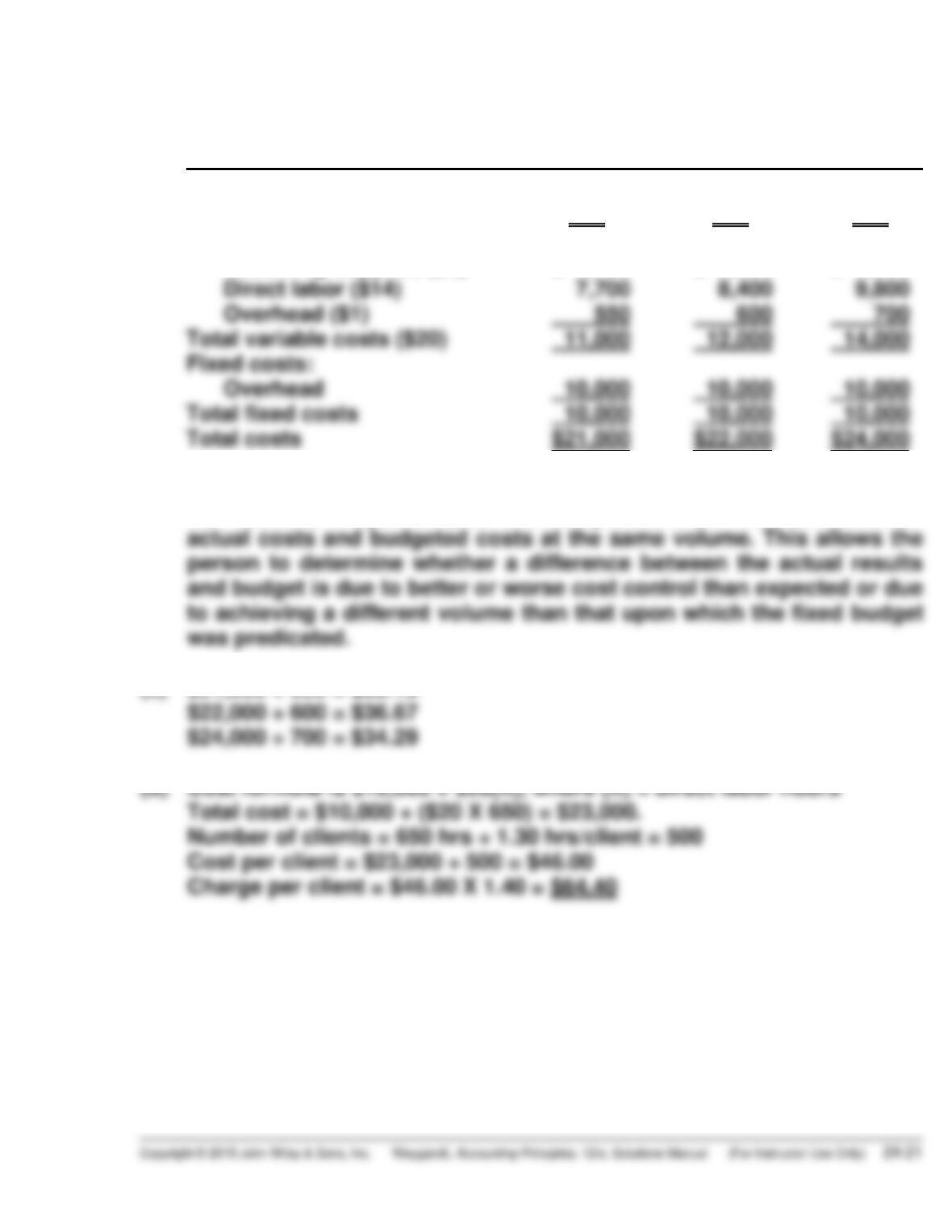

EXERCISE 24-8

(a) RENSING GROOMERS

Flexible Budget

Activity level

Direct labor hours 550 600 700

Variable costs:

Grooming supplies ($5) $ 2,750 $ 3,000 $ 3,500

Direct labor ($14) 7,700 8,400 9,800

Overhead ($1) 550 600 700

(b) A flexible budget presents expected costs at various levels of produc–

tion volume, not just one, so that comparisons can be made between

actual costs and budgeted costs at the same volume. This allows the

(c) $21,000 ÷ 550 = $38.18

(d) Cost formula is $10,000 + $20(X), where (X) = direct labor hours

Total cost = $10,000 + ($20 X 650) = $23,000.

EXERCISE 24-9

(a) SORIA COMPANY

Selling Expense Flexible Budget Report

Clothing Department

For the Month Ended October 31, 2017

Difference

Sales in units

Variable expenses

Sales commissions ($.30)

Advertising expense ($.09)

Fixed expenses

Rent

Sales salaries

Budget

10,000

$ 3,000

900

1,500

1,200

Actual

10,000

$ 2,600

850

1,500

1,200

Favorable F

Unfavorable U

$ 400 F

50 F

0 U

0 U

(b) No, Joe should not have been reprimanded. As shown in the flexible

budget report, variable costs were $1,450 below budget.

