CHAPTER 23

Budgetary Planning

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

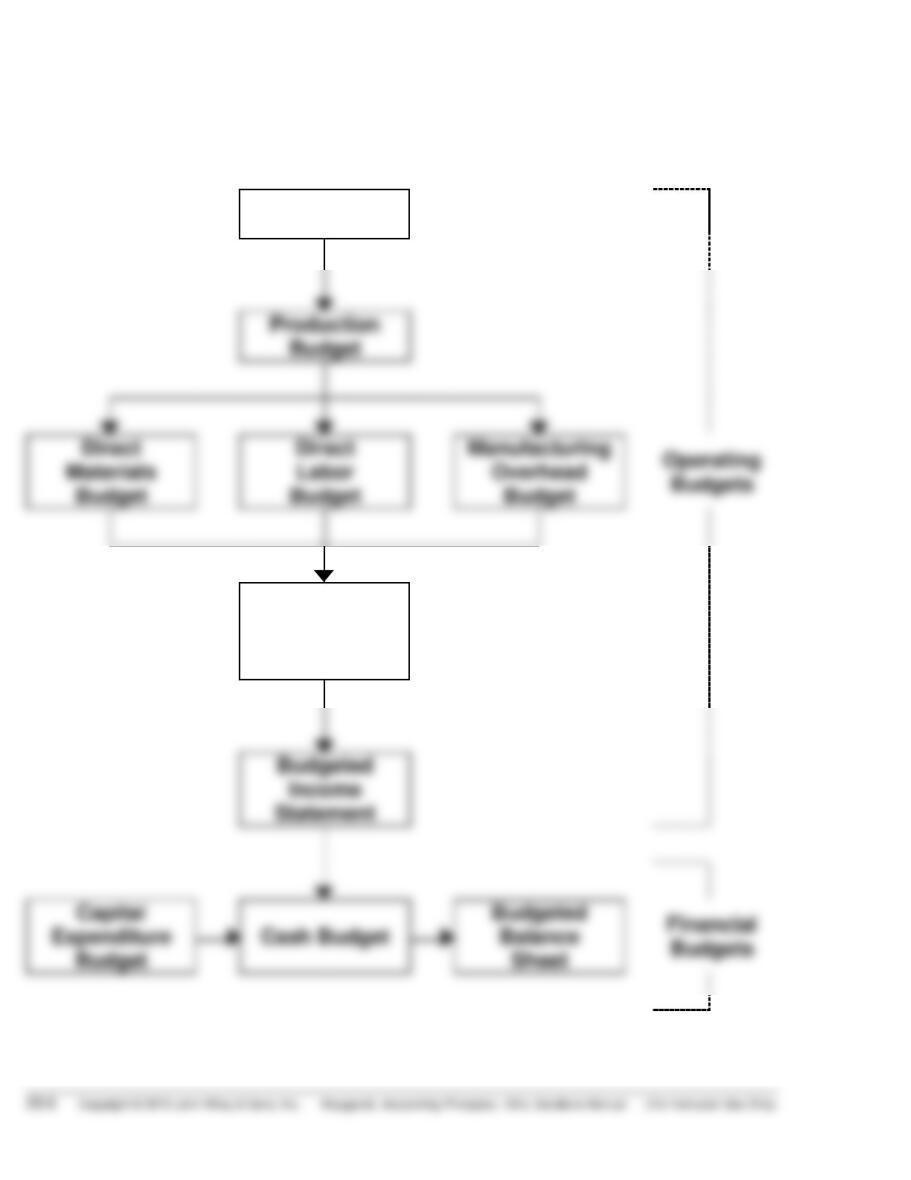

A

Problems

1. State the essentials of effective

budgeting and the components of

the master budget.

1, 2, 3, 4, 5,

6, 7, 8, 9,

10

1

1

1

2. Prepare budgets for sales,

production, and direct materials.

11, 12, 13

2, 3, 4,

2

2, 3, 4, 5, 6,

7, 8, 10

1A, 2A, 3A

3. Prepare budgets for direct labor,

manufacturing overhead, and

selling and administrative

expenses, and a budgeted

income statement.

14, 15, 16,

17, 18

5, 6, 7, 8

3

9, 10, 11,

12, 13

1A, 2A, 6A

4. Prepare a cash budget and a

budgeted balance sheet.

19, 20

9

4

14, 15, 16,

17, 18, 19

4A, 6A

5. Apply budgeting principles to

nonmanufacturing companies.

21, 22

10

5

19, 20, 21

5A

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Prepare budgeted income statement and supporting

budgets.

Simple

30–40

2A

Prepare sales, production, direct materials, direct labor,

and income statement budgets.

Simple

40–50

3A

Prepare sales and production budgets and compute cost

per unit under two plans.

Moderate

30–40

4A

Prepare cash budget for two months.

Moderate

30–40

5A

Prepare purchases and income statement budgets for a

merchandiser.

Simple

30–40

6A

Prepare budgeted cost of goods sold, income statement,

retained earnings and balance sheet.

Complex

40–50

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End–of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

1. State the essentials of

effective budgeting and

the components of the

master budget.

DI23-1

Q23-1

Q23-2

Q23-3

Q23-4

Q23-5

Q23-6

Q23-7

Q23-8

Q23-9

Q23-10

E23-1

BE23-1

2. Prepare budgets for sales,

production, and direct

materials.

