CHAPTER 23

OPERATIONAL BUDGETING

Brief Learning

Exercises Topic Objectives Skills

B. Ex. 23.1 Budgeting philosophies 23-3 Analysis, judgment

B. Ex. 23.2 Cash flow at Body Builders 23-1, 23-5 Analysis, judgment

B. Ex. 23.3 Production budget 23-4 Analysis

B. Ex. 23.4 Estimating direct materials inventory 23-4 Analysis

B. Ex. 23.5 Benefits of budgeting 23-2

Analysis, communication,

judgment

B. Ex. 23.6 Elements of the budget 23-4, 23-5 Analysis

B. Ex. 23.7 Flexible budgets 23-6 Analysis

B. Ex. 23.8 Operating expense budget 23-4, 23-5 Analysis

B. Ex. 23.9 Cost of budgeting systems 23-2, 23-3

Analysis, communication,

judgment

B. Ex. 23.10 Evaluating managers with flexible budgets 23-6

Analysis, communication,

judgment

Learning

Exercises Topic Objectives Skills

23.1 Budgeting purchases and cash payments 23-4, 23-5 Analysis

23.2 Budgeting labor costs 23-4, 23-5 Analysis

23.3 Production budgets 23-4, 23-5 Analysis

23.4 Production and direct materials budget 23-4, 23-5 Analysis, judgment

23.5 Budgeting for prepayments 23-4, 23-5 Analysis

23.6 Budgeting for interest expense 23-4, 23-5 Analysis

23.7 Preparing a flexible overhead budget 23-6 Analysis

23.8 Budgeting cash receipts 23-4, 23-5 Analysis

23.9 Budgeting an ending cash balance 23-4, 23-5 Analysis

23.10 Preparing a flexible budget 23-6 Analysis

23.11 More on flexible budgeting 23-6 Analysis

23.12 Budget estimates 23-2, 23-3

Analysis, communication,

judgment

23.13 Budgeting manufacturing overhead 23-4, 23-5 Analysis

23.14 Establishing budget amounts 23-2, 23-3

Analysis, communication,

judgment

23.15 Real World: Home Depot’s budget goals 23-2, 23-3

Analysis, communication,

judgment, research

OVERVIEW OF BRIEF EXERCISES, EXERCISES, PROBLEMS, AND CRITICAL

THINKING CASES

Problems

Sets A, B

Topic

Learning

Objectives

Skills

23.1 A,B

Budgeting production, inventories, and cost

of sales

23-4, 23-5 Analysis

23.2 A,B Short budgeting problem 23-4, 23-5 Analysis

23.3 A,B Budgeting for cash 23-4, 23-5 Analysis

23.4 A,B Estimating borrowing requirements

23-1, 23-2,

23-4, 23-5

Analysis, communication,

judgment

23.5 A,B Budgeted income statement and cash budget

23-1, 23-2,

23-4, 23-5

Analysis, communication,

judgment

23.6 A,B Preparing a cash budget

23-1, 23-2,

23-4, 23-5

Analysis, communication,

judgment

23.7 A,B Preparing and using a flexible budget

23-2, 23-4 –

23-6

Analysis, communication,

judgment

23.8 A,B Flexible budgeting

23-2, 23-4 –

23-6

Analysis, communication,

judgment

Critical Thinking Cases

23.1 Budgeting in a nutshell 23-2, 23-5

Analysis, communication,

judgment

23.2 An ethical dilemma 23-1–23–3

Analysis, communication,

judgment

23.3 Cash budgeting 23-1, 23-2 Analysis,

communication, judgment

23.4

Real World: Medlin Accounting

Shareware

(Internet) Budgeting shareware

23-2, 23-6

Analysis, communication,

research, technology

23. 5 Budgeting and internal controls 23-4 Analysis,

(Ethics, fraud, and corporate governance) communication, judgment

DESCRIPTIONS OF PROBLEMS AND CRITICAL THINKING CASES

Problems (Sets A and B)

Renfrow International/Frowren Domestic 25 Easy

Budget such quantities and amounts as the planned production of

finished goods, cost of goods manufactured, finished goods

inventory, and the cost of goods sold.

Lakeland Corporation/Harlow Corporation 20 Medium

Budget such quantities and amounts as the planned production of

finished goods, cost of goods manufactured, finished goods

inventory, and the cost of goods sold.

