24-41

SOLUTION

Requirement 1

ROI

=

Operating income

Average total assets

=

= 0.3480 = 34.80%

Requirement 2

Profit margin ratio

=

Operating income

Net sales

24-42

P24-26B, cont.

Requirement 3

Asset turnover ratio

=

Net sales

Average total assets

Requirement 4

Profit

margin ratio

×

Asset

turnover ratio

=

ROI

Paint Stores Division

12.02%

×

2.8953

=

0.3480 = 34.80%

Consumer Division

14.45%

×

0.8076

=

0.1167 = 11.67%

$ 185,000

$ 185,000

24-43

P24-26B, cont.

Requirement 6

P24-27B Determining transfer pricing

Learning Objective 5

3. Total CM $21,600

The Greco Company is decentralized, and divisions are considered investment centers. Greco has one

division that manufactures oak dining room chairs with upholstered seat cushions. The Chair Division

cuts, assembles, and finishes the oak chairs and then purchases and attaches the seat cushions. The Chair

Division currently purchases the cushions for $20 from an outside vendor. The Cushion Division

manufactures upholstered seat cushions that are sold to customers outside the company. The Chair

Division currently sells 900 chairs per quarter, and the Cushion Division is operating at capacity, which

is 900 cushions per quarter. The two divisions report the following information:

Requirements

1. Determine the total contribution margin for Greco Company for the quarter.

2. Assume the Chair Division purchases the 900 cushions needed from the Cushion Division at its

current sales price. What is the total contribution margin for each division and the company?

3. Assume the Chair Division purchases the 900 cushions needed from the Cushion Division at its

current variable cost. What is the total contribution margin for each division and the company?

4. Review your answers for Requirements 1, 2, and 3. What is the best option for Greco Company?

5. Assume the Cushion Division has capacity of 1,800 cushions per quarter and can continue to supply

its outside customers with 900 cushions per quarter and also supply the Chair Division with 900

cushions per quarter. What transfer price should Greco Company set? Explain your reasoning. Using

the transfer price you determined, calculate the total contribution margin for the quarter.

24-44

SOLUTION

Requirement 1

Contribution

Margin

for the Quarter

Units

×

Contribution

Margin per Unit

=

Total

Contribution

Margin

Chair Division

900

Cushion Division

900

Total

Requirement 2

Contribution

Margin

for the Quarter

Units

×

Contribution

Margin per Unit

=

Total

Contribution

Margin

Chair Division

900

×

$12 [$14 + $20 – $22]

=

$ 10,800

Cushion Division

900

×

=

Total

$ 21,600

Requirement 3

Contribution Margin

for the Quarter

Units

×

Contribution

Margin per Unit

=

Total

Contribution

Margin

Chair Division

900

×

$24 [$14 + $20 – $10]

=

$21,600

Cushion Division

900

×

$ 0 [$12 – $22 + $10]

=

Total

24-45

P24-27B, cont.

Requirement 4

The best option for Greco Company is the current scenario. By having the Chair Division purchase the

Requirement 5

Greco Company should set the transfer price at $10 to $20, the range of the variable cost to the outside

price. The total contribution margin does not change for the whole company when the transfer price

24-46

Continuing Problem

P24-28 Using ROI and RI to evaluate investment centers

This problem continues the Daniels Consulting situation from Problem P23-35 of Chapter 23. Daniels

Consulting reported 2018 sales of $3,200,000 and operating income of $185,600. Average total assets

during 2018 were $640,000. Daniels’s target rate of return is 17%.

Calculate Daniels’s profit margin ratio, asset turnover ratio, ROI, and RI for 2018.