Q23-11

Q23-12

Q23-13

BE23-2

BE23-3

BE23-4

DI23-2

E23-2

E23-3

E23-4

E23-5

E23-6

E23-7

E23-8

E23-10

P23-1A

P23-2A

P23-3A

3. Prepare budgets for direct

labor, manufacturing

overhead, and selling and

administrative expenses,

and a budgeted income

statement.

Q23-14

Q23-15

Q23-16

Q23-18

Q23-17

BE23-5

BE23-6

BE23-7

BE23-8

DI23-3

E23-9

E23-10

E23-11

E23-12

E23-13

P23-1A

P23-2A

P23-6A

4. Prepare a cash budget and

a budgeted balance sheet.

Q23-19

Q23-20

BE23-9

DI23-4

E23-14

E23-15

E23-17

E23-18

E23-19

P23-4A

P23-6A

E23-16

5. Apply budgeting

principles to

nonmanufacturing

companies.

Q23-21

Q23-22

BE23-10

DI23-5

E23-19

E23-20

E23-21

P23-5A

Broadening Your Perspective

BYP23-2

BYP23-3

BYP23-4

BYP23-1

BYP23-5

BYP23-6

BYP23-7

ANSWERS TO QUESTIONS

1. (a) A budget is a formal written statement of management’s plans for a specified future time period,

expressed in financial terms.

(b) A budget aids management in planning because it represents the primary method of commu–

nicating agreed-upon objectives throughout the organization. Once adopted, a budget becomes

an important basis for evaluating performance.

2. The primary benefits of budgeting are:

(1) It requires all levels of management to plan ahead and to formalize goals on a recurring basis.

(2) It provides definite objectives for evaluating performance at each level of responsibility.

(3) It creates an early warning system for potential problems, so that management can make

changes before things get out of hand.

4. (a) Disagree. Accounting information makes major contributions to the budgeting process. Accounting

provides the starting point of budgeting by providing historical data on revenues, costs, and

5. The budget period should be long enough to provide an attainable goal under normal business

conditions. The budget period should minimize the impact of seasonal and cyclical business

fluctuations, but it should not be so long that reliable estimates are impossible. The most common

budget period is one year.

6. Disagree. Long-range planning usually encompasses a period of at least five years. It involves

Questions Chapter 23 (Continued)

8. Budgetary slack is the amount by which a manager intentionally underestimates budgeted

revenues or overestimates budgeted expenses in order to make it easier to achieve budgetary

goals. Managers may have an incentive to create budgetary slack in order to increase the likelihood of

receiving a bonus, or decrease the likelihood of losing their job.

9. A master budget is a set of interrelated budgets that constitutes a plan of action for a specified

time period. The master budget is developed within the framework of a sales forecast.

15. (a) Manufacturing overhead rate based on direct labor cost is 48% [$198,000 + $162,000 =

$360,000; $360,000 ÷ (150,000 X 1/3 X $15/hr.) = 48%].

19. The three sections of a cash budget are: (1) cash receipts, (2) cash disbursements, and (3) financing.

The cash budget also shows the beginning and ending cash balances.

20. Cash collections are:

January—$600,000 X 40% = $240,000.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 23-1

Sales

Budget

Selling and

Administrative

Expense

Budget

BRIEF EXERCISE 23-2

PAIGE COMPANY

Sales Budget

For the Year Ending December 31, 2017

Quarter

1

2

3

4

Year

Expected

unit sales

10,000

14,000

15,000

18,000

57,000

BRIEF EXERCISE 23-3

PAIGE COMPANY

Production Budget

For the Six Months Ending June 30, 2017

Quarter

Six

Months

1

2

Expected unit sales

Add: Desired ending finished goods

10,000

3,500

a

14,000

3,750

c

BRIEF EXERCISE 23-4

PERINE COMPANY

Direct Materials Budget

For the Month Ending January 31, 2017

Units to be produced ………………………………………………. 4,000

Direct materials per unit …………………………………………. X 2

BRIEF EXERCISE 23-5

GUNDY COMPANY

Direct Labor Budget

For the Six Months Ending June 30, 2017

Quarter

Six

Months

1

2

Units to be produced

Direct labor time (hours) per unit

5,000

X 1.6

7,000

X 1.6

BRIEF EXERCISE 23-6

ROCHE INC.

