EXERCISE 24-18B

Jets:

ROI = Controllable margin ÷ Average operating assets

15% = Controllable margin ÷ $25,000,000

Controllable margin = $25,000,000 X 15%

= $3,750,000

Helicopters:

ROI

=

Controllable margin

÷

Average operating assets

10%

=

$95,000

÷

Average operating assets

Average operating assets

=

$95,000 ÷ 10%

=

$950,000

Contribution margin

EXERCISE 24-18B (Continued)

Satellites:

ROI = Controllable margin ÷ Average operating assets

= $255,000 ÷ $1,500,000

= 17%

Controllable margin

=

Contribution margin

–

Controllable fixed costs

Service revenue

Variable costs

SOLUTIONS TO PROBLEMS—SET C

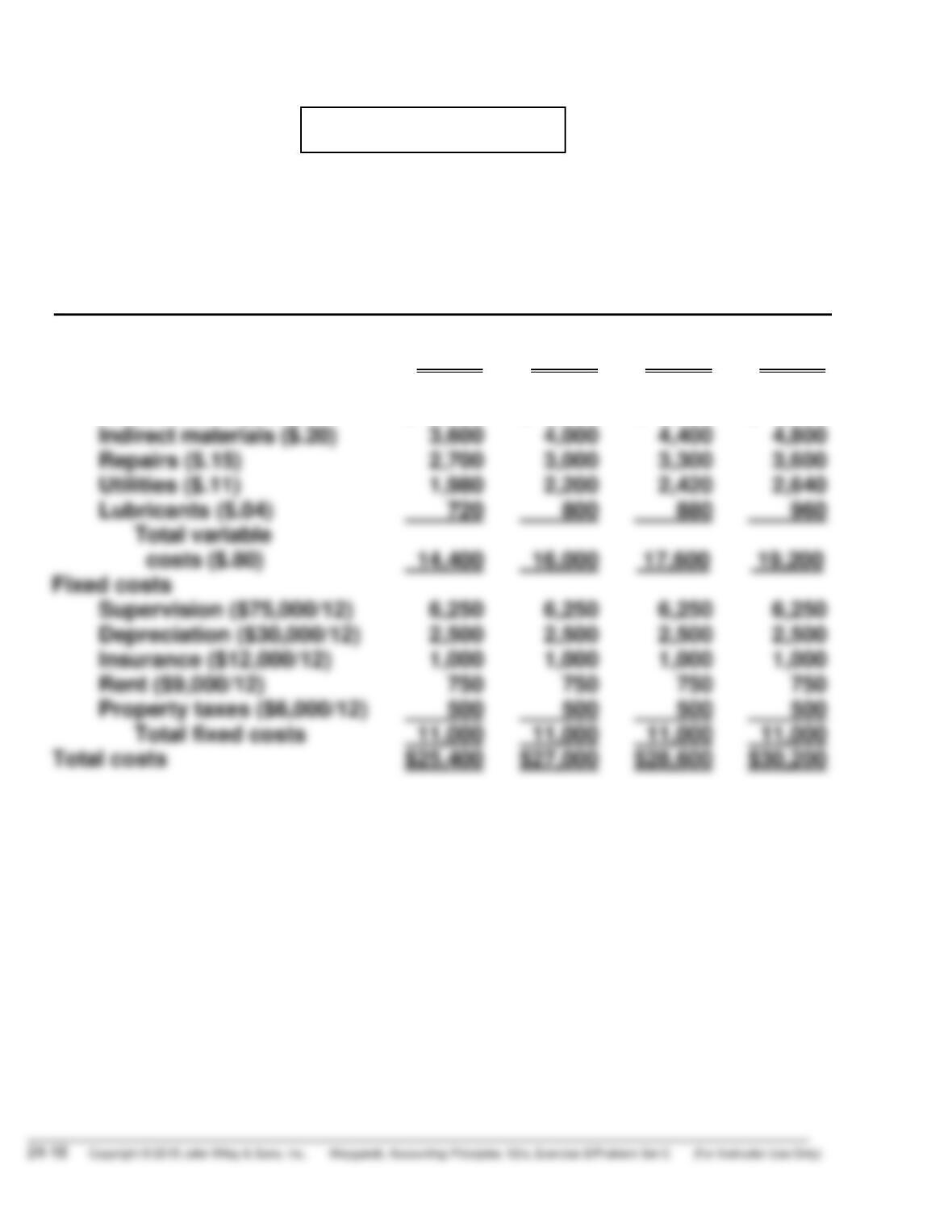

PROBLEM 24-1C

(a) DUNES COMPANY

Flexible Monthly Manufacturing Overhead Budget

Assembly Department

For the Year 2017

Activity level

Direct labor hours

Variable costs

Indirect labor ($.30)

Indirect materials ($.20)

