Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 24

1425

Chapter 24

Performance Measurement and

Responsibility Accounting

QUESTIONS

1. Many companies are divided into departments when they become too large to be

effectively managed as single units. This division into departments is often needed

2. Operating departments are directly involved in manufacturing or selling the

3. Controllable costs of a department are those that the department’s manager has the

power to control, determine or at least strongly influence. The manager does not

have the power to control, determine or influence the amounts of uncontrollable

5. Reports to higher-level managers are usually summarized in responsibility

7. Not usually; a cost center cannot usually be evaluated in terms of its profitability

8. Direct expenses of a department are expenses that are incurred for the sole benefit

of that department—there is little doubt about which department should be charged

9. a) Sales of the departments or the number of employees in each department.

b) Square feet of floor space, perhaps adjusted for its value.

10. A department’s contribution to overhead is measured by subtracting its direct

11. The individual responsible for controlling the cost needs timely reports with specific

12. A transfer price is an amount used to record transactions made between divisions

13.B A market-based transfer price is most likely to be used when a) the item being

14.C A joint cost is incurred to produce or purchase two or more different products at the

15. a) It is useful to know the amount of sales for each department as well as direct

costs for each department. This information can help assess the effectiveness of

16. Controllable cost examples — labor of department, packaging supplies, office

17. Cycle time is the time it takes a company to produce a product or service. Its

18. Value-added time provides value to a product or service from a customer’s

perspective. Non-value added time provides no value to the customer. Value-added

1427

19. Cycle efficiency is the ratio of value-added time divided by total cycle time. The

closer cycle efficiency is to 1, the more of a company’s time is spent on value-added

20. Yes. Samsung can use cycle time and cycle efficiency to measure operating

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 24

1428

QUICK STUDIES

Quick Study 24-1 (10 minutes)

Quick Study 24-2 (10 minutes)

Possible allocation bases for these indirect expenses and service

department expenses include:

1. Proportion of total processing time for each factory department; or

3. Proportion of total time in each department for maintenance; or

Quick Study 24-3 (5 minutes)

1429

Quick Study 24-4 (10 minutes)

Controllable costs for the service department would include:

Quick Study 24-5 (10 minutes)

% of

Advertising to

Allocated

Department

Sales

Total

allocate

amount

1 …………………………………

2 …………………………………

400,000

3 …………………………………

Quick Study 24-6 (10 minutes)

% of

Admin. Exp.

Allocated

Department

Employees

Total

to allocate

amount

Mixing …………………………

Bottling ……………………….

Quick Study 24-7 (10 minutes)

% of

Maint. Exp.

Allocated

Department

Sq. Feet

Total

to allocate

amount

Mixing …………………………

Bottling ……………………….

1430

Quick Study 24-8 (15 minutes)

The first step is to allocate total rent expense between the two floors.

Amount

Allocated

% of Total

Cost

$ 84,500

$130,000

The second step is to allocate these portions of total rent expense across

the departments occupying the two floors

First Floor

Sq. Feet

% of Total

Cost

Jewelry Dept. ……………………..

1,440

30%

$25,350

Totals …………………………..

4,800

$84,500

Second Floor

Sq. Feet

% of Total

Cost

Housewares Dept. ………………

2,016

42%

$19,110

1,824

1431

Quick Study 24-9 (15 minutes)