Barnum Distributors/Barley, Inc. 50 Strong

Prepare a cash budget for one month.

Fromer Corporation/Peter Corporation 40 Strong

Analyze collection patterns for accounts receivable and accounts

payable. Assess the company’s ability to generate adequate cash flow

to service additional debt.

Rizzo’s/Snyder’s 30 Strong

Analyze a budgeted income statement and a cash budget, and

determine why income recognition differs from cash flow.

23.6 A,B Marley Wholesale/Marlow Industries 60 Strong

Prepare a monthly cash budget for three months in support of a loan

application. Determine whether a scheduled loan repayment can be

met at the end of the period.

23.7 A,B Snells/Eight Flags 50 Medium

Prepare a statement comparing actual results with a flexible budget

and comment on the company’s performance.

23.8 A,B Braemar Saddlery/XL Industries 45 Medium

An excellent problem for demonstrating the importance of flexible

budgeting. Due to an increase in production, the production

department exceeds its budget by large amounts. The student is asked

to prepare a flexible budget showing that the company actually did

very well in controlling costs.

23.5 A,B

23.3 A,B

23.4 A,B

Below are brief descriptions of each problem and case. These descriptions are accompanied by the

estimated time (in minutes) required for completion and by a difficulty rating. The time estimates

assume use of the partially filled-in working papers.

23.1 A,B

23.2 A,B

Critical Thinking Cases

23.1

Budgeting in a Nutshell 30 Medium

A short budgeting case that shows the interrelationships among

budgeted financial statements. but more importantly, it provides an

opportunity for students to review the relationships between cash

flows and accrual accounting. A real favorite.

23.2

An Ethical Dilemma 20 Medium

A company in need of bank financing has inflated its master

budget figures due to a large receivable with a questionable

likelihood of being collected. The company’s CPA is aware of the

problem and knows that if the company is denied credit, his

accounting firm will not be paid. Students must decide whether the

role of a CPA is to serve the client or to serve the client’s

creditors.

23.3 Cash Budgeting 20 Medium

The case describes six steps of cash budgeting for businesses and

individuals. Students are asked about strategies for managing cash

flows when inflows and outflows are mismatched. Students write a

paragraph explaining how a personal cash budget would help

them

23.4 Budgeting Shareware 30 Medium

Internet

Student is asked to explore free software available on the Internet

to help companies with budgeting.

23.5 Budgeting and Internal Controls 30 Medium

Ethics, Fraud & Corporate Governance

Students trace an error due to an internal control weakness through

multiple budgets and consider how strong internal controls can

help prevent these errors.

SUGGESTED ANSWERS TO DISCUSSION QUESTIONS

1.

2.

a.

The process of preparing the budget forces management to consider all aspects of the

3.

4.

5.

Preparation of the sales budget is an early step in the budgeting process because many budgeted

Planning is the process of setting financial and operational goals, including cost levels, and

The most widely used budgeting “philosophy” is to set budgeted amounts at reasonable and

achievable levels. A second approach is to set these amounts at levels achievable only under

A business may expect to benefit from preparing a formal budget in several ways, including

(three required):

Responsibility budgets are subsections of the master budget showing only the business activities

6.

7.

8.

9.

10.

First, consider the Behavioral approach. The fundamental assumption under this approach is

that managers will be motivated by budgets that are set at reasonable and achievable levels .

The average collection period in days is determined by dividing the number of days per year

A flexible budget may be geared to any volume level and therefore can be based on the actual

If a budgeted expenditure can be directly influenced by the manager responsible for such an

When companies undergo periods of rapid growth, increased demand for their products can

12.

13.

14.

15.

