Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

24-1

CHAPTER 24

PERFORMANCE MEASUREMENT AND

RESPONSIBILITY ACCOUNTING

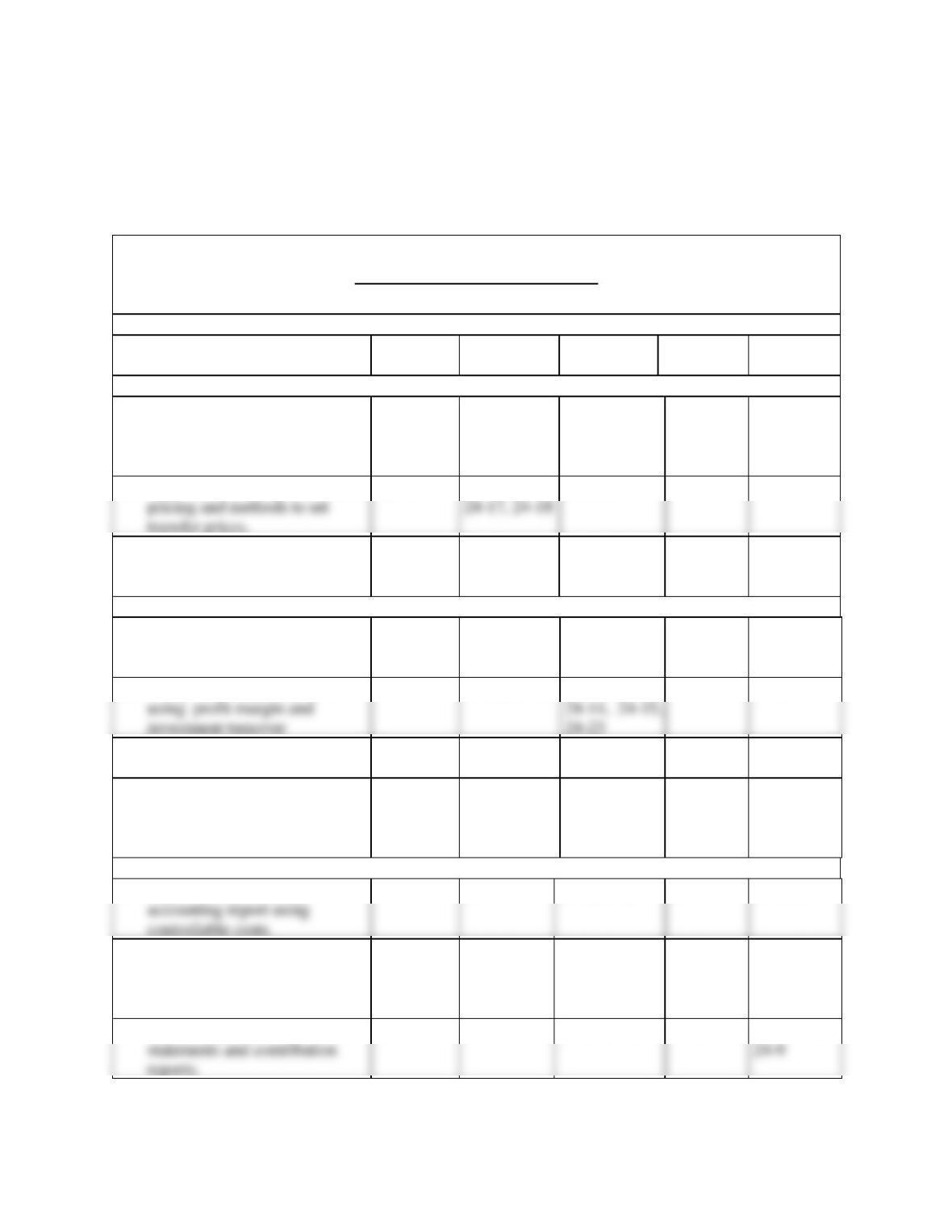

Related Assignment Materials

Student Learning Objectives

Discussion

Questions

Quick

Studies*

Exercises*

Problems*

Beyond the

Numbers

Conceptual objectives:

C1. Distinguish between direct and

indirect expenses and identify

bases for allocating indirect

expenses to departments

1,2,3,4,5,

6,7,8,9,11,

15,16

24-1, 24-2,

24-3

24-1, 24-8

C2. Appendix 24B—Explain transfer

12, 13

24-7, 24-16,

24-20,

C3. Appendix 24C—Describe

allocation of joint costs across

products.

