CHAPTER 23 Evaluating Variances from Standard Costs

Ex. 23-15

Direct labor hours 18,000 20,000 22,000

V

ariable overhead cost:

Indirect factory labor $162,000 $180,000 $198,000

Power and light 10,800 12,000 13,200

Indirect materials 57,600 64,000 70,400

1

($180,000 ÷ 20,000) × 18,000 units

For the Month Ended November 30

Leno Manufacturing Company

Factory Overhead Cost Budget—Press Department

1

2

3

CHAPTER 23 Evaluating Variances from Standard Costs

Ex. 23-16

a.

Direct labor hours 9,000 10,000 11,000

b. Overhead applied at actual production:

Actual hours……………………………………………………………………

…

9,000

× Overhead application rate*…………………………………………………

…

$ 10.50

Factory overhead applied……………………………………………………

…

$94,500

*Total factory overhead rate to be applied to production:

V

ariable factory overhead…………………………………………… $ 4.50

Wiki Wiki Company

Monthly Factory Overhead Cost Budget—Fabrication Department

CHAPTER 23 Evaluating Variances from Standard Costs

Ex. 23-17

Variable factory overhead controllable variance:

Actual variable factory overhead cost incurred……

…

$192,000

Less budgeted variable factory overhead

for 15,600 hrs. [15,600 × ($20.00 – $8.00)]…………… 187,200

V

ariance—unfavorable………………………………

…

$4,800

Fixed factory overhead volume variance:

Productive capacity at 100%……………………………

…

16,000 hrs.

*

Actual Overhead – Applied Overhead = Total Overhead Variance:

($192,000 + $128,000) – $312,000 = $8,000

Actual costs 320,000 Applied costs 312,000

Balance (underapplied) 8,000

Actual Applied

Factory Factory

Overhead Overhead

Produced

Overhead for Amount

Alternative Computation of Overhead Variances

Factory Overhead

Budgeted Factory

V

…

CHAPTER 23 Evaluating Variances from Standard Costs

Ex. 23-18

a. Controllable variance:

Actual variable factory overhead

b. Volume variance:

V

olume at 100% of normal capacity…………………………

…

100,000

Less standard hours…………………………………………… 92,500

Idle capacity……………………………………………………

…

7,500

× Fixed overhead rate

2

…………………………………………

…

$2.40

V

olume variance—unfavorable………………………………

…

18,000

Total factory overhead cost

variance—unfavorable………………………………………

…

$ 5,000

3

×

1

CHAPTER 23 Evaluating Variances from Standard Costs

Ex. 23-18 (Concluded)

Actual costs 782,000 Applied costs 777,000

Balance (underapplied) 5,000

Applied

Factory

Overhead

Alternative Computation of Overhead Variances

Factory Overhead

Budgeted Factory

Produced

Actual

Factory

Overhead

Overhead for Amount

*

CHAPTER 23 Evaluating Variances from Standard Costs

Ex. 23-19

In determining the volume variance, the productive capacity overemployed (2,000

hours) should be multiplied by the standard fixed factory overhead rate of $3.80

the total factory overhead rate of $7.30 per hour and reported it as unfavorable.

A correct determination of the factory overhead cost variances is as follows:

Variable factory overhead controllable variance:

Actual variable factory overhead cost incurred……

…

$458,000

Budgeted variable factory overhead for

132,000 hours (132,000 × $3.50)……………………

…

462,000

V

ariance—favorable…………………………………

…

$ (4,000)

Fixed factory overhead volume variance:

V

…

Total factory overhead cost variance—favorable……

…

$(11,600)

Actual costs 952,000 Applied costs 963,600

($458,000 + $494,000) [($3.50 + $3.80) × 132,000]

