24-56

Comprehensive Problem for Chapters 22-24, cont.

Requirement 1, cont.

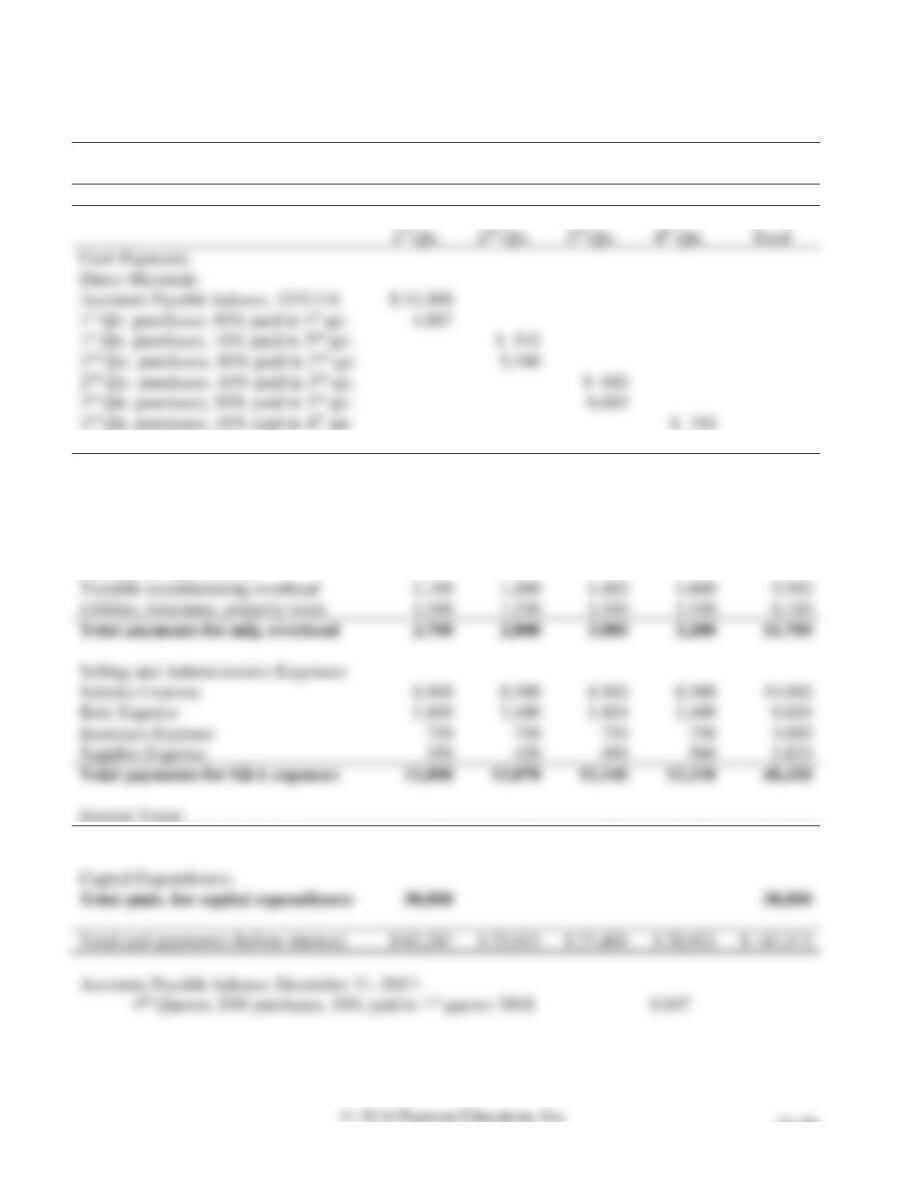

Schedule of Cash Payments

1st Qtr.

2nd Qtr.

3rd Qtr.

4th Qtr.

Total

Total direct materials purchases

$ 5,430

$ 6,400

$ 7,400

$ 8,470

$ 27,700

Total

Cash Payments

Direct Materials:

Accounts Payable balance, 12/31/16

4,887

5,760

2nd Qtr. purchases, 10% paid in 3rd qtr.

