40 Minutes, Strong PROBLEM 23.4A

FORMER CORPORATION

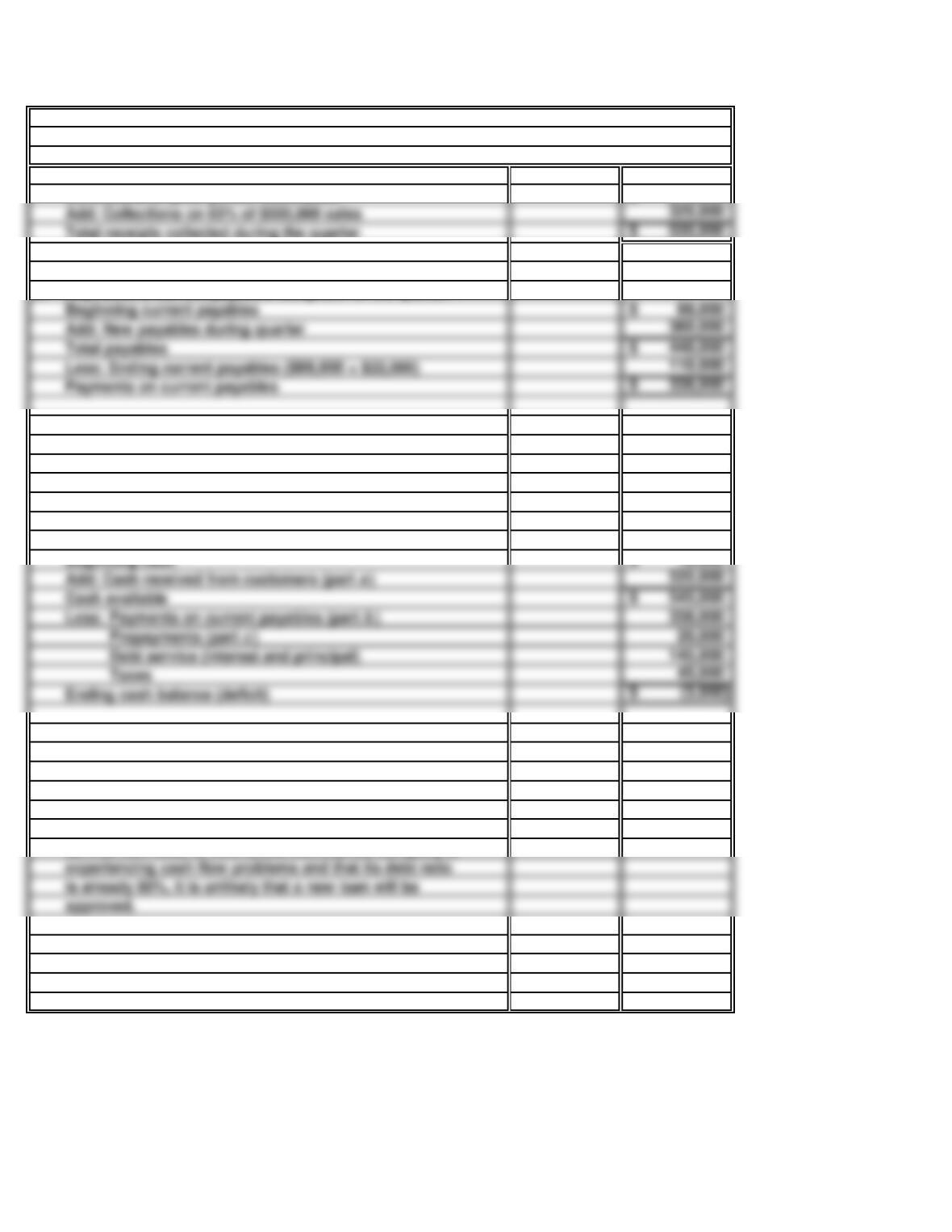

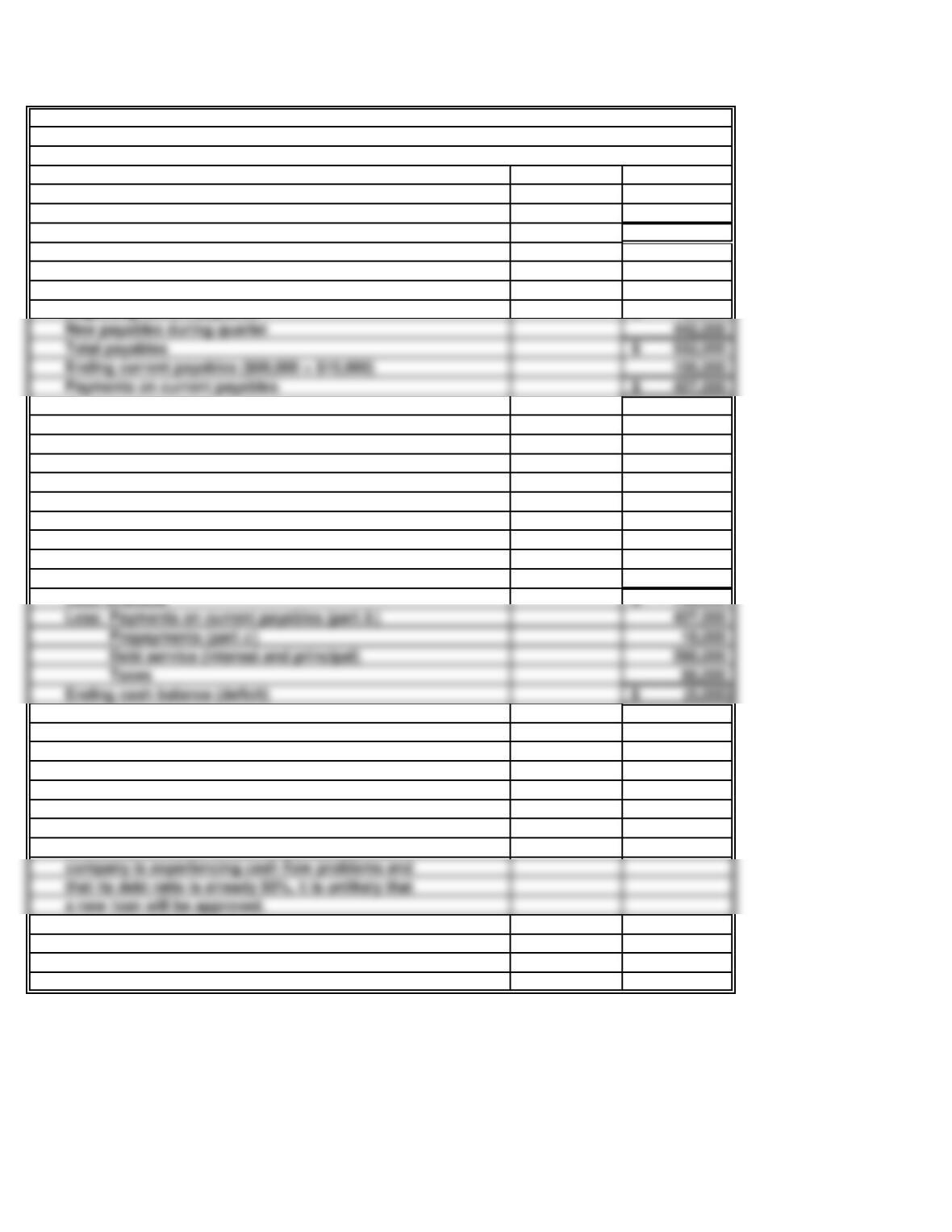

a. Budgeted cash receipts for the quarter:

Collections on prior period receivables

210,000$

Total receipts collected during the quarter 535,000$

88,000$

Add: New payables during quarter 360,000

b. Payments of current payables budgeted for the quarter:

Add: Cash received from customers (part a)535,000

Ending cash balance (deficit) (3,000)$

c. If beginning prepayments equal the ending prepayments,

the amount expired during the period equals the

prepayments made during the period, or $20,000.

d. Cash budget:

10,000$

e. Given a minimum required cash balance of $10,000, the

company must attempt to obtain a loan of $13,000.

f.