Balance (overapplied) 11,600

Actual Applied

Factory Factory

Overhead Overhead

Produced

Overhead for Amount

Alternative Computation of Overhead Variances

Factory Overhead

Budgeted Factory

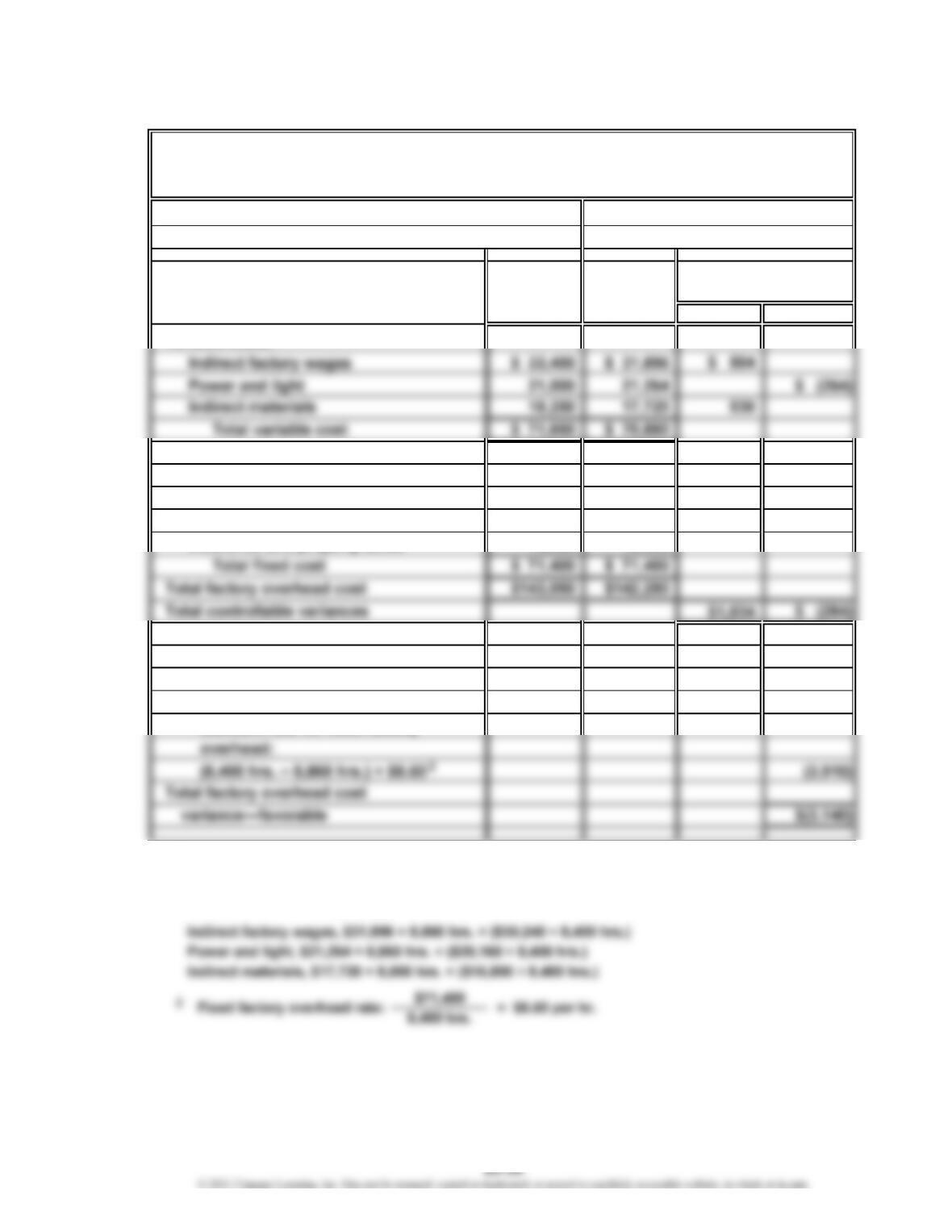

CHAPTER 23 Evaluating Variances from Standard Costs

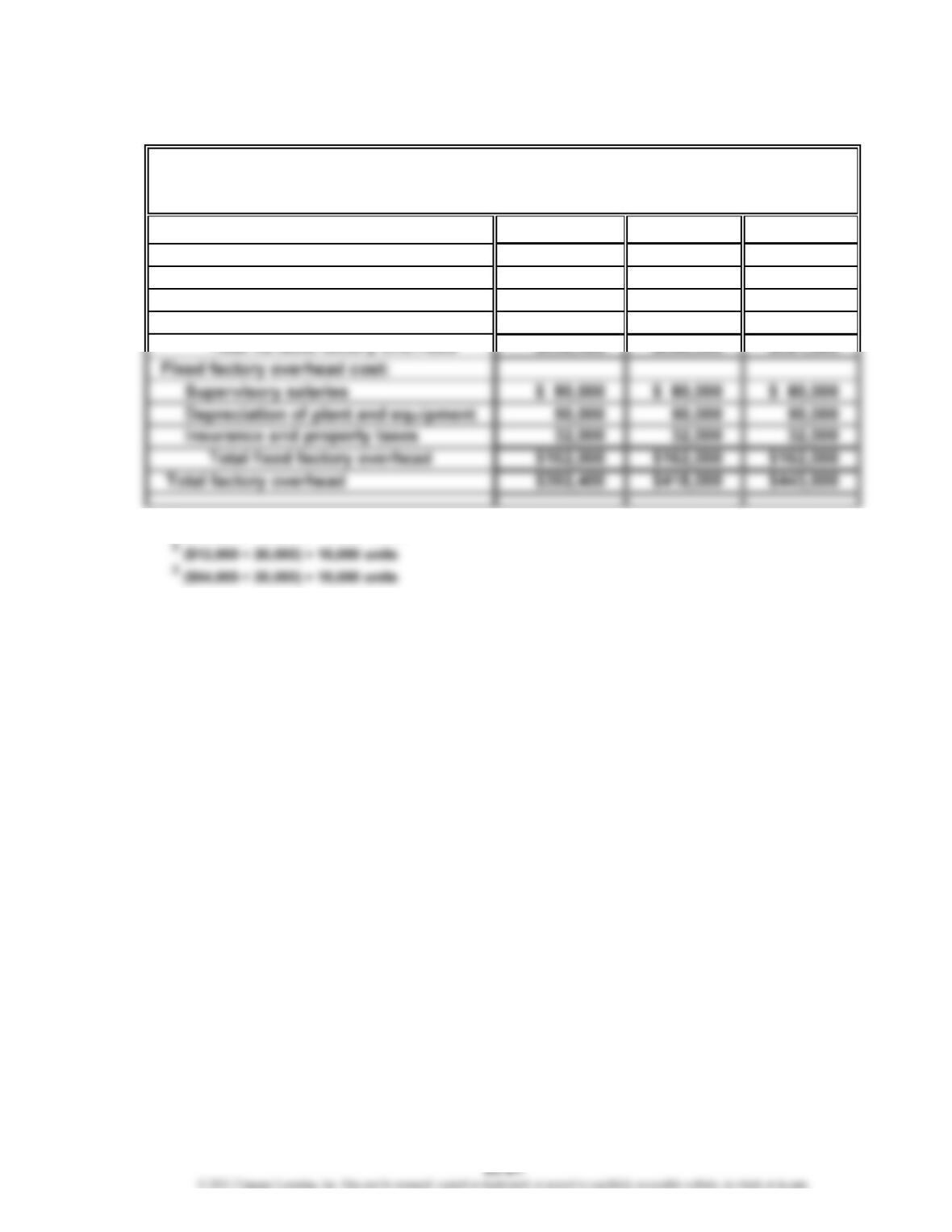

Ex. 23-20

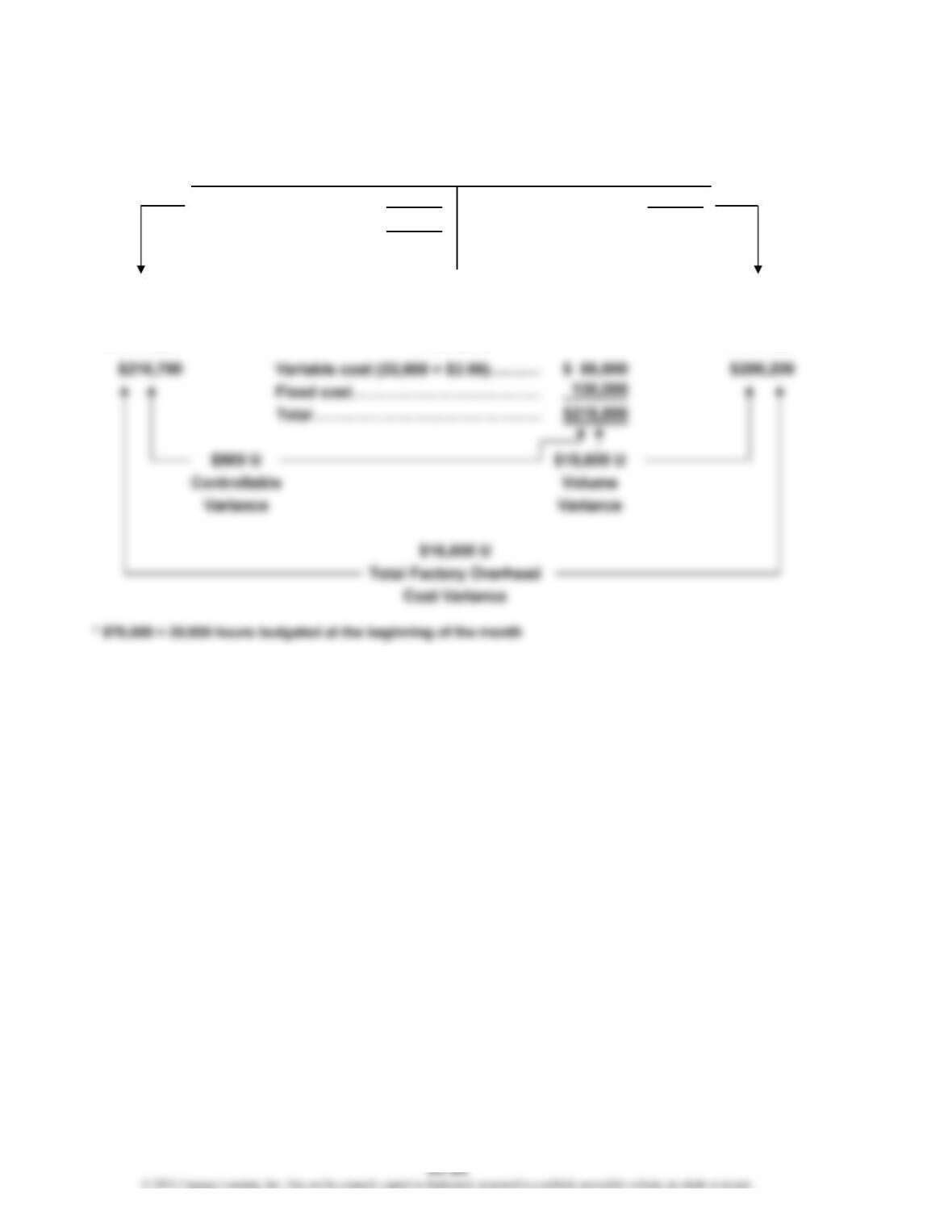

Productive capacity for the month 25,000 hrs.

Actual productive capacity used for the month 22,000 hrs.

Budget

(at actual

Total variable factory

overhead cost $ 86,700 $ 85,800

Fixed factory overhead costs:

Supervisory salaries $ 54,500 $ 54,500

Depreciation of plant and

equipment 40,000 40,000

Net controllable variance—unfavorable $ 900

Volume variance—unfavorable:

Idle hours at the standard rate

for fixed factory overhead:

(25,000 hrs. – 22,000 hrs.) × $5.20 15,600

Total factory overhead cost

variance—unfavorable $16,500

1

The budgeted variable factory overhead costs are determined by multiplying

22,000 hours by the variable factory overhead cost rate for each variable cost

category. These rates are determined by dividing each budgeted amount

(estimated at the beginning of the month) by the planned (budgeted) volume

of 20,000 hours. Thus, for example:

Tannin Products Inc.

