CHAPTER 23 Performance Evaluation for Decentralized Operations

Prob. 23–3B (FIN MAN); Prob. 8–3B (MAN)

1.

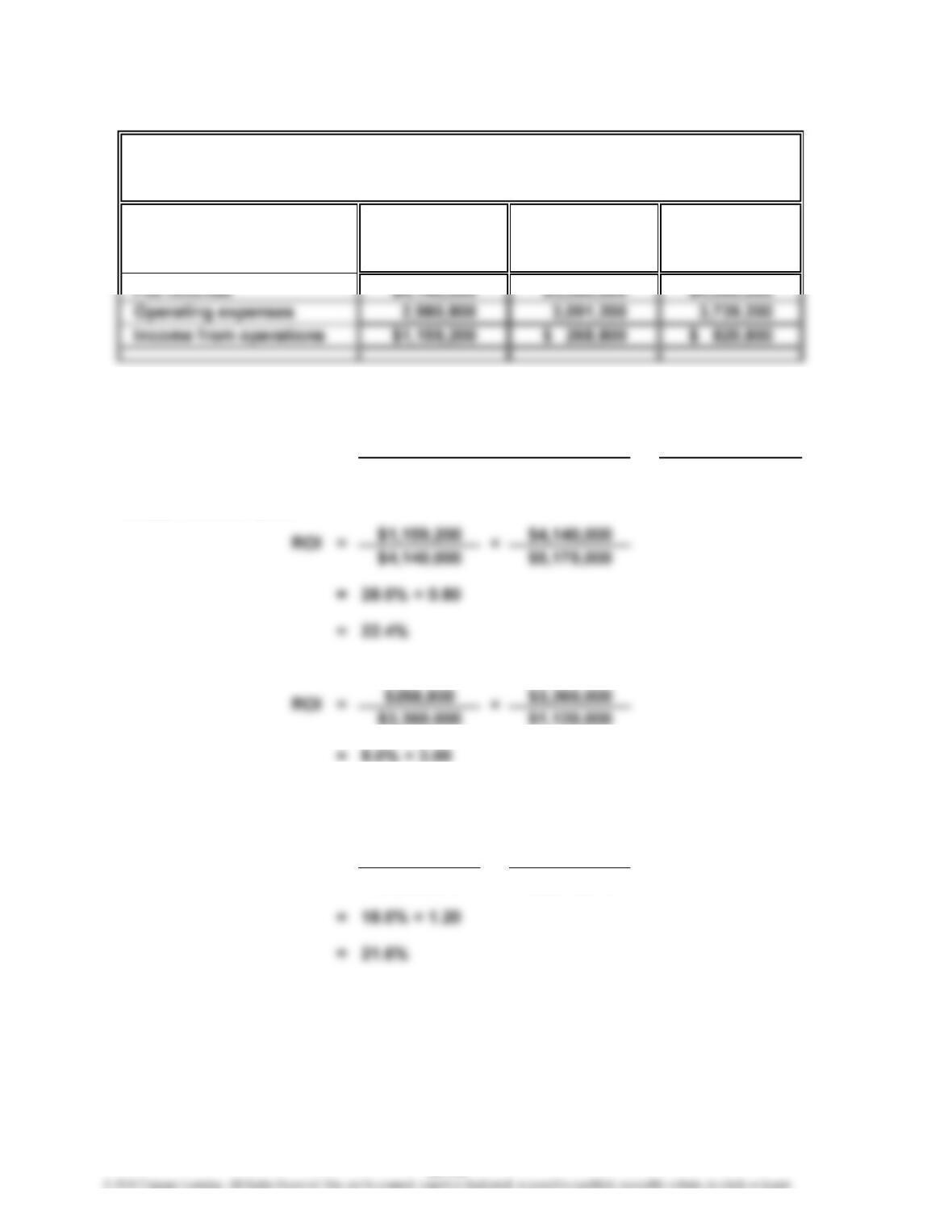

Mutual Fund Division:

Electronic Brokerage Division:

= 24.0%

Investment Banking Division:

$820,800 $4,560,000

$4,560,000 $3,800,000

ROI = ×

Division Division Division

=

Rate of Return

on Investment

2. Rate of Return

on Investment = Profit Margin × Investment Turnover

E.F. LYNCH COMPANY

Divisional Income Statements

For the Year Ended June 30, 2016

Mutual

Fund

Electronic

Brokerage

Investment

Banking

Income from Operations

×

Sales Invested Assets

Sales

23-36

CHAPTER 23 Performance Evaluation for Decentralized Operations

Prob. 23–3B (FIN MAN); Prob. 8–3B (MAN) (Concluded)

