CHAPTER 24

Budgetary Control and Responsibility Accounting

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

B

Problems

1. Describe budgetary

control and static budget

reports.

1, 2, 3, 4, 5

1, 2

1, 2, 8,4, 9

3A

3B

2. Prepare flexible budget

reports.

6, 7, 8, 9, 10,

11, 12

3, 4, 5

1, 2

1, 3, 4, 5,

6, 7, 8, 9,

10, 11, 12

1A, 2A, 3A

1B, 2B, 3B

3. Apply responsibility

accounting and to cost

and profit centers.

13, 14, 15, 16,

17, 18, 19, 20,

21, 24

6, 7

3

10, 11, 13,

14, 15, 16

4A, 6A

4B, 6B

4. Evaluate performance in

investment centers.

22, 23, 24

8, 9, 10

4

16, 17,

18, 19

5A

5B

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Prepare flexible budget and budget report for manufacturing

overhead.

Simple

20–30

2A

Prepare flexible budget, budget report, and graph for

manufacturing overhead.

Moderate

30–40

3A

State total budgeted cost formula, and prepare flexible

budget reports for two time periods.

Simple

20–30

4A

Prepare responsibility report for a profit center.

Moderate

20–30

5A

Prepare responsibility report for an investment center,

and compute ROI.

Moderate

40–50

6A

Prepare reports for cost centers under responsibility

accounting, and comment on performance of managers.

Moderate

40–50

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End–of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

1. Describe budgetary control

and static budget reports.

E24-1

Q24-1

Q24-2

Q24-3

Q24-4

Q24-5

BE24-1 E24-2

BE24-2 E24-9

P24-3A

E24-8

2. Prepare flexible budget

reports.

Q24-9

Q24-12

E24-1

Q24-6

Q24-7

Q24-8

Q24-10

Q24-11

BE24-4

DI24-1

DI24-2

E24-3

E24-5

E24-7

E24-9

E24-10

E24-11

E24-12

BE24-5

E24-4

E24-6

P24-1A

P24-3A

P24-1B

BE24-3

E24-8

P24-2A

3. Describe responsibility

accounting and apply it to

cost centres and profit

centres.

Q24-19

Q24-13

Q24-14

Q24-15

Q24-16

Q24-17

Q24-18

Q24-20

Q24-21

Q24-24

BE24-6

BE24-7

DI24-3

E24-10

E24-11

E24-13

E24-16

P24-6A

E24-14

E24-15

P24-4A

4. Evaluate performance in

investment centers.

Q24-22

Q24-23

Q24-24

BE24-8

BE24-9

BE24-10

DI24-4

E24-16

E24-17

E24-18

E24-19

P24-5A

Broadening Your Perspective

BYP24-4

BYP24-3

BYP24-5

BYP24-6

BYP24-1

BYP24-2

BYP24-7

BYP24-8

ANSWERS TO QUESTIONS

1. (a) Budgetary control is the use of budgets in controlling operations.

(b) The steps in budgetary control are:

(1) Develop the planned objectives (budget).

(2) Analyze differences between actual and budgeted results.

(3) Take corrective action.

(4) Modify future plans, if necessary.

2.

Purpose

Name of Report

Frequency

Primary Recipient(s)

(a)

Scrap

Daily

Production manager

4. There is no justification for Ken’s concern. The sales budget is derived from the sales forecast

and it represents management’s best estimate of sales. Thus, it is a useful basis for evaluating

sales performance.

5. A static budget is an appropriate basis for evaluating a manager’s effectiveness in controlling

costs when:

7. The performance is unfavorable. The budgeted indirect labor cost in the static budget is $1.35 per

direct labor hour ($54,000 ÷ 40,000). At 45,000 direct labor hours, budgeted costs are $60,750

(45,000 X $1.35). Thus, indirect labor is $3,250 over budget ($64,000 – $60,750).

10. Cali Company can say that total budgeted costs are $20,000 fixed plus $6.50 per direct labor

hour [($85,000 – $20,000) ÷ 10,000].

Questions Chapter 24 (Continued)

12. Management by exception means that top management’s review of a budget report is focused

either entirely or primarily on differences between actual results and planned objectives. The

criteria for identifying exceptions are materiality and controllability of the item.

13. Responsibility accounting is a method of controlling operations that involves accumulating and

reporting costs (and revenues, where relevant) on the basis of the manager who has the authority

to make the day-to-day decisions about the items. The purpose of responsibility accounting is to

evaluate a manager’s performance on the basis of matters directly under that manager’s control.