14

24-19

24-21, 24-22

24-5

Analytical objectives:

A1. Analyze investment centers

using return on investment and

residual income.

24-10, 24-11,

24-12, 24-20

24-9, 24-10,

24-12, 24-13,

24-15

ES

using profit margin and

investment turnover

24-14, 24-15,

24-23

A2. Analyze investment centers

24-12, 24-13

24-11, 24-12,

24-2

A3. Analyze investment centers

using the balance scorecard

24-14, 24-15

24-16, 24-17,

SP

A4. Compute cycle time and cycle

efficiency, and explain their

importance to production

management.

17,18, 19,

20

24-16

24-18, 24-19,

Procedural objectives:

accounting report using

controllable costs.

P1. Prepare a responsibility

24-4

24-1, 24-2,

24-1

24-6, 24-8

P2. Allocate indirect expenses to

departments.

24-5, 24-6

24-7, 24-8

24-3, 24-4,

24-5, 24-6,

24-2

24-4, 24-5

P3. Prepare departmental income

10

24-9

24-7, 24-8,

24-3, 24-4

24-3, 24-7,

pricing and methods to set

transfer prices.

24-17, 24-18

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

24-2

*See additional information on next page that pertains to these quick studies, exercises and problems.

SP refers to the Serial Problem

ES refers to Excel Simulations

Additional Information on Related Assignment Material

Connect

Available on the instructor’s course-specific website) repeats all numerical Quick Studies, all Exercises

and Problems Set A. Connect also provides algorithmic versions for Quick Study, Exercises and

Problems. It allows instructors to monitor, promote, and assess student learning. It can be used in

practice, homework, or exam mode.

Connect Insight

The Serial Problem (SP) for Success Systems continues in this chapter.

General Ledger

Assignable within Connect, General Ledger (GL) problems offer students the ability to see how transactions post

from the general journal all the way through the financial statements. Critical thinking and analysis components are

added to each GL problem to ensure understanding of the entire process. GL problems are auto-graded and provide

instant feedback to the student.

Excel Simulations

Synopsis of Chapter Revisions

NEW opener—Ministry of Supply and entrepreneurial assignment.

Reorganized chapter.

Revised discussion of performance evaluation and decentralization.

Revised discussion of Kraft Heinz responsibility centers.

Revised exhibit on responsibility accounting.

Revised discussion of responsibility accounting reports.

Added NTKs on responsibility accounting, cost allocations, and balanced scorecard.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

24-3

Chapter Outline

I. Responsibility Accounting

A. Performance Evaluation

2. In decentralized organizations, decisions are made by unit

managers rather than top management.

4. The methods of performance evaluation vary for cost centers,

profit centers and investment centers.

a. Cost center⎯incurs cost or expenses without directly

5. Basis for evaluating performance:

a. Cost center managers are evaluated on their success in

II. Controllable versus Uncontrollable Costs

A. Controllable Costs –

1. Those which a manager has the power to determine or at least

significantly affect the amount incurred.

B. Uncontrollable costs –

1. Are not within the manager’s control.

2. A manager’s performance is evaluated using responsibility

3. Distinguishing between controllable and uncontrollable costs

5. Good judgment is required when identifying controllable costs.

Notes

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

24-4

Chapter Outline

C. Responsibility Accounting Performance Report

1. Reports actual expenses that a manager is responsible for and

their budgeted amounts.

2. Responsibility Accounting Report

a. Provide relevant information for each management level.

b. At lower levels, managers have limited responsibilities and

therefore fewer controllable costs.

III. Profit Centers

A. The responsibility report focuses on how well each department

controlled costs and generated revenues.

B. The departmental income statement is a common way to report

profit center performance.

C. When computing department profits, two key accounting challenges

involve allocating expenses:

2. How to allocate service department expenses, such as payroll or

purchasing, that perform services that benefit several

departments.

D. Direct and Indirect Expenses

1. Direct Expenses are readily traced to a department.

2. Indirect Expenses are incurred for joint benefit of more than one

department; can’t be readily traced to just one department.

Notes

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

24-5

Chapter Outline

E. General Model – indirect and service department expenses are

allocated across departments benefiting from them. Allocated using a

cause-effect relation. Sometimes hard to identify.

