chapter

23

Performance Evaluation

Using Variances from

Standard Costs

______________________________________________

OPENING COMMENTS

Standard cost systems set budgets for the materials, labor, and factory overhead used by a manufacturer to

produce its product. Deviations from these standards are reported as variances.

After studying the chapter, your students should be able to:

1. Describe the types of standards and how they are established.

2. Describe and illustrate how standards are used in budgeting.

3. Compute and interpret direct materials and direct labor variances.

4. Compute and interpret factory overhead controllable and volume variances.

5. Journalize the entries for recording standards in the accounts and prepare an income statement that

includes variances from standard.

6. Describe and provide examples of nonfinancial performance measures.

KEY TERMS

budget performance report

budgeted variable factory overhead

controllable variance

cost variance

currently attainable standards

420 Chapter 23 Performance Evaluation Using Variances from Standard Costs

direct labor rate variance

direct labor time variance

direct materials price variance

direct materials quantity variance

factory overhead cost variance report

favorable cost variance

ideal standards

nonfinancial performance measure

process

standard cost

standard cost systems

standards

total manufacturing cost variance

unfavorable cost variance

volume variance

STUDENT FAQS

• Do we need to know all these variance formulas? If so, is there a shortcut method we can use to

calculate the six formulas?

• What is a standard, and why can it vary from company to company?

• How often should a standard change?

• Why does management need to evaluate variances and make adjustments?

• Factory overhead is divided into fixed and variable costs. Why not call volume, fixed and

controllable, variable? It is easier to remember.

• Remind me again, what’s the difference between “applied” and “budgeted”?

• What do volume and controllable variances really mean?

OBJECTIVE 1

Describe the types of standards and how they are established.

SYNOPSIS

Manufacturing companies usually use standard costs for direct materials, direct labor, and factory

overhead. Accounting systems use standard cost systems to determine how much a product should cost

and how much it does cost. The differences are reported as cost variances. It requires the efforts of

engineers, accountants, and others to set standards. Ideal standards are those that can be achieved only

under perfect conditions; currently attainable standards are those that can be achieved with reasonable

effort. Standards are periodically reviewed to ensure they reflect current conditions. The use of standards

is often criticized for the following reasons: discourage improvement beyond standard, too difficult to

maintain, cause employees to lose sight of larger goals, and encourage a narrow focus.

Chapter 23 Performance Evaluation Using Variances from Standard Costs 421

Key Terms and Definition

• Currently Attainable Standards – Standards that represent levels of operation that can be

attained with reasonable effort.

• Ideal Standards – Standards that can be achieved only under perfect operating conditions, such

as no idle time, no machine breakdowns, and no materials spoilage; also called theoretical

standards.

• Standard Cost – A detailed estimate of what a product should cost.

• Standard Cost Systems – Accounting systems that use standards for each element of

manufacturing cost entering into the finished product.

• Standards – Performance goals, often relating to how much a product should cost.

SUGGESTED APPROACH

Manufacturing firms set standards for the amount and price of direct materials, direct labor, and overhead

consumed by their products. Standards establish a benchmark to be used in evaluating actual

performance. They allow management to recognize when costs are not in line with the company’s

projections and to take corrective action.

Ask your students to describe examples of standards in their daily lives. Examples include maximum and

minimum speed limits on highways or rating scales on video games (such as novice, expert, etc.)

This objective also discusses the motivational impact of standards and when they should be revised.

Stress the following points:

1. Unrealistically high standards frustrate employees and stifle motivation. As a result, most companies

do not use theoretical standards, which can be achieved only under perfect operating conditions.

2. Standards that are too low encourage employees to be inefficient. Most companies use currently

attainable standards (normal standards), which can be achieved with reasonable effort.

3. Standards should be changed when they no longer reflect operating conditions. They should not be

revised simply because workers fail to meet standards.

CLASS DISCUSSION—Motivational Impact of Standards

Ask your students to discuss whether they view the grading standards of this course, or other college

courses, as ideal (theoretical standards) or normal (currently attainable standards). Ask them to comment

on how grading standards impact their motivation to study and complete assignments.

422 Chapter 23 Performance Evaluation Using Variances from Standard Costs

OBJECTIVE 2

Describe and illustrate how standards are used in budgeting.

SYNOPSIS

Budgeting assists managers in their control function or budgetary performance evaluation. Manufacturing

standard costs are split into two components: standard price and standard quantity. The standard cost per

unit is computed as: standard cost per unit = standard price × standard quantity. The differences between

actual and standard costs are variances. A favorable cost variance occurs when the actual cost is less than

the standard cost. An unfavorable variance occurs when the actual cost exceeds the standard cost. The

total manufacturing cost variance is the difference between total standard cost and total actual cost for the

units produced. For control purposes, the total cost variance is separated into direct materials, direct labor,

and factory overhead cost variance. Each of these variances is compared to the standard cost and

investigated so the reasons for the favorable and unfavorable variances can be understood.