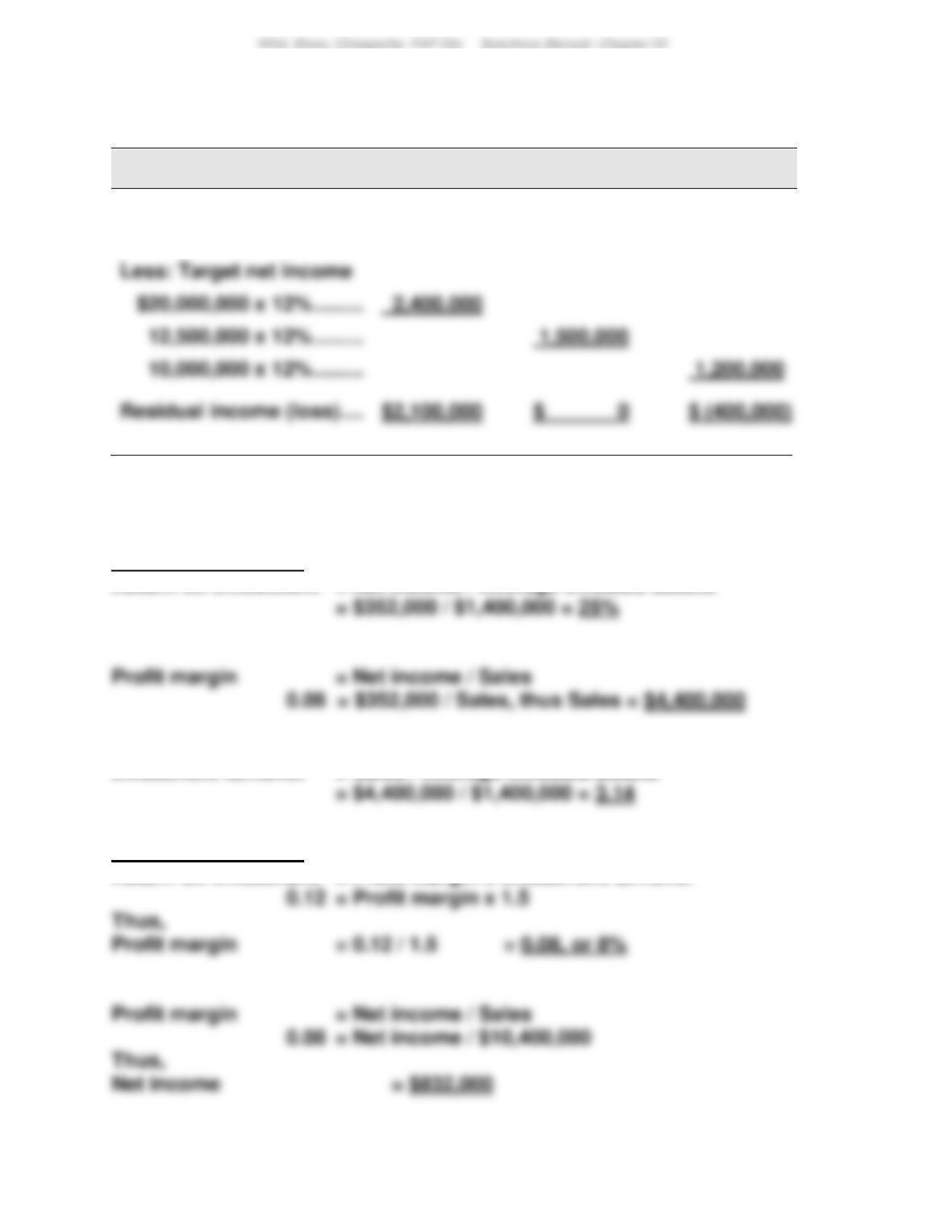

Departmental contribution to overhead

Dept. A: $18,815 – $ 3,660 = $15,155

Quick Study 24-10 (10 minutes)

Investment Center

Income

Average Assets

Return on

Investment

Cameras and

camcorders ……………….

$4,500,000

$20,000,000

22.5%

12.0%

1432

Quick Study 24-11 (10 minutes)

Cameras &

camcorders

Phones &

communication

Computers &

accessories

Net income …………………………

$4,500,000

$1,500,000

$ 800,000

Quick Study 24-12 (15 minutes)

Investment center A:

Return on investment = Net income / Average invested assets

Investment turnover = Sales / Average invested assets

Investment center B:

Return on investment = Profit margin x Investment turnover

Quick Study 24-12 (continued)

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 24

Investment turnover = Sales / Average invested assets

Quick Study 24-13 (10 minutes)

Quick Study 24-14 (5 minutes)

4. I 8. C

Quick Study 24-15 (10 minutes)

Process Perspective Actual Target Trend

Quick Study 24-16 (10 minutes)

a.

Process time ……………………………………………………………………

15.0 minutes

Move time ………………………………………………………………………..

Wait time …………………………………………………………………………

36.6 minutes

Manufacturing cycle time …………………………………………………

60.0 minutes

Manufacturing cycle efficiency (15.0 min./ 60.0 min.) ………..

Quick Study 24-17B (10 minutes)

Without excess capacity, a market-based transfer price of $450 per

Quick Study 24-18B (10 minutes)

If the windshield division has excess capacity, a range of acceptable

Quick Study 24-19C (15 minutes)

Total joint cost = $325,000 + $50,000 = $375,000

1435

Quick Study 24-20 (5 minutes)

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 24

1436

EXERCISES

Exercise 24-1 (15 minutes)

Responsibility Accounting Performance Report

Dept. Manager, Snowmobile Department

For the Year

Budgeted

Actual

Over (Under)

