Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Exercise 23-13 (30 minutes)

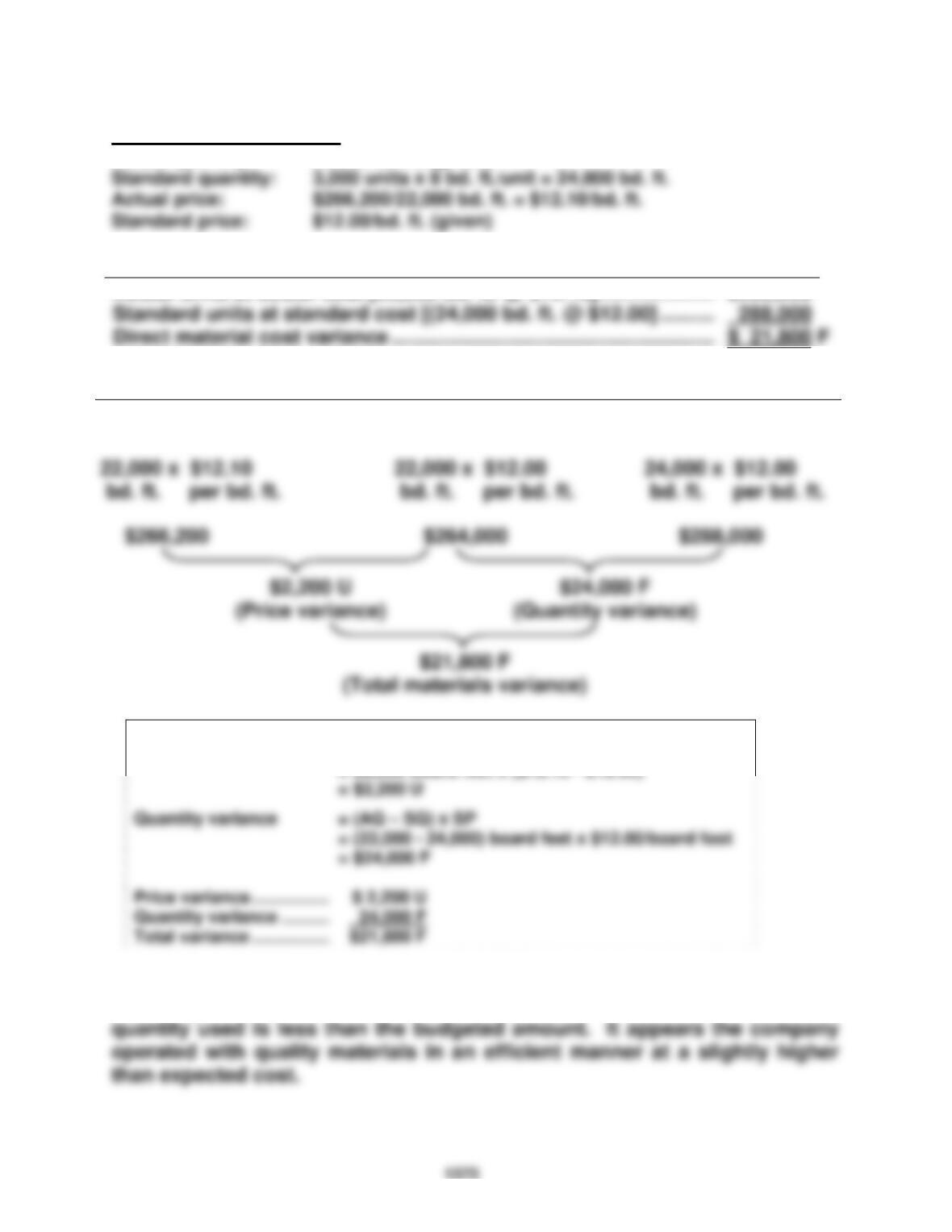

1. Preliminary computations

Actual quantity: 22,000 bd. ft. (given)

Direct material cost variances

Actual units at actual cost [22,000 bd. ft. @ $12.10] ................................

$266,200

Price and quantity variances

Actual Cost

AQ x AP

AQ x SP

Standard Cost

SQ x SP

Alternate solution format

Price variance

= AQ x (AP – SP)

= 22,000 board feet x ($12.10 - $12.00)

2. The unfavorable price variance means the actual price paid is more than

the budgeted price. The favorable quantity variance means the actual

1374

Exercise 23-14A (25 minutes)

1.

Work in Process Inventory ......................................................

288,000

2.

Direct Materials Quantity Variance ................................

24,000

3. The $24,000 materials quantity variance should be investigated because of

1375

Exercise 23-15 (25 minutes)

Part 1

Direct materials price variance:

Actual cost of direct materials used (16,000 x $4.05) ...............................

$ 64,800

Part 2

Direct labor rate variance:

Actual hours x Actual rate per hour (5,545 x $19.00***) ...........................

$105,355

Actual hours x Standard rate per hour (5,545 x $20.00) ...........................

110,900

Direct labor rate variance ................................................................

