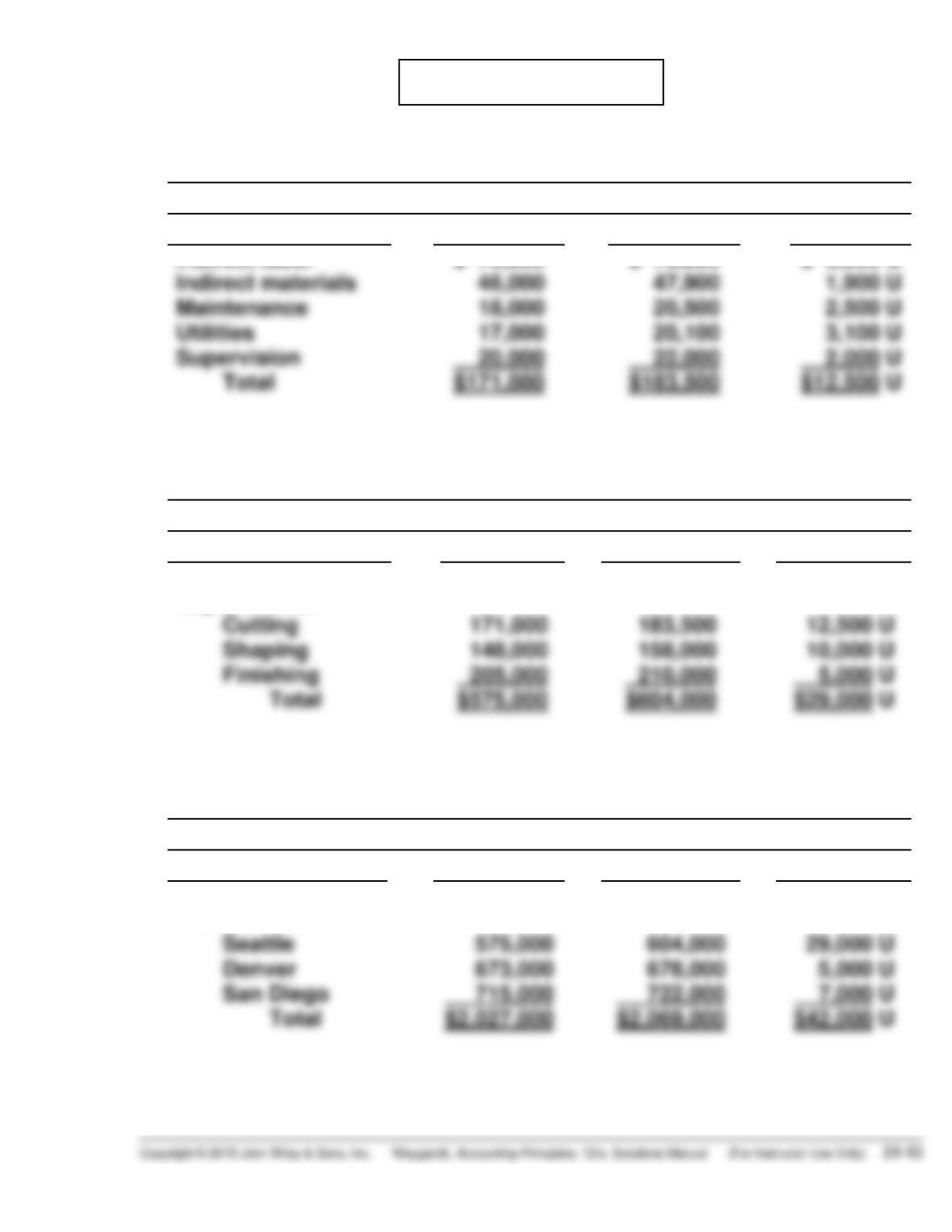

PROBLEM 24–6A

(a) No. 1

To Cutting Department Manager—Seattle Division Month: January

Controllable Costs:

