1. a. Differential revenue is the amount of increase or decrease in revenue expected from a

p

articular course of action compared with an alternative.

2. The differential income and costs of the lease option should be compared against selling the building.

The differential revenue would be the lease revenue compared to the proceeds from sale. The

p

4. A business should only accept business at a special price if the lower price will not contaminate the

regular pricing for other customers or induce other customers to demand the special price. In

5. It would be reasonable to purchase from the supplier if the fixed cost per unit was less than 50 cents.

6. Some of the financial considerations include the profitability of the store, including all the revenues

and the variable and fixed costs associated with the store because they would all be differential to the

7. In the long run, the normal selling price must be set high enough to cover all costs (both fixed an

d

variable) and provide a reasonable amount for profit.

CHAPTER 24 (FIN MAN); CHAPTER 9 (MAN)

DIFFERENTIAL ANALYSIS AND PRODUCT PRICING

DISCUSSION QUESTIONS

24-1

CHAPTER 24 Differential Analysis and Product Pricing

DISCUSSION QUESTIONS (Continued)

9. The target cost concept begins with a price that can be sustained in the marketplace, then

subtracts a target profit, thus determining the target cost. The cost is made to conform to the

p

rice required in the market. In contrast, under cost plus, a markup is added to the cost. The

24-2

b

CHAPTER 24 Differential Analysis and Product Pricing

PE 24–1A (FIN MAN); PE 9–1A (MAN)

Differential

Lease Sell Effect

Machine Machine on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues $272,000 $262,000 –$10,000

*

$262,000 × 5%

Claxon Company should lease the machine.

PE 24–1B (FIN MAN); PE 9–1B (MAN)

Differential

Lease Sell Effect

Equipment Equipment on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues $84,600 $82,000 –$2,600

Differential Analysis

Lease Equipment (Alt. 1) or Sell Equipment (Alt. 2)

March 23

PRACTICE EXERCISES

Differential Analysis

Lease Machine (Alt. 1) or Sell Machine (Alt. 2)

January 12

CHAPTER 24 Differential Analysis and Product Pricing

PE 24–2A (FIN MAN); PE 9–2A (MAN)

Differential

Continue Discontinue Effect

Product TS-20 Product TS-20 on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenue $102,000 $ 0 –$102,000

Costs:

PE 24–2B (FIN MAN); PE 9–2B (MAN)

Differential

Continue Discontinue Effect

Product B Product B on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenue $39,500 $ 0 –$39,500

Costs:

Variable cost of goods sold –25,500 0 25,500

Differential Analysis

Continue Product B (Alt. 1) or Discontinue Product B (Alt. 2)

May 9

Differential Analysis

Continue Product TS-20 (Alt. 1) or Discontinue Product TS-20 (Alt. 2)

September 12

24-4

CHAPTER 24 Differential Analysis and Product Pricing

PE 24–3A (FIN MAN); PE 9–3A (MAN)

Differential

Make Buy Effect

Bread Bread on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Unit costs:

Purchase price $ 0 –$110 –$110

Delivery 0 –15 –15

PE 24–3B (FIN MAN); PE 9–3B (MAN)

Differential

Make Buy Effect

Bottles Bottles on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Unit costs:

Purchase price $ 0 –$35 –$35

Differential Analysis

Make Bottles (Alt. 1) or Buy Bottles (Alt. 2)

March 30

Differential Analysis

Make Bread (Alt. 1) or Buy Bread (Alt. 2)

August 16

CHAPTER 24 Differential Analysis and Product Pricing

PE 24–4A (FIN MAN); PE 9–4A (MAN)

Continue Replace Differential

with Old Old Effect

Machine Machine on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues:

Proceeds from sale of old machine $ 0 $ 84,000 $ 84,000

Costs:

The company should replace the old machine.

PE 24–4B (FIN MAN); PE 9–4B (MAN)

Continue Replace Differential

with Old Old Effect

Machine Machine on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues:

Proceeds from sale of old machine $ 0 $50,500 $50,500

Costs:

Differential Analysis

Continue with Old Machine (Alt. 1) or Replace Old Machine (Alt. 2)

April 11

Differential Analysis

Continue with Old Machine (Alt. 1) or Replace Old Machine (Alt. 2)

