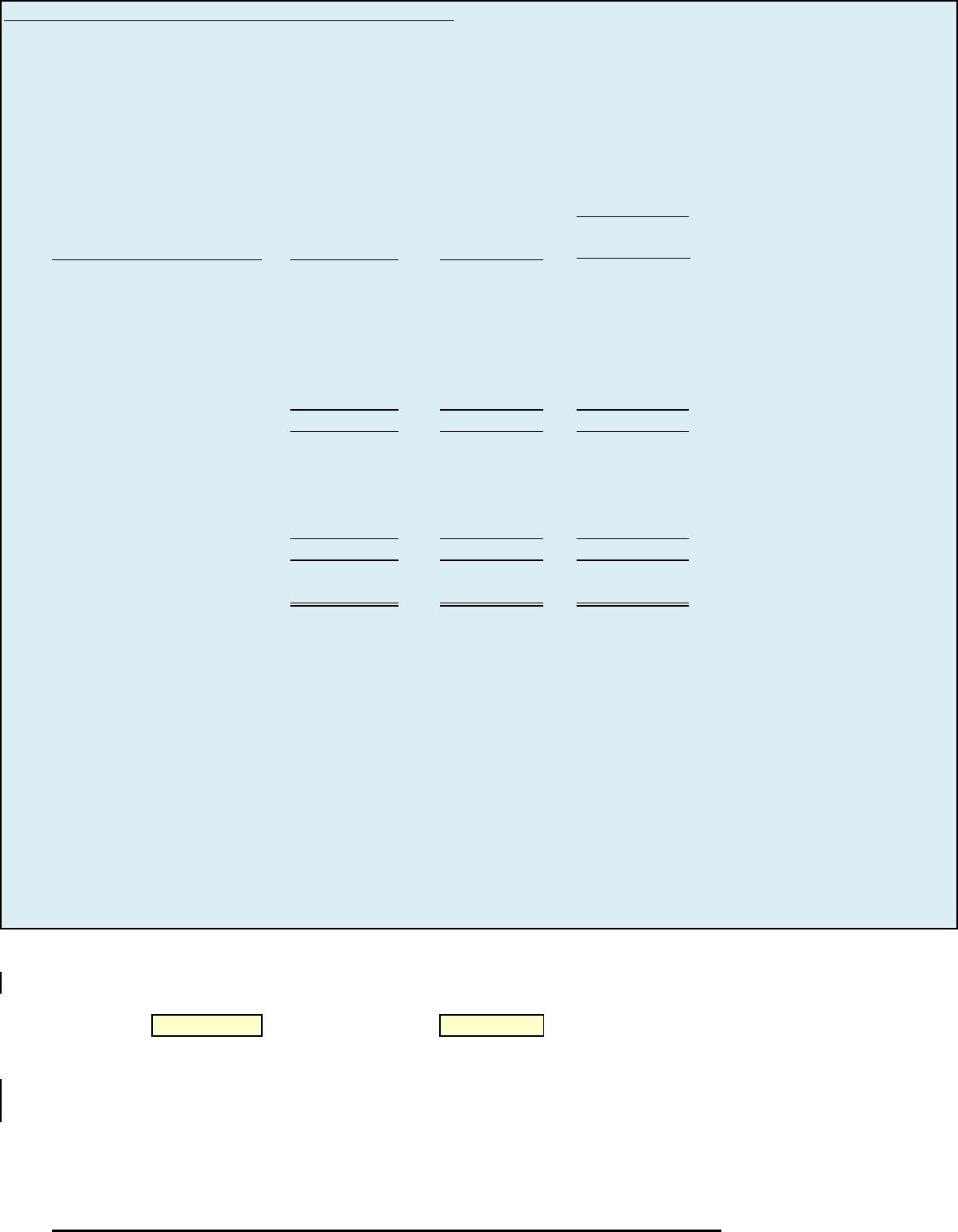

P24-3A Prepare flexible manufacturing overhead budget

Ratchet Company uses budgets in controlling costs. The August 2017 budget report for the company’s Assembling

Department is as follows.

