Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

22-1

CHAPTER 22

MASTER BUDGETS AND PLANNING

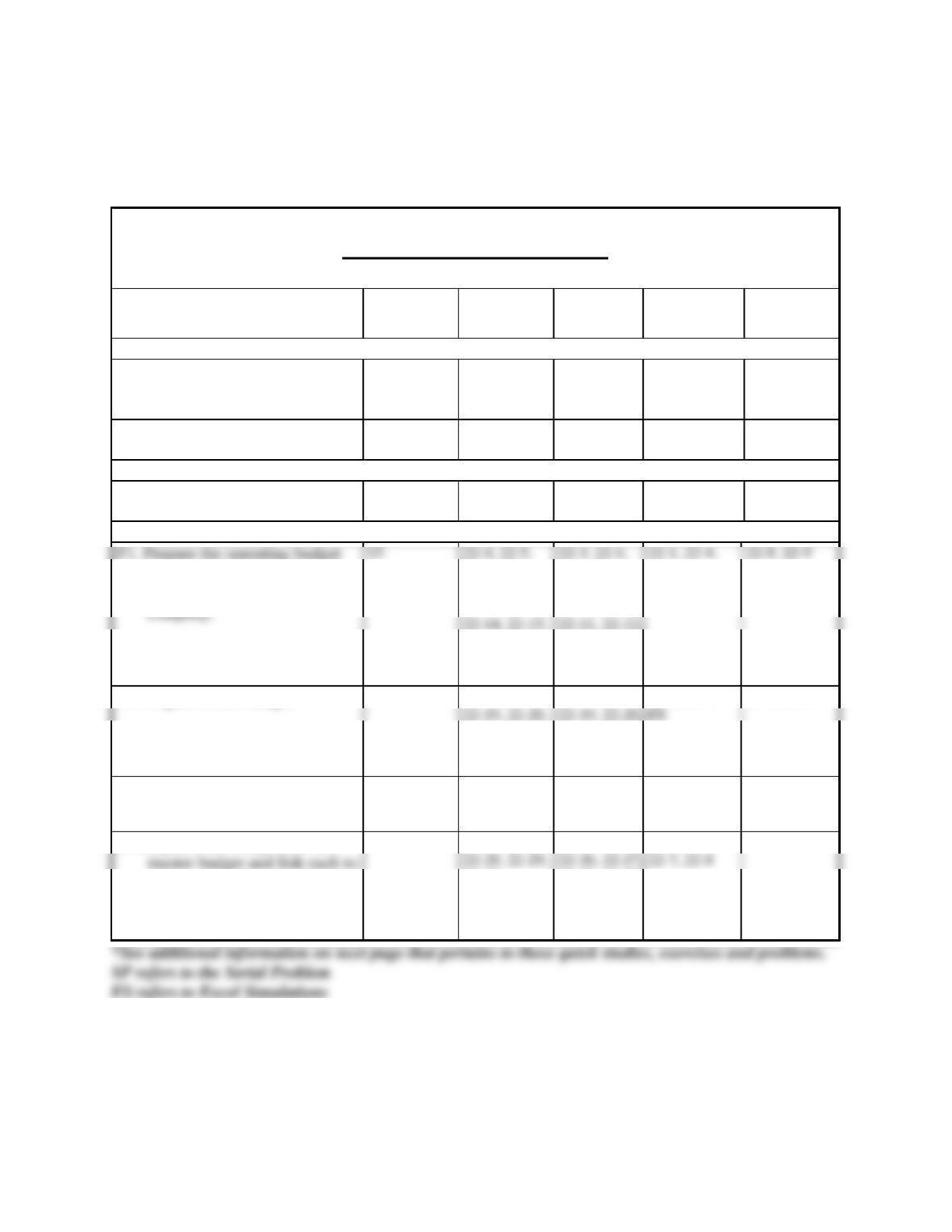

Related Assignment Materials

Student Learning Objectives

Discussion

Questions

Quick

Studies*

Exercises*

Problems*

Beyond the

Numbers

Conceptual objectives:

C1. Describe the benefits of

budgeting and the process of

budget administration.