Budget

Actual

Fav/Unfav

Indirect labor

Indirect materials

$ 70,000

46,000

$ 73,000

47,900

$ 3,000 U

1,900 U

No. 2

To Division Production Manager—Seattle Month: January

Controllable Costs:

Budget

Actual

Fav/Unfav

Seattle Division

Departments:

$ 51,000

$ 52,500

$ 1,500 U

No. 3

To Vice President—Production Month: January

Controllable Costs:

Budget

Actual

Fav/Unfav

V-P Production

Divisions:

$ 64,000

$ 65,000

$ 1,000 U

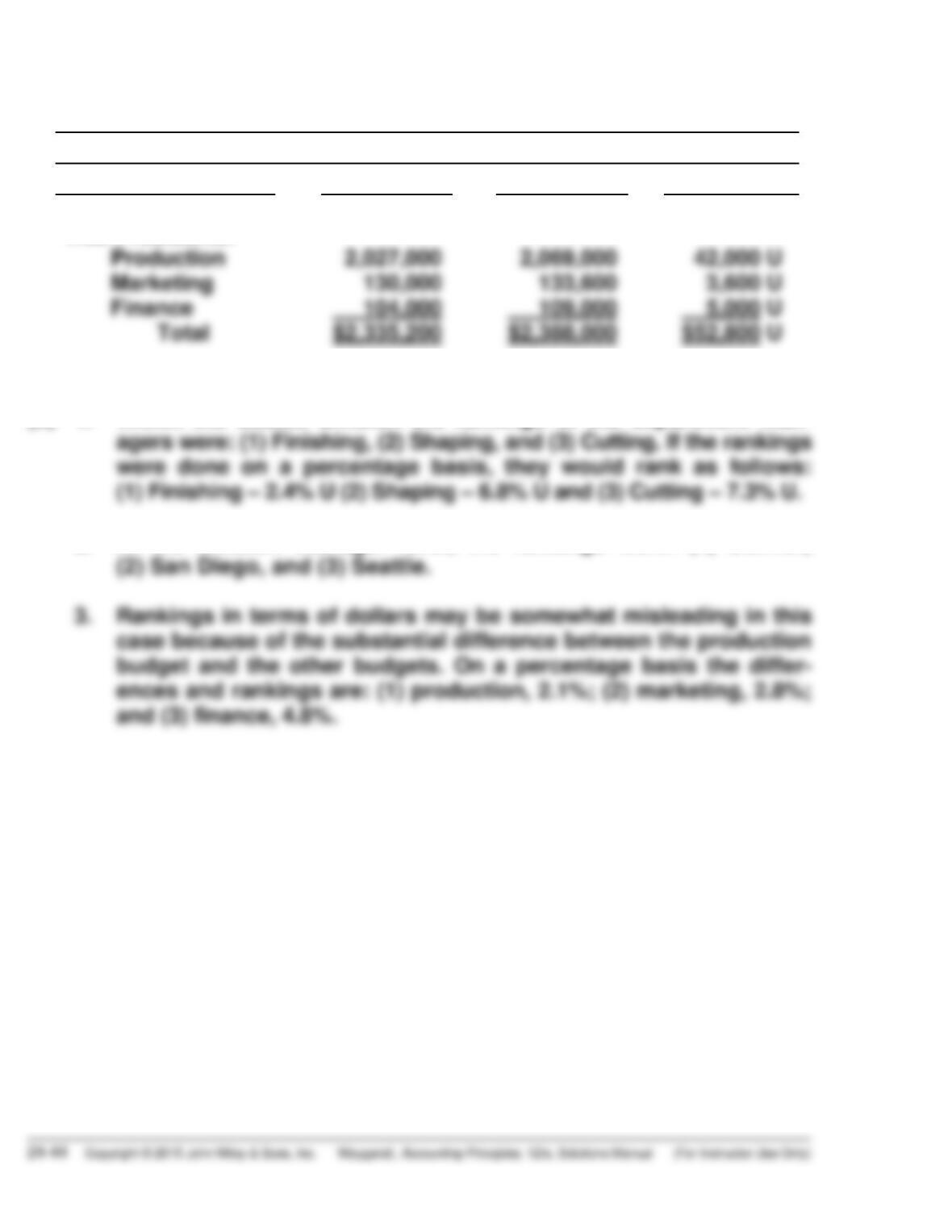

PROBLEM 24-6A (Continued)

