CHAPTER 22 Budgeting

Prob. 22–2B

1.

Unit Sales Unit Selling

Volume Price Total Sales

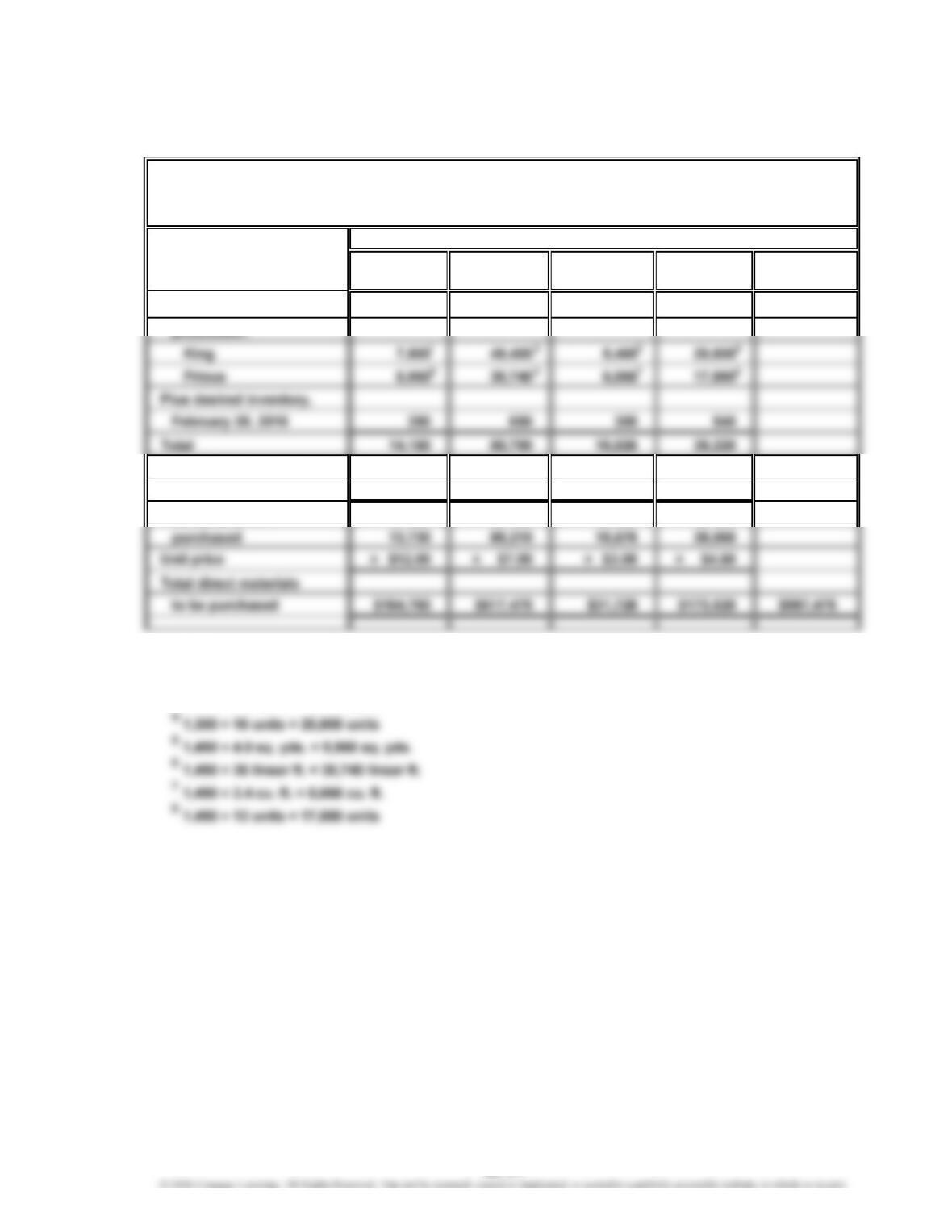

King:

Northern Domestic 610 $780 $ 475,800

Southern Domestic 340 780 265,200

Prince:

Northern Domestic 750 $550 $ 412,500

Southern Domestic 440 550 242,000

2.

King Prince

Expected units to be sold 1,310 1,480

For the Month Ending February 28, 2016

Units

Product and Area

ROYAL FURNITURE COMPANY

Sales Budget

For the Month Ending February 28, 2016

ROYAL FURNITURE COMPANY

Production Budget

22-40

CHAPTER 22 Budgeting

Prob. 22–2B (Continued)

3.

Fabric Wood Filler Springs

(sq. yds.) (linear ft.) (cu. ft.) (units) Total

Required units for

Less estimated inventory,

February 1, 2016 420 580 250 660

Total units to be

1

1,300 × 6.0 yds. = 7,800 sq. yds.

2

1,300 × 38 linear ft. = 49,400 linear ft.

3

1,300 × 4.2 cu. ft. = 5,460 cu. ft.

ROYAL FURNITURE COMPANY

Direct Materials Purchases Budget

For the Month Ending February 28, 2016

Direct Materials

22-41

CHAPTER 22 Budgeting

Prob. 22–2B (Concluded)

4.

Framing Cutting Upholstery

Department Department Department Total

Hours required for production:

King

1

1,560 650 1,040

ROYAL FURNITURE COMPANY

Direct Labor Cost Budget

For the Month Ending February 28, 2016

22-42

CHAPTER 22 Budgeting

Prob. 22–3B

1.