Key Terms and Definitions

• Budget Performance Report – A report comparing actual results with budget figures.

• Cost Variance – The difference between actual cost and the flexible budget at actual volumes.

• Favorable Cost Variance – A variance that occurs when the actual cost is less than standard cost.

• Total Manufacturing Cost Variance – The difference between total standard costs and total

actual costs for units produced.

• Unfavorable Cost Variance – A variance that occurs when the actual cost exceeds the standard

cost.

Relevant Example Exercises and Exhibits

• Exhibit 1 – Standard Cost for XL Jeans

• Exhibit 2 – Cost Variances

• Exhibit 3 – Budget Performance Report

• Exhibit 4 – Manufacturing Cost Variances

SUGGESTED APPROACH

Budgets exist to help companies plan, direct, and control operations. The budget performance report is a

tool that compares actual costs to budgeted costs.

A sample budget performance report is presented in text Exhibit 2. Point out that the column labeled

“Standard Cost at Actual Volume” is essentially a flexible budget. Flexible budgets were introduced in

Chapter 22.

The following example can be used to illustrate performance measurement under standard costing.

Assume a pizza company has set $5 as the standard cost of ingredients per pizza. The company

anticipates selling 1,000 pizzas during the next week. The budget at the beginning of the week would be

$5,000. This amount would be used for planning.

Chapter 23 Performance Evaluation Using Variances from Standard Costs 423

Now, assume the actual number of pizzas sold during the week was 1,200. The standard cost for

ingredients to make 1,200 pizzas is $6,000. If the pizza parlor actually used $6,900 in ingredients during

the week, there is a $900 variance from standard. This is an unfavorable variance since actual costs

exceeded the standard cost for 1,200 pizzas.

This information would be presented on a budget performance report as follows:

Standard Cost

Actual at Actual Volume Cost Variance

Cost (1,200 pizzas) (Favorable)/Unfavorable

Pizza Ingredients $6,900 $6,000 $900

Management should investigate to determine whether this variance resulted from using ingredients that

were more expensive than anticipated or from using more ingredients per pizza than budgeted. Note that

comparing the $6,900 actual cost to the $5,000 original budget is not meaningful.

OBJECTIVE 3

Compute and interpret direct materials and direct labor variances.

SYNOPSIS

As demonstrated in the prior objective, direct materials and direct labor variances are separated. The direct

materials variance is separated into price and quantity variances. The actual cost is calculated as follows:

actual direct materials cost = actual price × actual quantity. The standard materials cost is calculated as

follows: standard direct materials cost = standard price × standard quantity. The direct materials price

variance is calculated as follows: direct materials price variance = (actual price – standard price) × actual

quantity. The direct materials quantity variance is calculated as: direct materials quantity variance = (actual

quantity – standard quantity) × standard price. These relationships are shown in Exhibit 6.

The direct labor variance is separated into rate and time variances. The actual costs are calculated as:

actual direct labor cost = actual rate per hour × actual time. The standard costs are calculated as follows:

standard direct labor cost = standard rate per hour × standard time. The direct labor rate variance is: direct

labor rate variance = (actual rate per hour – standard rate per hour) × actual hours. The direct labor time

variance is calculated as follows: direct labor time variance = (actual direct labor hours – standard direct

labor hours) × standard rate per hour. These relationships are illustrated in Exhibit 7. Direct labor time

standards can also be developed for administrative, selling, and service activities.

Key Terms and Definitions

• Direct Labor Rate Variance – The cost associated with the difference between the standard rate

and the actual rate paid for direct labor used in producing a commodity.

• Direct Labor Time Variance – The cost associated with the difference between the standard

hours and the actual hours of direct labor spent producing a commodity.

424 Chapter 23 Performance Evaluation Using Variances from Standard Costs

• Direct Materials Price Variance – The cost associated with the difference between the standard

price and the actual price of direct materials used in producing a commodity.

• Direct Materials Quantity Variance – The cost associated with the difference between the

standard quantity and the actual quantity of direct materials used in producing a commodity.

Relevant Example Exercises and Exhibits

• Example Exercise 23-1 Direct Materials Variances

• Example Exercise 23-2 Direct Labor Variances

• Exhibit 5 – Direct Materials and Direct Labor Cost Variances

• Exhibit 6 – Direct Materials Variance Relationships

• Exhibit 7 – Direct Labor Variance Relationships

SUGGESTED APPROACH—Direct Material

Variances are a perplexing topic for many students. As a result, you will probably need to dedicate

significant class time to this topic. For materials variances, demonstrate how each variance is calculated

and give your students the opportunity to practice these calculations using group learning activities.