$ 5,545

F

1376

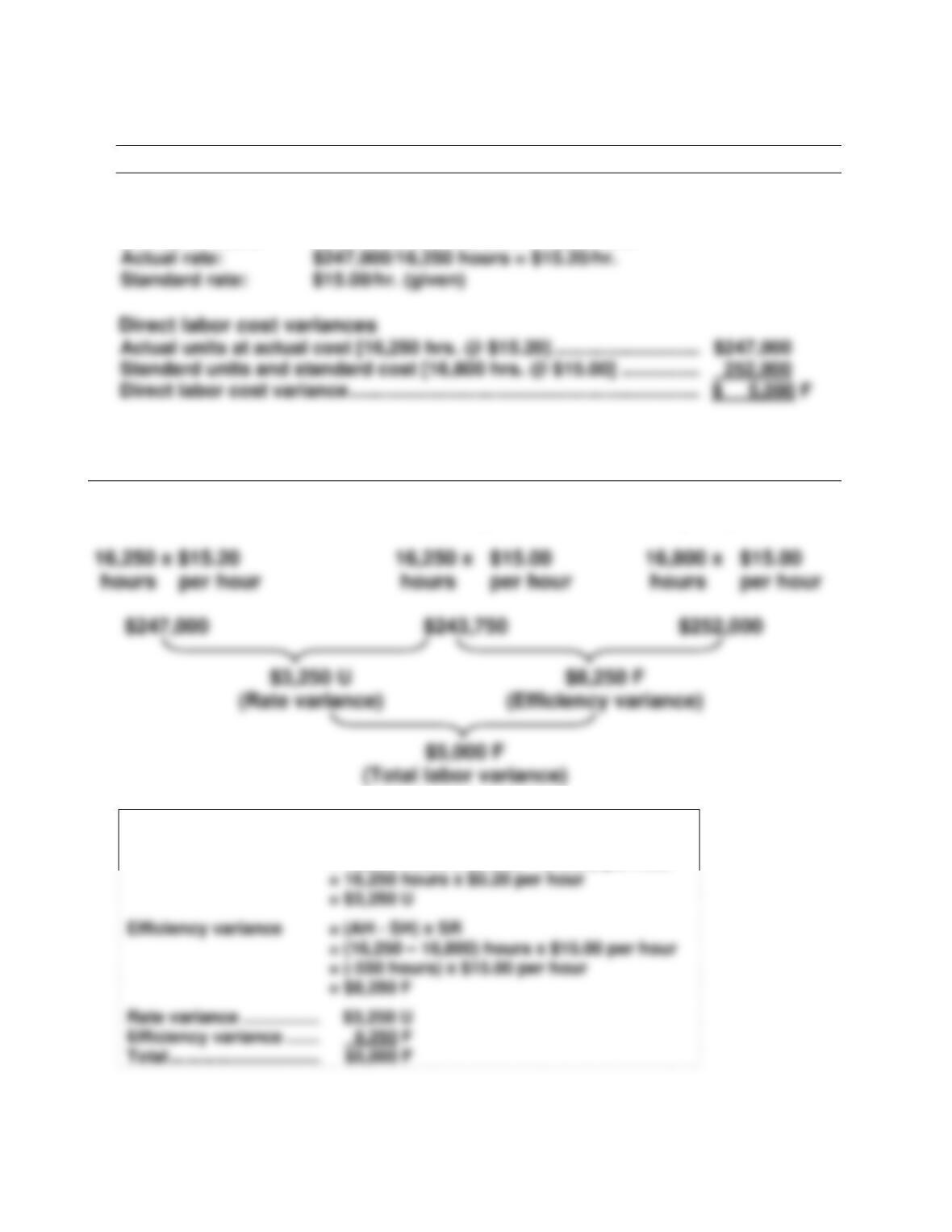

Exercise 23-16 (30 minutes)

1.

October variances

Preliminary computations

Actual hours: 16,250 hours (given)

Standard hours: 5,600 units x 3 hrs./unit = 16,800 hrs.

Rate and efficiency variances

Actual Cost

AH x AR

AH x SR

Standard Cost

SH x SR

Alternate solution format

Rate variance

= AH x (AR – SR)

