Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

1445

Exercise 24-12 (20 minutes)

(1)

Division

Operating

income

Average assets*

Return on

investment

(2)

Division

Operating

income

Sales

Profit margin

(3)

Division

Sales

Average assets*

Investment

turnover

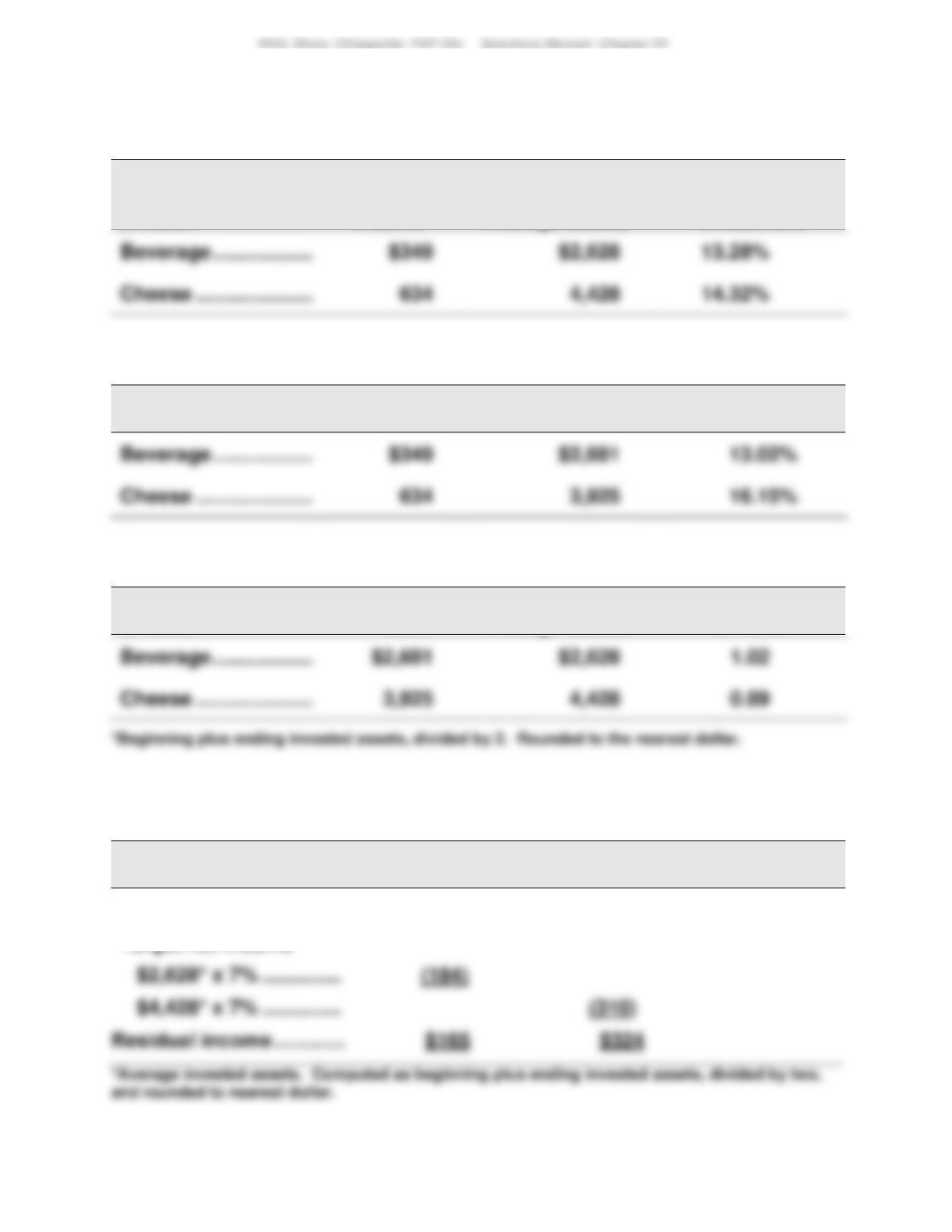

Exercise 24-13 (10 minutes)

($ millions)

Beverage

Cheese

Operating income ........

