CHAPTER 23 Performance Evaluation for Decentralized Operations

Prob. 23–1A (FIN MAN); Prob. 8–1A (MAN)

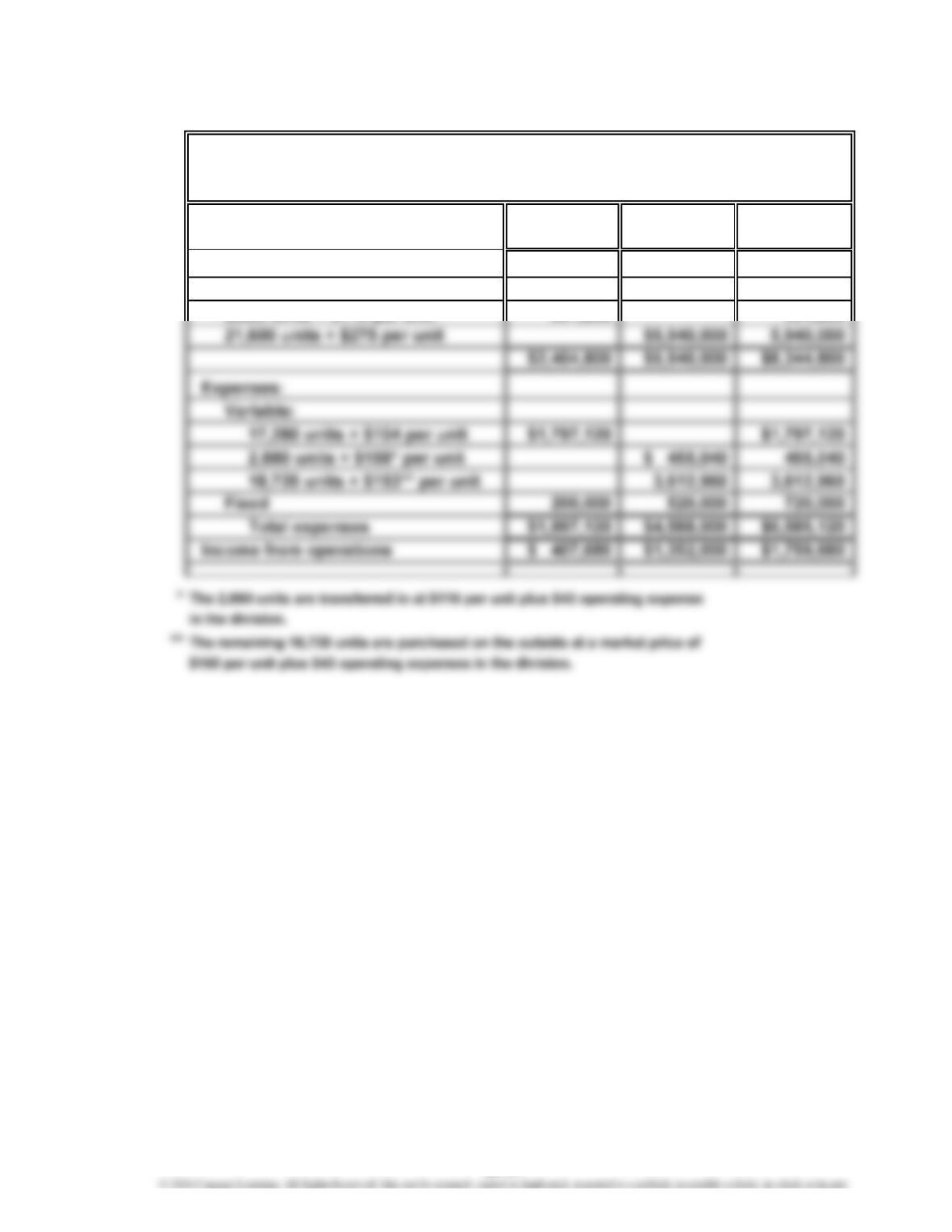

1.