3rd Qtr. purchases, 90% paid in 3rd qtr.

6,660

3rd Qtr. purchases, 10% paid in 4th qtr.

4th Qtr. purchases, 90% paid in 4th qtr.

7,623

Total payments for direct materials

15,887

6,303

7,300

8,363

$ 37,853

Direct Labor:

Total payments for direct labor

1,160

1,260

1,460

1,660

5,540

Manufacturing Overhead:

Variable manufacturing overhead

1,160

1,260

1,460

1,660

5,540

Utilities, insurance, property taxes

1,540

1,540

1,540

1,540

6,160

Total payments for mfg. overhead

2,700

2,800

3,000

3,200

11,700

Selling and Administrative Expenses:

Salaries Expense

8,500

8,500

8,500

8,500

34,000

Rent Expense

2,400

2,400

2,400

2,400

9,600

Insurance Expense

3,000

Supplies Expense

1,820

Total payments for S&A expenses

12,000

12,070

12,140

12,210

48,420

Income Taxes:

Total payments for income taxes

3,500

3,500

3,500

3,500

14,000

Capital Expenditures:

Total pmts. for capital expenditures

30,000

30,000

Total cash payments (before interest)

Accounts Payable balance, December 31, 2017:

4th Quarter, DM purchases, 10% paid in 1st quarter 2018

$ 847

24-57

Comprehensive Problem for Chapters 22-24, cont.

Requirement 1, cont.