DEMONSTRATION PROBLEM—Direct Materials Variances

To demonstrate materials variances, use the following data for Martin Manufacturing during the month of

November.

Standard: 5 pounds of direct materials are required per unit at $3.20 per pound

Actual: 104,000 pounds were used to produce 20,000 units; actual materials cost was

$3.15 per pound

Price Variance: Emphasize that a direct materials price variance shows the difference between the actual

and standard price for the actual quantity of materials used. The formula for this calculation is:

(Actual Price per Unit – Standard Price per Unit) Actual Quantity Used

(AP – SP) AQ Used

Using the data from Martin Manufacturing:

($3.15 – $3.20) 104,000 = $5,200 favorable price variance

This variance is favorable because the materials cost $0.05 less per pound than standard.

Quantity Variance: Emphasize that the direct materials quantity variance shows the difference between

the actual and standard quantity of materials used. This difference is measured at the standard price

because the effect of the $0.05 per pound price savings was computed in the price variance. The formula

to compute the quantity variance is:

Chapter 23 Performance Evaluation Using Variances from Standard Costs 425

(Actual Quantity Used – Standard Quantity) Standard Price per Unit

(AQ Used – SQ) SP per Unit

Using the data from Martin Manufacturing:

(104,000 – 100,000) $3.20 = $12,800 unfavorable quantity variance

Note that the standard quantity is 100,000 (5 lbs. per unit 20,000 units actually produced).

This variance is unfavorable because Martin used 4,000 more pounds than standard.

Total Variance: The total materials variance is the difference between the actual and standard cost of

materials. It may be computed as follows:

(Actual Quantity Actual Price per Unit) – (Standard Quantity Standard Price per Unit)

(AQ AP per Unit) – (SQ SP per Unit)

Using the data from Martin Manufacturing:

(104,000 pounds $3.15 per pound) – (100,000 pounds $3.20 per pound)

= $327,600 – $320,000

= $7,600 unfavorable total direct materials cost variance

The total variance may also be computed as follows:

Price variance $ 5,200 favorable

Quantity variance 12,800 unfavorable

Total variance $ 7,600 unfavorable

GROUP LEARNING ACTIVITY—Direct Materials Variances

Transparency Master (TM) 23-1 presents standard and actual cost data for direct materials used by Brass

Works, Inc., a manufacturer of brass lamps and gift products. Instruct your students to compute materials

price and quantity variances for Brass Works, Inc. The solution to this activity is on TM 23-2.

CLASS DISCUSSION—Interpreting Materials Variances

As you review the solution to the group learning activity above (TM 23-2), ask your students to identify

which department of Brass Works, Inc. should be held accountable for each variance. Also ask them to

brainstorm possible reasons for the variance. Some examples follow:

Amount Responsibility Possible Reason(s) for Variance

Materials $420 U Purchasing Price increase from supplier.

Price Variance Department Extra freight charge on a rush order.

426 Chapter 23 Performance Evaluation Using Variances from Standard Costs

Materials $250 U Production Waste due to machine malfunction.

Quantity Variance Department Poor quality materials.

SUGGESTED APPROACH—Direct Labor

The labor rate and time variances closely mirror the materials price and quantity variances. As you

present the formulas to calculate labor variances, stress the similarity to the materials variances. Ask your

students to apply these formulas using a Group Learning Activity.

LECTURE AID—Direct Labor Variances

Differences between actual and standard labor costs are analyzed by computing a rate and a time

variance. The labor rate variance essentially performs the same analysis as the materials price variance. It

computes the cost difference due to a change in labor rate. The formula for the rate variance is:

(Actual Rate per Hour – Standard Rate per Hour) Actual Hours Worked

(AR per Hour – SR per Hour) AH Worked

The labor time variance computes the labor cost difference due to using more or less labor time than

standard. This variance parallels the materials quantity variance. The formula is:

(Actual Hours Worked – Standard Hours) Standard Rate per Hour

(AH Worked – SH) SR per Hour

Ask your students to identify which labor variances could be caused by new employees. Answer: New

employees will usually create an unfavorable time variance as they learn their job. They may also cause a

favorable rate variance if standards were based on wages earned by experienced employees and the new

employee wage rate is below that amount.

GROUP LEARNING ACTIVITY—Direct Labor Variances

TM 23-3 presents labor data for Brass Works, Inc. Ask your students to work in groups to calculate labor

rate and time variances using the above formulas. The solution is shown on TM 23-4.