Over Under

Budget Actual Budget Budget

Customer service salaries $ 546,840 $ 602,350 $ 55,510

Insurance and property taxes 114,660 110,240 $ 4,420

Distribution salaries 872,340 861,200 11,140

2. The customer service and marketing salaries are significantly over budget. The

director should investigate the cause of these results. One possibility is that the

PROBLEMS

VALOTIC TECH, Inc.

Budget Performance Report—Director, Consumer Products Division

For the Month Ended January 31, 2016

23-21

CHAPTER 23 Performance Evaluation for Decentralized Operations

Prob. 23–2A (FIN MAN); Prob. 8–2A (MAN)

1.

West Central

Revenues $1,032,000 $1,872,000

Operating expenses 618,240 1,166,940

Income from operations before service

Supporting Schedule:

Service department charge rates for the two service departments, Customer Support

and Legal, are determined as follows:

West Central Total

Number of customer contacts… 6,000 9,000 20,000

Number of hours billed…………

…

2,160 1,890 5,400

Note (A) East Division: ($400,000 ÷ 20,000 contacts) × 5,000 contacts

West Division: ($400,000 ÷ 20,000 contacts) × 6,000 contacts

Note: The Shareholder Relations Department and general corporate officers’ salaries

TRAXONIA RAILROAD INC.

Divisional Income Statements

For the Quarter Ended December 31, 2016

East

East

$870,000

563,300

5,000

1,350

23-22

CHAPTER 23 Performance Evaluation for Decentralized Operations

Prob. 23–2A (FIN MAN); Prob. 8–2A (MAN) (Concluded)

2. The CEO evaluates the three divisions using income from operations as a

percent of revenues (profit margin). This measure is calculated for the three

3. To: CEO

The method used to evaluate the performance of the divisions should be

reevaluated. The present method identifies the amount of income from

operations per dollar of earned revenue. However, this company requires a

23-23

CHAPTER 23 Performance Evaluation for Decentralized Operations

Prob. 23–3A (FIN MAN); Prob. 8–3A (MAN)

1.

Sales

Cost of goods sold

Cereal Division:

Snack Cake Division:

$480,000 $8,000,000

$8,000,000 $4,000,000

Retail Bakeries Division:

$682,500 $9,750,000

$9,750,000 $6,500,000

×

2. Rate of Return

on Investment = Profit Margin × Investment Turnover

ROI =

Invested Assets

=

Rate of Return

on Investment

ROI = ×

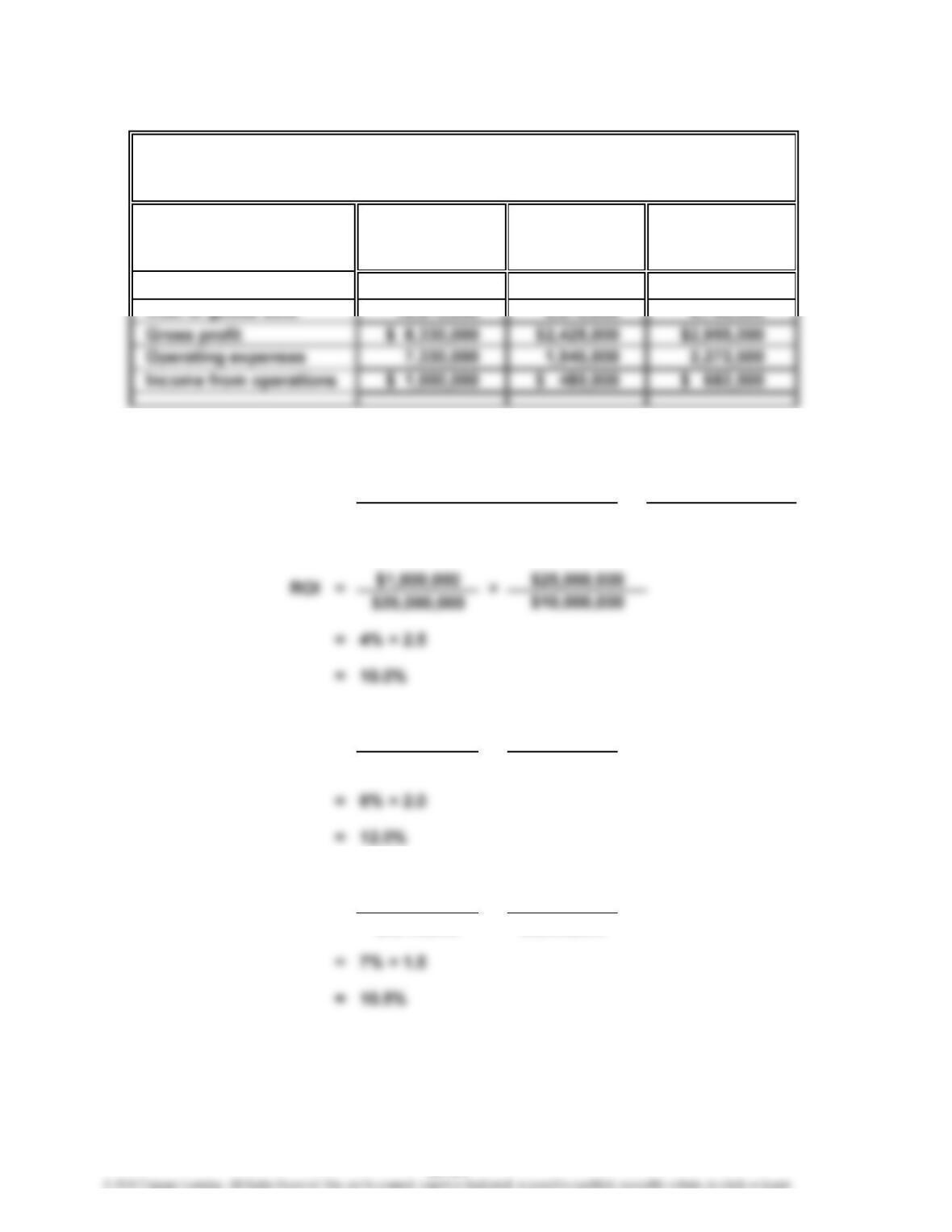

THE CRUNCHY GRANOLA COMPANY

Divisional Income Statements

For the Year Ended June 30, 2016

Sales

Cereal Snack Cake

Retail

Bakeries

6,795,000

Division Division Division

$25,000,000 $8,000,000 $9,750,000

×

Sales

Income from Operations

16,670,000 5,575,000

23-24

CHAPTER 23 Performance Evaluation for Decentralized Operations

Prob. 23–3A (FIN MAN); Prob. 8–3A (MAN) (Concluded)

3. Per dollar of invested assets, the Snack Cake Division is the most profitable

of the three divisions. Assuming that the rates of return on investments do not

23-25

CHAPTER 23 Performance Evaluation for Decentralized Operations

Prob. 23–4A (FIN MAN); Prob. 8–4A (MAN)

2.

