Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 23

1301

Chapter 23

Flexible Budgets and Standard Costs

QUESTIONS

1. Fixed budget performance reports have limited usefulness because they do not

2. The primary purpose of a flexible budget is to help managers better evaluate past

performance, which can improve their abilities to monitor and control operations.

3. The proper title is:

Spalding Company

Flexible Budget Performance Report

For Year Ended December 31, 2017

The proper title communicates to the user the focus of the report. Although it may

4. A flexible budget performance report is useful for an analysis of the difference

6. The human resource department is usually responsible for a labor rate variance.

The production department is usually responsible for a labor efficiency variance.

7. A price variance is that portion of a cost variance caused by a difference between

1302

8. Standard costs are used to establish a basis to assess the reasonableness of actual

9. An overhead volume variance is the difference between (a) the amount of (fixed)

10. A predetermined standard overhead rate is a measure computed and used in a

standard cost system to assign overhead costs to products. Before the period

11. In general, variance analysis is said to provide information about price and quantity

variances.

12. A controllable variance is the difference between (a) the total overhead cost actually

13. Standard costs provide a basis for evaluating actual performance. Summary

information comparing actual costs to budgeted costs is captured and reported in a

14. Before a period starts, the manager can prepare flexible budgets for the various

types of advertising. Then, she could estimate both the best and worst case

15. Apple schedules appointments with customers to service Apple computers,

1303

16. The controllable variance should not be affected by achieving an actual operating

level different from the budgeted level. If the company operated at 75% of capacity,

17. Positive features of standard cost systems include: Provides benchmarks to be

used in management by exception; motivates employees to work towards goals;

18. Management by exception involves managers focusing on the most significant

variances for analysis and action strategies. It also results in less attention given to

