g.

844,920

h.

Overhead Spending Variance (favorable) ………………………………………

Overhead Volume Variance (favorable) ………………………………………….

Cost of Goods Sold ……………………………………………………

To close overhead variances to Cost of Goods Sold.

PROBLEM 24.4B

HANS ENTERPRISES (concluded)

Entry to close overapplied overhead to cost of goods sold:

Entry to transfer the 160 batches of crow bait produced in June to finished goods:

Finished Goods Inventory (at standard cost) …………………………………..

Work in Process Inventory (at standard cost) …………………………………….

To transfer 160 batches of crow bait to finished goods in June.

a. =

=

b. =

=

8,300 hours × ($15 – $14)

*Standard Hours Allowed = 10,000 cases × 0.80 hours/case = 8,000 hours

$8,300 Favorable

$15 per hour × (8,000 hours* – 8,300 hours)

-$4,500 (or $4,500 Unfavorable)

45 Minutes, Strong

Actual Quantity Used × (Standard Price – Actual Price)

34,000 gallons × ($1.32 – $1.28*)

Materials Price Variance

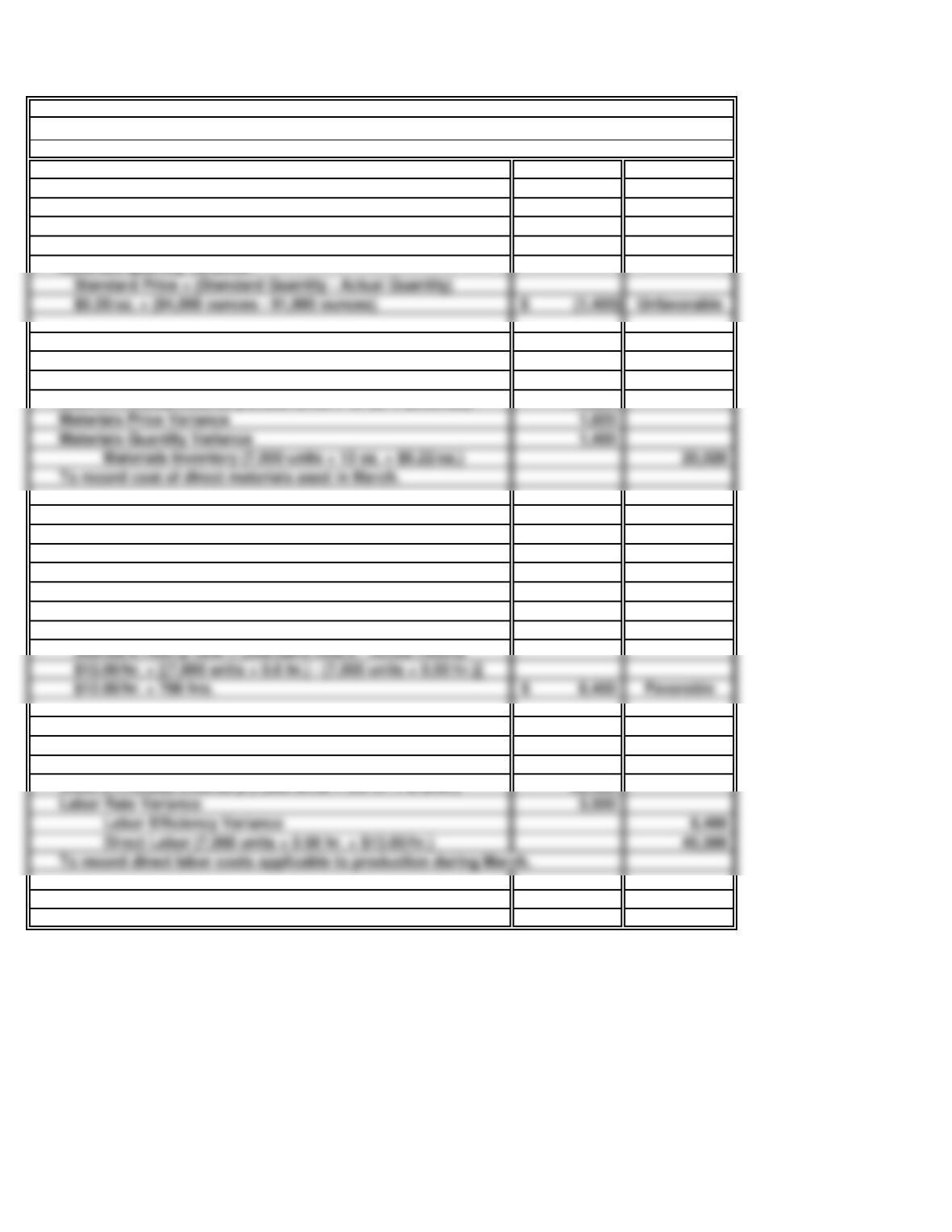

PROBLEM 24.5B

SMOOTH CORPORATION

Actual Labor Hours × (Standard Rate – Actual Rate)

Labor Rate Variance

$1,360 Favorable

*Actual Price per Pound = $43,520 ÷ 34,000 gallons = $1.28/gallon

-$5,280 (or $5,280 Unfavorable)

*Standard Quantity Allowed = 10,000 cases × 3.0 gallons/case = 30,000 gallons

c.

$ 5,252

d. (1) 39,600 *

Materials Quantity Variance (unfavorable) ……………………………………….

Materials Price Variance (favorable) ………………………………………………………….

Direct Materials Inventory (at actual cost) ……………………………………………………

To record the cost of direct materials charged to production.

(2) 120,000 *

4,500

Overhead Volume Variance (unfavorable) ……………………………………………

Manufacturing Overhead (at actual cost) …………………………………………………………