No. 4

To President Month: January

Controllable Costs:

Budget

Actual

Fav/Unfav

President

Vice-Presidents:

$ 74,200

$ 76,400

$ 2,200 U

(b) 1. Within the Seattle division the rankings of the department man-

agers were: (1) Finishing, (2) Shaping, and (3) Cutting. If the rankings

2. At the division manager level, the rankings were: (1) Denver,

CD24 CURRENT DESIGNS

(a) Current Designs

Rotomolded Line

Manufacturing Budget

For the Year Ended December 31, 2017

4,000 kayaks

Units to be produced

Calculation

Amount budgeted

Costs:

Variable costs

Polyethylene powder

4,000 X 54 X $1.50

$ 324,000

Finishing kits

4,000 X $170

680,000

4,000 X 3 X $12

144,000

Indirect materials

Maintenance and utilities

88,000

Total variable costs

Fixed costs

Supervision

Insurance

Total fixed costs

214,200

Total costs

$1,664,000

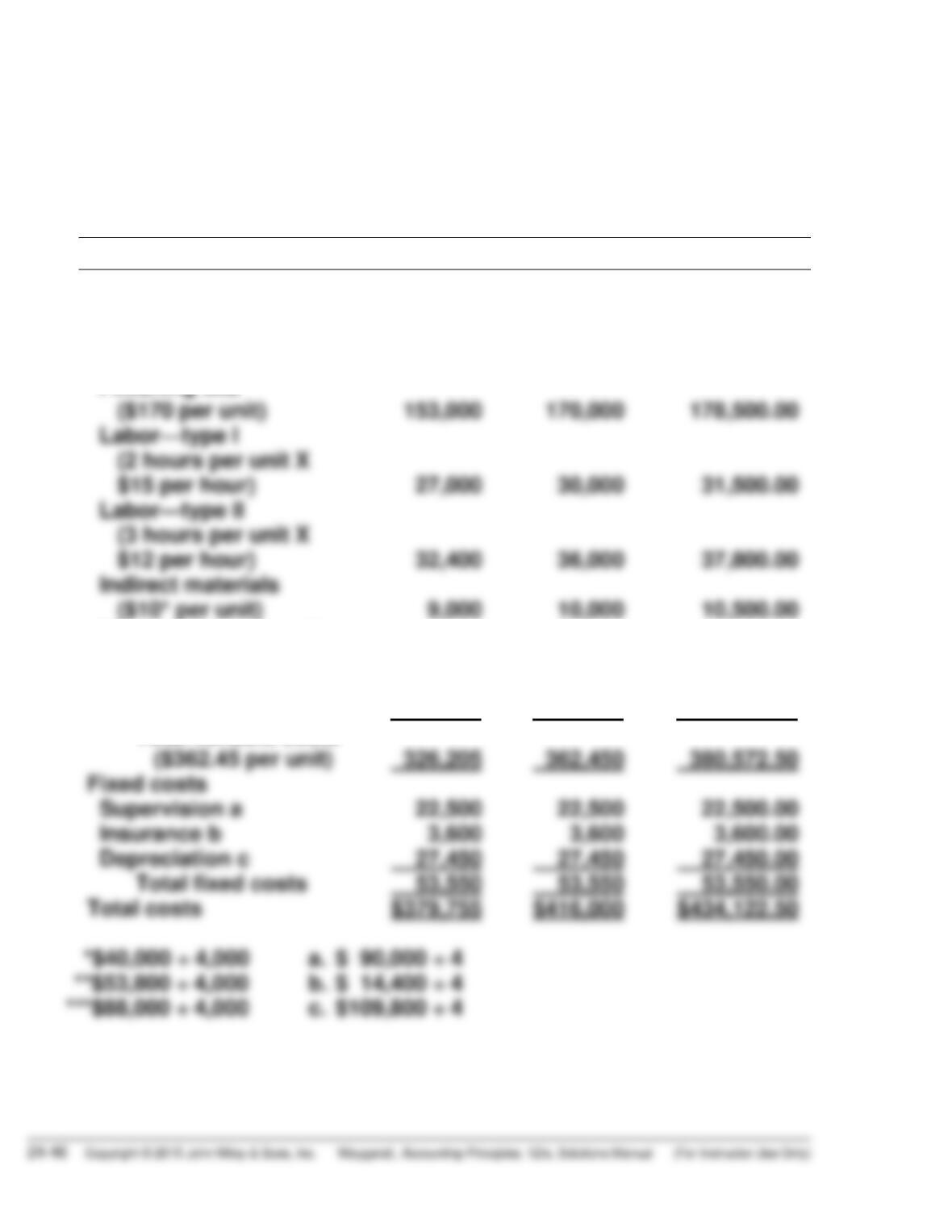

CD24 (Continued)

(b) Current Designs

Rotomolded Line

Manufacturing Flexible Budget Report

For the Quarter Ended March 31, 2017

Units to be produced

900 kayaks

1,000 kayaks

1,050 kayaks

Costs:

Variable costs

Polyethylene powder

(54 X 1.50 per unit)

$ 72,900

$ 81,000

$ 85,050.00

Finishing kits

($170 per unit)

153,000

170,000

178,500.00

$15 per hour)

Labor—type II

$12 per hour)

Indirect materials

Labor—type I

Manufacturing supplies

($13.45** per unit)

12,105

13,450

14,122.50

Maintenance and utilities

($22*** per unit)

19,800

22,000

23,100.00

Fixed costs

22,500

22,500

22,500.00

Total fixed costs

Total costs

Total variable costs

CD24 (Continued)