QUICK STUDIES

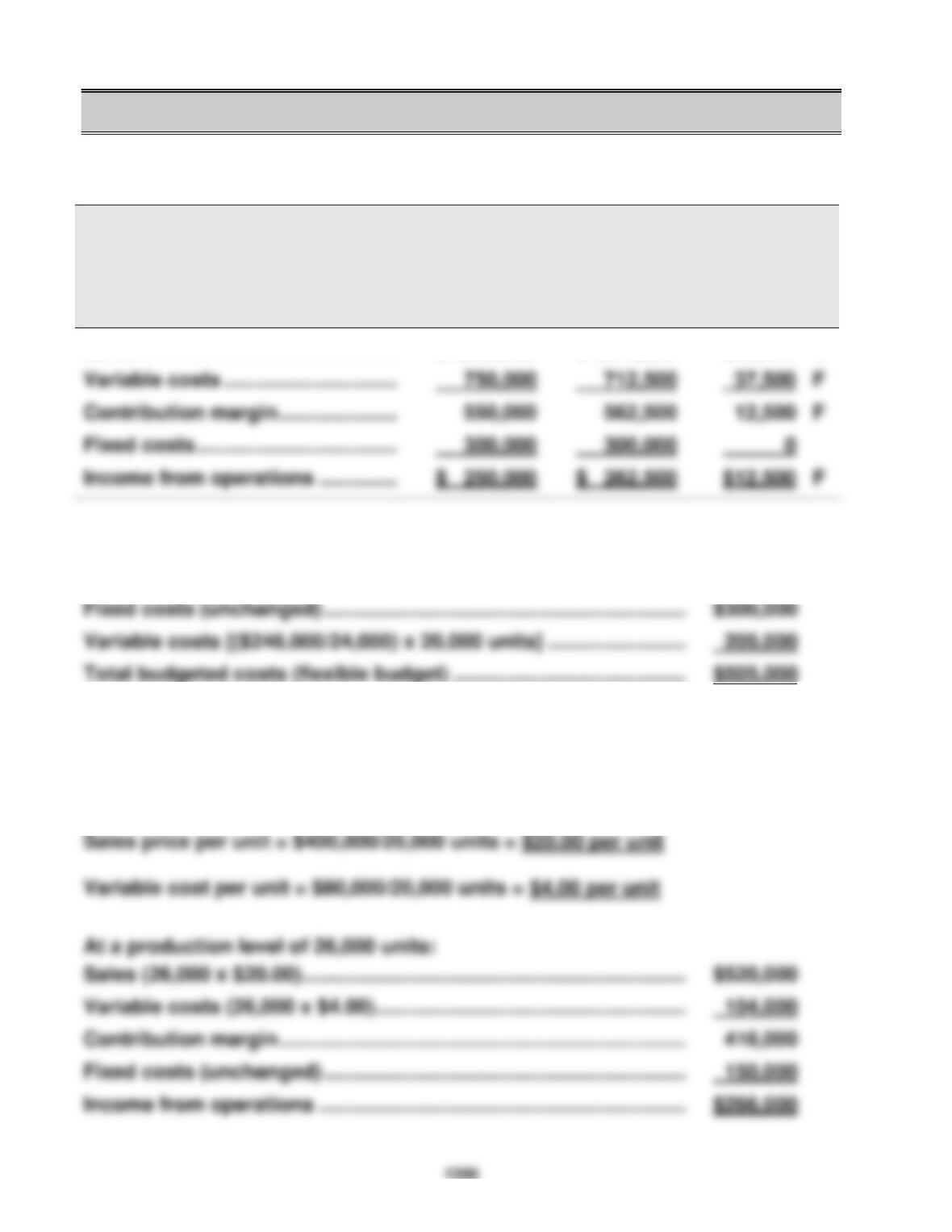

Quick Study 23-1 (15 minutes)

BEECH COMPANY

Flexible Budget Performance Report

For Month Ended May 31

Flexible

Actual

Budget

Results

Variances

Sales ..................................................

$1,300,000

$1,275,000

$25,000

U

Quick Study 23-2 (5 minutes)

Quick Study 23-3 (10 minutes)

From the flexible budget at 20,000 units, compute the sales price and variable

costs per unit:

Quick Study 23-4 (10 minutes)

BRODRICK COMPANY

Flexible Budget Performance Report

For Year Ended December 31

Flexible

Actual

Budget

Results

Variances

Sales (26,000 units) .........................

$520,000

$480,000

$40,000

U

Quick Study 23-5 (5 minutes)

A standard cost card for one bat would include:

Quick Study 23-6 (5 minutes)

Actual cost for one bat ......................................................................

$40

Quick Study 23-7 (10 minutes)

Quick Study 23-8 (10 minutes)

Direct materials price variance:

Actual cost of direct materials used (given) ..............................................

$535,000

1359

Quick Study 23-9 (15 minutes)

Following information is given:

It is also known that:

Material price variance = Price variance per pound x Actual pounds used

Quick Study 23-10 (10 minutes)

Standard direct materials cost ..........................................................

$150,000

Quick Study 23-11 (10 minutes)

Direct labor rate variance:

Actual hours x Actual rate per hour (65,000 x $15) ................................

$975,000

Actual hours x Standard rate per hour (65,000 x $14) ..............................

910,000

Direct labor rate variance ................................................................

$ 65,000

U

Direct labor efficiency variance:

Actual hours x Standard rate per hour (65,000 x $14) ..............................

$910,000

Standard hours x Standard rate per hour (67,000 x $14) .........................

938,000

Direct labor efficiency variance ................................................................

$ 28,000

F

Quick Study 23-12 (10 minutes)

Standard direct labor cost ................................................................

$400,000

Quick Study 23-13 (10 minutes)

Actual overhead incurred ................................................................

$262,800

Quick Study 23-14 (10 minutes)

Actual overhead incurred ................................................................

$ 28,175

Quick Study 23-15 (5 minutes)

Budgeted fixed overhead (at 12,000 units) ................................................

$12,000

1361

1362

Quick Study 23-16 (10 minutes)

Standard overhead cost ..............................................................................

$225,000

Quick Study 23-17A (10 minutes)

Work in Process Inventory ......................................................

225,000

Quick Study 23-18 (10 minutes)

Actual overhead (4,700 x $4.15)*................................................................

$19,505

Quick Study 23-19A (15 minutes)