Disadvantages highlighted by the authors include: (1) Budgets are often applied too

Fixed costs should be divided into committed costs and controllable costs because only the

A rolling budget is a budget that always covers the upcoming twelve months by adding a new

Cash budget estimates and operating budget estimates can be very different because of timing

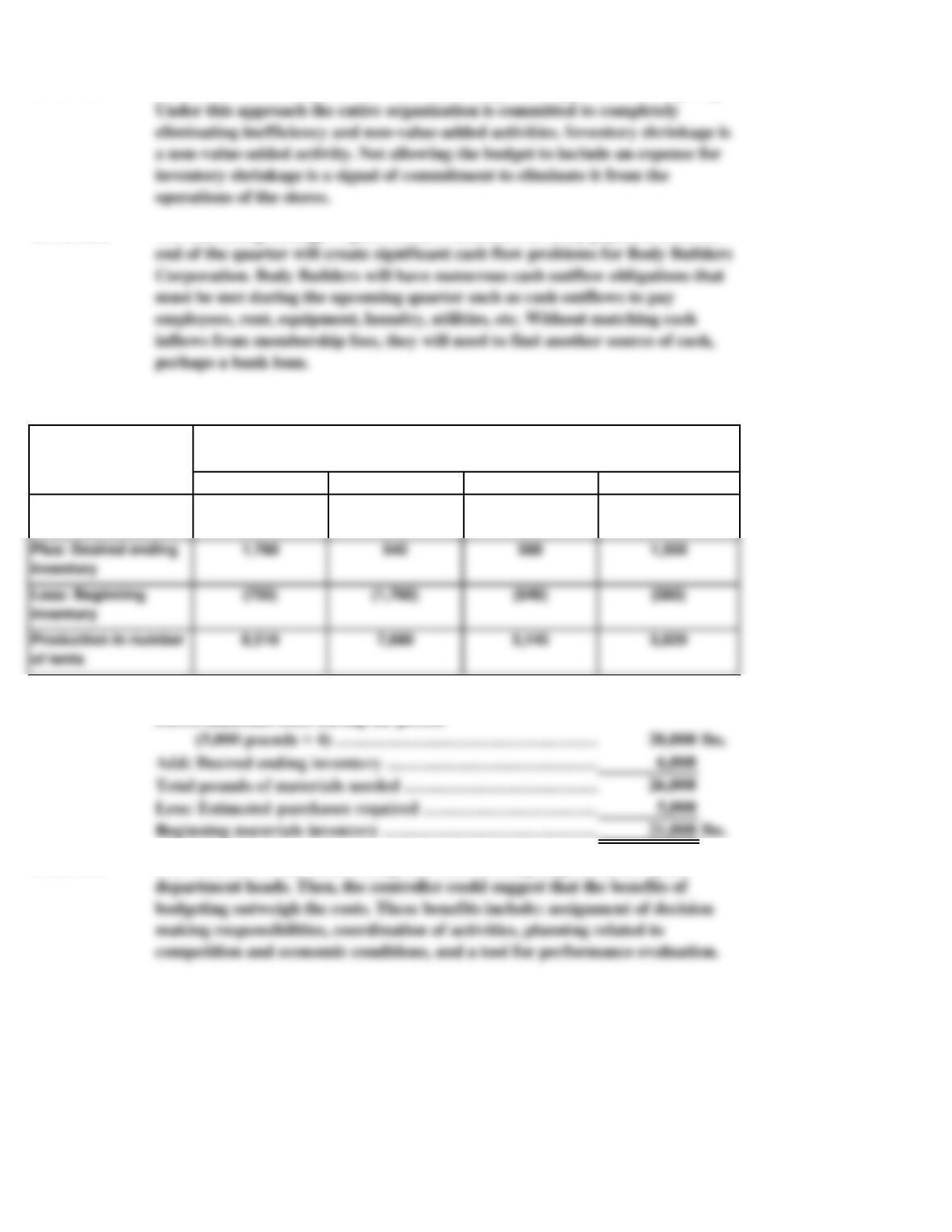

B. Ex. 23.1

B. Ex. 23.2

B. Ex. 23.3

Q1 Q2 Q3

7,500 8,800 3,200

B. Ex. 23.4

Direct materials used during the period

B. Ex. 23.5

The controller could acknowledge the costs of budgeting discussed by the

2,900

Expected sales

Sandy’s Camping Gear

Budgeted Production

SOLUTIONS TO BRIEF EXERCISES

Q4

Renaldo’s is following the Total Quality Management approach of budgeting.