1. Allocated Cost = Total Cost to Allocate x Percentage of

Allocation Base Used.

F. Allocating Indirect Expenses – allocation bases vary across

departments and organizations. Managers must use careful judgment

in developing allocation bases. Commonly used allocation bases:

1. Wages and salaries –allocated using relative amount of hours

worked in each department.

2. Rent and Utilities⎯allocated based on portion of floor space

4. Depreciation – allocated using hours of depreciable asset used.

G. Service Department expenses – provide support to an organization’s

operating departments. Common allocation bases:

1. Office, personnel, and payroll expenses – allocated based on

number of employees in each department.

3. Maintenance expenses – allocated based on square footage.

H. Departmental Income Statements

1. Departmental income is computed using the following formula:

Departmental income = Dept. sales – Dept. direct expenses –

Allocated indirect expenses – Allocated service dept. expenses.

2. Four Steps for allocating costs and preparing departmental

income statements:

a. Step one – accumulate revenues and direct and indirect

expenses by department. Involves collecting the necessary

Notes

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

24-6

Chapter Outline

c. Step three – allocate service department expenses to

operating departments using a departmental expense

allocation spreadsheet. After service department costs are

allocated, no expenses remain in the service departments.

I. Departmental Contribution to Overhead (see Exhibit 24.12)

1. Departmental income statements not always best for evaluating

3. Behavioral Aspects of Departmental Performance Reports –

a. Indirect expenses are typically uncontrollable, so a better way

to evaluate is using departmental contribution to overhead.

IV. Investment Center

A. Financial Performance Evaluation Measures include:

1. Return on investment, return on assets, computed as investment

center income / by investment center average invested assets.

2. Residual income – Expressed in dollars. Encourages division

3. Profit margin and investment turnover – split return on

investment into two measures – profit margin and investment

turnover.

Notes

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

24-7

Chapter Outline

4. Nonfinancial Performance Evaluation Measures – using solely

5. Balanced Scorecard: system of performance measures,

including nonfinancial measures used to assess company and

division manager performance. Requires managers to think of

their company from four perspectives.

a. Customer: what do they think of us?

V. Decision Analysis Cycle Time and Cycle Efficiency

A. As lean manufacturing practices help companies move toward just

in time manufacturing it is important for companies to reduce the

time it takes to manufacture its products and improve efficiency.

1. Cycle time measures the time element which describes the time

it takes to produce a product or service.

Cycle time = Process + Inspection + Move + Wait

Time Time Time Time

a. Process time is considered value-added time – it is the only

activity in cycle time that adds value to the product from the

2. Cycle Efficiency measures production efficiency. It is the ratio

of value added time to total cycle time.

reduce the non-value added activities.

VI. Appendix 24A – Cost Allocations uses the general model of cost

allocation to show how the cost allocations in Exhibits 24.10 and 24.11

for A-1 Hardware. Rent expense, utilities expense, advertising expense

and insurance expense are allocated first. Then, the two service

department’s expenses are allocated to the three operating departments.

Notes

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

24-8

Chapter Outline

VII. Appendix 24B – Transfer Pricing

The price used to record transfers between divisions in the same

company is called a transfer price. Can be used in cost, profit and

investment centers.

A. If there is no excess capacity, the internal supplier will not accept a

transfer price less than the market price. This is called market based

transfer pricing.

B. If there is excess capacity, the internal supplier should accept a price

between the costs to manufacturer the part and the market price.

This is called cost based transfer pricing.

C. Other issues to consider in determining transfer prices include:

1. Market price may not exist

2. Cost controls

III. Appendix 24C – Joint Costs

A. Joint Costs⎯the costs incurred to produce or purchase two or more

products at the same time; similar to indirect expense in that it’s

shared across more than one cost object.