Difference

Favorable F

Budget Actual Unfavorable U

Variable costs

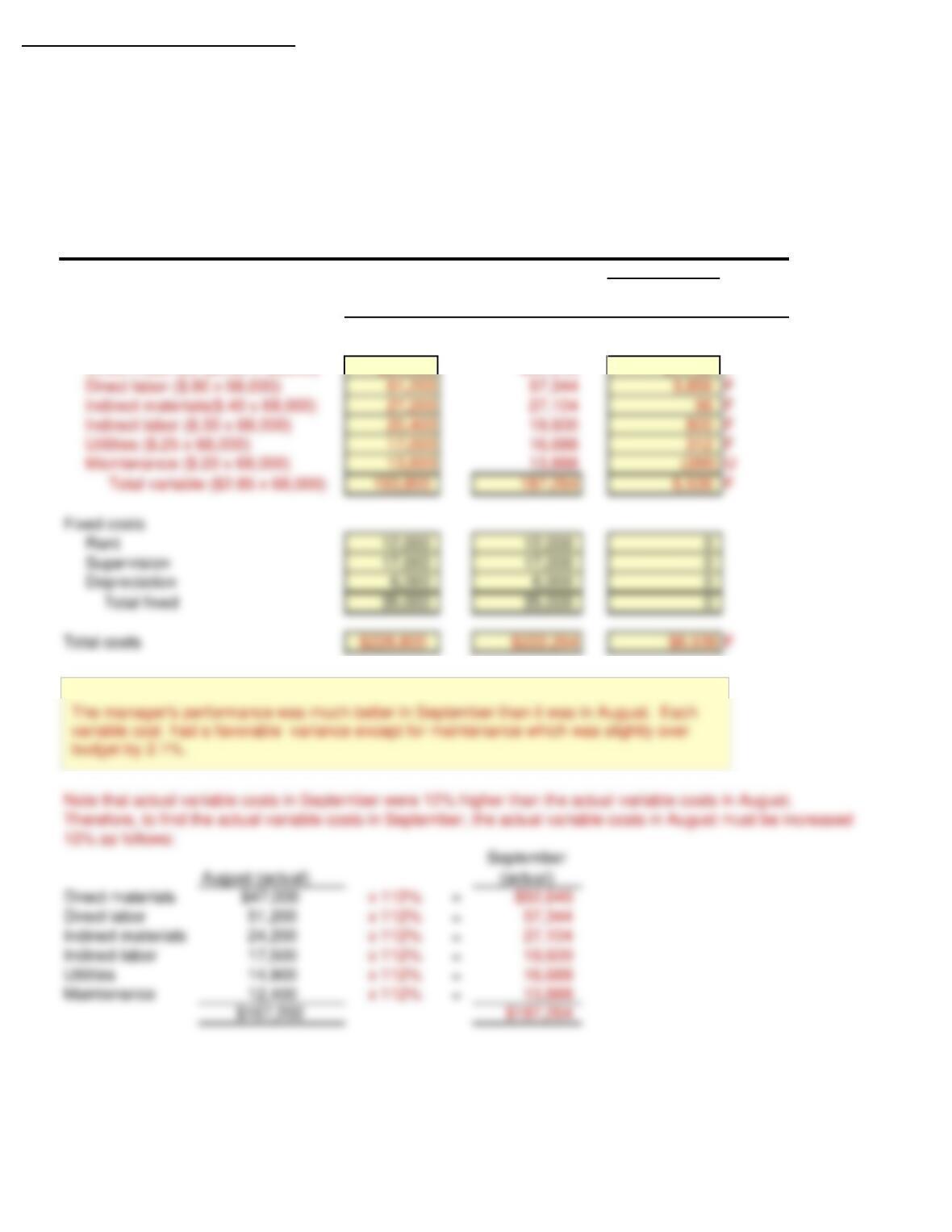

Direct materials $48,000 $47,000 $1,000 F

Direct labor 54,000 51,200 2,800 F

Indirect materials 24,000 24,200 200 U

Indirect labor 18,000 17,500 500 F

Utilities 15,000 14,900 100 F

Maintenance 12,000 12,400 400 U

Total variable 171,000 167,200 3,800 F

Fixed costs

Rent 12,000 12,000 0

Supervision 17,000 17,000 0

Depreciation 6,000 6,000 0

Total fixed 35,000 35,000 0

Total costs $206,000 $202,200 $3,800 F

The monthly budget amounts in the report were based on an expected production of 60,000 units per month

or 720,000 units per year. The Assembling Department manager is pleased with the report and expects a raise,

or at least praise for a job well done. The company president, however, is unhappy with the results for August

because only 58,000 units were produced.

Instructions

(a) State the total monthly budgeted cost formula.

(b) Prepare a budget report for August using flexible budget data. Why does this report provide a better

basis for evaluating performance than the report based on static budget data?

(c) In September, 64,000 units were produced. Prepare the budget report using flexible budget data, assuming

(1) each variable cost was 10% higher than its actual cost in August, and (2) fixed costs were the same in

September as in August.