The marketing manager’s plan to allow customers to delay payment until the

1,760 640 580

1,500

Plus: Desired ending

Less: Beginning

B. Ex. 23.7

B. Ex. 23.8

B. Ex. 23.9

B. Ex. 23.10

The variable cost per gallon can be found by finding the difference in total cost

between any two levels of production and dividing that cost difference by the

Because one half of selling and administrative costs are variable, then the

The managers’ complaints are realistic. Managers do consume large amounts of

time thinking about, preparing, and reconsidering the budget. In addition, there

is evidence that managers increase budget requests to allow for increased

The budget overage may have been caused by the expansion of the Dry Goods

Ex. 23.1 a. 300,000$

Ex. 23.2

Total Smoking Packing

Smoking: 500,000 pounds × 0.08 hours/pound

Ex. 23.3 a.

Target ending inventory ………………………………………………………….

Cases budgeted to be available for sale ……………………………………….

Less: Beginning inventory ……………………………………………………..

Selling price per case …………………………………………………………..

Budgeted sales (cases) ………………………………………………………..

Variable overhead ………………………………………………………………..

Direct materials ………………………………………………………………….

Direct labor (1.5 hours/case × $8/hour) ………………………………………..

1,500

SOLUTIONS TO EXERCISES

Direct materials budgeted for use during the year ……………………………

For the Month Ended March 31st

DEEP VALLEY FOODS

Budget for Direct Labor Costs

Sales forecast:

Budgeted sales (in cases) ………………………………………………………

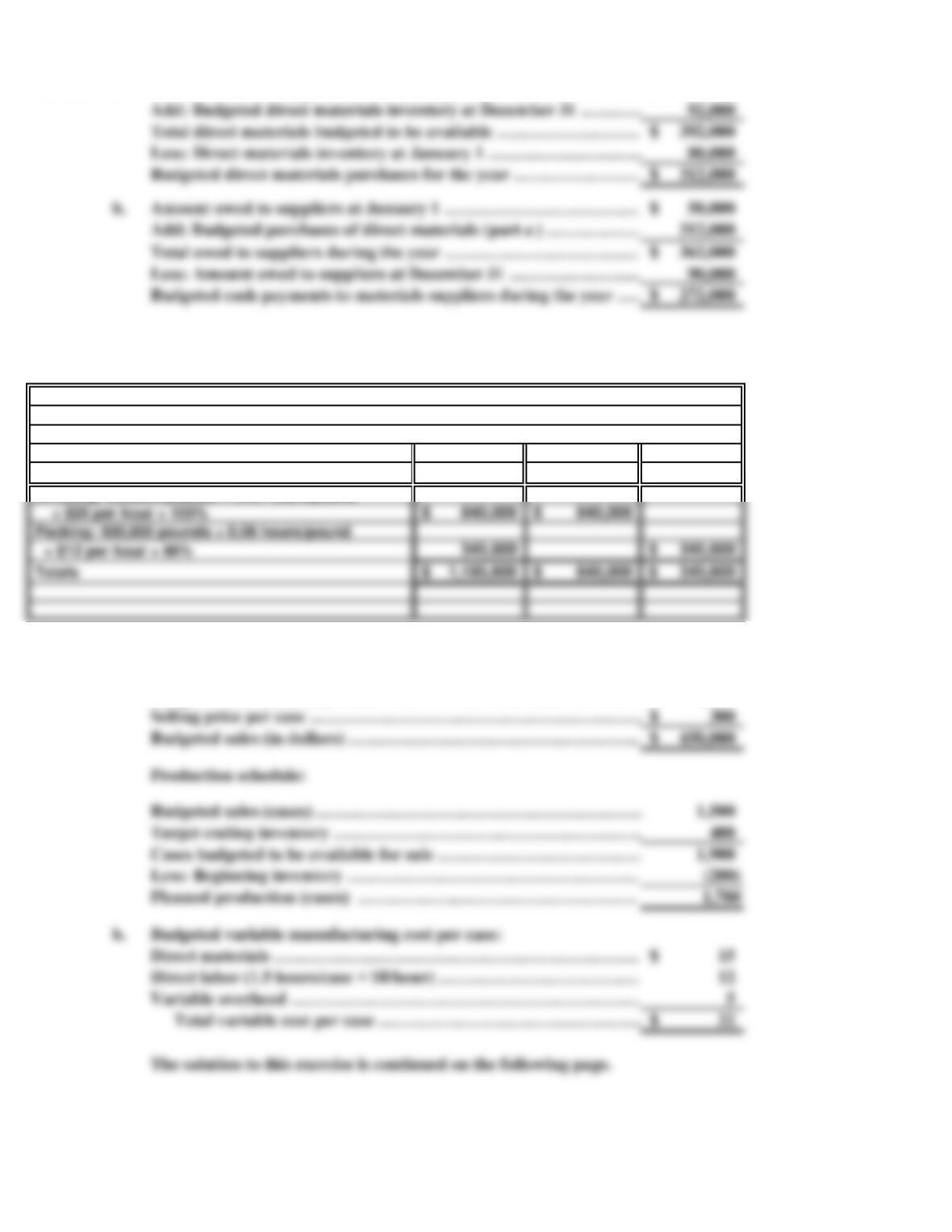

Add: Budgeted direct materials inventory at December 31 ……………….

Total direct materials budgeted to be available ……………………………….

Total owed to suppliers during the year ………………………………………

Less: Amount owed to suppliers at December 31 …………………………….

Less: Direct materials inventory at January 1 ………………………………

Amount owed to suppliers at January 1 ………………………………………

Ex. 23.3

(continued)

c.

Ex. 23.4 a.

Less: Beginning inventory ………………………………………………..

Planned production ……………………………………………

Budgeted sales (units) …………………………………………………….

Target ending inventory ……………………………………………………..

Units budgeted to be available for sale …………………………………….

b.

Glass: (6,460 doors × 6 square feet/door) ……………………………….

129,200 lbs. 38,760 sq. ft.

80,000 lbs. 4,000 sq. ft.

209,200 lbs. 42,760 sq. ft.

(40,000) lbs. (6,000) sq. ft.

169,200 lbs. 36,760 sq. ft.

Raw materials to be purchased

Direct materials available for use ……………….

Less: Beginning inventory ………………..

× Budgeted purchase price

Budgeted direct materials

(units) …………………………………

Materials purchases budget:

Glass

Materials requirements based on planned production of 6,460 doors:

Manufacturing cost budget:

Variable manufacturing costs:

Production schedule:

Steel

Direct materials used ………………………………

Target ending inventory …………………….

d.