Amount

Amount

Budget

Controllable Costs

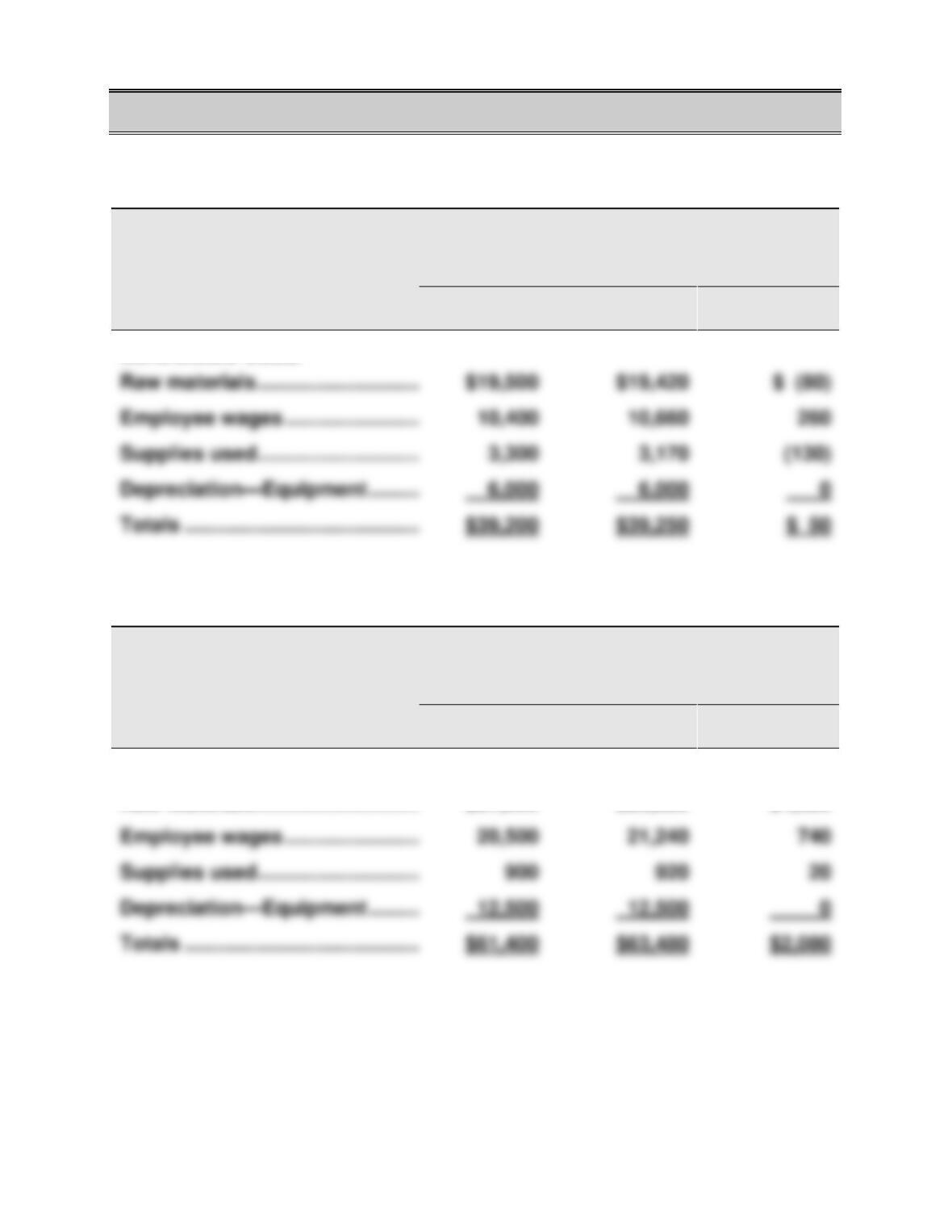

Exercise 24-2 (15 minutes)

Responsibility Accounting Performance Report

Dept. Manager, ATV Department

For the Year

Budgeted

Actual

Over (Under)

Amount

Amount

Budget

Controllable Costs

Raw materials …………………………..

$27,500

$28,820

$1,320

Supplies used …………………………..

1437

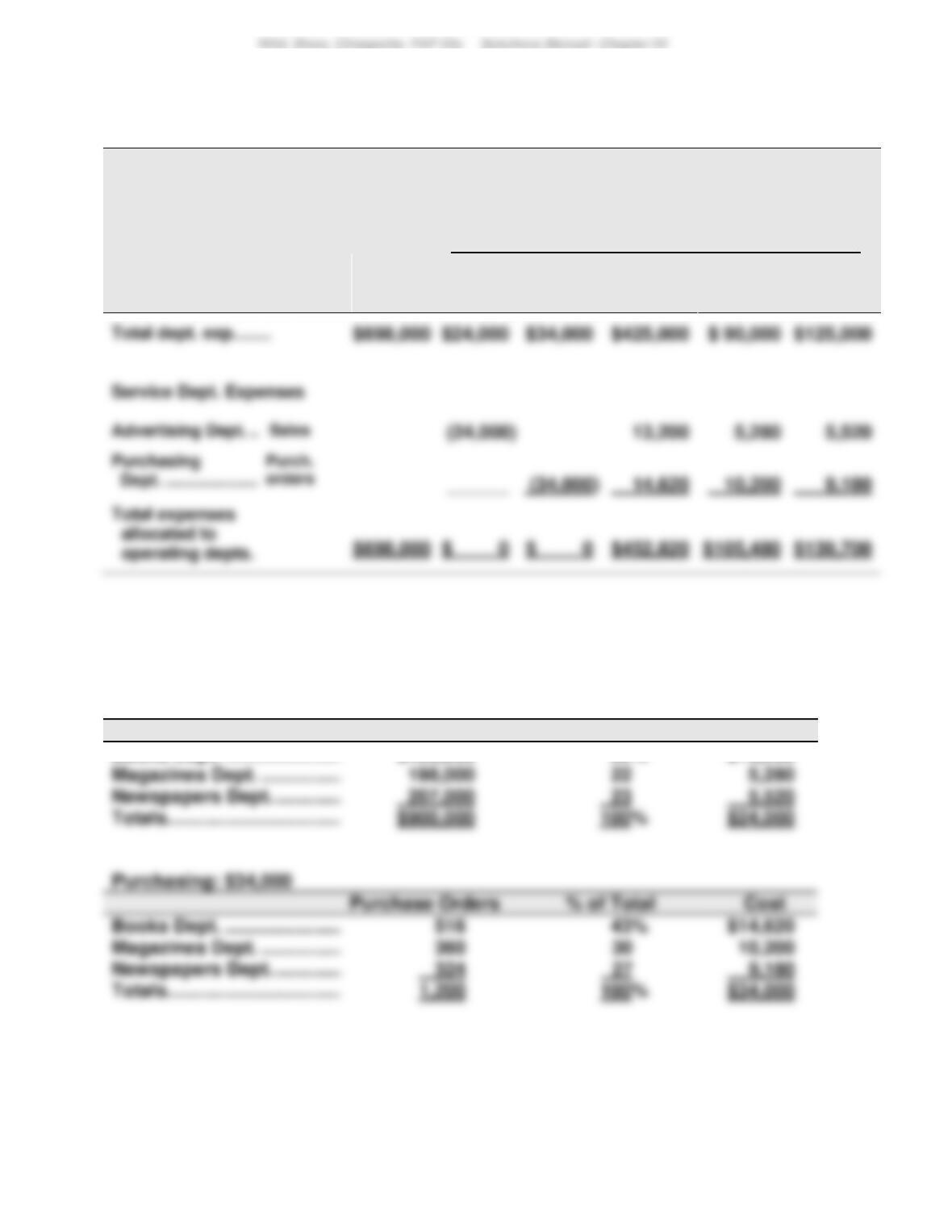

Exercise 24-3 (25 minutes)

COZY BOOKSTORE

Departmental Expense Allocation Spreadsheet

For Period Ended _______

Allocation of Expenses to Departments .