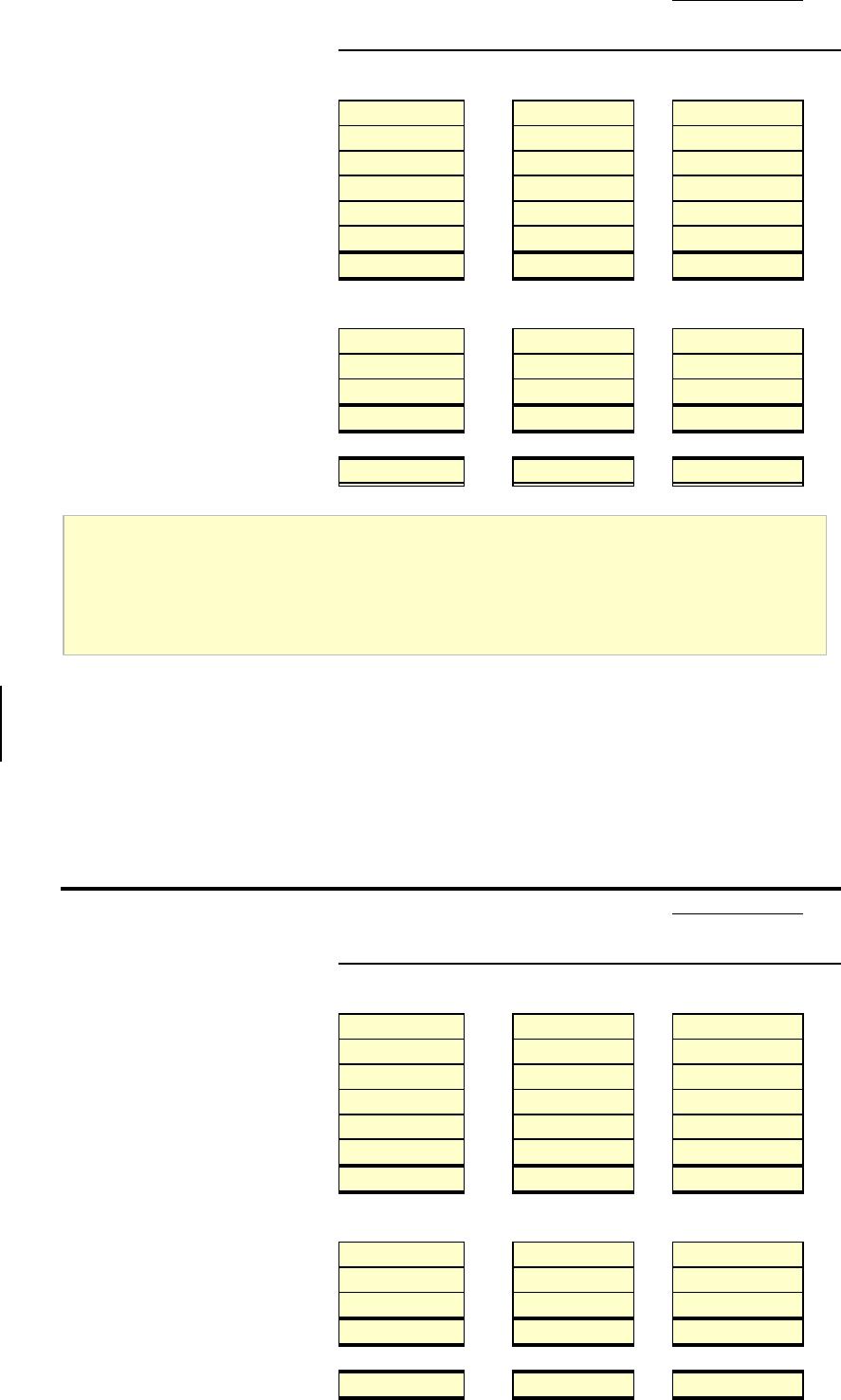

NOTE: Enter a number in cells requesting a value; enter either a number or a formula in cells with a “?” .

(a) State the total monthly budgeted cost formula.

Fixed cost Value + variable cost of Value per unit

(b) Prepare a budget report for August using flexible budget data. Why does this report provide a better

basis for evaluating performance than the report based on static budget data?

Manufacturing Cost

RATCHET COMPANY

Budget Report

Assembling Department

For the Month Ended August 31, 2017

RATCHET COMPANY

Assembling department

Flexible budget Report

For the Month Ended August 31, 2017

Difference

Budget at

Actual Costs

Favorable F

Units 58,000 units 58,000 units Unfavorable U

Variable costs

Direct materials ? Value ?

Direct labor ? Value ?

Indirect materials ? Value ?

Indirect labor ? Value ?

Utilities ? Value ?

Maintenance ? Value ?

Total variable ? ? ?

Fixed costs

Rent Value Value ?

Supervision Value Value ?

Depreciation Value Value ?

Total fixed ? ? ?

Total costs ? ? ?

(c) In September, 64,000 units were produced. Prepare the budget report using flexible budget data, assuming

(1) each variable cost was 10% higher than its actual cost in August, and (2) fixed costs were the same in

September as in August.

Difference

Budget at

Actual Costs

Favorable F

Units 64,000 units 64,000 units Unfavorable U

Variable costs

Direct materials ? ? ?

Direct labor ? ? ?

Indirect materials ? ? ?

Indirect labor ? ? ?

Utilities ? ? ?

Maintenance ? ? ?

Total variable ? ? ?

Fixed costs

Rent Value Value Value

Supervision Value Value Value

Depreciation Value Value Value

Total fixed ? ? ?

Total costs ? ? ?

Assembling department

Flexible budget Report

For the Month Ended September 30, 2017

RATCHET COMPANY

Response:

After you have completed P24-3A consider the following additional question.

1. Assume that the number of units produced in September changed to 68,000. Revise

the flexible budget report for September assuming (1) each variable cost was 12%

higher than its actual cost in August and (s) fixed costs remain the same in September

as in August.