A bank will look for evidence that Former has the ability to

service new debt. In view of the fact that the company is

Add: Collections on 65% of $500,000 sales 325,000

30 Minutes, Strong PROBLEM 23.5A

RIZZO’S

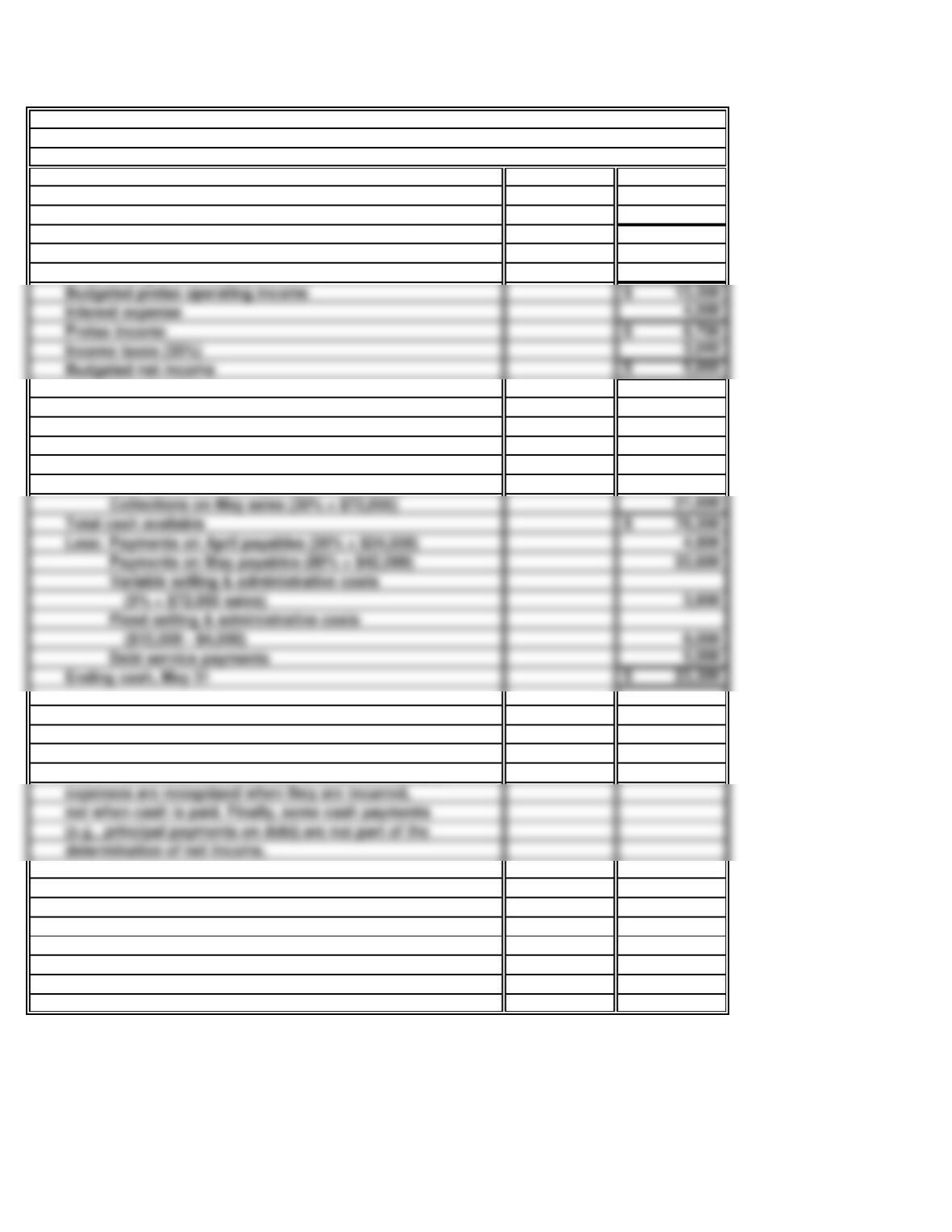

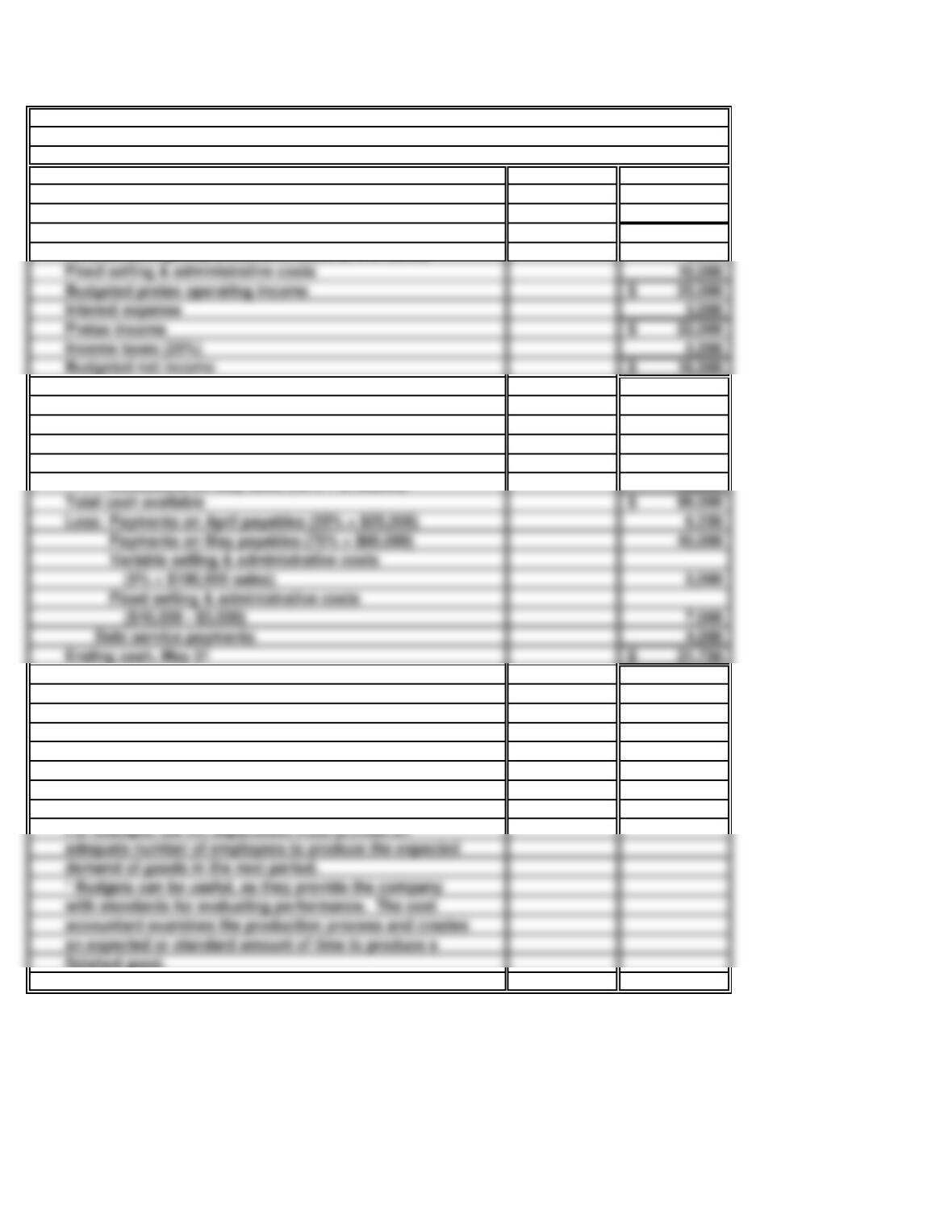

a. Budgeted income statement:

Budgeted sales 72,000$

Cost of goods sold (60% of sales) 43,200

Gross profit (40% of sales) 28,800$

Variable selling & administrative costs (5% of sales) 3,600

Fixed selling & administrative costs 12,000

b. Cash budget:

Beginning cash, May 1 25,000$

Add: Collections on March sales (10% × $65,000) 6,500

Collections on April sales (60% × $42,000) 25,200

Ending cash, May 31 23,300$

c. The company’s cash flow differs from its income

because, in accrual accounting, revenue is recognized

when it is earned, not when cash is received. Further,

Interest expense 4,500

Income taxes (35%) 3,045

Budgeted net income 5,655$

60 Minutes, Strong PROBLEM 23.6A

MARLEY WHOLESALE

a. MARLEY WHOLESALE

Cash Budget

For Third Quarter of Current Year

July August September

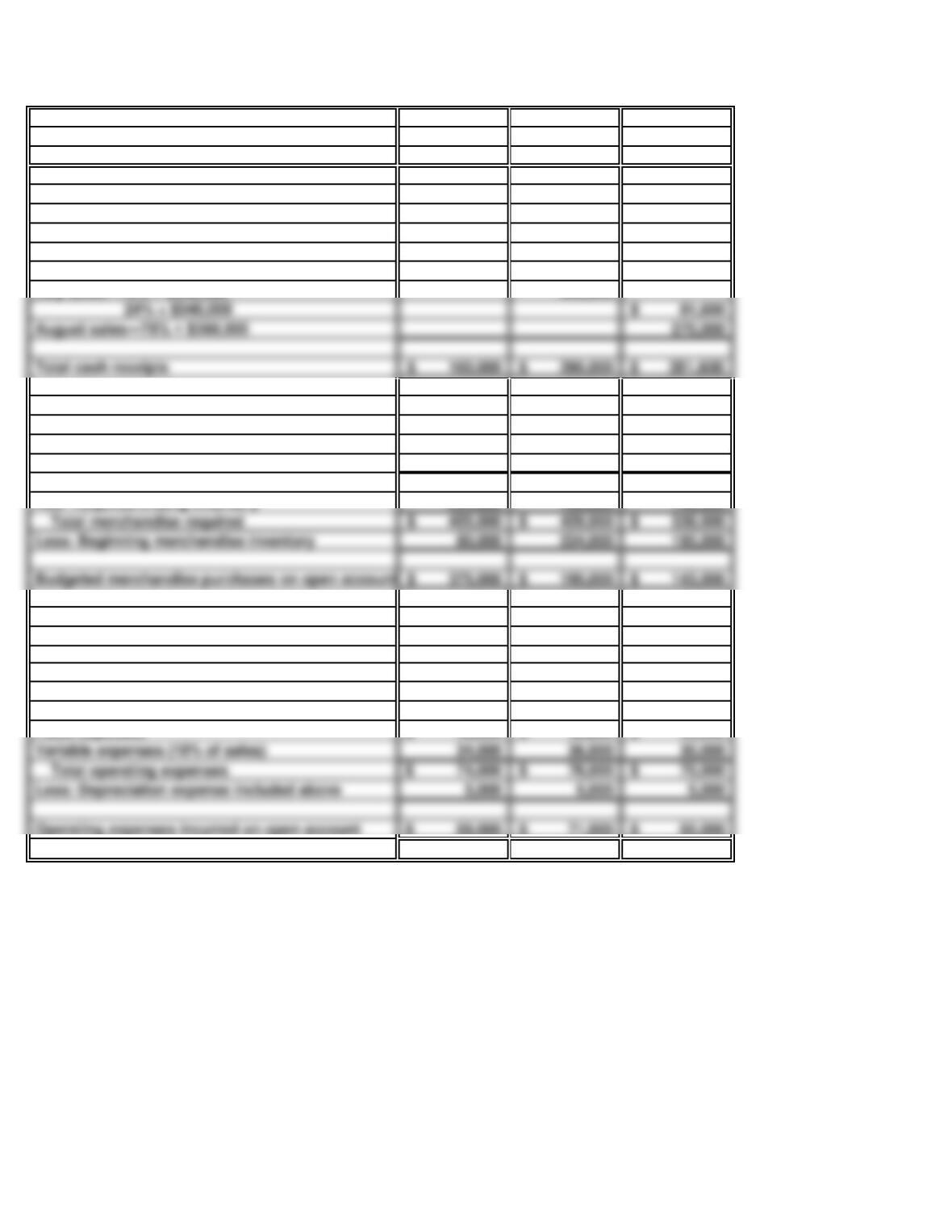

Cash balance at beginning of month 20,000$ 168,000$ 53,400$

Receipts:

Bank loan 194,000

Collections on receivables (Schedule 1) 120,000 280,000 345,000

Supporting Schedules

Schedule 1—Estimated Cash Collections

on Receivables

Receivables outstanding at June 30 120,000$ 40,000$

July sales—80% × $300,000 240,000

July sales—19% × $300,000 57,000$

August sales—80% × $360,000 288,000

Total cash receipts 120,000$ 280,000$ 345,000$

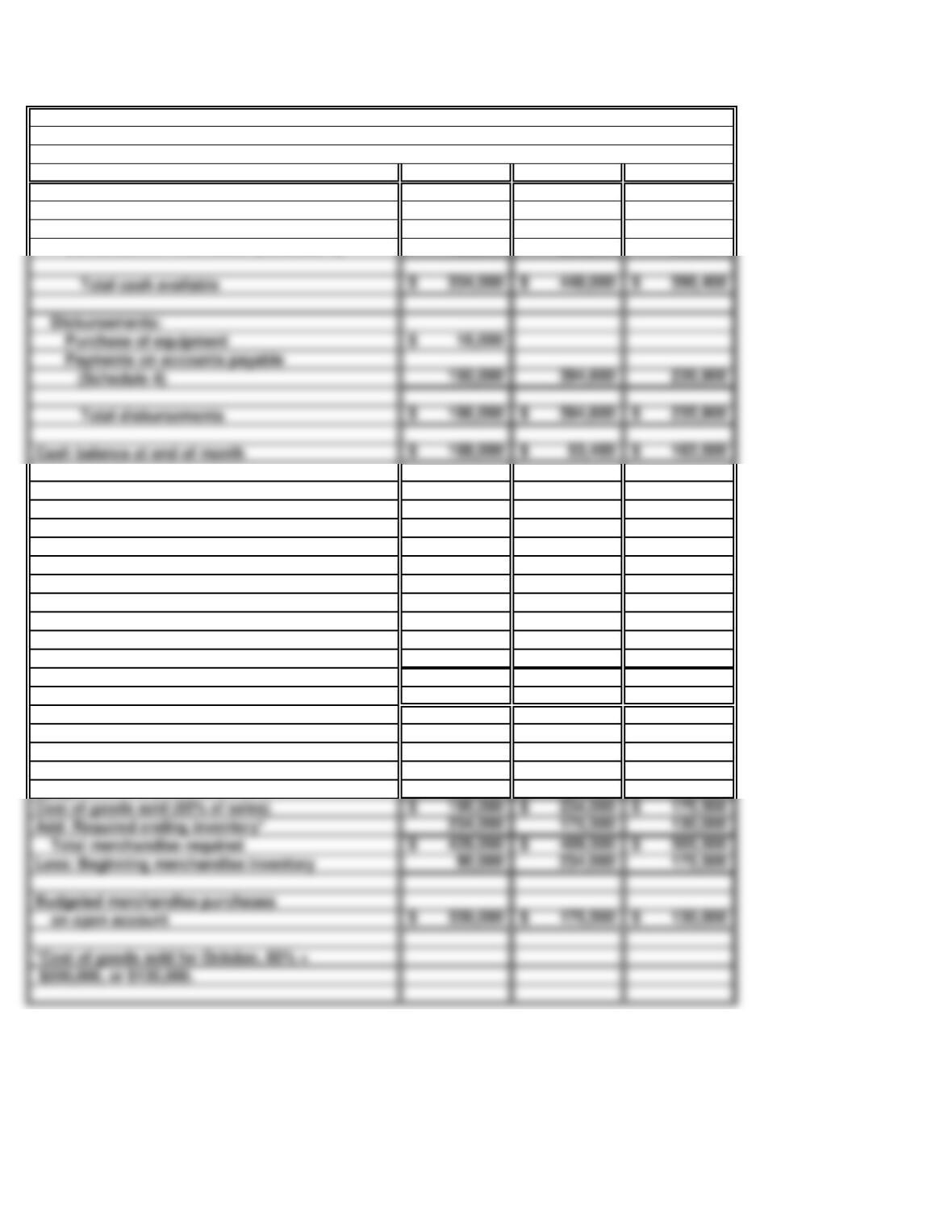

Schedule 2—Estimated Merchandise Purchases

Sales 300,000$ 360,000$ 270,000$

Cost of goods sold (65% of sales) 195,000$ 234,000$ 175,500$

Add: Required ending inventory* 234,000 175,500 130,000

Less: Beginning merchandise inventory 90,000 234,000 175,500

$200,000, or $130,000.

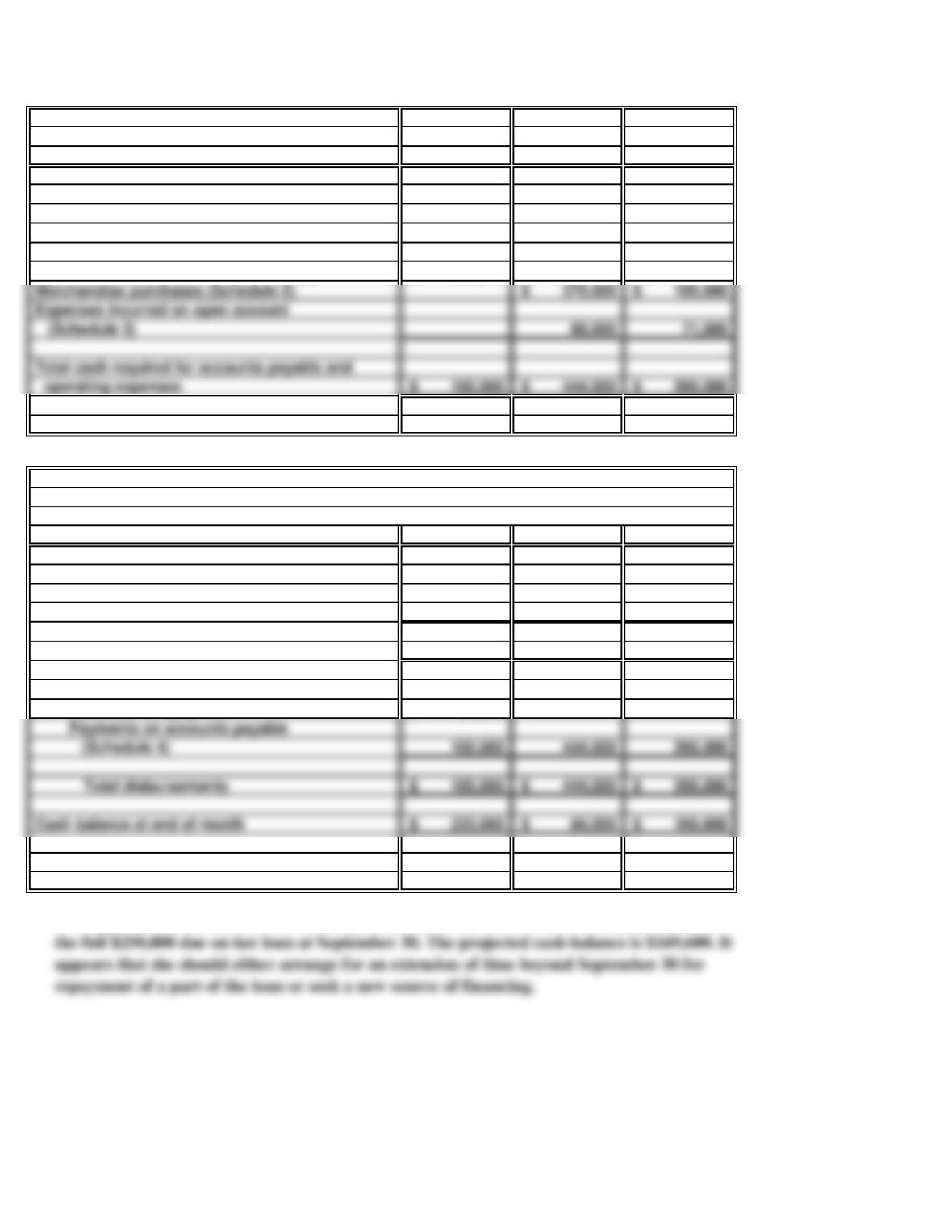

Disbursements:

Purchase of equipment 16,000$

Cash balance at end of month 168,000$ 53,400$ 162,500$

PROBLEM 23.6A

MARLEY WHOLESALE (concluded)