February 18

24-6

CHAPTER 24 Differential Analysis and Product Pricing

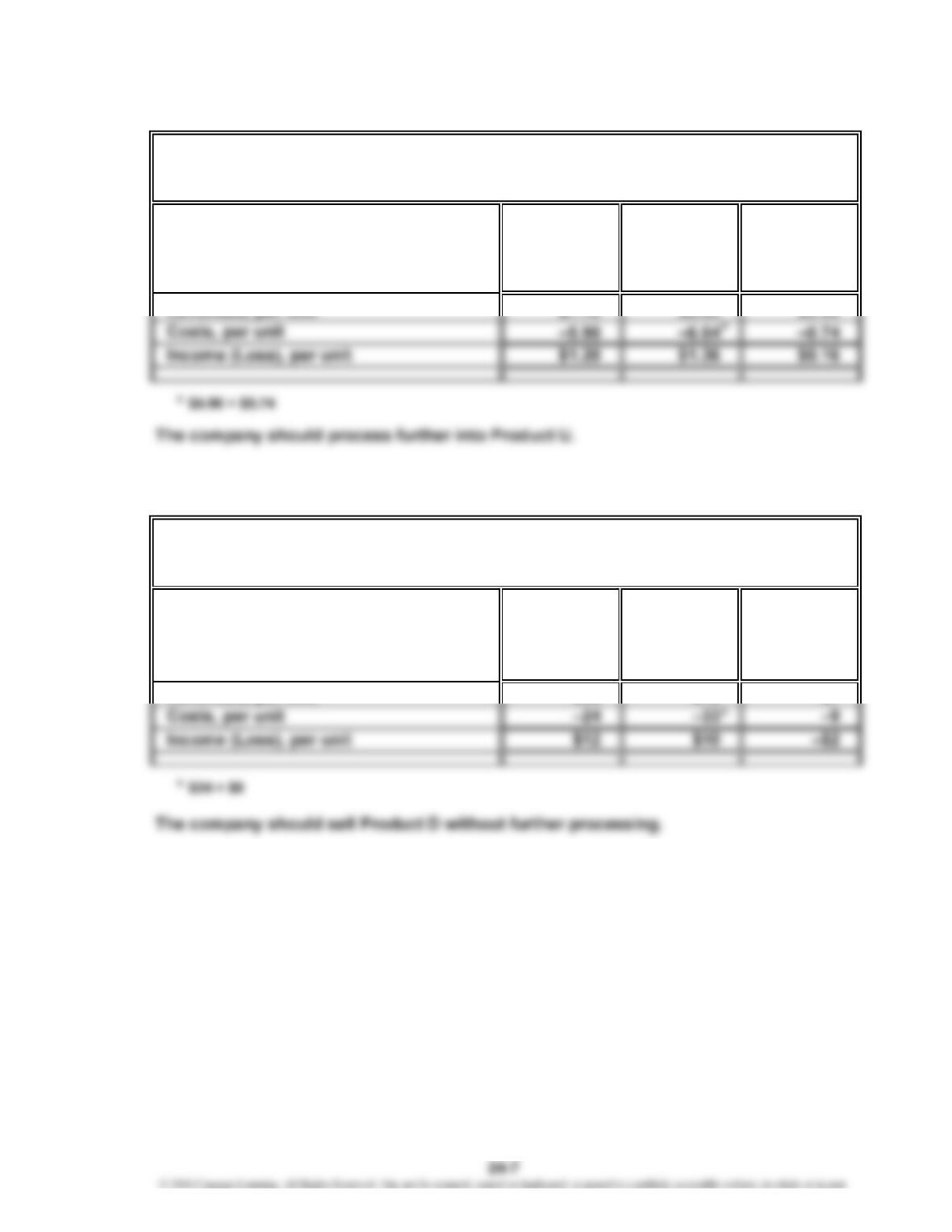

PE 24–5A (FIN MAN); PE 9–5A (MAN)

Process Differential

Sell Further into Effect

Product T Product U on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues, per unit $7.10 $8.00 $0.90

PE 24–5B (FIN MAN); PE 9–5B (MAN)

Process Differential

Sell Further into Effect

Product D Product E on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues, per unit $36 $43 $7

Differential Analysis

Sell Product D (Alt. 1) or Process Further into Product E (Alt. 2)

February 26

Differential Analysis

Sell Product T (Alt. 1) or Process Further into Product U (Alt. 2)