18,000

$ 5,400

3,600

20,000

$ 6,000

4,000

22,000

$ 6,600

4,400

24,000

$ 7,200

4,800

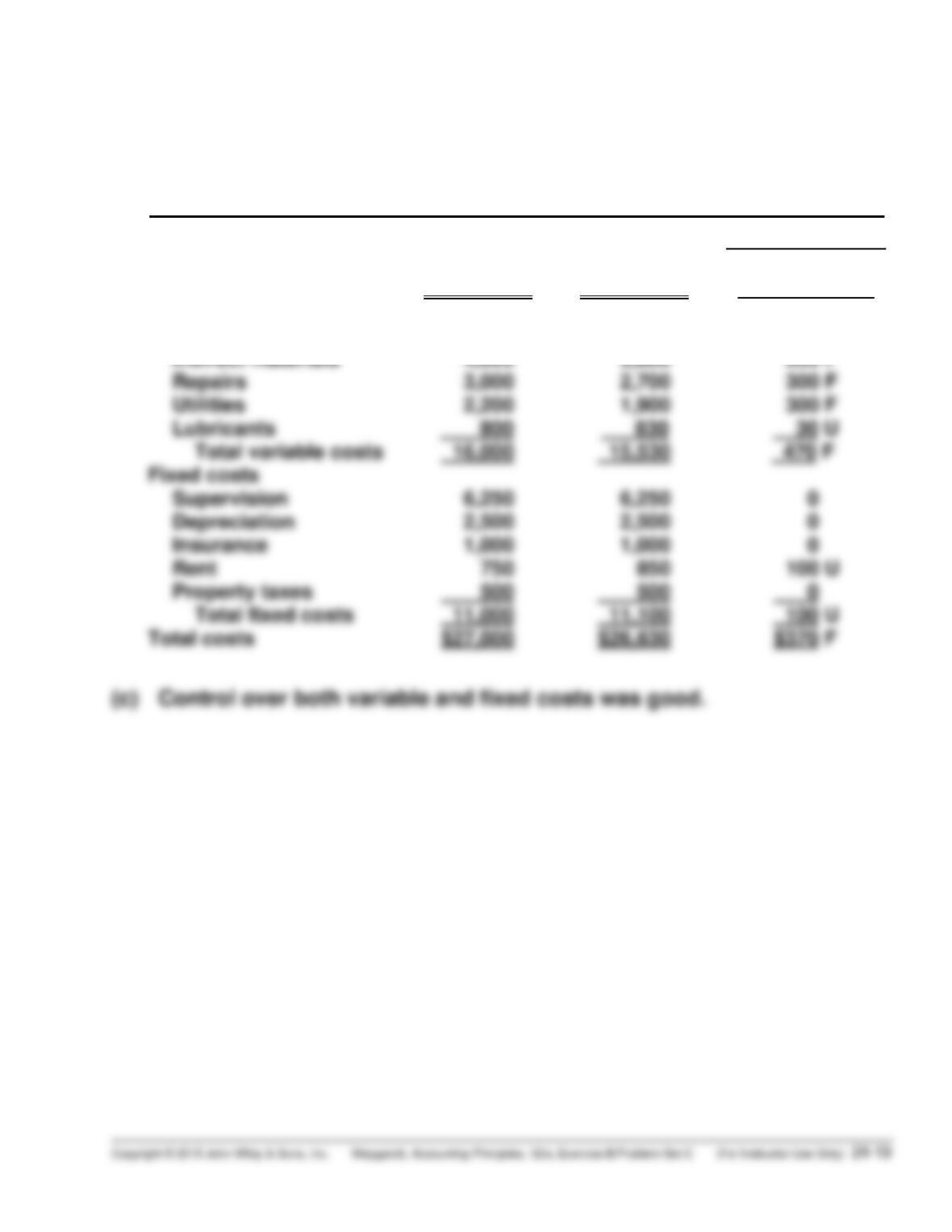

PROBLEM 24-1C (Continued)

(b) DUNES COMPANY

Manufacturing Overhead Budget Report (Flexible)

Assembly Department

For the Month Ended January 31, 2017

Difference

Direct labor hours (DLH)