SOLUTION

Profit margin ratio

=

Operating income

Net sales

0.2900 = 29.00%

ROI can also be calculated as:

ROI

=

Operating income

Average total assets

=

= 0.2900 = 29.00%

RI

=

Operating income

–

(Target rate of return × Average total assets)

=

$ 185,600

–

(17% × $640,000)

=

$ 185,600

–

24-47

Comprehensive Problem for Chapters 22-24

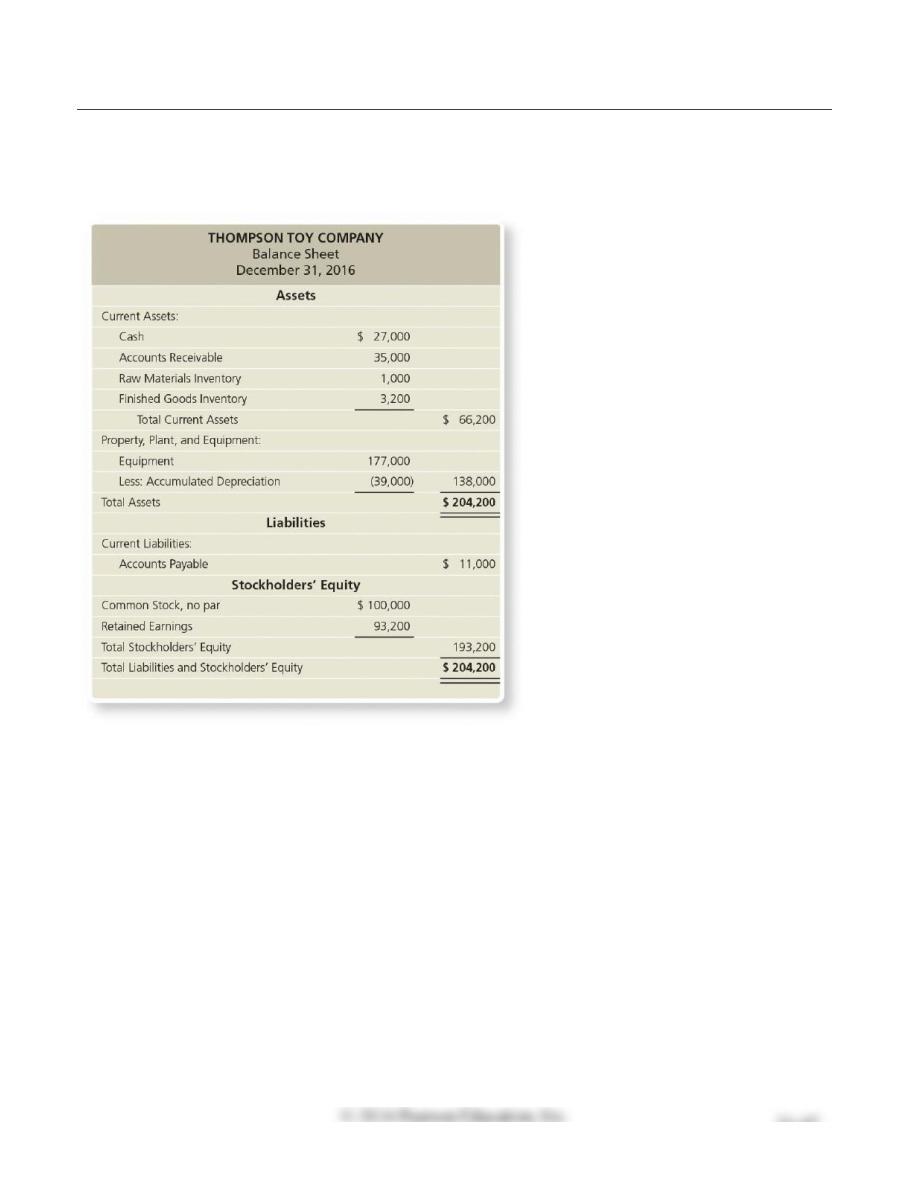

The Thompson Toy Company manufactures toy building block sets for children. Thompson is planning

for 2017 by developing a master budget by quarters. Thompson’s balance sheet for December 31, 2016,

follows:

Other budget data for Thompson Toy Company:

a. Budgeted sales are 500 sets for the first quarter and expected to increase by 100 sets per quarter.