14. Eve should know that the following conditions contribute to the effective use of responsibility

accounting:

15. A cost is controllable at a given level of managerial responsibility if the manager has the power to

incur the cost within a given period of time. Most costs incurred directly are controllable, whereas costs

incurred indirectly and allocated to a responsibility level are noncontrollable at that level.

16. Responsibility reports differ from budget reports in two respects: (1) a distinction is made between

controllable and noncontrollable items and (2) performance reports either emphasize, or only

include, items controllable by the individual manager.

17. Usually there is a relationship between a responsibility reporting system and a company’s organization

chart. In a responsibility reporting system, reports are prepared for each level of responsibility in the

organization chart.

20. Direct fixed costs relate specifically to one center and are incurred for the sole benefit of that

center. An indirect fixed cost relates to the company’s overall activities and is incurred for the

benefit of more than one profit center. Both types of fixed costs are controllable. A direct fixed

Questions Chapter 24 (Continued)

22. The primary basis for evaluating the performance of the manager of an investment center is

return on investment (ROI). The formula is: Controllable Margin divided by Average Operating Assets.

23. ROI can be improved by: (1) increasing controllable margin and (2) reducing average operating

assets. Controllable margin can be increased by increasing sales or by reducing variable and

controllable fixed costs.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 24-1

CROIX COMPANY

Sales Budget Report

For the Quarter Ended March 31, 2017

Product Line

Budget

Actual

Difference

Garden-Tools

BRIEF EXERCISE 24-2

CROIX COMPANY

Sales Budget Report

For the Quarter Ended June 30, 2017

Second Quarter

Year to Date

Product Line

Budget

Actual

Difference

Budget

Actual

Difference

BRIEF EXERCISE 24-3

(a) ROONEY COMPANY

Static Direct Labor Budget Report

For the Month Ended January 31, 2017

Budget

Actual

Difference

(b) ROONEY COMPANY

Flexible Direct Labor Budget Report

For the Month Ended January 31, 2017

Budget

Actual

Difference

BRIEF EXERCISE 24-3 (Continued)

The static budget does not provide a proper basis for evaluating performance

because the budget is not based on the hours actually worked. In contrast,

BRIEF EXERCISE 24-4

GUNDY COMPANY

Monthly Flexible Manufacturing Budget

For the Year 2017

Activity level

Finished units

Variable costs

Direct materials ($5)

Direct labor ($6)

80,000

$ 400,000

480,000

100,000

$ 500,000

600,000

120,000

$ 600,000

720,000

BRIEF EXERCISE 24-5

GUNDY COMPANY

Manufacturing Flexible Budget Report

For the Month Ended March 31, 2017

Budget

Actual

Difference

Units produced

Variable costs

Direct materials

100,000

$ 500,000

100,000

$ 520,000

Favorable F

Unfavorable U

$20,000 U

BRIEF EXERCISE 24-6

HANNON COMPANY

Assembly Department

Manufacturing Overhead Cost Responsibility Report

For the Month Ended April 30, 2017

Controllable Cost

Budget

Actual

Difference

Indirect materials

Indirect labor

$16,000

20,000

$14,300

20,600

Favorable F

Unfavorable U

$1,700 F

600 U

BRIEF EXERCISE 24-7

TORRES COMPANY

Water Division

Responsibility Report

For the Year Ended December 31, 2017

Budget

Actual

Difference

Sales

Variable costs

$2,000,000

1,000,000

$2,080,000

1,050,000

Favorable F

Unfavorable U

$80,000 F

50,000 U

BRIEF EXERCISE 24-8

COBB COMPANY

Plastics Division

Responsibility Report

For the Year Ended December 31, 2017

Budget

Actual

Difference

Contribution margin

$700,000

$710,000

Favorable F

Unfavorable U

$10,000 F

BRIEF EXERCISE 24-9

III 28% ($1,400,000 ÷ $5,000,000)

BRIEF EXERCISE 24–10

III A $300,000 ($2,000,000 X .15) increase in sales will increase contribution

margin and controllable margin $210,000 ($300,000 X 70%). The new

ROI is 32.2% ($1,610,000 ÷ $5,000,000).