Unit Sales Unit Selling

Volume Price Total Sales

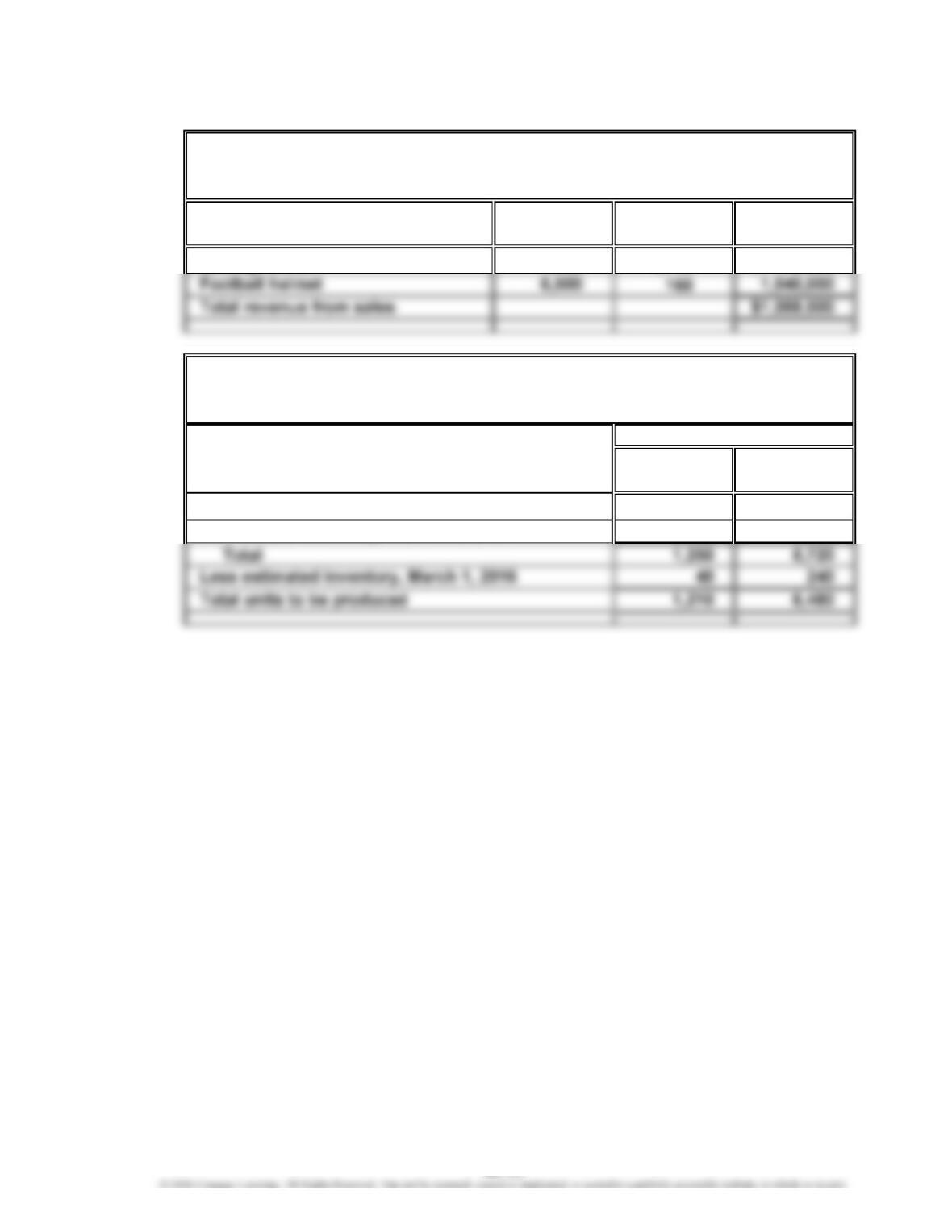

Batting helmet 1,200 $ 40 $ 48,000

2.

Batting Football

Helmet Helmet

Expected units to be sold 1,200 6,500

Plus desired inventory, March 31, 2016 50 220

For the Month Ending March 31, 2016

Units

GOLD MEDAL ATHLETIC CO.

Sales Budget

For the Month Ending March 31, 2016

GOLD MEDAL ATHLETIC CO.

Production Budget

22-43

CHAPTER 22 Budgeting

Prob. 22–3B (Continued)

