CHAPTER 24 Differential Analysis and Product Pricing

Prob. 24–6A (FIN MAN); Prob. 9–6A (MAN)

1.

High Good Regular

Grade Grade Grade

Selling price………………………………………… $280 $270 $250

V

ariable conversion cost per unit………………

…

$180 $165 $150

2. The contribution margin per unit may give false signals when an organization

has production bottlenecks. Instead, Hercules should use the contribution margin

per bottleneck hour to determine relative product profitability, as follows:

High Good Regular

Grade Grade Grade

Contribution margin per unit……………………

…

$10 $21 $20

÷

Furnace (bottleneck) hours per unit…………

…

4 3 2.5

The Good Grade steel has the largest contribution margin per unit ($21); however,

the Regular grade has the largest contribution margin per furnace hour ($8).

Thus, using production bottleneck analysis indicates that the Regular Grade is

actually more profitable at a $8.00 contribution margin per furnace hour than

High Grade’s $2.50 or Good Grade’s $7.00 contribution margin per furnace hour.

Therefore, the company would want to sell product in the following preference

order:

1. Regular Grade

3. High Grade

* ** ***

24-36

…

…

CHAPTER 24 Differential Analysis and Product Pricing

Prob. 24–1B (FIN MAN); Prob. 9–1B (MAN)

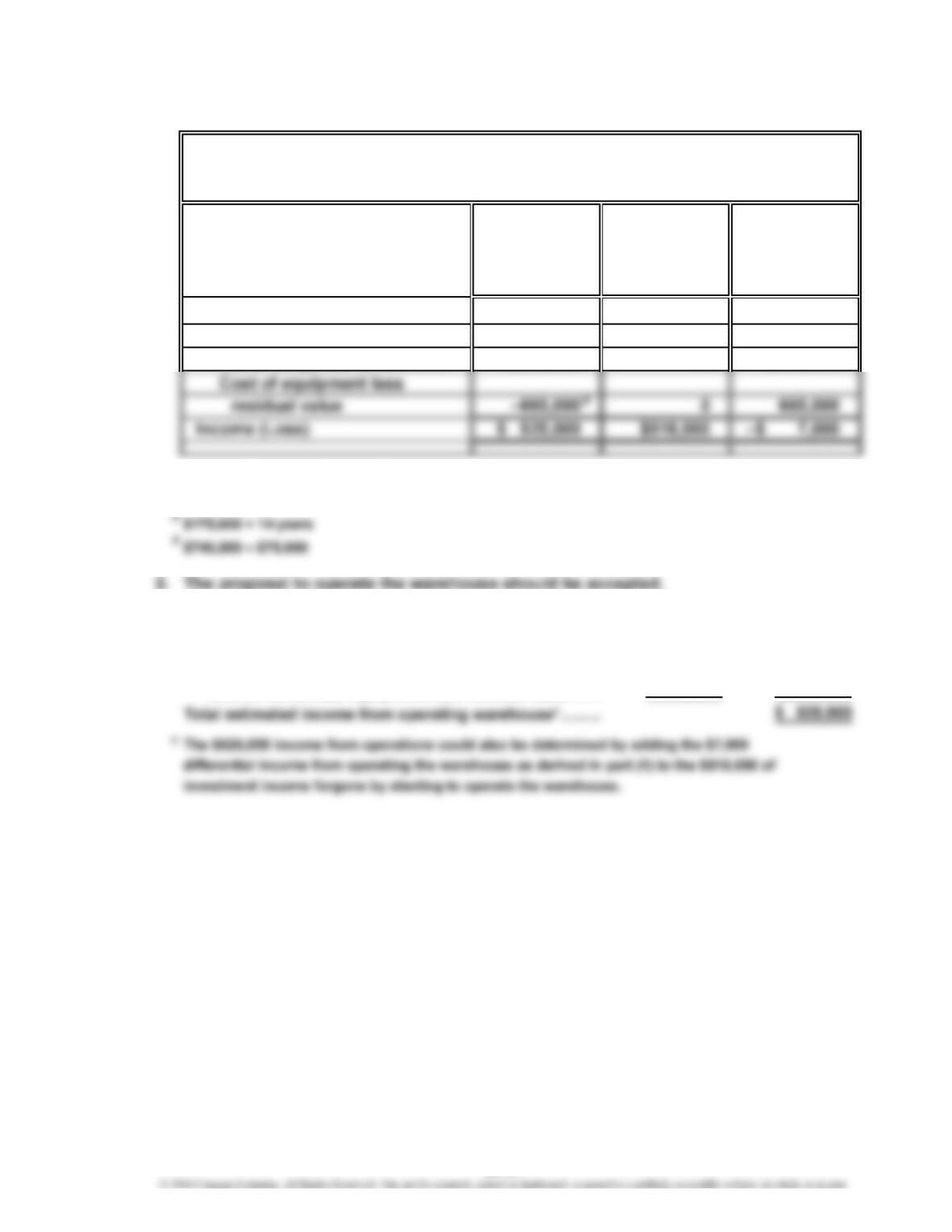

1.