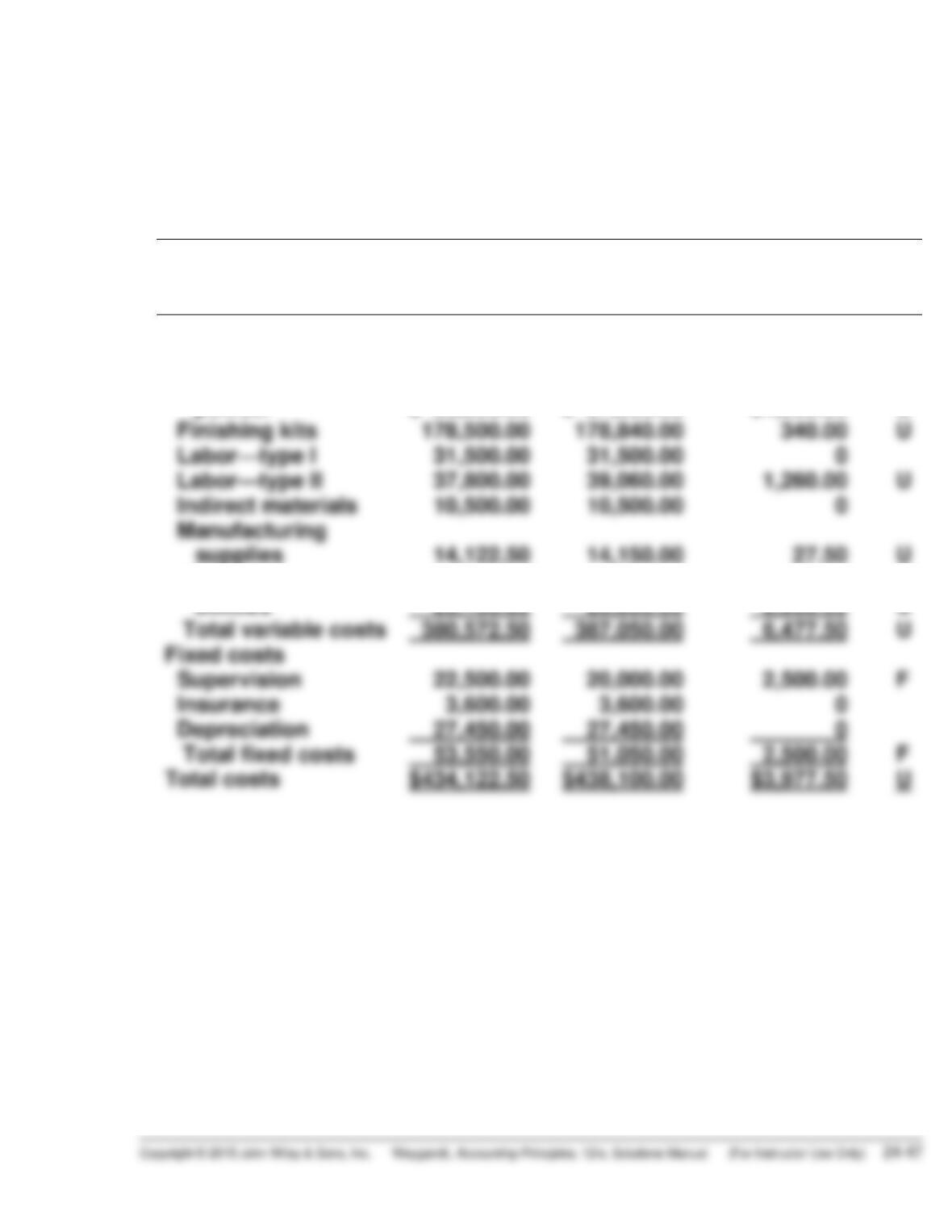

(c) Current Designs

Rotomolded Line

Manufacturing Flexible Budget Report

For the Quarter Ended March 31, 2017

Units to be produced

Budget for

1,050 kayaks

Actual costs for

1,050 kayaks

Difference

F = favorable

U = unfavorable

Costs:

Variable costs

Polyethylene

powder

$ 85,050.00

$ 87,000.00

$1,950.00

U

U

U

supplies

U

Maintenance and

utilities

23,100.00

26,000.00

2,900.00

U

Total variable costs

380,572.50

387,050.00

6,477.50

U

Fixed costs

F

Total fixed costs

F

Total costs

U

BYP 24-1 DECISION-MAKING ACROSS THE ORGANIZATION

(a) 1. The primary causes of the loss in net income were the decrease in

the number of boarding days and the decrease in the boarding

fee. The number of boarding days decreased by 2,900 or approxi-

mately 13% (2,900 days ÷ 21,900 days), and the boarding fee

2. Management did a poor job in controlling variable expenses.

Given that boarding days declined by about 13%, variable

expenses should decline by about 13%, or more precisely,

variable expenses should decline by $25,520 ($192,720 X

3. Management’s decisions to stay competitive probably were sound.

Given the decline in boarding days, the decision not to replace the

BYP 24-1 (Continued)