Alloca-

tion Base

Exp.

Account

Balance

Adver-

tising

Dept.

Purch-

asing

Dept.

Books

Dept.

Maga-

zines

Dept.

News-

papers

Dept.

Computations for allocations of service dept. costs to operating departments

Advertising: $24,000

Sales

% of Total

Cost

Books Dept. ………………………….

$495,000

55%

$13,200

Magazines Dept. ……………………

22

Newspapers Dept. …………………

Books Dept. ………………………….

$14,620

Magazines Dept. ……………………

Newspapers Dept. …………………

1438

Exercise 24-4 (20 minutes)

Allocation of annual wages between the two departments

Hours Worked*

% of Total

Cost

*Computation of hours worked in the two selling departments

Jewelry department

57 hours

Cosmetics department

Total hours ……………………………………………….

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 24

1439

Exercise 24-5 (25 minutes)

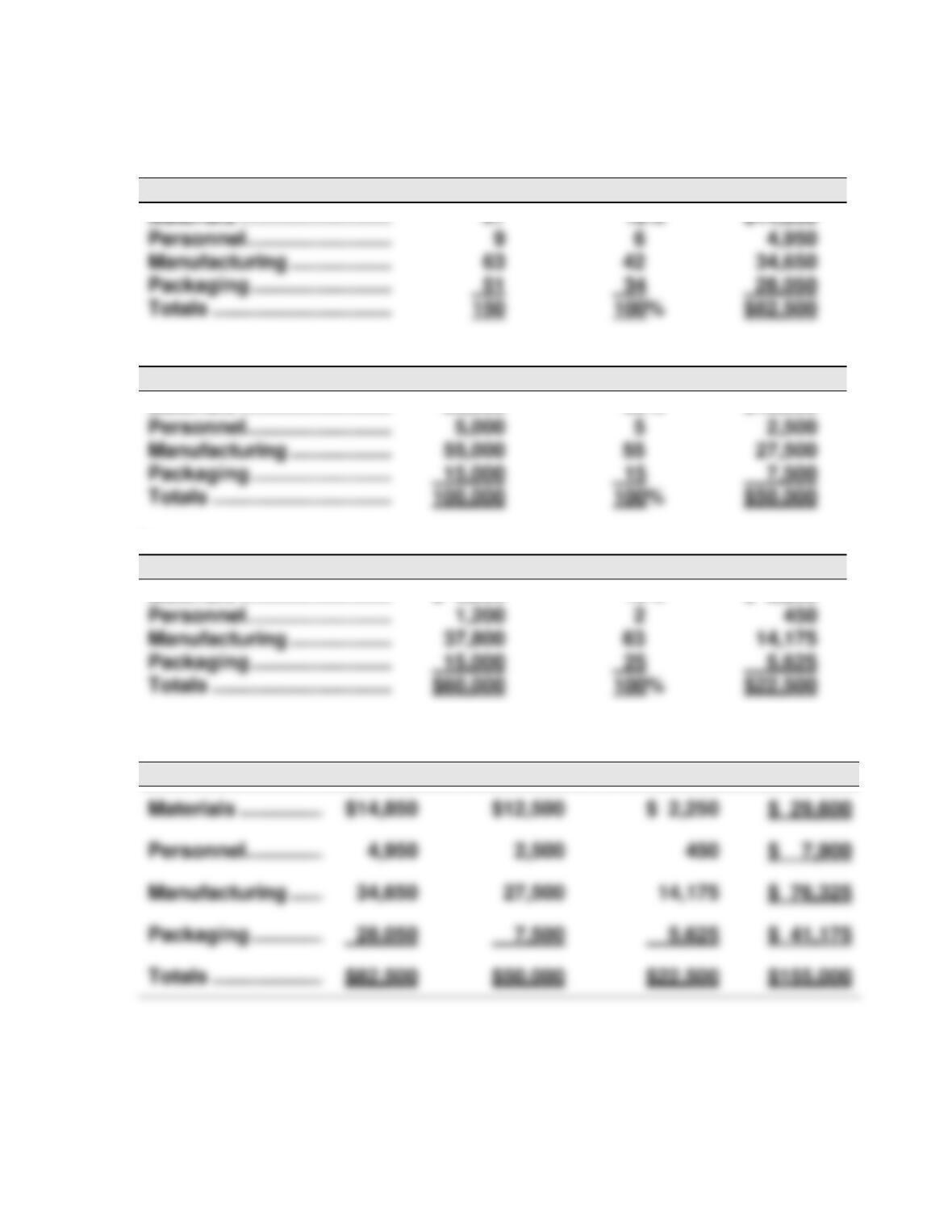

1. Allocation of Indirect Expenses to Four Operating Departments

Supervision expenses

Department

Employees

% of Total

Cost

Utilities expenses

Department

Square Feet

% of Total

Cost

Materials …………………………..