Sales

Cost of goods sold

1

$2,480,000 + $105,000

2

$2,500,000 – $312,500

3

$2,480,000 – $560,000

2,585,000

$2,905,000

Proposal 3

$3,500,000

Proposal 1

For the Year Ended December 31, 2016

Proposal 2

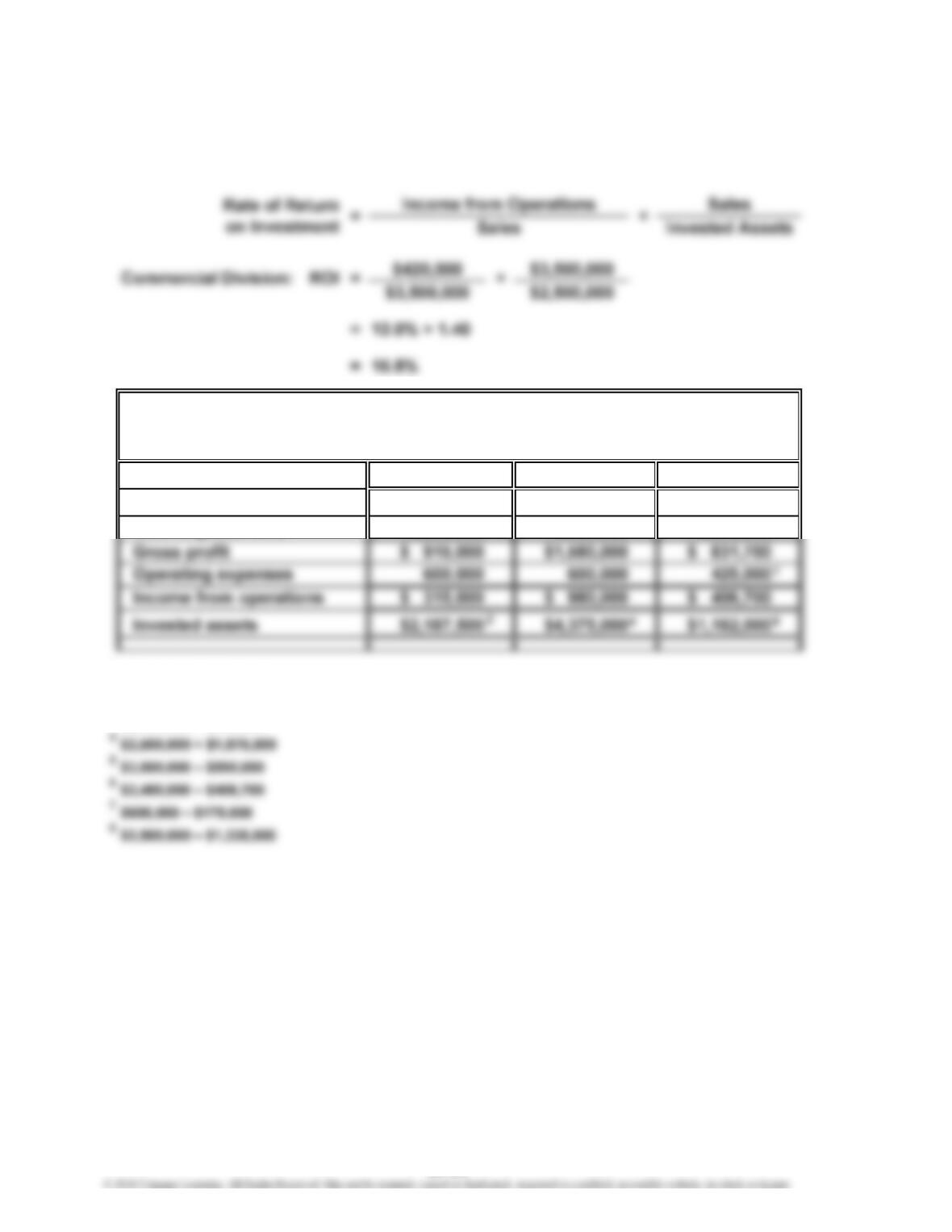

MAXELL MANUFACTURING INC.—COMMERCIAL DIVISION

Estimated Income Statements

1. =

1,920,000 2,073,300

$3,500,000

Profit Margin × Investment Turnover

Rate of Return

on Investment

1

3

5

6

23-26

CHAPTER 23 Performance Evaluation for Decentralized Operations

Prob. 23–4A (FIN MAN); Prob. 8–4A (MAN) (Concluded)

$315,000 $3,500,000

$3,500,000 $2,187,500

$980,000 $3,500,000

$3,500,000 $4,375,000

$406,700 $2,905,000

$2,905,000 $1,162,000

4. Proposal 3 would yield a rate of return on investment of 35.0%. Proposal 2 would

yield a rate of return on investment of 22.4%.