Variable overhead spending and efficiency variances

Actual Overhead

AH x AVR

AH x SVR

Applied Overhead

SH x SVR

1363

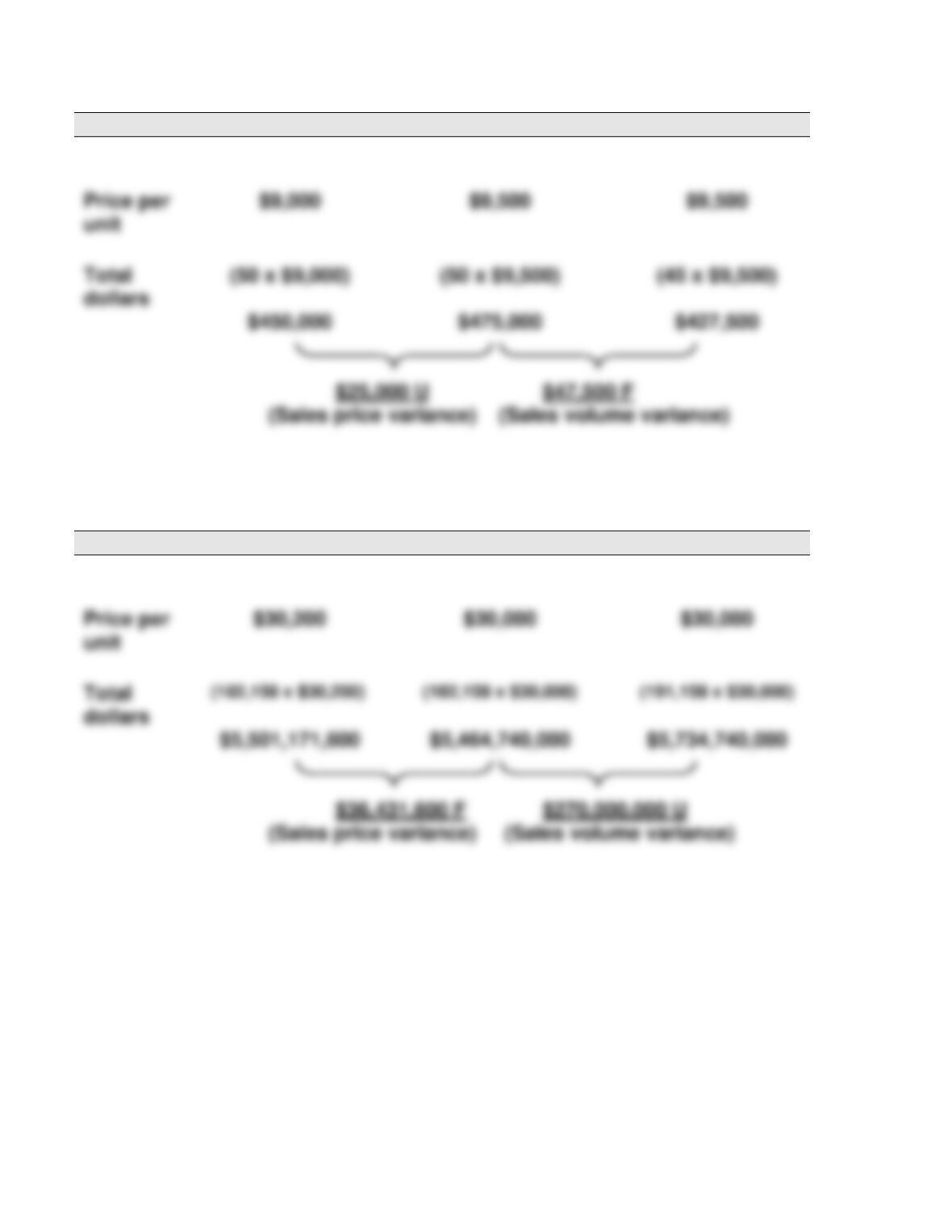

Sales

Actual

Flexible Budget

Fixed Budget

Units

50

50

45

Quick Study 23-21 (15 minutes)

Sales

Actual

Flexible Budget

Fixed Budget

Units

182,158

182,158

191,158

1364

Quick Study 23-22 (5 minutes)

Quick Study 23-23 (10 minutes)

a) Standard overhead rate before sustainability improvement:

b) Standard overhead rate after sustainability improvement:

Exercise 23-1 (20 minutes)