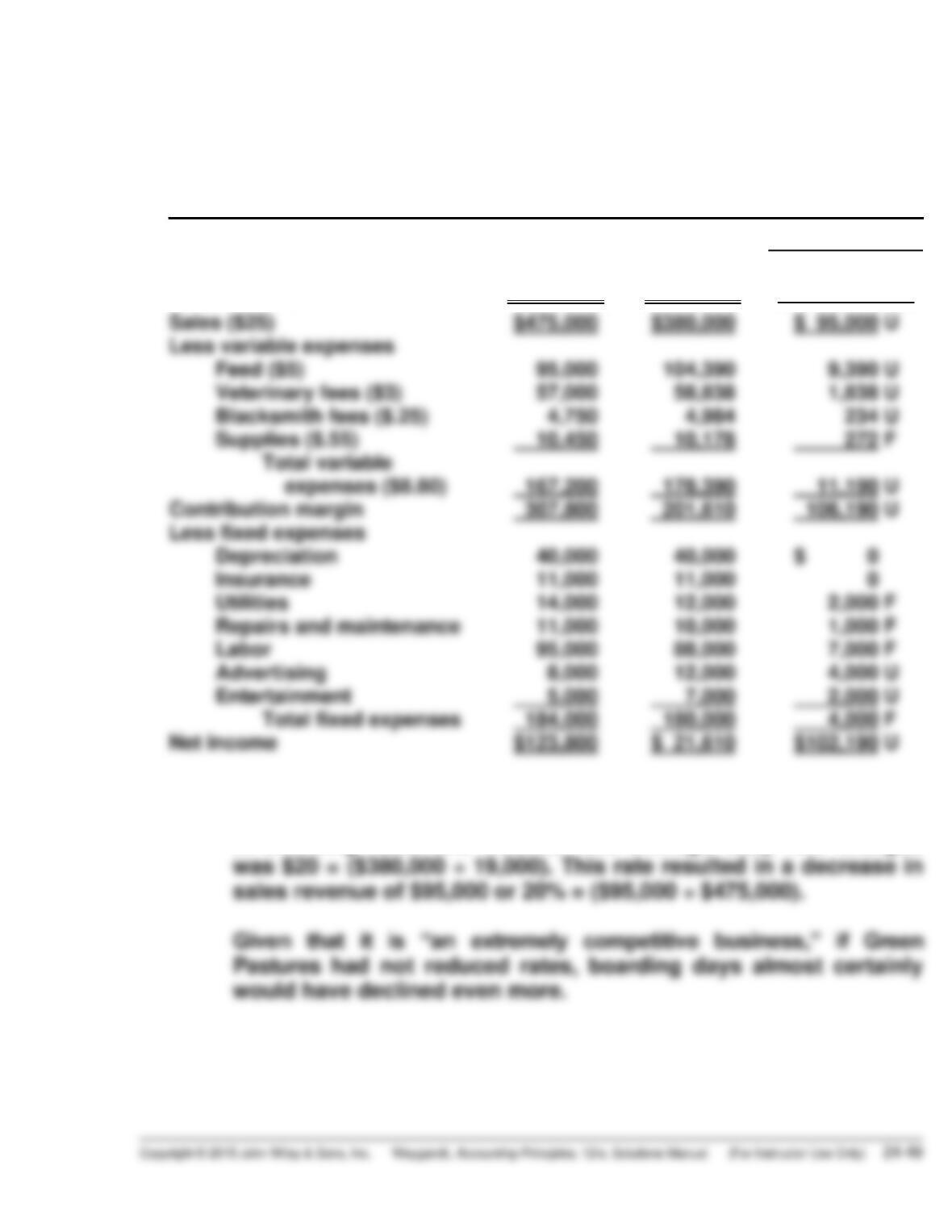

(b) GREEN PASTURES

Income Statement

Flexible Budget Report

For the Year Ended December 31, 2017

Difference

Boarding days (BD)

Sales ($25)

Less variable expenses

Feed ($5)

Veterinary fees ($3)

Budget at

19,000 BD

$475,000

95,000

57,000

Actual at

19,000 BD

$380,000

104,390

58,838

Favorable F

Unfavorable U

$ 95,000 U

9,390 U

1,838 U

(c) 1. The primary causes of the decrease in net income are the decreases

in boarding rates and volume. The average daily rate charged

was $20 = ($380,000 ÷ 19,000). This rate resulted in a decrease in

BYP 24-1 (Continued)

2. Management did a poor job of controlling variable expenses. These

expenses in total were $11,190 over budget or 6.7%, or ($11,190 ÷

$167,200).

Moreover, each individual variable expense was over budget,

(d) Given that the industry is “extremely competitive,” management should

consider two options. One, become the lowest cost operator. If Green

Pastures is the company with the lowest operating costs, it can under-

price its competitors and take customers away from them (increasing

Option two is to offer its customers a superior product or service. If cus–

tomers perceive that Green Pastures is the “best” boarding stable in

BYP 24-2 MANAGERIAL ANALYSIS

(a) Mary Gammel—Profit Center: Responsible for sales, inventory cost,

advertising, sales personnel, printing, and travel. She is not responsible

for the assets invested in her division and probably does not control

the rent or depreciation costs either. As a profit center manager she

might have control of the insurance, but she probably does not.