1, 2, 3, 4, 5, 6,

9, 12, 13, 14

22-1, 22-2

22-1

22-3, 22-5,

22-7

C2. Describe a master budget and

the process of preparing it.

7, 8, 10, 11

22-3

22-2

22-1

22-4, 22-8

Analytical objectives:

A1. Analyze expense planning

using activity-based budgeting.

22-31, 22-32

22-35

22-6

Procedural objectives:

components of a master budget

— for a manufacturing

22-7, 22-8,

22-9, 22-11,

22-12, 22-13,

22-16, 22-17,

22–18, 22-33

22-5, 22-6,

22-7, 22-8,

22-9, 22-10,

22-13, 22-14,

22-15, 22-16

P2. Prepare a cash budget.

11

22-6, 22-10,

22-21, 22-22,

22-23, 22-24

22-17, 22-18,

22-21, 22-22,

22–23

22-2, 22-4,

22-1, 22-2

P3 Prepare budgeted financial

statements.

22–25

22-33, 22-34

22-3, 22-4, SP

P4 Prepare each component of a

the budgeting process—for a

merchandising company.

(Appendix 22A)

22-26, 22-27,

22–30

22-24, 22-5,

22-28, 22–29,

22-30, 22–31,

22-32,

22-5, 22-6,

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

22-2

Additional Information on Related Assignment Material

Connect

Available on the instructor’s course-specific website) repeats all numerical Quick Studies, all Exercises

Connect Insight

The first and only analytics tool of its kind, Connect Insight is a series of visual data displays that are each framed

by an intuitive question and provide at-a-glance information regarding how an instructor’s class is performing.

Connect Insight is available through Connect titles.

The Serial Problem (SP) for Success Systems continues in this chapter.

General Ledger

Assignable within Connect, General Ledger (GL) problems offer students the ability to see how transactions post

from the general journal all the way through the financial statements. Critical thinking and analysis components are

added to each GL problem to ensure understanding of the entire process. GL problems are auto-graded and provide

instant feedback to the student.

Excel Simulations

Synopsis of Chapter Revision

NEW opener—TaTa Topper and entrepreneurial assignment.

Revised discussion, with new exhibit, of budgeting as a management tool.

Revised discussion of benefits of budgeting.

Added graphic on benefits of budgeting.

Revised discussion of budgeting and human behavior.

New Decision Insight on zero-based budgeting.

New NTK on the benefits and potential costs of budgeting.

Revised master budget process exhibit to reflect types of activities.

Added graphics showing formulas to compute direct materials requirements and direct labor cost.

Revised discussions of direct materials, direct labor, and factory overhead budgets.

Added discussion and exhibits of estimated cash receipts with alternative collection timing and uncollectible

accounts.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

22-3

Chapter Outline

I. Budging as a Management Tool—ensures that activities of

employees and departments contribute to meeting the company’s

overall goals. Budgeting is the process of planning future business

actions and expressing them as formal plans.

A. Budget Process⎯ process of planning future business activities.

1. Budget⎯Formal statement of a company’s plans, expressed in

monetary terms.

3. Useful in controlling operations.

4. Budgetary control process refers to management’s use of

budgets to see that planned objectives are met.

B. Benefits of Budgeting—fulfill key managerial functions of

planning and controlling. Benefits include:

1. Focuses on future opportunities and threats to the

3. Helps coordinate activities so all employees and departments

understand and work towards company’s overall goals.

4. Written budget effectively communicate management’s

5. Budgets can be used to motivate employees. Provide goals to

attain or exceed.

C. Budgeting and Human Behavior

2. Three guidelines to ensure positive effect on employees’

attitudes.

a. Employees affected by budget should be involved in its

preparation to increase commitment to meeting it

(participatory budgeting).

b. Goals should be challenging but attainable.