= 16,250 hours x ($15.20 - $15.00) per hour

1377

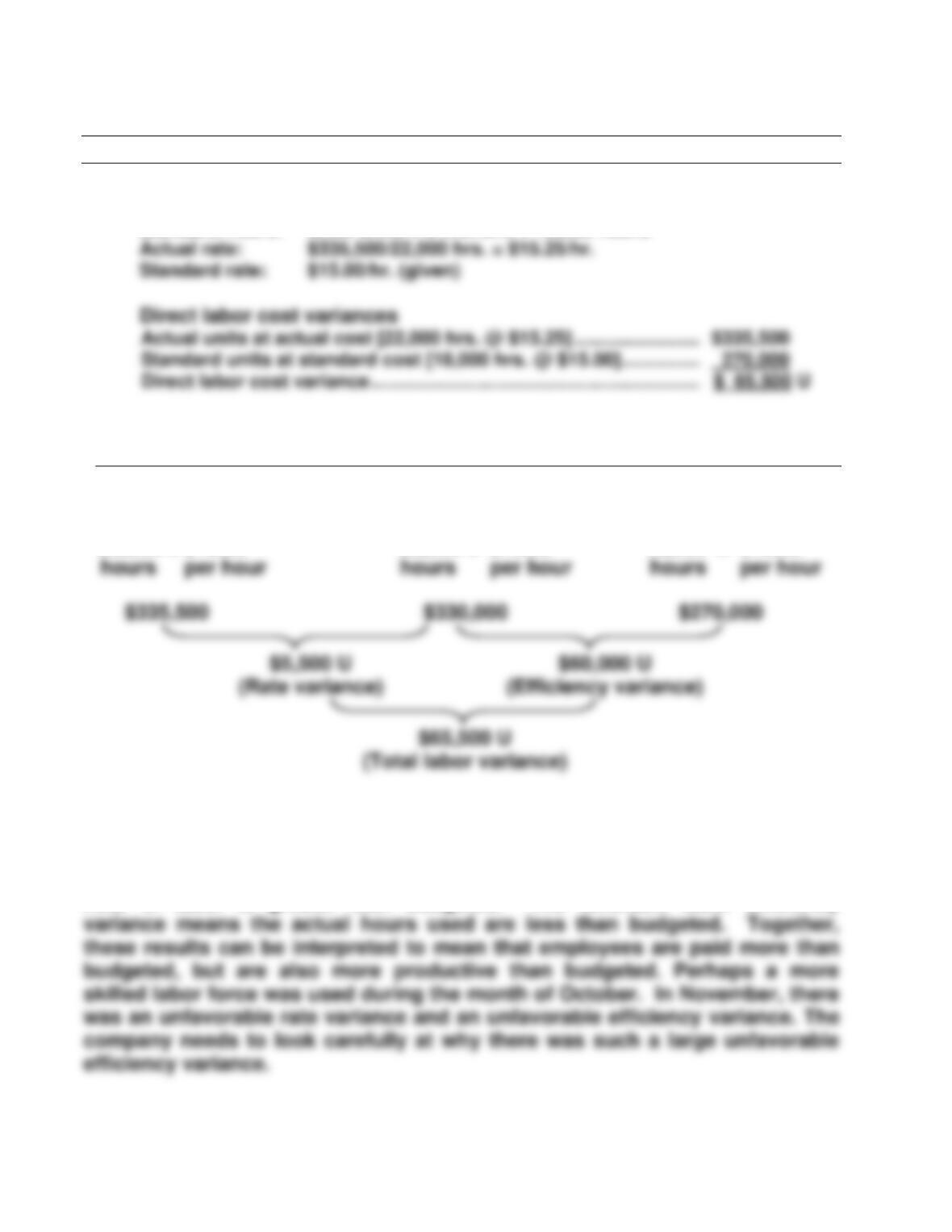

Exercise 23-16 (Concluded)

November variances

Preliminary computations

Actual hours: 22,000 hours (given)

Standard hours: 6,000 units x 3 hrs./unit = 18,000 hours

Rate and efficiency variances

Actual Cost

AH x AR

AH x SR

Standard Cost

SH x SR

22,000 x $15.25

22,000 x $15.00

18,000 x $15.00

2.

The unfavorable labor rate variance in October means the actual rate for an

hour of labor is greater than budgeted. The favorable labor efficiency

Exercise 23-17 (20 minutes)

1. Predetermined overhead rate computations

Expected volume ......................................................................

75%

2. Variable overhead cost variance

Variable overhead cost incurred [given] ................................

$1,375,000

Variable overhead cost applied [350,000 hrs. @ $4.00] ...........................

