CHAPTER 23 Evaluating Variances from Standard Costs

Prob. 23-5A

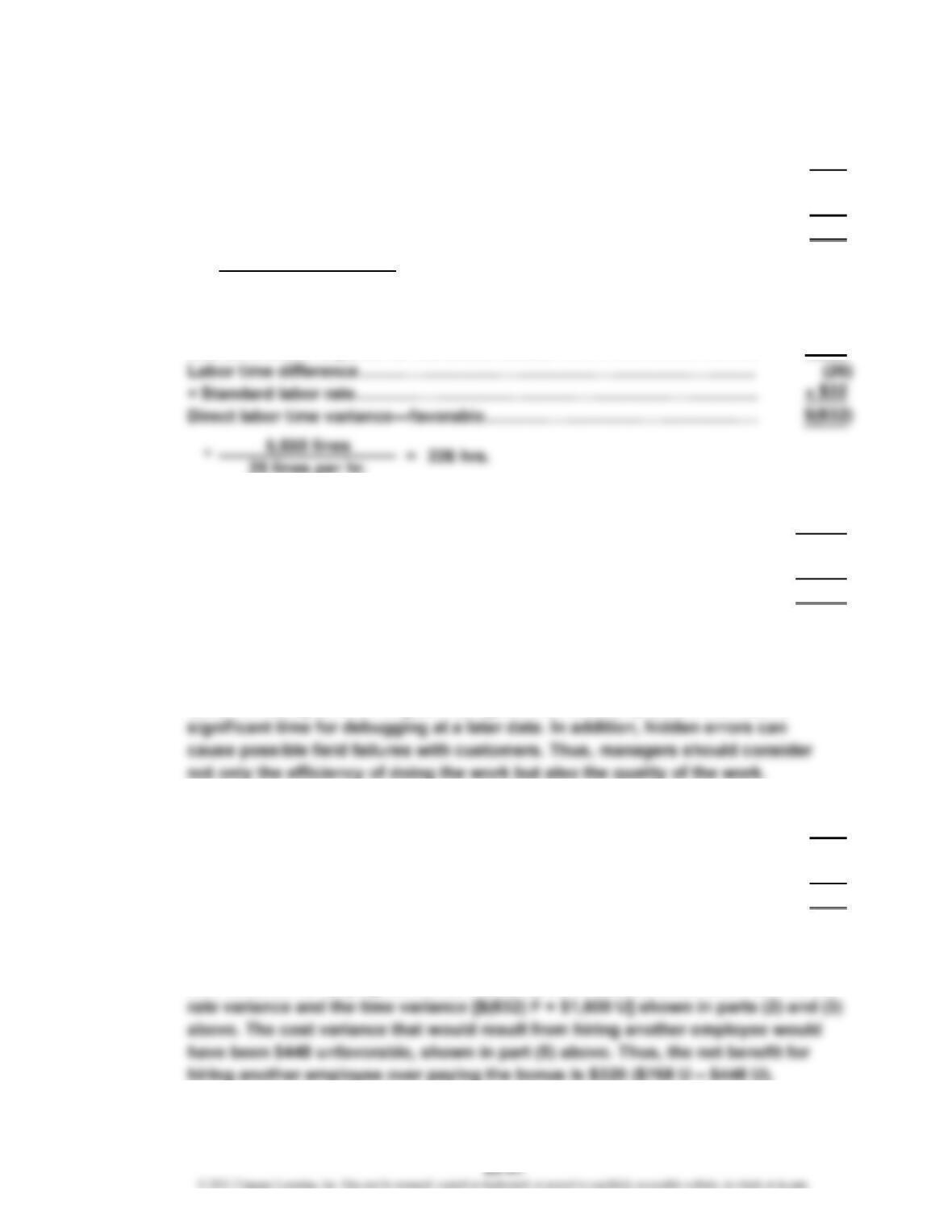

1. Actual hours provided (5 × 40 hrs.)……………………………………………

…

200

Standard hours required for the original plan*………………………………

…

186

Labor time difference……………………………………………………………

…

14

×

Standard labor rate……………………………………………………………… $32

Direct labor time variance—unfavorable……………………………………… $448

4,650 lines

25 lines per hr.