Cash sales are expected to be 40% of total sales, with the remaining 60% of sales on account. Sets

are budgeted to sell for $70 per set.

b. Finished Goods Inventory on December 31, 2016, consists of 100 sets at $32 each.

c. Desired ending Finished Goods Inventory is 30% of the next quarter’s sales; first quarter sales for

2018 are expected to be 900 sets. FIFO inventory costing method is used.

d. Direct materials cost is $10 per set.

e. Desired ending Raw Materials Inventory is 10% of the next quarter’s direct materials needed for

production; desired ending inventory for December 31, 2017, is $1,000; indirect materials are

insignificant and not considered for budgeting purposes.

f. Each set requires 0.20 hours of direct labor; direct labor costs average $10 per hour.

g. Variable manufacturing overhead is $2 per set.

h. Fixed manufacturing overhead includes $4,000 per quarter in depreciation and $1,540 per quarter for

other costs, such as utilities, insurance, and property taxes.

i. Fixed selling and administrative expenses include $8,500 per quarter for salaries; $2,400 per quarter

for rent; $750 per quarter for insurance; and $1,500 per quarter for depreciation.

24-48

j. Variable selling and administrative expenses include supplies at 1% of sales.

k. Capital expenditures include $30,000 for new manufacturing equipment, to be purchased and paid

for in the first quarter.

l. Cash receipts for sales on account are 30% in the quarter of the sale and 70% in the quarter

following the sale; Accounts Receivable balance on December 31, 2016, is expected to be received

in the first quarter of 2017; uncollectible accounts are considered insignificant and not considered for

budgeting purposes.

m. Direct materials purchases are paid 90% in the quarter purchased and 10% in the following quarter;

Accounts Payable balance on December 31, 2016, is expected to be paid in the first quarter of 2017.

n. Direct labor, manufacturing overhead, and selling and administrative costs are paid in the quarter

incurred.

o. Income tax expense is projected at $3,500 per quarter and is paid in the quarter incurred.

p. Thompson desires to maintain a minimum cash balance of $25,000 and borrows from the local bank

as needed in increments of $1,000 at the beginning of the quarter; principal repayments are made at

the beginning of the quarter when excess funds are available and in increments of $1,000; interest is

5% per year and paid at the beginning of the quarter based on the amount outstanding from the

previous quarter.

Requirements

1. Prepare Thompson’s operating budget and cash budget for 2017 by quarter. Required schedules and

budgets include: sales budget, production budget, direct materials budget, direct labor budget,

manufacturing overhead budget, cost of goods sold budget, selling and administrative expense

budget, schedule of cash receipts, schedule of cash payments, and cash budget. Manufacturing

overhead costs are allocated based on direct labor hours.

2. Prepare Thompson’s annual financial budget for 2017, including budgeted income statement,

budgeted balance sheet, and budgeted statement of cash flows.