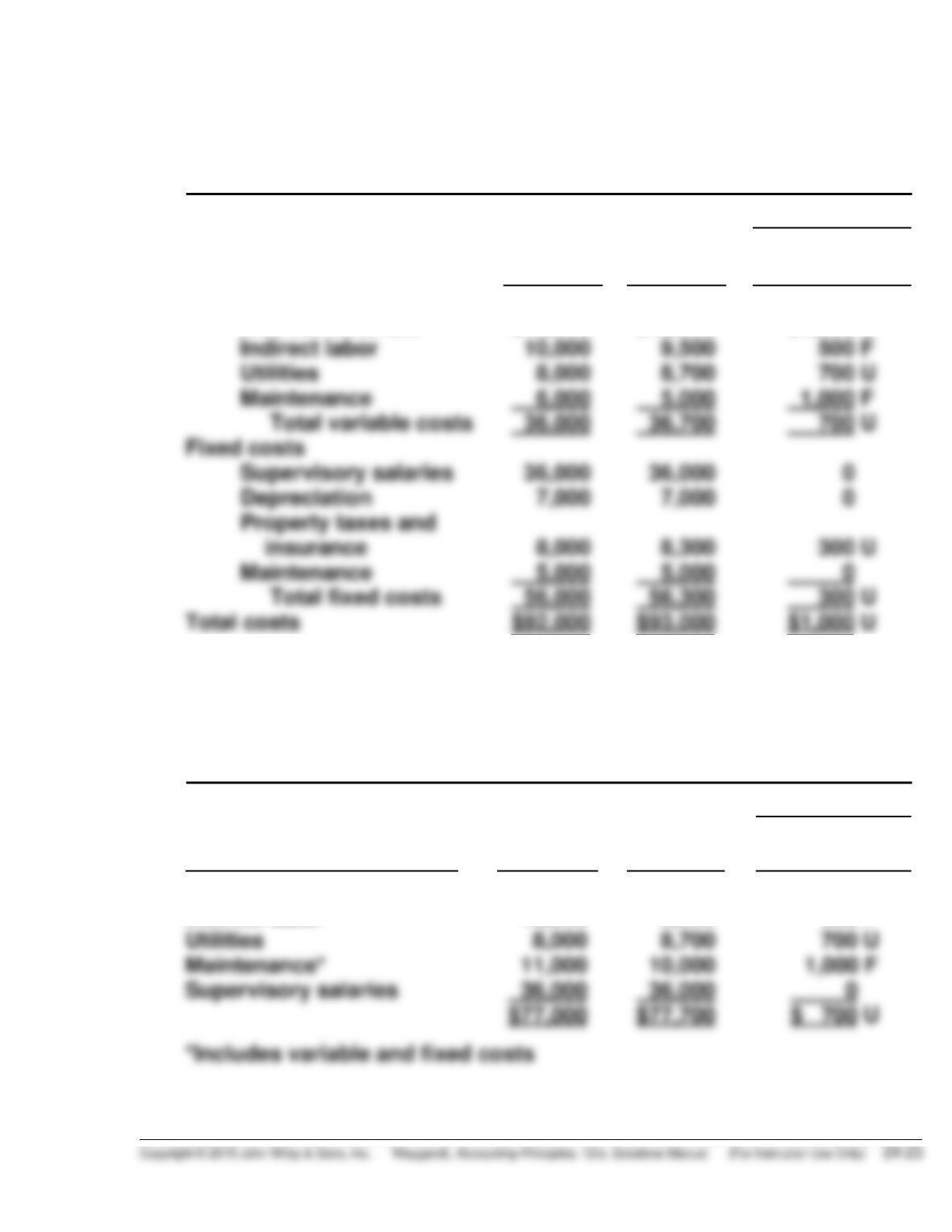

EXERCISE 24–10

(a) CHUBBS INC.

Manufacturing Overhead Flexible Budget Report

For the Quarter Ended March 31, 2017

Difference

Budget

Actual

Favorable F

Unfavorable U

Variable costs

Indirect materials

Indirect labor

Utilities

$12,000

10,000

8,000

$13,500

9,500

8,700

$1,500 U

500 F

700 U

(b) CHUBBS INC.

Manufacturing Overhead Responsibility Report

For the Quarter Ended March 31, 2017

Difference

Controllable Costs

Budget

Actual

Favorable F

Unfavorable U

Indirect materials

Indirect labor

$12,000

10,000

$13,500

9,500

$1,500 U

500 F

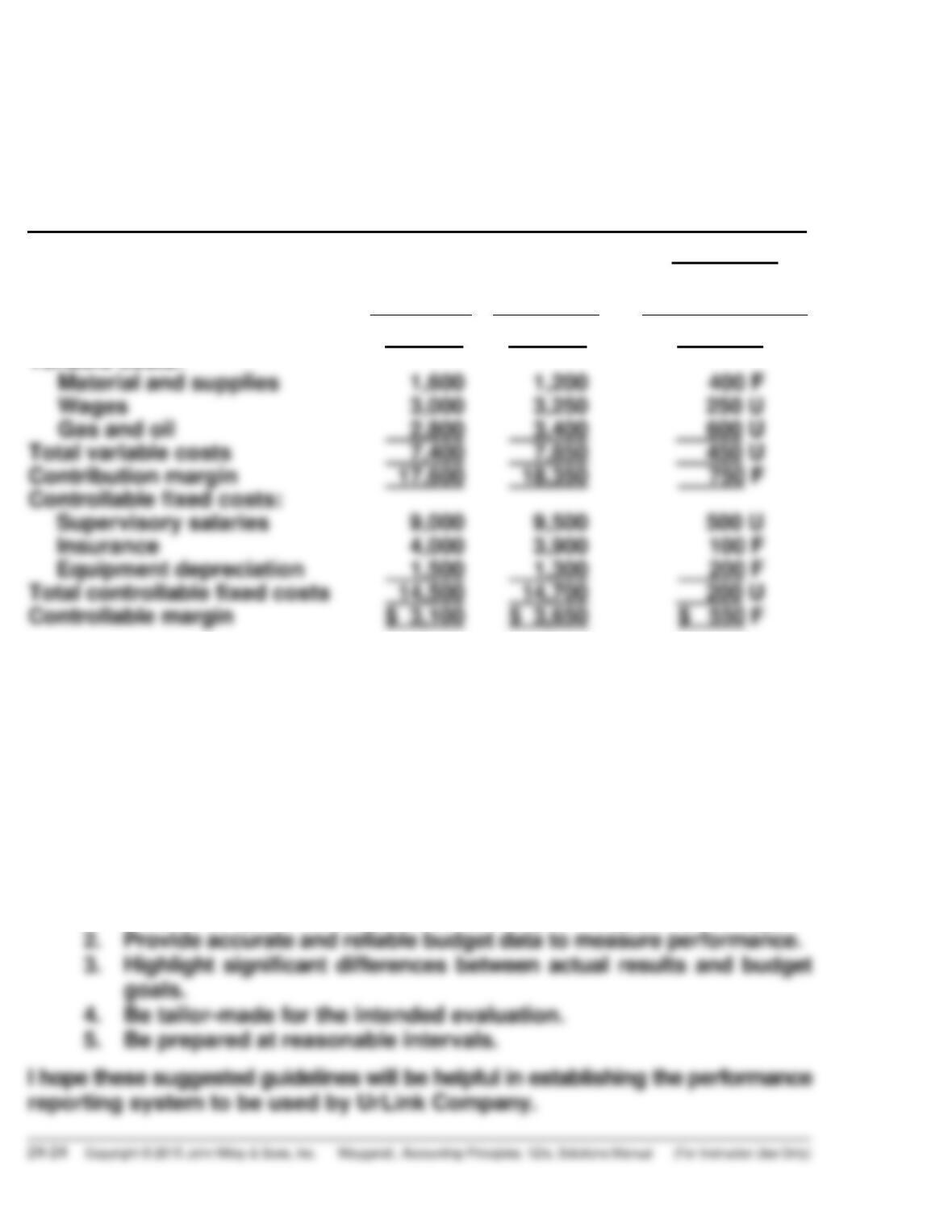

EXERCISE 24–11

(a)

URLINK COMPANY

Home Internet Service Segment

Responsibility Report

For the Quarter Ended March 31, 2017

Budget

Actual

Difference

Favorable F

Unfavorable U

Service revenue

$25,000

$26,200

$1,200 F

Variable costs:

Material and supplies

1,600

1,200

400 F

Wages

3,000

3,250

250 U

Gas and oil

2,800

Total variable costs

7,400

Contribution margin

Controllable fixed costs:

9,000

9,500

500 U

4,000

1,500

Total controllable fixed costs

Controllable margin

$ 3,100

(b)

MEMO

TO: Lenny Kirkland

FROM: Student

SUBJECT: The Reporting Principles of Performance Reports

When evaluating the performance of a company’s segments, the performance

reports should:

1. Contain only data that are controllable by the segment’s manager.

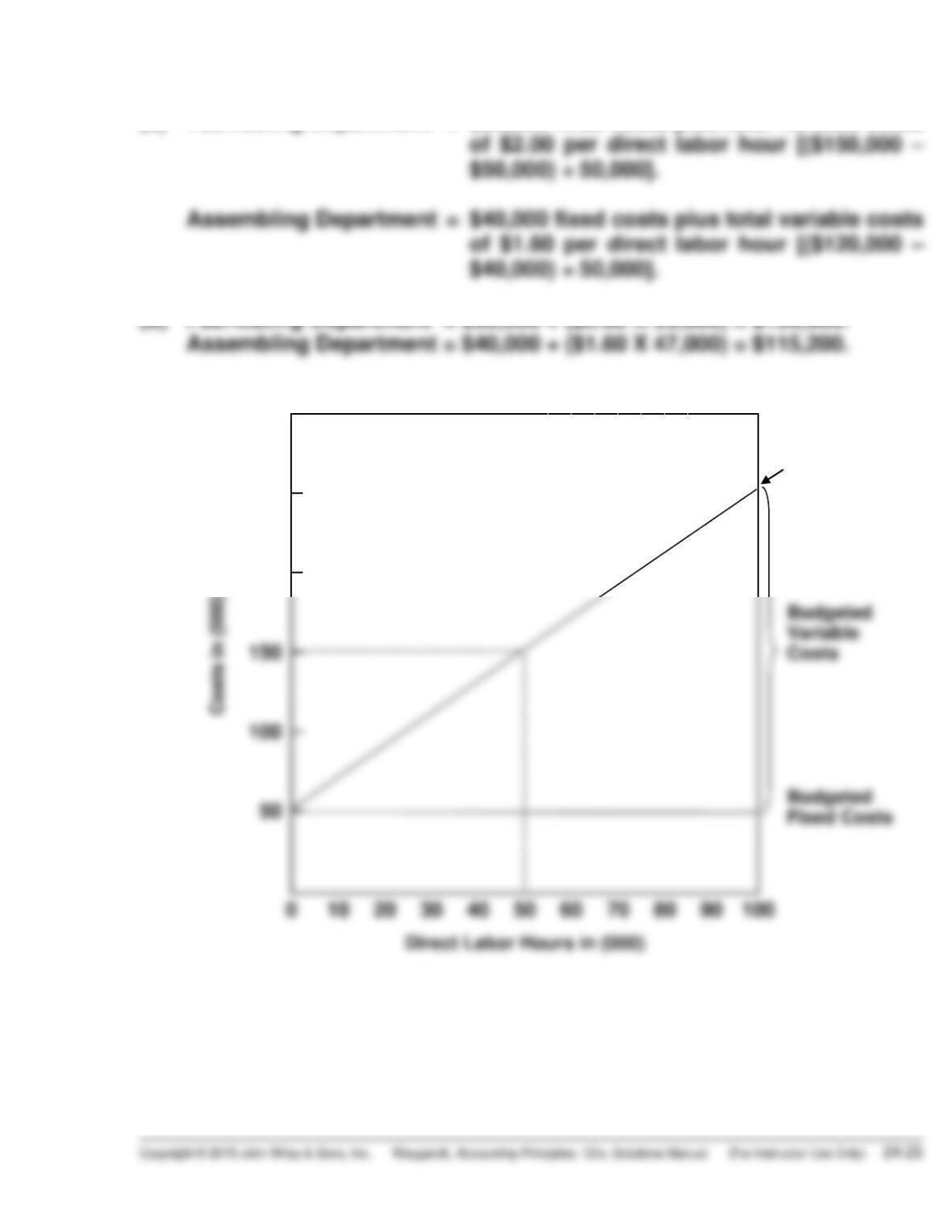

EXERCISE 24–12

(a) Fabricating Department = $50,000 fixed costs plus total variable costs

of $2.00 per direct labor hour [($150,000 –

$50,000) ÷ 50,000].

(c)

$300

150

100

Total

Budgeted

Cost Line

250

200

EXERCISE 24–13

(a)

To Dallas Department Manager—Finishing Month: July

Controllable Costs:

Budget

Actual

Fav/Unfav

$175,200

Direct Materials

Direct Labor

$ 44,000

82,000

$ 42,500

83,400

$1,500 F

1,400 U

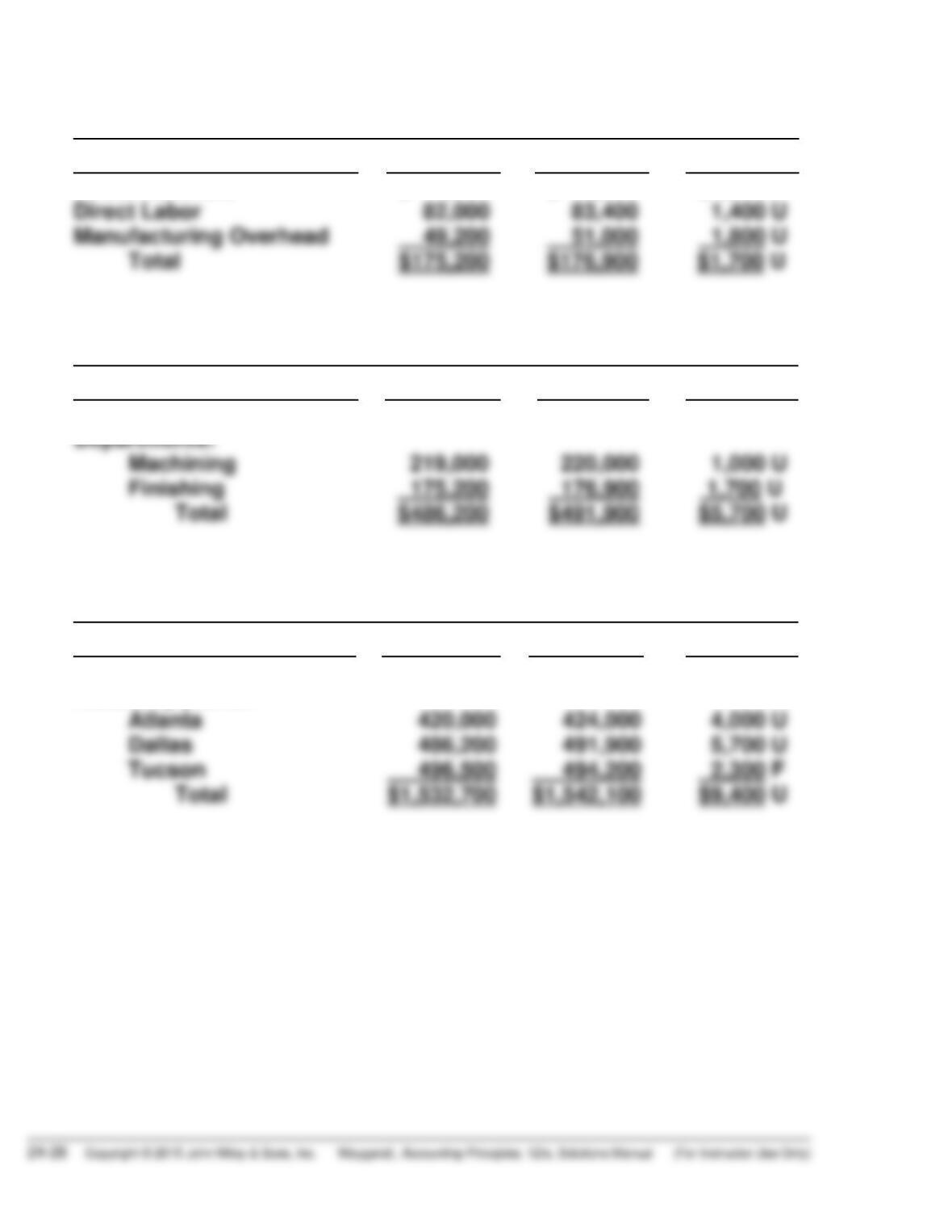

(b)