2. Actual hours provided (5 × 40 hrs.)……………………………………………

…

200

Standard hours required for the actual results*……………………………

…

226

3. Actual labor rate…………………………………………………………………… $40

Standard labor rate………………………………………………………………

…

32

Difference…………………………………………………………………………… $ 8

× Actual hours provided (5 × 40 hrs.)…………………………………………

…

200

Direct labor rate variance—unfavorable………………………………………

…

$1,600

The labor cost variance is $768 unfavorable [($832) favorable time variance +

$1,600 unfavorable rate variance].

4. The labor rate and time variances fail to consider the number of errors in the

code from programmer fatigue. A program that has many errors will require

5. Actual hours provided (6 × 40 hrs.)……………………………………………

…

240

Standard hours required for the actual results*……………………………

…

226

Labor time difference……………………………………………………………

…

14

×

Standard labor rate……………………………………………………………… $32

Direct labor time variance—unfavorable……………………………………… $448

*

From part (2) above

6. Hiring an extra employee is less costly than the bonus by $320. The direct labor

cost variance for paying the bonus was $768 unfavorable, which is the sum of the

=* 186 hrs.

×

×

×

…

…

CHAPTER 23 Evaluating Variances from Standard Costs

Prob. 23-1B

a. Standard

Materials and

Labor Cost

per Unit

Direct materials ($5.00 × 5.0 yds.)……………………………………………

…

$25.00

Direct labor [$12.00 × (12 min. ÷ 60 min.)]…………………………………

…

2.40

$27.40

Quantity variance:

= (26,200 yds. – 26,100 yds.*) × $5.00 per yd.

= $500 Unfavorable

=

Direct Materials

Quantity Variance

(Actual Quantity – Standard Quantity) × Standard Price

CHAPTER 23 Evaluating Variances from Standard Costs

Prob. 23-1B (Concluded)

c.

Rate variance:

Time variance:

= (1,000 hrs. – 1,044 hrs.*) × $12.00 per hour

= $(528) Favorable

*(12 min. ÷ 60 min.) × 5,220

Total direct labor cost variance:

Direct Labor Cost Variance

(Actual Direct Labor Hours – Standard Direct Labor

Hours) × Standard Rate per Hour

Direct Labor

Time Variance

=

CHAPTER 23 Evaluating Variances from Standard Costs

Prob. 23-2B

1. a.

Direct Materials Variance

Price variance:

Actual price………………………………

…

$ 1.90 $ 8.20

Standard price……………………………

…

2.00 8.00

V

ariance……………………………………

…

$ (0.10) $ 0.20

× Actual quantity…………………………

…

48,000 85,100

Direct materials price variance……

…

$ (4,800) F$17,020 U $12,220 U

Quantity variance:

48,000 85,100

Total direct materials cost variance………

…

$10,940 U

Alternatively, total direct materials cost variance:

Actual cost

2

………………………………

…

$91,200 $697,820

Standard cost

3

……………………………

…

95,520 682,560

Total direct materials cost variance

…

$ (4,320) F$ 15,260 U$10,940 U

1

47,760 = (4.0 lb. × 4,400 actual production of women’s coats) + (5.2 lb. × 5,800 actual production of

Filler Liner Total

××

V

…

CHAPTER 23 Evaluating Variances from Standard Costs

Prob. 23-2B (Concluded)

1. b.

Direct Labor Variance

Rate variance:

Actual rate…………………………………

…

$ 14.10 $ 13.30

Standard rate………………………………

…

14.00 13.00

V

ariance……………………………………

…

$ 0.10 $ 0.30

× Actual time………………………………

…

1,825 2,800

Direct labor rate variance……………

…

$182.50 U$ 840 U $1,022.50 U

Time variance:

Total direct labor cost variance……………

…

$ 632.50 U

Alternatively, total direct labor cost variance:

Actual cost

2

………………………………… $25,732.50 $37,240.00

Standard cost

3

……………………………

…

24,640.00 37,700.00

Total direct labor cost variance……

…

$ 1,092.50 U$ (460.00) F$ 632.50 U

1

1,760 = 0.40 hr. × 4,400 actual production of women’s coats

2,900 = 0.50 hr. × 5,800 actual production of men’s coats

2. The variance analyses should be based on the standard amounts at actual

volumes. The budget must flex with the volume changes. If the actual volume

Coats Coats Total

Women’s Men’s

××

…

V

…

CHAPTER 23 Evaluating Variances from Standard Costs

Prob. 23-3B

a.