August 2

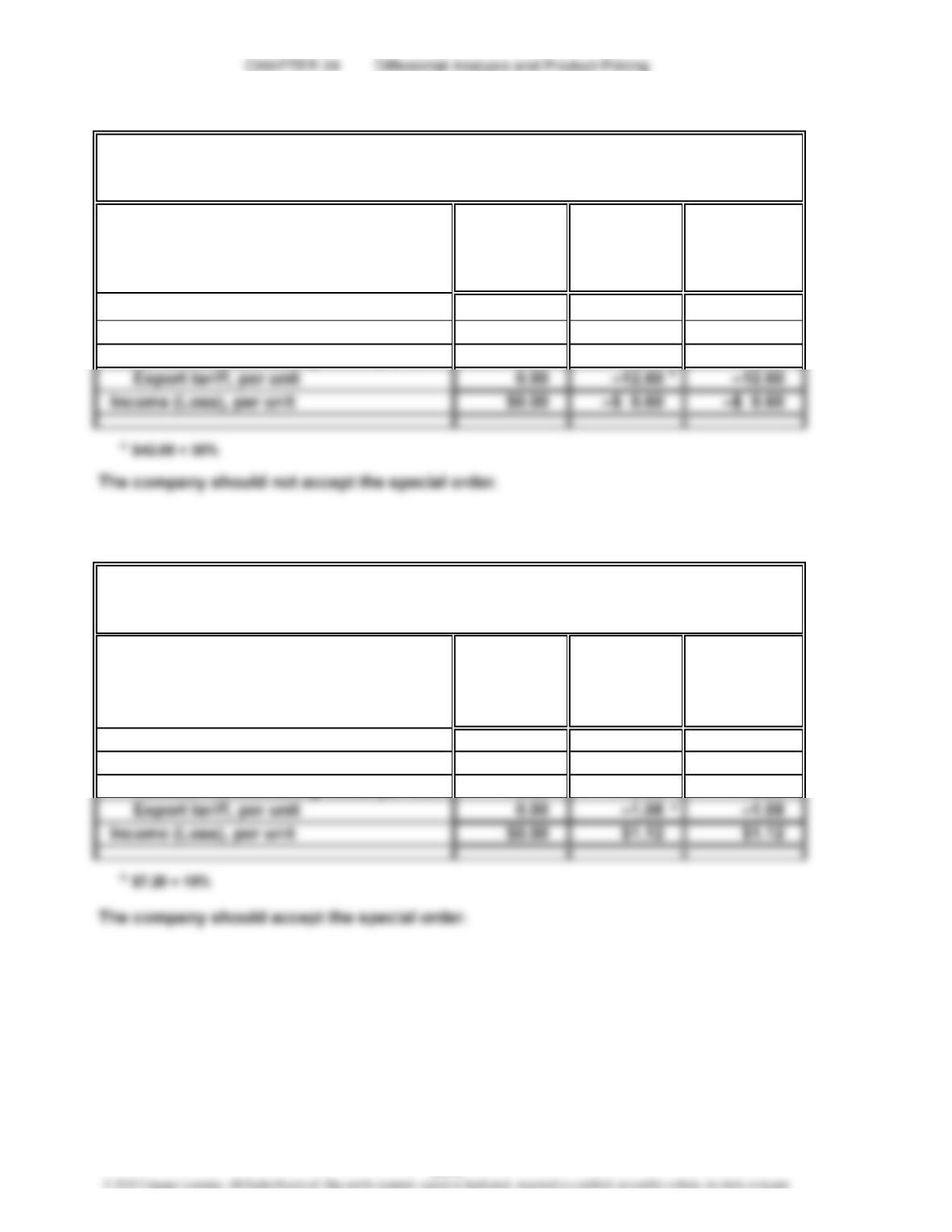

PE 24–6A (FIN MAN); PE 9–6A (MAN)

Differential

Reject Accept Effect

Order Order on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues, per unit $0.00 $42.00 $42.00

Costs:

Variable manufacturing costs, per unit 0.00 –30.00 –30.00

PE 24–6B (FIN MAN); PE 9–6B (MAN)

Differential

Reject Accept Effect

Order Order on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues, per unit $0.00 $7.20 $7.20

Costs:

Variable manufacturing costs, per unit 0.00 –5.00 –5.00

Differential Analysis

Reject Order (Alt. 1) or Accept Order (Alt. 2)

March 16

Differential Analysis

Reject Order (Alt. 1) or Accept Order (Alt. 2)

October 23

24-8

CHAPTER 24 Differential Analysis and Product Pricing

PE 24–7A (FIN MAN); PE 9–7A (MAN)

PE 24–7B (FIN MAN); PE 9–7B (MAN)

PE 24–8A (FIN MAN); PE 9–8A (MAN)

Product A Product B

Unit contribution margin……………………………………………

…

$24 $30

PE 24–8B (FIN MAN); PE 9–8B (MAN)

Product K Product L

…

Desired Profit + Selling and Admin. Exp.

Total Product Cost

Markup percentage on product cost:

Markup percentage on product cost: Desired Profit + Selling and Admin. Exp.

Total Product Cost

24-9

CHAPTER 24 Differential Analysis and Product Pricing

Ex. 24–1 (FIN MAN); Ex. 9–1 (MAN)

a.