25,000

25%

$12,500

Personnel …………………………..

Manufacturing ……………………

55,000

Packaging ………………………….

Totals …………………………..

100,000

$50,000

Insurance expenses

Department

Assets Value

% of Total

Cost

Materials …………………………..

$ 6,000

10%

$ 2,250

Personnel …………………………..

Manufacturing ……………………

37,800

Packaging ………………………….

Totals …………………………..

$60,000

$22,500

2. Report of Indirect Expenses Assigned to Four Operating Departments

Supervision

Utilities

Insurance

Total

Materials …………………………..

18%

$14,850

Personnel …………………………..

Manufacturing ……………………

Packaging ………………………….

Totals …………………………..

$82,500

1440

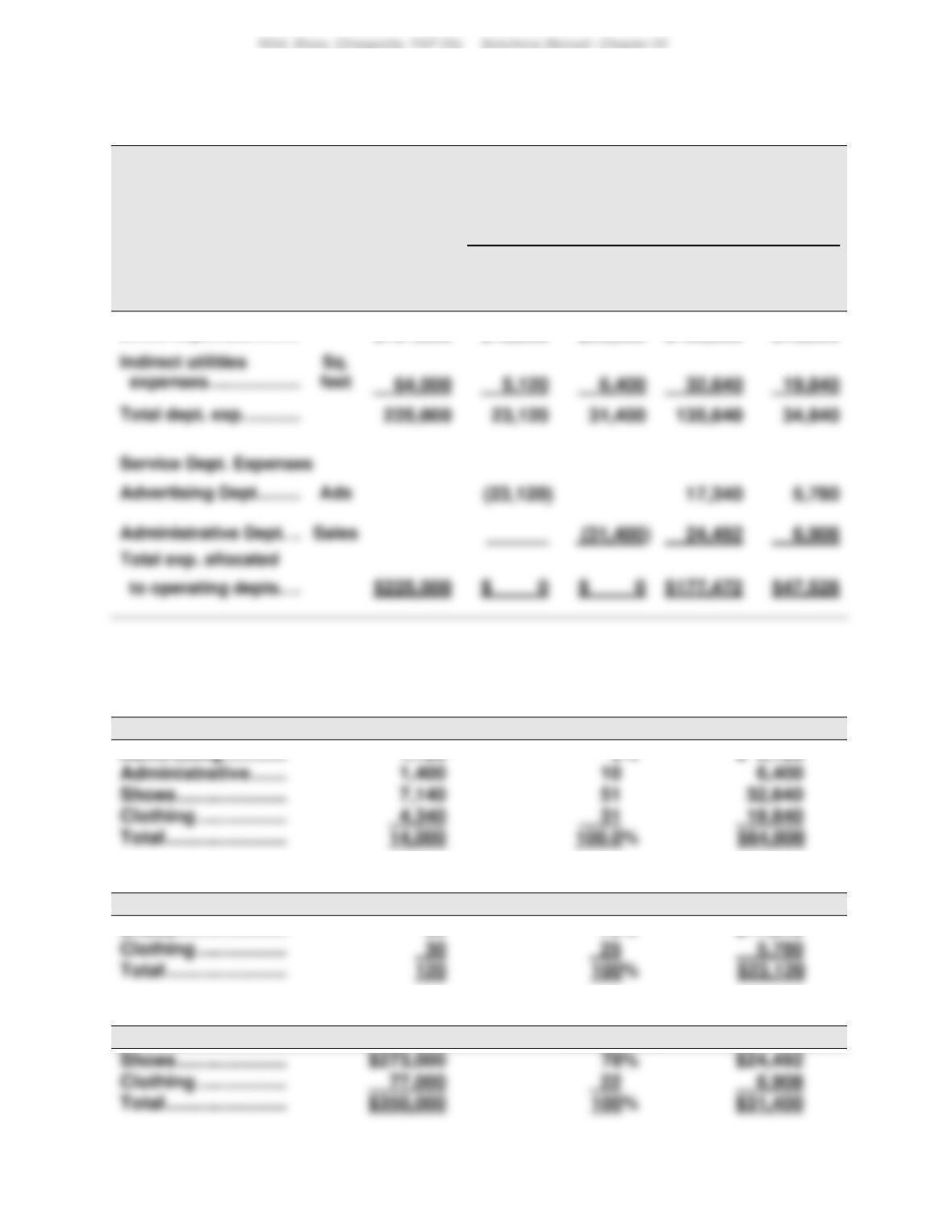

Exercise 24-6 (20 minutes)

MARATHON RUNNING SHOP

Departmental Expense Allocation Spreadsheet

For Year Ended December 31, 2017

Allocation of Expenses to Departments .

Alloca-

tion

Base

Expense

Account

Balance

Adver-

tising

Dept.

Admini-

strative

Dept.

Shoes

Dept.

Clothing

Dept.

Direct expenses …………

$161,000

$18,000

$25,000

$103,000

$15,000

Total dept. exp. ………….

225,000

135,640

Advertising Dept.……….

$225,000

$177,472

$47,528

Supporting expense allocation calculations

Utilities expense: $64,000

Square Feet

% of Total

Cost

Advertising …………

1,120

8%

$ 5,120

Administrative …….

1,400

Shoes …………………

7,140

Clothing ……………..

Advertising expense: $23,120

Ads Placed

% of Total

Cost

Shoes …………………

90

75%

$17,340

Clothing ……………..