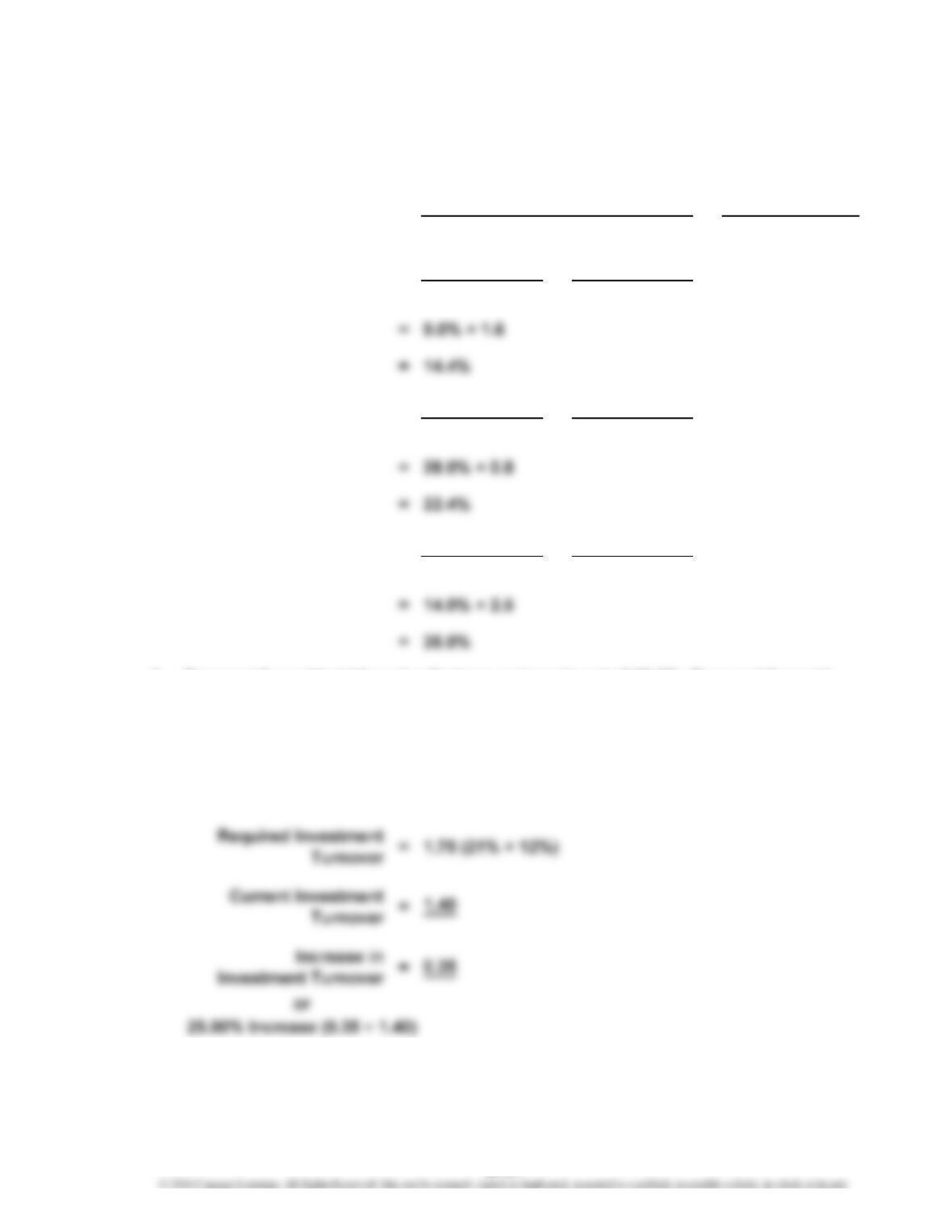

5.

=

3. = Profit Margin × Investment Turnover

12% × Required Investment Turnover

ROI =

Sales

Rate of Return

on Investment

Rate of Return

on Investment

Rate of Return

on Investment

21%

×

×

×

Profit Margin × Investment Turnover

= ×

Sales

Income from Operations

Invested Assets

ROI =

ROI =

=

Proposal 1:

Proposal 2:

Proposal 3:

23-27

CHAPTER 23 Performance Evaluation for Decentralized Operations

Prob. 23–5A (FIN MAN); Prob. 8–5A (MAN)

1.

