CHAPTER 24 Differential Analysis and Product Pricing

Ex. 24–15 (FIN MAN); Ex. 9–15 (MAN)

a.

Differential

Reject Accept Effect

Order Order on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues $0 $2,320,000 $2,320,000

Costs:

Direct materials 0 –1,120,000 –1,120,000

Direct labor 0 –440,000 –440,000

Variable factory overhead 0 –300,000 –300,000

Variable selling and admin.

1

20,000 tires × $116 per tire

2

20,000 tires × $56 per tire

3

20,000 tires × $22 per tire

Brightstone should accept the special order from Euro Motors.

Differential Analysis

Reject Order (Alt. 1) or Accept Order (Alt. 2)

January 21

1

2

3

4

24-21

CHAPTER 24 Differential Analysis and Product Pricing

Ex. 24-16 (FIN MAN); Ex. 9–16 (MAN)

a. Contribution margin per room night:

Rate per room night $180

Variable costs per room night:

Housekeeping service 23

b. The discount price should be set greater than the variable costs per room

night so that the resulting contribution margin contributes to fixed costs and

profitability. Thus, the price should be greater than $33. The fixed costs are not

24-22

CHAPTER 24 Differential Analysis and Product Pricing

Ex. 24–17 (FIN MAN); Ex. 9–17 (MAN)

a. Desired profit = $250,000 × 22% = $55,000

b. Cost amount (product cost) per unit: $32,000 ÷ 800 units = $40.00

d. Cost amount (product cost) per unit……………………………………………

…

$ 40.00

Ex. 24–18 (FIN MAN); Ex. 9–18 (MAN)

a. Desired profit = $1,200,000 × 30% = $360,000

b. Cost amount (product cost) per unit: $2,500,000* ÷ 10,000 units = $250

*($215 manufacturing variable cost per unit × 10,000 units) + $350,000 manfacturing

fixed cost

…

Desired Profit +

c. Total Selling and Administrative Expenses

Total Manufacturing Costs

Markup Percentage =

24-23

CHAPTER 24 Differential Analysis and Product Pricing

Ex. 24–19 (FIN MAN); Ex. 9–19 (MAN)

a. The price will be set at the estimated market price required to remain

competitive, or $27,000. Under the target cost concept, the market dictates

the price, not the markup on cost.

b. The required profit margin of 20% of the estimated $27,000 price implies a

$21,600 target product cost as follows:

Target Product Cost = $27,000 – ($27,000 × 20%)

24-24

CHAPTER 24 Differential Analysis and Product Pricing

Ex. 24–20 (FIN MAN); Ex. 9–20 (MAN)

$460 – $230

$230

$230

b. Required cost reduction: $230 – $200 = $30

$30

60 min.

Direct material reduction: 20.00 17.00

3. Injection molding productivity improvement:

a.

=

Historical markup percentage on product cost: = 100%

50% of selling priceor,

1.c.

Direct labor reduction:

× 15 min. =

$ 7.50

24-25

CHAPTER 24 Differential Analysis and Product Pricing

Ex. 24–21 (FIN MAN); Ex. 9–21 (MAN)

Determine the contribution margin per furnace hour as follows:

Revenue……………………………………

…

$43,000 $49,000 $56,500

V

ariable cost………………………………

…

34,000 28,000 26,500

Contribution margin……………………… $ 9,000 $21,000 $30,000

÷ Divide by number of units……………

…

5,000 units 5,000 units 5,000 units

Unit contribution margin………………… $ 1.80 $ 4.20 $ 6.00

Unit contribution margin

per furnace hour*………………………

…

$ 0.30 $ 0.70 $ 0.50

*Calculated as follows:

$1.80

6 hours

$6.00

12 hours

Type 5 Type 10 Type 20

Type 5: = $0.30 per furnace hour

Type 20: = $0.50 per furnace hour

24-26

CHAPTER 24 Differential Analysis and Product Pricing

Ex. 24–22 (FIN MAN); Ex. 9–22 (MAN)

a. Large Medium Small Total

Units produced…………………

…

3,000 3,000 3,000

Revenues………………………… $552,000 $480,000 $300,000 $1,332,000

b. The Small glass product is the most profitable in a bottleneck operation,

demonstrated as follows:

24-27

CHAPTER 24 Differential Analysis and Product Pricing

Ex. 24–23 (FIN MAN); Ex. 9–23 (MAN)

a. Total costs:

Desired Profit

Total Costs

…

…

Ex. 24–24 (FIN MAN); Ex. 9–24 (MAN)

a. Total variable costs: ($240 × 10,000 units)…………………………………

…

$2,400,000

Cost amount per unit: $2,400,000 ÷ 10,000 units = $240

*

$1,200,000 × 30% = $360,000

c. Cost amount per unit……………………………………………………………

…

$240

…

Desired Profit + Total Fixed Costs

Total Costs

b.

b. Markup percentage =

Markup percentage =

24-28

CHAPTER 24 Differential Analysis and Product Pricing

Prob. 24–1A (FIN MAN); Prob. 9–1A (MAN)

1.