D. Potential Negative Outcomes of Budgeting

1. Managers must be aware of negative outcomes

Notes

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

22-4

Chapter Outline

a. Employees may understate the sales budget and/or

overstate the expense budget to allow a budgetary slack in

meeting targets.

E. Budget Reporting and Timing

2. To help control operations, the annual budget usually is

separated into quarterly or monthly budgets.

4. Variances are differences between actual and budgeted

5. Budget Timing – Many companies apply continuous budgeting

by preparing rolling budgets. In continuous budgeting:

a. Company continually revises its budgets as time passes.

c. Management is continuously planning ahead.

II. The Master Budget⎯Formal, comprehensive plan for a company’s

future.

A. Master Budget Components

1. Contains several individual budgets that are linked with each

other to provide a coordinated plan for the company.

3. Typically begins with the sales budgets and ends with the cash

budget and budgeted financial statements.

4. Sequence required; certain budgets cannot be prepared until

Notes

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

22-5

Chapter Outline

B. Operating Budgets⎯Four major types.

1. Sales budget

a. First step in preparing master budget – shows planned unit

sales and expected dollars from those sales

b. Comes from a careful analysis of forecasted economic and

market conditions, business capacity and advertising

plans.

2. Production Budget – shows number of units to be produced in

a period. Is based on the budgeted unit sales in the sales

budget and inventory considerations.

a. Whether company manufacturers or purchases the

products it sells, budgeted future sales volume is primary

factor in inventory management decisions.

b. Companies will keep enough inventory on hand to reduce

risk of running short (called safety stock); provides

protection against lost sales caused by unfulfilled

customer demands or delays in shipments from suppliers.

c. A manufacturer will prepare a production budget. Sales

budget used as basis for production budget.

d. Production budget does not show costs – it is always

expressed in units of product.

e. Units to be produced is determined by:

Budgeted unit sales

f. Use these three steps to complete the production budget:

i. Compute budgeted ending inventory, based on the

Notes

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

22-6

Chapter Outline

g. The production budgeted is used as basis for three

manufacturing budgets.

3. Direct Materials Budget:

shows budgeted costs for direct materials that will be needed

to be purchased to satisfy the estimated production for the

period.

Budgeted units to be produced

x Material requirements per unit

4. Direct Labor Budget:

shows budgeted costs for direct labor that will be needed to

satisfy the period’s estimated production.

Budgeted units to be produced

5. Factory Overhead Budget:

shows budgeted costs for factory overhead that will be needed

to complete the estimated production:

6. Product cost per unit:

With the information from the 3 manufacturing

budgets, the product cost per unit can be computed.

Notes

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

22-7

Chapter Outline

7. Selling Expense Budget:

a. Based on sales volume (either dollars or units depending

8. General and Administrative Expense Budget:

a. Plan showing predicted operating expenses not included in

9. Capital Expenditures Budget:

a. Shows estimated amounts to be received from plant asset

disposals, and estimated amounts to be spent on

purchasing additional plant assets; assumes proposed

C. Financing Budgets

1. Cash Budget⎯shows expected cash inflows and outflows

during budget period. Managing cash is vital for the firm’s

success. Helps company meet cash balance goal.

Beginning cash balance

+ Budgeted cash receipts

Notes

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

22-8

Chapter Outline

b. Budgeted cash receipts include:

i. Expected cash sales – from sales budget.

ii. Expected cash collections of accounts receivable.

iii. Other expected cash receipts such as interest revenue,

sale of assets, etc.

c. Budgeted cash payments include:

i. Budgeted cash payments from selling expense budget

and general and administrative expense budget.

ii. Expected cash payments for interest expense and

income taxes.

iii. Expected cash purchases for a merchandiser.

iv. Expected direct materials, direct labor and overhead

payments (excluding depreciation) for a manufacturer.

v. Expected cash payments on accounts payable.

vi. Other expected cash payments such as owner’s

withdrawals or dividends, repayment of notes, etc.

d. Loan Activity: if company has agreement with bank to

keep a minimum cash balance, company will need to

borrow if preliminary balance is less than this minimum

amount. They will need to repay any loan balance when

preliminary balance is greater than the minimum amount.