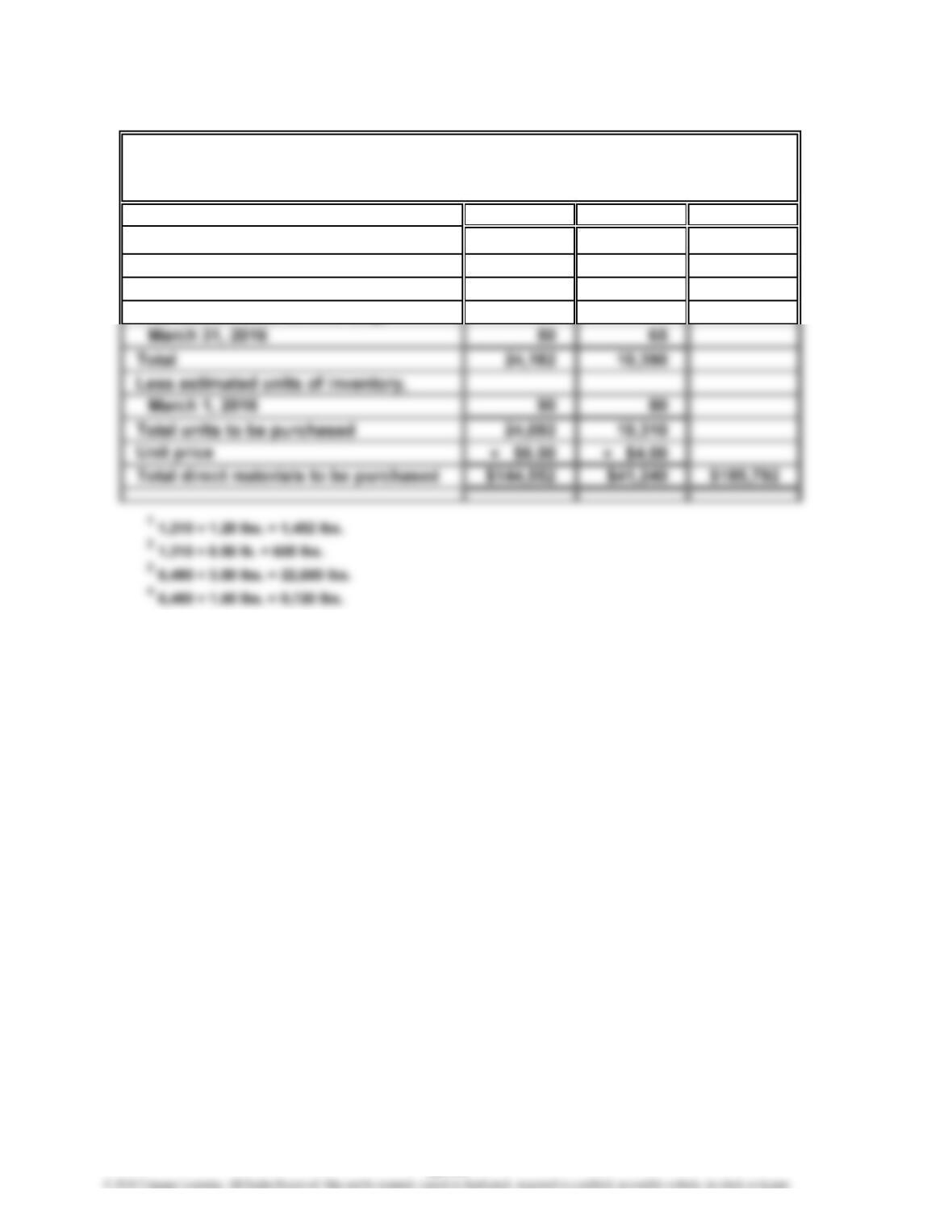

3.

Plastic Foam Lining Total

Units required for production:

Batting helmet 1,452 605

Football helmet 22,680 9,720

Plus desired units of inventory,

GOLD MEDAL ATHLETIC CO.

Direct Materials Purchases Budget

For the Month Ending March 31, 2016

12

34

22-44

CHAPTER 22 Budgeting

Prob. 22–3B (Continued)

4.