To Assembly Plant Manager—Dallas Month: July

Controllable Costs:

Budget

Actual

Fav/Unfav

Dallas Office

Departments:

Machining

Finishing

Total

$ 92,000

219,000

175,200

$486,200

$ 95,000

220,000

176,900

$491,900

$3,000 U

1,000 U

1,700 U

$5,700 U

(c)

To Vice President—Production Month: July

Controllable Costs:

Budget

Actual

Fav/Unfav

V P Production

Assembly plants:

Atlanta

$ 130,000

420,000

$ 132,000

424,000

$2,000 U

4,000 U

EXERCISE 24–14

(a) MALONE COMPANY

Mixing Department

Responsibility Report

For the Month Ended January 31, 2017

Controllable Cost

Budget

Actual

Difference

Indirect labor

Indirect materials

$12,000

7,700

$12,250

10,200

$ 250 UU

2,500 U

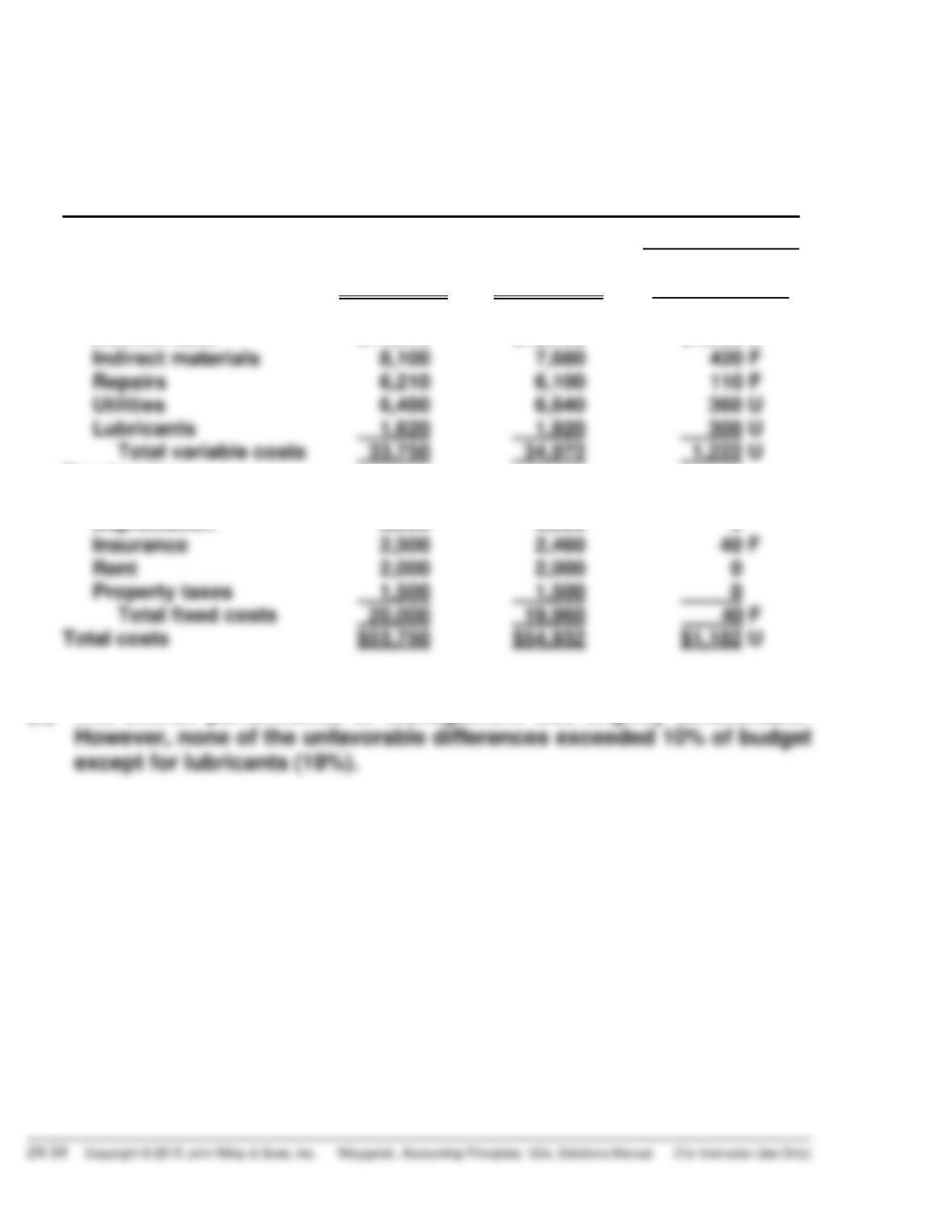

(b) Most likely, when management examined the responsibility report for

January, they would determine that the differences were insignificant

for indirect labor (2.1% of budget), lubricants (1.5%), and maintenance

EXERCISE 24–15

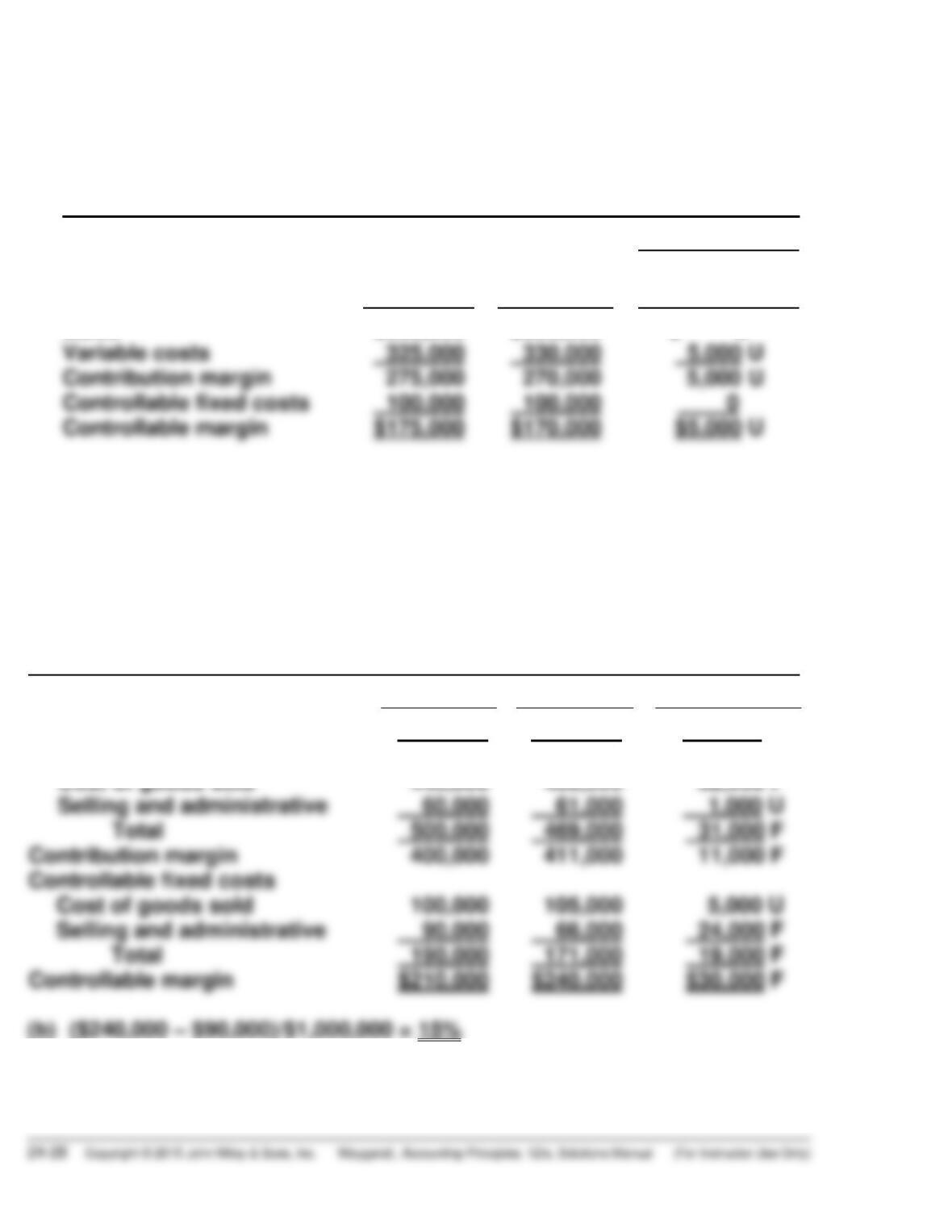

(a) 1. Controllable margin ($270,000 – $100,000) $170,000

2. Variable costs ($600,000 – $270,000) 330,000

3. Contribution margin ($450,000 – $320,000) 130,000

EXERCISE 24-15 (Continued)

(b) HORATIO INC.

Women’s Shoe Division

Responsibility Report

For the Month Ended June 30, 2017

Difference

Budget

Actual

Favorable F

Unfavorable U

