PROBLEM 23-4A (Continued)

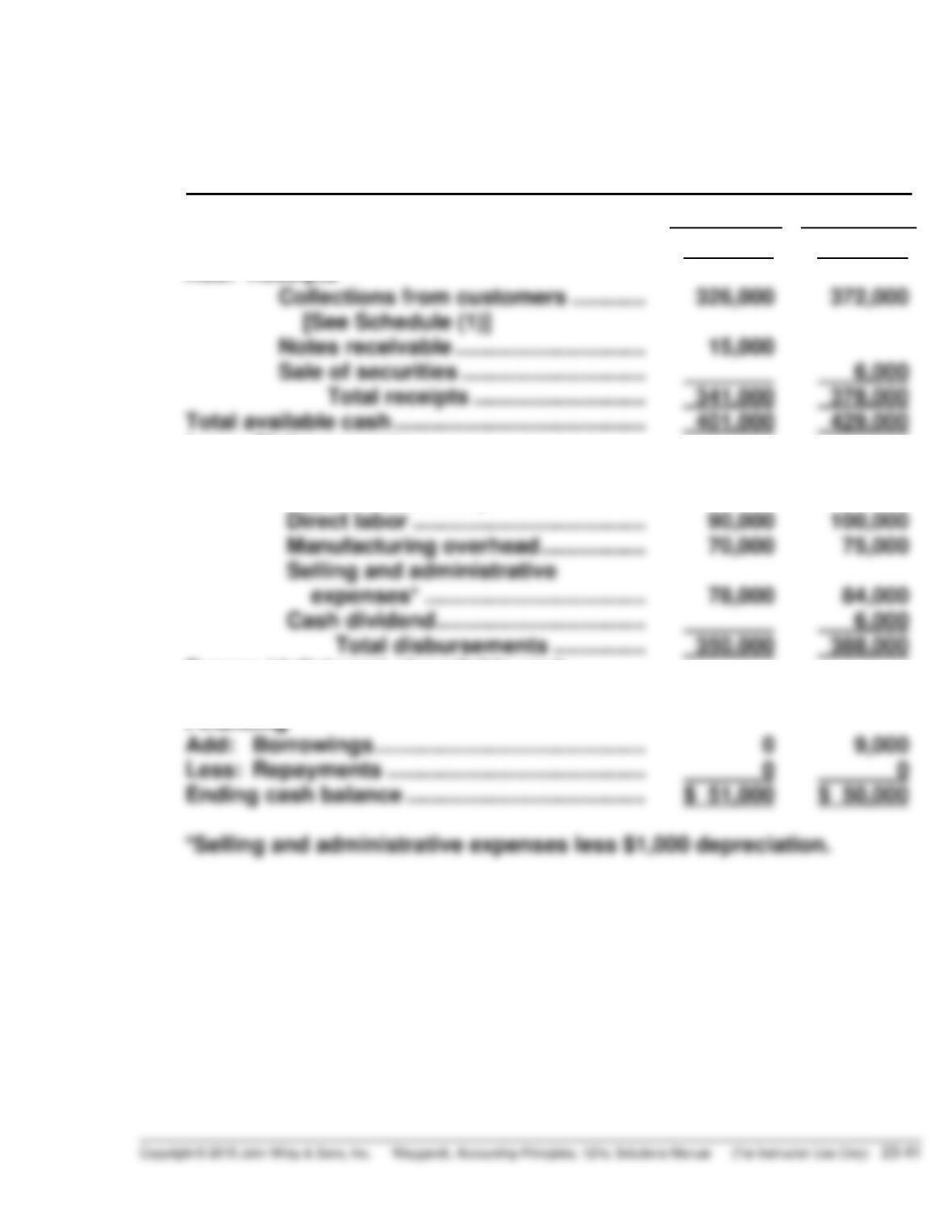

(b) COLTER COMPANY

Cash Budget

For the Two Months Ending February 28, 2017

January

February

Beginning cash balance …………………………….

Add: Receipts

Collections from customers …………

[See Schedule (1)]

Total available cash …………………………………..

$ 60,000

326,000

401,000

$ 51,000

372,000

429,000

$ 51,000

$ 50,000

Less: Disbursements

Direct materials ………………………….

[See Schedule 2]

Excess (deficiency) of available cash

over cash disbursements ……………………….