Overhead Spending Variance (favorable) ……………………………………………………….

To apply overhead to production.

Direct Labor (at actual cost) ………………………………………………………………………

Work in Process Inventory (at standard cost) …………………………………….

To record the cost of direct labor charged to production.

(4) 180,800

To transfer 10,000 cases to finished goods in June.

Overhead Volume Variance (unfavorable) ………………………………………………………

Cost of Goods Sold ………………………………………………………………………………..

Overhead Spending Variance (favorable) …………………………………..

PROBLEM 24.5B

SMOOTH CORPORATION (concluded)

Overhead variances:

$ 4,500

Costs Allowed

Fixed

Overhead

Costs Applied

Actual Overhead

Costs Incurred

Standard Overhead

Fixed

Work in Process Inventory (at standard cost) …………………………………..

8,300

Labor Rate Variance (favorable) …………………………………………………………………..

Work in Process Inventory (at standard cost) …………………………………………

Labor Efficiency Variance (unfavorable) ………………………………………

Finished Goods Inventory (at standard cost) ………………………………….

Work in Process Inventory (at standard cost) …………………………………………………

180,800*

40 Minutes, Strong PROBLEM 24.6B

MONOGLUT, INC.

a. Materials price variance:

Actual Quantity × (Standard Price – Actual Price)

(7,000 units × 13 ounces) × ($0.20/oz. – $0.22/oz.) (1,820)$ Unfavorable

Materials quantity variance:

Journal entry to record direct materials used in March:

Work in Process Inventory (7,000 units × 12 oz. × $0.20/oz.) 16,800

b. Labor rate variance:

Actual Hours × (Standard Hourly Rate – Actual Hourly Rate)

(7,000 units × 0.50 hr.) × ($12.00/hr. – $13.00/hr.) (3,500)$ Unfavorable

Labor efficiency variance:

Journal entry to record direct labor cost for March:

Work in Process Inventory (7,000 units × 0.6 hr. × $12/hr.) 50,400

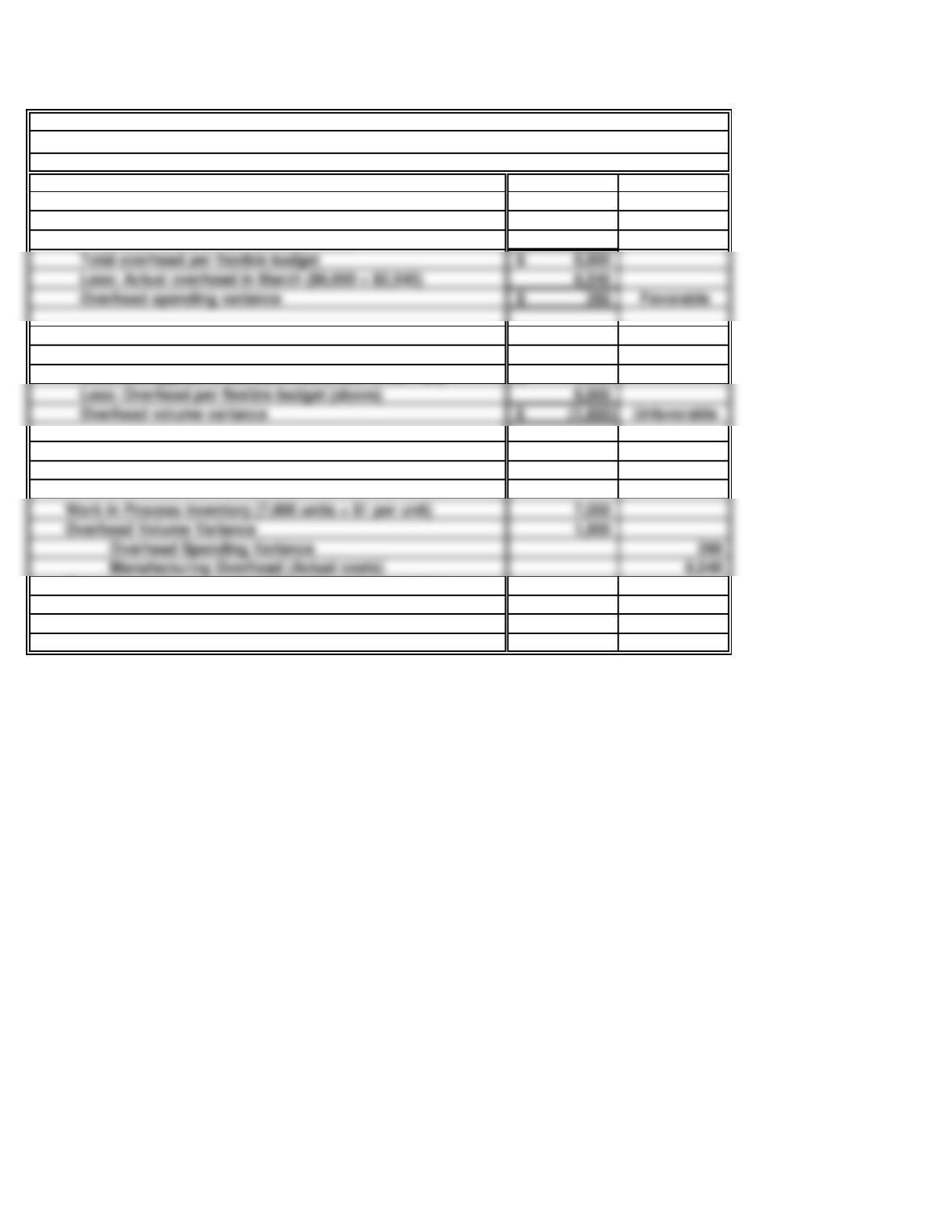

c. Overhead spending variance:

Overhead per flexible budget—7,000 units:

Fixed 6,000$

Variable (7,000 units × $0.40 per unit) 2,800

Overhead volume variance:

Overhead applied at standard cost (7,000 units × $1) 7,000$

Journal entry to record overhead applied to work in process:

To apply overhead cost to 7,000 units produced at the

standard rate of $1 per unit.

PROBLEM 24.6B

MONOGLUT, INC. (concluded)

PROBLEM 24.7B

COLONIAL FURNITURE CO.

a. (1)

(2)

$1.50/ft. × -9,000 ft.

Standard Price × (Standard Quantity – Actual Quantity)

-$13,500 (or $13,500 Unfavorable)

$1.50/ft. × [(1,800 units × 100 ft.) – (189,000 ft.)]

(3)

Actual Hours × (Standard Hourly Rate – Actual Hourly Rate)

(1,800 units × 4.5 hrs.) × ($10.00/hr. – $9.00/hr.)

8,100 hrs. × $1.00

$8,100 Favorable

(4)

Overhead variances are computed on the following page.

