CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

Prob. 22–5B (FIN MAN); Prob. 7–5B (MAN)

1. Actual hours provided (3 × 40 hrs.)……………………………………………

…

120

Standard hours required for the original plan*………………………………

…

117

2. Actual hours provided (3 × 40 hrs.)……………………………………………

…

120

Standard hours required for the actual results*……………………………… 127

Labor time difference……………………………………………………………… (7)

…

3. Actual labor rate……………………………………………………………………

…

$30

Standard labor rate………………………………………………………………… 23

…

…

4. Actual hours provided (4 × 40 hrs.)……………………………………………

…

160

…

5. The bonus is the better approach by $80. The direct labor cost variance for

paying the bonus was $679 unfavorable which is the sum of the time variance

6. The labor rate and time variances fail to consider the number of errors in the

report from typist fatigue. A report that has many errors will require significant

22-56

…

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

Part A

Total Cost = (Variable Cost per Unit × Units of Production) + Fixed Cost

At the high point: At the low point:

$740 = ($0.20 × 1,200 units) + Fixed Cost $600 = ($0.20 × 500 units) + Fixed Cost

Fixed Cost = $500 Fixed Cost = $500

2. Selling price…………………………………………………………

…

$100.00

Less variable costs per case:

Direct materials…………………………………………………

…

$17.00

Direct labor………………………………………………………

…

7.20

3. Total fixed costs:

Utilities [see part (1)]…………………………………………………………

…

$ 500

4.