Price variance:

= ($7.30 per lb. – $7.25 per lb.) × 252,500 lb.

= $12,625 Unfavorable

Total direct materials cost variance:

= $12,625 Unfavorable + $18,125 Unfavorable

= $30,750 Unfavorable

b.

Rate variance:

Time variance:

= (5,000 hrs. – 5,200 hrs.) × $17.00 per hour

= $(3,400) Favorable

Total direct labor cost variance:

Direct Labor Cost Variance

Direct Labor

Time Variance

=(Actual Direct Labor Hours – Standard Direct Labor

Hours) × Standard Rate per Hour

Direct Materials

Price Variance

Direct Materials Cost Variance

= (Actual Price – Standard Price) × Actual Quantity

Direct Materials

Cost Variance =Direct Materials Price Variance +

Direct Materials Quantity Variance

CHAPTER 23 Evaluating Variances from Standard Costs

Prob. 23-3B (Concluded)

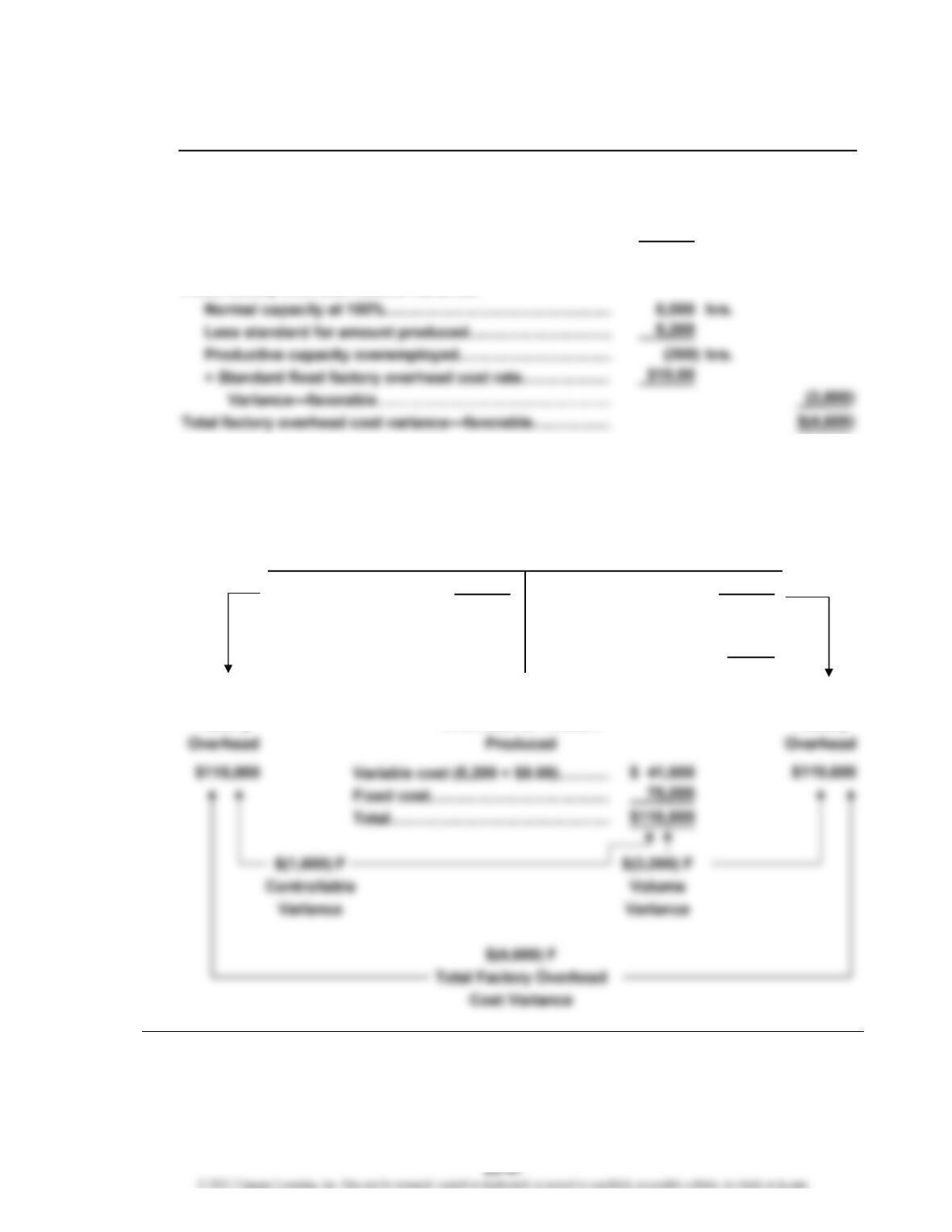

Variable factory overhead controllable variance:

Actual variable factory overhead cost incurred…………

…

$40,000

Less budgeted variable factory overhead

for 5,200 hrs.* ………………………………………………

…

41,600

V

ariance—favorable………………………………………

…

$(1,600)

Fixed factory overhead volume variance:

10,400 units × 0.5 hr.