2. Budgeted Income Statement

a. Managerial accounting report showing predicted amounts

3. Budgeted Balance Sheet

a. Final step in preparing master budget.

b. Shows predicted amounts for assets, liabilities, and

D. Using the Master Budget

1. Planning: the master budget is clearly a plan for future

activities

Notes

Notes

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

22-9

Chapter Outline

III. Budgeting for Service Companies – service providers also use master

budgets. Master budgets for service provider includes:

A. Sales, Direct Labor, Factory Overhead, Capital expenditures, Cash,

IV. Decision Analysis—Activity-Based Budgeting (ABB)-––budget

system based on expected activities.

A. Traditional budgets are based on figures from previous year,

adjusted for changes in operating conditions.

B. Activity-based budgeting requires management to list activities

and to understand the resources required to perform these

activities.

2. Helps management reduce costs by eliminating non-value-

added activities.

Notes

V. Appendix 22A – Merchandise Purchases Budget

A. Merchandisers⎯Sales budget used as basis for merchandise

purchases budget.

B. Preparing the merchandise purchases budget: expressed in both

units and dollars.

Next month’s budgeted unit sales

x Ratio of inventory to future sales

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

22–10

Chapter 22 Alternate Demo Problem

ABC Company started business on January 1, 20xx. The company

estimated that sales for the first six months would be as follows:

Month

Units

Dollars

January

10,000

$ 50,000

February

8,000

40,000

March

15,000

75,000

April

17,000

85,000

May

22,000

110,000

June

30,000

150,000

The company sells all items on account and expects collections of

accounts receivable to be as follows: 60% in the month of the sale, and the

remaining 40% in the month after the sale.

Required:

(a) Compute the expected cash collections during the months of January,

February, March, April, May and June.

(b) The company has decided that finished goods inventory at the end of

each month should ideally be equal to 40% of next month’s sales. What

should budgeted production be for each of the first four months?

(c) It takes two pounds of raw material to make one unit of finished

product. The company wants to keep an ending inventory of raw

material equal to 30% of next month’s production needs. How many

pounds of raw material should be purchased in each of the first three

months?

(d) The raw material costs $2 per pound. The company pays for 70% of its

purchases during the month of purchase and the remainder in the

following month. How much cash will be disbursed during the month of

March for the purchase of raw material?

(e) The projected cash balance on March 1 is $13,500. What is the

estimated cash balance at the end of the month? (Prepare a formal

cash budget for the month of March.)