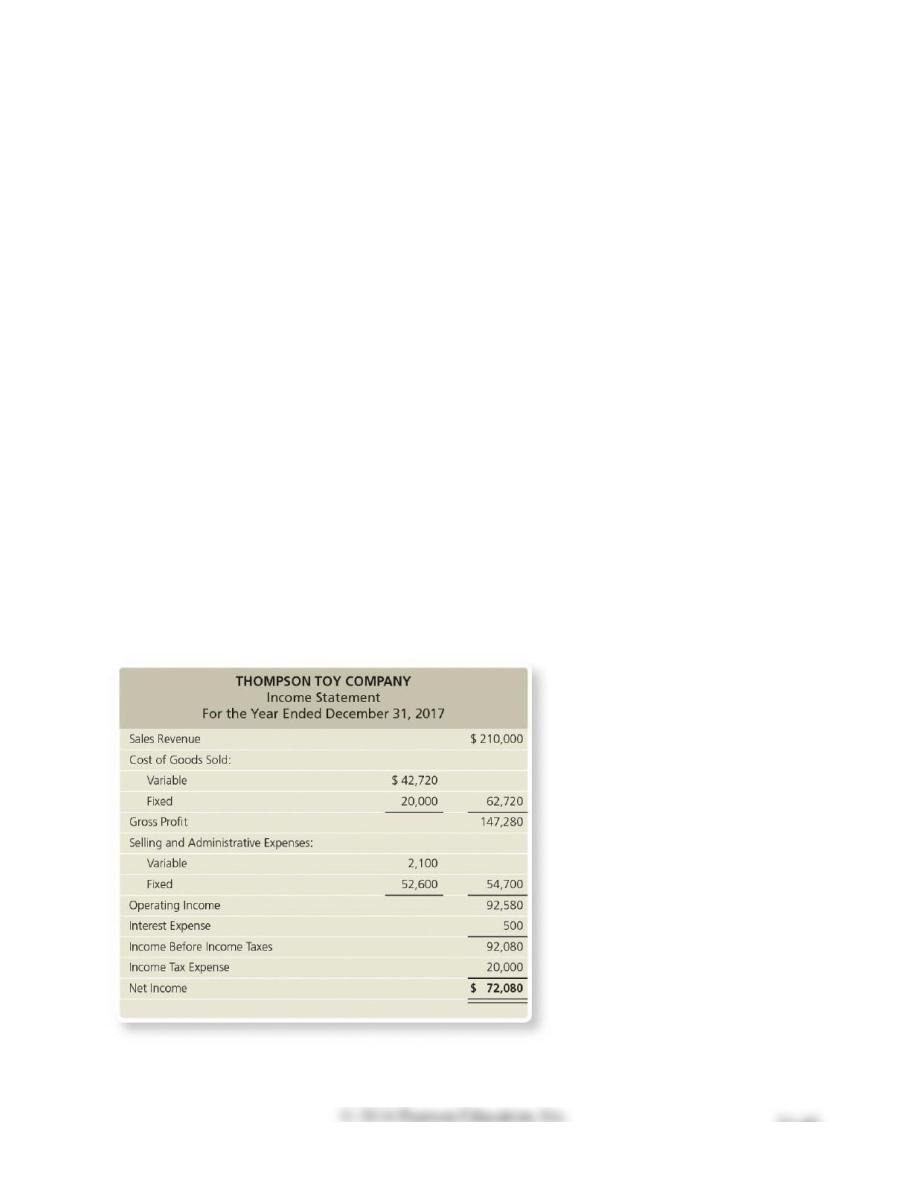

3. Thompson sold 3,000 sets in 2017, and its actual operating income was as follows:

24-49

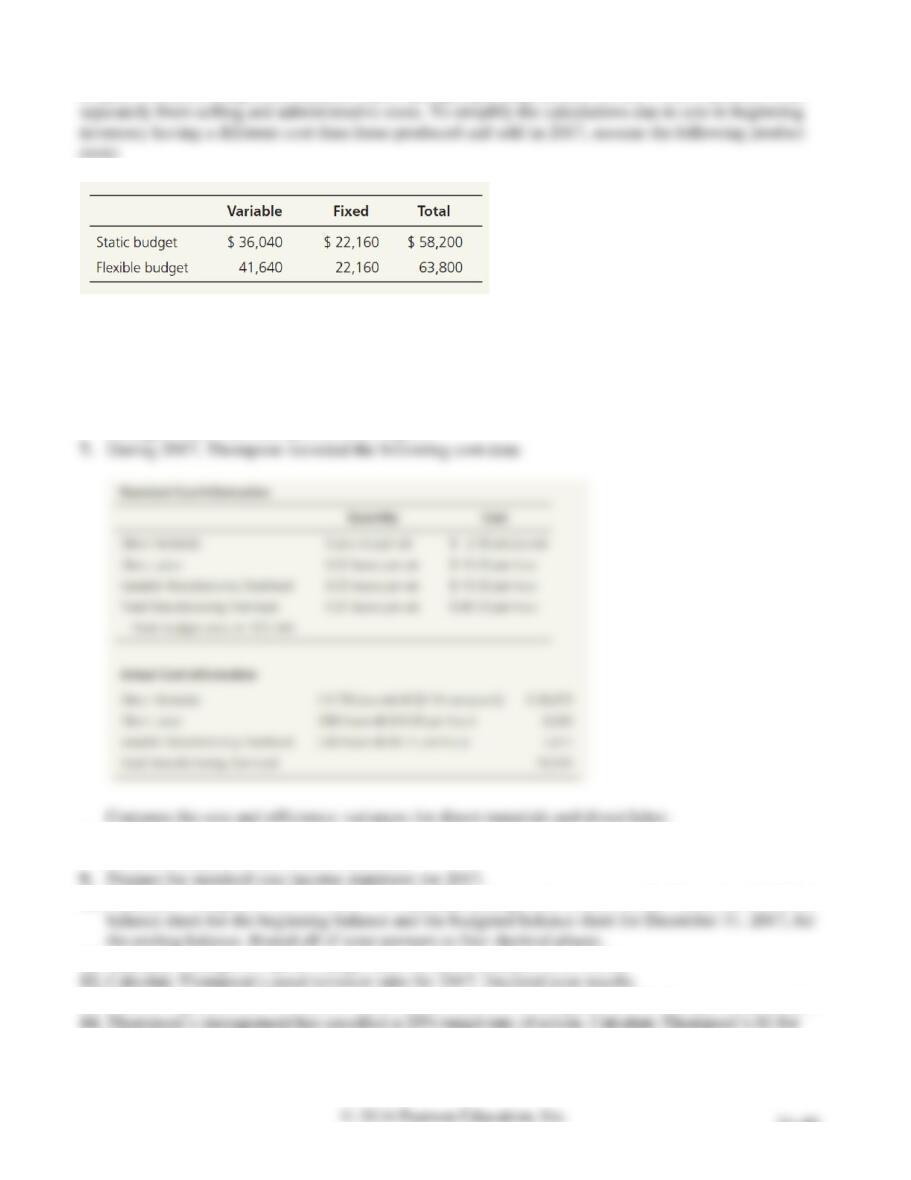

Prepare a flexible budget performance report through operating income for 2017. Show product costs

4. What was the effect on Thompson’s operating income of selling 400 sets more than the static budget

level of sales?

5. What is Thompson’s static budget variance for operating income?

6. Explain why the flexible budget performance report provides more useful information to

Thompson’s managers than the static budget performance report. What insights can Thompson’s

managers draw from this performance report?

8. For manufacturing overhead, compute the variable overhead cost and efficiency variances and the

fixed overhead cost and volume variances.