Variable costs

Indirect labor

Indirect materials

Repairs

Budget at

20,000 DLH

$ 6,000

4,000

3,000

Actual Costs

20,000 DLH

$ 6,300

3,800

2,700

Favorable F

Unfavorable U

$300 U

200 F

300 F

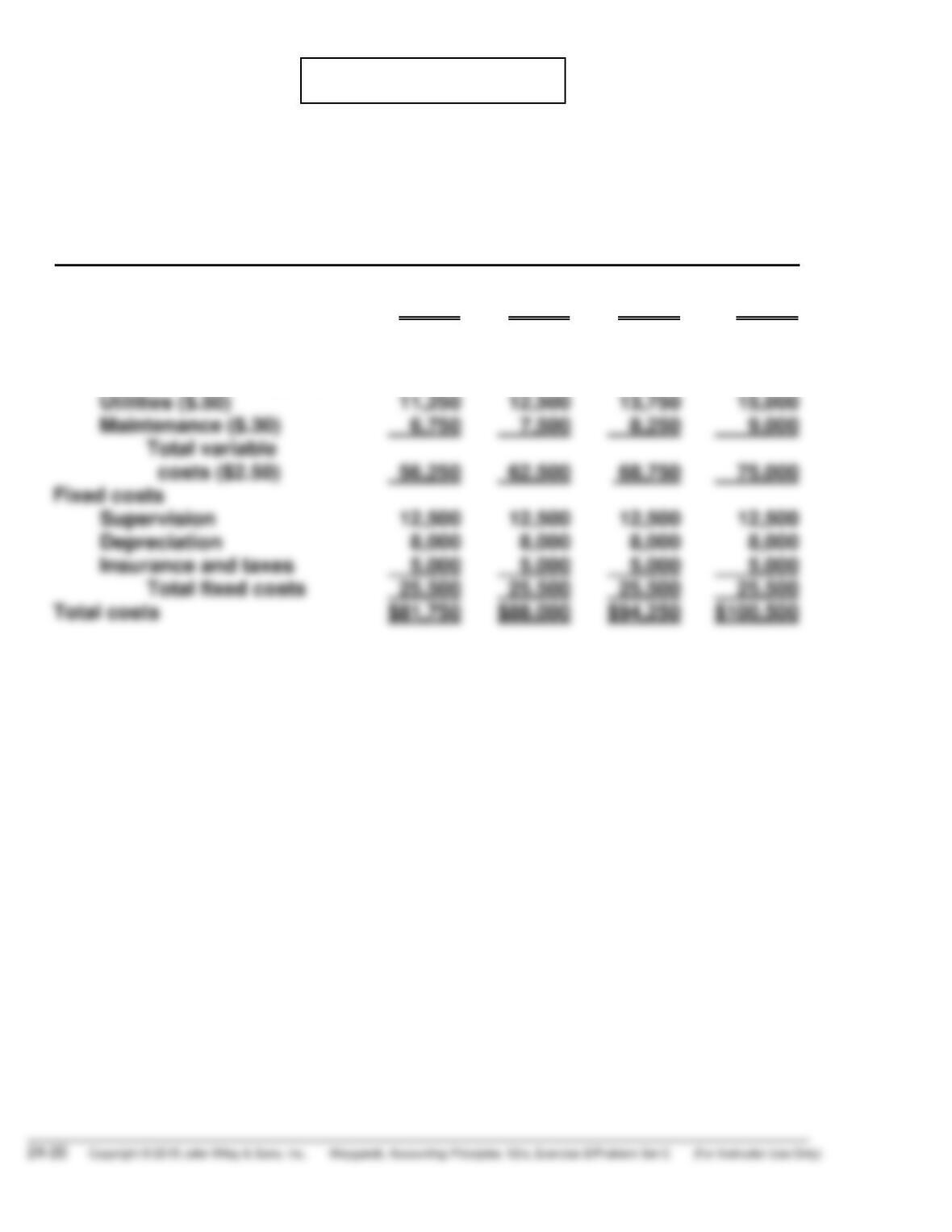

PROBLEM 24-2C

(a) WILLARD MANUFACTURING COMPANY

Flexible Monthly Manufacturing Overhead Budget

Assembly Department

For the Year 2017

Activity level

Direct labor hours

Variable costs

Indirect labor ($1.10)

Indirect materials ($.60)

22,500

$24,750

13,500

25,000

$27,500

15,000

27,500

$30,250

16,500

30,000

$ 33,000

18,000

PROBLEM 24-2C (Continued)