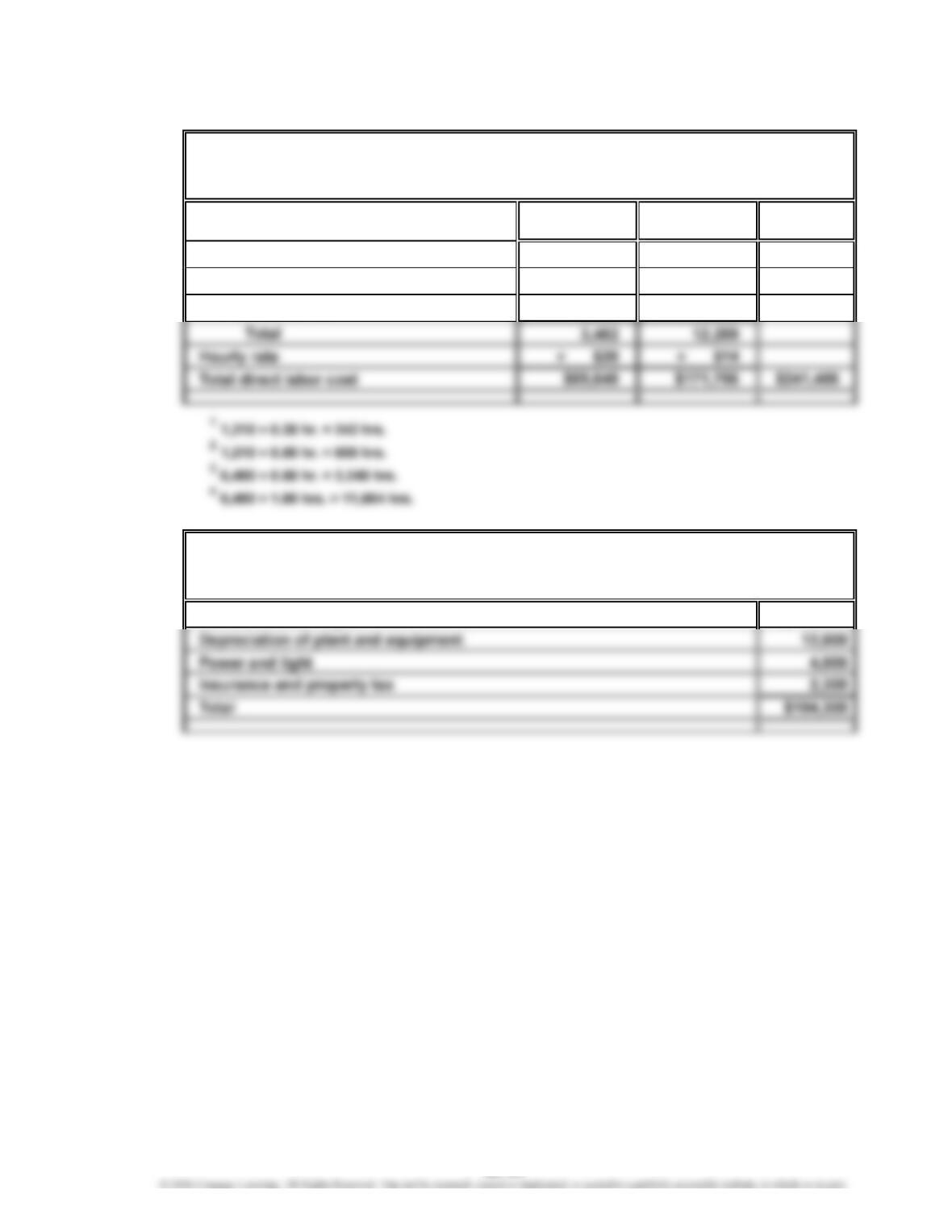

Molding Assembly

Department Department Total

Hours required for production:

Batting helmet 242 605

Football helmet 3,240 11,664

5.

Indirect factory wages $ 86,000

Factory Overhead Cost Budget

For the Month Ending March 31, 2016

GOLD MEDAL ATHLETIC CO.

Direct Labor Cost Budget

For the Month Ending March 31, 2016

GOLD MEDAL ATHLETIC CO.

12

34

22-45

CHAPTER 22 Budgeting

Prob. 22–3B (Continued)

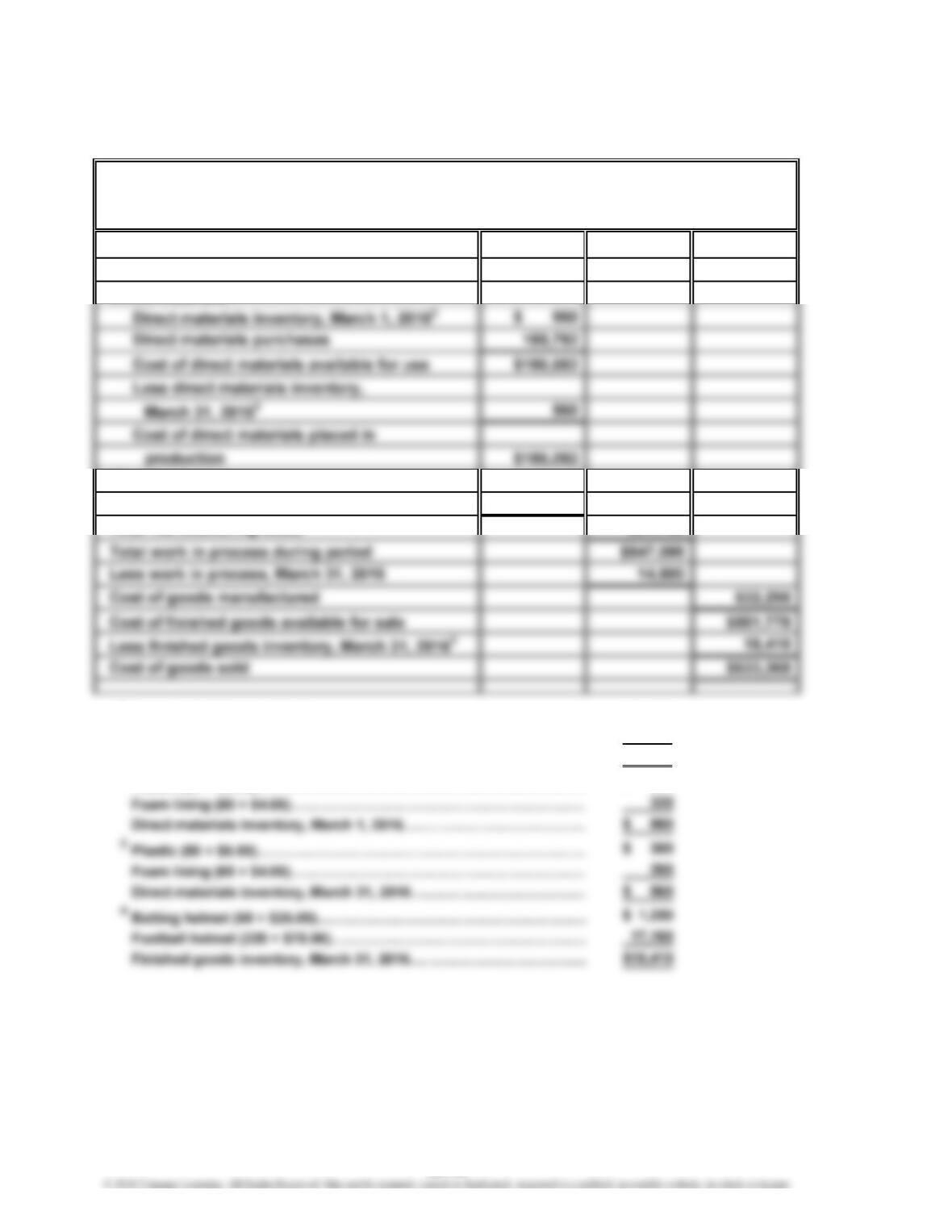

6.