Differential

Lease Sell Effect

Machinery Machinery on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues $216,000 $221,000 $5,000

b. Sell the machinery. The net gain from selling is $8,150.

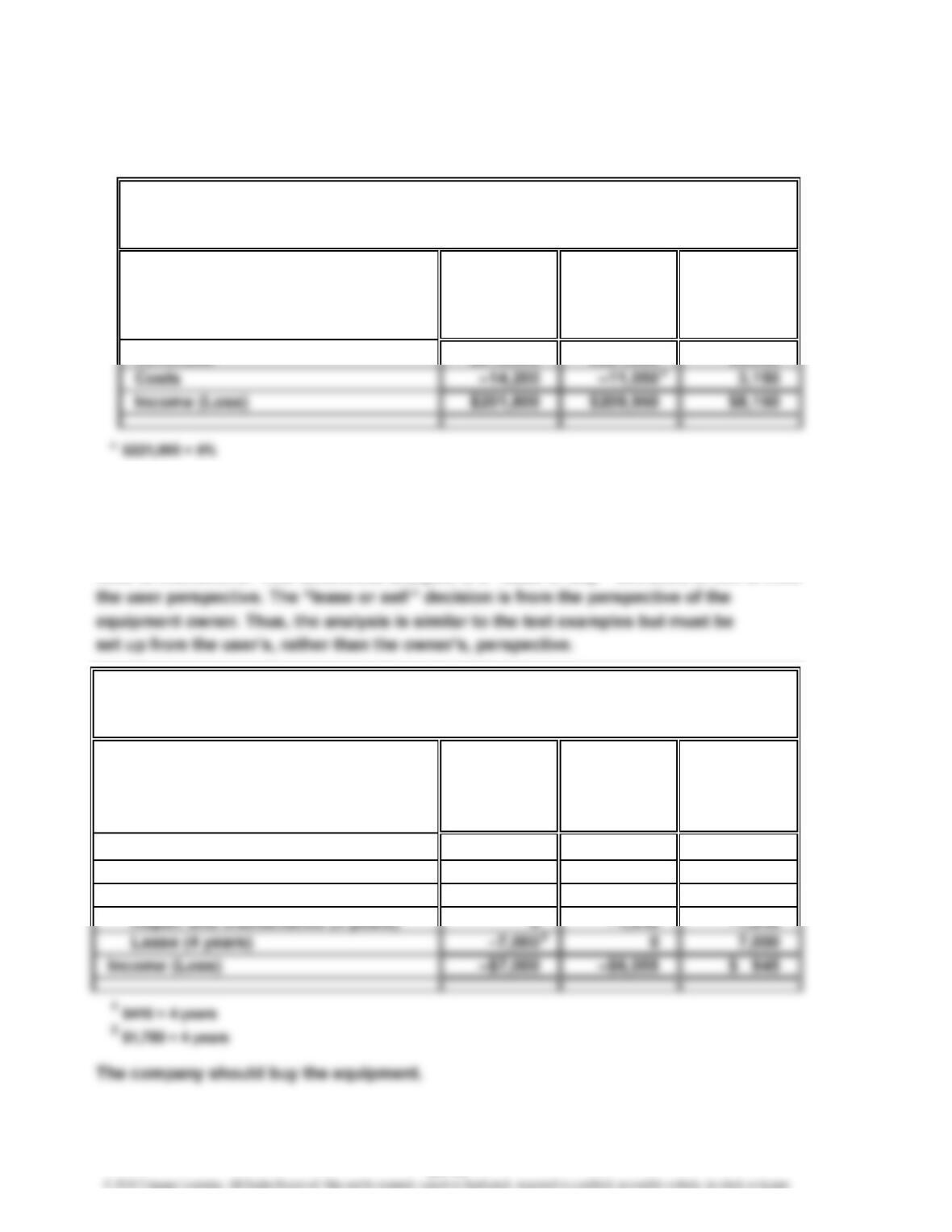

Ex. 24–2 (FIN MAN); Ex. 9–2 (MAN)

Note to Instructors: This differential analysis is a “lease or buy ” decision, which is from

Differential

Lease Buy Effect

Equipment Equipment on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Costs:

Purchase price $ 0 –$3,900 –$3,900

Freight and installation 0 –515 –515

EXERCISES

Differential Analysis

Lease Equipment (Alt. 1) or Buy Equipment (Alt. 2)

August 4

Differential Analysis

Lease Machinery (Alt. 1) or Sell Machinery (Alt. 2)

April 16

1

24-10

CHAPTER 24 Differential Analysis and Product Pricing

Ex. 24–3 (FIN MAN); Ex. 9–3 (MAN)

a.