-$9,000 (or $9,000 Unfavorable)

$10.00/hr. × -900 hours

Standard Hourly Rate × (Standard Hours – Actual Hours)

$10.00/hr. × [(1,800 units × 4 hrs.) – (1,800 units × 4.5 hrs.)]

40 Minutes, Strong

Computation of materials price variance (MPV):

Computation of labor efficiency variance (LEV):

Computation of labor rate variance (LRV)

Computation of materials quantity variance (MQV):

$18,900 Favorable

Actual Quantity Used × (Standard Price – Actual Price)

(1,800 units × 105 ft.) × ($1.50/ft. – $1.40/ft.)

189,000 ft. × $0.10

(5) Computation of overhead spending variance:

Overhead per flexible budget for 800 units:

Fixed 20,000$

b.

General Journal

May 31 Work in Process Inventory (at standard) 270,000

Materials Quantity Variance 13,500

Materials Price Variance 18,900

Materials Inventory (at actual) 264,600

To record direct materials used during May.

Standard cost = 1,800 units @ $150 = $270,000

Actual cost = 1,800 units @ $147 = $264,600

31 Work in Process Inventory (at standard) 72,000

Labor Efficiency Variance 9,000

Labor Rate Variance 8,100

Direct Labor (actual cost) 72,900

To charge May production with direct labor cost.

Standard cost = 1,800 units @ $40.00 = $72,000

Actual cost = 1,800 units @ $40.50 = $72,900

31 Work in Process Inventory (at standard) 32,400

Volume Variance 2,000

Overhead Spending Variance 200

Manufacturing Overhead (actual cost) 34,200

To charge overhead to production at standard cost.

Standard cost = 1,800 units @ $18.00 = $32,400

Actual cost = $34,200

PROBLEM 24.7B

COLONIAL FURNITURE CO. (continued)

Variable (1,800 units × $8.00 per unit) 14,400 34,400$

Less: Actual overhead for the month 34,200

Overhead spending variance (favorable) 200$

(6) Computation of volume variance:

Overhead applied using standard cost

($1,800 units × $18 per unit) 32,400$

Overhead per flexible budget for 1,800 units

(computed above) 34,400

Volume variance (unfavorable) (2,000)$

PROBLEM 24.7B

COLONIAL FURNITURE CO. (concluded)

c.

The company appears to be having significant problems in two areas. First, the large

unfavorable materials quantity variance ($13,500) indicates that far more material is being

used in the production process than is provided for in the cost standards. Assuming that the

The company had two significantly favorable variances: (1) the material price variance, and

(2) the labor rate variance. The favorable price variance may indicate that the purchasing

Comments on cost variances:

a.

b.

c.

d.

Standard Hourly Rate × (Standard Hours – Actual

60 Minutes, Strong

PROBLEM 24.8B

FODING CORPORATION

Based on the journal entry to charge direct materials costs to work in process, the actual

quantity of material purchased and used during May is determined as follows:

Based on the journal entry to charge direct material costs to work in process, the standard

quantity of material allowed for the actual level of output achieved in May is determined

as follows:

Based on the journal entry to charge direct labor costs to work in process, the standard

direct labor hours allowed during May is determined as follows:

Based on the journal entry to charge direct labor costs to work in process, the average per

hour labor cost incurred in May is determined as follows:

e.

f. 72,500

72,500*

PROBLEM 24.8B

FODING CORPORATION (concluded)

$25,000

Thus, standard overhead costs allowed for in May of $22,000 can be computed as follows:

Based on the journal entry to charge overhead costs to work in process, the following

relationships exist:

Finished Goods Inventory (at standard cost) …………………………………….

Work in Process Inventory (at standard cost) …………………………………………………..

To transfer cost of completed units to finished goods.

Materials Price Variance (favorable) ……………………………………………..

Direct Labor Rate Variance (unfavorable) …………………………………………………………

Materials Quantity Variance (unfavorable) ………………………………………………………..

Overhead Volume Variance (favorable) …………………………………….

Cost of Goods Sold ………………………………………………………….

Direct Labor Efficiency Variance (unfavorable) …………………………………………………………..