Manufacturing Overhead Budget

For the Year Ending December 31, 2017

Quarter

1

2

3

4

Year

Total manufacturing overhead

Variable costs

$20,000

$25,000

$30,000

$35,000

$110,000

BRIEF EXERCISE 23-7

ELBERT COMPANY

Selling and Administrative Expense Budget

For the Year Ending December 31, 2017

Quarter

1

2

3

4

Year

Variable expenses

$24,000

$28,000

$32,000

$36,000

$120,000

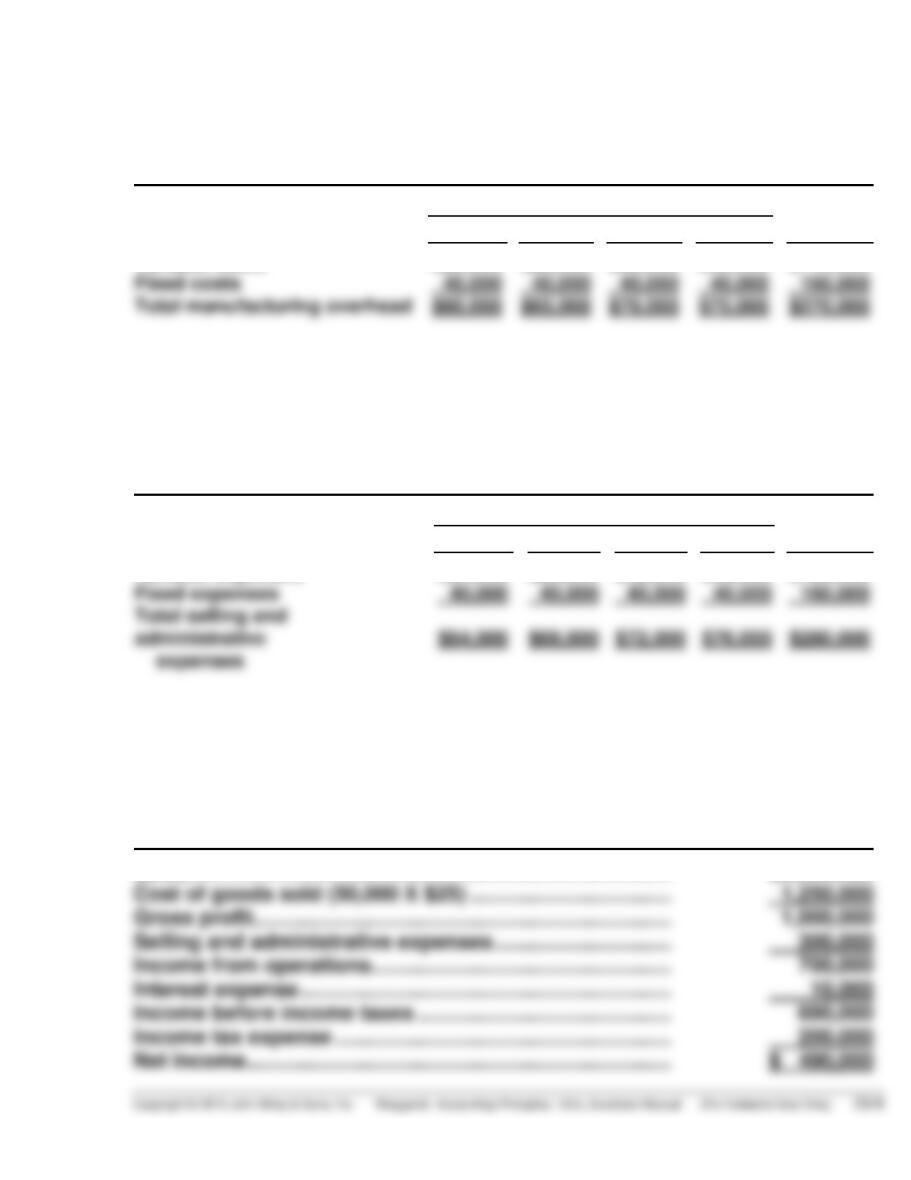

BRIEF EXERCISE 23-8

NORTH COMPANY

Budgeted Income Statement

For the Year Ending December 31, 2017

Sales ………………………………………………………………………. $2,250,000

Cost of goods sold (50,000 X $25) ……………………………. 1,250,000

Gross profit …………………………………………………………….. 1,000,000

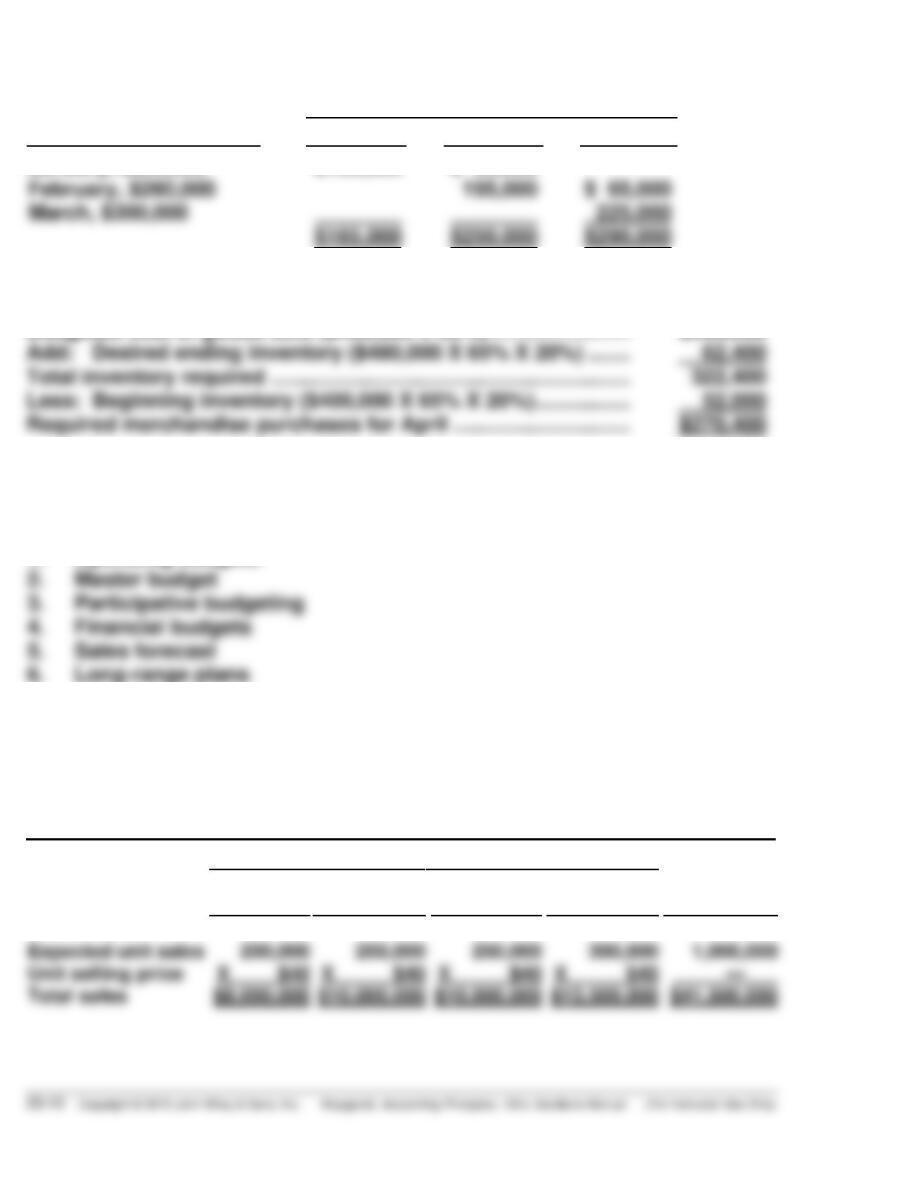

BRIEF EXERCISE 23-9

Collections from Customers

Credit Sales

January

February

March

January, $220,000

$165,000

$ 55,000

BRIEF EXERCISE 23–10

Budgeted cost of goods sold ($400,000 X 65%) …………………… $260,000

Add: Desired ending inventory ($480,000 X 65% X 20%) ……. 62,400

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 23-1

1. Operating budgets

2. Master budget

DO IT! 23-2

PARGO COMPANY

Sales Budget

For the Year Ending December 31, 2017

Quarter

1

2

3

4

Year

Expected unit sales

200,000

250,000

250,000

300,000

1,000,000

Total sales

DO IT! 23-2 (Continued)

PARGO COMPANY

Production Budget

For the Year Ending December 31, 2017

Quarter

1

2

3

4

Year

Expected unit sales

Add: Desired ending finished

goods units

200,000

62,500

250,000

62,500

250,000

75,000

300,000

60,000*

PARGO COMPANY

Direct Materials Budget

For the Year Ending December 31, 2017

Quarter

1

2

3

4

Year

Units to be produced

Direct materials per unit

Total pounds needed for

production

Add: Desired ending

direct materials

212,500

X 2

425,000

250,000

X 2

500,000

262,500

X 2

525,000

285,000

X 2

570,000

DO IT! 23-3

(a) Total unit cost:

Cost Element

Quantity

Unit Cost

Total

Direct materials …………………………

2 pounds

$12.00

$24.00

(b) PARGO COMPANY

Budgeted Income Statement

For the Year Ending December 31, 2017

Sales (1,000,000) units from sales budget, page 23–10 ….. $41,500,000

Cost of goods sold (1,000,000 X $34.50/unit) ……………… 34,500,000

DO IT! 23-4

BATISTA COMPANY

Cash Budget

April

Beginning cash balance…………………………………………………….. $ 25,000

Add: Cash receipts for April ……………………………………………… 245,000

Total available cash …………………………………………………………… 270,000

DO IT! 23-5

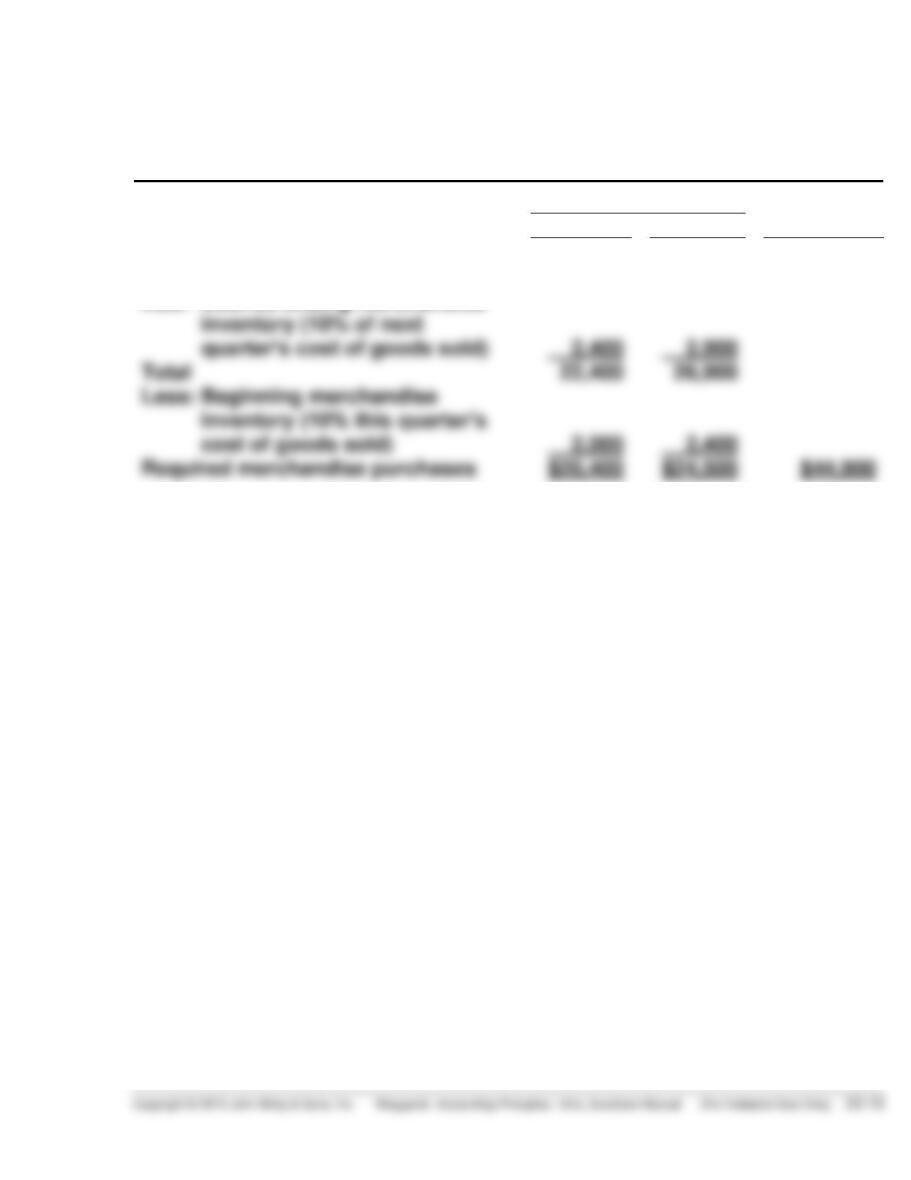

Zeller COMPANY

Merchandise Purchases Budget

For the Six Months Ending June 30, 2017

Quarter

Six

1

2

Months

Budgeted cost of goods sold

(Sales .50)

$20,000

$24,000

Total

Required merchandise purchases

Add: Desired ending merchandise

inventory (10% of next

SOLUTIONS TO EXERCISES

EXERCISE 23-1

MEMO

To Jim Dixon

From: Student

Re: Budgeting

I am glad Trusler Company is considering preparing a formal budget. There are

many benefits derived from budgeting, as I will discuss later in this memo.

A budget is a formal written statement of management’s plans for a specified

future time period, expressed in financial terms. The master budget gener–

The primary benefits of budgeting are:

1. It requires all levels of management to plan ahead and to formalize

goals on a recurring basis.

2. It provides definite objectives for evaluating performance at each

level of responsibility.

3. It creates an early warning system for potential problems, so that

management can make changes before things get out of hand.

4. It facilitates the coordination of activities within the business by cor–

EXERCISE 23-2

EDINGTON ELECTRONICS INC.

Sales Budget

For the Six Months Ending June 30, 2017

Quarter 1

Quarter 2

Six Months

Product

Units

Selling

Price

Total

Sales

Units

Selling

Price

Total

Sales

Units

Selling

Price

Total

Sales

XQ–103

20,000

$15

$300,000

22,000

$15

$330,000

42,000

$15

$ 630,000

THOME AND CREDE, CPAs

Sales Revenue Budget

For the Year Ending December 31, 2017

Quarter 1

Quarter 2

Quarter 3

Quarter 4

Billable

Billable

Total

Billable

Billable

Total

Billable

Billable

Total

Billable

Billable

Total

Dept.

Hours

Rate

Rev.

Hours

Rate

Rev.

Hours

Rate

Rev.

Hours

Rate

Rev.