Administrative expense: $31,400

Sales

% of Total

Cost

Shoes …………………

$24,492

(1)

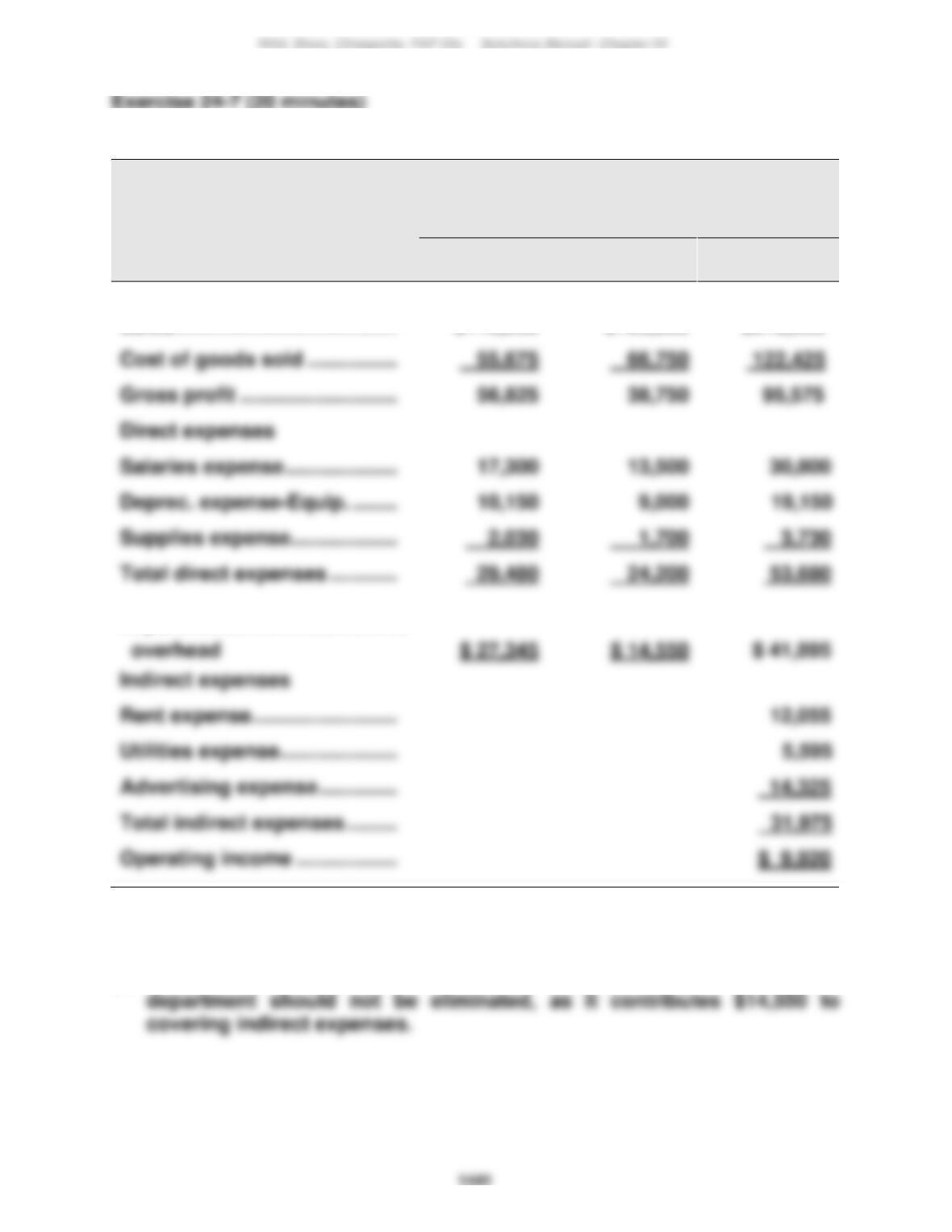

WHOLESALE GUITARS

Departmental Contribution Statements

For Year Ended December 31, 2017

Acoustic

Electric

Dept.

Dept.

Combined

Sales ………………………………….