Factory Overhead Cost Variance Report—Trim Department

For the Month Ended July 31

Variances

2

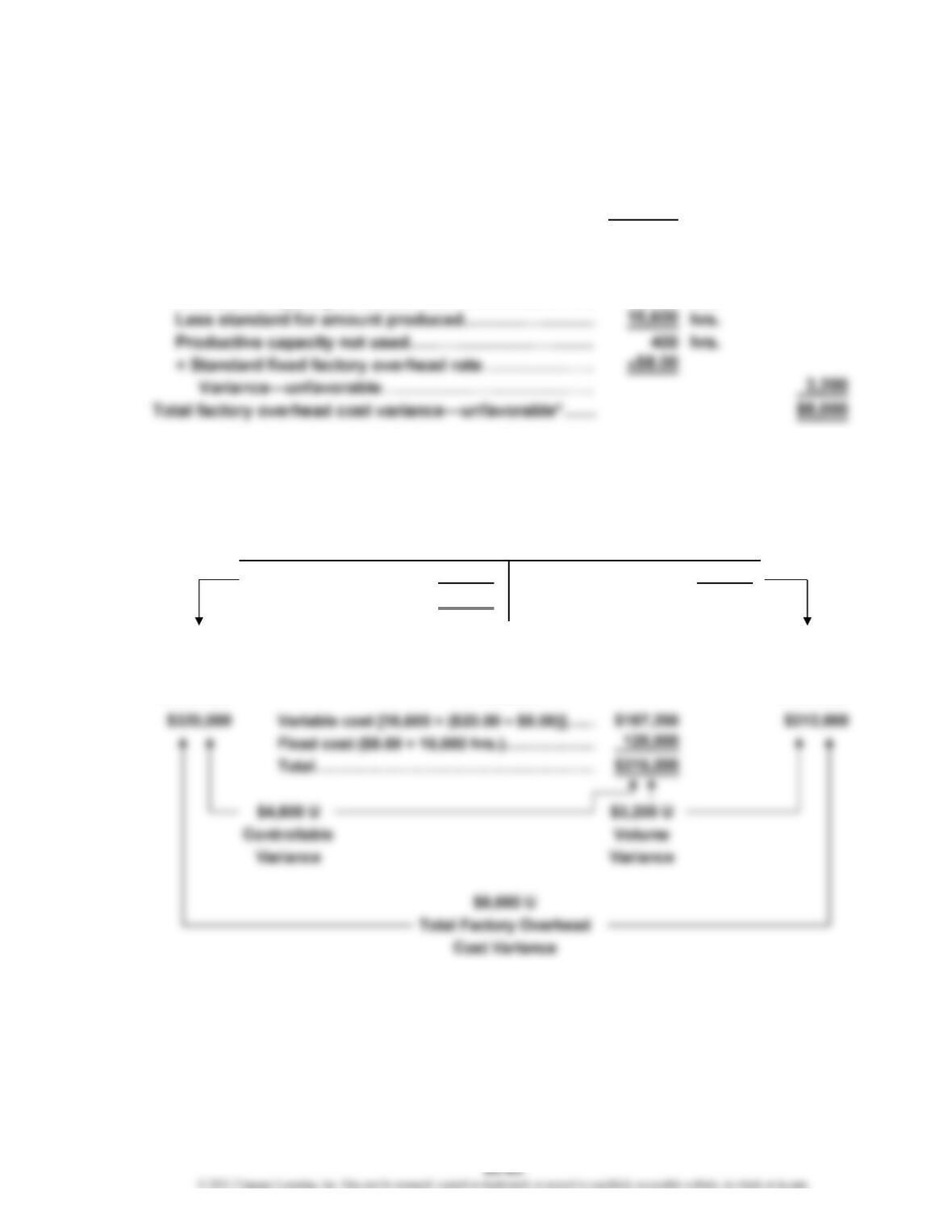

CHAPTER 23 Evaluating Variances from Standard Costs

Ex. 23-20 (Concluded)

Actual costs 216,700 Applied costs 200,200

Balance (underapplied) 16,500 [22,000 × ($3.90* + $5.20)]