Item

Cost

a. Bike frames

Variable

b. Screws for assembly

Variable

1366

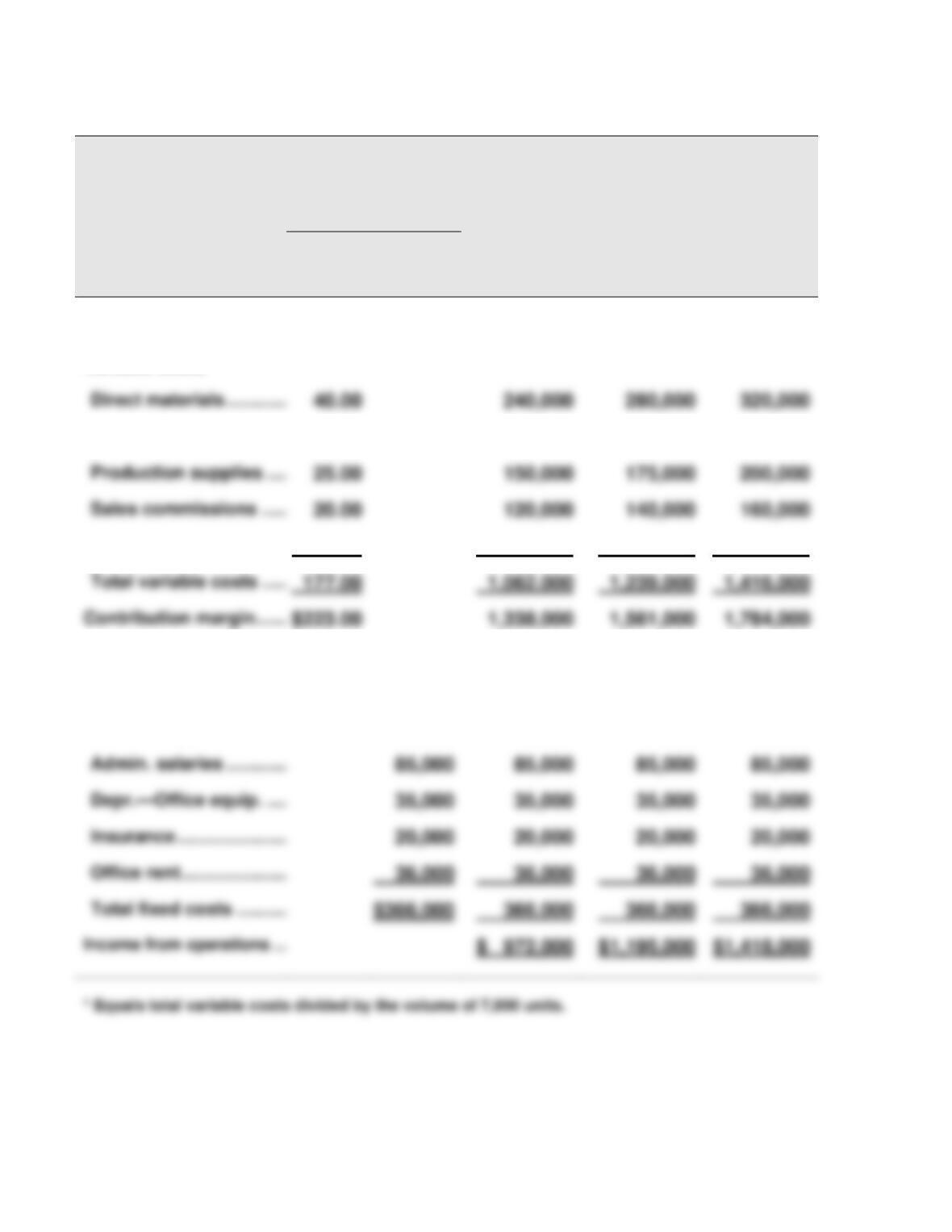

Exercise 23-2 (30 minutes)

TEMPO COMPANY

Flexible Budgets

For Quarter Ended March 31, 2017

Flexible Budget

Flexible

Flexible

Flexible

Variable

Amount

per Unit*

Total

Fixed

Cost

Budget for

Unit Sales

of 6,000

Budget for

Unit Sales

of 7,000

Budget for

Unit Sales

of 8,000

Sales ................................

$400.00

$2,400,000

$2,800,000

$3,200,000

Variable costs

Direct labor .......................

70.00

420,000

490,000

560,000

Packaging .........................

22.00

132,000

154,000

176,000

Fixed costs

Plant manager salary .......

$ 65,000

65,000

65,000

65,000

Advertising .......................