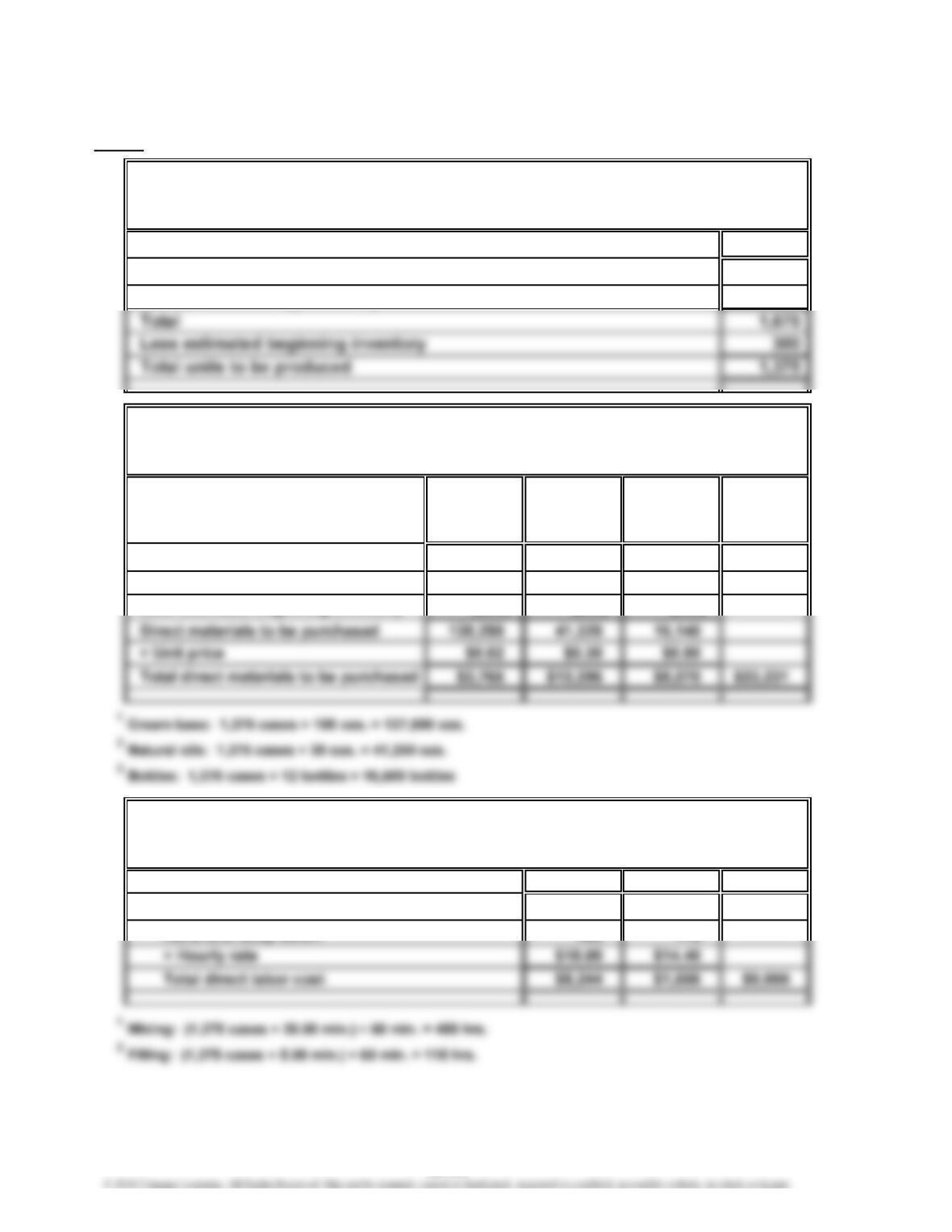

COMPREHENSIVE PROBLEM 5

Variable Cost per Unit1. = Difference in Total Cost

Difference in Production

=Variable Cost per Unit = $0.20 per case

$740 – $600

1,200 cases – 500 cases

Break-Even Sales (units) =

Fixed Costs

Unit Contribution Margin

22-57

…

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

COMPREHENSIVE PROBLEM 5 (Continued)

Part B

5.

Cases

Expected cases to be sold 1,500

Plus desired ending inventory 175

6.

Cream Natural

Base Oils Bottles Total

(ozs.) (ozs.) (bottles)

Units required for production 137,500 41,250 16,500

Plus desired ending inventory 1,000 360 240

Less estimated beginning inventory (250) (290) (600)

7.

Mixing Filling Total

Hours required for production of:

Hand and body lotion 458 115

For the Month Ended August 31, 2016

Production Budget

GENUINE SPICE INC.

Direct Labor Budget

For the Month Ended August 31, 2016

GENUINE SPICE INC.

Direct Materials Purchases Budget

For the Month Ended August 31, 2016

GENUINE SPICE INC.