10. Calculate Thompson’s ROI for 2017. To calculate average total assets, use the December 31, 2016,

11. Calculate Thompson’s profit margin ratio for 2017. Interpret your results.

13. Use the expanded ROI formula to confirm your results from Requirement 10. Interpret your results.

2017. Interpret your results.

24-50

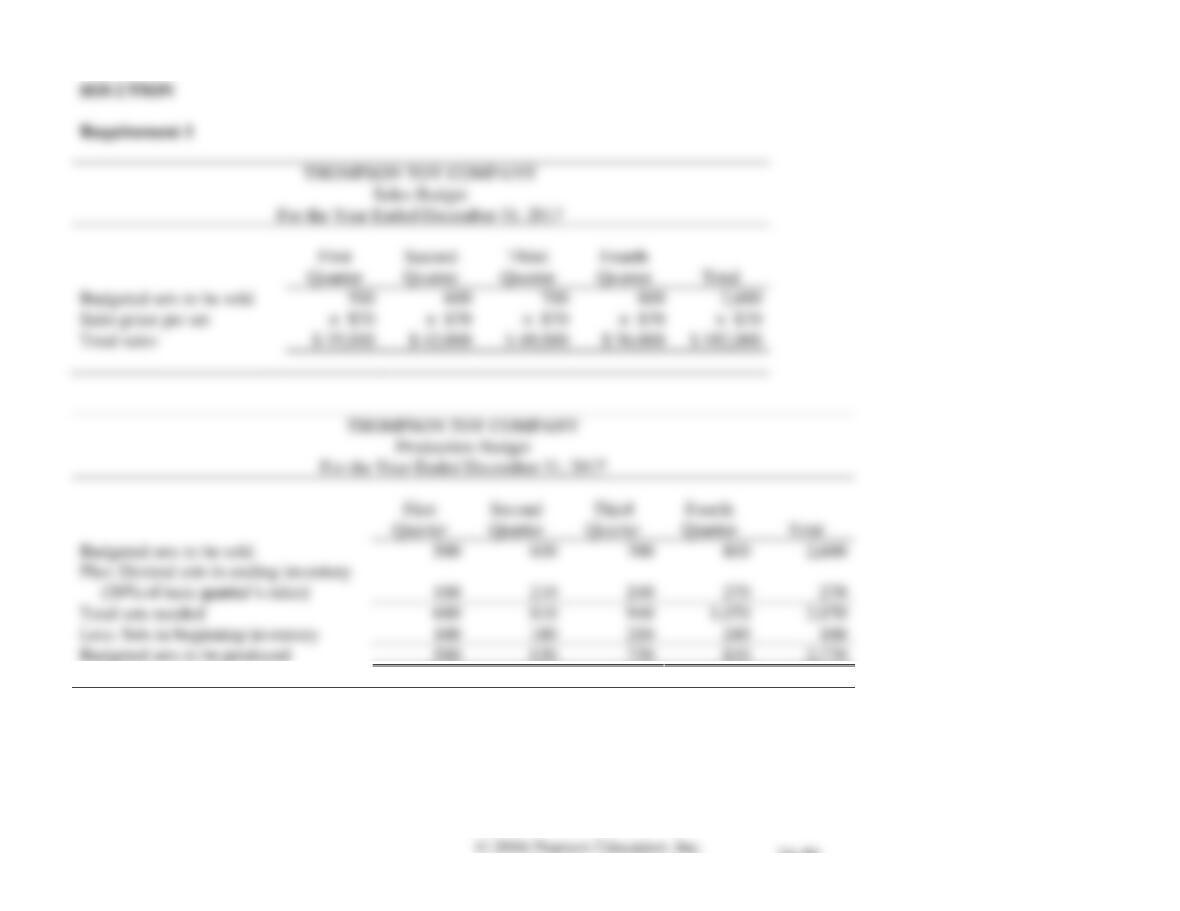

Budgeted sets to be sold

Sales price per set

Total sales

Budgeted sets to be sold

(30% of next quarter’s sales)