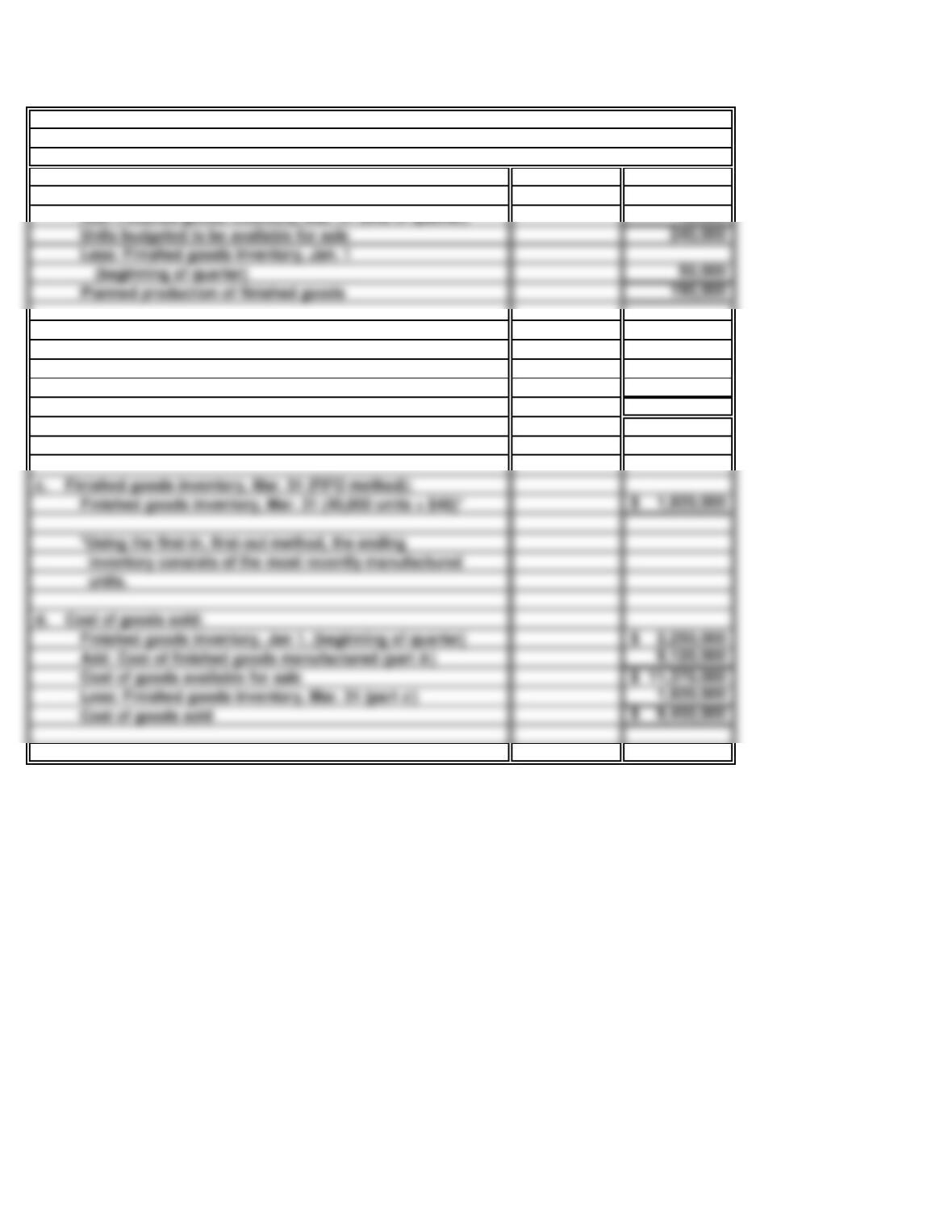

Target ending inventory (cases) × Manufacturing cost per unit

Ending inventory value = $82,000

Variable overhead (1,700 cases × $5/case) …………………………..

Direct materials (1,700 cases × $15/case) ………………………..

Direct labor (1,700 cases × $12/case) …………………………………..

Ending inventory value:

Total variable manufacturing costs ……………………………………..

Add: Fixed manufacturing overhead ……………………………………..

Ex. 23.4

(continued)

c.

Ex. 23.5

500,000$

Lock Tight may wish to increase its ending inventory level of steel if the price of

steel this year is expected to be much lower than the price next year. However,

First, calculate prepayments to be expired during the period:

Total costs and expenses ……………………………………………………….……

Depreciation expense ……………………………………..……………

Amount financed with current payables ………………………………………

Ex. 23.6

February March April

a.

Willmar Corporation

Debt Service Schedule

For February through April

Note Payable at the

Beginning of the month

Budgeted interest expense reported on the February income statement is

computed as follows:

Ex. 23.7

Fixed

Portion

Budgeted

Overhead at

2,800 Hours

$ 2,000 $ 16,000

Ex. 23.8

— within discount period, $880,000 × 70% × 98% ……….

— after discount period, $800,000 × 6% ……………………

— within discount period, $800,000 × 12% × 98% ……..…

— after discount period, $880,000 × 10% …………………

Ex. 23.9 a. $ 500,000

Less: Expenditures ……………………………………………………………….

Collections on January sales ($300,000 × 15%) ……………………………..

Collections on February sales ($400,000 × 30%) ……………………………..

Collections on March sales ($600,000 × 50%) ………………………………..

Total cash available ……………………………………………………………….

Cash balance on March 1 ……………………………………………………..

Estimated cash collections of accounts receivable in February are computed below.

On accounts receivable representing sales in:

Variable Cost Per Hour Formula

($17,000-$12,000) ÷ (3,000 hrs-2,000 hrs.) = $5.00/hr.

Maintenance

Ex. 23-9

(continued)

b. $ 565,000

c. $ 755,000

90,000

210,000

400,000

$ 1,455,000

400,000

Total cash available ………………………………………………………………..

Less: Expenditures …………………………………………………………..

Collections on April sales ($700,000 × 30%) …………………………………

Collections on May sales ($800,000 × 50%) …………………………………..

Ex. 23.10

$ 1,800,000

1,080,000

$ 720,000

450,000

$ 270,000

81,000

$320,000 ÷ 80,000 units = $4 variable expenses per unit.

Sales ($1,600,000 80,000 units = $20 per unit;

Cost of goods sold ($960,000 ÷ 80,000 units = $12 per unit;

Gross profit on sales

Operating expenses [($4 variable expenses per unit* ×

Income taxes ($270,000 × 30%) …………………………………….