125,000

125,000

125,000

125,000

1367

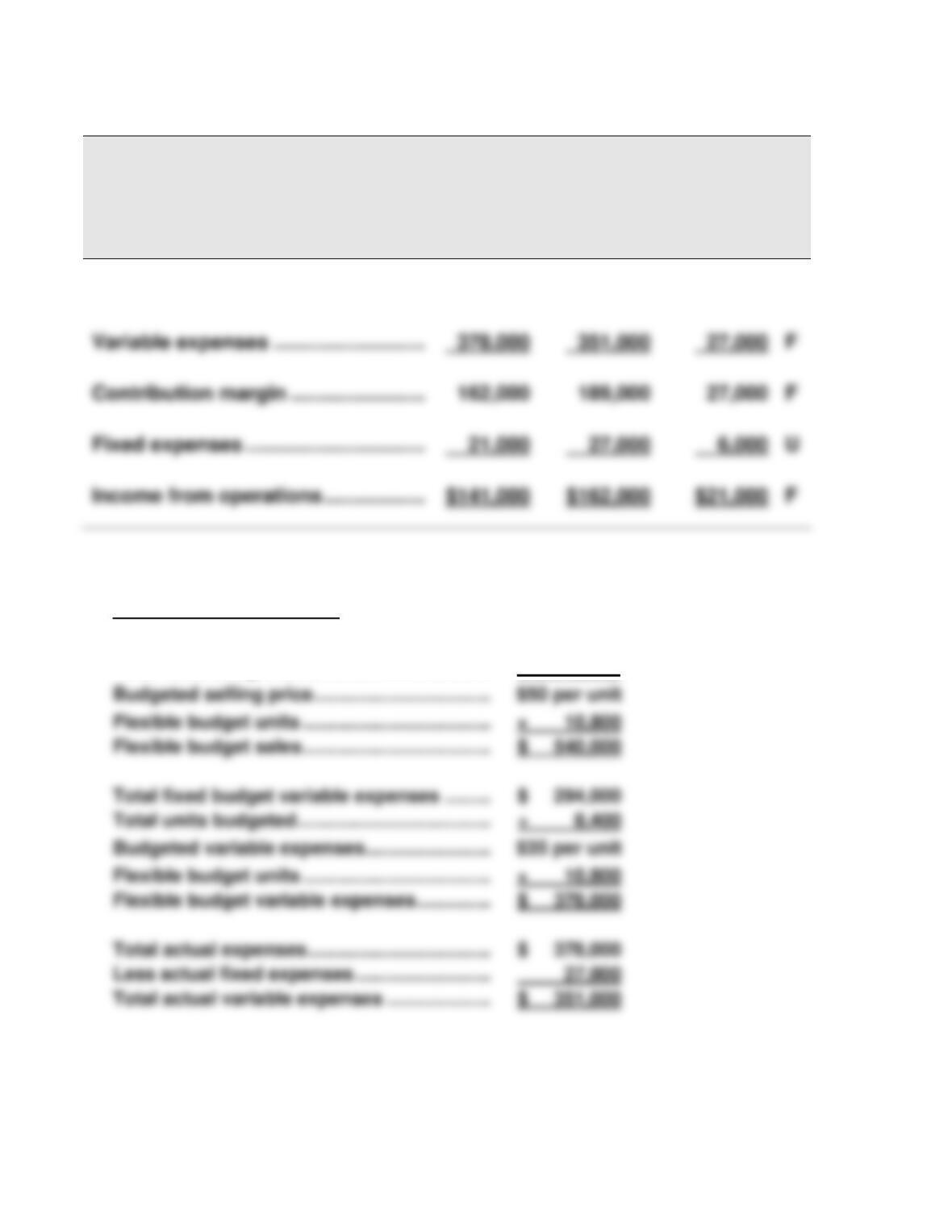

Exercise 23-3 (25 minutes)

SOLITAIRE COMPANY

Flexible Budget Performance Report

For Month Ended June 30

Flexible

Actual

Budget

Results

Variances

Sales (10,800 units) .........................

$540,000

$540,000

$ 0

Supporting computations

Total fixed budget sales ................................

$ 420,000

Total fixed budget units ................................

÷ 8,400

1368

Exercise 23-4 (25 minutes)

BAY CITY COMPANY

Flexible Budget Performance Report

For Month Ended July 31

Flexible

Actual

Budget

Results

Variances

Sales (7,200 units)............................

$720,000

$737,000

$17,000

F

Supporting computations

Total fixed budget sales ................................

$ 750,000

Total units budgeted ..................................................

÷ 7,500

1369

Exercise 23-5 (10 minutes)

Exercise 23-6 (5 minutes)

Following management by exception, the company should focus on those

Exercise 23-7 (15 minutes)

Exercise 23-8 (10 minutes)

(1) The standard cost for one unit is computed as:

Direct materials (6 lbs. @$8 per lb.) ................................................

$ 48

1370

Exercise 23-8 (continued)

(2) Total cost variance

Actual costs incurred during the month:

Direct materials (48,500 x $8.10) ................................................................

$392,850

Direct labor (15,700 x $16.50) ................................................................

259,050

Exercise 23-9 (15 minutes)

Direct materials price variance:

Actual cost of direct materials used (48,500 x $8.10) ...............................

$392,850

1371

Exercise 23-10 (15 minutes)

Direct labor rate variance:

Actual hours x Actual rate per hour (15,700 x $16.50) ..............................

$259,050

Exercise 23-11 (25 minutes)

Part 1

Direct materials price variance:

Actual cost of direct materials used (138,000 x $3.75) .............................

$517,500

1372

Exercise 23-11 (continued)

Part 2 Direct labor rate variance:

Actual hours x Actual rate per hour (31,000 x $15.10) ..............................

$468,100

Exercise 23-12 (25 minutes)

Part 1 Direct materials price variance:

Actual cost of direct materials used (92,000 x $2.95) ...............................

$271,400

Direct materials quantity variance:

Actual quantity used x Standard price (92,000 x $3.00) ...........................

$276,000