$112,500

$105,500

$218,000

Departmental contributions to

(2) Based on departmental contribution to overhead, the electric guitar

1442

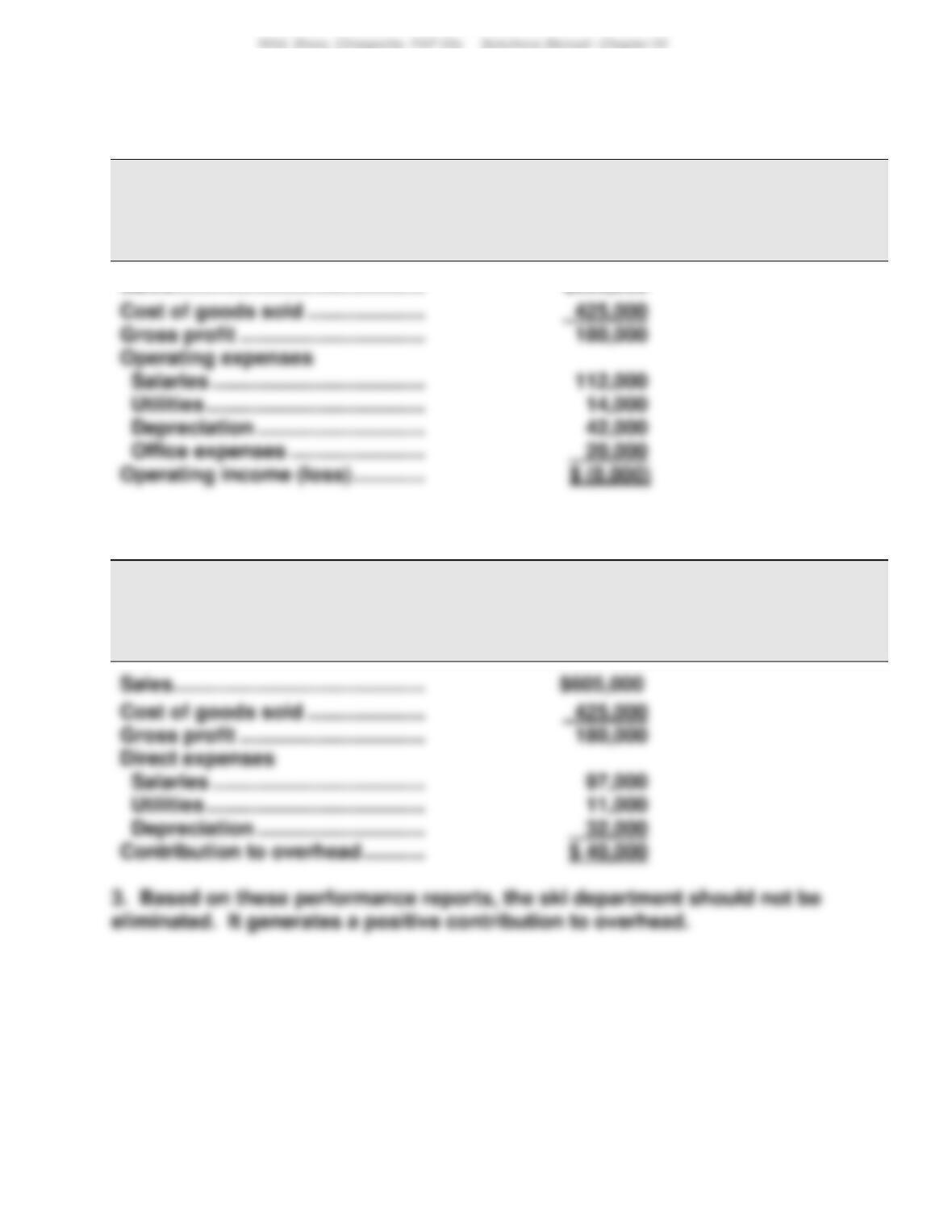

Exercise 24-8 (25 minutes)

1.

JANSEN COMPANY

Departmental Income Statement—Ski Department

For Year Ended December 31, 2017

Ski Dept.

Sales ………………………………………

$605,000

2.

JANSEN COMPANY

Departmental Contribution to Overhead—Ski Department

For Year Ended December 31, 2017

Ski Dept.