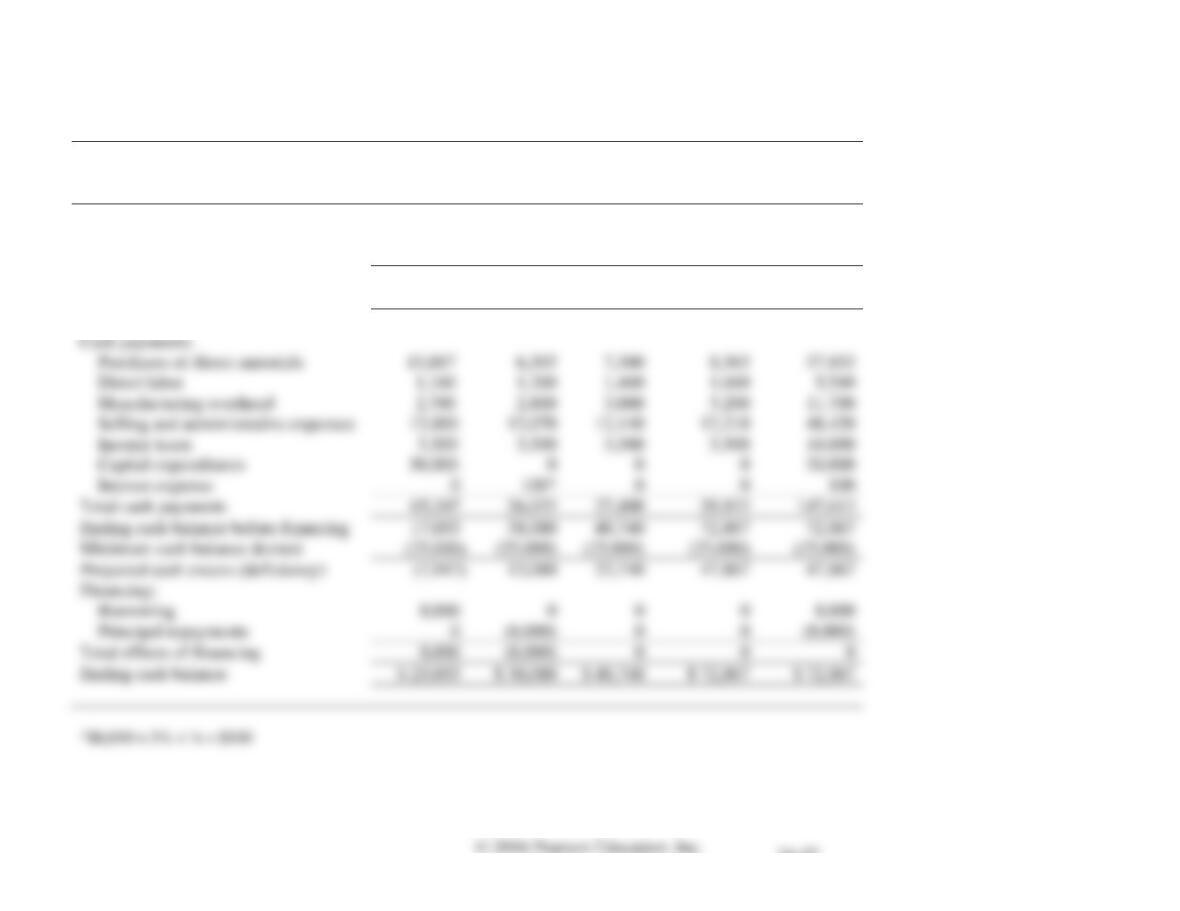

THOMPSON TOY COMPANY

Cash Budget

For the Year Ended December 31, 2017

First

Quarter

Second

Quarter

Third

Quarter

Fourth

Quarter

Total

Beginning cash balance

$ 27,000

$ 25,053

$ 30,080

$ 48,740

$ 27,000

Cash receipts

55,300

39,060

46,060

53,060

193,480

Cash available

82,300

64,113

76,140

101,800

220,480

Cash payments:

Purchases of direct materials

15,887

6,303

7,300

37,853

Direct labor

1,160

1,260

1,460

Manufacturing overhead

2,700

2,800

3,000

11,700

Selling and administrative expenses

12,070

12,140

12,210

48,420

Income taxes

3,500

3,500

14,000

Capital expenditures

0

0

0

30,000

Interest expense

0

0

Total cash payments

65,247

26,033

27,400

28,933

147,613

Ending cash balance before financing

17,053

38,080

48,740

72,867

72,867

Minimum cash balance desired

Projected cash excess (deficiency)

13,080

23,740

47,867

47,867

Financing:

Borrowing

8,000

0

0

0

Principal repayments

0

0

Total effects of financing

8,000

0

0

Ending cash balance

$ 25,053

$ 30,080

$ 48,740

$ 72,867

$ 72,867

24-58

Comprehensive Problem for Chapters 22-24, cont.

Requirement 2

THOMPSON TOY COMPANY

Budgeted Income Statement

For the Year Ended December 31, 2017

Sales Revenue

$ 182,000

Cost of Goods Sold

58,200

Gross Profit

Selling and Administrative Expenses

54,420

Operating Income

69,380

Interest Expense

100

Income Before Income Taxes

69,280

Income Tax Expense

14,000

Net Income

THOMPSON TOY COMPANY

Budgeted Balance Sheet

December 31, 2017

Assets

Current Assets:

Cash

Raw Materials Inventory

Finished Goods Inventory (270 sets at $22 each)

Total Current Assets

$ 103,327

Property, Plant, and Equipment:

Equipment ($177,000 + $30,000)

207,000

Less: Accumulated Depreciation ($39,000 + $16,000 + $6,000)

146,000

Total Assets

$ 249,327

Current Liabilities:

Accounts Payable

$ 847

Stockholders’ Equity

Common Stock

$ 100,000

Retained Earnings ($93,200 + $55,280 – $0)

148,480

Total Stockholders’ Equity

248,480

$ 249,327

24-59

Comprehensive Problem for Chapters 22-24, cont.

Requirement 2, cont.