CLASS DISCUSSION—Interpreting Materials Variances

As you review the solution on TM 23-4, ask your students to identify which department of Brass Works,

Inc. should be held accountable for each labor variance. Also ask them to brainstorm possible reasons for

the variance. Some examples follow:

Amount Responsibility Possible Reason(s) for Variance

Labor $2,380 F Production Workers at lower wage rate

Rate Variance Department assigned to job (e.g., temporary

employees, less-skilled workers).

Chapter 23 Performance Evaluation Using Variances from Standard Costs 427

Labor $3,800 U Production Extra labor time required due to

Time Variance Department poor quality materials.

Extra labor time required due to

machine malfunctions.

SUGGESTED APPROACH—Nonmanufacturing Businesses

Standards can be applied to nonmanufacturing businesses, provided that they use repetitive activities to

produce a common product or service. For example, businesses that specialize in fast, no-appointment-

needed oil changes provide a standard service comprised of repetitive activities. A standard cost to

perform an oil change could be developed based on the (1) standard labor time to change a customer’s oil,

(2) standard wage rate, (3) standard quantity of supplies used (motor oil, filters, etc.), and (4) standard

price of supplies.

Public accounting firms are another example of businesses that rely heavily upon standards. Budgets and

standards are used to measure performance on various client engagements, such as audits and tax work.

WRITING EXERCISE—Standards in a Nonmanufacturing Environment

Ask your students to answer the following in writing (TM 23-8).

Describe a nonmanufacturing business that could benefit from the use of standards. Also

explain how standards would help that business control its operations.

Possible response: One example of a business that could benefit from the use of standards in a

nonmanufacturing environment would be medical or legal transcription. The number of words

transcribed per minute is an easy measurement to determine how employees are performing

against a standard. Labor rates are also easy to track in this environment. This is only one

example; your students should provide additional examples to discuss.

OBJECTIVE 4

Compute and interpret factory overhead controllable and volume variances.

SYNOPSIS

The factory overhead costs are analyzed differently than materials and labor due to fixed and variable

components. Factory overhead is first separated to allow its components to be analyzed. The factory

overhead rate is figured as: factory overhead rate = budgeted factory overhead at normal capacity/normal

productive capacity. The formula to analyze the variable component is: variable factory overhead rate =

budgeted variable overhead at normal capacity/normal productive capacity. To find the fixed factory

component, fixed factory overhead rate = budgeted fixed overhead at normal capacity/normal productive

capacity. The variable factory overhead controllable variance is the difference between the actual

428 Chapter 23 Performance Evaluation Using Variances from Standard Costs

overhead costs and the budgeted variable overhead for actual production. It is computed as: variable

factory overhead controllable variance = actual variable factory overhead – budgeted variable factory

overhead. The budgeted variable overhead is computed as: budgeted variable factory overhead = standard

hours for actual units produced × variable factory overhead rate. The variable factory controllable

variance is computed as: variable factory overhead controllable variance = actual variable factory

overhead – budgeted variable factory overhead. The fixed factory overhead volume variance is the

difference between the budgeted fixed overhead at 100% of normal capacity and the standard fixed

overhead for the actual units produced computed as: fixed factory overhead volume variance = (standard

hours for 100% of normal capacity – standard hours for actual units produced) × fixed factory overhead

rate. The volume variance measures the use of fixed overhead resources. Management should determine

the causes of the unfavorable variance and consider taking corrective action. The total factory overhead

cost variance can also be determined as the sum of the variable factory overhead costs. The factory

overhead cost variance report is shown in Exhibit 10. At the end of the period, the factory overhead

account normally has a balance. A debit balance in Factory Overhead represents underapplied overhead,

which occurs when actual factory overhead costs exceed the applied factory overhead. A credit balance in

Factory Overhead occurs when actual factory overhead costs are less than the actual applied factory

overhead. If the actual factory overhead exceeds the budgeted factory overhead, the controllable variance

is unfavorable. If the actual factory overhead is less than the budgeted factory overhead, the volume

variance is unfavorable.

Key Terms and Definitions

• Budgeted Variable Factory Overhead – The standard variable overhead for the actual units

produced.

• Controllable Variance – The difference between the actual amounts of variable factory overhead

cost incurred and the amount of variable factory overhead budgeted for the standard product.

• Factory Overhead Cost Variance Report – Reports budgeted and actual costs for variable and

fixed factory overhead along with the related controllable and volume variances.

• Volume Variance – The difference between the budgeted fixed overhead at 100% of normal

capacity and the standard fixed overhead for the actual production achieved during the period.