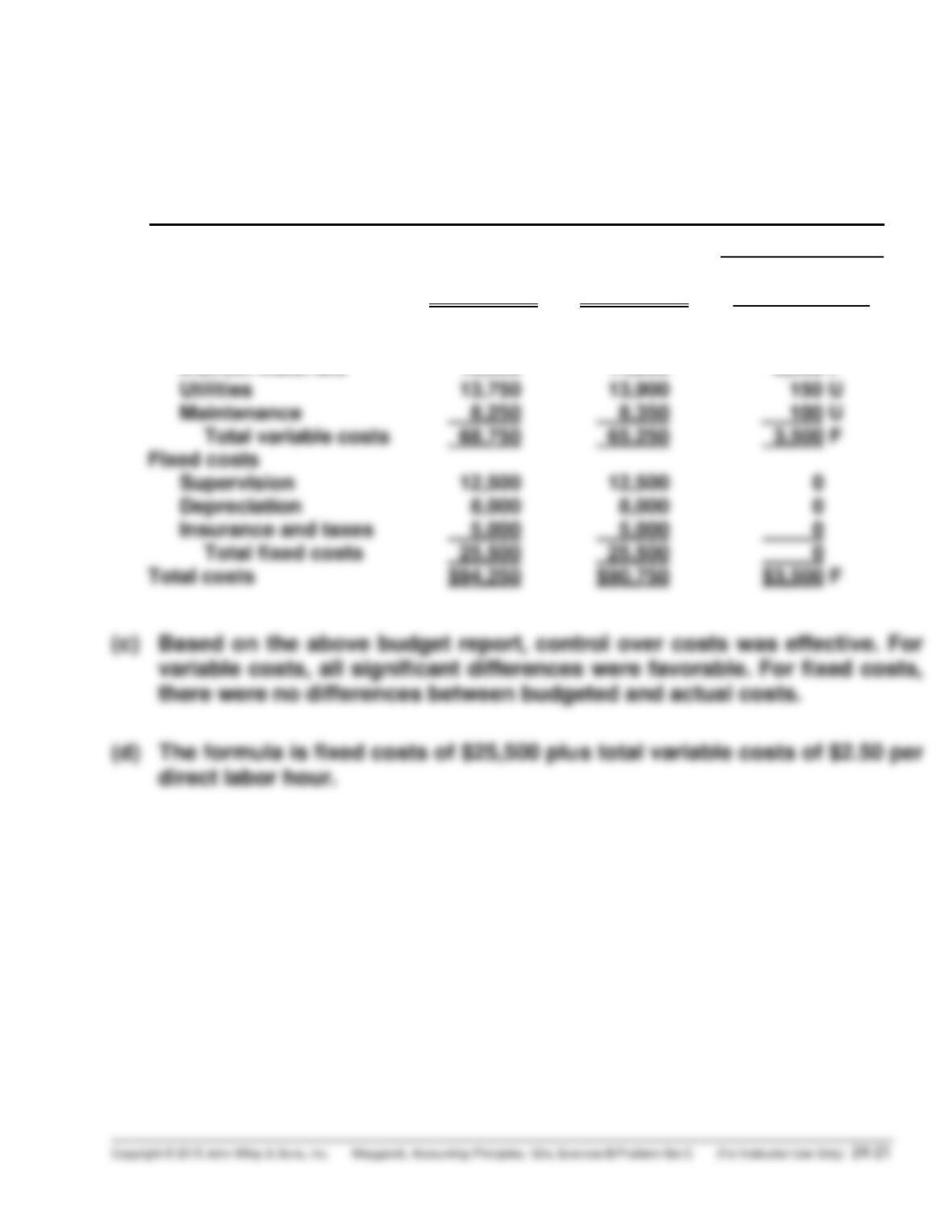

(b) WILLARD MANUFACTURING COMPANY

Assembly Department

Manufacturing Overhead Budget Report (Flexible)

For the Month Ended July 31, 2017

Difference

Direct labor hours (DLH)

Variable costs

Indirect labor

Indirect materials

Utilities

Budget at

27,500 DLH

$30,250

16,500

13,750

Actual Costs

27,500 DLH

$29,000

14,000

13,900

Favorable F

Unfavorable U

$1,250 F

2,500 F

150 U

PROBLEM 24-2C (Continued)