1. Ignored when deciding to sell product as is or process further.

2. Allocated to different products produced from it when total cost

3. Allocation bases

a. Physical basis⎯allocates joint costs using physical

characteristics such as ratio of pounds, cubic feet or gallons

of each joint product to the total pounds, cubic feet or

Notes

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

24-9

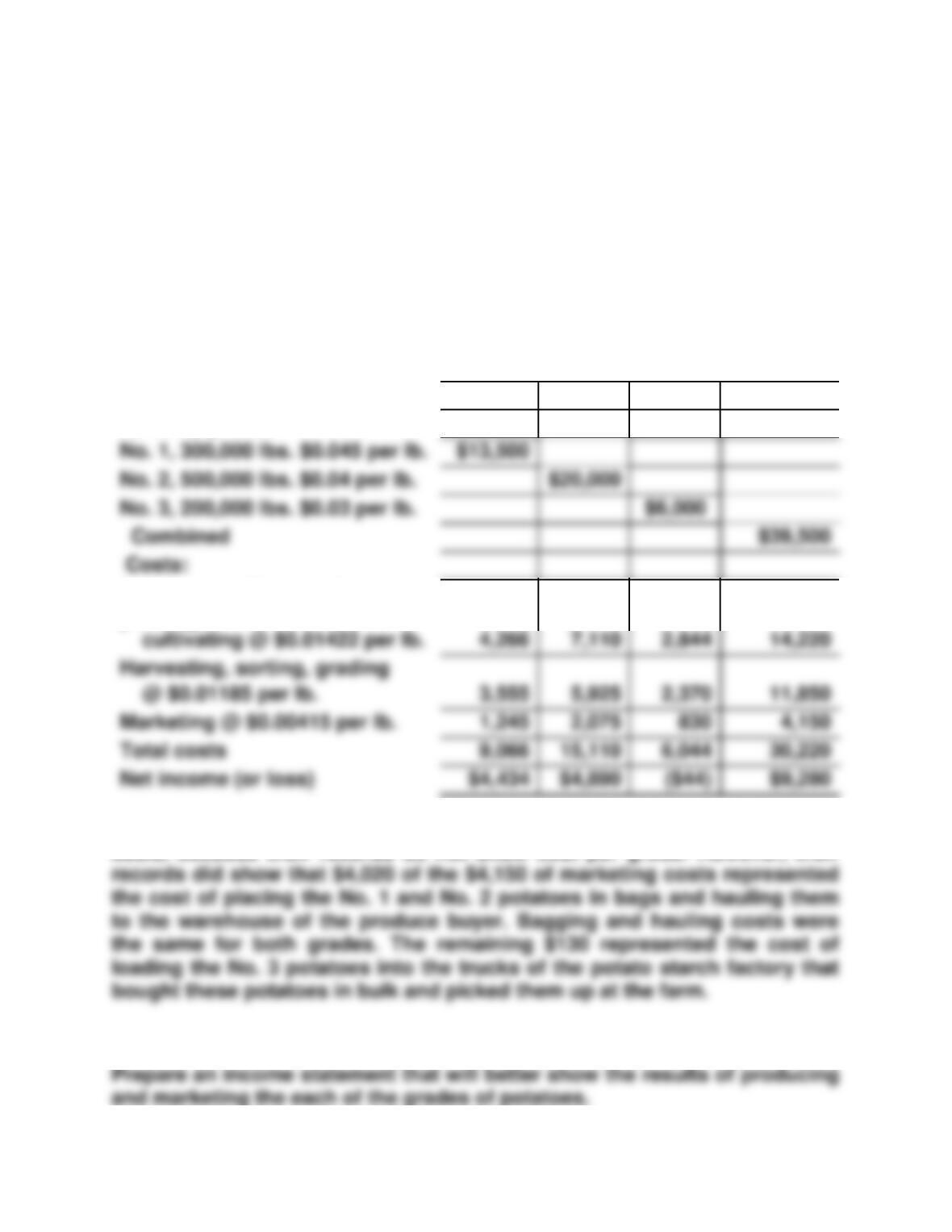

Chapter 24 Alternate Demo Problem

Jack and Susan Roberts own a farm that produces potatoes. Based on a

review of the income statement shown below, Jack remarked that they

should have fed the No. 3 potatoes to the pigs; then they would have

avoided the loss from the sale of the those potatoes.

JACK AND SUSAN ROBERTS

Income from the Production and Sale of Potatoes

For Year Ended December 31, 20xx

Results by Grade

No. 1

No. 2

No. 3

Combined

Sales by grades:

Land preparation, seed,

planting,

Marketing @ $0.00415 per lb.