Relevant Example Exercises and Exhibits

• Example Exercise 23-3 Factory Overhead Controllable Variance

• Example Exercise 23-4 Factory Overhead Volume Variance

• Exhibit 8 – Factory Overhead Cost Budget Indicating Standard Factory Overhead Rate

• Exhibit 9 – Graph of Fixed Overhead Volume Variance

• Exhibit 10 – Factory Overhead Cost Variance Report

• Exhibit 11 – Factory Overhead Variances

SUGGESTED APPROACH

Consider spending extra time covering factory overhead variances, since students seem to have the most

difficulty with these variances. One of the major reasons for this is that, while direct materials and direct

labor costs are variable, factory overhead costs have both fixed and variable components. You can

continue the pattern of demonstrating variance calculations and asking students to practice these

computations, using the aids below.

Chapter 23 Performance Evaluation Using Variances from Standard Costs 429

DEMONSTRATION PROBLEM—Overhead Variances

In most cases, factory overhead costs are applied to production, using a predetermined factory overhead

rate, calculated as follows:

Estimated Total Factory Overhead Costs

Estimated Activity Base (or Driver) (e.g., direct labor or machine hours)

Factory overhead variances result when factory overhead applied to products does not equal actual

overhead. Therefore, factory overhead variances occur whenever:

1. Factory overhead costs were greater or less than estimated.

2. The company operated above or below the capacity anticipated when estimating the activity driver.

Use the following data to illustrate factory overhead variances.

Martin Manufacturing applies factory overhead to products using direct labor hours. To calculate a

predetermined overhead rate, Martin developed the following estimates for one month of production.

Direct labor hours at 100 percent of normal capacity 12,000 hrs.

Estimated fixed factory overhead costs $120,000

Estimated variable factory overhead costs at 100 percent of normal capacity $ 84,000

As a result, Martin’s predetermined factory overhead rate is $17 per direct labor hour. Of that rate, fixed

factory overhead is $10 per hour ($120,000/12,000 hrs.) and variable factory overhead is $7 per hour

($84,000/12,000 hrs.).

Martin’s labor standards allow 0.5 direct labor hours for each unit produced. During November, 20,000

units were produced. Actual fixed factory overhead costs were $120,000. Actual variable factory

overhead costs were $88,000.

Variable Factory Overhead Controllable Variance: The text defines this variance as the difference

between actual variable overhead costs and variable overhead budgeted for the amount of product actually

produced. (Note that the text is essentially presenting a two-way overhead analysis.) This can be

expressed in the following formula:

Actual Var. OH – (Var. OH Rate per Hr. Units Produced Standard Hrs. per Unit)

Using data from Martin Manufacturing:

Actual Variable Factory Overhead = $88,000

Budgeted Variable Factory Overhead for

Actual Amount Produced = $7 20,000 units 0.50 hrs. per unit = $70,000

Controllable Variance = $88,000 – $70,000 = $18,000 unfavorable

430 Chapter 23 Performance Evaluation Using Variances from Standard Costs

Fixed Factory Overhead Volume Variance: This variance measures the difference between the budgeted

fixed overhead at 100 percent of normal capacity and the standard fixed overhead for the amount of

product actually produced. In essence, it measures the impact of spreading fixed overhead over the wrong

number of units, whenever actual production does not equal the amount anticipated by the predetermined

fixed overhead rate. This can be expressed in the following formula:

(Hrs. at 100% of normal capacity – Std. Hrs. for Actual Production) Fixed OH Rate per Hr.

Remind students that the term “Hrs. at 100% of normal capacity” is the hours used in computing the

predetermined overhead rate.

Using the data from Martin Manufacturing:

(12,000 hours – 10,000 hours) $10 per hr. = $20,000 unfavorable

Therefore, Martin’s total overhead variance is as follows:

Controllable variance $ 18,000 unfavorable

Volume variance 20,000 unfavorable

Total overhead variance $ 38,000 unfavorable

Emphasize that the total factory overhead variance is also the difference between actual overhead costs

and overhead applied using a predetermined overhead rate. Therefore, the $38,000 unfavorable total

factory overhead variance also represents $38,000 of underapplied overhead. The concept of over– and

underapplied overhead was introduced in Chapter 19 when covering Job Order Costing.

GROUP LEARNING ACTIVITY—Overhead Variances

TM 23-5 presents data for your students to use in calculating overhead variances. The solution to the

exercise is provided on TM 23-6.

OBJECTIVE 5

Journalize the entries for recording standards in the accounts and prepare an income

statement that includes variances from standard.

SYNOPSIS

Standard costs may be used as a management tool to control costs separately from the accounts in the

general journal in the general ledger. However, many companies include standard costs in their accounts.