(b) Mary Gammel Budget differences: The cost of goods sold is 28%

($42,000 ÷ $150,000) above budget and so should definitely be brought

to her attention. Travel is 30% ($6,000 ÷ $20,000) below budget.

Students may differ as to whether they believe that this should be

brought to her attention. The differences in rent and depreciation should

not be brought to her attention because she does not control those

costs.

BYP 24-2 (Continued)

Jose Gomez Budget differences: As manager of an investment center,

Mr. Gomez is responsible for all categories of the budget. The

selection in this case would be which differences merit his attention.

Any decrease in a company’s gross profit rate (gross profit ÷ sales) is

BYP 24-3 REAL-WORLD FOCUS

(a) The company’s costs do not increase proportionately with the revenues

increase in the third and fourth quarter because the behavior of the

costs is primarily fixed.

BYP 24-4 REAL-WORLD FOCUS

(a) The two most common pain points are (1) dealing with other managers

and (2) technology issues, mainly frustration of budgeting in Excel

spreadsheets.

(d) The most commonly defined range of acceptable tolerance levels was

that variances were tolerated up to 5 to 10 percent. Beyond that level

there were consequences.

BYP 24-5 COMMUNICATION ACTIVITY

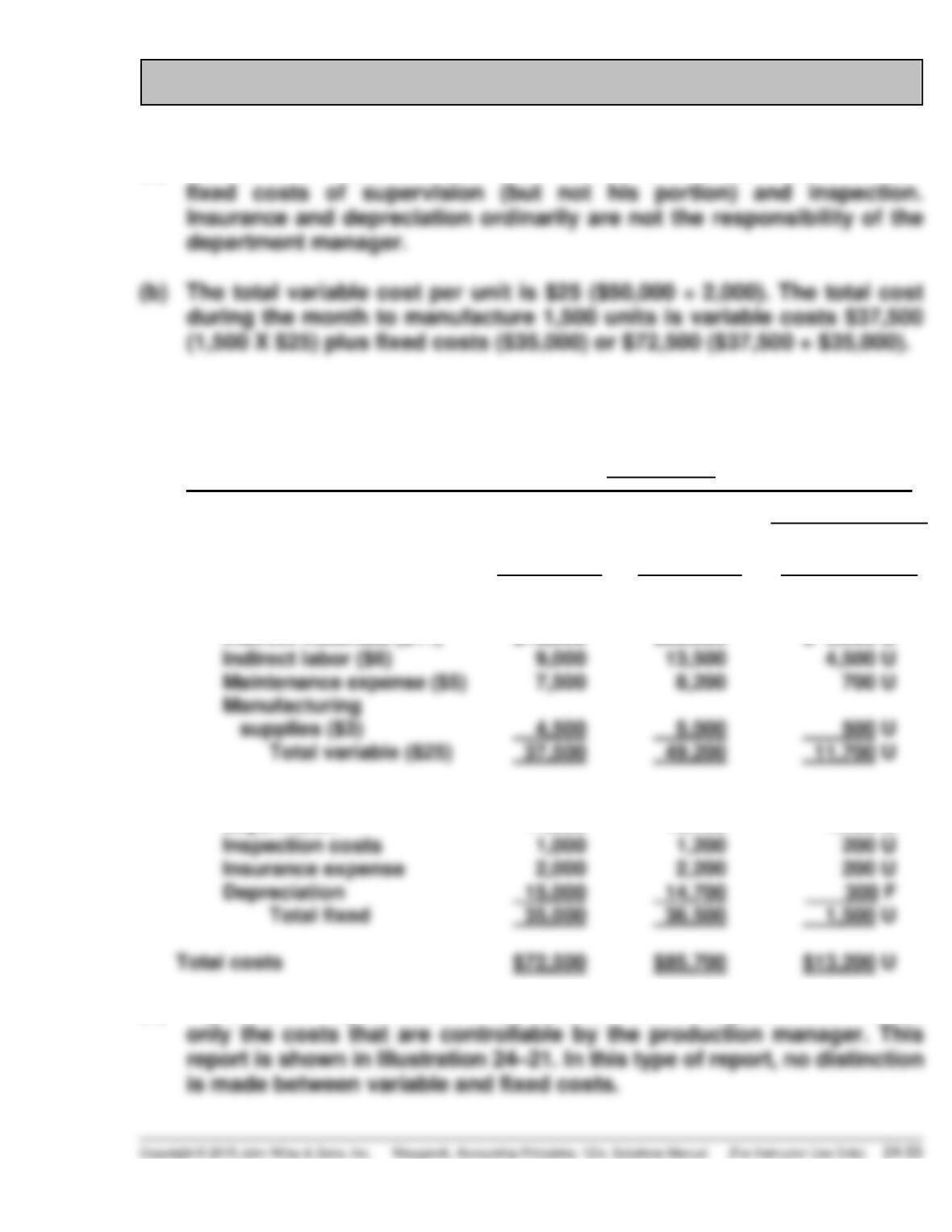

(a) Fred Bedner should be able to control all the variable costs and the

fixed costs of supervision (but not his portion) and inspection.

Insurance and depreciation ordinarily are not the responsibility of the

department manager.

(c) FLEMING COMPANY

Production Department

Manufacturing Overhead Flexible Budget Report

For the Month Ended

Difference

Variable costs

Indirect materials ($11)

Indirect labor ($6)

Fixed costs

Supervision

Inspection costs

Insurance expense

Budget at

1,500 units

$16,500

9,000

17,000

1,000

2,000

Actual at

1,500 units

$22,500

13,500

18,400

1,200

2,200

Favorable F

Unfavorable U

$ 6,000 U

4,500 U

1,400 U

200 U

200 U

(d) A production department is a cost center. Thus, the report should include

only the costs that are controllable by the production manager. This