Finished goods inventory, March 1, 2016

1

$ 19,480

Work in process inventory, March 1, 2016 $ 15,300

Direct materials:

Direct labor 241,406

Factory overhead 104,300

Total manufacturing costs 531,798

1

Batting helmet (40 × $25.00)…………………………………………………

…

$ 1,000

Football helmet (240 × $77.00)………………………………………………

…

18,480

Finished goods inventory, March 1, 2016…………………………………

…

$19,480

2

Plastic (90 × $6.00)……………………………………………………………

…

$ 540

…

…

…

…

…

GOLD MEDAL ATHLETIC COMPANY

Cost of Goods Sold Budget

For the Month Ending March 31, 2016

22-46

CHAPTER 22 Budgeting

Prob. 22–3B (Concluded)

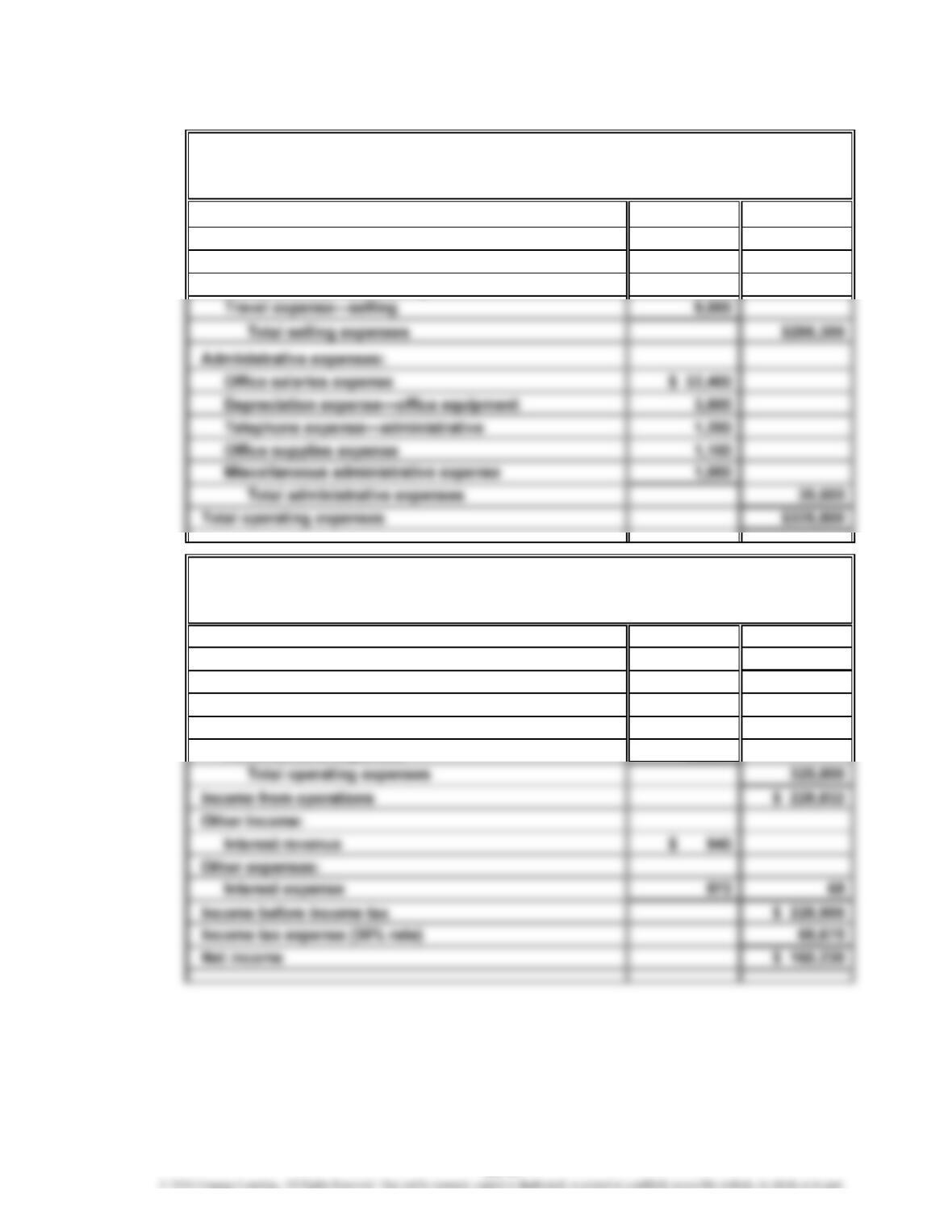

7.

Selling expenses:

Sales salaries expense $184,300

Advertising expense 87,200

Telephone expense—selling 5,800

8.

Revenue from sales $1,088,000

Cost of goods sold 533,368

Gross profit $ 554,632

Operating expenses:

Selling expenses $286,300

Administrative expenses 39,500

GOLD MEDAL ATHLETIC CO.

Budgeted Income Statement

For the Month Ending March 31, 2016

GOLD MEDAL ATHLETIC CO.