$349

$634

Target net income

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 24

1446

Exercise 24-14 (15 minutes)

Geographic segment

Operating

income

Sales

Profit margin

Exercise 24-15 (20 minutes)

1. Return on investment = $1,000,000/$12,500,000 = 8%

Exercise 24-16 (20 minutes)

1447

Exercise 24-17 (15 minutes)

Exercise 24-18 (15 minutes)

Part 1

Process time ..............................................................................

6.0 days

Part 2

Part 3

1448

Exercise 24-19 (15 minutes)

Part 1

Process time ..............................................................................

16.0 hours

Part 2

Part 3

To increase the manufacturing cycle efficiency to 0.80 Best Ink needs to

1449

Exercise 24-20B (15 minutes)

1. If the trailer division is currently operating at full capacity, its manager

2. If the trailer division is currently producing 20,000 trailers and the

3. The trailer division would prefer a transfer price of $140 per trailer, since

1450

Exercise 24-21C (20 minutes)

Preliminary calculations

Land cost ................................................................

$4,000,000

Allocated cost—value basis of allocation: $7,500,000

Market

% of

Allocated

Average

Value

Total

Cost

Lot Cost

1451

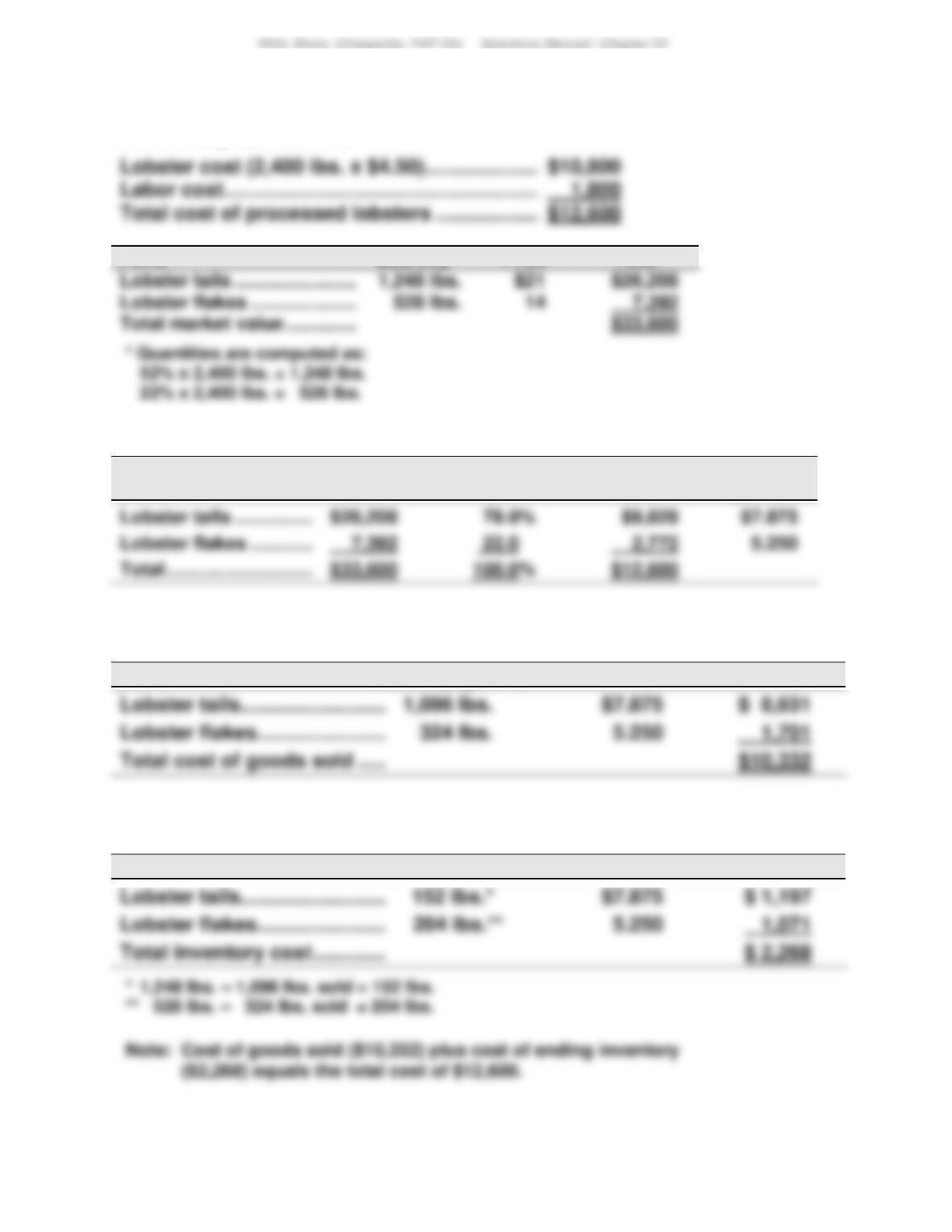

Exercise 24-22C (25 minutes)

Preliminary calculations

Parts

Quantity*

Price

Total

Allocated cost—value basis allocation: $12,600

Market

% of

Allocated

Cost

Parts

Value

Total

Cost

per lb.

(1) Cost of goods sold

Parts

Quantity (given)

Cost

Total

(2) Cost of ending inventory

Parts

Quantity

Cost

Total

1452