1,400,000

1379

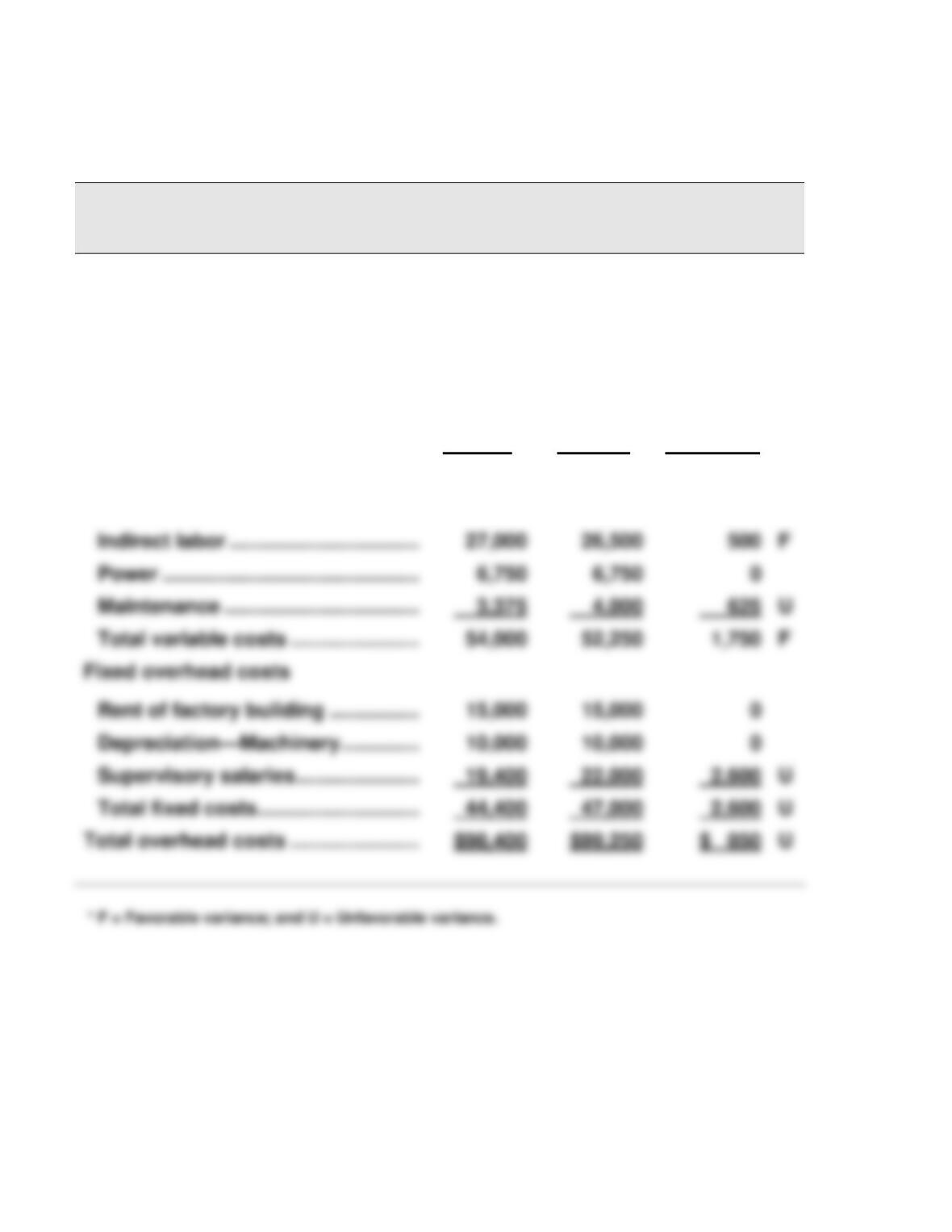

Exercise 23-18A (20 minutes)

1.

Variable overhead spending and efficiency variances

Actual Overhead

AH x AVR

AH x SVR

Applied Overhead

SH x SVR

(Given)

340,000 x $4.00

350,000 x $4.00

Interpretation:

The $15,000 unfavorable spending variance means the actual cost of variable

overhead is more than budgeted. This unfavorable variance can occur

1380

Exercise 23-18A (continued)

2.

Fixed overhead spending and volume variances

Actual Overhead

Budgeted Overhead

Applied Overhead

(Given)

(Given)

350,000 x $1.60

hours per hour

Interpretation

The $28,600 unfavorable spending variance means actual cost of fixed

overhead is more than budgeted.

3. The controllable variance is computed as:

Variable overhead spending variance ...................................

$15,000 U

Variable overhead efficiency variance ...................................

40,000 F

1381

Exercise 23-19 (20 minutes)

Information given

Planned units to be produced = 80% x 50,000 capacity = 40,000 units

1. Total overhead planned at 80% level (25,000 direct labor hours)

Budgeted

Cost

Ovhd.

Rate*

Fixed overhead.................................

$ 50,000

$ 2.00

2. Total overhead variance

Total actual overhead (given) ................................................................

$305,000

1382

Exercise 23-20 (30 minutes)

1. The overhead volume variance is computed as:

2. Overhead controllable variance*

Total actual overhead (given)

$305,000

Budgeted overhead

1383

EX

Exercise 23-21 (25 minutes)

Preliminary calculations:

Variable overhead rate per DL hour = $48,000/24,000 = $2 per hour

Part 1

Total actual overhead (given) …………………………

$99,250

Budgeted overhead

Part 2

Total budgeted fixed overhead (given) ………………

$44,400

1384

Exercise 23-21 (continued)