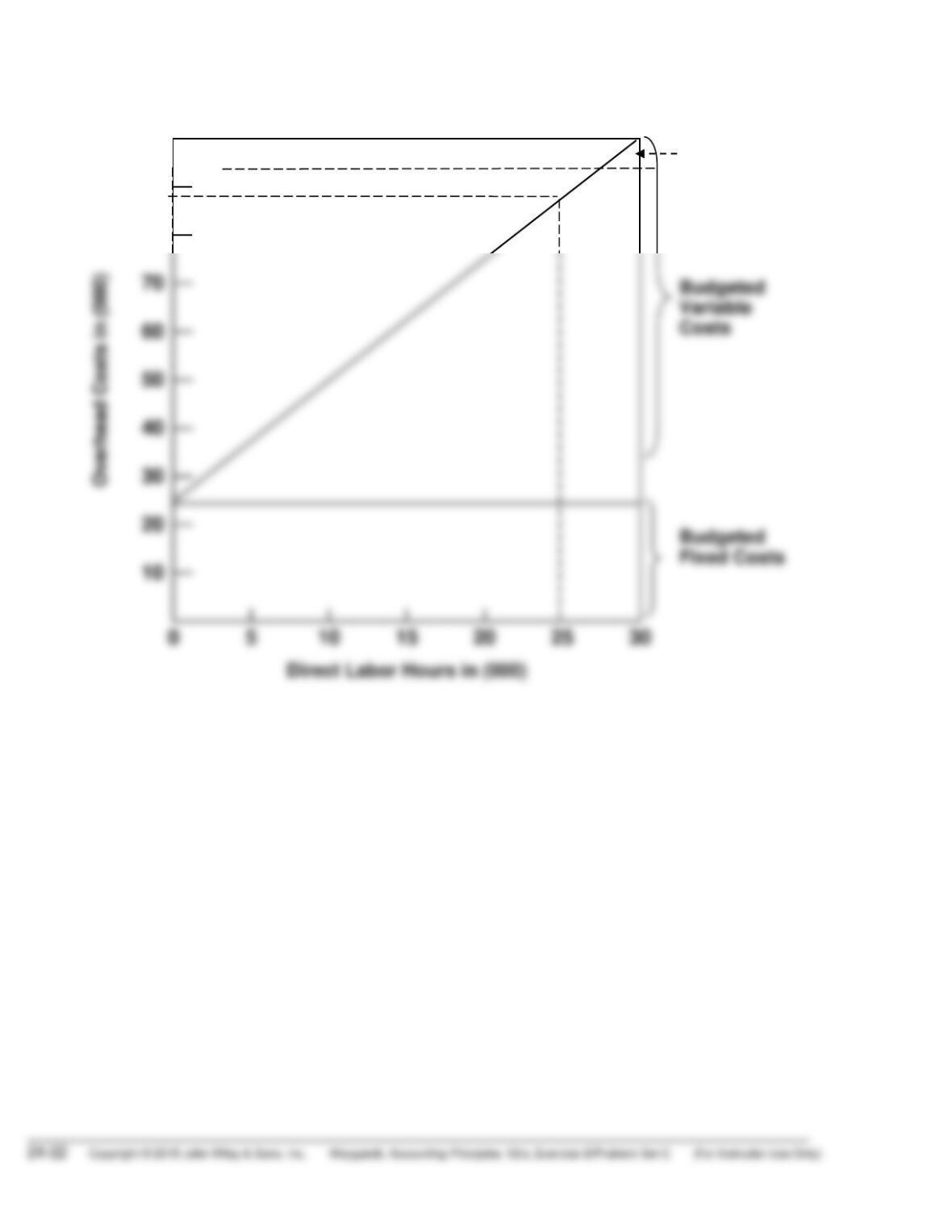

(e)

$100

Total

Budgeted

Cost Line

70

60

40

30

20

10

90

80

PROBLEM 24-3C

(a) The formula is fixed costs $22,000 plus total variable costs of $2.50 per

unit ($125,000 ÷ 50,000 units).

(b) ANSON COMPANY

Packaging Department

Budget Report (Flexible)

For the Month Ended May 31, 2017

Difference

Units

Variable costs*

Direct materials ($.75 X 55,000)

Direct labor ($.90 X 55,000)

Indirect materials ($.30 X 55,000)

Indirect labor ($.25 X 55,000)

Budget at

55,000 Units

$ 41,250

49,500

16,500

13,750

Actual Costs

55,000 Units

$ 38,000

47,000

15,200

13,000

Favorable F

Unfavorable U

$3,250 F

2,500 F

1,300 F

750 F

PROBLEM 24-3C (Continued)