Selling and Administrative Expenses Budget

For the Month Ending March 31, 2016

22-47

CHAPTER 22 Budgeting

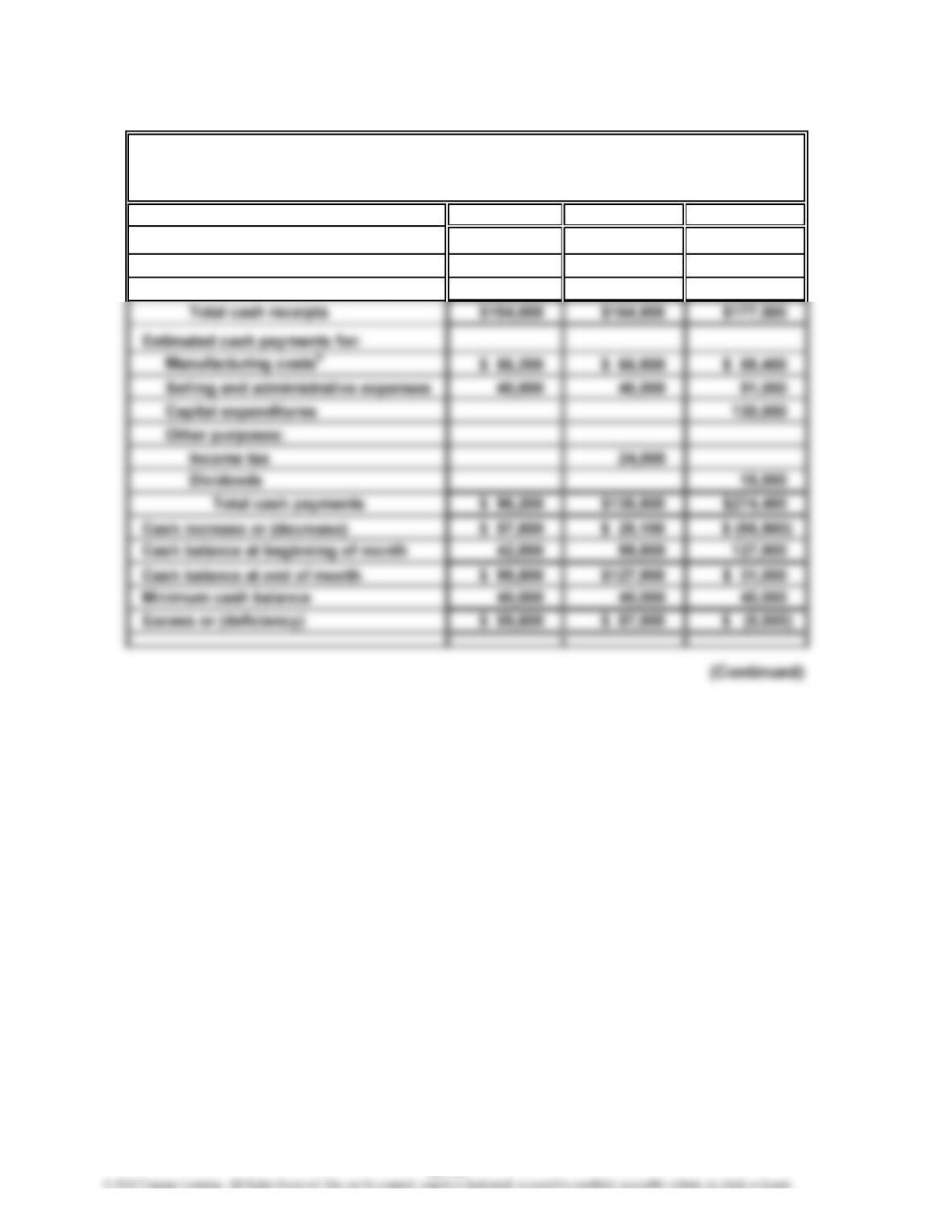

Prob. 22–4B

1.

June July August

Estimated cash receipts from:

Cash sales $ 16,000 $ 18,500 $ 20,000

Collection of accounts receivablea138,000 146,400 157,500

MERCURY SHOES INC.

For the Three Months Ending June 30, 2016

Cash Budget

22-48

CHAPTER 22 Budgeting

Prob. 22–4B (Concluded)

Computations:

a

Collections of accounts receivable: June July August

April sales………………………………………

…

$ 48,000

1

$120,000 × 40% = $48,000

2

$150,000 × 60% = $90,000

3

$150,000 × 40% = $60,000

b

Payments for manufacturing costs: June July August

Payment of accounts payable,

beginning of month balance

c

……………

…

$13,000 $10,800 $14,000

Accounts payable, June 1 balance = $13,000

($66,000 – $12,000) × 20% = $10,800

($82,000 – $12,000) × 20% = $14,000

2. The budget indicates that the minimum cash balance will not be maintained in

August. This is due to the capital expenditures requiring significant cash outflows

1

22-49

CHAPTER 22 Budgeting

Prob. 22–5B

1.

Sales1$456,000

Cost of goods sold:

Direct materials2$114,000

Operating expenses:

Selling expenses:

Sales salaries and commissions5$64,100

Advertising 13,200

Miscellaneous sellin

g

ex

p

enses610,500

13,800 units × $120

23,800 units × $30

33,800 units × $8.40

MESA PUBLISHING CO.

Budgeted Income Statement

For the Year Ending December 31, 2017

22-50

CHAPTER 22 Budgeting

Prob. 22–5B (Concluded)

2.