Part 3

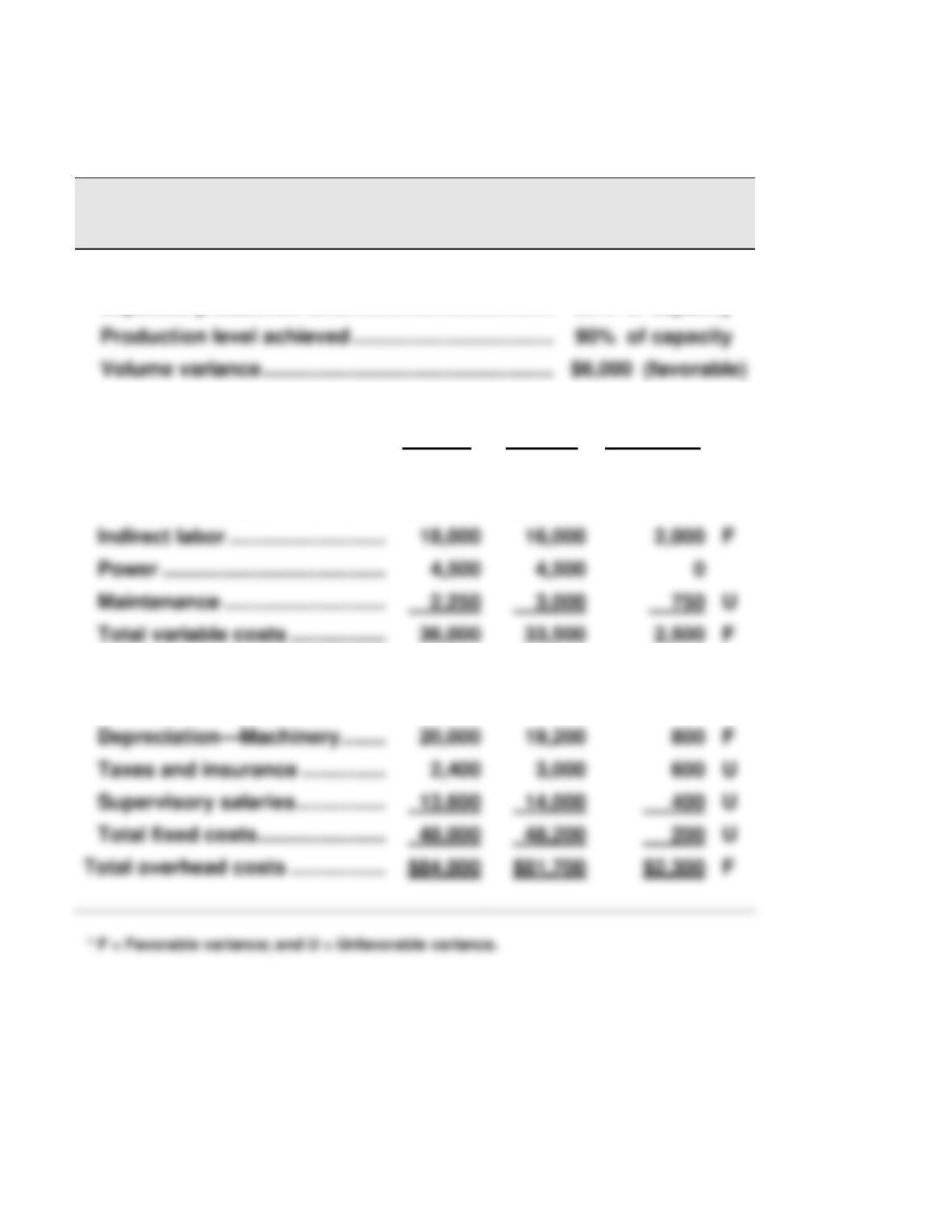

JAMES CORP.

Overhead Variance Report

For Month Ended May 31

Volume Variance

Expected production level ....................................................

80% of capacity

Production level achieved ....................................................

90% of capacity

Volume variance ................................................................

$5,550 (favorable)

Flexible

Actual

Controllable Variance

Budget

Results

Variances*

Variable overhead costs

Indirect materials ................................

$16,875

$15,000

$1,875

F

1385

Exercise 23-22 (25 minutes)

Preliminary calculations:

Variable overhead rate per DL hour = $32,000/32,000 = $1 per hour

Part 1

Total actual overhead (given) …………………………

$81,700

Budgeted overhead

Part 2

1386

Exercise 23-22 (continued)

Part 3

BLAZE CORP.

Overhead Variance Report

For Month Ended March 31

Volume Variance

Expected production level ..........................................

80% of capacity

Flexible

Actual

Controllable Variance

Budget

Results

Variances*

Variable overhead costs

Indirect materials ...........................

$11,250

$10,000

$1,250

F

Fixed overhead costs

Rent of factory building ................

12,000

12,000

0

1387

Exercise 23-23 (25 minutes)