Differential

Operate Invest in Effect

Warehouse Bonds on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues $3,640,000 $518,000 –$3,122,000

Costs:

Costs to operate warehouse –2,450,000 02,450,000

1

(7 yrs. × $280,000) + (7 yrs. × $240,000)

2

5% × $740,000 × 14 years

3.

Total estimated revenue from operating warehouse……

…

$3,640,000

Total estimated expenses to operate warehouse:

Costs to operate warehouse, excluding depreciation

…

$2,450,000

Cost of warehouse equipment less residual value…… 665,000 3,115,000

Differential Analysis

Operate Warehouse (Alt. 1) or Invest in Bonds (Alt. 2)

July 1

12

3

24-37

CHAPTER 24 Differential Analysis and Product Pricing

Prob. 24–2B (FIN MAN); Prob. 9–2B (MAN)

1.

Continue Replace Differential

with Old Old Effect

Machine Machine on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues:

Proceeds from sale of old machine $ 0 $12,900 $12,900

Note: Revenues and nonmanufacturing operating expenses are not affected by

the decision to replace the old machine and, thus, are not included in the analysis.

2. Other factors to be considered include the following:

a. Are there any improvements in the quality of work turned out by the new

machine?

b. What effect does the federal income tax have on the decision?

c. What opportunities are available for the use of the $44,100 of funds

($57,000 less $12,900 proceeds from the old machine) that are required to

purchase the new machine?

After considering such factors as those listed above, the net cost reduction

anticipated over the six-year period may not be sufficient to justify the

Differential Analysis

Continue with Old Machine (Alt. 1) or Replace Old Machine (Alt. 2)

November 8

24-38

CHAPTER 24 Differential Analysis and Product Pricing

Prob. 24–3B (FIN MAN); Prob. 9–3B (MAN)

1.

Differential

Promote Promote Effect

Tennis Shoe Walking Shoe on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues $595,000 $700,000 $105,000

Costs:*

Direct materials –133,000 –224,000 –91,000

Direct labor –56,000 –84,000 –28,000

Variable factory overhead –49,000 –35,000 14,000

Sole Mates Inc. should promote tennis shoes.

2. The sales manager’s tentative decision should be opposed. The sales

manager erroneously considered the full unit costs instead of the differential

Differential Analysis

Promote Tennis Shoe (Alt. 1) or Promote Walking Shoe (Alt. 2)

June 19

12

24-39

CHAPTER 24 Differential Analysis and Product Pricing

Prob. 24–4B (FIN MAN); Prob. 9–4B (MAN)

1.

Process

Further into Differential

Sell Rolled Effect

Ingot Aluminium on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues, per ton $88,000 $140,800 $52,800

2. International Aluminum Co. should decide to process aluminum ingot further,

Differential Analysis

Sell Ingot (Alt. 1) or Process Further into Rolled Aluminum (Alt. 2)

February 5

12

24-40

CHAPTER 24 Differential Analysis and Product Pricing

Prob. 24–5B (FIN MAN); Prob. 9–5B (MAN)

1. $60,000 ($600,000 × 10%)

2. a. Total manufacturing costs:

V

ariable ($52* × 10,000 units)………………………………………………

…

$520,000

Fixed factory overhead………………………………………………………

…

180,000

Total Selling and Administrative Expenses

Desired Profit +

Total Manufacturing Costs

$520,000 + $180,000

b. Markup Percentage =

$60,000 + $80,000 + ($7 × 10,000 units)

=

24-41

CHAPTER 24 Differential Analysis and Product Pricing

Prob. 24–5B (FIN MAN); Prob. 9–5B (MAN) (Continued)

3. (Appendix)

a. Total costs:

V

ariable ($59 × 10,000 units)………………………………………………

…

$590,000

= 7.06%

c. Cost amount per unit………………………………………………………

…

$85

4. (Appendix)

a. Variable cost amount per unit: $59.00

Total variable costs: $59 × 10,000 units = $590,000

= 54.24% (rounded)

c. Cost amount per unit………………………………………………………

…

$59

5. The cost-plus approach price of $91 should be viewed as a general guideline for

24-42

…

CHAPTER 24 Differential Analysis and Product Pricing

Prob. 24–5B (FIN MAN); Prob. 9–5B (MAN) (Concluded)

6. a.