Differential

Continue Discontinue Effect

Star Cola Star Cola on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues $390,000 $ 0 –$390,000

Costs:

Variable cost of goods sold –147,200 0 147,200

Variable operating expenses –178,500 0 178,500

Differential Analysis

Continue Star Cola (Alt. 1) or Discontinue Star Cola (Alt. 2)

January 21

1

2

24-11

CHAPTER 24 Differential Analysis and Product Pricing

Ex. 24–4 (FIN MAN); Ex. 9–4 (MAN)

a.

Differential

Continue Discontinue Effect

Cups Cups on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues $31,300 $ 0 –$31,300

Costs:

Variable cost of goods sold –14,280 0 14,280

Variable selling and admin.

b. The Cups line should be retained. As indicated by the differential analysis in part (a),

the income will decrease by $7,000 if the Cups line is discontinued.

Differential Analysis

Continue Cups (Alt. 1) or Discontinue Cups (Alt. 2)

March 31, 2016

1

24-12

CHAPTER 24 Differential Analysis and Product Pricing

Ex. 24–5 (FIN MAN); Ex. 9–5 (MAN)

Note to Instructors: Many students may be unfamiliar with the financial services

industry. This exercise provides an opportunity to introduce students to some

basic terms and concepts used within the industry.

a. The “Investor Services” segment serves the retail customer, you and me.

These are the brokerage, Internet, and mutual fund services used by individual

b. Variable costs in the “Investor Services” segment include:

2. Fees paid to exchanges for executing trades

4. Advertising

Fixed costs in the “Investor Services” segment include:

2. Depreciation on brokerage office equipment, such as computers and

computer networks

3. Property taxes on brokerage offices

c. Investor Institutional

Services Services

(in millions) (in millions)

Income from operations……………………………………… $ 865 $514

d. If one assumes that the fixed costs that serve institutional investors (computers,

servers, and facilities) would not be sold but would be used by the other sector,