SOLUTIONS FOR DO IT! EXERCISES

DO IT! 24-1

Difference

Favorable F

Unfavorable U

Budget

Actual

Units produced

Variable costs

Direct materials ($7)

$ 42,000

$ 38,850

$3,150 F

Direct labor ($13)

78,000

76,440

1,560 F

Overhead ($18)

108,000

116,640

8,640 U

Total variable costs

Fixed costs

Depreciation*

Supervision**

3,800

200 U

Total fixed costs

Total costs

$239,800

$243,930

$4,130 U

The static budget indicates that actual variable costs exceeded budgeted

amounts by $3,930. Fixed costs were unfavorable by $200. The static

budget gives the impression that the company did not control its variable

DO IT! 24-2

Using the graph data, fixed costs are $90,000, and variable costs are $5.20

DO IT! 24-3

ROCKIES DIVISION

Responsibility Report

For the Year Ended December 31, 2017

Difference

Favorable F

Budget Actual Unfavorable U

Sales $2,000,000 $1,890,000 $110,000 U

Variable costs 800,000 760,000 40,000 F

DO IT! 24-4

(a) Controllable margin for 2017:

Sales ……………………………………………..

$500,000

Variable costs ………………………………..

300,000

Contribution margin ……………………….

Controllable fixed costs ………………….

75,000

Controllable margin ………………………..

(b) Expected return on investment for alternative 1:

$125,000*

DO IT! 24-4 (Continued)

Controllable margin for alternative 2:

Sales ($500,000 + 100,000) ……………………….

$600,000

Contribution margin ………………………………..

Variable costs

SOLUTIONS TO EXERCISES

EXERCISE 24-1

1. True.

2. False. Budget reports are prepared as frequently as needed.

3. True.

EXERCISE 24-2

(a) CREDE COMPANY

Selling Expense Report

For the Quarter Ending March 31

By Month

Year–to–Date

Month

Budget

Actual

Difference

Budget

Actual

Difference

January

$30,000

$31,200

$1,200 U

$ 30,000

$ 31,200

$1,200 U

February

$35,000

$34,525

$ 475 F

$ 65,000

$ 65,725

$ 725 U

March

$40,000

$46,000

$6,000 U

$105,000

$111,725

$6,725 U

EXERCISE 24-3

MYERS COMPANY

Monthly Manufacturing Overhead Flexible Budget

For the Year 2017

Activity level

Direct labor hours

Variable costs

Indirect labor ($1)

Indirect materials ($.70)

7,000

$ 7,000

4,900

8,000

$ 8,000

5,600

9,000

$ 9,000

6,300

10,000

$10,000

7,000

EXERCISE 24-4

(a) MYERS COMPANY

Manufacturing Overhead Flexible Budget Report

For the Month Ended July 31, 2017

Difference

Direct labor hours (DLH)

Variable costs

Indirect labor

Budget at

9,000 DLH

$ 9,000

Actual Costs

9,000 DLH

$ 8,800

Favorable F

Unfavorable U

$200 F

EXERCISE 24-4 (Continued)

(b) MYERS COMPANY

Manufacturing Overhead Flexible Budget Report

For the Month Ended July 31, 2017

Difference

Direct labor hours (DLH)

Variable costs

Indirect labor ($1.00)

Indirect materials ($0.70)

Budget at

8,500 DLH

$ 8,500

5,950

Actual Costs

8,500 DLH

$ 8,800

5,800

Favorable F

Unfavorable U

$300 U

150 F

(c) In case (a) the performance for the month was satisfactory. In case

(b) management may need to determine the causes of the differences

EXERCISE 24-5

FALLON COMPANY

Monthly Selling Expense Flexible Budget

For the Year 2017

Activity level

Sales

Variable expenses

Sales commissions (6%)

Advertising (4%)

Fixed expenses

Sales salaries

$170,000

$ 10,200

6,800

35,000

$180,000

$ 10,800

7,200

35,000

$190,000

$ 11,400

7,600

35,000

$200,000

$ 12,000

8,000

35,000

EXERCISE 24-6

(a) FALLON COMPANY

Selling Expense Flexible Budget Report

For the Month Ended March 31, 2017

Difference

Sales

Variable expenses

Sales commissions

Advertising

Budget

$170,000

$ 10,200

6,800

Actual

$170,000

$ 11,000

6,900

Favorable F

Unfavorable U

$800 U

100 U

EXERCISE 24-6 (Continued)