Sales

Variable costs

$600,000

325,000

$600,000

330,000

$ 0 U

5,000 U

EXERCISE 24–16

(a) HARRINGTON COMPANY

Sports Equipment Division

Responsibility Report

2017

Budget

Actual

Difference

Sales

$900,000

$880,000

$20,000 U

Variable costs

Cost of goods sold

440,000

408,000

32,000 F

Selling and administrative

60,000

61,000

1,000 U

Total

500,000

469,000

31,000 F

Contribution margin

400,000

411,000

24,000 F

Controllable margin

$30,000 F

EXERCISE 24–17

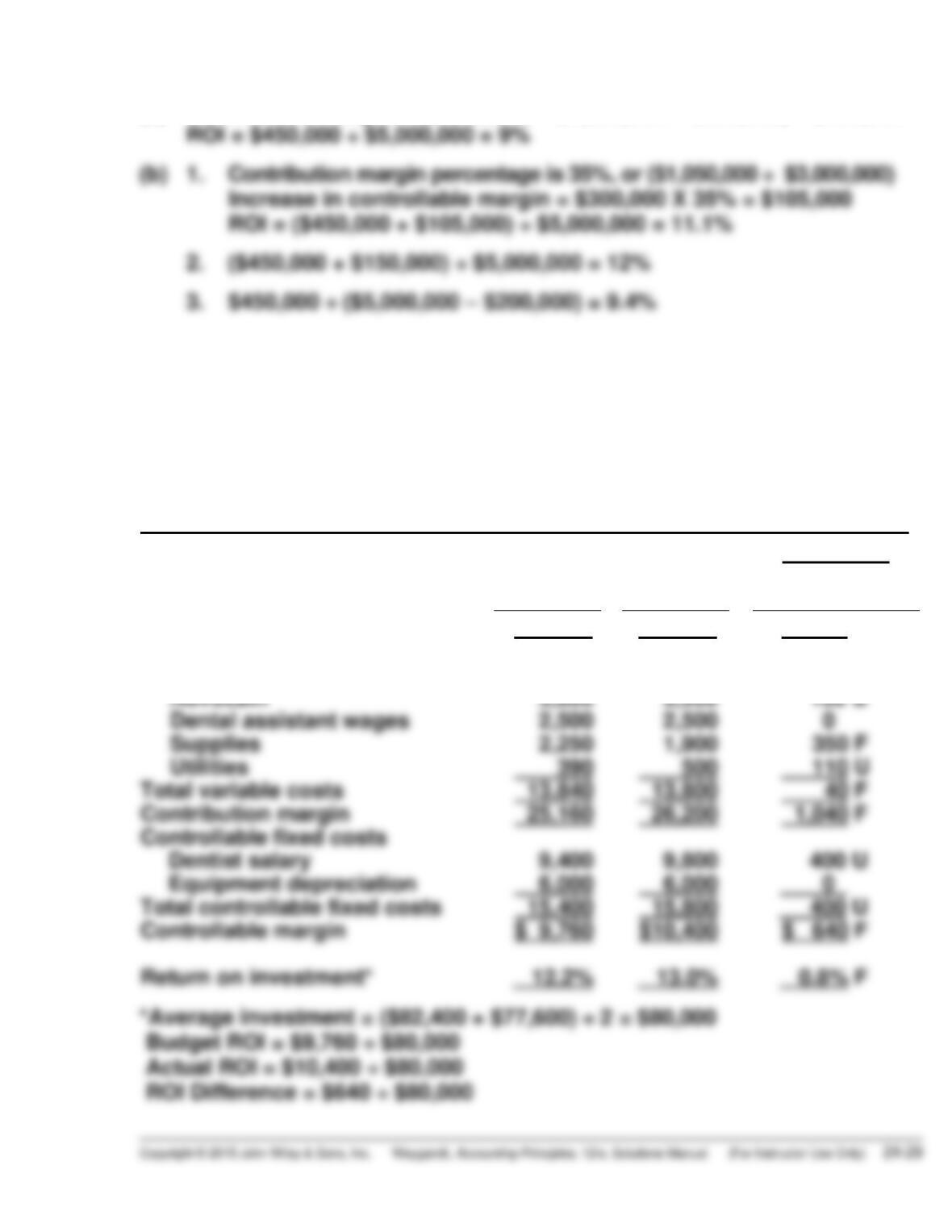

(a) Controllable margin = ($3,000,000 – $1,950,000 – $600,000) = $450,000

ROI = $450,000 ÷ $5,000,000 = 9%

EXERCISE 24–18

(a)

DINKLE AND FRIZELL DENTAL CLINIC

Preventive Services

Responsibility Report

For the Month Ended May 31, 2017

Budget

Actual

Difference

Favorable F

Unfavorable U

Service revenue

$39,000

$40,000

$1,000 F

Variable costs

Filling materials

4,900

5,000

100 U

Novocain

3,800

3,900

100 U

Dental assistant wages

2,500

2,500

0

Supplies

2,250

1,900

Utilities

390

500

110 U

Total variable costs

40 F

Contribution margin

Controllable fixed costs

Dentist salary

9,400

400 U

Equipment depreciation

6,000

6,000

0

Controllable margin

$ 9,760

$10,400

$ 640 F

Return on investment*

12.2%

13.0%

0.8% F

*Average investment = ($82,400 + $77,600) ÷ 2 = $80,000

EXERCISE 24-18 (Continued)