5,200 hrs. × $8.00

Actual costs 115,000 Applied costs 119,600

($40,000 + $75,000) [5,200 × ($8.00 + $15.00)]

Balance (overapplied) 4,600

Actual Applied

Factory Factory

V

*

**

c.

Factory Overhead Cost Variance

Overhead for Amount

Alternative Computation of Overhead Variances

Factory Overhead

Budgeted Factory

**

V

…

CHAPTER 23 Evaluating Variances from Standard Costs

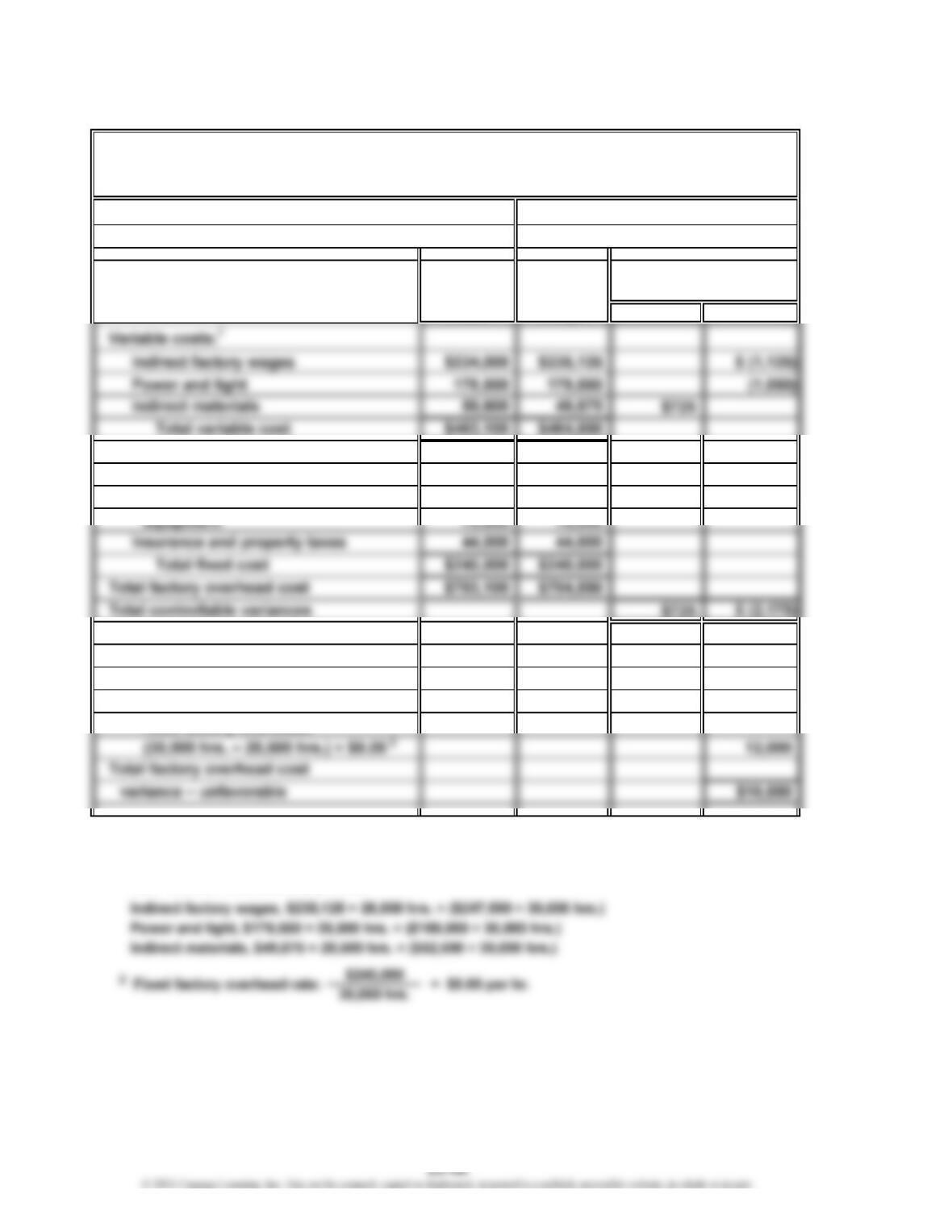

Prob. 23-4B

Normal capacity for the month 30,000

hrs.