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

22–11

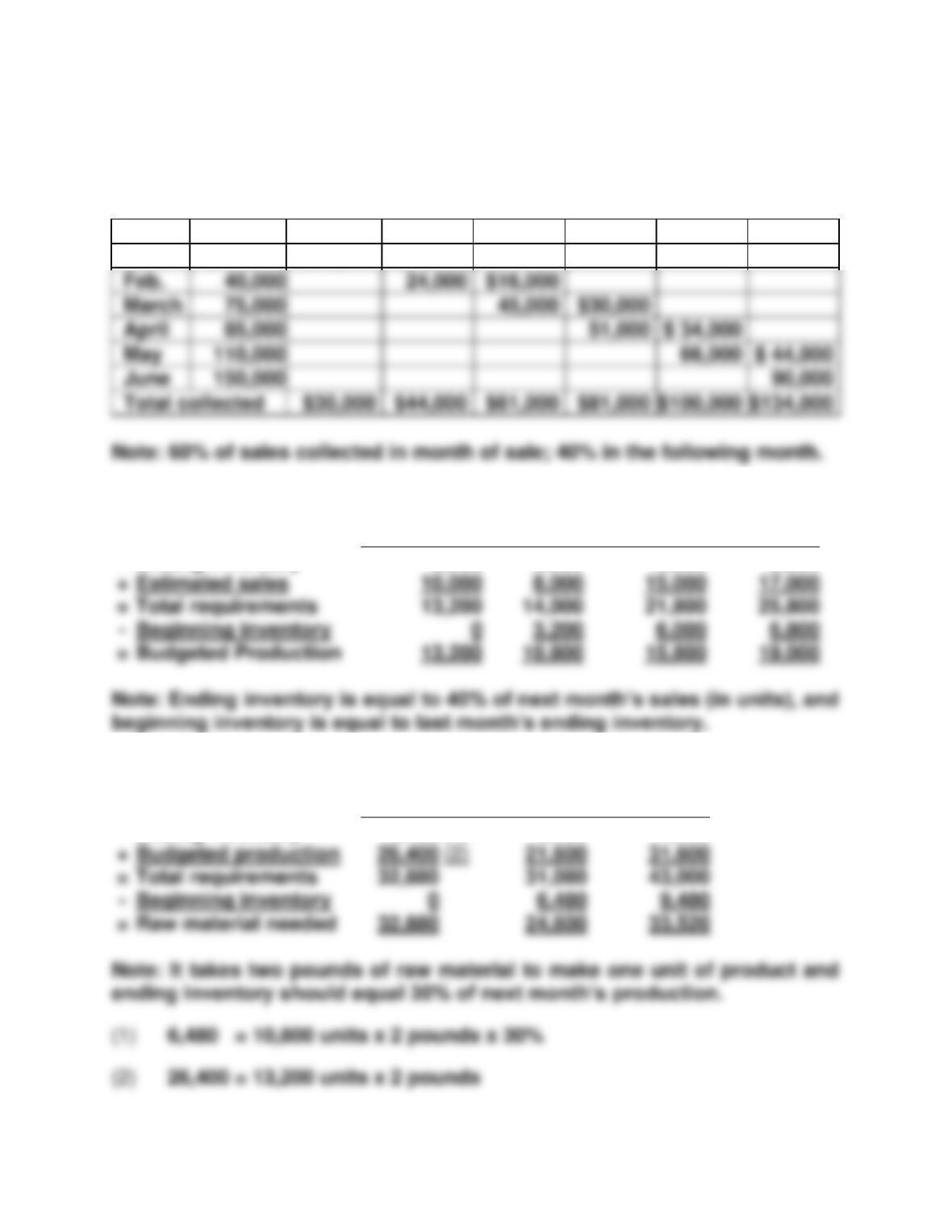

Chapter 22 Solution: Alternate Demo Problem

(a)

Collections

Month

Sales

Jan.

Feb.

March

April

May

June

Jan.

$ 50,000

$30,000

$20,000

(b)

Jan.

Feb.

March

April

Ending inventory

3,200

6,000

6,800

8,800

Estimated sales

8,000

15,000

Total requirements

21,800

3,200

6,000

6,800

Budgeted Production

15,800

(c)

Jan.

Feb.

March

Ending inventory

6,480

(1)

9,480

11,400

Budgeted production

(2)

31,600

Total requirements

43,000

Raw material needed

33,520

$16,000

March

$30,000

May

June

Total collected

$30,000

$44,000

$61,000

$81,000

$100,000

$134,000

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

22–12

(d)

Jan.

Feb.

March

Purchases (in units)

$32,880

24,600

33,520

(e)

ABC COMPANY

Cash Budget

For the Month of March 20xx

Beginning cash balance

$13,500

Cash receipts from customers

Total cash available

Cash payments

$12,812

X

Price per pound

=

Purchase cost

$65,760

Purchases from:

February

March

+

Total cash paid for materials