Exercise 24-23 (20 minutes)

(1) Profit margin = Income/Sales

Division

Income*

Sales*

Profit margin

(2) Investment turnover = Sales/Average invested assets

Investment center

Sales*

Avg. assets*

Investment

turnover

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 24

1453

PROBLEM SET A

Problem 24-1A (50 minutes)

Part 1

a.

Responsibility Accounting Performance Report

Dept. Manager, Camper Department

For the Year

Budgeted

Actual

Over (Under)

Amount

Amount

Budget

Controllable Costs

b.

Responsibility Accounting Performance Report

Dept. Manager, Trailer Department

For the Year

Budgeted

Actual

Over (Under)

Amount

Amount

Budget

Controllable Costs

Raw materials ................................

$275,000

$273,200

$(1,800)

1454

Problem 24-1A (Continued)

c.

Responsibility Accounting Performance Report

Plant Manager, Indiana Plant

For the Year

Budgeted

Actual

Over (Under)

Amount

Amount

Budget

Controllable Costs

Dept. manager salaries ................

$ 95,000

$ 97,500

$ 2,500

Part 2

The plant manager did a better job of controlling costs and meeting the

1455

Problem 24-2A (60 minutes)

Part 1

Part 2

Market rates are used to allocate occupancy costs for depreciation,

interest, and taxes. Heating, lighting, and maintenance costs are allocated

1456

Problem 24-2A (Continued)

Value-based costs are allocated to departments in two steps

(i) Compute market value of each floor

Floor

Square

Footage

Value per

Sq. Ft.

Total

(ii) Allocate $54,000 to each floor based on its percent of market value

Floor

Market

Value

% of

Total

Allocated

Cost

Cost per

Sq. Ft.