July August September

Schedule 3—Estimated Cash Payments

for Operating Expenses

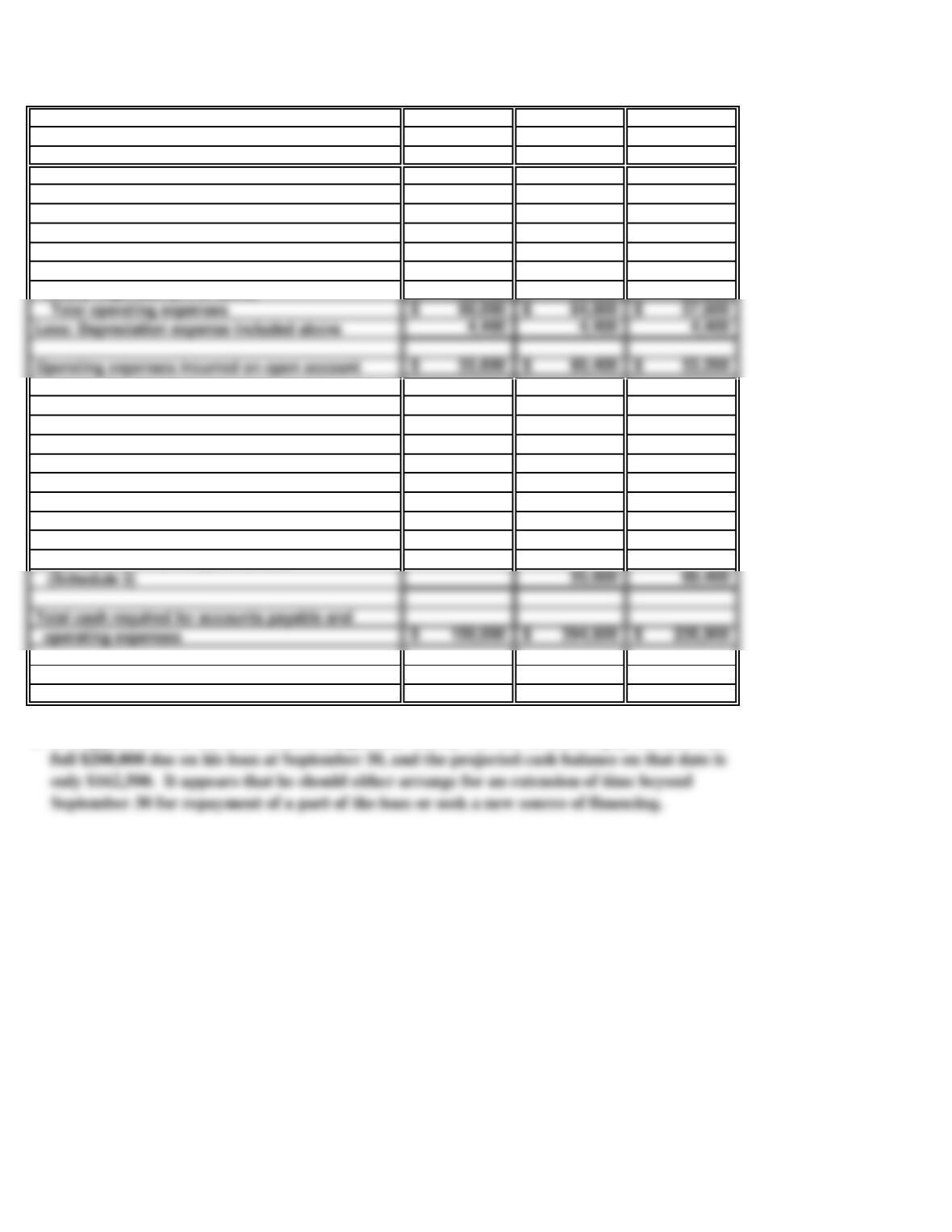

Fixed expenses

36,000$ 36,000$ 36,000$

Variable expenses (8% of sales) 24,000 28,800 21,600

Schedule 4—Estimated Cash Payments

on Accounts Payable (Including

Operating Expenses)

Accounts payable balance on June 30

(includes accrued operating expenses)

150,000$

Merchandise purchases (Schedule 2)

339,000$ 175,500$

Expenses incurred on open account

operating expenses 150,000$ 394,600$ 235,900$

b.

It is apparent from the three-month budget that Marley will not be able to pay the bank the

Less: Depreciation expense included above 4,400 4,400 4,400

50 Minutes, Medium PROBLEM 23.7A

SNELLS

a. SNELLS

Comparison of Budgeted and Actual Revenue and Expenses

For the Year Ended December 31

Flexible Over (or

Budget Actual Under) Budget

Net sales 10,500,000$ 10,500,000$ 0$

Cost of goods sold 6,300,000 6,180,000 (120,000)

Gross profit on sales 4,200,000$ 4,320,000$ 120,000$

Operating expenses:

b.

Comment on performance:

Operating income was better than budgeted by $168,000. This result may be attributed to

Total operating expenses 2,919,000$ 2,871,000$ (48,000)$

Operating income 1,281,000$ 1,449,000$ 168,000$

45 Minutes, Medium PROBLEM 23.8A

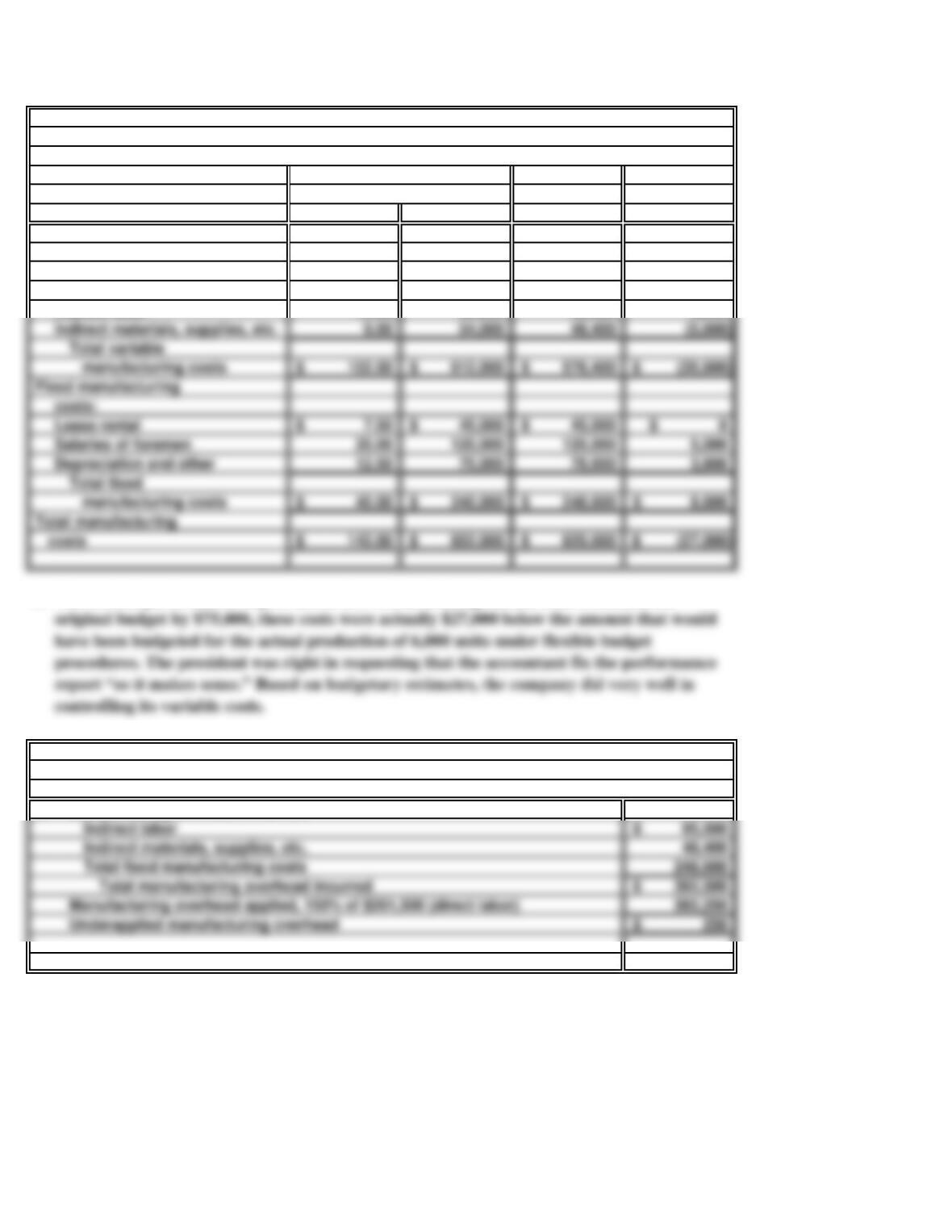

BRAEMAR SADDLERY

a. BRAEMAR SADDLERY

Performance Report for Custom Saddle Production Dept.