To do so, when purchasing materials, Materials would be debited at the standard price, Accounts Payable

would be credited for the actual price, and the variance would be debited or credited depending on the

difference between the prices. The variance for quantity would be journalized in a similar manner. Work

in Process would be debited, Direct Materials Quantity Variance would be either debited or credited

depending on whether the amount requested was above or below the standard, and Materials would be

Chapter 23 Performance Evaluation Using Variances from Standard Costs 431

credited. A debit balance in the direct materials quantity variance account represents an unfavorable

variance. The direct labor entries are summarized as: Work in Process is debited, Wages Payable is

credited for the actual direct labor cost, Direct Labor Rate Variance is debited for an unfavorable variance

and credited for a favorable variance, and Direct Labor Time Variance is debited for an unfavorable

variance and credited for a favorable variance. These variances may be reported on an income statement

prepared for management’s use. These variances are not on the income statement for external users.

Relevant Example Exercises and Exhibits

• Example Exercise 23-5 Standard Cost Journal Entries

• Example Exercise 23-6 Income Statement with Variances

• Exhibit 12 – Variance from Standards in Income Statement

SUGGESTED APPROACH

Some companies choose to integrate standards and variances into their accounting records. When this

occurs, entries to the materials, work in process, and finished goods inventory accounts are recorded at

standard, not actual, costs. It is helpful to illustrate these entries for your students. A demonstration

problem is included below for that purpose.

DEMONSTRATION PROBLEM—Journal Entries at Standard

The group learning activities under Objectives 3 and 4 asked your students to compute materials and labor

variances. Use these calculations to illustrate the following journal entries.

Purchase of Materials: Brass Works used 1,050 pounds of direct materials that cost $5.40 per pound. The

effect of paying $0.40 more per pound than standard was a $420 unfavorable price variance. The purchase

of these materials would be recorded as follows:

Materials (1,050 pounds $5.00) 5,250

Direct Materials Price Variance 420

Accounts Payable (1,050 pounds $5.40) 5,670

Note that the Materials account is debited for the standard cost of materials purchased.

Requisition of Materials: Brass Works used 1,050 pounds of direct materials for production when the

standard materials quantity was only 1,000 pounds. The effect of using more materials than standard is

recorded when the materials are transferred to Work in Process.

Work in Process (1,000 pounds $5.00) 5,000

Direct Materials Quantity Variance 250

Materials (1,050 pounds $5.00) 5,250

Note that the work in process account is debited for the standard price and quantity of materials. The

materials account is credited for the actual quantity of materials used but at the standard price. The actual

432 Chapter 23 Performance Evaluation Using Variances from Standard Costs

quantity of materials used must be removed from the account in order to have an accurate record of the

amount of materials still on hand.

Payment of Direct Labor Costs: Brass Works incurred 2,380 direct labor hours at a cost of $9 per hour.

The standard was 2,000 hours at $10 per hour. The payroll entry to record direct labor wages is:

Work in Process (2,000 hours $10) 20,000

Direct Labor Time Variance 3,800

Direct Labor Rate Variance 2,380

Wages Payable 21,420

The work in process account is debited for the standard labor rate and standard labor time.

Remind students that variances are usually transferred to Cost of Goods Sold at the end of the year.

Unfavorable variances (resulting from costs above standard) increase Cost of Goods Sold; favorable

variances (resulting from costs below standard) decrease Cost of Goods Sold. If variances are material,

they should be allocated to Work in Process, Finished Goods, and Cost of Goods Sold.

LECTURE AID—Reporting Variances on the Income Statement

Variances are not usually reported on financial statements prepared for stockholders, creditors, or other

parties outside company management. However, they may be included on income statements prepared for

management use. Exhibit 9 in the text provides an example of an income statement that reports variances.

The key to this exhibit is understanding how the variances affect gross profit. Use the chart on TM 23-7 to

explain the impact of favorable and unfavorable variances on gross profit.

OBJECTIVE 6

Describe and provide examples of nonfinancial performance measures.

SYNOPSIS

A nonfinancial performance measure expresses performance in a measure other than dollars. Using

financial and nonfinancial performance measures aids managers and employees in considering multiple

performance objectives. Examples of nonfinancial performance measures are listed in Exhibit 13.

Nonfinancial measures are often linked to either the inputs or outputs of an activity or process. A process

is a sequence of activities for performing a task. The relationship between an activity or a process and its

inputs can be measured; this relationship is shown in Exhibit 14.

Key Terms and Definitions

• Nonfinancial Performance Measure – A performance measure expressed in units rather than

dollars.

• Process – A sequence of activities linked together for performing a particular task.