Operate Differential

Retail Invest in Effect

Store Bonds on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues $1,264,000 $172,800 –$1,091,200

Costs:

3. Total estimated revenue from operating store………

…

$1,264,000

Total estimated expenses to operate store:

Costs to operate store, excluding depreciation…

…

$928,000

Differential Analysis

Operate Retail Store (Alt. 1) or Invest in Bonds (Alt. 2)

October 1

PROBLEMS

12

24-29

CHAPTER 24 Differential Analysis and Product Pricing

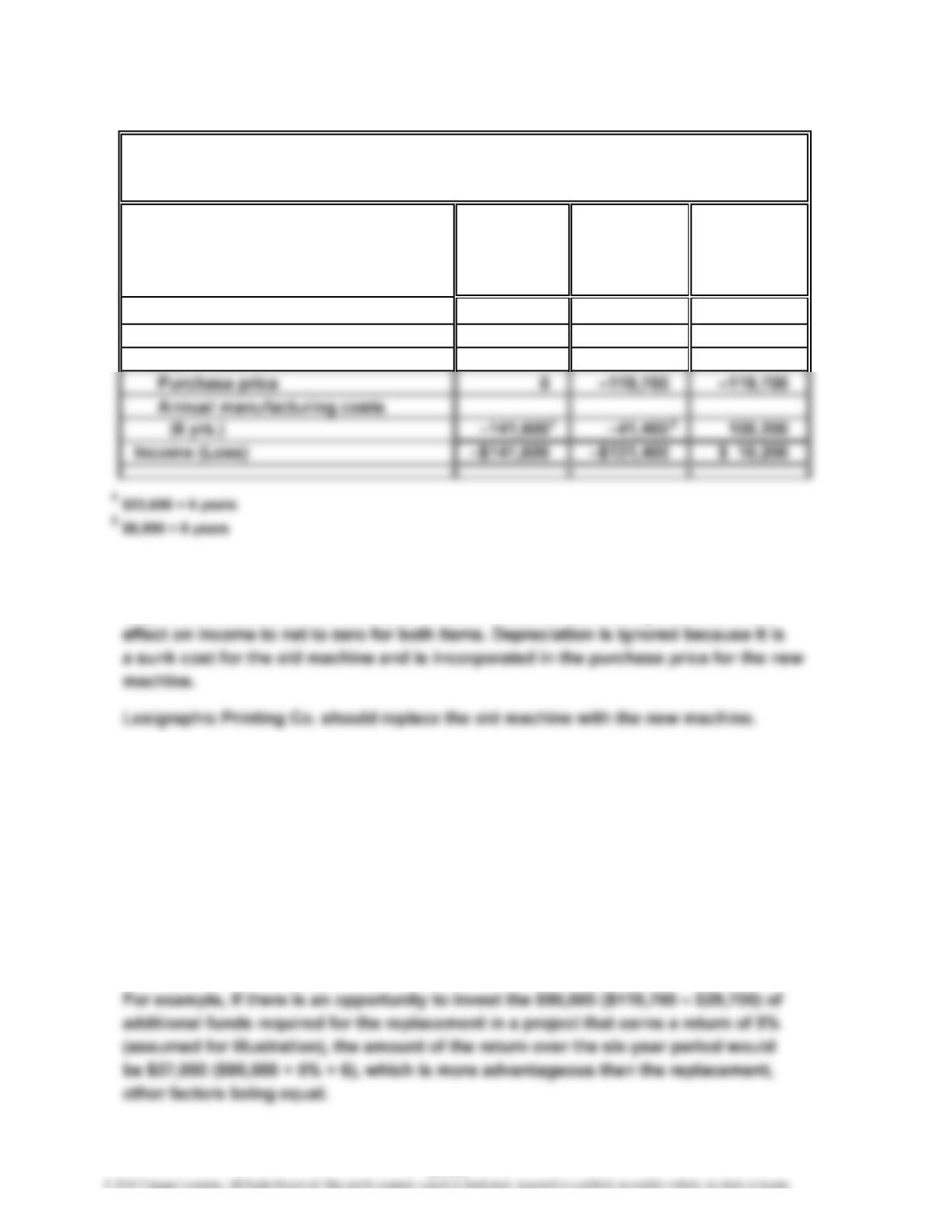

Prob. 24–2A (FIN MAN); Prob. 9–2A (MAN)

1.