We can then compute total allocation rates for the floors

Floor

Value

Usage

Total

These rates are applied to allocate occupancy costs to departments

Department

Square

Footage

Rate

Total

Part 3

A second-floor manager would prefer allocation based on market value. This is a

1457

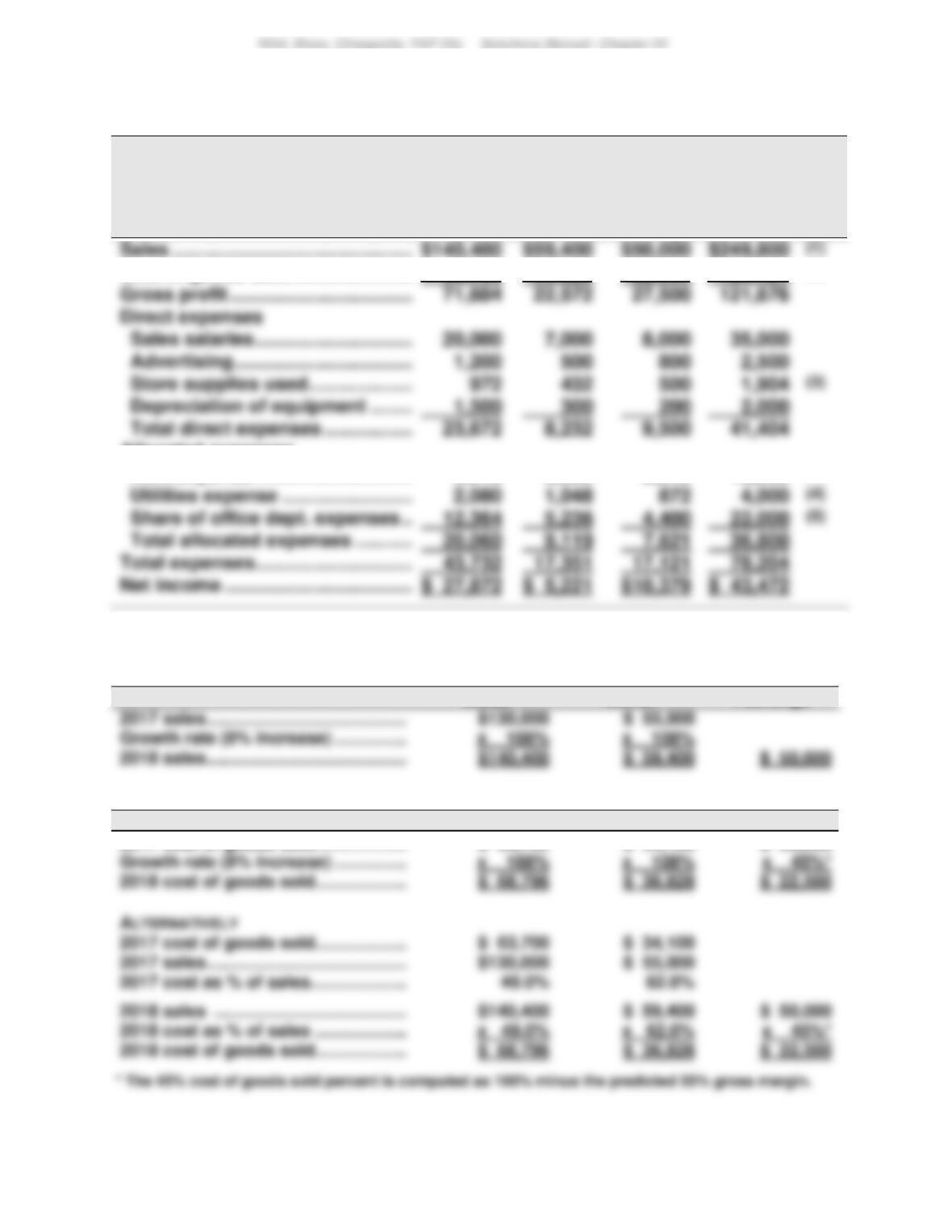

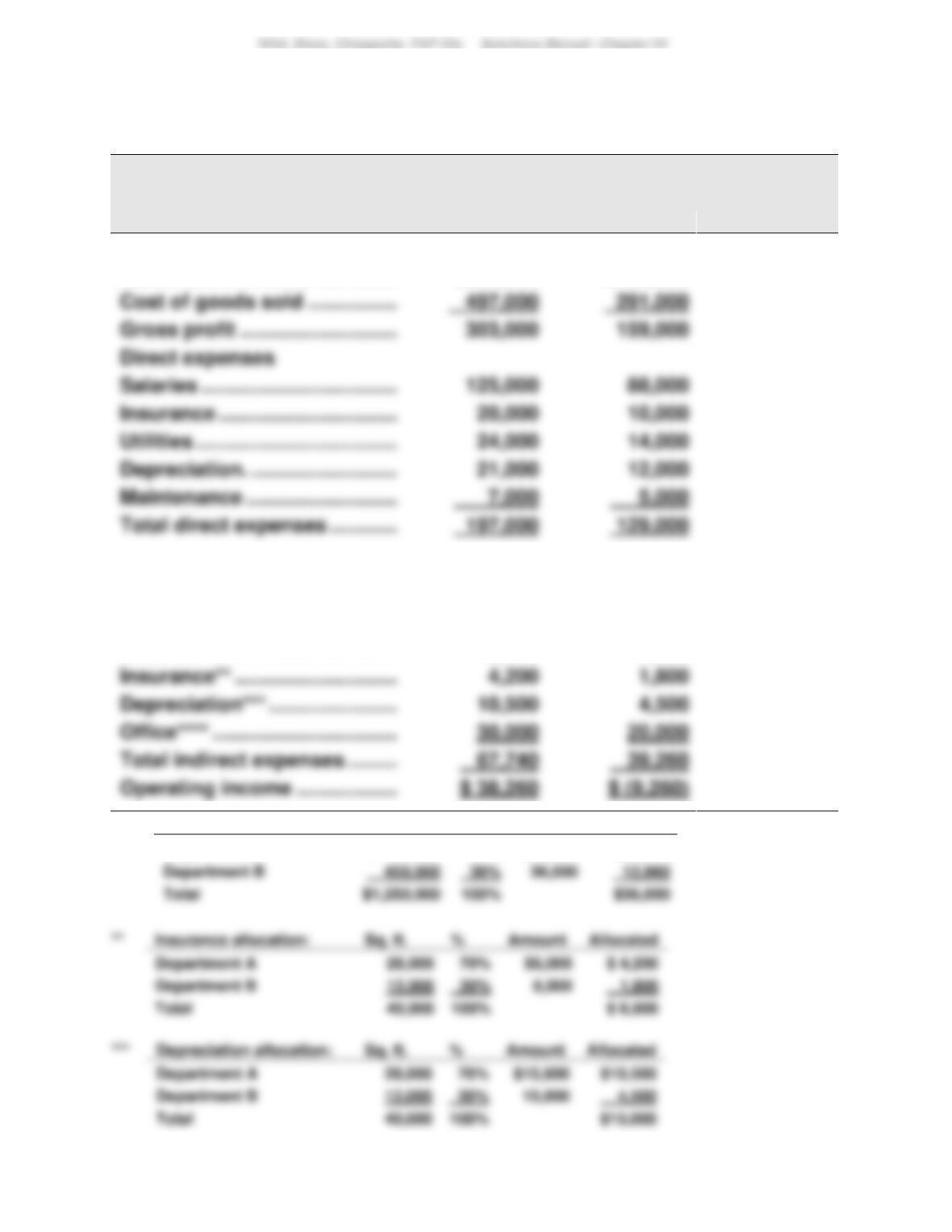

Problem 24-3A (70 minutes)

Williams Company

Forecasted Departmental Income Statements

For Year Ended December 31, 2018

Clock

Mirror

Paintings

Combined

Cost of goods sold ........................

68,796

36,828

22,500

128,124

(2)

Allocated expenses

Rent expense ...............................

5,616

2,835

2,349

10,800

(4)

Supporting Computations—coded (1) through (5) in statement above

Note 1 (Sales)

Clock

Mirror

Paintings

Note 2 (Cost of Goods Sold)

Clock

Mirror

Paintings

2017 cost of goods sold ...................

$ 63,700

$ 34,100

$ 50,000

1458

Problem 24-3A (Continued)

Note 3 (Store Supplies Used)

Clock

Mirror

Paintings

2017 store supplies used ....................

$ 900

$ 400

1459

Problem 22-4A (45 minutes)

Part 1

VORTEX COMPANY

Departmental Contribution Statements

Dept. A

Dept. B

Sales ........................................

$800,000

$450,000

Departmental contributions to

overhead ...............................

Allocated indirect expenses

106,000

30,000

Salaries* ..................................

23,040

12,960

*

Salaries allocation:

Sales

%

Amount

Allocated

Department A

$ 800,000

64%

$36,000

$23,040

1460

Problem 22-4A (Concluded)

****

Office expense allocation:

Employees

%

Amount

Allocated

Department A

75

60%

$50,000

$30,000

Part 2

Although Department B has a negative departmental income, it is

1461

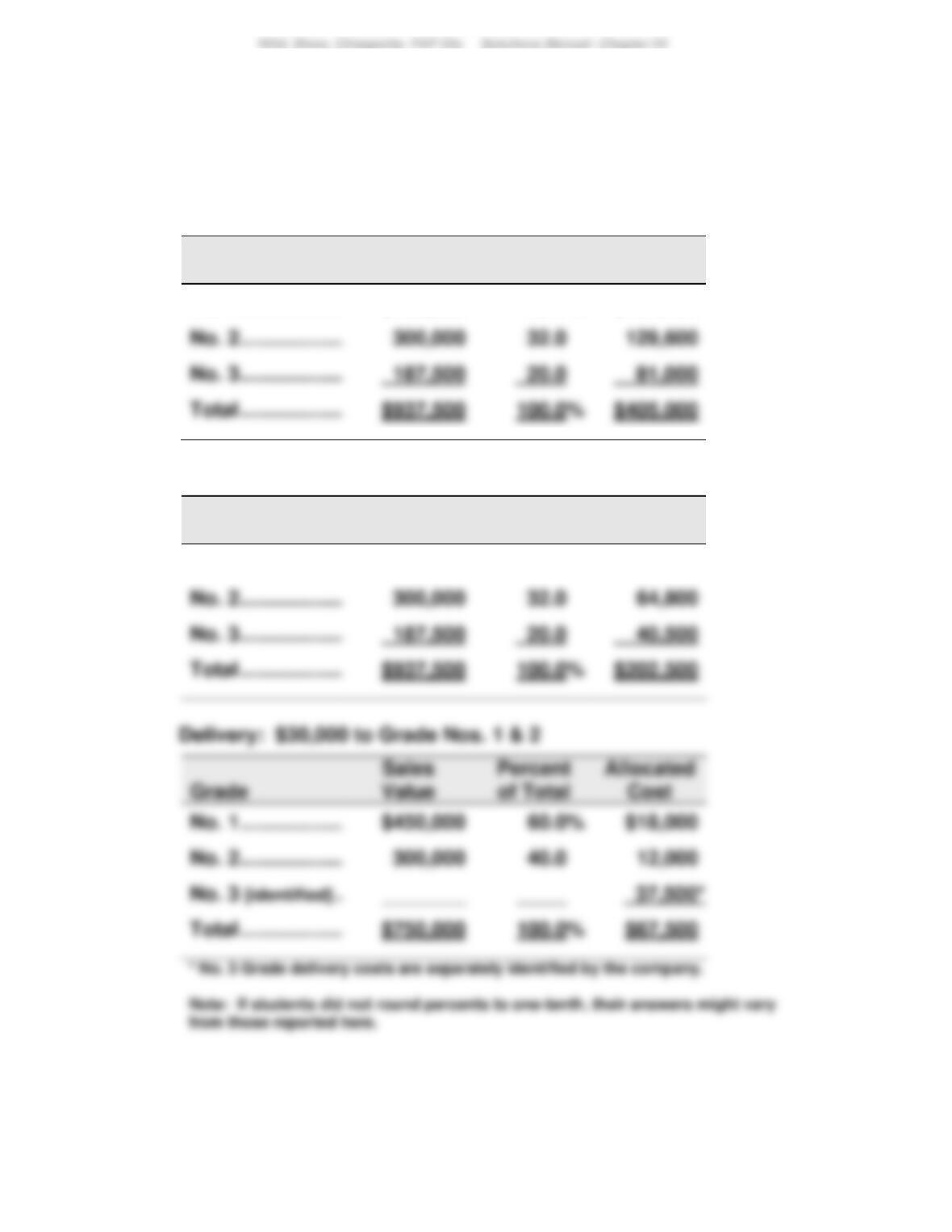

P

Problem 24-5AC (60 minutes)

Part 1

Allocations of joint costs on the basis of sales values

Tree pruning and care: $405,000

Grade

Sales

Value

Percent

of Total

Allocated

Cost

No. 1 ...............................

$450,000

48.0%

$194,400

Picking, sorting, and grading: $202,500

Grade

Sales

Value

Percent

of Total

Allocated

Cost

No. 1 ...............................

$450,000

48.0%

$ 97,200

1462

Problem 24-5AC (Continued)

Part 2

GEORGIA ORCHARDS

Income Statement

For Year Ended December 31, 2017

No. 1

No. 2

No. 3

Combined

Sales (by grade)

No. 1: 300,000 lbs. @ $1.50 ............

$450,000

Part 3

Delivery costs include both crating and hauling costs. Georgia is able to

identify the portion of the cost directly related to the No. 3 peaches,