Actual production for the month 28,500 hrs.

Actual Budget Unfavorable (Favorable)

Fixed costs:

Supervisory salaries $126,000 $126,000

Depreciation of plant and

Net controllable variance—favorable $ (1,450)

Volume variance—unfavorable:

Idle hours at the standard rate for

1

The budgeted variable costs are determined by multiplying 28,500 actual hours

by the variable overhead rate (the October budget divided by 30,000 hours for

each variable overhead cost). Thus,

Feeling Better Medical Inc.

Factory Overhead Cost Variance Report—Assembly Department

For the Month Ended October 31

Variances

CHAPTER 23 Evaluating Variances from Standard Costs

Prob. 23-4B (Concluded)

Actual costs 703,100 Applied costs* 692,550

[28,500 × ($16.30 + $8.00)]

Balance (underapplied

)

10,550

Actual Applied

Factory Factory

Overhead Overhead

$489,000 ÷ 30,000 hrs. = $16.30

$240,000 ÷ 30,000 hrs. = $8.00

Produced

Overhead for Amount

Alternative Computation of Overhead Variances

Factory Overhead

Budgeted Factory

*

CHAPTER 23 Evaluating Variances from Standard Costs

Prob. 23-5B

1. Actual hours provided (3 × 40 hrs.)……………………………………………

…

120

Standard hours required for the original plan*………………………………

…

117

2. Actual hours provided (3 × 40 hrs.)……………………………………………

…

120

Standard hours required for the actual results*……………………………… 127

Labor time difference……………………………………………………………… (7)

× Standard labor rate………………………………………………………………

…

$23

Direct labor time variance—favorable…………………………………………

…

$(161)

88,900 lines

700 lines per hr.

3. Actual labor rate……………………………………………………………………

…

$30

Standard labor rate………………………………………………………………… 23

…

…

4. Actual hours provided (4 × 40 hrs.)……………………………………………

…

160

Standard hours required for the actual results………………………………

…

127

Labor time difference……………………………………………………………… 33

× Standard labor rate………………………………………………………………

…

$23

Direct labor time variance—unfavorable………………………………………

…

$ 759

5. The bonus is the better approach by $80. The direct labor cost variance for

paying the bonus was $679 unfavorable which is the sum of the time variance

6. The labor rate and time variances fail to consider the number of errors in the

report from typist fatigue. A report that has many errors will require significant

time for correction at a later date. In addition, report errors can cause doctors

to draw incorrect conclusions from the test analyses. Thus, managers should

consider not only the efficiency of doing the work but also the quality of the

work.

* = 127 hrs.

…

…

Part A

2. Selling price…………………………………………………………

…

$100.00

Less variable costs per case:

Direct materials…………………………………………………

…

$17.00

Direct labor………………………………………………………

…

7.20

Utilities [see part (1)]……………………………………………

…

0.20

Selling expenses…………………………………………………

…

20.00

Total variable costs per case…………………………………

…

44.40

Contribution margin per case……………………………………

…

$ 55.60

3. Total fixed costs:

Utilities [see part (1)]…………………………………………………………

…

$ 500

4.

$19,460

$55.60

Break-Even Sales (units) =

Break-Even Sales (units) = = 350 cases

Fixed Costs

Unit Contribution Margin

COMPREHENSIVE PROBLEM 5

Variable Cost per Unit1. = Difference in Total Cost

Difference in Production

=Variable Cost per Unit = $0.20 per case

$740 – $600

1,200 cases – 500 cases

CHAPTER 23 Evaluating Variances from Standard Costs

Comp. Prob. 5 (Continued)

Part B

5.