Actual Applied

Factory Factory

Overhead Overhead

Produced

Overhead for Amount

Alternative Computation of Overhead Variances

Factory Overhead

Budgeted Factory

CHAPTER 23 Evaluating Variances from Standard Costs

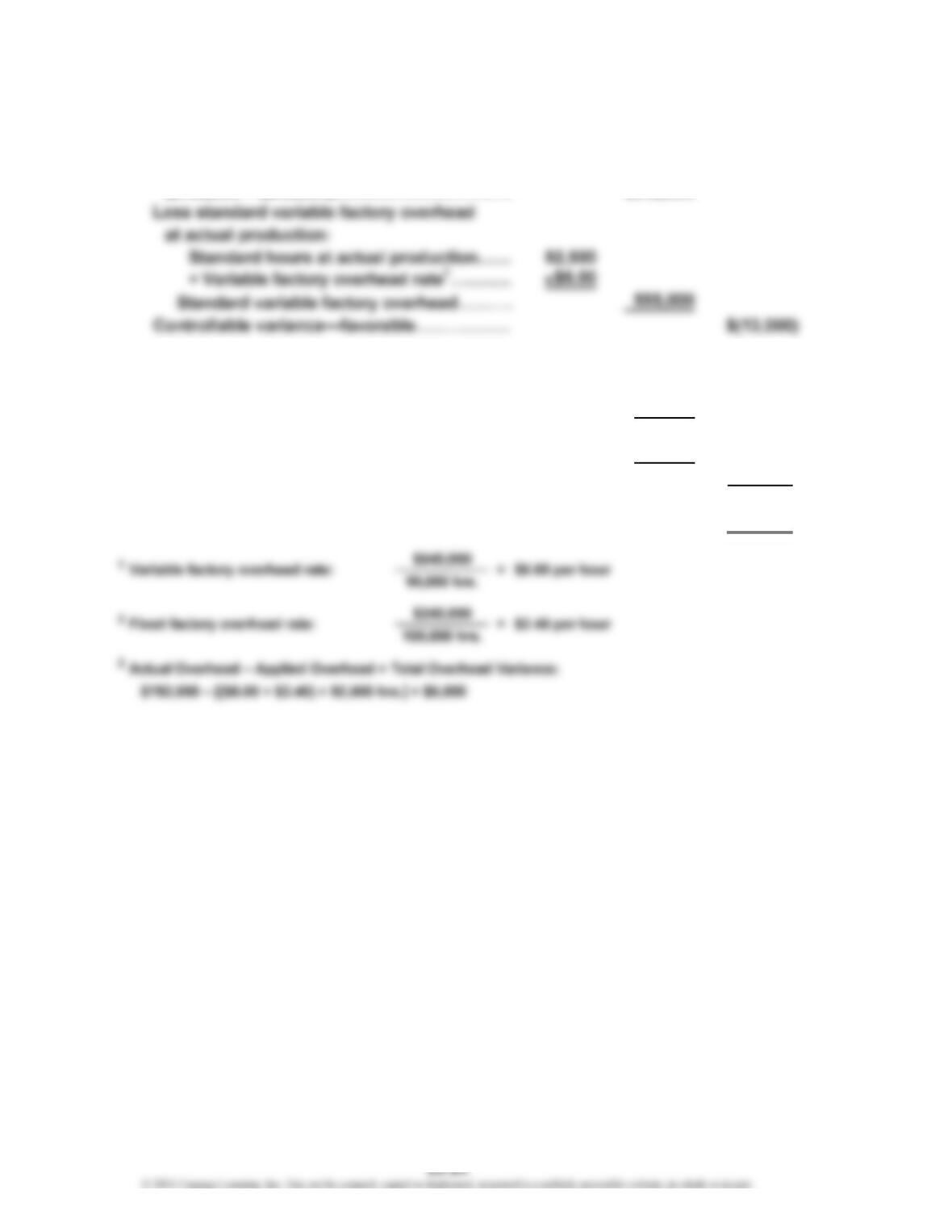

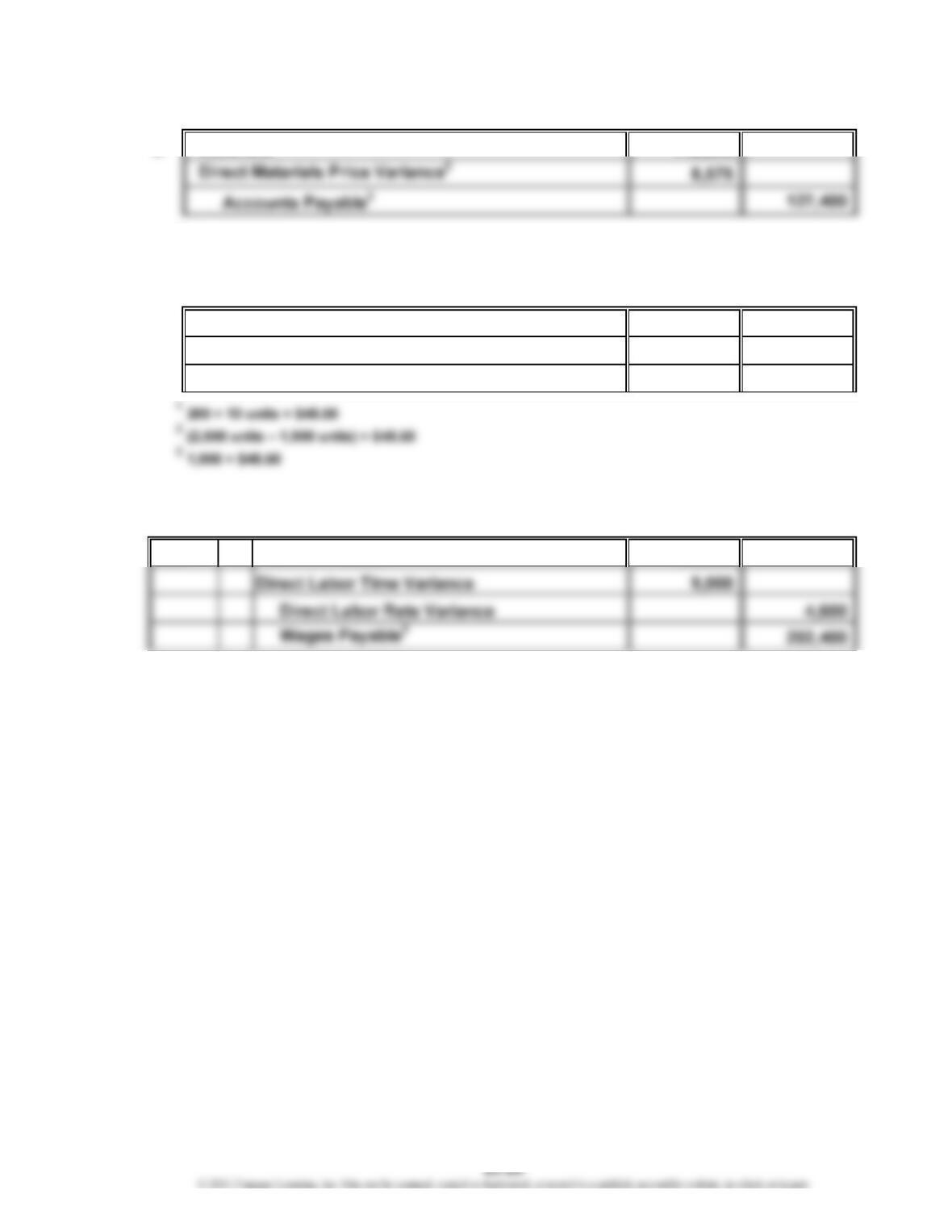

Ex. 23-21

12,450 × $48.50

22,450 × $3.50 ($52.00 – $48.50)

32,450 × $52.00

b. Work in Process197,000

Direct Materials Quantity Variance24,850

Materials392,150

Ex. 23-22

31 Work in Process1198,000

15,000 × 2.20 hrs. × $18.00

Direct labor time variance: (11,500 – 11,000) × $18.00 = $9,000 U

Direct labor rate variance: ($17.60 – $18.00) × 11,500 = $(4,600) F

211,500 hours × $17.60 per hour

Mar.

CHAPTER 23 Evaluating Variances from Standard Costs

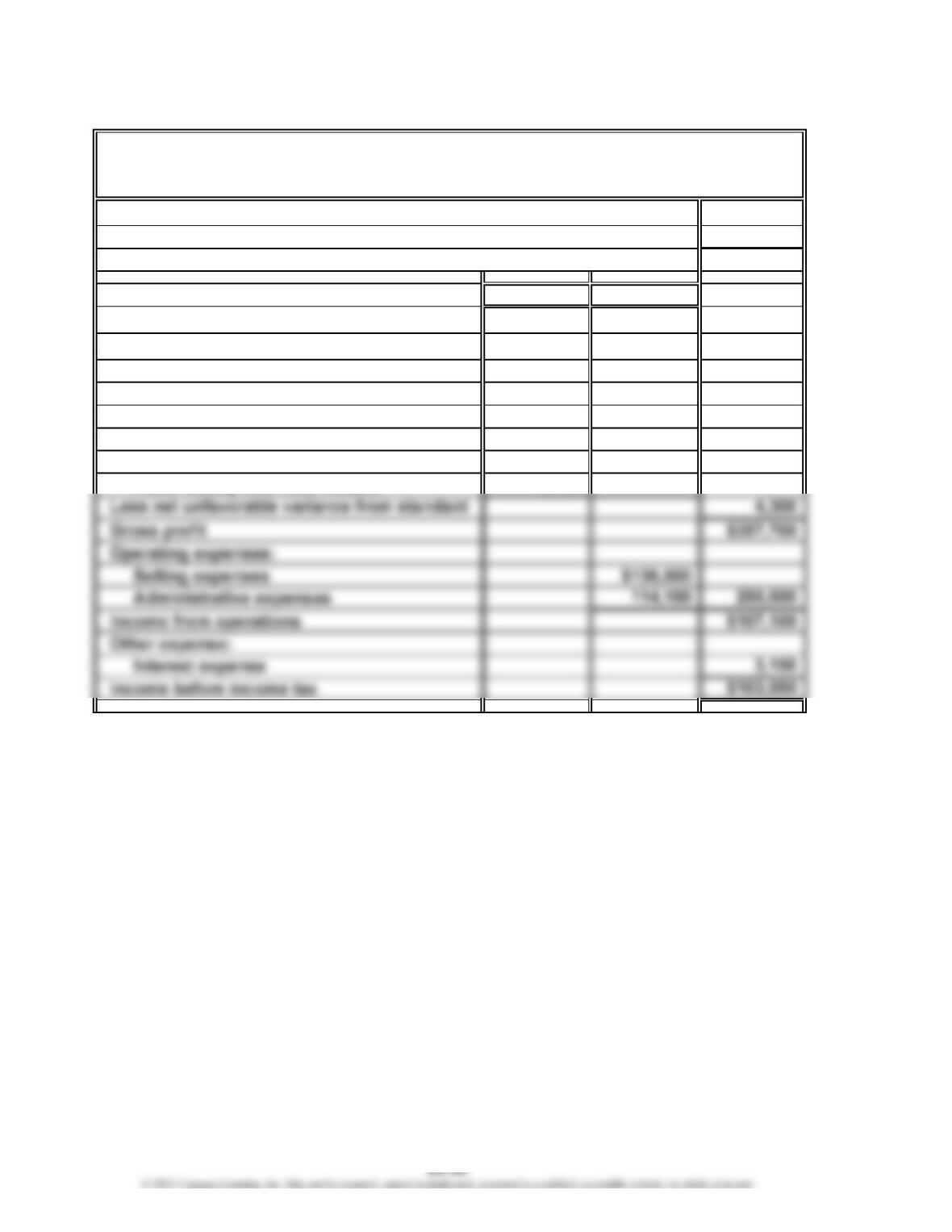

Ex. 23-23

Sales $996,000

Cost of goods sold—at standard 634,000

Gross profit—at standard $362,000

Unfavorable (Favorable)