3. Per dollar of invested assets, the Electronic Brokerage Division is the most

profitable of the three divisions. Assuming that the rates of return on

investments do not change in the future, an expansion of the Electronic

Brokerage Division will return 24 cents (24%) on each dollar of invested assets,

23-37

CHAPTER 23 Performance Evaluation for Decentralized Operations

Prob. 23–4B (FIN MAN); Prob. 8–4B (MAN)

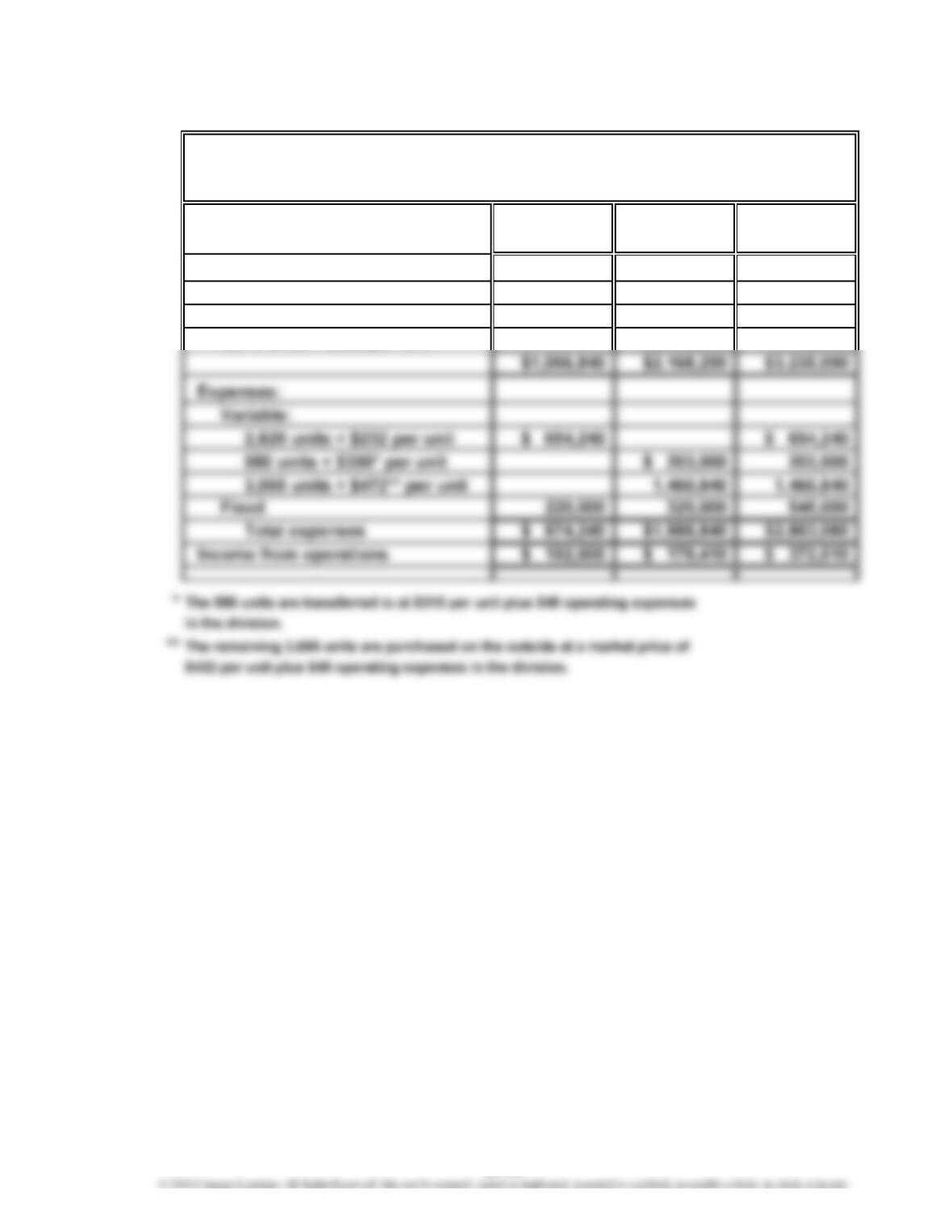

Electronics Division:

$126,000 $1,575,000

$1,575,000 $1,050,000

2.