Overhead Spending Variance (unfavorable) …………………………………………………………………

To close the cost variance accounts.

a.

c. =

=

=

=

$ 900

Fixed overhead allowed ($4 × 225 units) …………………………………………………………

500

$ 1,400

PROBLEM 24.9B

NINNA COMPANY

45 Minutes, Medium

Since the direct materials quantity variance is $0, the actual quantity of materials used

per shelf must equal the budgeted quantity per shelf. Thus the total quantity purchased

and used is:

$200

.50 hours per unit × 250 units × ($12 per hour – actual

rate)

Labor Rate Variance

$200 (Favorable)

125 hours × ($12 per hour – actual rate)

Actual Labor Hours × (Standard Rate – Actual Rate)

Total overhead allowed …………………………………………………………………………

Variable overhead allowed ($2 × 250 units) ……………………………………………………

250 shelves × 4 square feet per shelf = 1,000 square feet.

1,000 sq. ft. × ($0.20 – actual price)/sq. ft.

Actual Quantity Used × (Standard Price – Actual Price)

Standard Hourly Rate × (Standard Hours – Actual

$12 × (.4 hours per unit – actual hours per unit) × 250

SOLUTIONS TO CRITICAL THINKING CASES

CASE 24.1

IT’S NOT MY FAULT

CABINETS, INC.

a.

b.

25 Minutes, Strong

The basic problem is that the production manager is being unfairly charged with cost

overruns that should be assigned to the sales department. If we assume that filling the large

The production manager should not be penalized by the extra direct labor costs incurred

when the production department is asked to produce beyond normal capacity. The extra

costs relating to overtime should be considered a “normal” cost of the “rush” order and,

a.

b.

Revised

Standard

Cost

per Unit

$ 0.70

Material X-2, 100,000 pounds @ $0.50 …………….

Finished goods:

Material X-1, 200,000 ounces @ $0.70 …………….

Revised schedule of inventory at the end of the year:

Materials:

CASE 24.2

The president is not correct in arguing that the standard costs for Tough-Coat should not

be revised for purposes of valuing the inventory at the end of the year. The standards set

50 Minutes, Strong

ARMSTRONG CHEMICAL

Material X-1 ($840,000 ÷ 1,200,000 ounces purchased) ………………

0.50

1.40

$ 3.48

Total revised cost per unit …………………………………………….

Factory overhead (No change required) ………………………………..

Material X-2 (No change required) …………………………………….

CASE 24.2

c.

d. (1)

(2)

(1,000,000 units × $1.40) – $1,400,000

Actual Quantity Used × (Standard Price – Actual Price)

$0

Standard Labor Cost – Actual Labor Cost

(1,000,000 units × $0.80) – $880,000

1,050,000** pounds × ($0.50/lb. – $0.50/lb.)

0

$0.50 × (1,000,000 lbs. – 1,050,000** lbs.)

Standard Price × (Standard Quantity – Actual Quantity)

Materials quantity variance (MQV) for X-2:

Materials price variance (MPV) for X-2:

Materials price variance (MPV) for X-1:

As the schedule above indicates, the ending inventory would be reduced from $560,000

ARMSTRONG CHEMICAL (concluded)

$1.00/ounce × (1,000,000 ounces – 1,000,000* ounces)

*$1,200,000 oz. purchased – 200,000 oz. in ending inventory

Materials quantity variance (MQV) for X-1:

Actual Quantity Used × (Standard Price – Actual Price)

1,000,000* ounces × ($1.00/oz. – $0.70/oz.)

$300,000 Favorable

Standard Price × (Standard Quantity – Actual Quantity)

30 Minutes, Medium

CASE 24.3

TRAVELOCITY.COM

INTERNET

b.

The reasonableness of the standard will be affected by current airline pricing policies and

30 Minutes, Medium

CASE 24.4

STANDARD COST SYSTEM

AND INVENTORY MISSTATEMENT

JAMS AND JELLIES, INC.

a.

b.

•

Buck appears to be attempting to increase the factory’s profit by closing the material favorable

The IMA code of ethics suggests the following procedure to resolve ethical conflicts:

follow your organization’s established policies on the resolution of such conflict. If these policies

do not resolve the ethical conflict, Sheila should consider the following courses of action:

Sheila should discuss the issue with her immediate supervisor except when it appears that the

supervisor is involved. In that case, present the issue to the next level. If she cannot achieve a