Weygandt, Accounting Principles, 12e,

Chapter Twenty Three

Solutions to Challenge Exercises

Solution

CE23-1

(a)

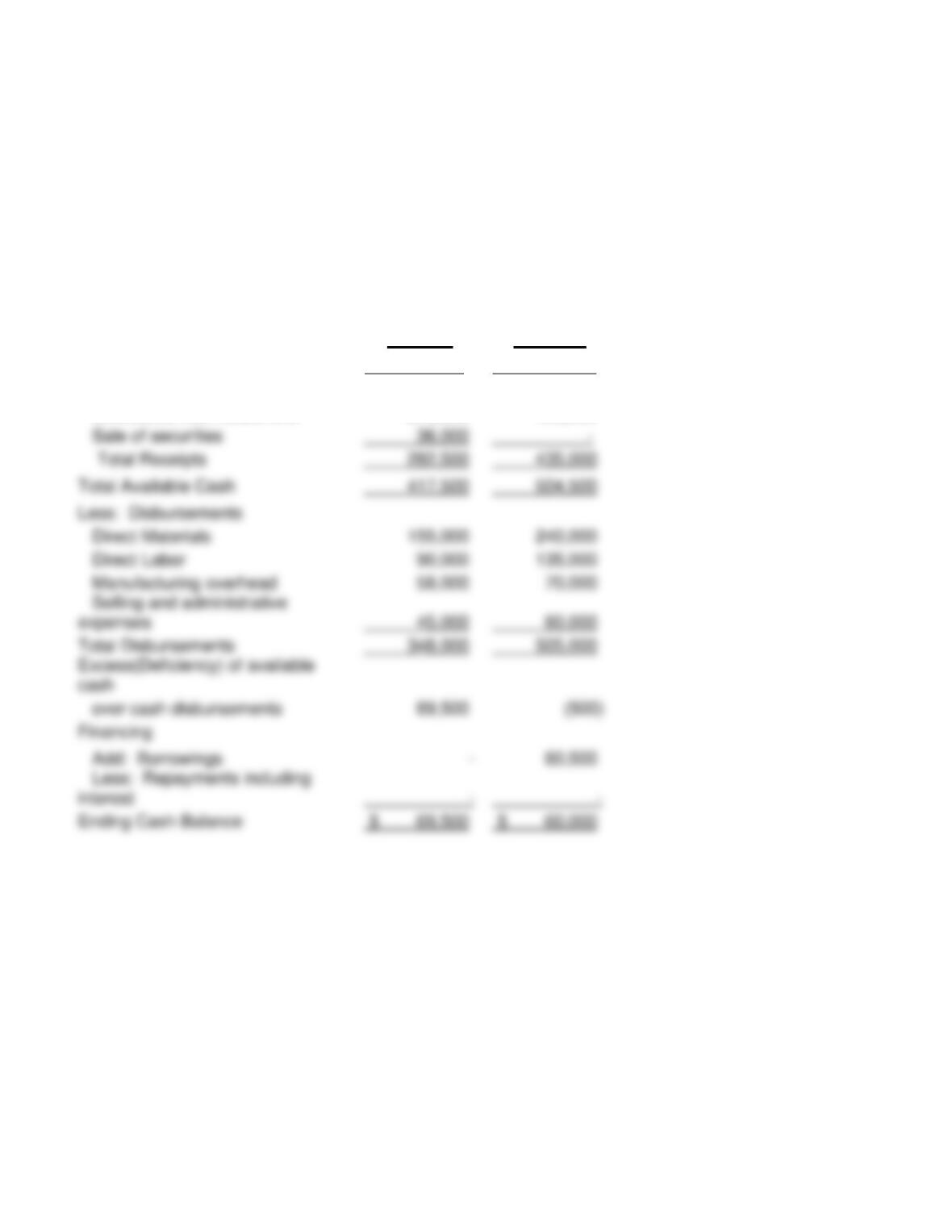

Martin Company

Cash Budget

For the months ending February 2017

January

February

Beginning cash balance

$ 135,000

$ 69,500

Add: Receipts

Collections from customers

246,500

435,000

Sale of securities

36,000

__________–

(continued on the next page)

CE23-1

Total Receipts

282,500

435,000

Total Available Cash

417,500

504,500

Less: Disbursements

Direct Materials

155,000

240,000

Direct Labor

90,000

135,000

Manufacturing overhead

58,000

70,000

expenses

45,000

60,000

cash

over cash disbursements

69,500

(500)

Financing

Add: Borrowings

–

60,500

interest

–

–

Ending Cash Balance

$ 69,500

$ 60,000

(b) (1)

Martin Company

Cash Budget

For the months ending March 2014

January February March

Beginning cash balance $135,000 $ 69,500 $ 60,000

Add: Receipts

(2) $14,500. Martin Company is only approved to borrow up to $75,000 with its credit line. The

company has an outstanding balance of $60,500 on the credit line which means that only

(3) The company will only have to borrow $8,100 if the marketable securities are sold. Selling the

$50,000 securities provides the company with an ending cash balance before borrowing of

(4) Martin Company is running very low on cash during March. The bright spot is that they did end

up with a positive cash balance, however, the company needed to cash out securities and borrow

expenses or find a new source of funds from which to borrow.

Solution

CE23-2

(a)

Moorcroft Company

Schedule of Expected Collections from Customers

Sales April May June

April $300,000 $156,000 90,000 46,800

(b) Moorcroft Company

Schedule of Expected Payment for Direct Materials

Purchases April May June

April $ 45,000 $22,500 9,000 13,500

(c) Moorcroft Company

Schedule of Expected Collections from Customers

Sales April May June

April $300,000 $174,000 90,000 32,400

May 320,000 185,600 96,000

(d)

Moorcroft Company

Schedule of Expected Payment for Direct Materials

Purchases April May June

April $ 45,000 $18,000 10,800 16,200