Total sets needed

Less: Sets in beginning inventory

Budgeted sets to be produced

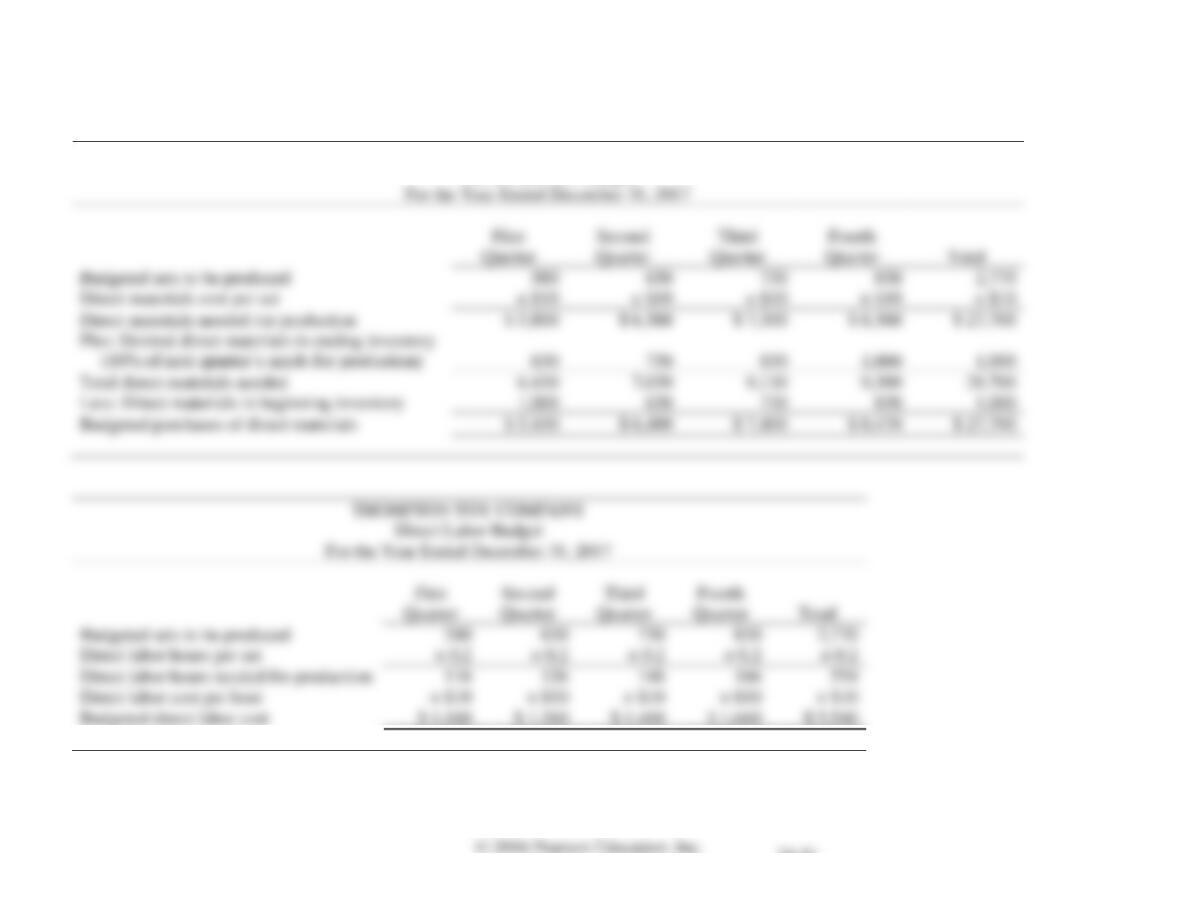

24-51

Comprehensive Problem for Chapters 22-24, cont.

Requirement 1, cont.

THOMPSON TOY COMPANY

Direct Materials Budget

Budgeted sets to be produced

Direct materials cost per set

Direct materials needed for production

(10% of next quarter’s needs for production)

Total direct materials needed

Less: Direct materials in beginning inventory

Budgeted purchases of direct materials

Budgeted sets to be produced

Direct labor hours per set

Direct labor hours needed for production

Direct labor cost per hour

Budgeted direct labor cost

24-52

Comprehensive Problem for Chapters 22-24, cont.

Requirement 1, cont.