Response:

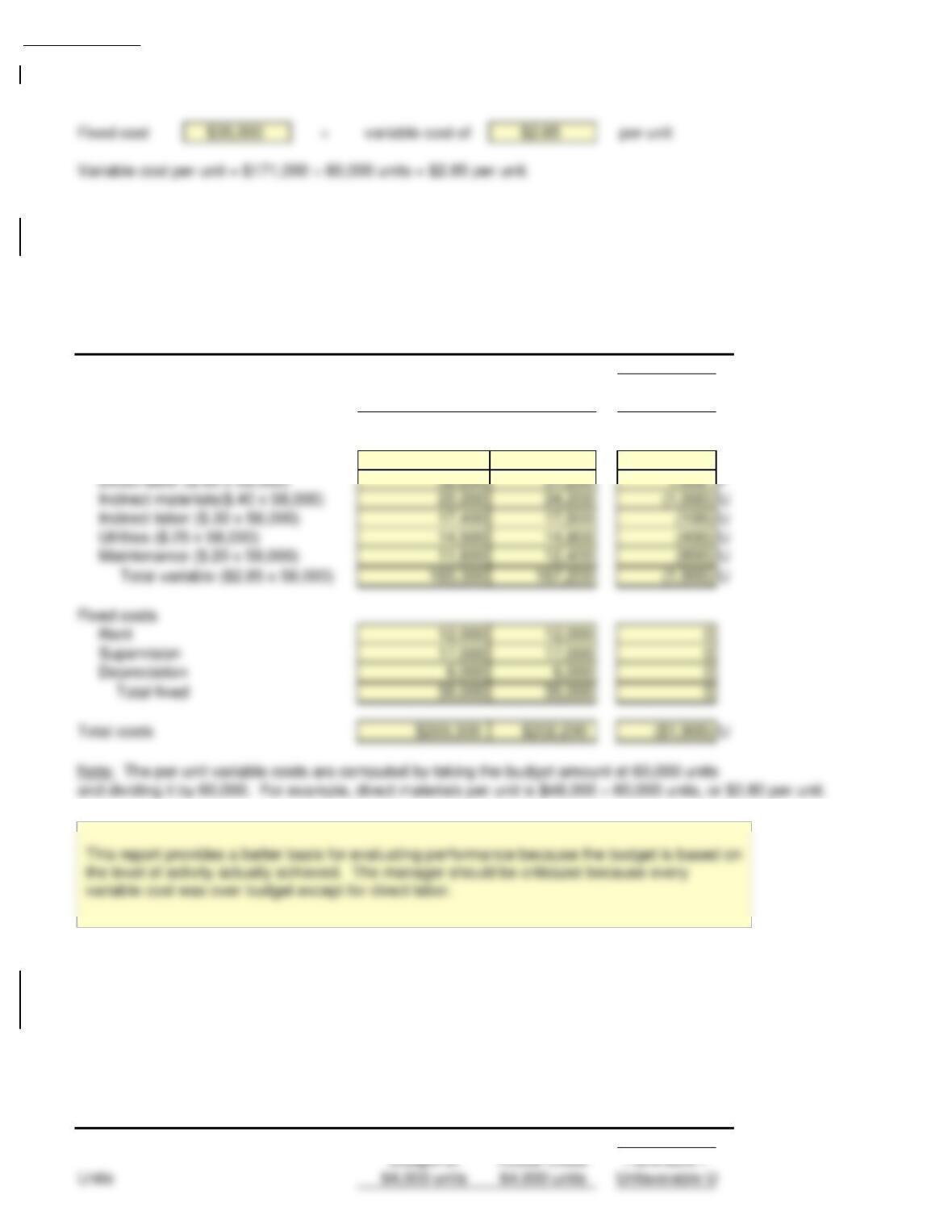

P24-3A Solution

(a) State the total monthly budgeted cost formula.

Fixed cost $35,000 + variable cost of $2.85 per unit

Variable cost per unit = $171,000 ÷ 60,000 units = $2.85 per unit.

(b) Prepare a budget report for August using flexible budget data. Why does this report provide a better

basis for evaluating performance than the report based on static budget data?

Difference

Budget at Actual Costs Favorable F

Units 58,000 units 58,000 units Unfavorable U

Variable costs*

Direct materials ($0.80 x 58,000) $46,400 $47,000 ($600) U

Direct labor ($.90 x 58,000)

52,200 51,200 1,000 F

Indirect materials($.40 x 58,000) 23,200 24,200 (1,000) U

Note: The per unit variable costs are computed by taking the budget amount at 60,000 units

and dividing it by 60,000. For example, direct materials per unit is $48,000 ÷ 60,000 units, or $0.80 per unit.

(c) In September 64,000 units were produced. Prepare the budget report using flexible budget data, assuming

(1) each variable cost was 10% higher than its actual cost in August, and (2) fixed costs were the same in

September as in August.

Difference

Assembling department

Flexible budget Report

For the Month Ended September 30, 2017

RATCHET COMPANY

RATCHET COMPANY

Assembling department

Flexible budget Report

For the Month Ended August 31, 2017

Variable costs

Direct materials ($0.80 x 64,000) $51,200 $51,700 ($500) U

Direct labor ($.90 x 64,000)

57,600 56,320 1,280 F

Indirect materials($.40 x 64,000) 25,600 26,620 (1,020) U

Fixed costs

Rent 12,000 12,000 0

Supervision 17,000 17,000 0

Note that actual variable costs in September were 10% higher than the actual variable costs in August. Therefore,

to find the actual variable costs in September, the actual variable costs in August must be increased 10% as follows:

August (actual)

September

(actual)

Direct materials $47,000 x 110% = $51,700

Direct labor 51,200 x 110% = 56,320

P24-3A Solution to additonal question

1. Assume that the number of units produced in September changed to 68,000. Revise

the flexible budget report for September assuming (1) each variable cost was 12%

higher than its actual cost in August and (s) fixed costs remain the same in September

as in August.