Sales

Sales

Income from Operations

Invested Assets

Sales

Rate of Return

on Investment

=

×

2. = Profit Margin × Investment Turnover

Rate of Return

on Investment

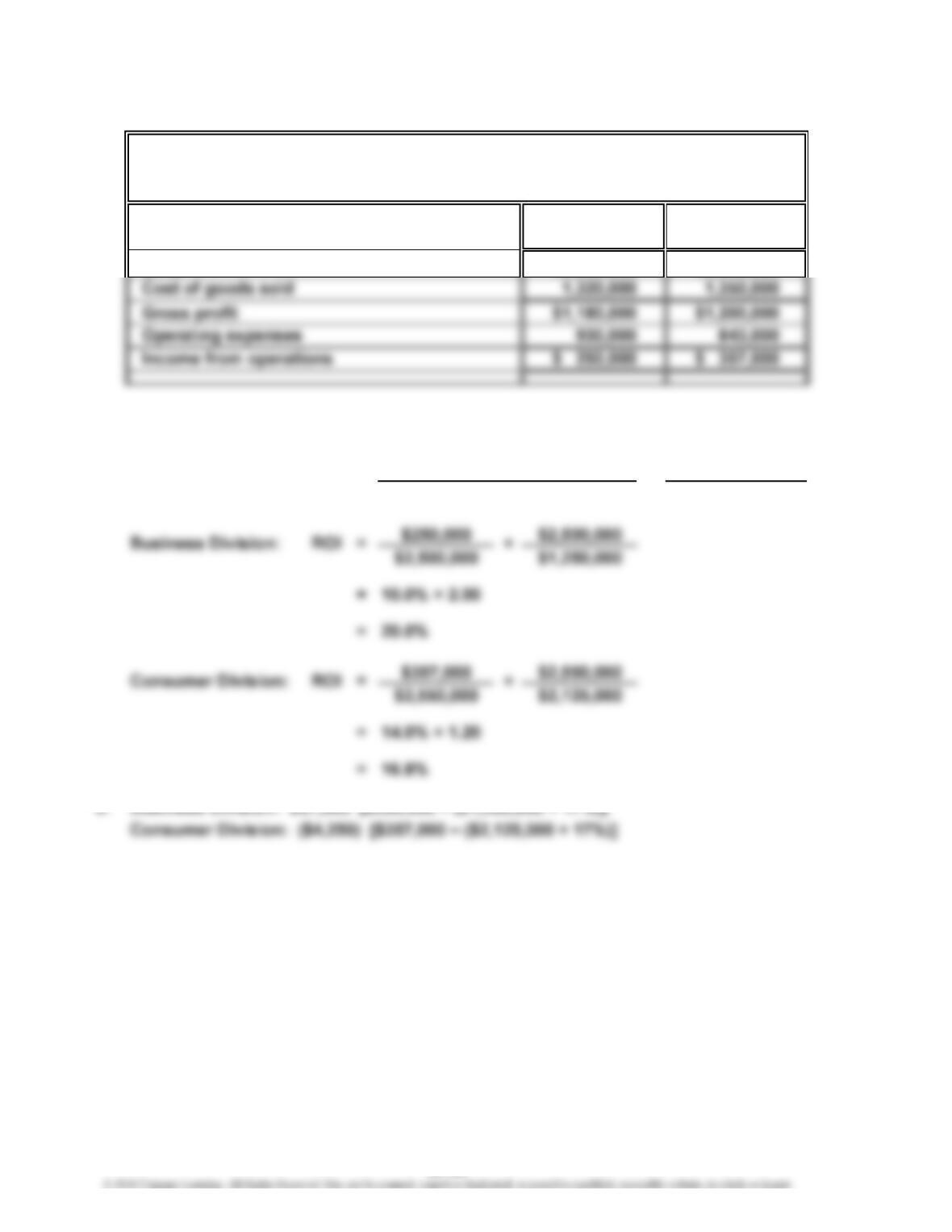

PAVONE COMPANY

Divisional Income Statements

For the Year Ended December 31, 2016

$2,550,000

Business Consumer

Division Division

$2,500,000

23-28

CHAPTER 23 Performance Evaluation for Decentralized Operations

Prob. 23–5A (FIN MAN); Prob. 8–5A (MAN) (Concluded)