Differential

Reject Accept Effect

Order Order on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues $0 $91,200 $91,200

Costs

Differential Analysis

Reject Order (Alt. 1) or Accept Order (Alt. 2)

September 5

1

24-43

CHAPTER 24 Differential Analysis and Product Pricing

Prob. 24–6B (FIN MAN); Prob. 9–6B (MAN)

1.

Ethylene Butane Ester

Selling price…………………………………………

…

$170 $155 $130

V

ariable conversion cost per unit………………

…

$40 $40 $30

2. The contribution margin per unit may give false signals when an organization

has production bottlenecks. Instead, Wilmington Chemical Company should use

the contribution margin per bottleneck hour to determine relative product

profitability as follows:

Ethylene Butane Ester

Contribution margin per unit……………………

…

$15 $27 $15

****

24-44

…

…

CHAPTER 24 Differential Analysis and Product Pricing

CP 24–1 (FIN MAN); CP 9–1 (MAN)

No, it would be unethical for Aaron to attend the meeting. Such a meeting

CP 24–2 (FIN MAN); CP 9–2 (MAN)

The contribution margin is $4 ($22 – $18) per dozen on the special order. Thus,

Varden’s manager can contribute to fixed costs by accepting the order. However,

there are some additional considerations the manager must consider before

accepting this order.

1. Have we ever done business overseas? Exports require additional

2. Will the customer sell the golf balls overseas, or will they re-label the golf

balls and have them imported back into the United States? Such a situation

3. Is it likely that other customers will learn of the “special deal” the overseas

4. Will the overseas customer want to do business in the future, or is this just a

single sale? If the overseas customer is expected to purchase more golf balls

5. Is there a possibility of another customer being willing to purchase the golf

balls at the $35 price? If so, Varden may not want to commit capacity to the

6. Will we help the overseas customer establish a presence in the overseas golf

CASES & PROJECTS

CHAPTER 24 Differential Analysis and Product Pricing

CP 24–3 (FIN MAN); CP 9–3 (MAN)

First, Marriott has excess capacity for this day, so it should be willing to accept

additional customers. The Priceline.com customer generates incremental revenue

that will not reduce other business. Given this, however, the price must at least

cover variable cost, or else Marriott will incur a loss. The variable cost per room

night is shown below.

Housekeeping labor cost………………………………………………………………… $38

Cost of room supplies (soap, paper, etc.)……………………………………………

…

8

These costs are mostly avoidable, or variable to room nights. This answer

assumes that the maid and laundry staff hours are highly flexible and can be

staffed to demand. Likewise, the air conditioning and lights can be turned off if

the room is not rented for the night, saving most of the utility cost. The desk staff

24-46

CHAPTER 24 Differential Analysis and Product Pricing

CP 24–4 (FIN MAN); CP 9–4 (MAN)

a. Juanita believes that the fixed costs should be treated as a sunk cost and

ignored in the pricing decision. In essence, Juanita is suggesting that the new

computer model be treated as an incremental decision. However, the new

b. Target costing provides a different perspective to the pricing issue. Under

target costing, Diamond Computer Company should begin with the price the

market is willing to pay, which is $1,250. This price should then be reduced by

the required profit markup. This would yield a target cost of $1,000 ($1,250 ÷

1.25), which is $200 lower than the present product cost. The new target cost

should be established as a cost reduction target. The company should

CHAPTER 24 Differential Analysis and Product Pricing

CP 24–5 (FIN MAN); CP 9–5 (MAN)

a. This activity is designed to have students access a number of products and

services on the Internet to see their commercial potential. Each of the listed

sites will provide product descriptions and pricing.

The list of costs in the products will not be determined at the Internet site but

must be assumed. Some examples include:

Delta Air Lines—Airline tickets Fixed or Variable?

Fuel………………………………………………………………

…

V

Crew salaries…………………………………………………… F

Assume that the activity base is the number of passenger miles for

determining fixed and variable costs. Employee salaries for an airline

are relatively fixed and only become variable when there are significant

changes to the flight schedule.

Amazon.com—Books Fixed or Variable?

Cost of books (purchased for resale)……………………… V

…

…

Assume that the activity base is the number of books sold for determining

fixed and variable costs.

Dell Inc.—Personal computers Fixed or Variable?

Cost of computers (dl, dm, and foh)………………………

…

V (mostly)

Web page design and programming………………………

…

F

Advertising……………………………………………………

…

F

*Depends on contract terms with software vendor

24-48

…

CHAPTER 24 Differential Analysis and Product Pricing

CP 24–5 (FIN MAN); CP 9–5 (MAN) (Concluded)

b. The product with the largest markup on variable cost is the airline ticket. The

portion of variable cost to total cost for an airline flight will be much smaller

24-49