(b)

MEMO

TO: Drs. Reese Dinkle and Anita Frizell

FROM: Student

SUBJECT: Deficiencies in the Current Responsibility Reporting System

The current reporting system has the following deficiencies:

1. It does not clearly show both budgeted goals and actual performance.

2. It does not indicate the contribution margin generated by the center,

showing the amount available to go towards covering controllable

EXERCISE 24–19

Planes:

ROI = Controllable margin ÷ Average operating assets

12% = Controllable margin ÷ $25,000,000

Controllable margin = $25,000,000 X 12%

Taxis:

ROI

=

Controllable margin

÷

Average operating assets

10%

=

$80,000

÷

Average operating assets

Average operating assets

$80,000 ÷ 10%

Controllable margin

=

Contribution margin

–

Controllable fixed costs

$250,000 – $80,000

=

$500,000 – Variable costs

=

$250,000

=

Service revenue – Variable costs

EXERCISE 24-19 (Continued)

Limos:

ROI = Controllable margin ÷ Average operating assets

= $210,000 ÷ $1,500,000

= 14%

SOLUTIONS TO PROBLEMS

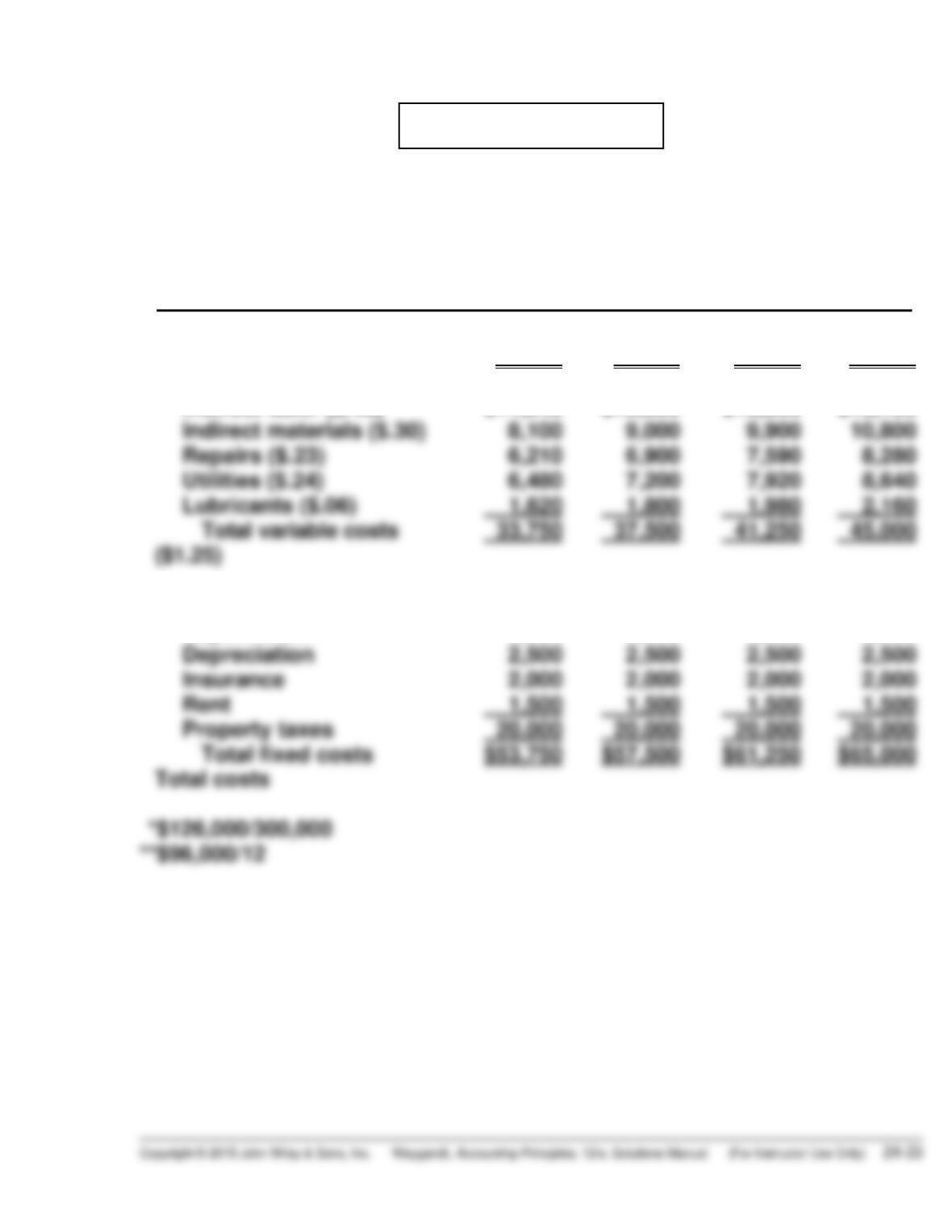

PROBLEM 24–1A

(a) BUMBLEBEE COMPANY

Packaging Department

Monthly Manufacturing Overhead Flexible Budget

For the Year 2017

Activity level

Direct labor hours

Variable costs

Indirect labor ($.42)*

Indirect materials ($.30)

Fixed costs

Supervision**

Depreciation

27,000

$11,340

8,100

8,000

6,000

2,500

30,000

$12,600

9,000

8,000

6,000

2,500

33,000

$13,860

9,900

8,000

6,000

2,500

36,000

$15,120

10,800

8,000

6,000

2,500

PROBLEM 24-1A (Continued)

(b) BUMBLEBEE COMPANY

Packaging Department

Manufacturing Overhead Flexible Budget Report

For the Month Ended October 31, 2017

Difference

Direct labor hours (DLH)

Variable costs

Indirect labor

Fixed costs

Supervision

Depreciation

Insurance

Budget at

27,000 DLH

$11,340

8,000

6,000

2,500

Actual Costs

27,000 DLH

$12,432

8,000

6,000

2,460

Favorable F

Unfavorable U

$1,092 U

0 U

0 U

40 F

(c) The overall performance of management was slightly unfavorable.