4. On the basis of income from operations, the Consumer Division generated

$107,000 ($357,000 – $250,000) more income from operations than did the

Business Division. However, income from operations does not consider the

amount of invested assets in each division. On the basis of the rate of return on

23-29

CHAPTER 23 Performance Evaluation for Decentralized Operations

Prob. 23–6A (FIN MAN); Prob. 8–6A (MAN)

1. No. When unused capacity exists in the supplying division (the Consumer

2. The Consumer Division’s income from operations would increase by $31,680:

Increase in Consumer Variable

(Supplying) Division’s Transfer Cost Units

Income from Operations = Price – per Unit × Transferred

$31,680 =($115 –$104) × 2,880

By selling to the Commercial Division, the Consumer Division earns $11 per unit

on these sales.

The Commercial Division’s income from operations would increase by $100,800:

Increase in Commercial

(Purchasing) Division’s Market Transfer Units

23-30

CHAPTER 23 Performance Evaluation for Decentralized Operations

Prob. 23–6A (FIN MAN); Prob. 8–6A (MAN) (Continued)

3.

Consumer Commercial

Division Division Total

Sales:

14,400 units × $144 per unit $2,073,600 $2,073,600

2,880 units × $115 per unit 331,200 331,200

GARCON INC.

Divisional Income Statements

For the Year Ended December 31, 2016

23-31

CHAPTER 23 Performance Evaluation for Decentralized Operations

Prob. 23–6A (FIN MAN); Prob. 8–6A (MAN) (Concluded)

4. The Consumer Division’s income from operations would increase by $63,360:

Increase in Consumer Variable

(Supplying) Division’s Transfer Cost Units

Income from Operations = Price – per Unit × Transferred

$63,360 =($126 –$104) × 2,880

By selling to the Commercial Division, the Consumer Division earns $22 per

unit on these sales.

The Commercial Division’s income from operations would increase by $69,120:

Increase in Commercial

Garcon Inc.’s total income from operations would increase by the same amount

as in part (2), $132,480:

Variable

Increase in Garcon Market Cost Units

5. a. Any transfer price greater than the Consumer Division’s variable expenses

per unit of $104 but less than the market price of $150 would be acceptable.