Sales

Cost of goods sold

1

$891,000 – $31,400

2

$1,050,000 – $300,000

3

$1,575,000 – $180,000

859,600

$1,575,000

Proposal 3

$1,575,000

ROI =

×

Proposal 1

For the Year Ended December 31, 2016

Proposal 2

GIHLBI INDUSTRIES INC.—ELECTRONICS DIVISION

Estimated Income Statements

1. =

771,450 702,000

$1,395,000

Profit Margin × Investment Turnover

Rate of Return

on Investment

1

3

4

7

23-38

CHAPTER 23 Performance Evaluation for Decentralized Operations

Prob. 23–4B (FIN MAN); Prob. 8–4B (MAN) (Concluded)

$157,400 $1,575,000

$1,575,000 $750,000

$125,550 $1,395,000

$1,395,000 $937,500

$315,000 $1,575,000

$1,575,000 $1,968,750

4. Proposal 1 would yield a rate of return on investment of 21.0%.

5.

=

3. = Profit Margin × Investment Turnover

8% × Required Investment Turnover

ROI =

Rate of Return

on Investment

Rate of Return

on Investment

20%

×

×

×

Profit Margin × Required Investment Turnover

ROI =

ROI =

=

Proposal 1:

Proposal 2:

Proposal 3:

23-39

CHAPTER 23 Performance Evaluation for Decentralized Operations

Prob. 23–5B (FIN MAN); Prob. 8–5B (MAN)

1.

Sales

Cost of goods sold

Road Bike Division:

Mountain Bike Division:

$123,200 $1,760,000

$1,760,000 $800,000

3. Road Bike Division: $28,800 [$172,800 – ($1,440,000 × 10%)]

$1,760,000

1,380,000 1,400,000

FREE RIDE BIKE COMPANY

Divisional Income Statements

For the Year Ended December 31, 2016

BikeBike

Road Mountain

Division Division

$1,728,000

2. = Profit Margin × Investment Turnover

Rate of Return

on Investment

ROI = ×

Rate of Return

on Investment

Invested Assets

=SalesIncome from Operations ×

Sales

23-40

CHAPTER 23 Performance Evaluation for Decentralized Operations

Prob. 23–5B (FIN MAN); Prob. 8–5B (MAN) (Concluded)

4. On the basis of income from operations, the Road Bike Division generated

$49,600 ($172,800 – $123,200) more income from operations than did the Mountain

Bike Division. However, income from operations does not consider the amount of

invested assets in each division. On the basis of the rate of return on investment,

23-41

CHAPTER 23 Performance Evaluation for Decentralized Operations

Prob. 23–6B (FIN MAN); Prob. 8–6B (MAN)

1. No. When unused capacity exists in the supplying division (the Semiconductors

2. The Semiconductors Division’s income from operations would increase by

$45,240:

By selling to the Navigational Systems Division, the Semiconductors Division

earns $78 per unit on these sales.

The Navigational Systems Division’s income from operations would increase

by $70,760:

Exoplex Industries Inc.’s total income from operations would increase by

$116,000:

23-42

CHAPTER 23 Performance Evaluation for Decentralized Operations

Prob. 23–6B (FIN MAN); Prob. 8–6B (MAN) (Continued)

3.

Semi- Navigational

conductors Systems Total

Sales:

2,240 units × $396 per unit $ 887,040 $ 887,040

580 units × $310 per unit 179,800 179,800

3,675 units × $590 per unit $2,168,250 2,168,250

EXOPLEX INDUSTRIES INC.

Divisional Income Statements

For the Year Ended December 31, 2016

23-43

CHAPTER 23 Performance Evaluation for Decentralized Operations

Prob. 23–6B (FIN MAN); Prob. 8–6B (MAN) (Concluded)

4. The Semiconductors Division’s income from operations would increase by

$62,640:

Increase in Semiconductors Variable

(Supplying) Division’s Transfer Cost Units

By selling to the Navigational Systems Division, the Semiconductors Division

earns $108 per unit on these sales.