24-13

CHAPTER 24 Differential Analysis and Product Pricing

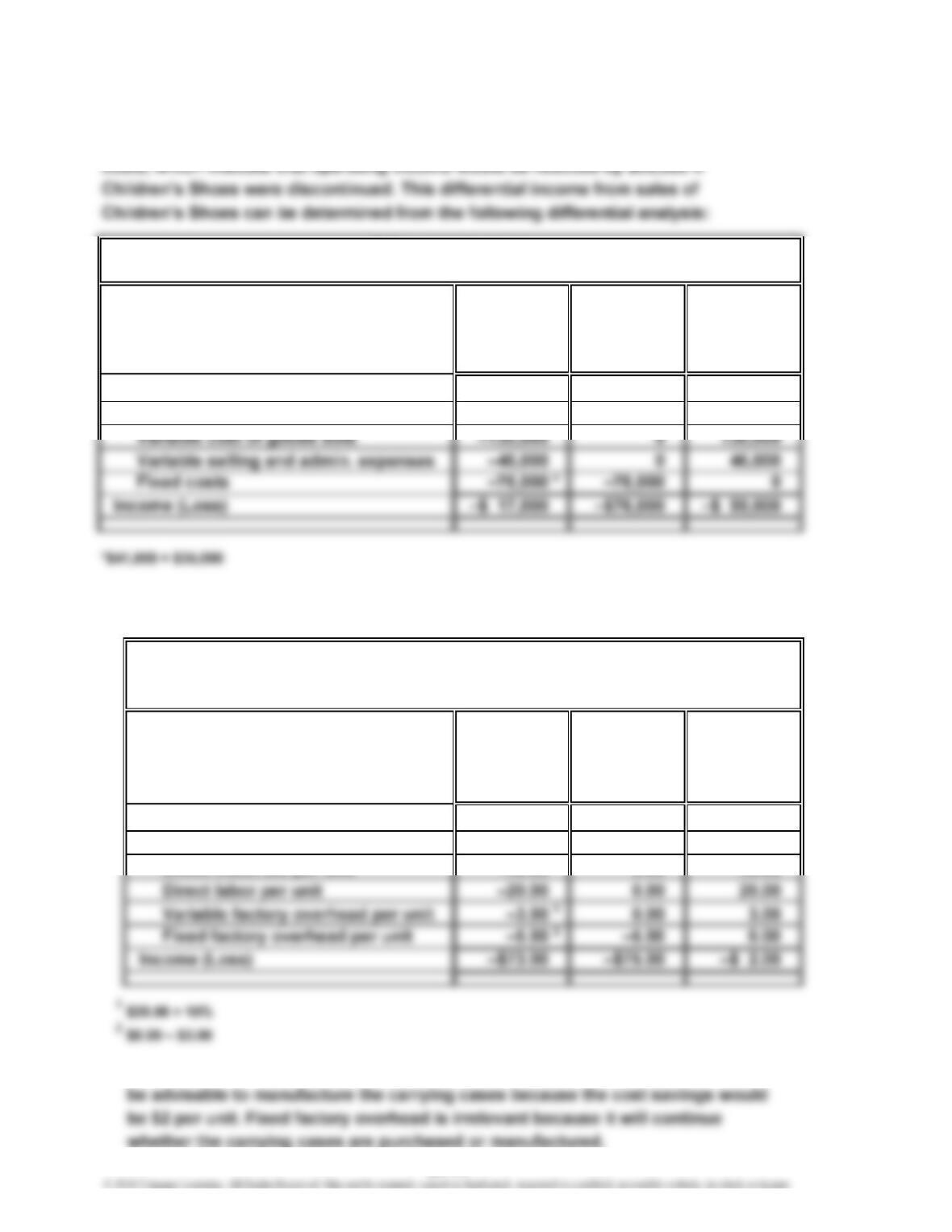

Ex. 24–6 (FIN MAN); Ex. 9–6 (MAN)

The flaw in the decision is the failure to focus on the differential revenues and

Continue Discontinue Differential

Children’s Children’s Effect

Shoes Shoes on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues $235,000 $ 0 –$235,000

Costs:

Ex. 24–7 (FIN MAN); Ex. 9–7 (MAN)

a.

Make Buy Differential

Carrying Carrying Effect

Case Case on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Costs:

Purchase price $ 0.00 –$70.00 –$70.00

Direct materials per unit –45.00 0.00 45.00

b. Assuming there were no better alternative uses for the spare capacity, it would

Differential Analysis

Make Carrying Case (Alt. 1) or Buy Carrying Case (Alt. 2)

July 19

Differential Analysis

Continue Children’s Shoes (Alt. 1) or Discontinue Children’s Shoes (Alt. 2)

24-14

CHAPTER 24 Differential Analysis and Product Pricing

Ex. 24–8 (FIN MAN); Ex. 9–8 (MAN)

a.

Lay Out Purchase Differential

Pages Layout Effect

Internally Services on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Costs:

Purchase price of layout work $ 0 –$312,000 –$312,000

Salaries –224,000 0 224,000

Benefits –36,000 0 36,000

b. The benefit from using an outside service is shown to be $8,000 greater

than performing the layout work internally. The fixed costs (depreciation

expenses) in the budget are irrelevant to the decision. Thus, the work should

be purchased from the outside on a strictly financial basis.

Differential Analysis

Lay Out Pages Internally (Alt. 1) or Purchase Layout Services (Alt. 2)

February 22

*

24-15

CHAPTER 24 Differential Analysis and Product Pricing

Ex. 24–9 (FIN MAN); Ex. 9–9 (MAN)

a.

Continue Replace Differential

with Old Old Effect

Machine Machine on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues:

Proceeds from sale of old

machine $ 0 $231,000 $231,000

Costs:

The company should replace the old machine.

b. The sunk cost is the $250,000 book value ($600,000 cost less $350,000 accumulated

Differential Analysis

Continue with Old Machine (Alt. 1) or Replace Old Machine (Alt. 2)

September 13

24-16

CHAPTER 24 Differential Analysis and Product Pricing

Ex. 24–10 (FIN MAN); Ex. 9–10 (MAN)

a.

Continue Replace Differential

with Old Old Effect

Machine Machine on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues:

Sales (5 years)* $1,025,000 $1,025,000 $ 0

Costs:

Purchase price 0 –180,000 –180,000

Direct materials (5 years)* –360,000 –360,000 0

b. The proposal should not be accepted.

c. In addition to the factors given, consideration should be given to such factors

as: Do both present and proposed operations provide the same capacity?

Differential Analysis

Continue with Old Machine (Alt. 1) or Replace Old Machine (Alt. 2)