1. Sales price and sales volume variances

Sales Actual Sales

Flexible Budget

Fixed Budget

Units 350

350

365

2. Interpretation

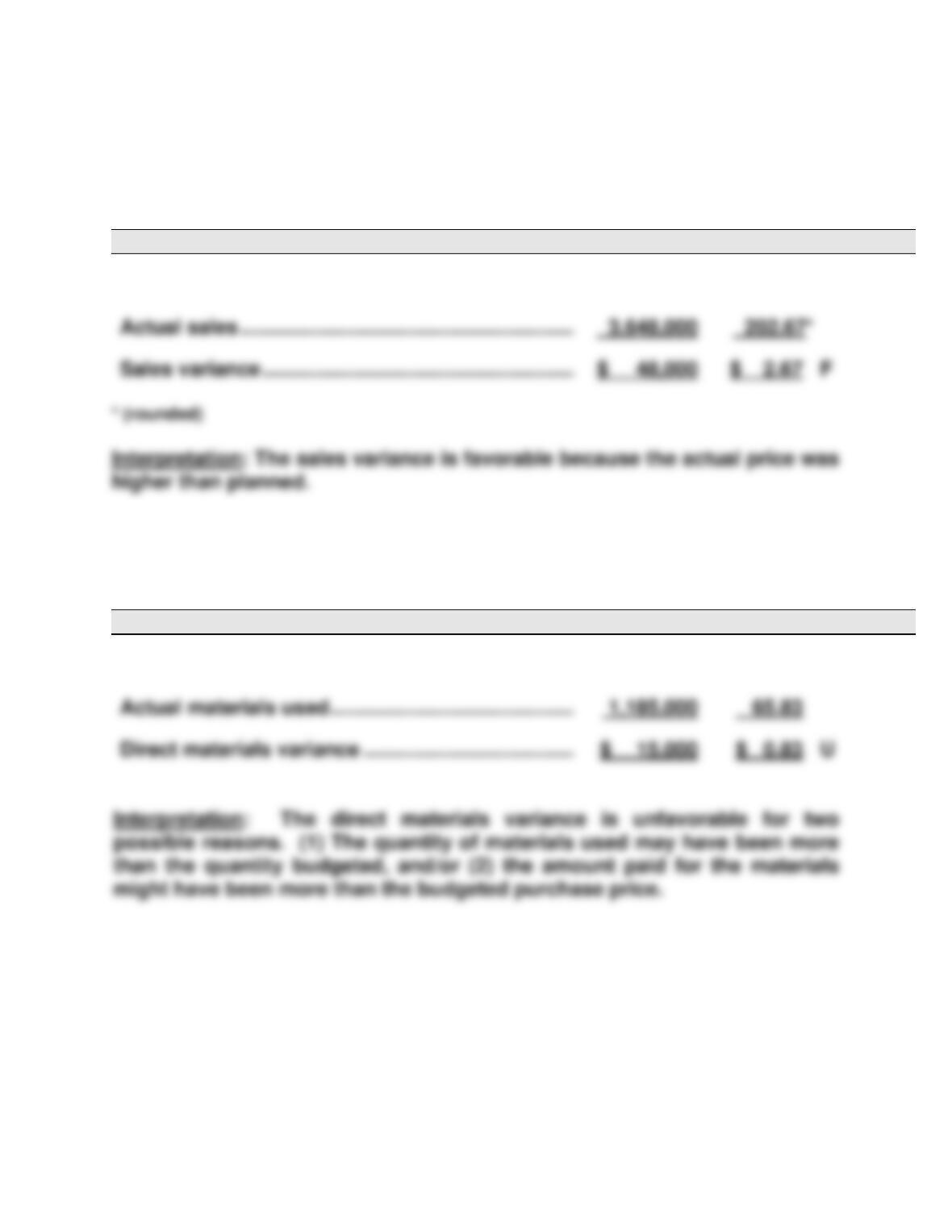

The $35,000 favorable sales price variance implies it sold computers for a

1388

PROBLEM SET A

Problem 23-1A (60 minutes)

Part 1

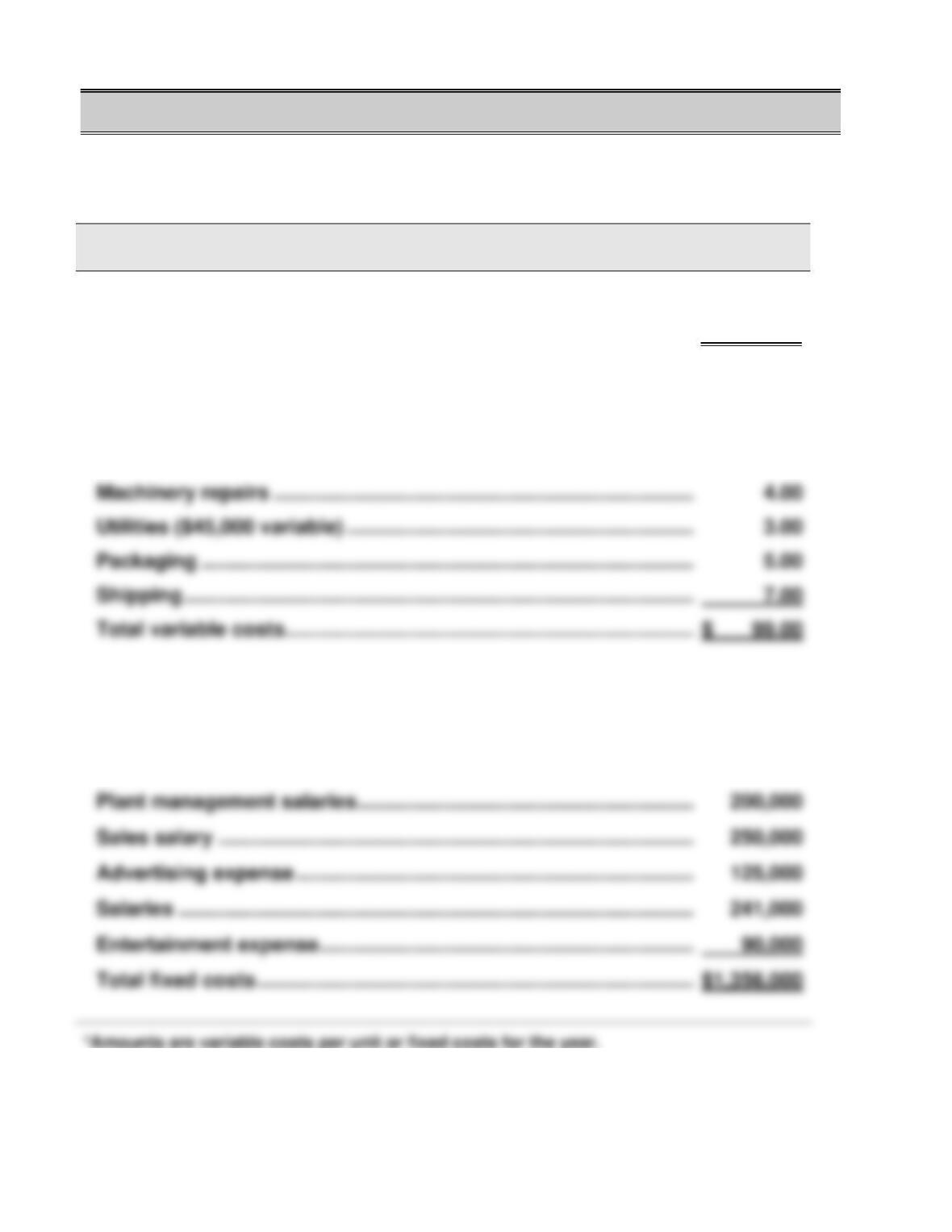

Variable or Fixed Classification

Amount*

Variable sales (total divided by 15,000 units)