THOMPSON TOY COMPANY

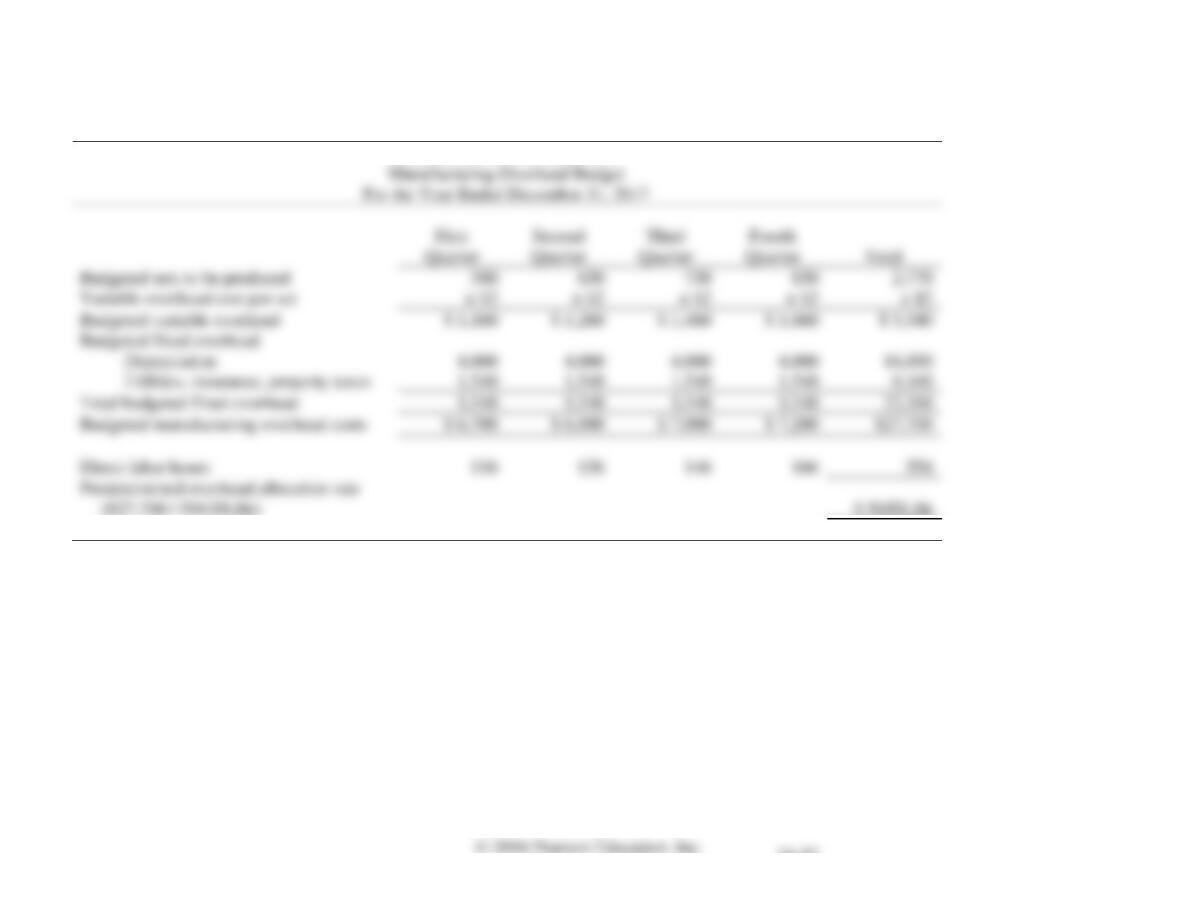

Budgeted sets to be produced

Variable overhead cost per set

Budgeted variable overhead

Budgeted fixed overhead

Depreciation

Utilities, insurance, property taxes

Total budgeted fixed overhead

Budgeted manufacturing overhead costs

Direct labor hours

($27,700 / 554 DLHr)

24-53

Comprehensive Problem for Chapters 22-24, cont.

Requirement 1, cont.

Calculations for Cost of Goods Sold Budget:

Year ended December 31, 2017:

Direct materials cost per set

Direct labor cost per set (0.2 DLHr/set × $10/DLHr)

Manufacturing overhead cost per set (0.2 DLHr/set × $50/DLHr)

Total projected manufacturing cost per set

Beginning inventory, 100 sets at $32 each

Sets produced and sold in 2017 at $22 each

Total budgeted cost of goods sold

24-54

Comprehensive Problem for Chapters 22-24, cont.

Requirement 1, cont.

THOMPSON TOY COMPANY

Salaries Expense

Rent Expense

Insurance Expense

Depreciation Expense

Supplies Expense (1% of sales)

Total budgeted selling and administrative expense

Comprehensive Problem for Chapters 22-24, cont.

Requirement 1, cont.

Schedule of Cash Receipts from Customers

Total sales

First

Second

Third

Fourth

Cash Receipts from Customers:

Accounts Receivable balance, December 31, 2016

6,300

7,560

8,820

Total cash receipts from customers

Accounts Receivable balance, December 31, 2017:

First

Second

Third

Fourth