(b) FALLON COMPANY

Selling Expense Flexible Budget Report

For the Month Ended March 31, 2017

Difference

Sales

Variable expenses

Sales commissions

Advertising

Fixed costs

Sales salaries

Depreciation

Budget

$180,000

$ 10,800

7,200

35,000

7,000

Actual

$180,000

$ 11,000

6,900

35,000

7,000

Favorable F

Unfavorable U

$200 U

300 F

0 U

0 U

(c) Flexible budgets are essential in evaluating a manager’s performance

in controlling variable expenses because the budget allowance varies

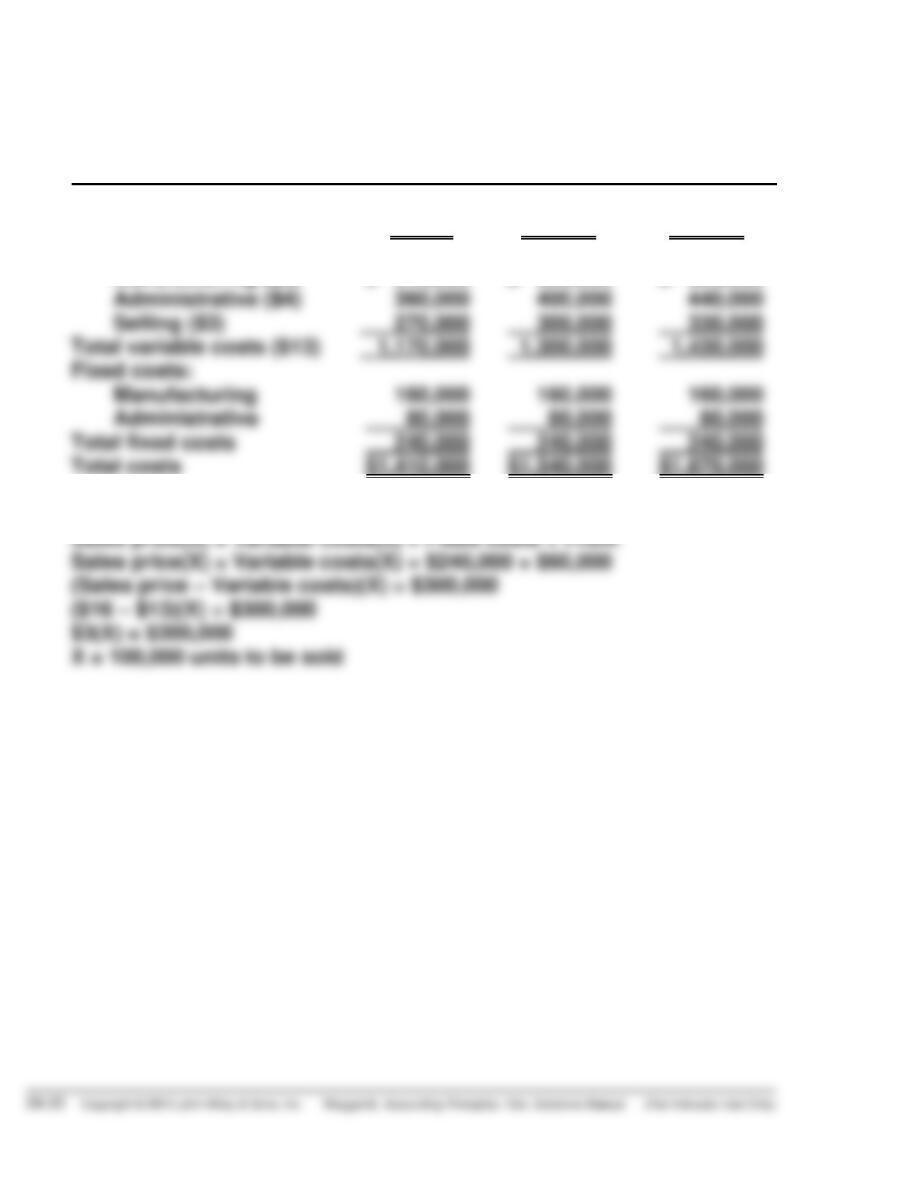

EXERCISE 24-7

(a) APPLIANCE POSSIBLE INC.

Flexible Production Cost Budget

Activity level

Production levels 90,000 100,000 110,000

Variable costs:

Manufacturing ($6) $ 540,000 $ 600,000 $ 660,000

(b) Let (X) represent number of units

Sales price(X) = Variable costs(X) + Fixed costs + Profit

Sales price(X) = Variable costs(X) + $240,000 + $60,000