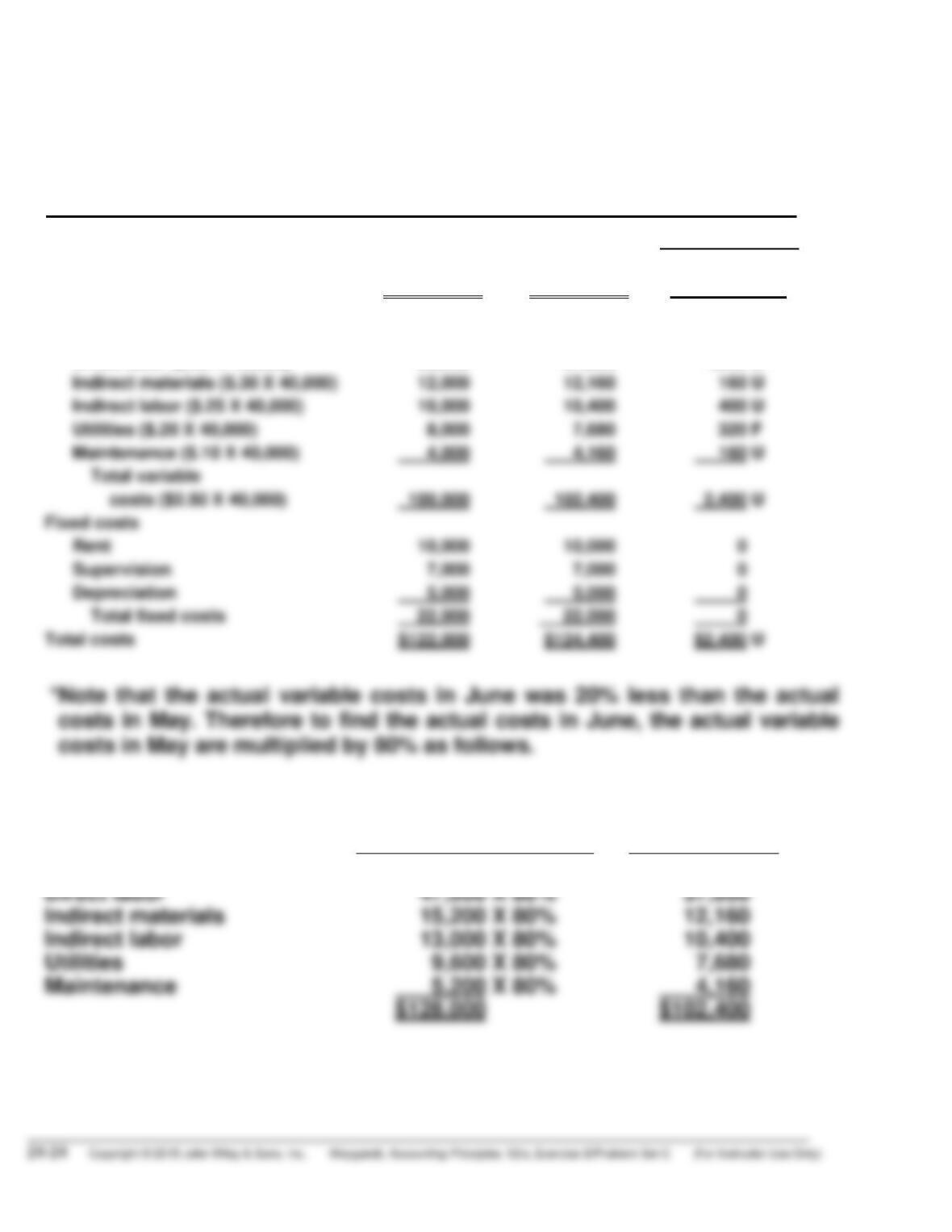

(c) ANSON COMPANY

Packaging Department

Budget Report (Flexible)

For the Month Ended June 30, 2017

Difference

Units

Variable costs

Direct materials ($.75 X 40,000)

Direct labor ($.90 X 40,000)

Indirect materials ($.30 X 40,000)

Indirect labor ($.25 X 40,000)

Budget at

40,000 Units

$ 30,000

36,000

12,000

10,000

Actual Costs

40,000 Units

$ 30,400*

37,600

12,160

10,400

Favorable F

Unfavorable U

$ 400 U

1,600 U

160 U

400 U

*Note that the actual variable costs in June was 20% less than the actual

costs in May. Therefore to find the actual costs in June, the actual variable

costs in May are multiplied by 80% as follows.

May

(actual)

June

(actual)

Direct materials

$ 38,000 X 80%

=

$ 30,400

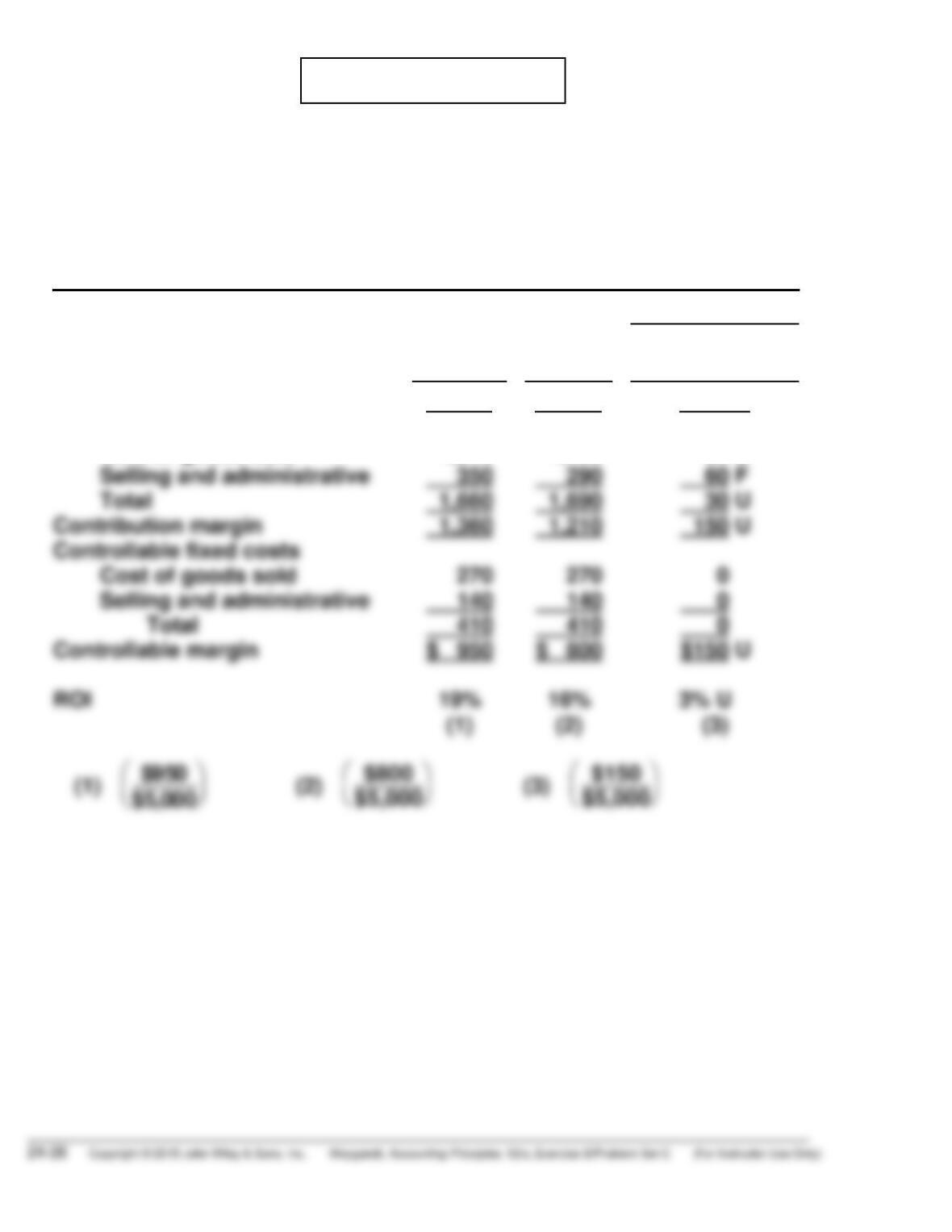

PROBLEM 24-4C

(a) ARLEN MANUFACTURING INC.