For the Year Ended December 31

Budgeted Costs Actual Over

for 6,000 Units Costs (or Under)

Per Unit Total Incurred Budget

Variable manufacturing

costs:

Direct materials 30.00$ 180,000$ 171,000$ (9,000)$

Direct labor 48.00 288,000 261,500 (26,500)

Indirect labor 15.00 90,000 95,500 5,500

b.

c. Manufacturing overhead incurred:

The revised performance report above shows that although actual costs exceeded the

costs

SOLUTIONS TO PROBLEMS SET B

25 Minutes, Easy PROBLEM 23.1B

FROWREN DOMESTIC

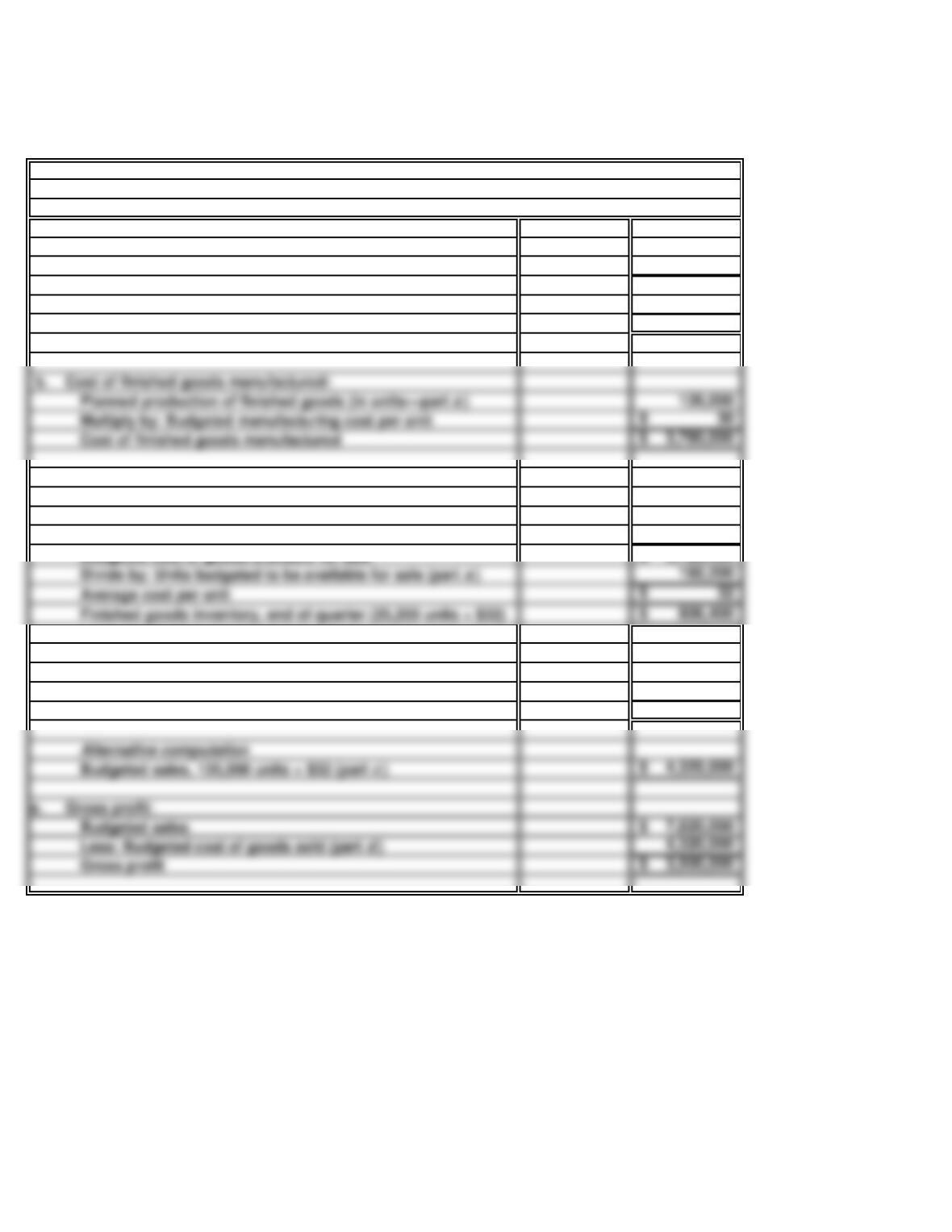

a. Planned production of finished goods (in units):

Budgeted sales

135,000

Add: Finished goods inventory, end of quarter 25,200

Units budgeted to be available for sale 160,200

Less: Finished goods inventory, beginning of quarter 34,200

Planned production of finished goods 126,000

c. Finished goods inventory at quarter-end (average cost):

Finished goods inventory, beginning of quarter

1,346,400$

Add: Cost of finished goods manufactured (part b)3,780,000

Budgeted cost of goods available for sale 5,126,400$

d. Cost of goods sold:

Budgeted cost of goods available for sale (part c)5,126,400$

Less: Finished goods inventory, end of quarter (part c)806,400

Cost of goods sold 4,320,000$

Budgeted sales, 135,000 units × $32 (part c)4,320,000$

7,820,000$

Less: Budgeted cost of goods sold (part d)4,320,000

Multiply by: Budgeted manufacturing cost per unit 30$

Cost of finished goods manufactured 3,780,000$

20 Minutes, Medium PROBLEM 23.2B

HARLOW CORPORATION

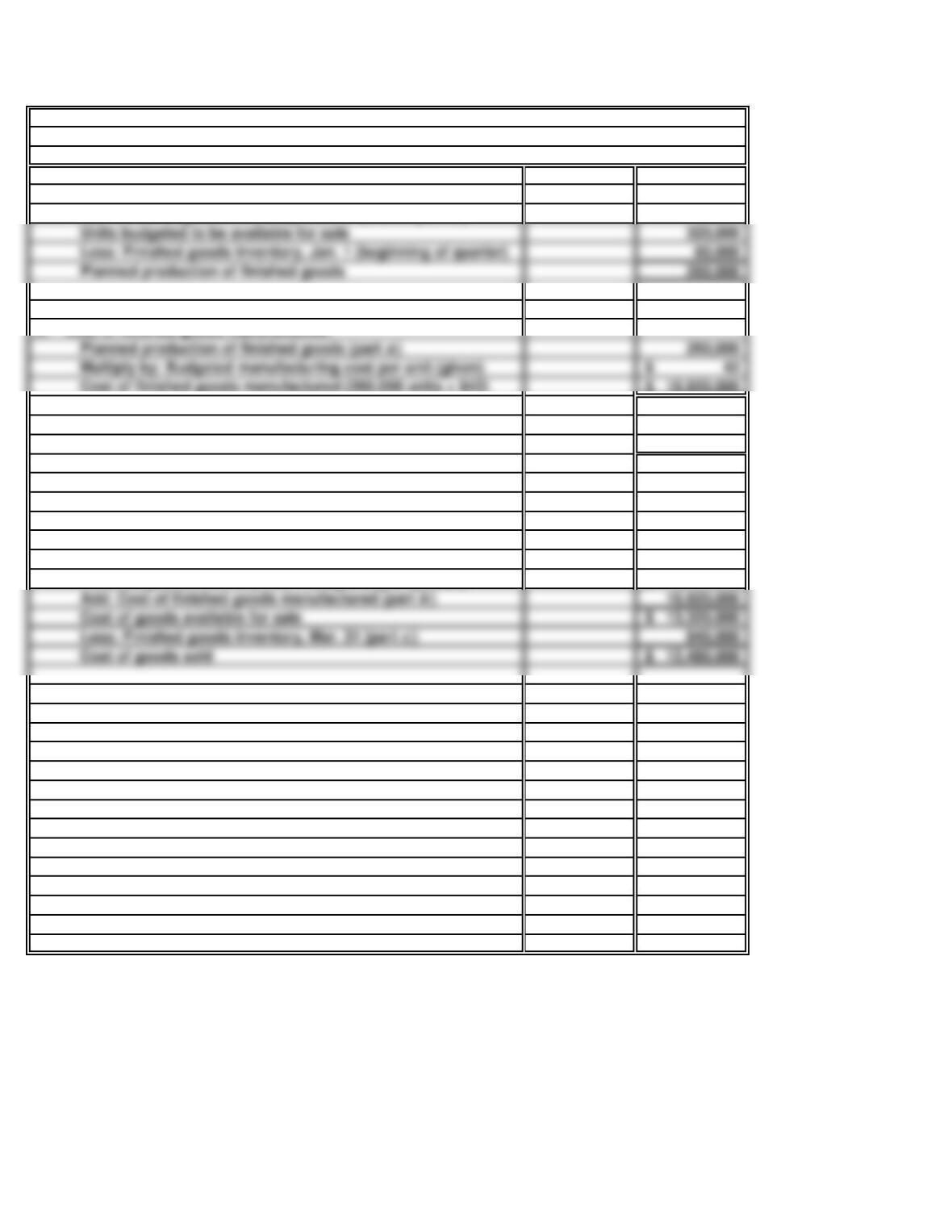

a. Planned production of finished goods (in units):

Budgeted sales 300,000

Add: Finished goods inventory, Mar. 31 (end of quarter) 20,000

b. Cost of finished goods manufactured:

Planned production of finished goods (part a)260,000

Cost of finished goods manufactured (260,000 units × $42) 10,920,000$

c. Finished goods inventory, Mar. 31 (FIFO method):

Finished goods inventory, Mar. 31 (20,000 units × $42)* 840,000$

*Using the first-in, first-out method, the ending

inventory consists of the most recently manufactured

units.

d. Cost of goods sold:

Finished goods inventory, Jan 1. (beginning of quarter) 2,400,000$

Add: Cost of finished goods manufactured (part b)10,920,000

Less: Finished goods inventory, Mar. 31 (part c)840,000

Cost of goods sold 12,480,000$

Less: Finished goods inventory, Jan. 1 (beginning of quarter) 60,000

Planned production of finished goods 260,000

50 Minutes, Strong PROBLEM 23.3B

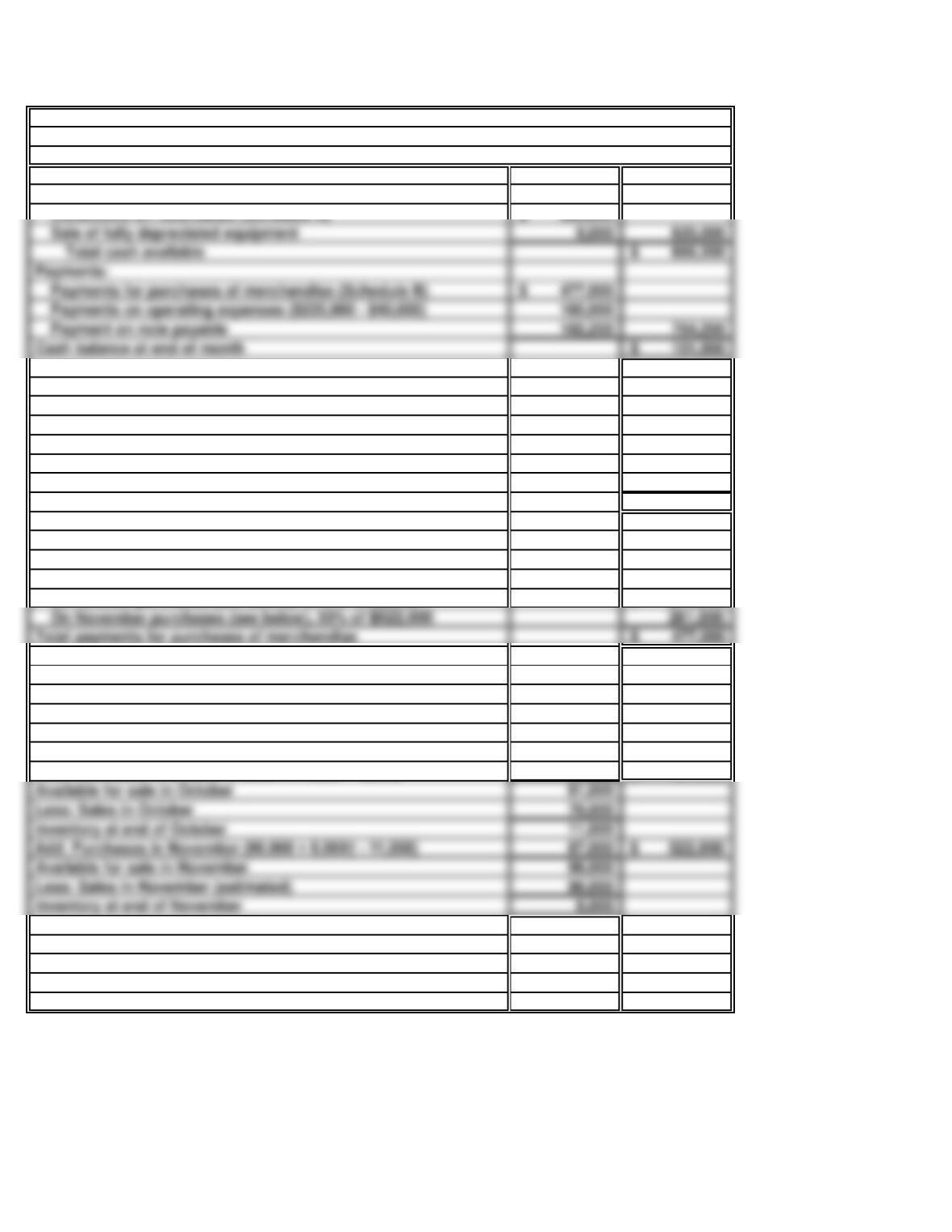

BARLEY, INC.

Cash balance at beginning of month 37,200$

Receipts:

Collections on receivables (Schedule A) 820,000$

Schedule A—Collections on Receivables in November

September sales: 3% × (50,000 × $10)—actual 15,000$

October sales: 25% × (70,000 × $10)—actual 175,000

November sales: 70% × (90,000 × $10)—estimated 630,000

Total collections on receivables 820,000$

Schedule B—Payments for Purchases of Merchandise

On October purchases (see below), 50% of $432,000 216,000$

On November purchases (see below), 50% of $522,000 261,000

Total payments for purchases of merchandise 477,000$

Purchases

Computation of Purchases Units ($6 Per Unit)

Inventory at end of September (2,000 + 10% of 70,000) 9,000

Add: Purchases in October (70,000 + 11,000* – 9,000) 72,000 432,000$

Less: Sales in October 70,000

Less: Sales in November (estimated) 90,000

*2,000 + 10% of 90,000 = 11,000 units

†2,000 + 10% of 60,000 = 8,000 units

BARLEY, INCORPORATED

Cash Budget

For the Month Ended November 30th

Cash balance at end of month 101,950$

40 Minutes, Strong PROBLEM 23.4B

PETER CORPORATION

a. Budgeted cash receipts for the quarter:

Collections on prior period receivables 250,000$

Collections on 70% of $700,000 sales 490,000

Total receipts collected during the quarter 740,000$

b. Payments of current payables budgeted for the quarter:

Beginning current payables 90,000$

c. If beginning prepayments equal the ending prepayments

the amount expired during the period equals the

prepayments made during the period, or $18,000.

d. Cash budget:

Beginning cash 10,000$

Cash received from customers (part a)740,000

Ending cash balance (deficit) (5,000)$

Cash available 750,000$

e. Given a minimum required cash balance of $10,000,

the company must attempt to obtain a loan of $15,000.

f. A bank will look for evidence that Peter has the ability

to service new debt. In view of the fact that the

New payables during quarter 442,000

Ending current payables ($90,000 + $15,000) 105,000

Payments on current payables 427,000$

30 Minutes, Strong PROBLEM 23.5B

SYNDER’S

a. Budgeted income statement:

Budgeted sales 100,000$

Cost of goods sold (60% of sales) 60,000

Gross profit (40% of sales) 40,000$

Variable selling & administrative costs (5% of sales) 5,000

b. Cash budget:

Beginning cash, May 1 30,000$

Add: Collections on March sales (10% × $90,000) 9,000

Collections on April sales (50% × $40,000) 20,000

Collections on May sales (40% × $100,000) 40,000

Ending cash, May 31 31,750$

c. Benefits of budgeting:

* Provides management with an early indication of

possible problems in the upcoming period, such as

insufficient amount of raw materials or labor needed

for production.

* Ensures the cooperation of different departments within

a company to meet the expected production levels.

finished good.

Fixed selling & administrative costs 10,000

Interest expense 3,000

Income taxes (25%) 5,500

Budgeted net income 16,500$

60 Minutes, Strong PROBLEM 23.6B

HOFFMAN INDUSTRIES

a.

July August September

Supporting Schedules

Schedule 1—Estimated Cash Collections

on Receivables

Receivables outstanding at June 30 160,000$ 40,000$

July sales—75% × $340,000 255,000

Schedule 2—Estimated Merchandise Purchases

Sales 340,000$ 360,000$ 300,000$

Cost of goods sold (65% of sales) 221,000$ 234,000$ 195,000$

Add: Required ending inventory* 234,000 195,000 143,000

Less: Beginning merchandise inventory 80,000 234,000 195,000

Budgeted merchandise purchases on open account

*Cost of goods sold for October, 65% ×

$220,000, or $143,000.

Schedule 3—Estimated Cash Payments

for Operating Expenses

Fixed expenses 40,000$ 40,000$ 40,000$

Variable expenses (10% of sales) 34,000 36,000 30,000

Less: Depreciation expense included above 5,000 5,000 5,000

Operating expenses incurred on open account 69,000$ 71,000$ 65,000$

PROBLEM 23.6B

HOFFMAN INDUSTRIES (concluded)

July August September

Schedule 4—Estimated Cash Payments

on Accounts Payable (Including

Operating Expenses)

Accounts payable balance on June 30

(includes accrued operating expenses) 160,000$

b.

HOFFMAN INDUSTRIES

Cash Budget

For Third Quarter of Current Year

July August September

Cash balance at beginning of month 18,000$ 233,000$ 84,000$

Receipts:

Bank loan 240,000

Collections on receivables (Schedule 1) 160,000 295,000 351,600

Total cash available 418,000$ 528,000$ 435,600$

Total disbursements 185,000$ 444,000$ 266,000$

Disbursements:

Purchase of equipment 25,000$

It is apparent from the three-month budget that Hoffman will not be able to pay the bank

50 Minutes, Medium PROBLEM 23.7B

EIGHT FLAGS

a. EIGHT FLAGS

Comparison of Budgeted and Actual Revenue and Expenses

For the Year Ended December 31

Flexible Over (or

Budget Actual Under) Budget

Net sales 18,000,000$ 18,000,000$ 0$

Cost of goods sold 11,700,000 11,160,000 (540,000)

Gross profit on sales 6,300,000$ 6,840,000$ 540,000$

Operating expenses:

Selling and promotion 1,780,000$ 800,000$ (980,000)$

Building occupancy 480,000 450,000 (30,000)

Total operating expenses 4,450,000$ 2,630,000$ (1,820,000)$

Operating income 1,850,000$ 4,210,000$ 2,360,000$

b.

Comment on performance:

45 Minutes, Medium PROBLEM 23.8B

XL INDUSTRIES

a. XL INDUSTRIES

Performance Report for Widget Production Dept.

For the Year Ended December 31st

Budgeted Costs Actual Over

for 5,000 Units Costs (or Under)

Per Unit Total Incurred Budget

Variable manufacturing

costs:

Direct materials 25.00$ 125,000$ 120,000$ (5,000)$

Direct labor 50.00 250,000 210,000 (40,000)

Total variable

manufacturing costs 97.00$ 485,000$ 423,000$ (62,000)$

Fixed manufacturing

costs:

Lease rental 8.00$ 40,000$ 40,000$ $ 0

Salaries of foremen 20.00 100,000 104,000 4,000

Depreciation

and other 14.40 72,000 75,000 3,000

Total fixed

manufacturing costs 42.40$ 212,000$ 219,000$ 7,000$

Total manufacturing costs 139.40$ 697,000$ 642,000$ (55,000)$

b.

c. Manufacturing overhead incurred:

Indirect labor 50,000$

Indirect materials, supplies, etc. 43,000

Total fixed manufacturing costs 219,000

Manufacturing overhead applied, 150% of $210,000 (direct labor) 315,000

Overapplied manufacturing overhead 3,000$

The revised performance report above shows that although actual costs exceeded the

Indirect labor 12.00 60,000 50,000 (10,000)

Indirect materials,

SOLUTIONS TO CRITICAL THINKING CASES

CASE 23.1

BUDGETING IN A NUTSHELL

30 Minutes, Medium

The value of this relatively unstructured problem lies in working it, not in the solution. We

find that it does much to refresh the students’ understanding of both accrual accounting and

cash flows.

Students should state clearly their assumptions concerning:

The amounts appearing in the budgeted statements will vary, depending upon the assumed

Payments on accounts payable

CASE 23.2

a.

b.

A banker who discovered that the Rembrant account was Beta’s primary source of revenue

and liquid assets would certainly question whether Beta was in violation of its loan

AN ETHICAL DILEMMA

20 Minutes, Medium

The primary purpose of a review (or an audit) by an independent CPA is to provide people

outside of the organization with an independent expert opinion on the fairness of the

presentation. If Gamm believes the receivable from Rembrant should be written off, he

should insist that it is—or make clear his reservations in his report. Beta’s budget of future

operating results has virtually nothing to do with the collectability of this receivable.

CASE 23.3

a.

CASH BUDGETING

20 Minutes, Medium

Student answers will vary. However, suggestions will likely be based on discussions in the

CASE 23.4

a.

•

b.

20 Minutes, Medium

The following features of the budgeting software are identified.

Because there are several features that allow comparisons among actual prior year results,

this year’s budgeted information, and actual outcomes, users of this software will be able to

BUDGETING SHAREWARE

Prints Statement of Income and Expense—monthly and year to date with the percent of

CASE 23.5

a.

b.

BUDGETING AND INTERNAL CONTROLS

30 Minutes, Medium

The internal control review required by the PCAOB is likely to uncover errors embedded in

Exhibit 23-2 suggests that a material overstatement of sales will result in planned over-

production and higher budgeted selling and administrative expenses than would be