Auditing

2,300

$ 80

$184,000

1,600

$ 80

128,000

2,000

$ 80

$160,000

2,400

$ 80

$192,000

Tax

3,000

90

270,000

2,200

90

198,000

2,000

90

180,000

2,500

90

225,000

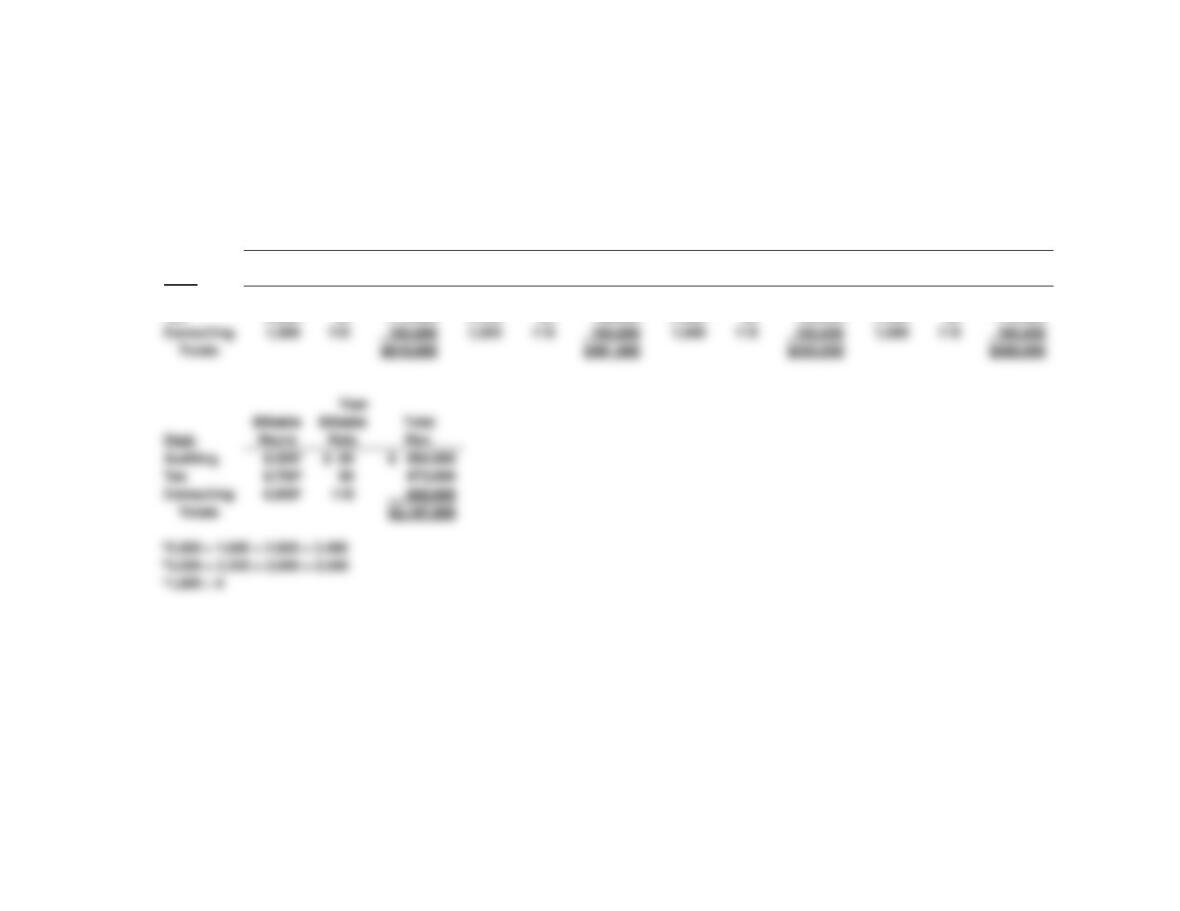

EXERCISE 23-3

1,500

1,500

1,500

1,500

$619,000

$491,000

$505,000

$582,000

Billable

Billable

Dept.

Hours

Rate

Auditing

$ 80

$ 664,000

$2,197,000

EXERCISE 23-4

TURNEY COMPANY

Production Budget

For the Year Ending December 31, 2017

Product HD-240

Quarter

1

2

3

4

Year

Expected unit sales

Add: Desired ending

finished goods units(1)

5,000

2,800

7,000

3,200

8,000

4,000

10,000

2,500

(2)