The Navigational Systems Division’s income from operations would increase

by $53,360:

Increase in Navigational Systems

By purchasing from the Semiconductors Division, the Navigational Systems

Division saves $92 per unit on its purchases.

Exoplex Industries Inc.’s total income from operations would increase by the

same amount as in (2), $116,000:

5. a. Any transfer price greater than the Semiconductors Division’s variable

expenses per unit of $232 but less than the market price of $432 would be

acceptable.

b. If the division managers cannot agree on a transfer price, a price of $332*

would be the best compromise. In this way, each division’s income from

operations would increase by $58,000.

23-44

CHAPTER 23 Performance Evaluation for Decentralized Operations

CP 23–1 (FIN MAN); CP 8–1 (MAN)

This scenario is a negotiation between two divisions. Dave is not behaving

unethically by attempting to get a better price from the Semiconductor Division than

from the market. He is not behaving unethically because he refuses market price. This

may not seem “fair,” but price negotiation is a very typical business activity and is part

of Dave’s job. It would be unethical only if the X-ray Division refused to deal with the

CASES & PROJECTS

CHAPTER 23 Performance Evaluation for Decentralized Operations

CP 23–2 (FIN MAN); CP 8–2 (MAN)

The Customer Service Department head is responsible for the quantity of service but

not the source of the service (i.e., not the price). Most accountants would hold the

department head responsible for the cost by transferring the cost of the brochures to

the Customer Service Department, even though the price is 25% higher than could be

23-46

CHAPTER 23 Performance Evaluation for Decentralized Operations

CP 23–3 (FIN MAN); CP 8–3 (MAN)

1. The rate of return on invested assets is computed as follows:

Snack Frozen

Goods Cereal Foods

Income from operations……………

…

$ 396,000 $ 554,400 $ 420,000

2. Not all projects that have greater than a 19% rate of return would be accepted.

This is because all three divisions have an ROI that is greater than 19%. Thus, any

3. There are two approaches to improving ROI: (1) improving the profit margin or

(2) improving the investment turnover. For all three divisions, the profit margin

is excellent:

Snack Goods 18% ($396,000 ÷ $2,200,000)

Cereal 22% ($554,400 ÷ $2,520,000)

CHAPTER 23 Performance Evaluation for Decentralized Operations

CP 23–4 (FIN MAN); CP 8–4 (MAN)

1. 2014 2015 2016

2. 2014 2015 2016

3. 2014 2015 2016

4. Anna is concerned about the Norsk Division because the return on investment

appears to be deteriorating over the 2014–2016 operating periods. This is

happening even though the profit margin is increasing over this time period. In

order for this to occur, the investment turnover must be dropping, which is the

case in part (2).

The investment turnover is dropping faster than the profit margin is increasing,

causing the rate of return on investment to drop. It appears as though the Norsk

23-48

CHAPTER 23 Performance Evaluation for Decentralized Operations

CP 23–5 (FIN MAN); CP 8–5 (MAN)

2. $64,000 (8.0 × $8,000 = $64,000, where 8.0 = 18.0% – 10.0%)

or

4. Even though the addition of the new product line would increase the overall

company rate of return on investment, its addition would decrease the Specialty

Rate of Return

on Investment =

Sales

Invested Assets

Income from Operations ×

Sales

3. Rate of Return

on Investment =Income from Operations

Invested Assets

1. =Invested Assets

Income from Operations

Rate of Return

on Investment

Rate of Return

on Investment =Income from Operations × Sales

Sales Invested Assets

CHAPTER 23 Performance Evaluation for Decentralized Operations

CP 23–5 (FIN MAN); CP 8–5 (MAN) (Concluded)

5. Use of residual income as a performance measure and as the basis for granting

bonuses would motivate division managers to accept investment opportunities

that exceed a minimum rate of return. If the minimum rate of return was set at

10%, the overall company average rate of return, any investment opportunity

whose rate exceeded 10% would be viewed as acceptable. If this performance

measure had been used, the Specialty Products Division manager would have

increased the division’s residual income by $892,800 through the addition of the

new product line, as shown below.

The manager’s bonus could then be calculated as a percent of residual income. In

this case, a bonus equal to 3% of residual income would achieve a bonus similar

to the initial plan:

Income from operations………………………………………………………… $4,860,000

Less: Minimum desired income (10% × $27,000,000)……………………

…

2,700,000

Residual income…………………………………………………………………

…

$2,160,000

…

…

…