Difference

Budget at Actual Costs Favorable F

Units 68,000 units 68,000 units Unfavorable U

Variable costs

Direct materials ($0.80 x 68,000) $54,400 $52,640 $1,760 F

Direct labor ($.90 x 68,000) 61,200 57,344 3,856 F

RATCHET COMPANY

Assembling department

Flexible budget Report

For the Month Ended September 30, 2017

The manager’s performance was much better in September than it was in August. Each

variable cost had a favorable variance except for maintenance which was slightly over

budget by 2.1%.

CD24 Prepare flexible manufacturing overhead budget

The Current Designs staff has prepared the annual manufacturing budget for the rotomolded line based on an

estimated annual production of 4,000 kayaks during 2017. Each kayak will require 54 pounds of polyethylene powder

and a finishing kit (rope, seat, hardware, etc.). The polyethylene powder used in these kayaks costs $1.50 per pound,

and the finishing kit cost $170 each. Each kayak will use two kinds of labor – 2 hours of type I labor from people who

run the oven and trim the plastic, and 3 hours of work from type II workers who attach the hatches and seat and other

hardware. The type I employees are paid $15 per hour, and the type II are paid $12 per hour.

Manufacturing overhead is budgeted at $396,000 for 2017, broken down as follows.

Variable costs

Indirect materials $40,000

Manufacturing supplies 53,800

Maintenance and utilities 88,000

181,800

Fixed costs

Supervision 90,000

Insurance 14,400

Depreciation 109,800

214,200

Total $396,000

During the first quarter, ended March 31, 2017, 1,050 units were actually produced with the

following costs.