Financing

112,000

51,000

123,000

41,000

PROBLEM 23–5A

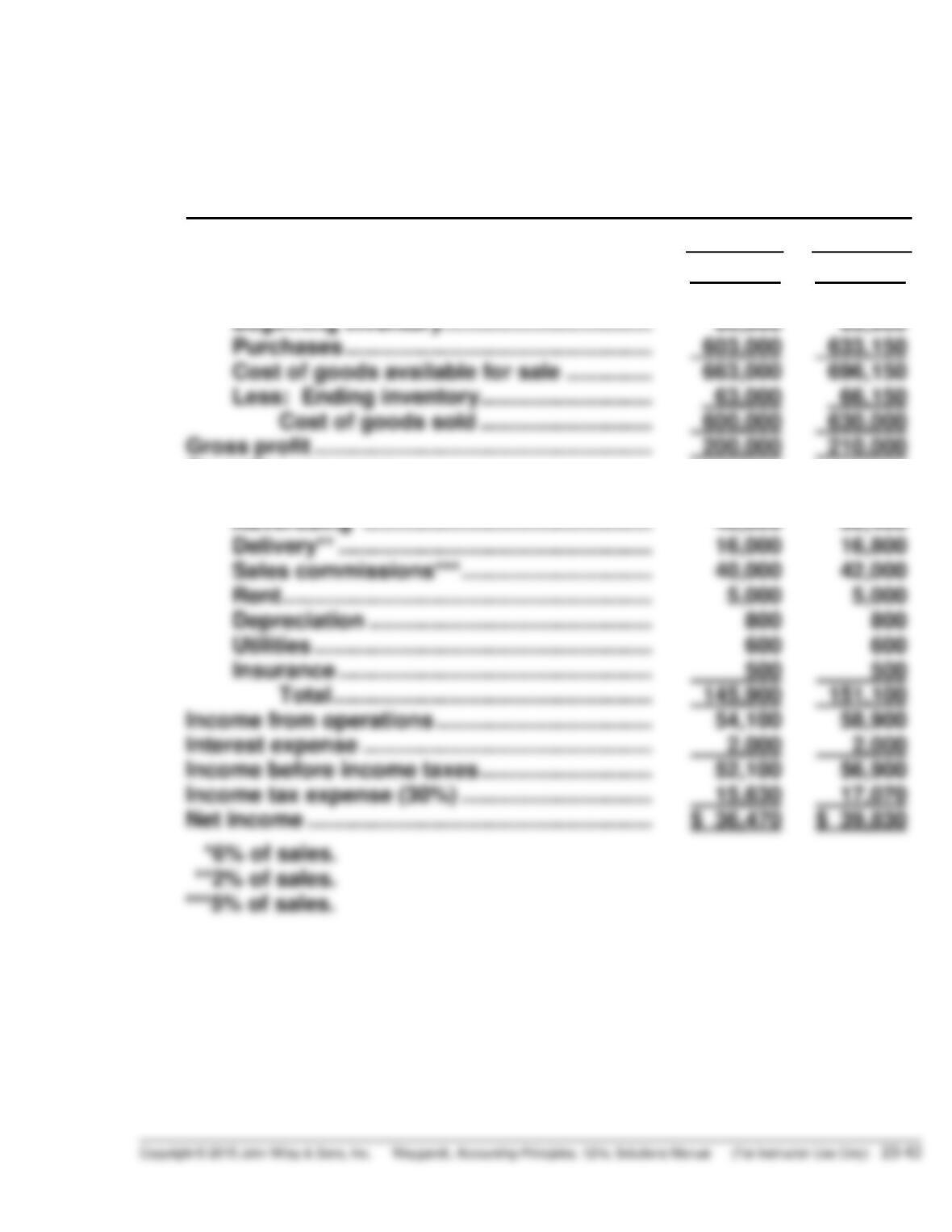

(a) SUPPAR COMPANY

San Miguel Store

Merchandise Purchases Budget

For the Months of May and June, 2017

May

June

Budgeted cost of goods sold ………………………

Add: Desired ending merchandise inventory …..

$600,000

63,000

(2)

$630,000

66,150

(1)

(3)

PROBLEM 23-5A (Continued)

(b) SUPPAR COMPANY

San Miguel Store

Budgeted Income Statement

For the Months of May and June, 2017

May

June

Sales ………………………………………………………...