Sales ………………………………………

1443

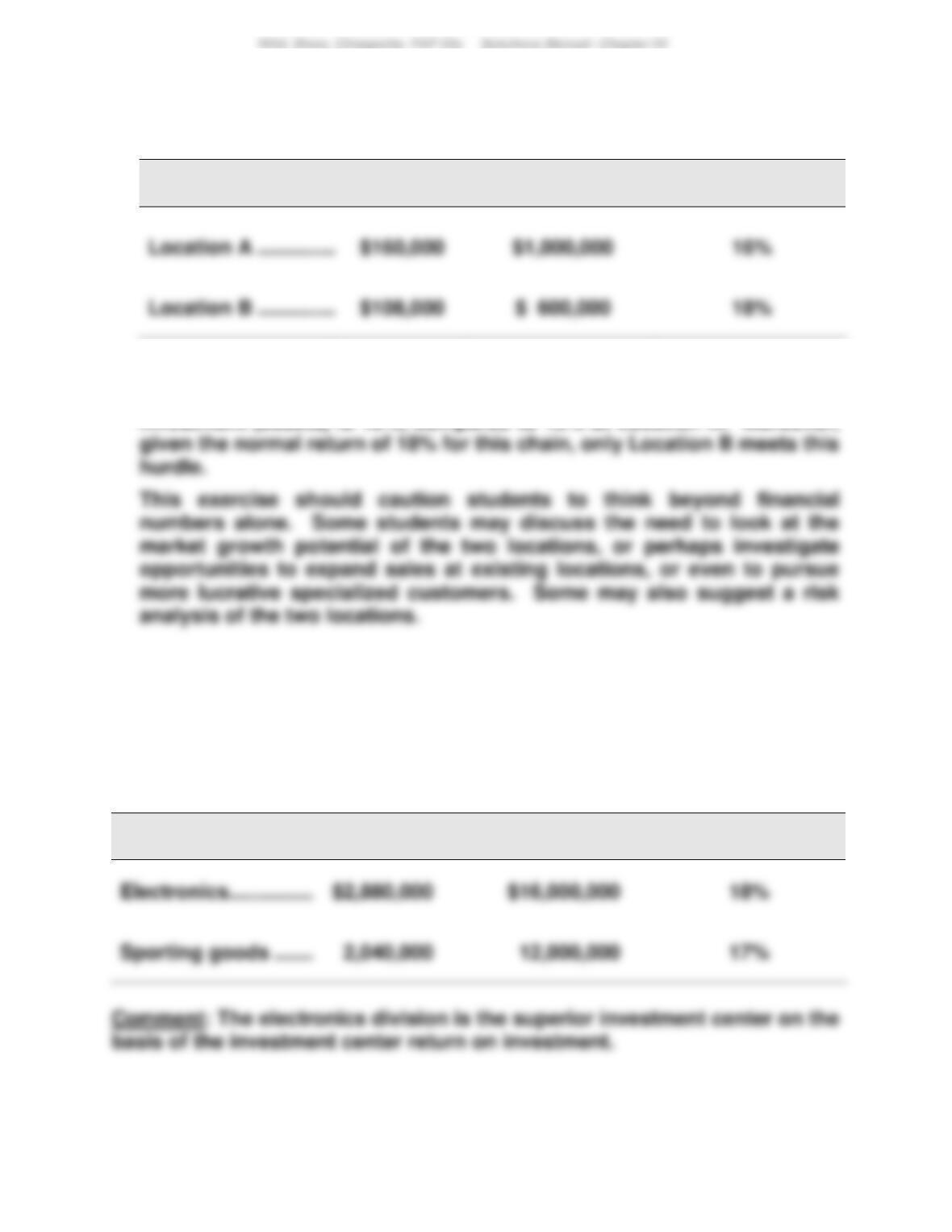

Exercise 24-9 (15 minutes)

1.

Location

Net income

Average assets

Return on

investment

2. The recommendation is to pursue Location B because its return on

investment (assets) is 18%, compared to 16% at Location A. Moreover,

Exercise 24-10 (20 minutes)

(1)

Investment center

Income

Average assets

Return on

investment

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 24

1444

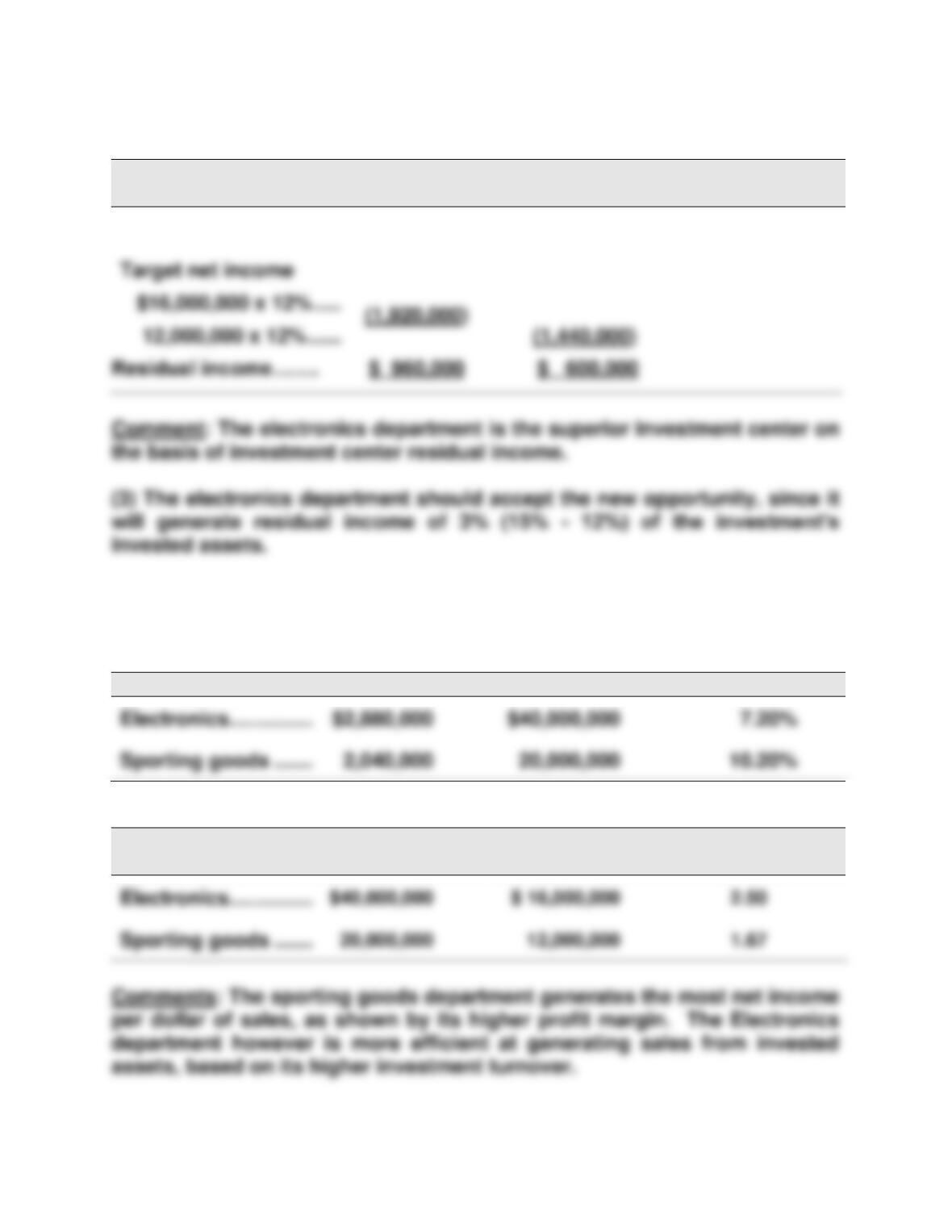

Exercise 24-10 (continued)

(2)

Investment Center

Electronics

Sporting goods

Net income ………………..

$2,880,000

$2,040,000

Exercise 24-11 (15 minutes)

Investment Center

Income

Sales

Profit margin

Investment Center

Sales

Average assets

Investment

turnover