Variance adjustments to gross profit

at standard:

Direct materials price $1,830

Direct materials quantity $ (720)

Direct labor rate (1,240)

Direct labor time 490

Variable factory overhead controllable (250)

Arseneault Company

Income Statement

For the Month Ended December 31

CHAPTER 23 Evaluating Variances from Standard Costs

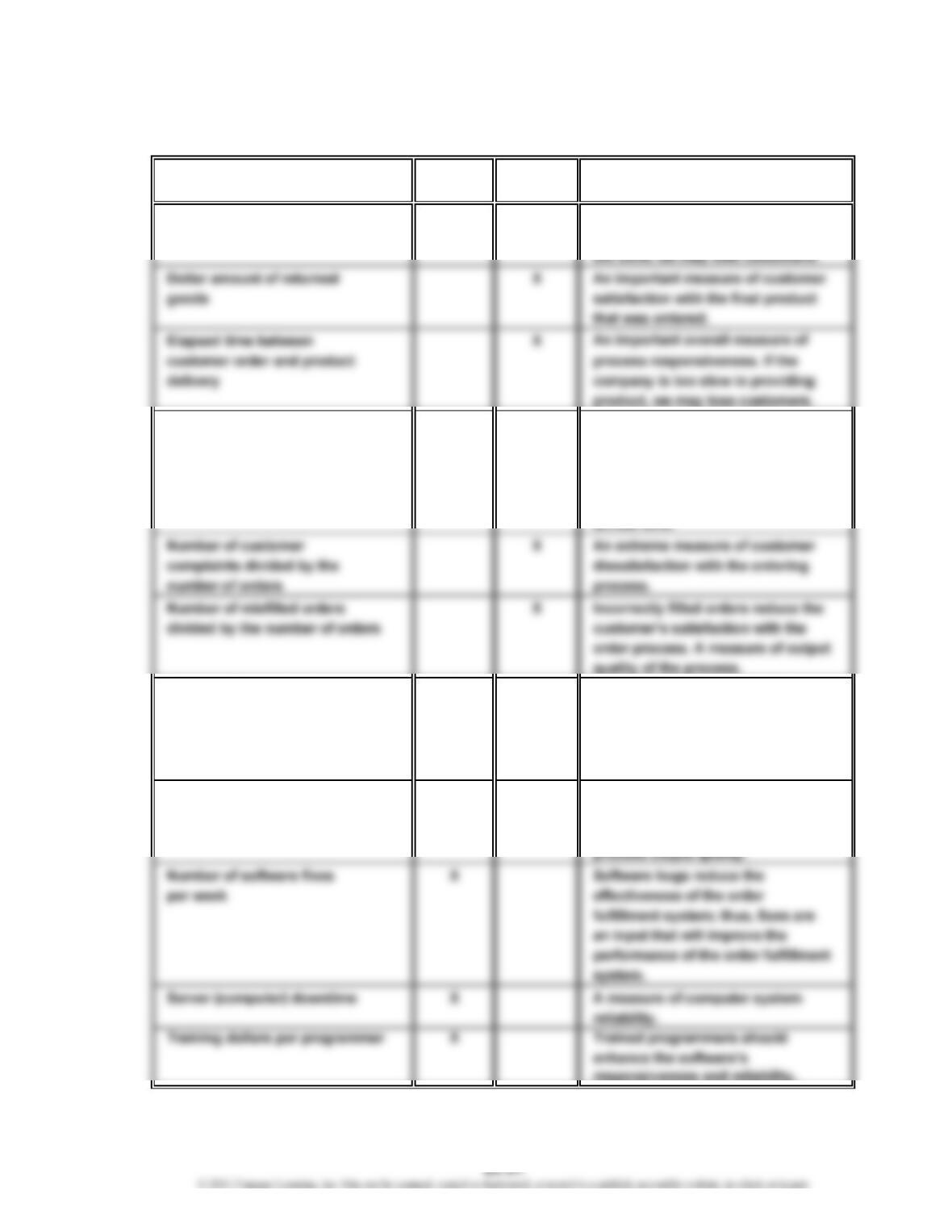

Ex. 23-24

a. and b.

Average computer response X A measure of the speed of the

time to customer “clicks” ordering process. If the speed is

Maintenance dollars divided X A driver of the ordering system’s

by hardware investment reliability and downtime. The

maintenance dollars should be

divided by the amount of hardware

in order to facilitate comparison

Number of orders per X This measure is related to the

warehouse employee capacity of the warehouse relative

to the demands placed upon it.

This relationship will impact the

delivery cycle time.

Number of page faults or X The page errors will negatively

errors due to software impact the customer’s ordering

programming errors experience. It’s a measure of

responsiveness and reliability.

Explanation

Input

Measure

Output

Measure

CHAPTER 23 Evaluating Variances from Standard Costs

Ex. 23-25

a. Possible Input Measures

Registration staffing per student

Technology investment per period for registration process

Training hours per registration personnel

Amount of faculty staffing

Possible Output Measures

Cycle time for a student to register for classes

Number of times a course is unavailable

Number of separate registration events or steps (log-ons or line waits)