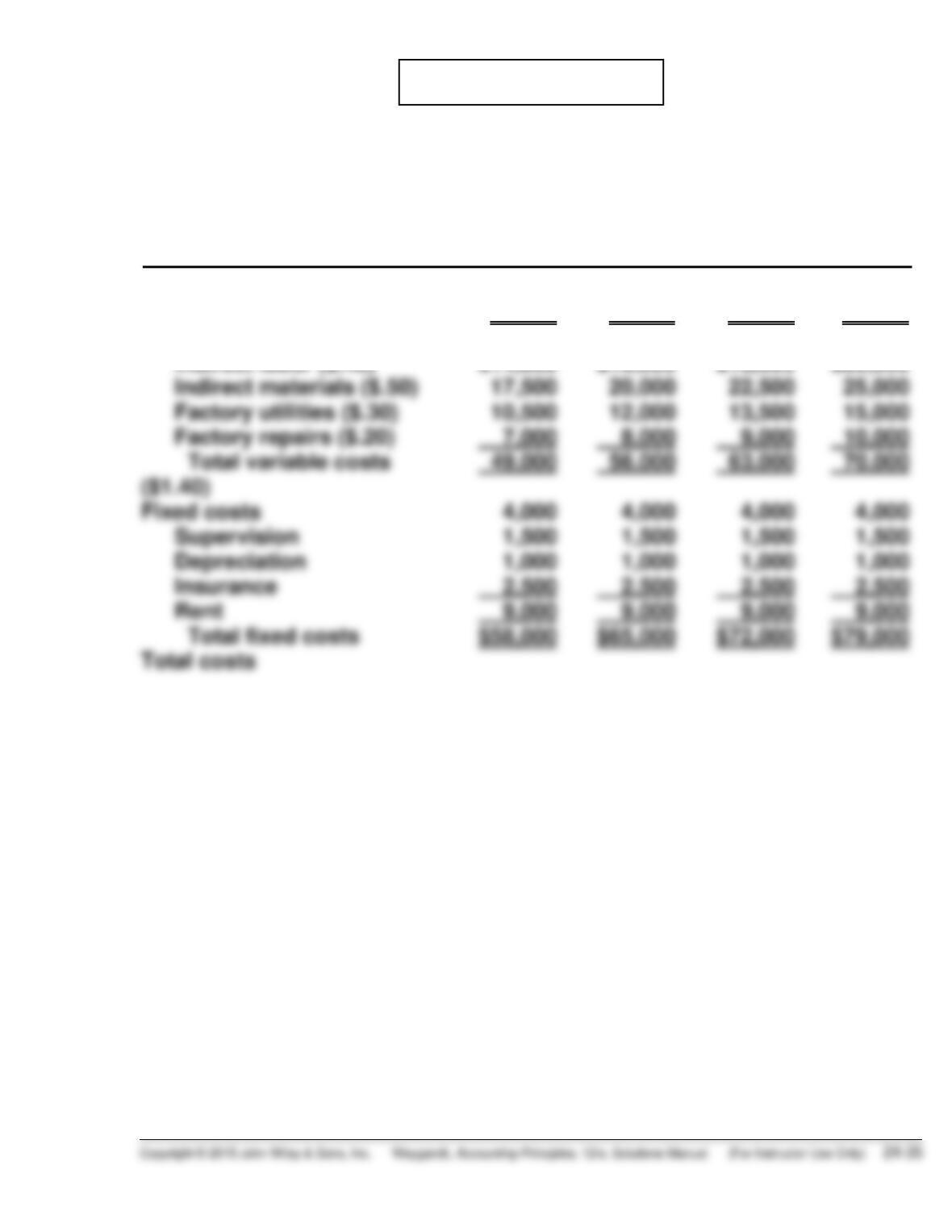

PROBLEM 24–2A

(a) ZELMER COMPANY

Monthly Manufacturing Overhead Flexible Budget

Ironing Department

For the Year 2017

Activity level

Direct labor hours

Variable costs

Indirect labor ($.40)

Indirect materials ($.50)

Factory utilities ($.30)

35,000

$14,000

17,500

10,500

40,000

$16,000

20,000

12,000

45,000

$18,000

22,500

13,500

50,000

$20,000

25,000

15,000

PROBLEM 24-2A (Continued)

(b) ZELMER COMPANY

Ironing Department

Manufacturing Overhead Flexible Budget Report

For the Month Ended June 30, 2017

Difference

Direct labor hours (DLH)

Variable costs

Indirect labor

Indirect materials

Fixed costs

Supervision*

Depreciation

Insurance

Budget at

41,000 DLH

$16,400 (1)

20,500 (2)

4,000

1,500

1,000

Actual Costs

41,000 DLH

$18,040 (5)

19,680 (6)

4,000

1,500

1,000

Favorable F

Unfavorable U

$1,640 U

820 F

0 U

0 U

0 U

(c) The manager was ineffective in controlling variable costs ($3,690 U).

Fixed costs were effectively controlled.

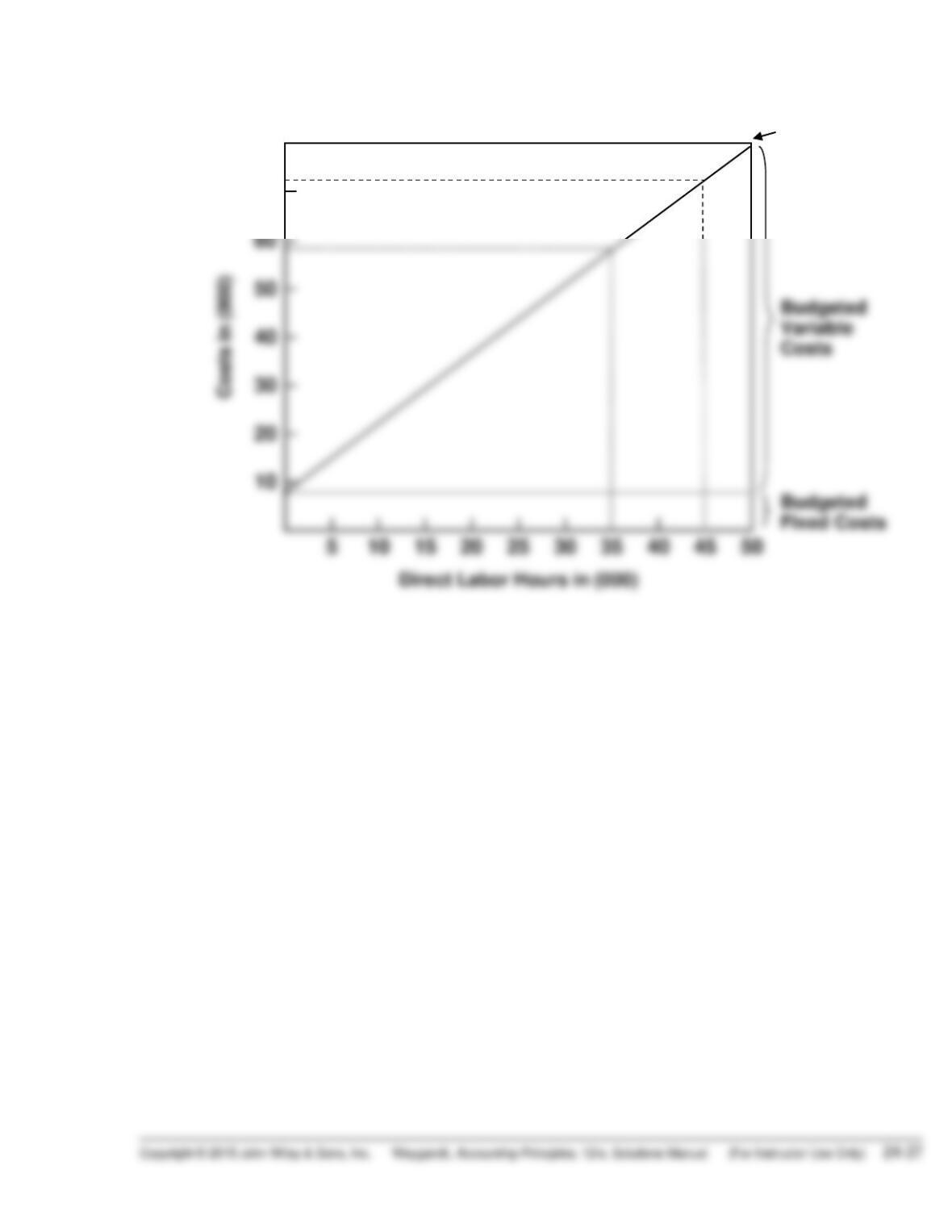

PROBLEM 24-2A (Continued)