May 4

24-17

CHAPTER 24 Differential Analysis and Product Pricing

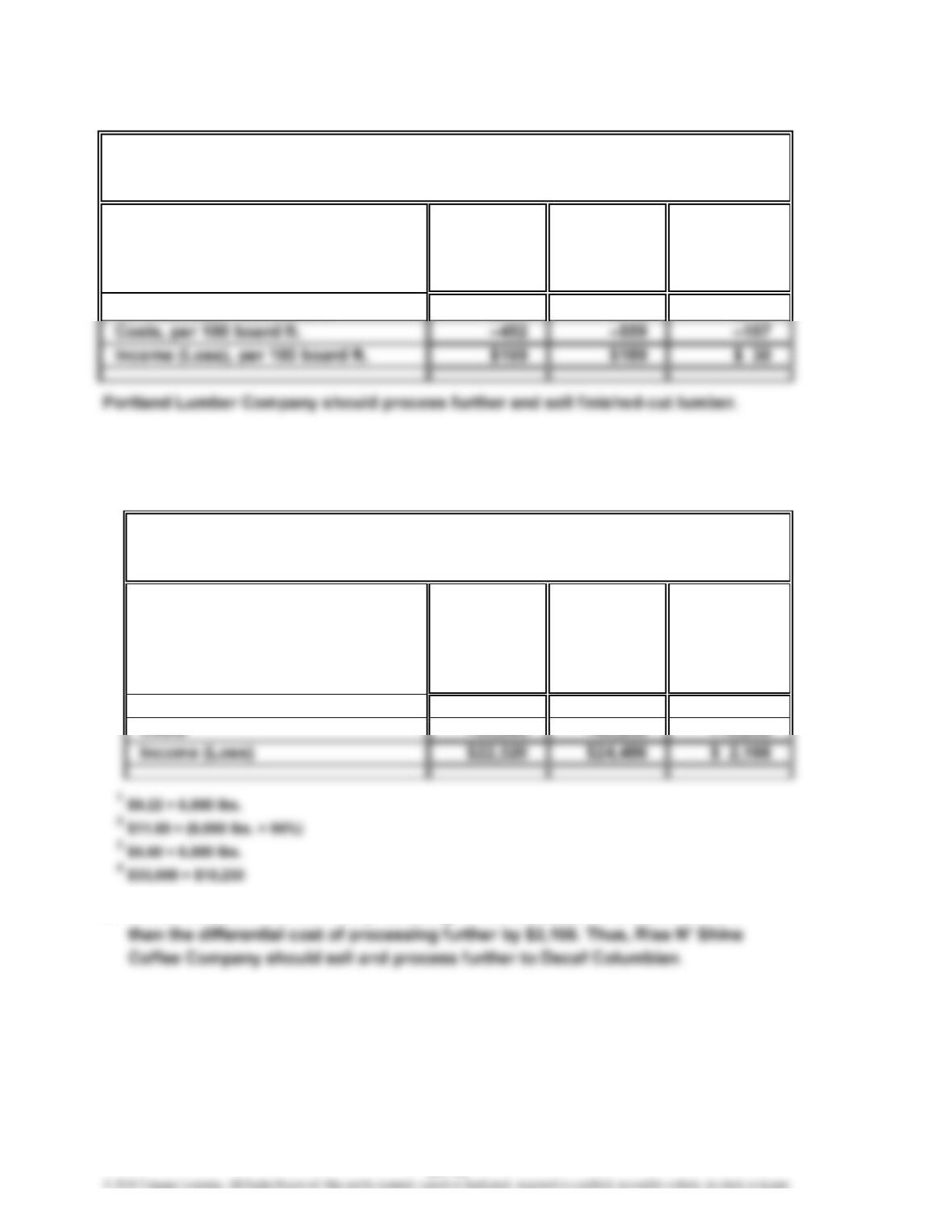

Ex. 24–11 (FIN MAN); Ex. 9–11 (MAN)

Process Differential

Sell Further into Effect

Rough Cut Finished Cut on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues, per 100 board ft. $611 $748 $137

Ex. 24–12 (FIN MAN); Ex. 9–12 (MAN)

a.

Process

Sell Further into Differential

Regular Decaf Effect

Columbian Columbian on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues $55,320 $67,716 $12,396

b. The differential revenue from processing further to Decaf Columbian is more

Sell Regular Columbian (Alt. 1) or Process Further into Decaf Columbian (Alt. 2)

October 6

Differential Analysis

Sell Rough Cut (Alt. 1) or Process Further into Finished Cut (Alt. 2)

June 14

Differential Analysis

12

34

24-18

CHAPTER 24 Differential Analysis and Product Pricing

Ex. 24–12 (FIN MAN); Ex. 9–12 (MAN) (Concluded)

c. The price of Decaf Columbian would need to decrease to $11.50 per pound

in order for the differential analysis to yield neither an advantage nor a

disadvantage (indifference). This is determined as follows:

The price of Decaf Columbian would need to be $0.38 lower, or $11.50, to

yield no net differential income or loss. This is verified by the following

differential analysis:

Sell Differential

Regular Effect

Columbian on Income

(Alternative 1) (Alternative 2)

Revenues $55,320 $10,230

Further into

Process

October 6

Differential Analysis

Sell Regular Columbian (Alt. 1) or Process Further into Decaf Columbian (Alt. 2)