Continue Replace Differential

with Old Old Effect

Machine Machine on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues

Proceeds from sale of old machine $ 0 $ 29,700 $ 29,700

Costs

Note: Revenues and nonmanufacturing operating expenses are not affected by the

decision to replace the old machine and, thus, are not included in the analysis. If

they were included, both alternatives would include them, causing the differential

2. Other factors to be considered include:

a. Are there any improvements in the quality of work turned out by the new

machine?

b. What effect does the federal income tax have on the decision?

c. What opportunities are available for the use of the $90,000 of funds ($119,700 less

$29,700 proceeds from the old machine) that are required to purchase the new

machine?

After considering such factors as those listed above, the net cost reduction

anticipated over the six-year period may not be sufficient to justify the replacement.

Differential Analysis

Continue with Old Machine (Alt. 1) or Replace Old Machine (Alt. 2)

April 30

24-30

CHAPTER 24 Differential Analysis and Product Pricing

Prob. 24–3A (FIN MAN); Prob. 9–3A (MAN)

1.

Differential

Promote Promote Effect

Moisturizer Perfume on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues $1,210,000 $1,200,000 –$10,000

Costs:*

Direct materials –198,000 –280,000 –82,000

Direct labor –66,000 –100,000 –34,000

Parisian should promote moisturizer.

2. The sales manager’s tentative decision should be opposed. The sales manager

erroneously considered the full unit costs instead of the differential (additional)

Differential Analysis

Promote Moisturizer (Alt. 1) or Promote Perfume (Alt. 2)

August 21

12

24-31

CHAPTER 24 Differential Analysis and Product Pricing

Prob. 24–4A (FIN MAN); Prob. 9–4A (MAN)

1.

Process

Further into Differential

Sell Raw Refined Effect

Sugar Sugar on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues, per batch $58,800 $73,920 $15,120

2. Dominican Sugar Company should not process raw sugar further to produce

Differential Analysis

Sell Raw Sugar (Alt. 1) or Process Further into Refined Sugar (Alt. 2)

March 24

12

24-32

CHAPTER 24 Differential Analysis and Product Pricing

Prob. 24–5A (FIN MAN); Prob. 9–5A (MAN)

1. $225,000 ($1,500,000 × 15%)

2. a. Total manufacturing costs:

V

ariable ($200* × 5,000 units)……………………………………………… $1,000,000

Fixed factory overhead……………………………………………………

…

250,000

…

Total Selling and Administrative Expenses

Desired Profit +

Total Manufacturing Costs

$1,250,000

b. Markup Percentage =

$225,000 + $150,000 + ($35 × 5,000 units)

=

24-33

CHAPTER 24 Differential Analysis and Product Pricing

Prob. 24–5A (FIN MAN); Prob. 9–5A (MAN) (Continued)

3. (Appendix)

a. Total costs:

V

ariable ($235 × 5,000 units)…………………………………………

…

$1,175,000

Fixed ($250,000 + $150,000)…………………………………………

…

400,000

Total…………………………………………………………………………

…

$1,575,000

4. (Appendix)

a. Variable cost amount per unit: $235

Total variable costs: $235 × 5,000 units = $1,175,000

c. Cost amount per unit……………………………………………………… $235

5. The cost-plus approach price of $360 should be viewed as a general guideline

for establishing long-run normal prices. Other considerations, such as the price

b. Markup Percentage =

Desired Profit + Total Fixed Costs

Total Variable Costs

24-34

CHAPTER 24 Differential Analysis and Product Pricing

Prob. 24–5A (FIN MAN); Prob. 9–5A (MAN) (Concluded)

6. a.

Differential

Reject Accept Effect

Order Order on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues $0 $180,000 $180,000

Costs:

Differential Analysis

Reject Order (Alt. 1) or Accept Order (Alt. 2)

August 3

24-35