Cost of goods sold

Beginning inventory …………………………….

Gross profit ……………………………………………….

$800,000

60,000

200,000

$840,000

63,000

210,000

$ 36,470

$ 39,830

Operating expenses

Sales salaries ……………………………………..

Advertising* ………………………………………..

Total …………………………………………….

Income from operations ……………………………..

Interest expense ………………………………………..

Income before income taxes ……………………….

35,000

48,000

145,900

54,100

2,000

52,100

35,000

50,400

151,100

58,900

2,000

56,900

PROBLEM 23–6A

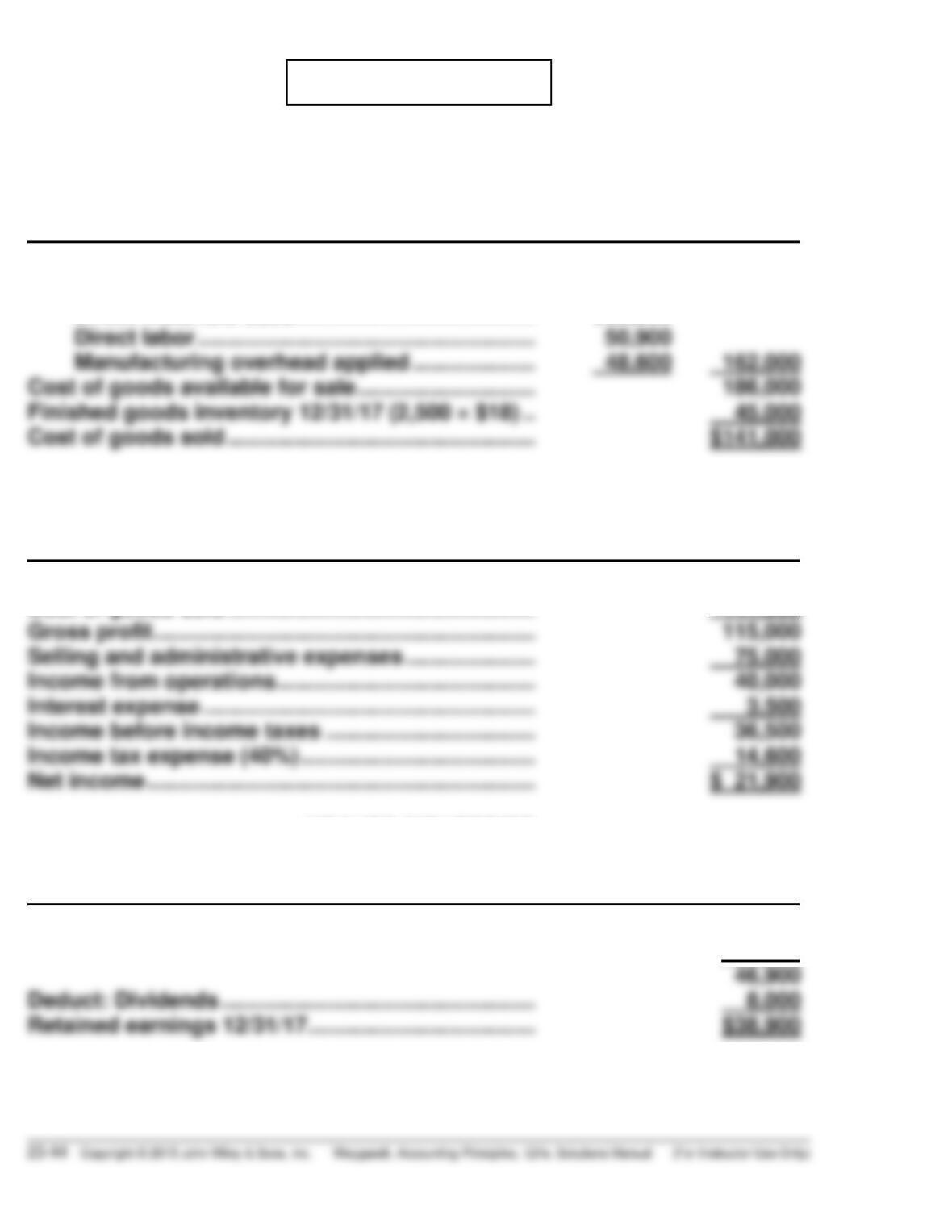

KRAUSE INDUSTRIES

Budgeted Cost of Goods Sold

For the Year Ending December 31, 2017

Finished goods inventory, 1/1/17 ……………………… $ 24,000

Cost of goods manufactured

Direct materials used ………………………………… $62,500

KRAUSE INDUSTRIES

Budgeted Income Statement

For the Year Ending December 31, 2017

Sales revenue (8,000 $32) ……………………………… $256,000

Cost of goods sold ………………………………………….. 141,000

Gross profit …………………………………………………….. 115,000

KRAUSE INDUSTRIES

Budgeted Retained Earnings Statement

For the Year Ending December 31, 2017

Retained earnings, 1/1/17 …………………………………. $25,000

Add: Net income …………………………..…………………. 21,900

PROBLEM 23-6A (Continued)

KRAUSE INDUSTRIES

Budgeted Balance Sheet

December 31, 2017

Assets

Current assets

Cash ……………………………………………………………. $ 5,880

Accounts receivable ($76,800 X 40%) ……………. 30,720

Property, plant, and equipment

Equipment ($40,000 + $9,000) ……………………….. $49,000

Liabilities and Stockholders’ Equity

Liabilities

Notes payable ($25,000 – $8,000) ………………….. $17,000

Accounts payable ($8,500* + $7,200) ……………… 15,700

Stockholders’ equity

Common stock …………………………………………….. $40,000

PROBLEM 23-6A (Continued)