Polyethylene powder $87,000

Finishing kits 178,840

Type I labor 31,500

Type II labor 39,060

Indirect materials 10,500

Manufacturing supplies 14,150

Maintenance and utilities 26,000

Supervision 20,000

Insurance 3,600

Depreciation 27,450

Total $438,100

Instructions

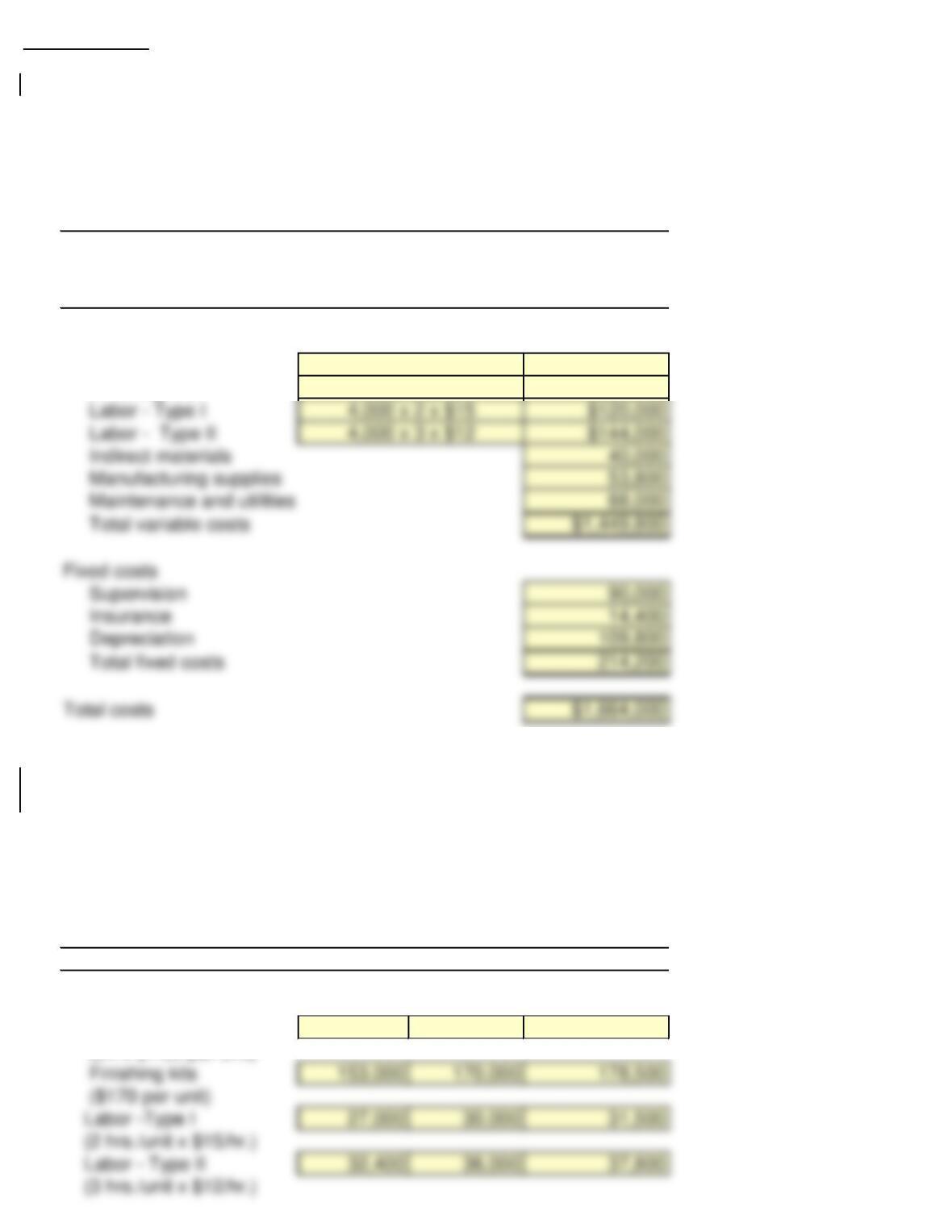

(a) Prepare the annual manufacturing budget for 2017, assuming that 4,000 kayaks will be produced.

(b) Prepare the flexible budget for manufacturing for the quarter ended March 31, 2017. Assume

activity levels of 900, 1,000 and 1,050 units.

(c)

Assuming the rotomolded line is treated as a profit center, prepare a flexible budget report for

manufacturing for the quarter ended March 31, 2017, when 1,050 units were produced.

NOTE: Enter a number in cells requesting a value; enter either a number or a formula in cells with a “?” .

(a) Prepare the annual manufacturing budget for 2017, assuming that 4,000 kayaks will be produced.

4,000 Kayaks

Amount

Budgeted

Costs:

Variable cost

Polyethylene powder ?

Finishing kits ?

Labor – Type I ?

Labor – Type II ?

Indirect materials Value

Manufacturing supplies Value

Value

Value

Value

Value

Current Designs

Manufacturing Budget

Rotomolded Line

For the Year Ended December 31, 2017

Units to be produced

Calculations

Maintenance and utilities Value

Total variable costs ?

Fixed costs

Supervision Value

Insurance Value

Depreciation Value

Total fixed costs ?

Total costs ?

(b) Prepare the flexible budget for manufacturing for the quarter ended March 31, 2017. Assume

activity levels of 900, 1,000 and 1,050 units.

Units to be produced 900 kayaks 1,000 kayaks 1,050 kayaks

Costs:

Variable costs

Polyethylene powder ? ? ?

Finishing kits ? ? ?

Labor -Type I ? ? ?

Labor – Type II ? ? ?

Indirect materials ? ? ?

Manufacturing supplies ? ? ?

Maintenance & utilities ? ? ?

Total variable costs ? ? ?

Fixed costs

Supervision (a) ? ? ?

Insurance (b) ? ? ?

Depreciation © ? ? ?

Total fixed costs ? ? ?

Total costs ? ? ?

(c)

Assuming the rotomolded line is treated as a profit center, prepare a flexible budget report for

manufacturing for the quarter ended March 31, 2017, when 1,050 units were produced.

Difference

Budget Actual costs F = favorable

Production in units

1,050 kayaks

1,050 kayaks U = unfavorable

Costs:

Variable costs

Polyethylene powder ? ? ?

Finishing kits ? ? ?

Labor -Type I ? ? ?

Manufacturing Flexible Budget Report

For the Quarter Ended March 31, 2017

Current Designs

Rotomolded Line

Manufacturing Flexible Budget Report

For the Quarter Ended March 31, 2017

Current Designs

Rotomolded Line

Labor -Type II ? ? ?

Indirect materials ? ? ?

Manufacturing supplies ? ? ?

Maintenance & utilities ? ? ?

Total variable costs ? ? ?

Fixed costs

Supervision ? ? ?

Insurance ? ? ?

Depreciation ? ? ?

Total fixed costs ? ? ?

Total costs ? ? ?

After you have completed CD24 consider the following additional questions.

1. Assume that the activity levels in the flexible budget for the quarter ended March 31, 2017

changed to 900, 1,000 and 1,200 in part (b). Show the impact of this change on the flexible budget.

2. Assuming the rotomolded line is treated as a profit center, revise the flexible budget report for

manufacturing for the quarter ended March 31, 2017, assuming 1,200 units were produced.

Assume that variable costs were 10% higher at this level of activity.

CD24 Solution

(a) Prepare the annual manufacturing budget for 2017, assuming that 4,000 kayaks will be produced.

4,000 Kayaks

Amount

Budgeted

Costs:

Variable cost

Polyethylene powder $324,000

Finishing kits $680,000

(b) Prepare the flexible budget for manufacturing for the quarter ended March 31, 2017. Assume

activity levels of 900, 1,000 and 1,050 units.

Production in units 900 kayaks 1,000 kayaks 1,050 kayaks

Costs:

Variable costs

Polyethylene powder $72,900 $81,000 $85,050

(54 x $1.50 per unit)

4,000 x 54 x $1.50

4,000 x $170

Current Designs

Rotomolded Line

Manufacturing Flexible Budget Report

For the Quarter Ended March 31, 2017

Current Designs

Rotomolded Line

Manufacturing Budget

For the Year Ended December 31, 2017

Units to be produced

Calculations

Indirect materials 9,000 10,000 10,500

($10 per unit (a))

Manufacturing supplies 12,105 13,450 14,123

($13.45 per unit (b))

(c) Assuming the rotomolded line is treated as a profit center, prepare a flexible budget report for

manufacturing for the quarter ended March 31, 2017, when 1,050 units were produced.