Current assets:

Cash 1 $106,660

Accounts receivable 23,800

Inventories:

Finished goods $16,900

Current liabilities:

1Cash balance, December 31, 2017:

Balance, January 1, 2017…………………………………………………………

…

$ 26,000

Add: Cash from operations

Net income………………………………………………………………… $114,660

Depreciation of plant and equipment………………………………… 4,000 118,660

$181,760

LIABILITIES

MESA PUBLISHING CO.

Budgeted Balance Sheet

December 31, 2017

ASSETS

22-51

CHAPTER 22 Budgeting

CP 22–1

Cam should reject Megan’s request to charge the convention-related costs against

July’s budget. This is just one example of many attempts to slide expenses into

different budget periods than when actually incurred. This is a common issue that

CP 22–2

a. The hospital’s new budget method is clearly an example of a flexible budget.

The budget changes with changes in underlying activity, such as patient-days.

Patient-days are the number of patients multiplied by the number of days in the

b. The advantage of a flexible budget is to accurately plan variable costs of the

hospital with changes in the underlying activity base. Using a static budget would

create actual deviations from budget that would be difficult to interpret. Managers

CASES & PROJECTS

22-52

CHAPTER 22 Budgeting

CP 22–3

a. The budget information indicates that the actual expenditures by the Operations

Department exceeded what was planned by $12,000. The bank manager may ask

b. The bank manager does not know if the actual resources consumed by the

Operations Department are the right amount of resources for doing the right

things. In other words, this budget doesn’t say anything about the actual work

of the Operations Department and how much cost this work consumes. The bank

manager doesn’t have a good sense if there is waste in the department or not. The

CHAPTER 22 Budgeting

CP 22–4

Domino’s could use a master budget to plan operations consistent with the sales

forecast. The sales forecast could be used to develop the production budget for

pizzas. The sales and production budgets would be identical because there would

be no finished goods inventory for cooked pizzas. The sales (production) budget

would be used to develop a direct materials purchases budget. For example, the

pizza ingredients, packaging materials, beverages, and other materials could be

22-54

CHAPTER 22 Budgeting

CP 22–5

a. The amount of actual expenditures was less than budget for the first 10 months of

the budget year. As the end of the budget year-end neared, the manager spent the

remaining excess budget and, as a result, went over the budget for May and June.

The amount spent for the year was equal to the total amount budgeted because

b. The budget system encourages this type of wasteful behavior. The budget could

be redesigned in a number of ways. The budget could be designed to flex with

underlying activity and adjusted monthly. Thus, the manager would always have

budgeted resources for changes in underlying activity. For example, if the number

of prisoners in the jail increased, then the budget would increase proportionately.

A manager with the flexible budget would be less likely to “reserve” the budget

during the year because an activity change would be automatically reflected in the