(Alternative 2)

Decaf Columbian

$65,550

*

24-19

CHAPTER 24 Differential Analysis and Product Pricing

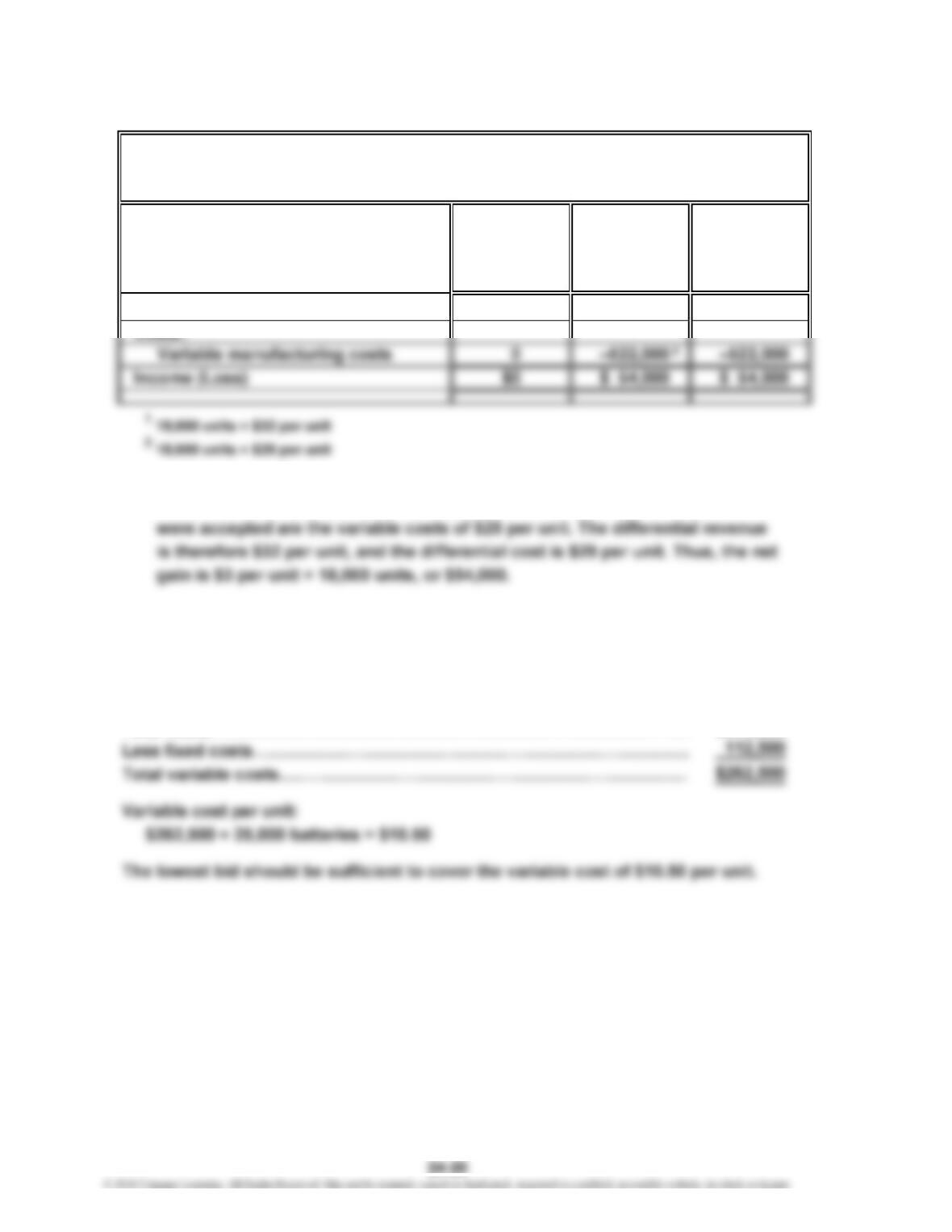

Ex. 24–13 (FIN MAN); Ex. 9–13 (MAN)

a.

Differential

Reject Accept Effect

Order Order on Income

(Alternative 1) (Alternative 2) (Alternative 2)

Revenues $0 $576,000 $576,000

b. The additional units can be sold for $32 each, and because unused capacity is

available, the only costs that would be added if this additional production

c. $29.01. Any selling price above $29 (variable costs per unit) will produce a

positive contribution margin.

Ex. 24–14 (FIN MAN); Ex. 9–14 (MAN)

Total costs…………………………………………………………………………

…

$375,000

Differential Analysis

Reject Order (Alt. 1) or Accept Order (Alt. 2)

November 12

1