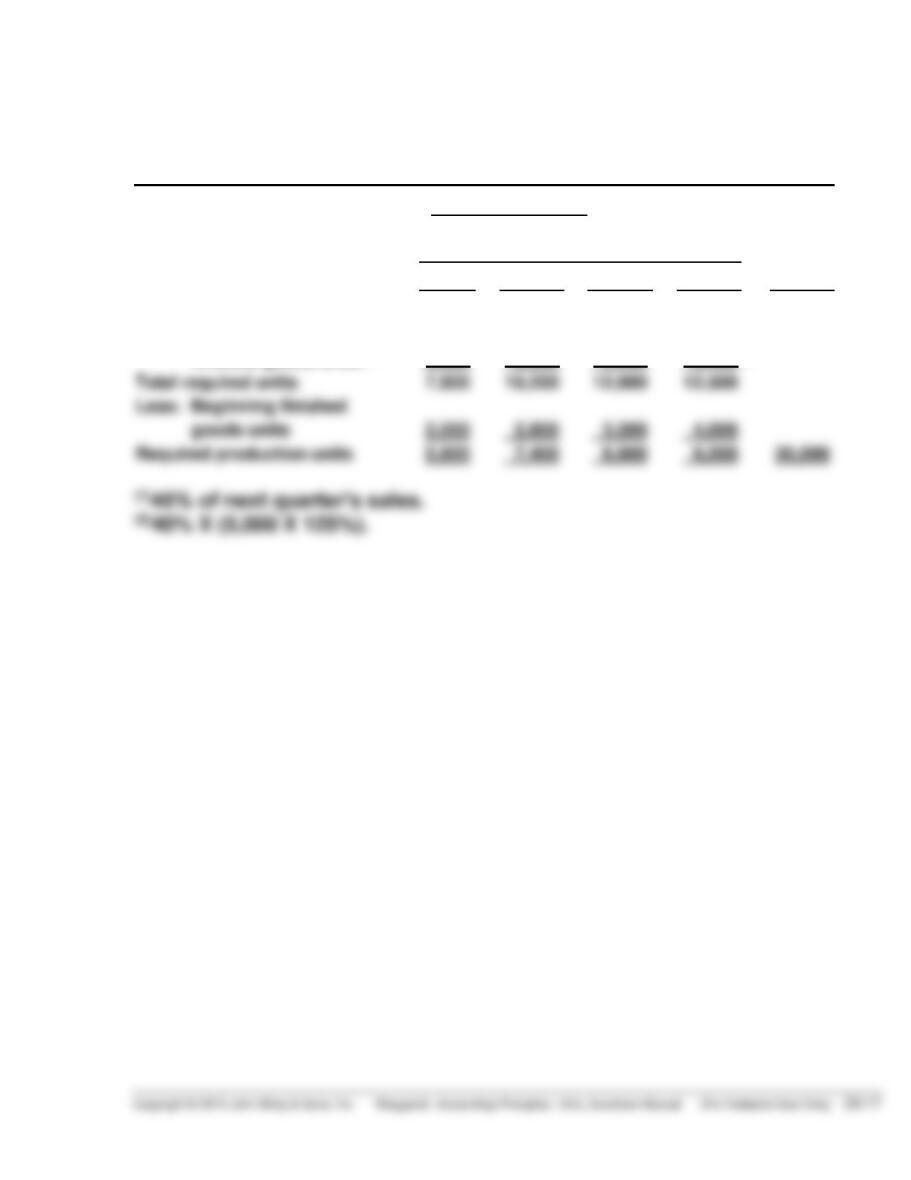

EXERCISE 23-5

DEWITT INDUSTRIES

Direct Materials Purchases Budget

For the Quarter Ending March 31, 2017

January

February

March

Units to be produced

Direct materials per unit

Total pounds needed for production

Add: Desired ending direct materials

10,000

X 2

20,000

8,000

X 2

16,000

5,000

X 2

10,000

EXERCISE 23-6

(a) HARDIN COMPANY

Production Budget

For the Six Months Ending June 30, 2017

Quarter

Six

Months

1

2

Expected unit sales

5,000

6,000

EXERCISE 23-6 (Continued)

(b) HARDIN COMPANY

Direct Materials Budget

For the Six Months Ending June 30, 2017

Quarter

Six

Months

1

2

$67,800

Units to be produced

Direct materials per unit

Total pounds needed for production

5,250

X 3

15,750

6,250

X 3

18,750

EXERCISE 23-7

Finished goods:

Sales ……………………………………………………………… 2,675

Plus: Ending inventory ……………………………………. 2,200

Total required …………………………………………………….. 4,875

Less: Beginning inventory ……………………………… 2,230

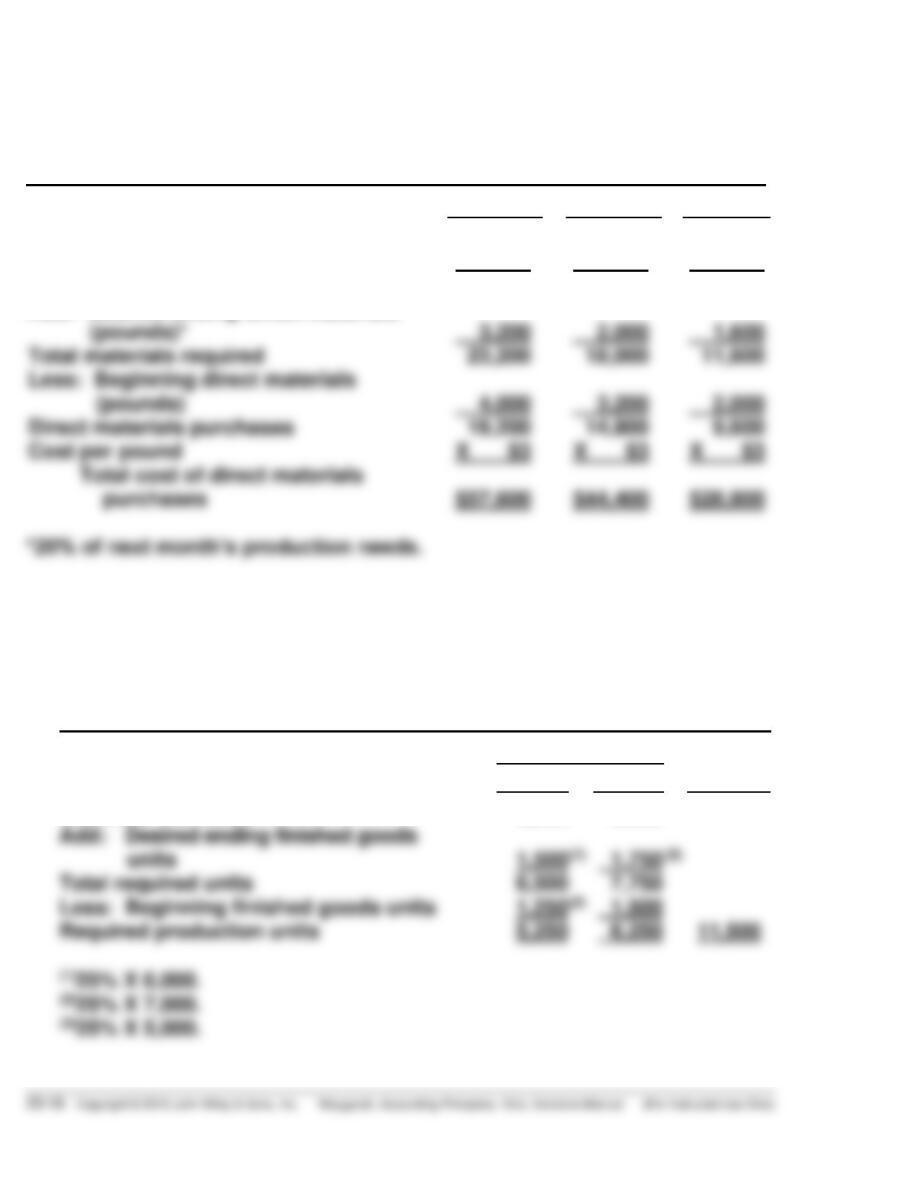

EXERCISE 23-8

(a) FUQUA COMPANY

Production Budget

For the Two Months Ending February 28, 2017

_____________________________________________________________

January

February

Expected unit sales ……………………………………..

10,000

12,000

Add: Desired ending finished goods

inventory …………………………………………..

2,400*

2,600***

Total required units ……………………………………..

12,400

14,600

10,400

12,200

(b) FUQUA COMPANY

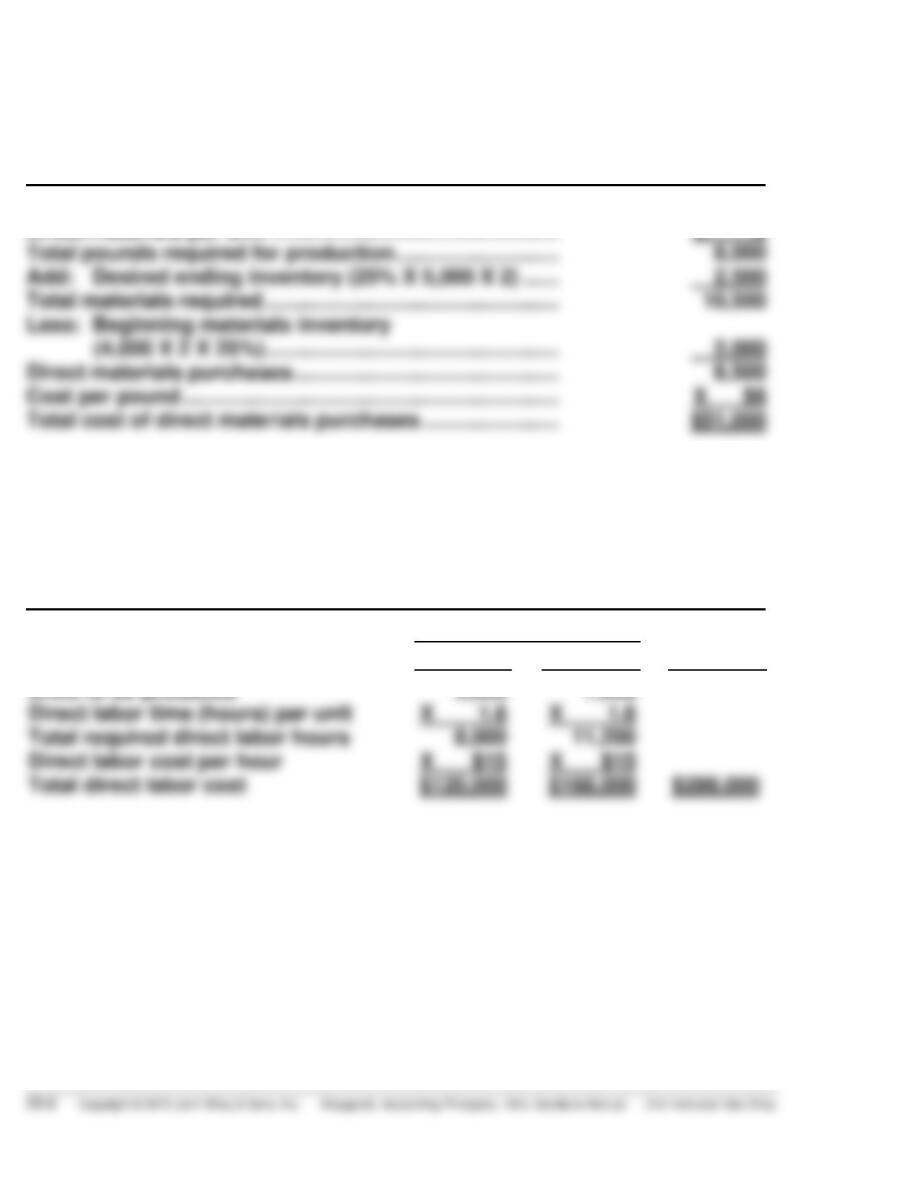

Direct Materials Budget

For the Month Ending January 31, 2017

_____________________________________________________________

January

Units to be produced ……………………………………………………

10,400

Direct material pounds per unit …………………………………….

X 4

Total pounds needed for production …………………………..…

41,600

Add: desired pounds in ending materials inventory ………

19,520*

Total materials required ……………………………………………….

61,120

Less: beginning direct materials (pounds) …………………….

Direct materials purchases …………………………………………..

44,480

Cost per pound …………………………..……………………………….

X $2

Total cost of direct materials purchases ………………………..

$88,960