b. If the division managers cannot agree on a transfer price, a price of $127*

23-32

CHAPTER 23 Performance Evaluation for Decentralized Operations

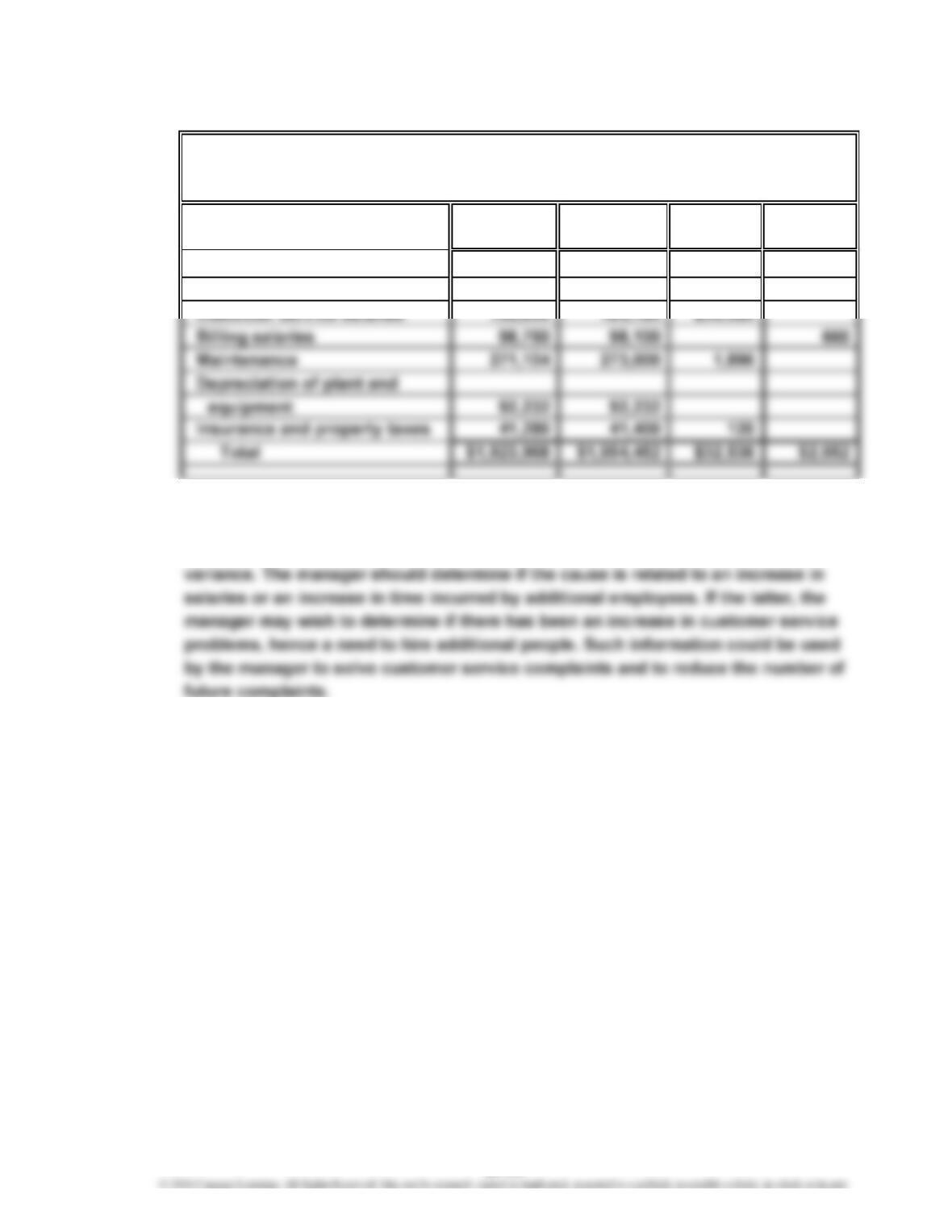

Prob. 23–1B (FIN MAN); Prob. 8–1B (MAN)

1.

Over Under

Budget Actual Budget Budget

Sales salaries $ 819,840 $ 818,880 $ 960

System administration salaries 448,152 447,720 432

2. The customer service salaries exceed the budget by 20% of budget ($30,520 ÷

$152,600). The manager should request additional detailed information about the

customer service department. There are several possible reasons for the budget

ADELSON INC.

Budget Performance Report—Supervisor, Eastern District

For the Month Ended December 31, 2016

23-33

CHAPTER 23 Performance Evaluation for Decentralized Operations

Prob. 23–2B (FIN MAN); Prob. 8–2B (MAN)

1.

South West

Revenues $5,673,000 $5,130,000

Operating expenses 4,494,890 3,770,050

Income from operations before service

Supporting Schedule:

Service department charge rates for the two service departments, Dispatching and

Equipment Management, are determined as follows:

South West Total

Number of scheduled trains……

…

1,105 845 2,600

Number of railroad cars in

inventory…………………………

…

8,400 9,600 24,000

Note (A) East Division: ($182,000 ÷ 2,600 scheduled trains) × 650

West Division: ($182,000 ÷ 2,600 scheduled trains) × 1,105

THOMAS RAILROAD COMPANY

Divisional Income Statements

For the Quarter Ended December 31, 2016

North

$3,780,000

2,678,500

North

650

6,000

23-34

CHAPTER 23 Performance Evaluation for Decentralized Operations

Prob. 23–2B (FIN MAN); Prob. 8–2B (MAN) (Concluded)

2. The CEO evaluates the three regions using income from operations as a percent

of revenues. This measure is calculated for the three regions as follows:

3. To: CEO

The method used to evaluate the performance of the regions should be

reevaluated. The present method identifies the amount of income from operations

per dollar of earned revenue. However, a railroad company requires a significant

23-35