Sales ..................................................................................................

$ 200.00

Variable costs (total divided by 15,000 units)

Direct materials ................................................................................

$ 65.00

Direct labor .......................................................................................

15.00

Fixed costs

Depreciation—Plant equipment ......................................................

$ 300,000

Utilities ($195,000 - $45,000 variable) .............................................

150,000

*Amounts are variable costs per unit or fixed costs for the year.

1389

Problem 23-1A (Continued)

Part 2

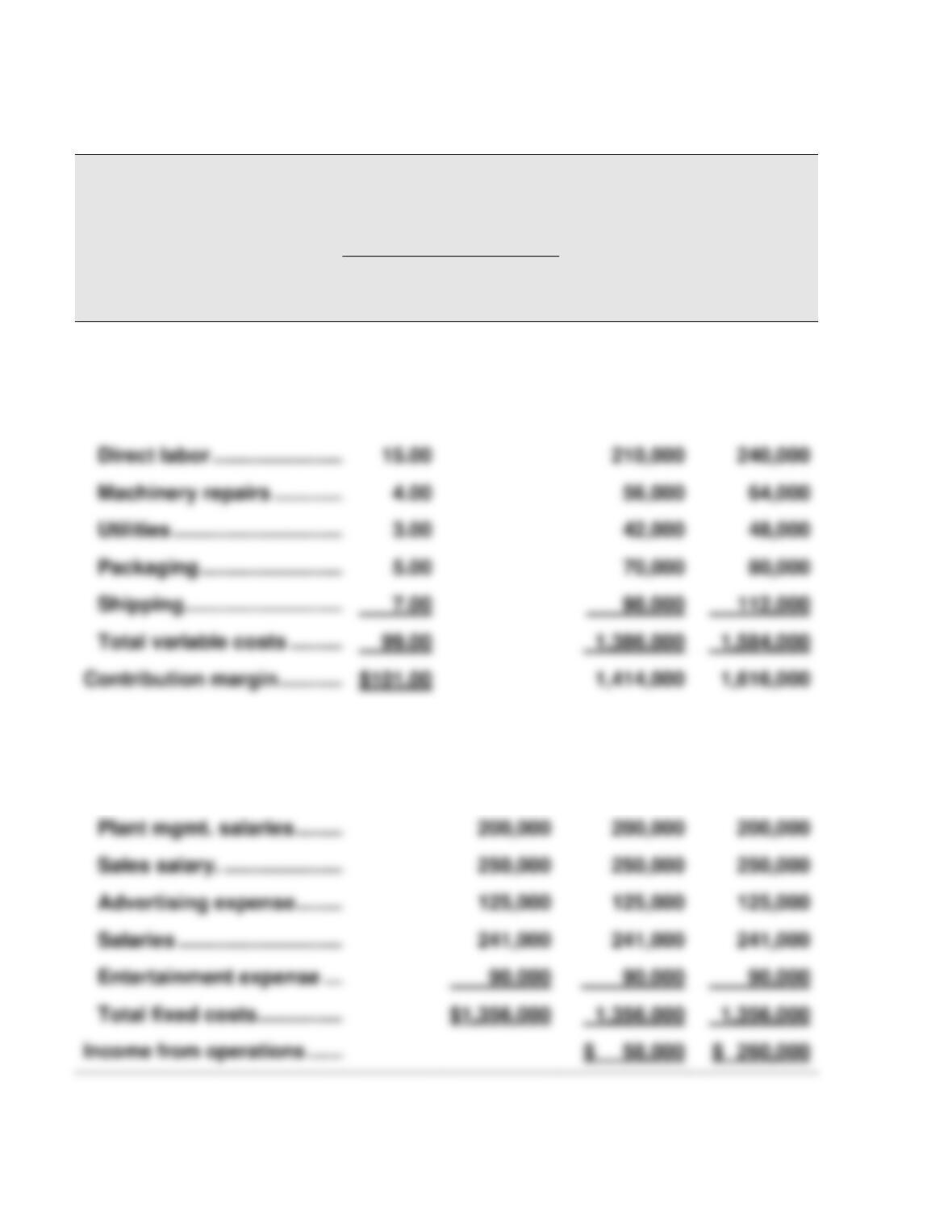

PHOENIX COMPANY

Flexible Budgets

For Year Ended December 31, 2017

Flexible Budget

Flexible

Flexible

Variable

Amount

per Unit

Total

Fixed

Cost

Budget for

Unit Sales

of 14,000

Budget for

Unit Sales

of 16,000

Sales .....................................