THOMPSON TOY COMPANY

Budgeted Statement of Cash Flows

For the Year Ended December 31, 2017

Operating Activities:

Cash receipts from customers

$ 193,480

Cash payments for operating expenses*

(103,513)

Cash payments for interest expense

Cash payments for income taxes

Net cash provided by operating activities

Investing Activities:

Cash payments for equipment purchases

Net cash used for investing activities

Financing Activities:

Proceeds from issuance of notes payable

Payment of notes payable

Net cash provided by (used for) financing activities

Net increase in cash

Cash balance, January 1, 2017

27,000

Cash balance, December 31, 2017

$ 72,867

24-60

Comprehensive Problem for Chapters 22-24, cont.

Requirement 3

THOMPSON TOY COMPANY

Flexible Budget Performance Report

For the Year Ended December 31, 2017

1

2

(1) – (3)

3

4

(3) – (5)

5

Budget

Amounts

Per Unit

Actual

Results

Flexible

Budget

Variance

Flexible

Budget

Sales

Volume

Variance

Static

Budget

Units

3,000

3,000

2,600

Sales Revenue

$ 70.00

$ 210,000

$ 0

$ 210,000

$ 28,000

F

$ 182,000

Variable Costs:

Product Costs

42,720

U

U

36,040

S&A Costs

U

1,820

Contribution Margin

165,180

U

166,260

22,120

F

Fixed Costs:

Product Costs

F

22,160

S&A Costs

52,600

Operating Income

F

$ 22,120

F

Flexible Budget Variance Sales Volume Variance

24-61

Comprehensive Problem for Chapters 22-24, cont.

Requirement 6

The static budget is prepared for only one level of sales volume—the 2,600 sets expected to be sold—

and it doesn’t change after it is developed. The $23,200 favorable static budget variance is the difference

Requirement 7

Direct Materials Cost Variance

=

(AC ̶ SC)

×

AQ

=

($2.10 per pound – $2.00 per pound)

×

14,750 pounds

=

$1,475 U

Direct Materials Efficiency Variance

=

×

=

×

$2.00 per pound

=

$500 F

=

(10.50 per DLHr – $10.00 per DLHr)

×

=

$290 U

Direct Labor Efficiency Variance

=

(AQ ̶ SQ)

×

SC

=

×

$10.00 per DLHr

=

$200 F

24-62

Comprehensive Problem for Chapters 22-24, cont.

Requirement 8

VOH Cost Variance

=

(AC ̶ SC)

×

AQ

=

($9.75 per DLHr – $10.00 per DLHr)

×

580 DLHr

=

$145 F

VOH Efficiency Variance

=

(AQ ̶ SQ)

×

SC

=

×

$10.00 per DLHr

=

$200 F

=

=

$2,160 F

=

=

=

$1,840 F

24-63

Comprehensive Problem for Chapters 22-24, cont.

Requirement 9

THOMPSON TOY COMPANY

Standard Cost Income Statement

For the Year Ended December 31, 2017

Sales Revenue at standard ($70/set × 3,000 sets)

$ 210,000

Cost of Goods Sold at standard ($22 per set × 3,000 sets)

$ 66,000

Manufacturing Cost Variances (from Req. 7 and 8):

Direct Materials Cost Variance

$ 1,475

Direct Materials Efficiency Variance

Direct Labor Cost Variance

Direct Labor Efficiency Variance

Variable Overhead Cost Variance

Variable Overhead Efficiency Variance

Fixed Overhead Cost Variance

Fixed Overhead Volume Variance

Cost of Goods Sold at actual

Gross Profit

Selling and Administrative Expenses:

Variable

Fixed

Operating Income

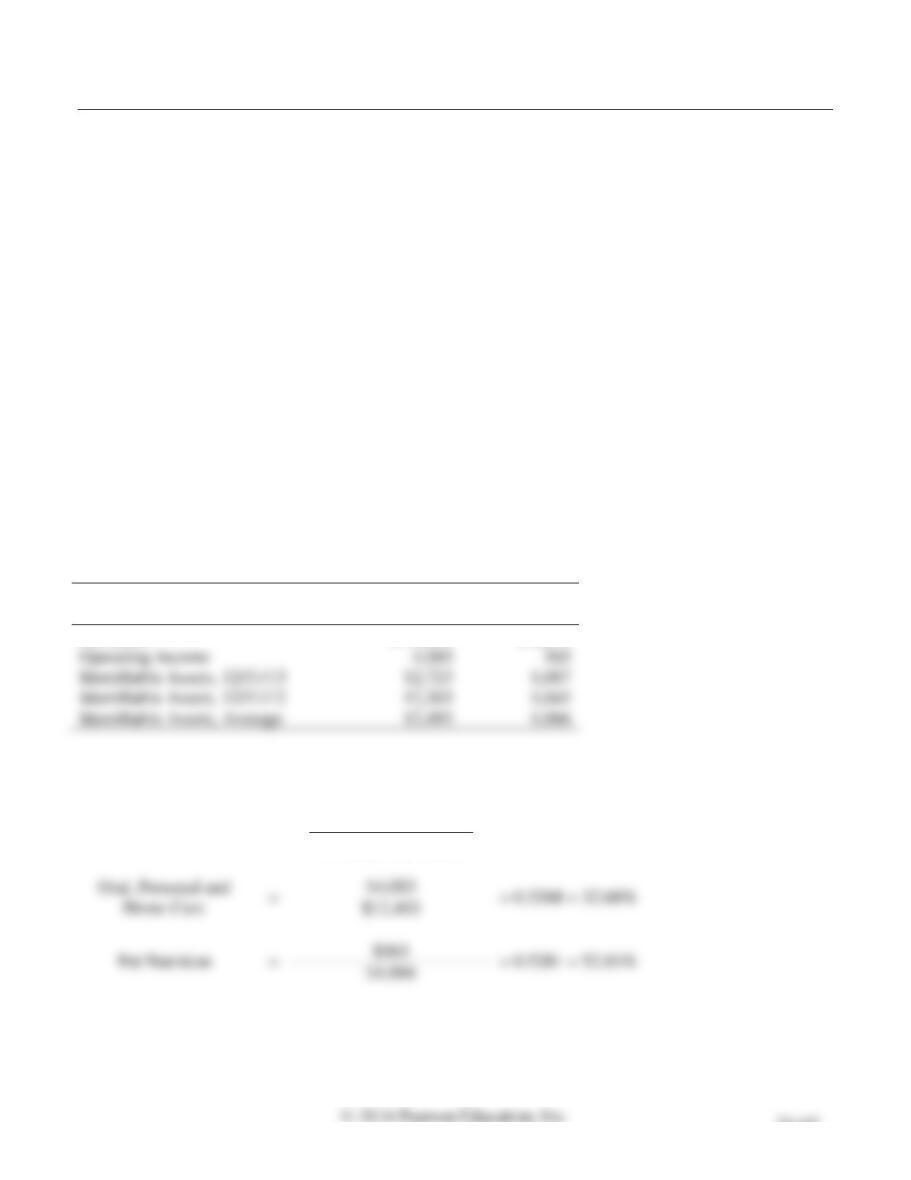

Requirement 10

ROI

=

Operating Income

Average total assets

24-64

Comprehensive Problem for Chapters 22-24, cont.

Requirement 11

Profit margin ratio

=

Operating income

Net sales

Requirement 12

Asset turnover ratio

=

Net sales

Average total assets

$210,000

Requirement 13

Profit margin

ratio

×

Asset turnover

ratio

=

ROI

0.4083 = 40.83%

Requirement 14

RI

=

Operating income

–

(Target rate of return × Average total assets)

–

–

24-65

Critical Thinking

Decision Case 24-1

Colgate-Palmolive Company operates two product segments. Go to the company Web site

(http://www.colgatepalmolive.com), and then click on the “For Investors” link. From there, go to the

SEC filings and select “10–K reports.” Select the Annual Report filed February 20, 2014, for the year

ended December 31, 2013. The necessary information will be in Note 15 (pages 86–89).