22-55

CHAPTER 22 Budgeting

CP 22–6

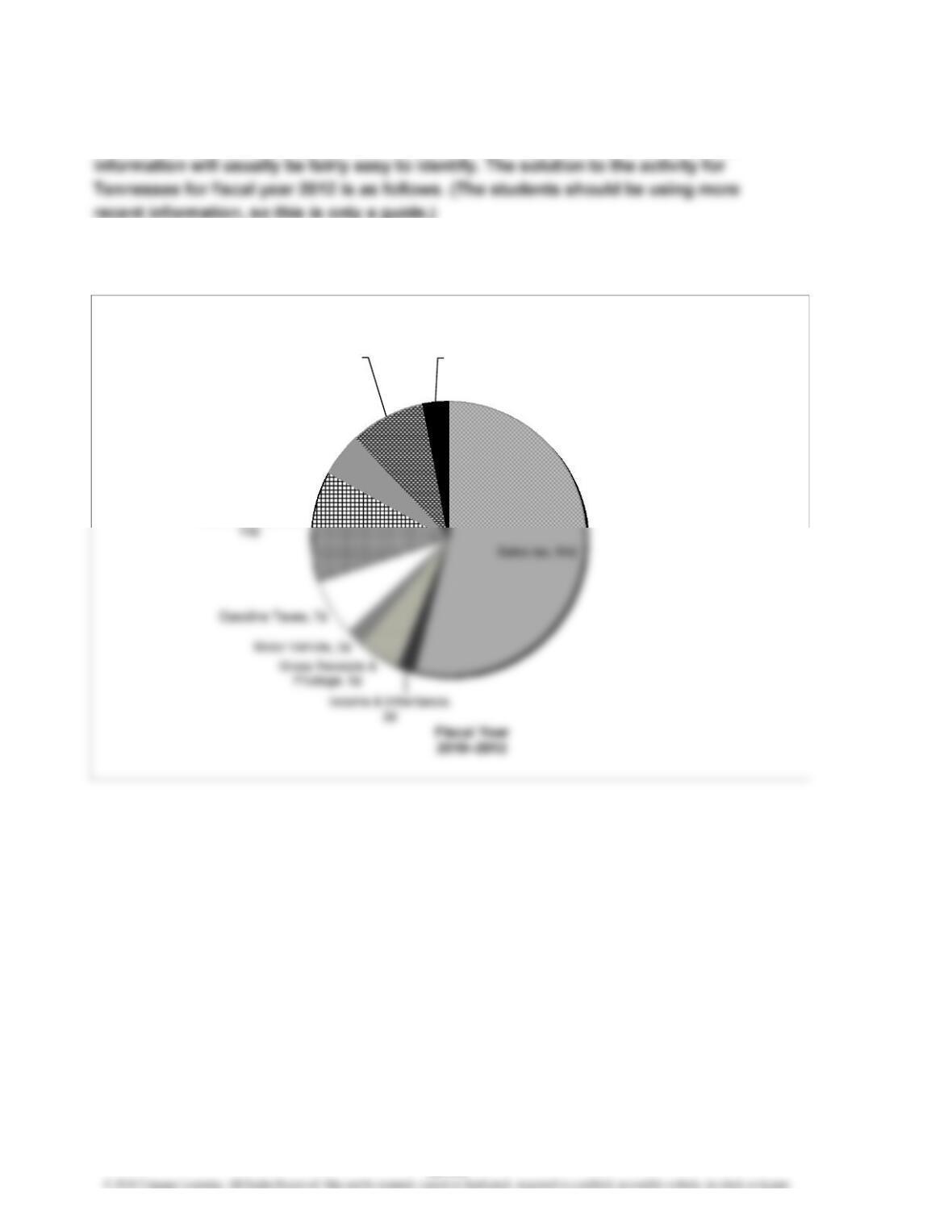

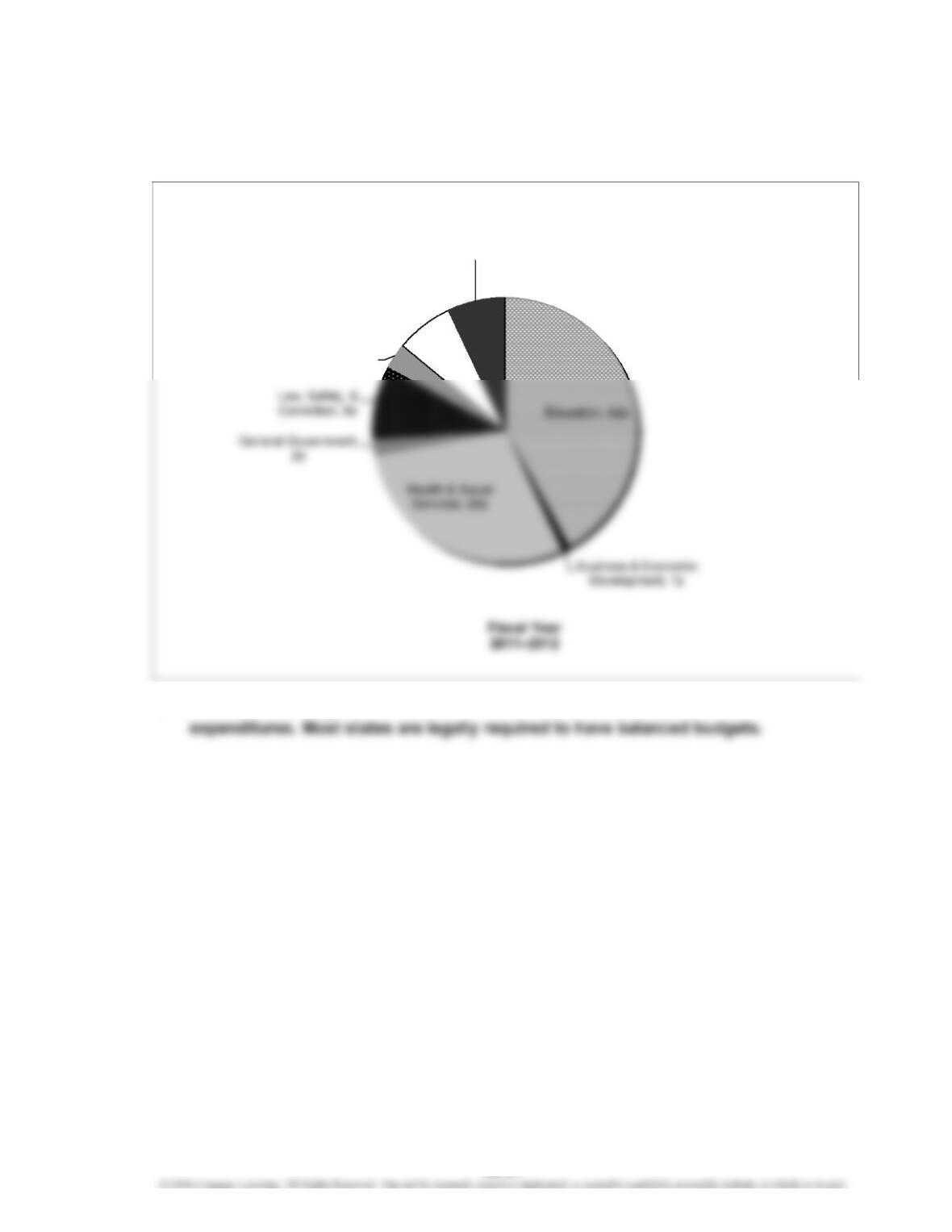

Most states have home pages and budget information available online. The budget

1. Where Your Tax Dollar Comes From

(in cents)

Franchise & Excise,

Insurance & Banking,

5¢

All Other Taxes, 9¢

Tobacco, Beer, &

Alcoholic Beverages,

3¢

22-56

CHAPTER 22 Budgeting

CP 22–6 (Concluded)

2.

3. Tennessee’s budget is in balance. That is, state revenues equal state

Where Your State Dollar Goes

(in cents)

Resources &

Regulation, 3¢

Transportation, 7¢

Cities & Counties, 7¢

22-57