Difference

Units to be produced Budget Actual costs F = favorable

1,050 kayaks

1,050 kayaks U = unfavorable

Costs:

Variable costs

Polyethylene powder $85,050 $87,000 ($1,950) U

Finishing kits 178,500 178,840 (340) U

For the Quarter Ended March 31, 2017

Current Designs

Rotomolded Line

Manufacturing Flexible Budget Report

CD24 Solution to additional question

1. Assume that the activity levels in the flexible budget for the quarter ended March 31, 2017

changed to 900, 1,000 and 1,200 in part (b). Show the impact of this change on the flexible budget.

2. Assuming the rotomolded line is treated as a profit center, revise the flexible budget report for

manufacturing for the quarter ended March 31, 2017, assuming 1,200 units were produced.

Assume variable costs were 10% higher at this level of activity.

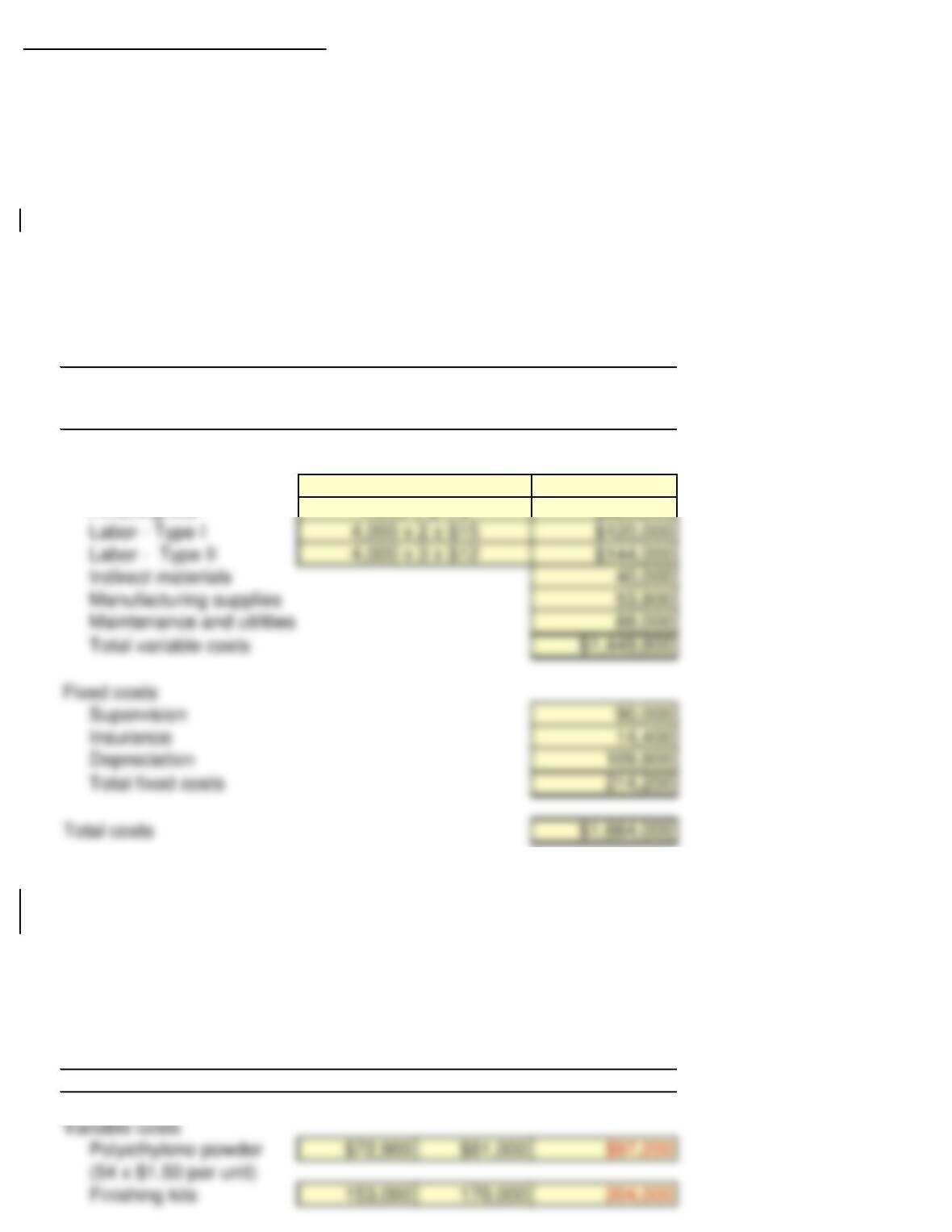

(a) Prepare the annual manufacturing budget for 2017, assuming that 4,000 kayaks will be produced.