Chapter 23 Performance Evaluation Using Variances from Standard Costs 433

Relevant Example Exercises and Exhibits

• Example Exercise 23-7 Activity Inputs and Outputs

• Exhibit 13 – Nonfinancial Performance Measures

• Exhibit 14 – Relationship Between a Process and Its Inputs and Outputs

• Exhibit 15 – Inputs/Outputs for a Fast-Food Restaurant

SUGGESTED APPROACH

Measurements encourage improving the actions that are being measured. This is true both in the business

world and in the classroom. Use the writing exercise below to stimulate your students to think about the

benefits and difficulties of nonfinancial performance measures.

WRITING EXERCISE—Nonfinancial Performance Measures

Ask your students to write their opinion on the following questions (TM 23-9):

Students’ scores on exams may be equated to financial measures used to evaluate

employee performance in a business. Should college professors limit their evaluation of

students to these “financial” measures? Do you see any potential benefits or disadvantages

of including other measures of student performance in assigning course grades?

Possible response: Professors use optional measures to evaluate students all the time.

Attendance, extra credit, and the subjective nature of some assignments provide options for

evaluation on course work other than exam scores. Benefits include motivating students to put in

extra time and effort to grasp the subject. In academia as in business, financial measures are not

always the final or only performance measure.

CLASS DISCUSSION—Nonfinancial Performance Measures

Ask your students to share examples of any nonfinancial measures used by their employers to evaluate

their work. Question your students on why these measures are used. In other words, what behavior is the

employer trying to encourage with these nonfinancial measures?

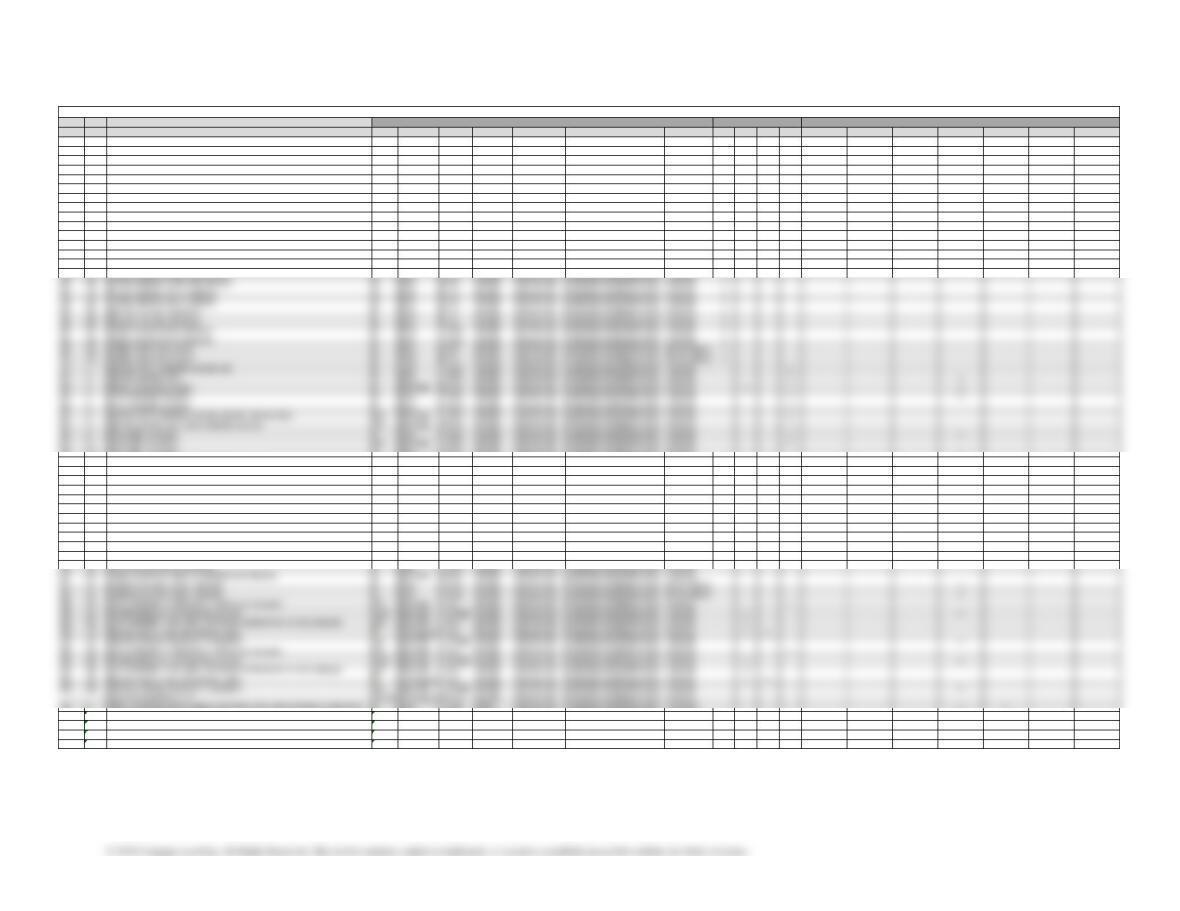

Type Item Description LO(s) Difficulty Time Est BUSPROG AICPA ACBSP – APC Bloom’s EE Excel GL SMH FAI Service Real World Writing Ethics Internet Group