per student

Number of times a replacement course was used by a student

Number of registration errors

b. Alpha University is interested in not only the efficiency of the process but

also the quality of the process. This means that the process must meet multiple

objectives. The college wants this process to meet the needs of students,

which means it should not pose a burden to students. Students should be able

CHAPTER 23 Evaluating Variances from Standard Costs

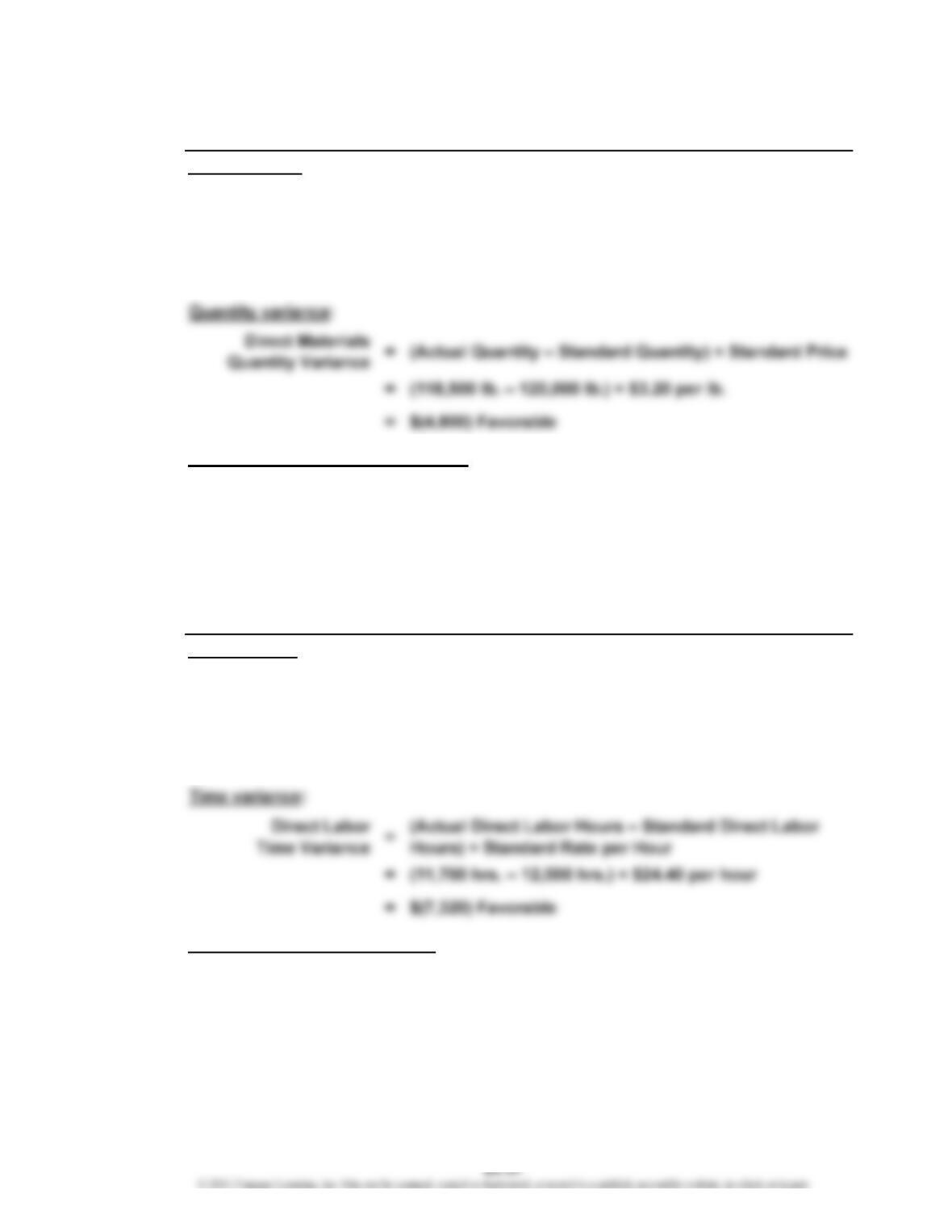

Prob. 23-1A

a. Standard

Materials and

Labor Cost

per Faucet

b.

Price variance:

= ($2.50 per lb. – $2.40 per lb.) × 14,350 lb.

= $1,435 Unfavorable

Total direct materials cost variance:

= $1,435 Unfavorable + $(120) Favorable

= $1,315 Unfavorable

Direct Materials

Cost Variance =Direct Materials Price Variance +

Direct Materials Quantity Variance

PROBLEMS

Direct Materials Cost Variance

Direct Materials

Price Variance = (Actual Price – Standard Price) × Actual Quantity

CHAPTER 23 Evaluating Variances from Standard Costs

Prob. 23-1A (Concluded)

c.

Rate variance:

*90 employees × 36 hrs.

Time variance:

= (3,240 hrs.* – 3,200 hrs.**) × $15.00 per hour

= $600 Unfavorable

*90 employees × 36 hrs.

** 4,800 units × (40 min. ÷ 60 min.)

Total direct labor cost variance:

Direct Labor Cost Variance

Direct Labor

Rate Variance

Direct Labor

Time Variance

=(Actual Rate per Hour – Standard Rate per Hour)

× Actual Hours

=(Actual Direct Labor Hours – Standard Direct Labor

Hours) × Standard Rate per Hour

CHAPTER 23 Evaluating Variances from Standard Costs

Prob. 23-2A

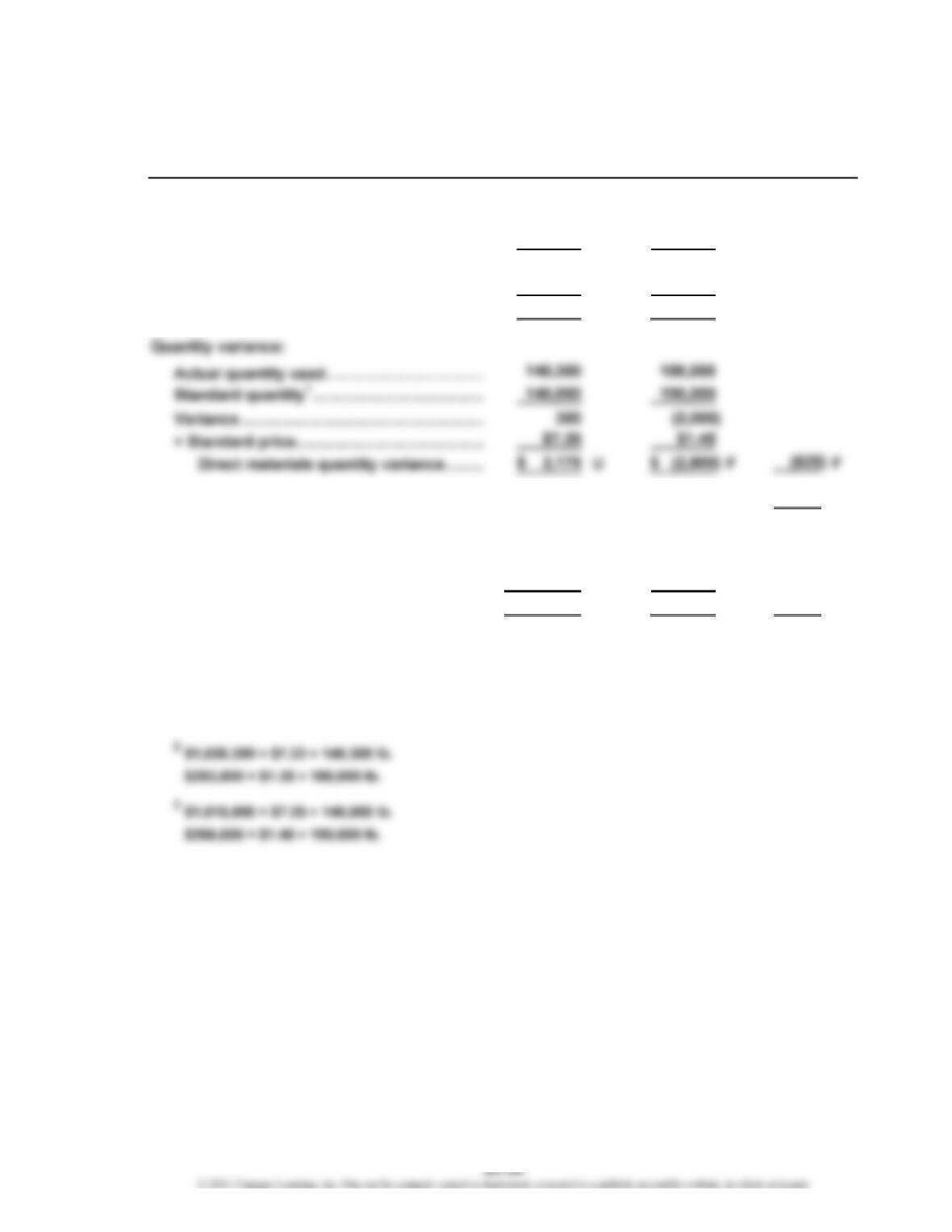

1. a.

Direct Materials Variance

Price variance:

Actual price……………………………………

…

$ 7.33 $ 1.35

Standard price………………………………… 7.25 1.40

V

ariance………………………………………

…

$ 0.08 $ (0.05)

× Actual quantity……………………………… 140,300 188,000

Direct materials price variance………… $ 11,224 U$ (9,400) F $1,824 U

Total direct materials cost variance…………

…

$1,199 U

Alternatively, total direct materials cost variance:

Actual cost 2…………………………………… $1,028,399 $253,800

Standard cost 3………………………………

…

1,015,000 266,000

Total direct materials cost variance…

…

$ 13,399 U$ (12,200) F$1,199 U

1140,000 = (12 lb. × 5,000 actual production of dark chocolate) + (8 lb.