4,000 Kayaks

Amount

Budgeted

Costs:

Variable cost

Polyethylene powder $324,000

Finishing kits $680,000

Labor – Type I $120,000

(b) Prepare the flexible budget for manufacturing for the quarter ended March 31, 2017. Assume

activity levels of 900, 1,000 and 1,200 units.

Production in units 900 kayaks 1,000 kayaks 1,200 kayaks

Costs:

Current Designs

Rotomolded Line

Manufacturing Budget

For the Year Ended December 31, 2017

Production in units

Calculations

4,000 x 54 x $1.50

4,000 x $170

4,000 x 2 x $15

Current Designs

Rotomolded Line

Manufacturing Flexible Budget Report

For the Quarter Ended March 31, 2017

4,000 x 3 x $12

($170 per unit)

Labor -Type I 27,000 30,000 36,000

(2 hrs./unit x $15/hr.)

Labor – Type II 32,400 36,000 43,200

Fixed costs

Supervision (d) 22,500 22,500 22,500

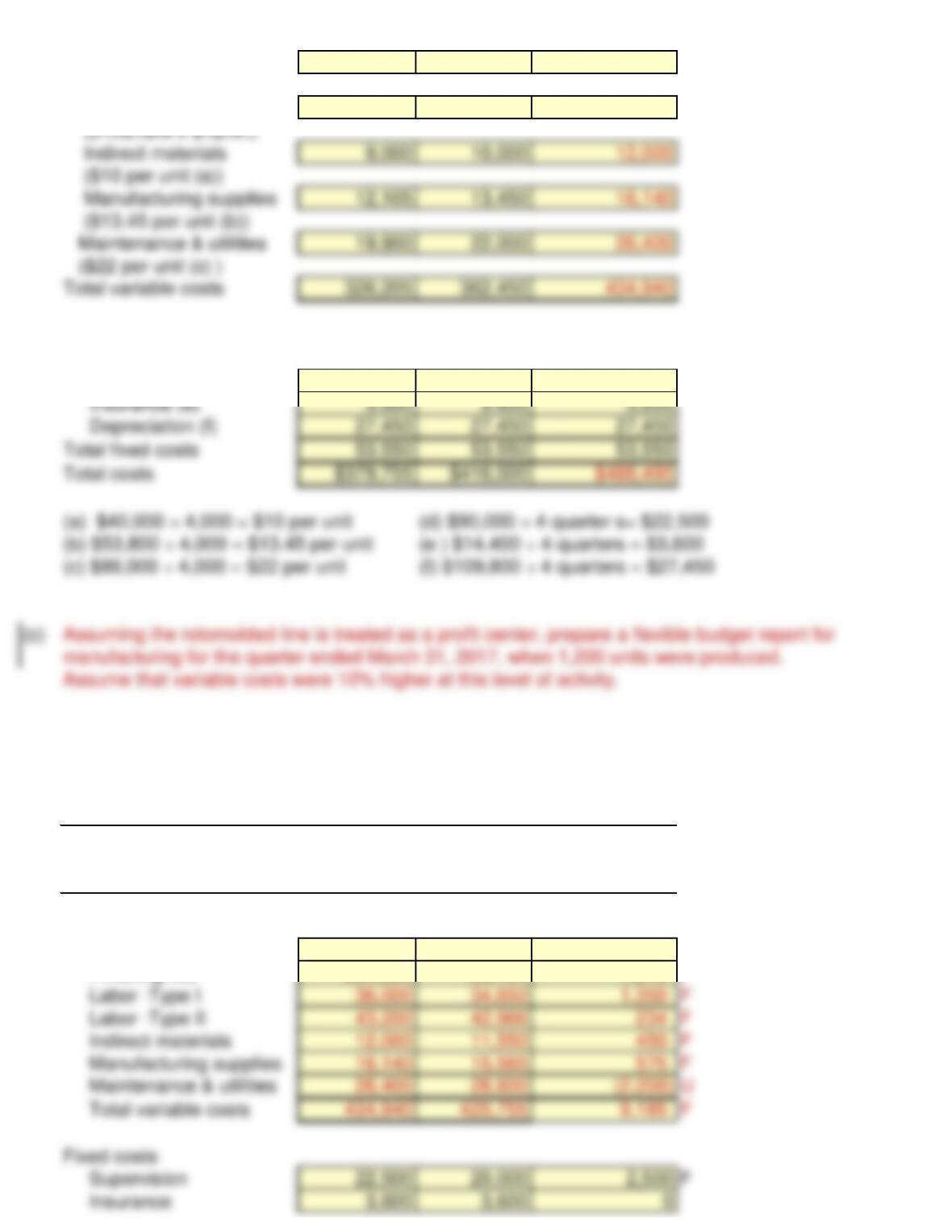

Difference

Units to be produced Budget Actual costs F = favorable

1,200 kayaks 1,200 kayaks U = unfavorable

Costs:

Variable costs

Polyethylene powder $97,200 $95,700 $1,500 F

Finishing kits 204,000 196,724 7,276 F

Labor -Type I 36,000 34,650 1,350 F

For the Quarter Ended March 31, 2017

Current Designs

Rotomolded Line

Manufacturing Flexible Budget Report

Depreciation 27,450 27,450 0