BYP 24-5 (Continued)

FLEMING COMPANY

Production Department

Manufacturing Overhead Responsibility Report

For the Month Ended

Difference

Controllable Cost

Budget

Actual

Favorable F

Unfavorable U

Indirect materials

Indirect labor

Maintenance expense

$16,500

9,000

7,500

$22,500

13,500

8,200

$ 6,000 U

4,500 U

700 U

*$10,000 is deducted from both budget and actual for Mr. Bedner’s cost.

To: Mr. Fred Bedner, Production Manager

From: , Vice President of Production

Subject: Performance Evaluation for the Month of XXXXX

Your performance in controlling costs that are your responsibility was

very disappointing in the month of XXXXX. As indicated in the accom-

Indirect labor 50%).

BYP 24-5 (Continued)

Fred, it is imperative that you get costs under control in your department

as soon as possible.

BYP 24-6 ETHICS CASE

(a) The stakeholders in this ethical situation are:

The employees and managers of each investment center.

The central management and chief executive officer.

(b) Pressure to perform is a frequently identified cause for unethical

conduct. Employees are more prone to engage in unethical conduct

when unreasonable demands are made upon them. Rather than lose

(c) The company might maintain open lines of communication with its em-

ployees to better know the pressures of its managers. By “keeping in

touch,” the company may avoid making unreasonable demands on its

BYP 24-7 ALL ABOUT YOU

(a) The basic idea is to set up individual envelopes for different expense

categories. Once you have used up the money in a particular envelope,

you can’t use more. Begin by preparing a monthly budget. Identify

those items that you will pay in cash. These would include things like

(b) Answers will vary by student.

BYP 24-8 CONSIDERING YOUR COSTS AND BENEFITS

In general, in past years it has usually been considered prudent to

purchase a home rather than to rent. As noted, over time, home prices have

usually appreciated in most parts of the country. Mortgage interest

provides some tax relief, and by purchasing a home you get some control

over your housing costs. However, recent turbulence in the housing market