× 10,000 actual production of light chocolate)

190,000 = (10 lb. × 5,000 actual production of dark chocolate) + (14 lb.

× 10,000 actual production of light chocolate)

Cocoa Sugar Total

V

…

CHAPTER 23 Evaluating Variances from Standard Costs

Prob. 23-2A (Concluded)

1. b.

Direct Labor Variance

Rate variance:

Time variance:

Actual time…………………………………

…

2,360 6,120

Standard time

1

……………………………

…

2,500 6,000

V

ariance……………………………………

…

(140) 120

× Standard rate……………………………

…

$ 15.50 $ 15.50

Direct labor time variance……………

…

$ (2,170) F$ 1,860 U(310) F

Total direct labor cost variance……………

…

$ 936 U

Alternatively, total direct labor cost variance:

…

2. The variance analyses should be based on the standard amounts at actual

volumes. The budget must flex with the volume changes. If the actual volume is

different from the planned volume, as it was in this case, then the budget used

for performance evaluation should reflect the amount of direct materials and

Chocolate Chocolate Total

Dark Light

…

V

…

CHAPTER 23 Evaluating Variances from Standard Costs

Prob. 23-3A

a.

Price variance:

= ($3.25 per lb. – $3.20 per lb.) × 118,500 lb.

= $5,925 Unfavorable

Total direct materials cost variance:

= $5,925 Unfavorable + $(4,800) Favorable

= $1,125 Unfavorable

b.

Rate variance:

= ($25.00 – $24.40) × 11,700 hrs.

= $7,020 Unfavorable

Total direct labor cost variance:

= $7,020 Unfavorable + $(7,320) Favorable

= $(300) Favorable

=

Direct Labor Cost Variance

Direct Labor

Rate Variance

=

Direct Labor Rate Variance + Direct Labor Time

Variance

(Actual Rate per Hour – Standard Rate per Hour)

× Actual Hours

Direct Labor

Cost Variance

= (Actual Price – Standard Price) × Actual Quantity

Direct Materials Cost Variance

Direct Materials

Cost Variance =

Direct Materials

Price Variance

Direct Materials Price Variance +

Direct Materials Quantity Variance

CHAPTER 23 Evaluating Variances from Standard Costs

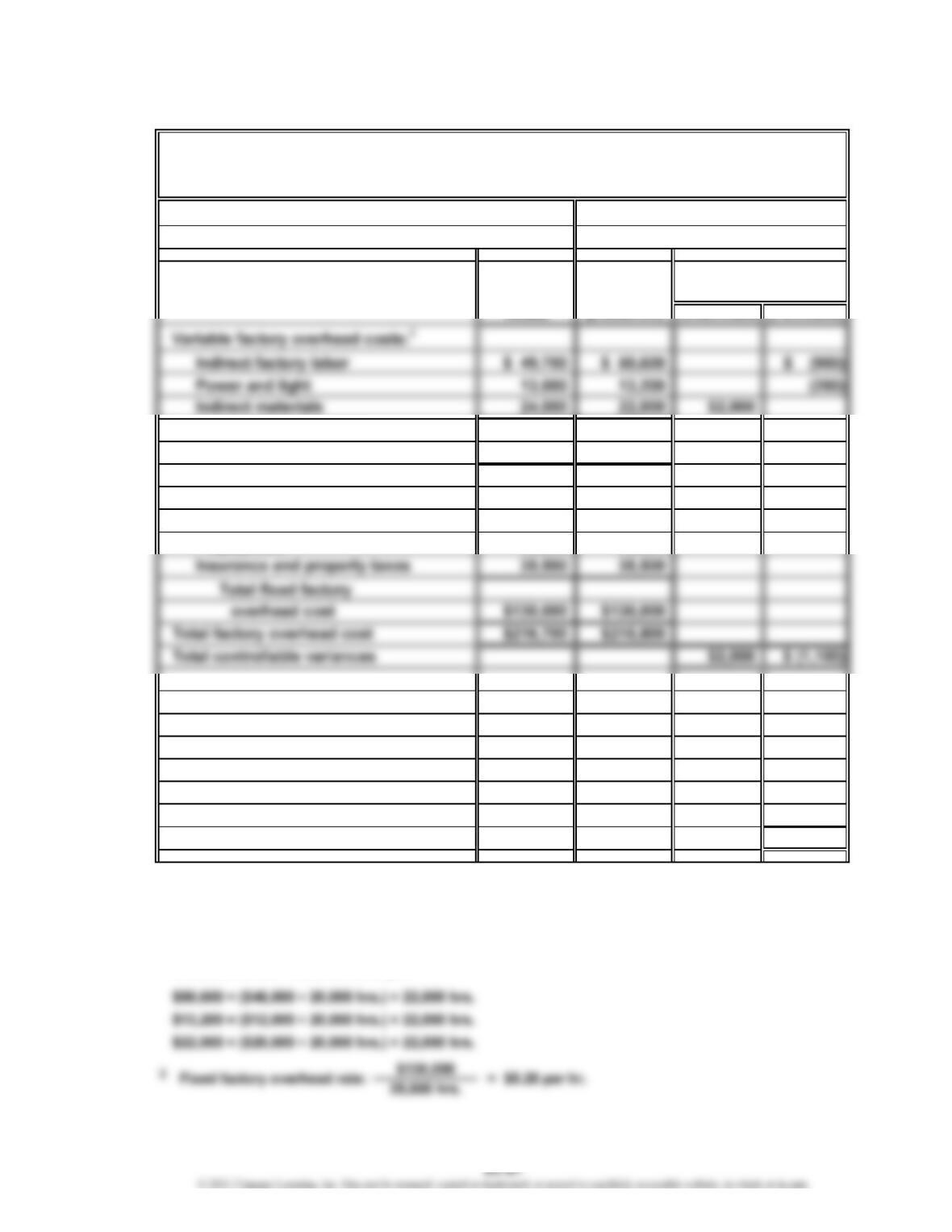

Prob. 23-3A (Concluded)

Variable factory overhead controllable variance:

Actual variable factory overhead cost incurred……………

…

$91,200

Less budgeted variable factory overhead for

12,000 hrs.* ……………………………………………………

…

96,000

V

ariance—favorable…………………………………………

…

$ (4,800)

× Standard fixed factory overhead cost rate………………

…

$10.00

V

ariance—unfavorable……………………………………

…

30,000

Total factory overhead cost variance—unfavorable…………

…

$25,200

40,000 units × 0.3 hr. per unit

12,000 hrs. × $8.00

Actual costs 241,200 Applied costs 216,000

($91,200 + $150,000) [12,000 × ($8.00 + $10.00)]

Balance (underapplied) 25,200

Actual Applied

Factory Factory

Overhead Overhead

V

Factory Overhead Cost Variance

c.