Requirements

1. What are the two product segments? Gather data about each segment’s net sales, operating income,

and identifiable assets for 2013.

2. Calculate ROI for each segment for 2013.

3. Which segment has the highest ROI? Explain why.

4. If you were on the top management team and could allocate extra funds to only one division, which

division would you choose? Why?

SOLUTION

Requirement 1

The information is from the 2013 Annual Report. All dollar amounts are in millions. The two segments

are Oral, Personal and Home Care and Pet Nutrition.

Oral, Personal

and Home Care

Pet Nutrition

Net Sales

$ 15,209

$ 2,211

Operating Income

Identifiable Assets, 12/31/13

Identifiable Assets, 12/31/12

Identifiable Assets, Average

Requirement 2

ROI

=

Operating income

Average total assets

=

= 0.3268 = 32.68%

=

24-66

Decision Case 24-1, cont.

Requirement 3

The Pet Nutrition Division has a much higher ROI than the Oral, Personal and Home Care Division. By

expanding the ROI calculation, it appears they both have about the same profit margin ratio, but the Pet

Nutrition Division generates more sales from its identifiable assets. Therefore, the Pet Nutrition Division

is more efficient in using its assets and has a higher ROI.

Profit margin ratio

=

Operating income

Net sales

=

Asset turnover ratio

=

Net sales

Average total assets

=

Requirement 4

The management team would most likely choose to allocate additional funds to the Pet Nutrition

24-67

Ethical Issue 24-1

Dixie Irwin is the department manager for Religious Books, a manufacturer of religious books that are

sold through Internet companies. Irwin’s bonus is based on reducing production costs.

Irwin has identified a supplier, Cheap Paper, that can provide paper products at a 10% cost reduction.

The paper quality is not the same as that of the current paper used in production. If Irwin uses the

supplier, she will certainly achieve her personal bonus goals; however, other company goals may be in

jeopardy. What is the ethical issue? Identify the key performance issues at risk, and recommend a plan

of action for Irwin.

SOLUTION

Irwin’s ethical issue is deciding if she should do what will benefit her the most personally or do what is

best for the company as a whole. Irwin’s bonus is based on reducing production costs. The purchase of

Fraud Case 24-1

Everybody knew Ed McAlister was a brilliant businessman. He had taken a small garbage collection

company in Kentucky and built it up to be one of the largest and most profitable waste management

companies in the Midwest. But when he was convicted of a massive financial fraud, what surprised

Requirements

1. If an asset has either too long a useful life or too high an estimated salvage value, what happens,

from an accounting perspective, when that asset is worn out and has to be disposed of?

24-68

SOLUTION

Requirement 1

When an asset is disposed of, any remaining net book value must be reported as a loss, which will

decrease income. If the estimated useful life is too long, or the salvage value unrealistically high, the

Requirement 2

GAAP does not mandate specific lives for assets. Companies are expected to estimate useful lives and

salvage values that are reasonable and realistic for the assets involved. Outside auditors have a

Requirement 3

If the useful life is too long or the salvage value of an asset is too high, the book value of the assets on

the balance sheet will be overstated. Also, operating income will be overstated due to the depreciation

Team Project 24-1

Each group should identify one public company’s product to evaluate. The team should gather all the

information it can about the product.

Requirement

Develop a list of key performance indicators for the product.

SOLUTION

24-69

Communication Activity 24-1

In 150 words or fewer, list each of the four perspectives of the balanced scorecard. Give an example of

one KPI from each of the perspectives, and explain what measure the KPI provides for a retailing

business.

SOLUTION

Student answers will vary. Key items to look for are:

Perspective

Strategy

Common Key Performance Indicators (KPIs)

Financial

Increase company profits

through increasing revenue

growth and productivity

• Net income

• Sales revenue growth

• Gross margin growth

• Cash flow

• Return on investment

• Residual income

Customer

Improve customer

satisfaction for long-term

• Customer satisfaction ratings

• Percentage of market share