Electronics Division

Responsibility Report

For the Year Ended December 31, 2017

Difference

Budget

Actual

Favorable F

Unfavorable U

Sales

Variable costs

Cost of goods sold

$2,400,000

1,200,000

$2,200,000

1,260,000

$200,000 U

60,000 U

(b) The manager did not effectively control revenues and costs. Contribution

margin was $252,000 unfavorable and controllable margin was $246,000

unfavorable. Contribution margin was unfavorable primarily because

PROBLEM 24-5C

(a) MARX MANUFACTURING COMPANY

Weedeater Division

Responsibility Performance Report

For the Year Ended December 31, 2016

(in thousands of dollars)

Difference

Budget

Actual

Favorable F

Unfavorable U

Sales

Variable costs

Cost of goods sold

Selling and administrative

$3,020

1,310

350

$2,900

1,400

290

$120 U

90 U

60 F

PROBLEM 24-5C (Continued)

(b) The performance of the manager of the Weedeater Division was below

budget expectations for the year. The item that top management should

likely investigate first is the reason why sales were $120,000 below

PROBLEM 24-6C

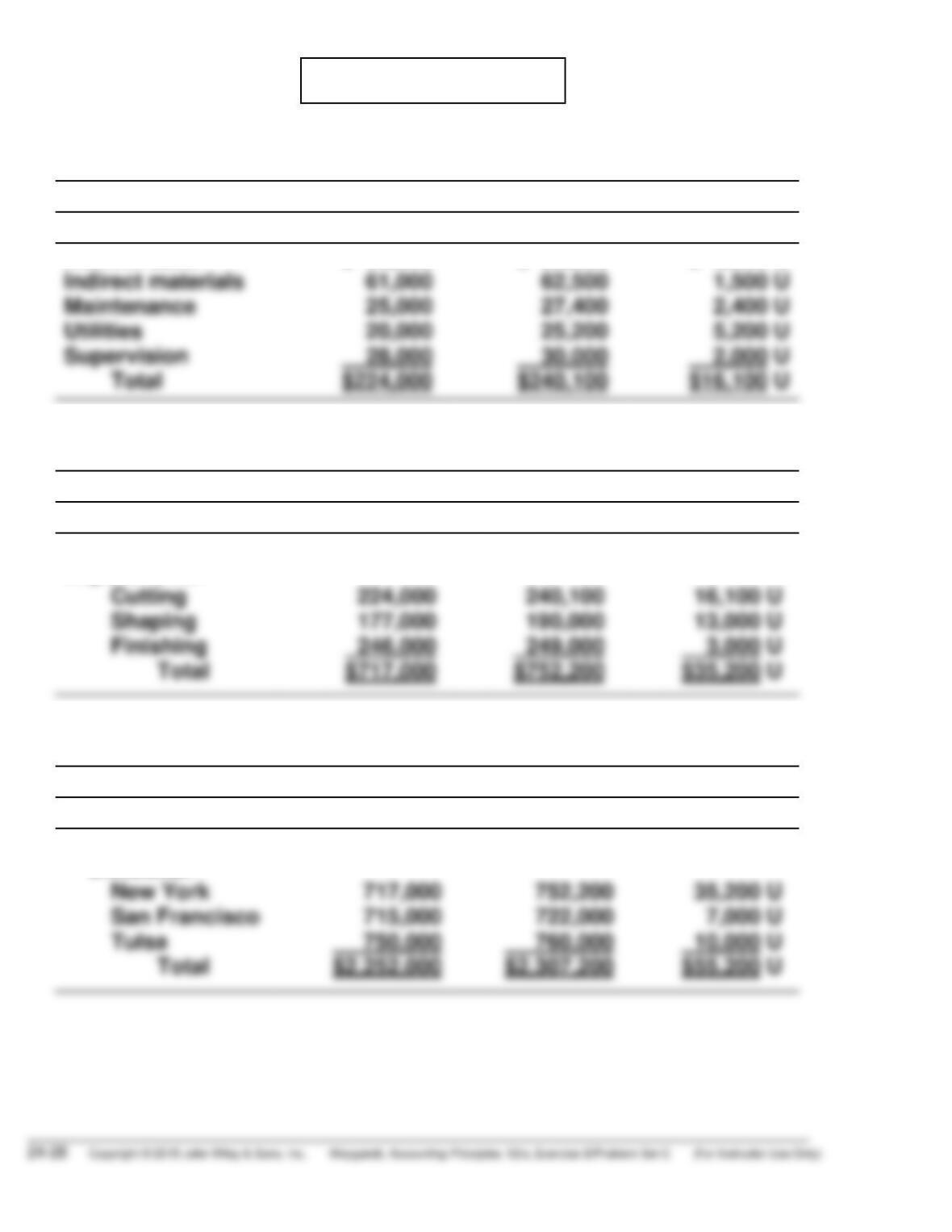

(a) No. 1

To Cutting Department Manager—New York Division Month: January

Controllable Costs:

Budget

Actual

Fav/Unfav

Indirect labor

Indirect materials

$ 90,000

61,000

$ 95,000

62,500

$ 5,000 U

1,500 U

No. 2

To Division Production Manager—New York Month: January

Controllable Costs:

Budget

Actual

Fav/Unfav

New York Division

Departments:

Cutting

$ 70,000

224,000

$ 73,100

240,100

$ 3,100 U

16,100 U

No. 3

To Vice-President—Production Month: January

Controllable Costs:

Budget

Actual

Fav/Unfav

V-P Production

Divisions:

$ 70,000

$ 73,000

$ 3,000 U

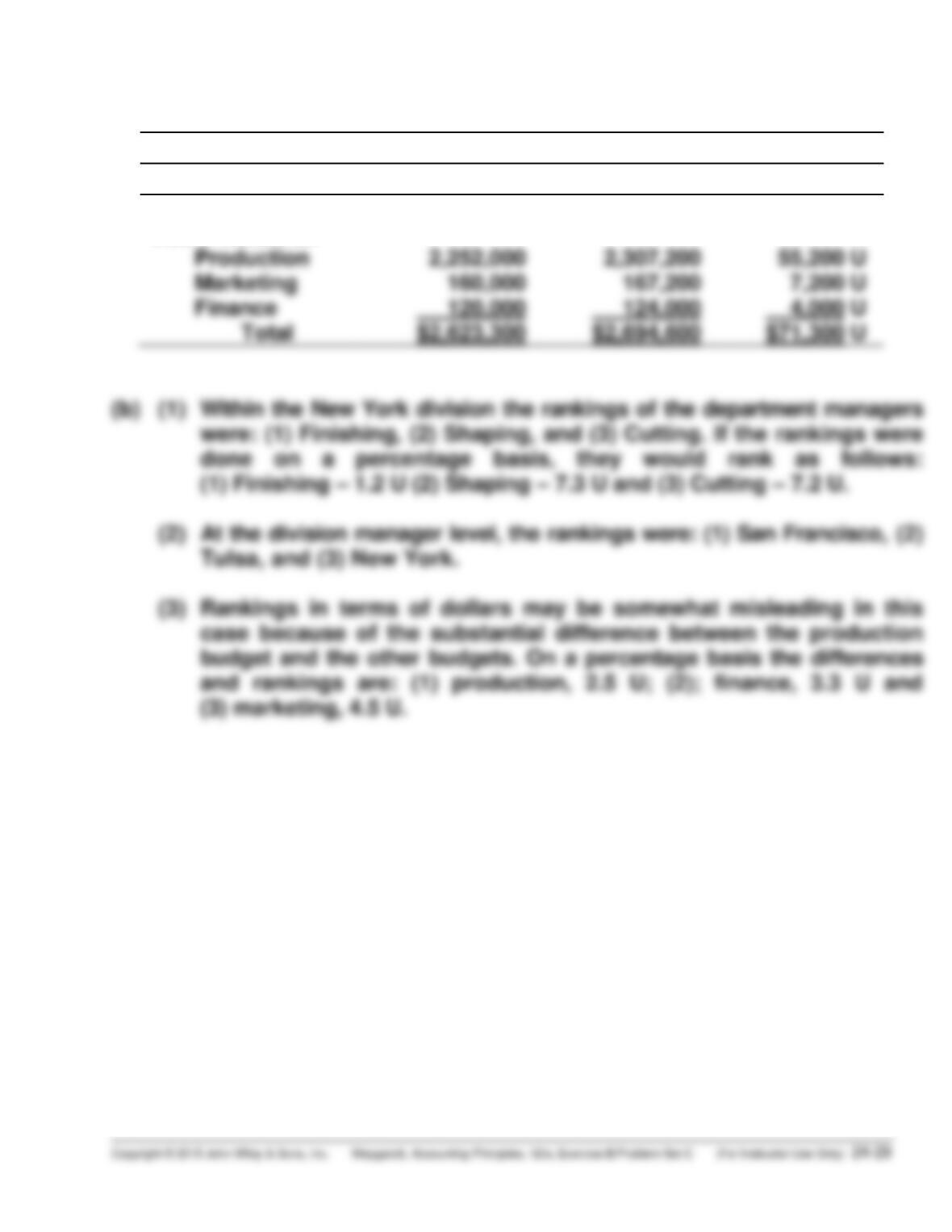

PROBLEM 24-6C (Continued)

No. 4

To President Month: January

Controllable Costs:

Budget

Actual

Fav/Unfav

President

Vice-Presidents:

Production

Marketing

$ 91,300

2,252,000

160,000

$ 96,200

2,307,200

167,200

$ 4,900 U

55,200 U

7,200 U