(e)

$80

Total

Budgeted

Cost Line

Costs in (000)

70

60

50

Budgeted

Variable

Costs

40

30

20

10

Budgeted

Fixed Costs

5

10

15

20

25

30

35

40

45

50

Direct Labor Hours in (000)

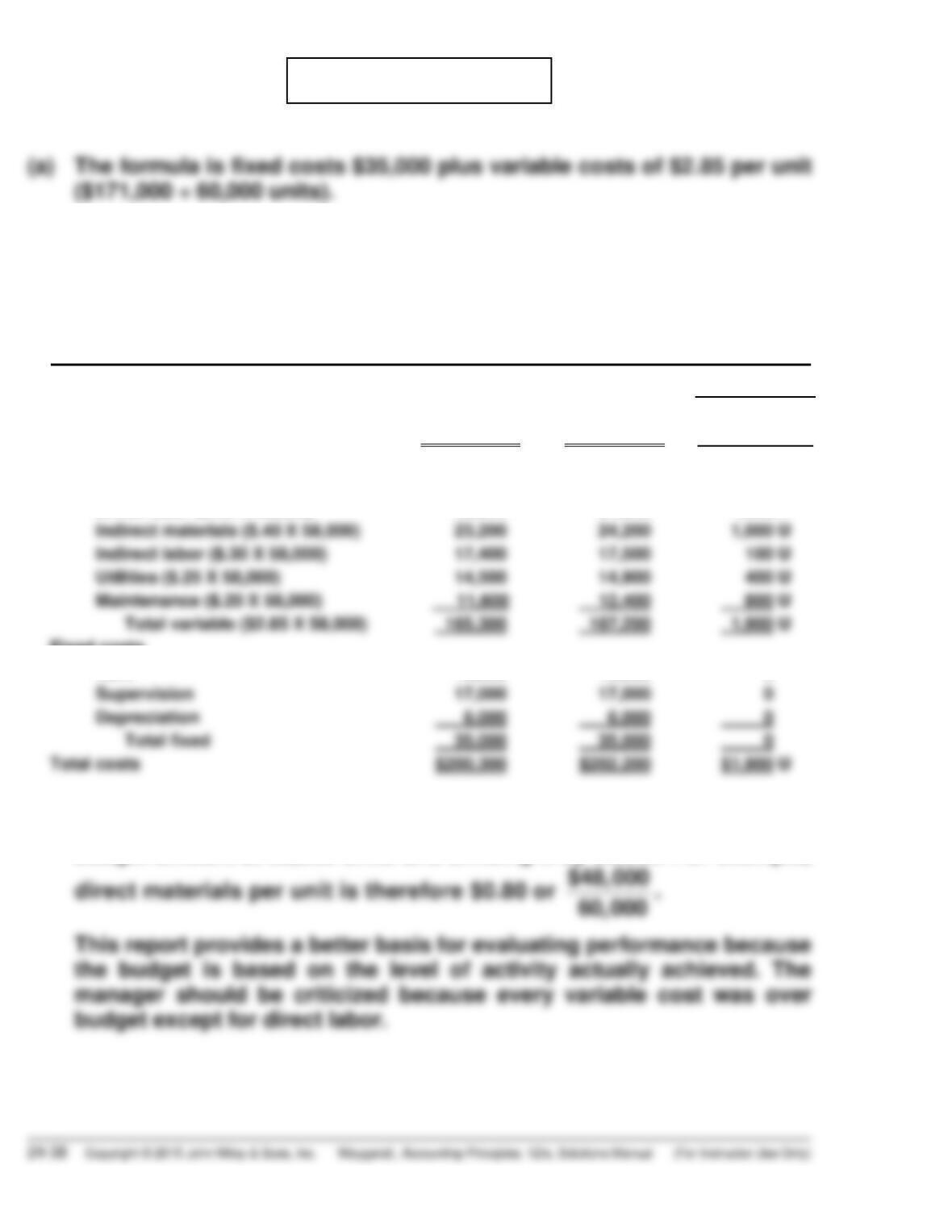

PROBLEM 24–3A

(b) RATCHET COMPANY

Assembling Department

Flexible Budget Report

For the Month Ended August 31, 2017

Difference

Units

Variable costs*

Direct materials ($.80 X 58,000)

Direct labor ($.90 X 58,000)

Indirect materials ($.40 X 58,000)

Fixed costs

Rent

Supervision

Budget at

58,000 Units

$ 46,400

52,200

23,200

12,000

17,000

Actual Costs

58,000 Units

$ 47,000

51,200

24,200

12,000

17,000

Favorable F

Unfavorable U

$ 600 U

1,000 F

1,000 U

0 U

0 U

*Note that the per unit variable costs are computed by taking the

budget amount at 60,000 units and dividing it by 60,000. For example,

PROBLEM 24-3A (Continued)

(c) RATCHET COMPANY

Assembling Department

Flexible Budget Report

For the Month Ended September 30, 2017

Difference

Units

Variable costs

Direct materials (.80 X 64,000)

Direct labor ($.90 X 64,000)

Indirect materials ($.40 X 64,000)

Indirect labor ($.30 X 64,000)

Budget at

64,000 Units

$ 51,200

57,600

25,600

19,200

Actual Costs

64,000 Units

$ 51,700

56,320

26,620

19,250

Favorable F

Unfavorable U

$ 500 U

1,280 F

1,020 U

50 U

The manager’s performance was slightly better in September than it

was in August. However, each variable cost was slightly over budget

again except for direct labor.

Note that actual variable costs in September were 10% higher than

the actual variable costs in August. Therefore to find the actual vari-

able costs in September, the actual variable costs in August must be

increased 10% as follows:

August

(actual)

September

(actual)

Direct materials

Direct labor

$ 47,000 X 110%

51,200 X 110%

=

$ 51,700

56,320

PROBLEM 24–4A

(a) CLARKE INC.

Patio Furniture Division

Responsibility Report

For the Year Ended December 31, 2017

Difference

Budget

Actual

Favorable F

Unfavorable U

Sales

$2,500,000

$2,550,000

$50,000 F

(b) The manager effectively controlled revenues and costs. Contribution

margin was $85,000 favorable and controllable margin was $80,000

favorable. Contribution margin was favorable primarily because sales

were $50,000 over budget and variable cost of goods sold was $41,000

(c) Two costs are excluded from the report: (1) noncontrollable fixed costs

and (2) indirect fixed costs. The reason is that neither cost is control-

lable by the Patio Furniture Division Manager.