Operating income ………………………………………………………..

Flexible budget at 90,000-unit level of activity:

Cash balance on May 1 (from b) ………………………………………………….

Cash balance on April 1 (from a) ………………………………………………

Collections on March sales ($600,000 × 15%) ……………………………………

Ex. 23.11

Flexible

Budget Actual Favorable Unfavorable

341,000$ 320,000$ 21,000$

Ex. 23.12 a.

Manufacturing costs:

*Budgeted variable manufacturing costs are restated from the 10,000 units of production level

b.

To purposely distort budget estimates for personal gain is an unethical practice

and should be avoided. In addition to ethical implications, distorting a sales

To avoid the manipulation of sales forecasts, the company may wish to

Direct materials used*

Upload Games Company

Performance Report—Packaging Department

For the Current Month

11,000 Units

Variances

Total manufacturing costs

Direct labor*

Variable manufacturing

Fixed manufacturing overhead

WELLS ENTERPRISES

Budget for Manufacturing Overhead Costs

Total Dept. I Dept. II

Fixed manufacturing overhead:

Dept. I: 10,000 units × $25

250,000$ 250,000$

Ex. 23.14

Ex. 23.15

1.

2.

3.

4.

5.

Average ticket price

Comparable store sales increase %

Weighted average sales per square foot

Number of customer transactions

Ex. 23.13

Imposed budgets do not generate commitment to budget goals. Also imposed budgets

Home Depot could use the following categories of store data:

Students will have various suggestions for how these data points might be used in

budgeting to set goals for each store and in performance evaluations of store managers.

Average square footage per store

SOLUTIONS TO PROBLEMS SET A

25 Minutes, Easy PROBLEM 23.1A

RENFROW INTERNATIONAL

a. Planned production of finished goods (in units):

Budgeted sales

180,000

Add: Finished goods inventory, end of quarter 33,600

b. Cost of finished goods manufactured:

Planned production of finished goods (in units—part a)168,000

Multiply by: Budgeted manufacturing cost per unit 40$

Cost of finished goods manufactured 6,720,000$

c. Finished goods inventory at quarter-end (average cost):

Finished goods inventory, beginning of quarter

1,396,800$

Add: Cost of finished goods manufactured (part b)6,720,000

Divide by: Units budgeted to be available for sale (part a)213,600

d. Cost of goods sold:

Budgeted cost of goods available for sale (part c)8,116,800$

Less: Finished goods inventory, end of quarter (part c)1,276,800

Cost of goods sold 6,840,000$

Budgeted sales, 180,000 units × $38 (part c)6,840,000$

9,840,000$

Less: Budgeted cost of goods sold (part d)6,840,000

Less: Finished goods inventory, beginning of quarter 45,600

Planned production of finished goods 168,000

20 Minutes, Medium PROBLEM 23.2A

LAKELAND CORPORATION

a. Planned production of finished goods (in units):

Budgeted sales

200,000

Add: Finished goods inventory, Mar. 31 (end of quarter) 40,000

b. Cost of finished goods manufactured:

Planned production of finished goods (part a)190,000

Multiply by: Budgeted manufacturing cost per unit (given) 48$

Cost of finished goods manufactured (190,000 units x $48) 9,120,000$

Finished goods inventory, Mar. 31 (40,000 units × $48)* 1,920,000$

Add: Cost of finished goods manufactured (part b)9,120,000

Cost of goods available for sale 11,370,000$

Less: Finished goods inventory, Mar. 31 (part c)1,920,000

Cost of goods sold 9,450,000$

Units budgeted to be available for sale 240,000

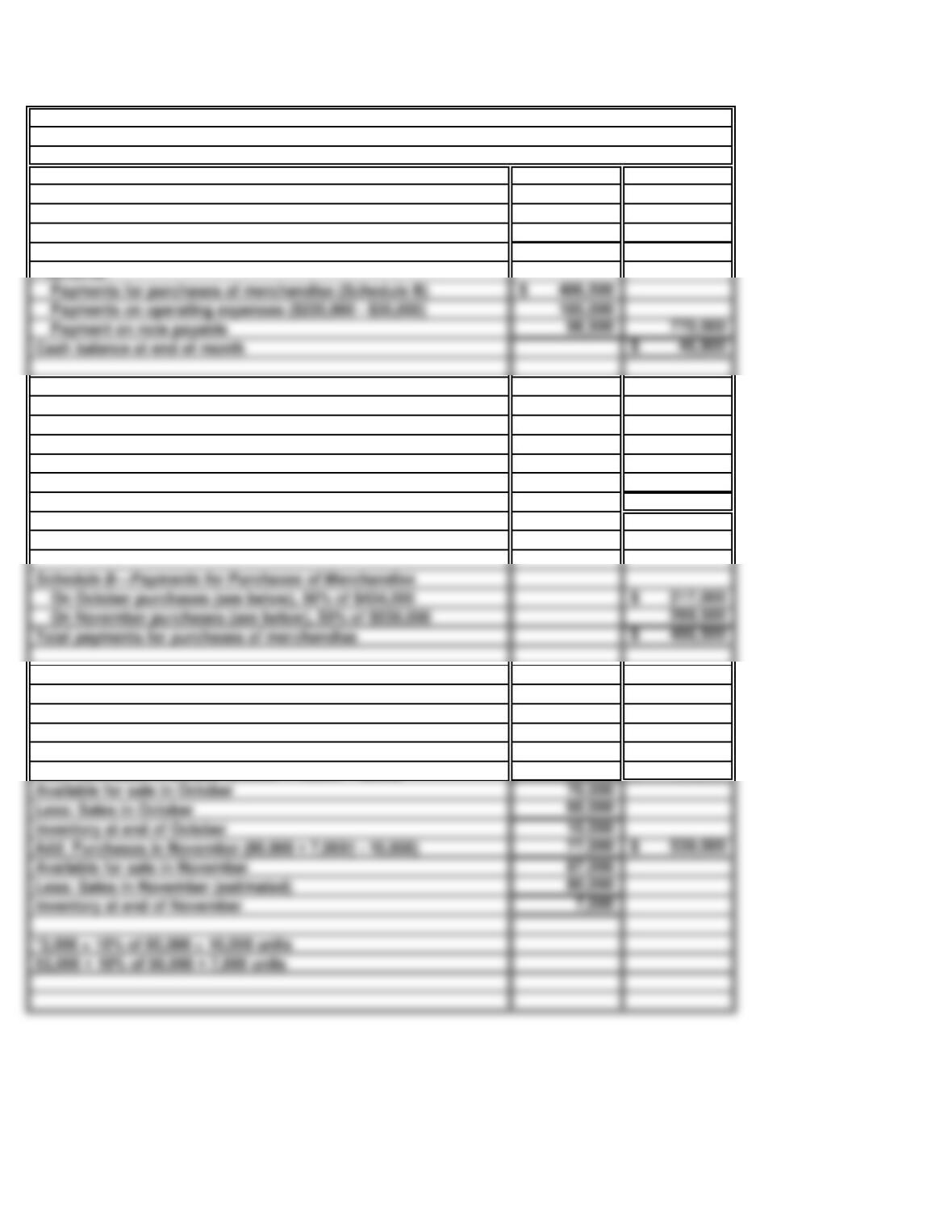

50 Minutes, Strong PROBLEM 23.3A

BARNUM DISTRIBUTORS

BARNUM DISTRIBUTORS

Cash Budget

For the Month Ended November 30

Cash balance at beginning of month

29,600$

Receipts:

Collections on receivables (Schedule A)

778,800$

Sale of fully depreciated equipment 8,400 787,200

Total cash available 816,800$

Payments:

Schedule A—Collections on Receivables in November

September sales: 7% × (40,000 × $11)—actual

30,800$

October sales: 20% × (60,000 × $11)—actual 132,000

November sales: 70% × (80,000 × $11)—estimated 616,000

Total collections on receivables 778,800$

Schedule B—Payments for Purchases of Merchandise

On November purchases (see below), 50% of $539,000 269,500

Total payments for purchases of merchandise 486,500$

Purchases

Computation of Purchases Units ($7 Per Unit)

Inventory at end of September (2,000 + 10% of 60,000)

8,000

Add: Purchases in October (60,000 + 10,000* – 8,000) 62,000 434,000$

Less: Sales in October 60,000

Less: Sales in November (estimated) 80,000

486,500$

Payment on note payable 98,500 770,000

Cash balance at end of month 46,800$