*

**

Produced

Overhead for Amount

Alternative Computation of Overhead Variances

Factory Overhead

Budgeted Factory

**

CHAPTER 23 Evaluating Variances from Standard Costs

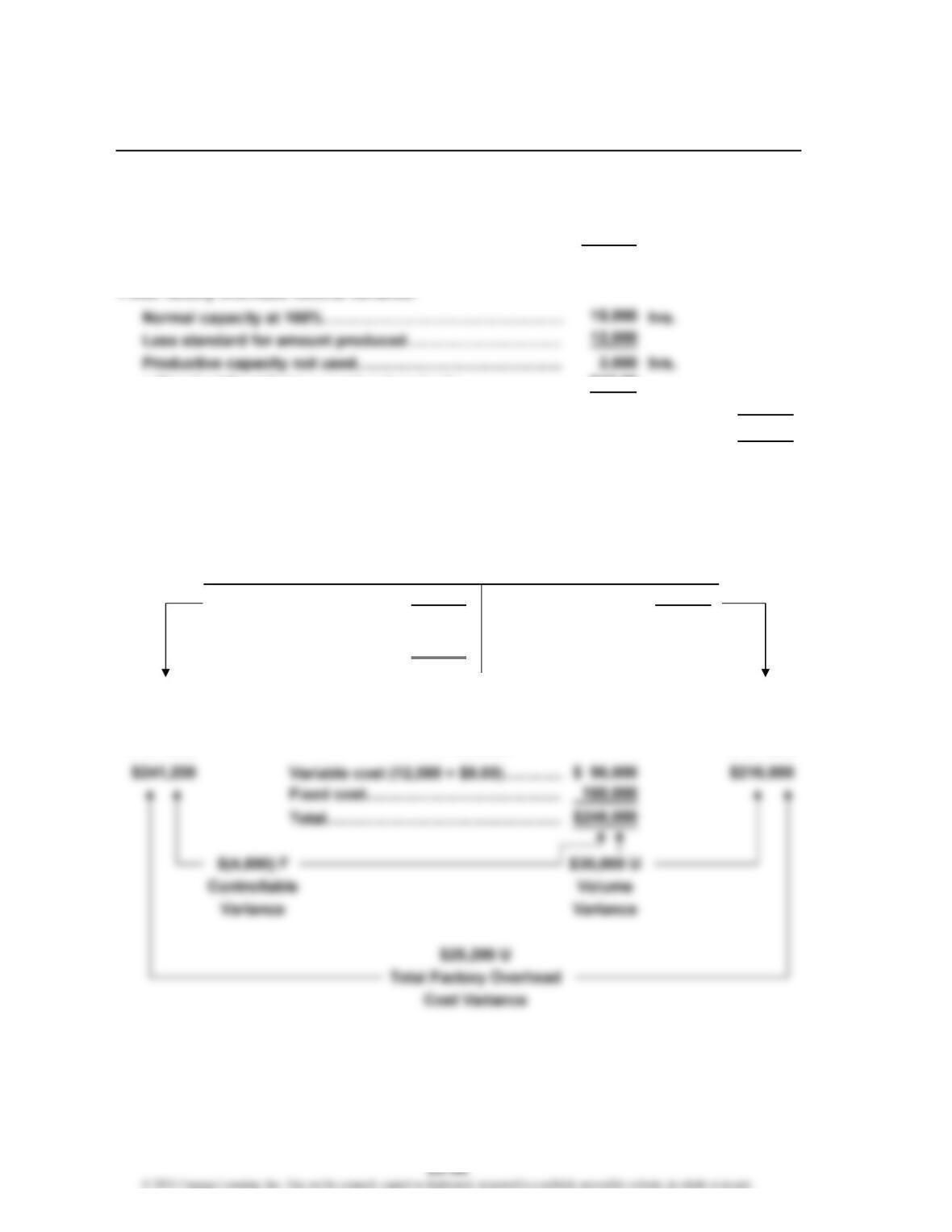

Prob. 23-4A

Normal capacity for the month 8,400

hrs.

Actual production for the month 8,860 hrs.

Actual Budget Unfavorable (Favorable)

Variable costs:

1

Fixed costs:

Supervisory salaries $ 20,000 $ 20,000

Depreciation of plant and

equipment 36,200 36,200

Net controllable variance—unfavorable $ 770

Volume variance—favorable:

Excess hours used over normal at the

1

The budgeted variable costs are determined by multiplying the 8,860 actual hours

by the variable overhead rate (the May budget divided by 8,400 hours for each

variable overhead cost). Thus,

Tiger Equipment Inc.

Factory Overhead Cost Variance Report—Welding Department

For the Month Ended May 31

Variances

CHAPTER 23 Evaluating Variances from Standard Costs

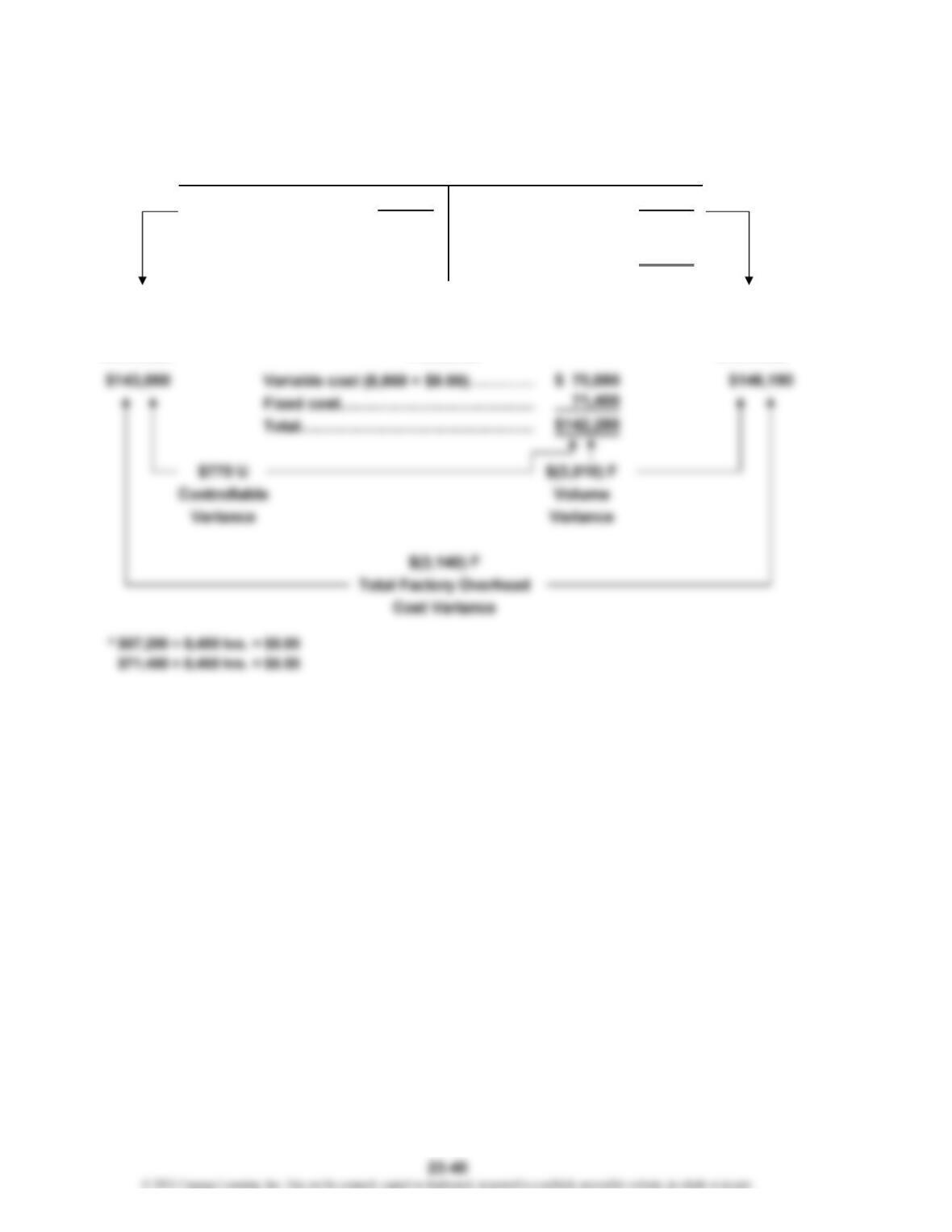

Prob. 23-4A (Concluded)

Actual costs 143,050 Applied costs* 146,190

[8,860 × ($8.00 + $8.50)]

Balance (overapplied) 3,140

Actual Applied

Factory Factory

Overhead Overhead

Produced

Overhead for Amount

Alternative Computation of Overhead Variances

Factory Overhead

Budgeted Factory