Total costs

Jack and Susan divided their costs among the grades on a per pound

basis, because their records do not show cost per grade. However, their

Required:

Costs:

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

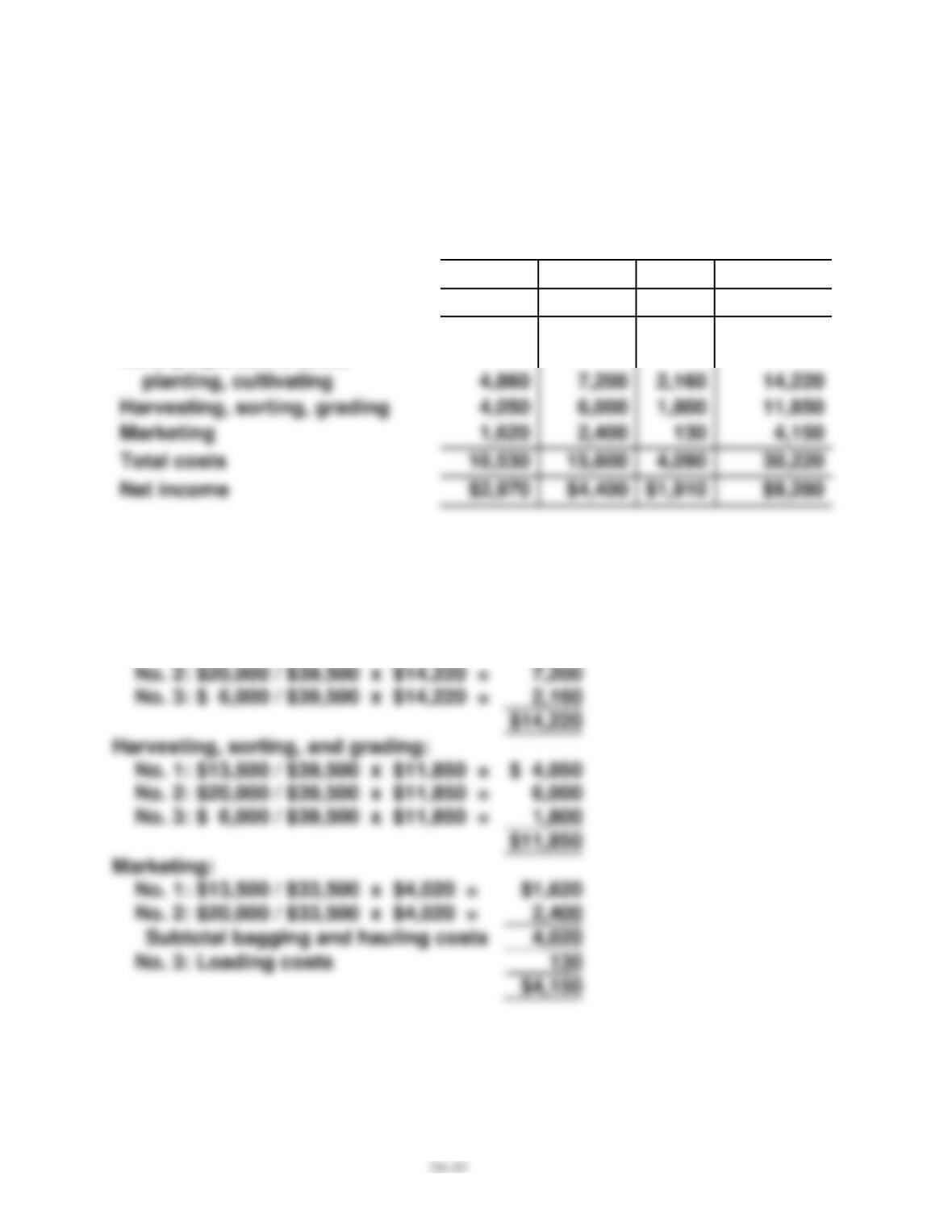

Chapter 24 Alternate Demo Problem: Solution

JACK AND SUSAN ROBERTS

Income from the Production and Sale of Potatoes

For Year Ended December 31, 20xx

Results by Grade

No. 1

No. 2

No. 3

Combined

Revenue from sales:

$13,500

$20,000

$6,000

$39,500

Costs:

Land preparation, seed,

Marketing

Total costs

$1,910

COST ALLOCATIONS

No. 1: $13,500 / $39,500 x $11,850 =

$ 4,050

Land preparation, seed, planting, and

cultivating:

No. 1: $13,500 / $39,500 x $14,220 =

$ 4,860