Proof of budgeted cash balance December 31, 2017

Beginning cash balance…………………………………… $ 7,500

Collections

306,280

Payments

Beginning accounts payable ……………………………. 45,000

Note payment ………………………………………………….. 8,000

Equipment purchase ……………………………………….. 9,000

CD23 CURRENT DESIGNS

CURRENT DESIGNS

Production Budget

For the Year Ending December 31, 2017

Quarter 1

Quarter 2

Quarter 3

Quarter 4

Total

Expected unit sales

1,000

1,500

750

750

4,000

Add: Desired ending

finished goods units

300*

150*

150*

220**

220

Total required units

1,300

1,650

900

970

4,220

goods units

300

150

200

Required production units

1,100

1,350

750

820

4,020

CD23 (Continued)

CURRENT DESIGNS

Direct Materials Budget

For the Year Ending December 31, 2017

Quarter 1

Quarter 2

Quarter 3

Quarter 4

Total

Units to be produced

1,100

1,350

750

820

4,020

Pounds of polyethylene

powder per unit

X 54

X 54

X 54

X 54

X 54

Total pounds needed for

production

59,400

72,900

40,500

44,280

217,080

Add: Desired ending

inventory of powder

18,225*

11,070*

15,930**

15,930

required

77,625

83,025

51,570

60,210

233,010

Less: Beginning inventory

19,400***

18,225

10,125

11,070

Pounds of polyethylene

powder to be purchased

58,225

64,800

41,445

49,140

213,610

Cost per pound

X $1.50

X $1.50

X $1.50

X $1.50

X $1.50

Cost of polyethylene

powder to be purchased

$ 87,337.50

$ 97,200.00

$ 62,167.50

$ 73,710.00

$ 320,415.00

manufactured) @$170 each

Cost of required finishing

*25% of needs for next quarter

**Desired ending inventory for Quarter 4 = 25% of amount needed for first

quarter of 2018 production.

CD23 (Continued)