DQ 1 1 Easy 5 min. Analytic Measurement Budgeting and Responsibility Remembering

DQ 2 1 Easy 5 min. Analytic Measurement Budgeting and Responsibility Remembering

DQ 3 3 Easy 5 min. Analytic Measurement Budgeting and Responsibility Remembering

DQ 4 2 Easy 5 min. Analytic Measurement Budgeting and Responsibility Remembering

DQ 5 3 Easy 5 min. Analytic Measurement Budgeting and Responsibility Remembering

DQ 6 3 Easy 5 min. Analytic Measurement Budgeting and Responsibility Remembering

DQ 7 3 Easy 5 min. Analytic Measurement Budgeting and Responsibility Remembering

DQ 8 4 Easy 5 min. Analytic Measurement Budgeting and Responsibility Remembering

DQ 9 5 Easy 5 min. Analytic Measurement Budgeting and Responsibility Remembering

DQ 10 6 Easy 5 min. Analytic Measurement Budgeting and Responsibility Remembering

PE 1A Direct materials variances 3 Easy 10 min. Analytic Measurement Budgeting and Responsibility Applying x

PE 1B Direct materials variances 3 Easy 10 min. Analytic Measurement Budgeting and Responsibility Applying x

PE 2A Direct labor variances 3 Easy 10 min. Analytic Measurement Budgeting and Responsibility Applying x

PE 2B Direct labor variances 3 Easy 10 min. Analytic Measurement Budgeting and Responsibility Applying x

PE 3A Factory overhead controllable variance 4 Easy 5 min. Analytic Measurement Budgeting and Responsibility Applying x

EX 10 Direct labor variances 3 Easy 10 min. Analytic Measurement Budgeting and Responsibility Applying x

EX 11 Direct labor standards for nonmanufacturing expenses 3 Moderate 15 min. Analytic Measurement Budgeting and Responsibility Applying

EX 12 Direct labor standards for nonmanufacturing operations 2,3 Easy 15 min. Analytic Measurement Budgeting and Responsibility Applying

EX 13 Direct labor variances for a service company 3 Moderate 15 min. Analytic Measurement Budgeting and Responsibility Applying x

EX 14 Direct materials and direct labor variances 3 Moderate 15 min. Analytic Measurement Budgeting and Responsibility Applying x

EX 15 Flexible overhead budget 4 Moderate 30 min. Analytic Measurement Budgeting and Responsibility Applying

EX 16 Flexible overhead budget 4 Moderate 30 min. Analytic Measurement Budgeting and Responsibility Applying

EX 17 Factory overhead cost variances 4 Moderate 20 min. Analytic Measurement Budgeting and Responsibility Applying

EX 18 Factory overhead cost variances 4 Easy 15 min. Analytic Measurement Budgeting and Responsibility Applying x

EX 19 Factory overhead variance corrections 4 Moderate 20 min. Analytic Measurement Budgeting and Responsibility Applying

EX 20 Factory overhead cost variance report 4 Moderate 30 min. Analytic Measurement Budgeting and Responsibility Applying x

EX 21 Recording standards in accounts 5 Easy 10 min. Analytic Measurement Budgeting and Responsibility Applying

CP 1 Ethics and professional conduct in business using nonmanufacturing standards 1 Easy 15 min. Ethics Measurement Budgeting and Responsibility Analyzing x x

CP 2 Nonfinancial performance measures 6 Easy 15 min. Analytic Measurement Budgeting and Responsibility Analyzing x

CP 3 Variance interpretation 3 Moderate 30 min. Analytic Measurement Budgeting and Responsibility Evaluating x

CP 4 Variance interpretation 4 Moderate 20 min. Analytic Measurement Budgeting and Responsibility Evaluating x x

CP 5 Nonmanufacturing performance measures – government 6 Moderate 1 hour Analytic Measurement Budgeting and Responsibility Applying

HOMEWORK CHART WITH LEARNING OUTCOMES TAGGING

TAGGING

RESOURCES

FOCUS