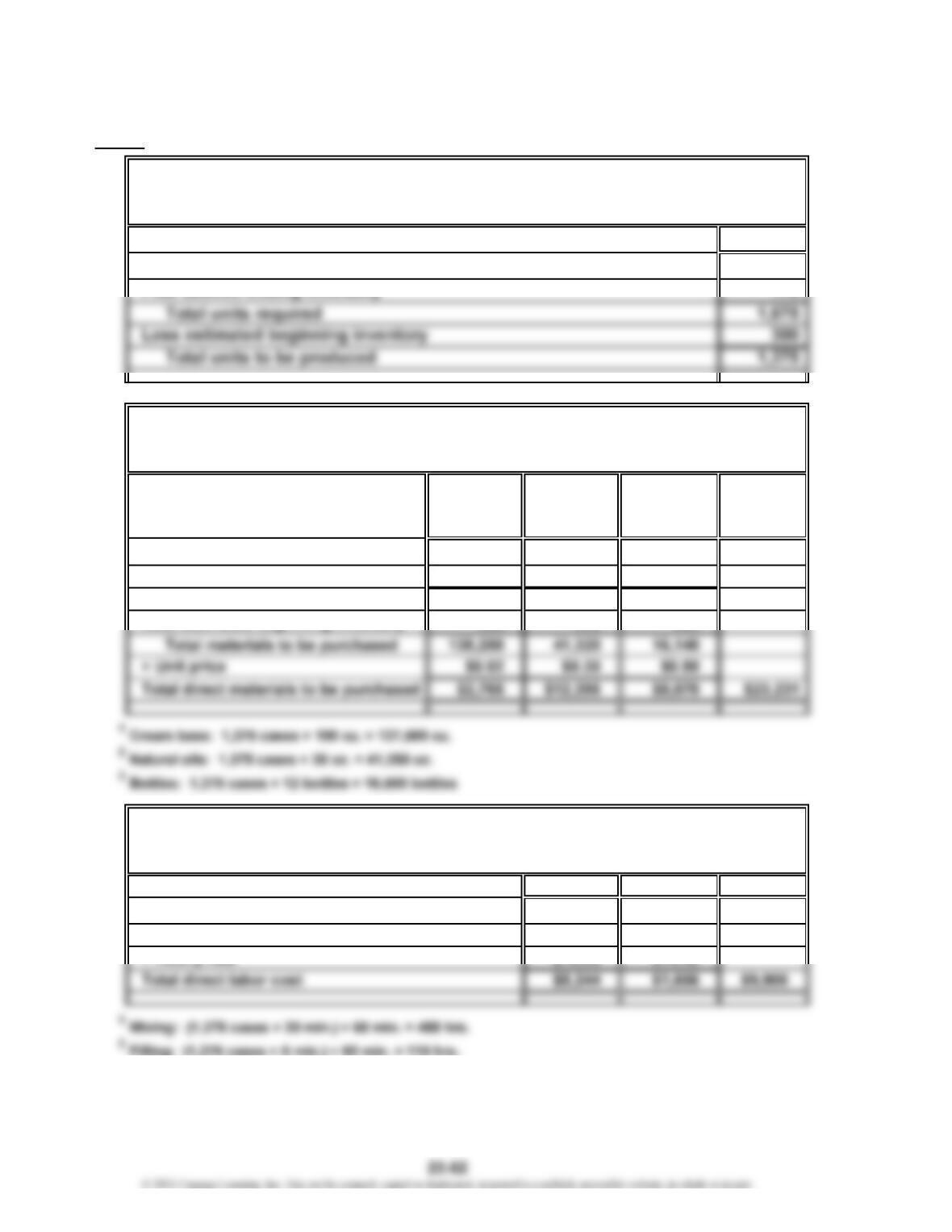

Cases

Expected cases to be sold 1,500

6.

Cream Natural

Base Oils Bottles Total

(oz.) (oz.) (bottles)

Units required for production 137,500 41,250 16,500

Plus desired ending inventory 1,000 360 240

Total units required 138,500 41,610 16,740

7.

Mixing Filling Total

Hours required for production of:

Hand and body lotion 458 115

Filling: (1,375 cases × 5 min.) ÷ 60 min. = 115 hrs.

Direct Labor Cost Budget

For the Month Ended August 31

Genuine Spice Inc.

Direct Materials Purchases Budget

For the Month Ended August 31

Genuine Spice Inc.

For the Month Ended August 31

Production Budget

Genuine Spice Inc.

23

1

21