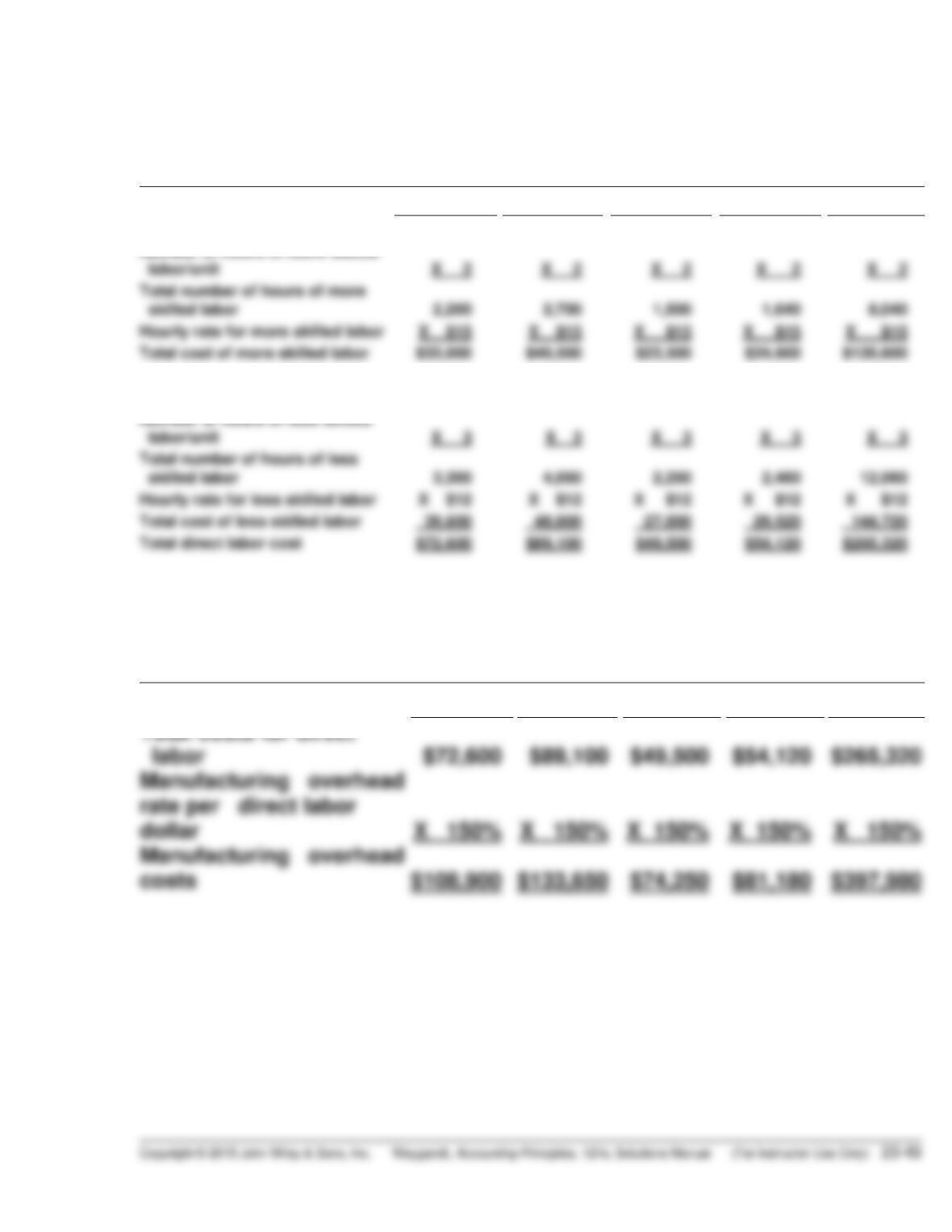

CURRENT DESIGNS

Direct Labor Budget

For the Year Ending December 31, 2017

Quarter 1

Quarter 2

Quarter 3

Quarter 4

Total

Units to be produced

1,100

1,350

750

820

4,020

Number of hours of more skilled

labor/unit

X 2

X 2

X 2

X 2

X 2

Hourly rate for more skilled labor

Total cost of more skilled labor

Total number of hours of more

Units to be produced

1,100

1,350

750

820

4,020

Number of hours of less skilled

labor/unit

X 3

X 3

X 3

X 3

X 3

Hourly rate for less skilled labor

Total cost of less skilled labor

Total direct labor cost

CURRENT DESIGNS

Manufacturing Overhead Budget

For the Year Ending December 31, 2017

Quarter 1

Quarter 2

Quarter 3

Quarter 4

Total

CD23 (Continued)

CURRENT DESIGNS

Selling and Administrative Expense Budget

For the Year Ending December 31, 2017

Quarter 1

Quarter 2

Quarter 3

Quarter 4

Total

Expected unit sales

1,000

1,500

750

750

4,000

Variable selling and

administrative

expenses at $45 per

BYP 23-1 DECISION-MAKING ACROSS THE ORGANIZATION

(a) The budget at Palmer Corporation is an imposed “top–down” budget

which fails to consider both the need for realistic data and the human

interaction essential to an effective budgeting/control process. The

president has not given any basis for his goals, so one cannot know

whether they are realistic for the company. True participation of company

employees in preparation of the budget is minimal and limited to mechani–

cal gathering and manipulation of data. This suggests there will be little

enthusiasm for implementing the budget.