$200.00

$2,800,000

$3,200,000

Variable costs

Direct materials .................

65.00

910,000

1,040,000

Fixed costs

Depreciation—Plant Equip ....

$ 300,000

300,000

300,000

Utilities ...............................

150,000

150,000

150,000

1390

Problem 23-1A (Continued)

Part 3

Operating income increase for a 15,000 to 18,000 unit sales increase

Possible sales (units) ...............................................................

18,000

Contribution margin per unit ...................................................

x $101

*Alternate solution format

Unit increase ...........................................................................................

3,000

Units

Part 4

Operating income (loss) at 12,000 units

Possible sales (units) ...............................................................

12,000

1391

Problem 23-2A (45 minutes)

Part 1

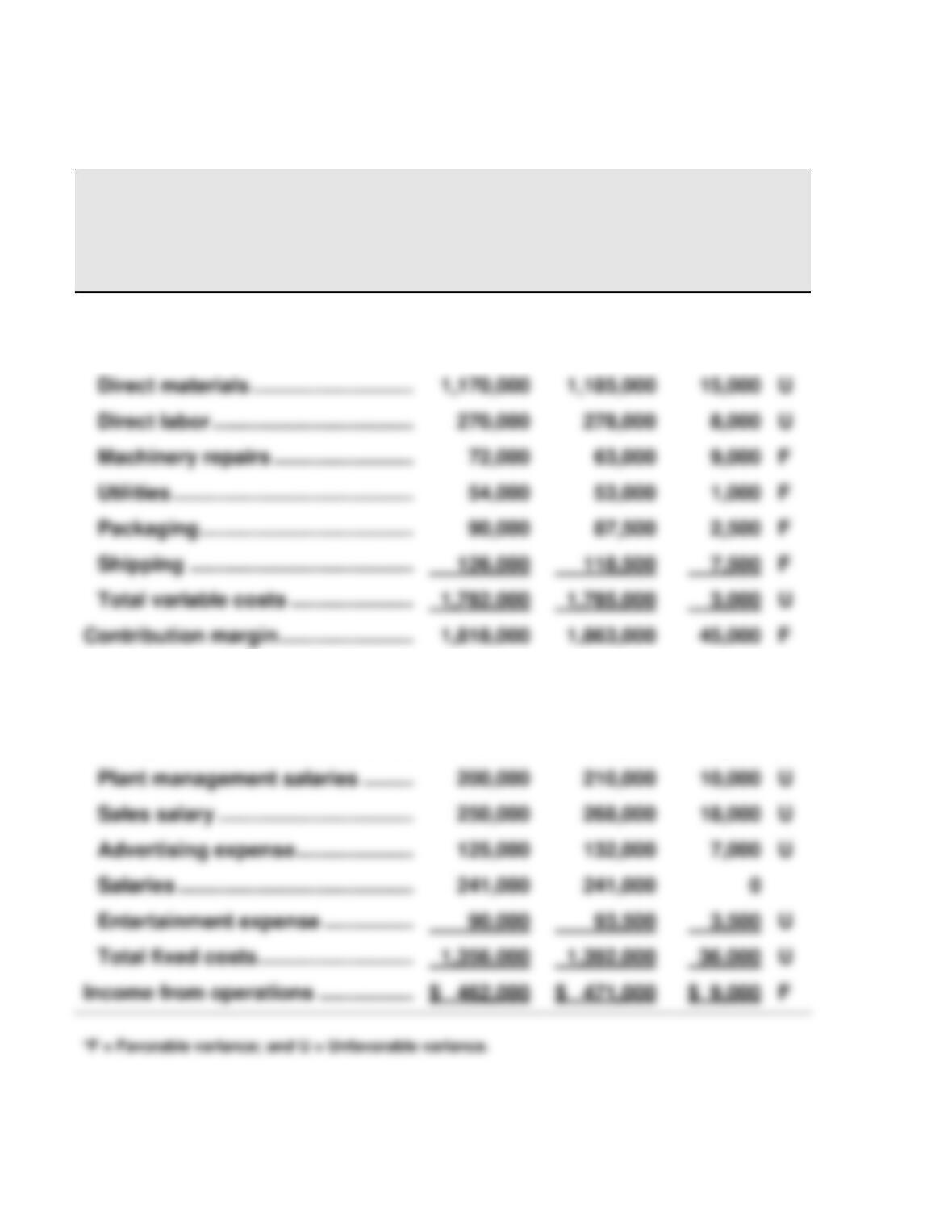

PHOENIX COMPANY

Flexible Budget Performance Report

For Year Ended December 31, 2017

Flexible

Actual

Budget

Results

Variances*

Sales (18,000 units) ..........................

$3,600,000

$3,648,000

$48,000

F

Variable costs

Fixed costs

Depreciation—Plant equip. ...........

300,000

300,000

0

Utilities ............................................

150,000

147,500

2,500

F

1392

Problem 23-2A (Continued)

Part 2

(a) Analysis of sales variance

(b)

Total

Per unit

Budgeted sales ..............................................................

$3,600,000

$200.00

(c) Analysis of direct materials variance

Total

Per unit

Budgeted materials........................................................

$1,170,000

$ 65.00