The budget process is the merging of the requirements of all facets of

the company on a basis of sound judgment and equity. Specific instances

of poor procedures other than the approach and goals include the

following:

1. The sales by product line should be based upon an accurate sales

forecast of potential market. Therefore, the sales by product line

should have been developed first to derive the sales target rather

than the reverse.

(b) Palmer Corporation should consider the adoption of a “bottom to top”

(participative) budget process. This means that the people responsible

for performance under the budget would participate in the decisions

by which the budget is established. In addition, this approach requires

BYP 23–1 (Continued)

The sales forecast should be developed considering internal sales

forecasts as well as external factors. Costs within departments should

be divided into fixed and variable, discretionary and nondiscretionary.

(c) The functional areas should not necessarily be expected to cut costs

when sales volume falls below budget. The time frame of the budget

(one year) is short enough so that many costs are relatively fixed in

amount. For those costs which are fixed, there is little hope for a

reduction as a consequence of short–run changes in volume. However, the

functional areas should be expected to cut costs should sales volume

fall below target when:

1. Control is exercised over the costs within their function.

BYP 23-2 MANAGERIAL ANALYSIS

(a) Direct materials Either lower quality materials resulting in an inferior

product and possible lost sales, or fewer units

produced resulting in lost sales.

Direct labor Reduced production resulting in lost sales, or

reduction in quality of product resulting in lost sales.

Machine repairs Less efficient operations, or lost production and

sales.

Sales salaries Lost sales.

Office salaries Less effective administrative functions.

Factory salaries Lost production due to inefficiency, and therefore

lost sales.

BYP 23-3 REAL-WORLD FOCUS

(a) According to Mr. LaFaive, zero-based budgeting requires that the

existence of a government program or programs be justified in each

fiscal year, as opposed to simply basing budgeting decisions on a

previous year’s funding level. Zero-based budgeting is often encouraged

by fiscal watchdog groups as a way to ensure against unnecessary

spending.

(b) In addition to saving money and improving services, zero-based

budgeting may:

• Increase restraint in developing budgets;

• Reduce the entitlement mentality with respect to cost increases; and

• Make budget discussions more meaningful during review sessions.

(c) On the cost side of the equation, zero-based budgeting:

• May increase the time and expense of preparing a budget;

• May be too radical a solution for the task at hand. You don’t need a

sledgehammer to pound in a nail;

• Can make matters worse if not done in the right way. A substantial

commitment must be made by all involved to ensure that this

doesn’t happen.

(d) In Oklahoma, which has recently adopted zero-based budgeting, officials

are applying the method to two departments and several agencies each

year. Once those reviews are complete, the same departments and

agencies will not see another zero-based review for eight years.

BYP 23-4 COMMUNICATION ACTIVITY

Date 2017

Mrs. Megan Parcells, CEO

Life Protection Products

Dear Mrs. Parcells:

Allow me to congratulate you on the success of your new venture! The

growth in sales you have experienced is phenomenal. You have managed the

business side of the venture very well also. At the same time, I understand

your concern about cash flow. You are selling these kits as fast as you can

make them, and yet you are running out of cash.

BYP 23–4 (Continued)

However, even if you raised prices, you will find that you need additional

cash as long as the business continues to expand. It certainly does not

mean that you and Sue are doing anything wrong. It just means that you

will be investing additional funds as long as you continue to grow.

In my opinion, the best way to make sure these kits are available to as

many families as possible is for you and Sue to have a consultant evaluate

BYP 23-5 ETHICS CASE

(a) At best, if you disclose the errors in your calculations, you will be

embarrassed. At worst, you will be dismissed without a recommendation

for another job.

BYP 23-6 ALL ABOUT YOU

Personal Budget

Typical Month

Income:

Wages earned ………………………………………….. $2,500

Interest income ………………………………………… 50

Expenses:

Rent ………………………………………………………………….. 500

Utilities

Electricity ………………………………………………… 85

Telephone and Internet …………………………….. 125

Food:

BYP 23-7 CONSIDERING YOUR COSTS AND BENEFITS

We are concerned that the personal budgets presented on websites and in

financial planning textbooks often list student loans among the sources of

income. This type of thinking can lead to an overreliance on debt during