231

21

22-58

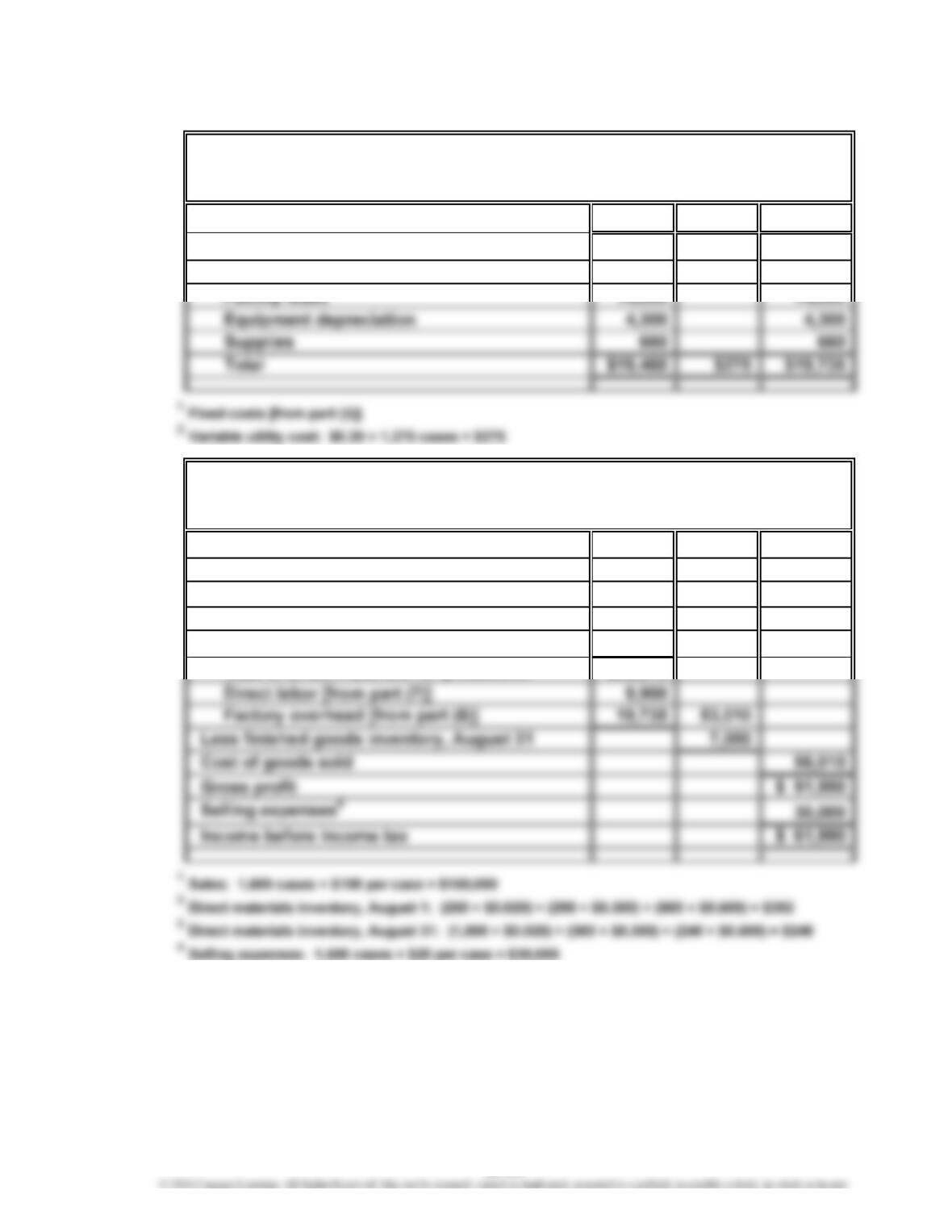

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

COMPREHENSIVE PROBLEM 5 (Continued)

8.

Fixed1Variable2Total

Factory overhead:

Utilities $ 500 $275 $ 775

9.

Sales1$150,000

Finished goods inventory, August 1 $12,000

Direct materials inventory, August 12$ 392

Direct materials purchases [from part (6)] 23,231

Less direct materials inventory, August 313248

Cost of direct materials for production $23,375

For the Month Ended August 31, 2016

GENUINE SPICE INC.

GENUINE SPICE INC.

Factory Overhead Budget

For the Month Ended August 31, 2016

Budgeted Income Statement

22-59

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

COMPREHENSIVE PROBLEM 5 (Continued)

Part C

10. Direct Materials Price Variance:

Actual price………………………

…

$ 0.016 $ 0.32 $ 0.42

Standard price……………………

…

0.020 0.30 0.50

Difference…………………………

…

$ (0.004) $ 0.02 $ (0.08)

*Actual quantity:

Cream base: 1,500 cases × 102 ozs. = 153,000 ozs.

Base

Cream Natural

BottlesOils

22-60

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

COMPREHENSIVE PROBLEM 5 (Continued)

Direct Materials Quantity Variance:

Actual quantity1………………………

…

153,000 ozs. 46,500 ozs. 18,750 btls.

Standard

q

uantit

y

2……………………

…

150,000 45,000 18,000

Difference………………………………

…

3,000 ozs. 1,500 ozs. 750 btls.

Note: All the direct materials quantity variances were unfavorable, indicating

some material losses, scrap, and quality rejections. All the quantity variances

1Actual quantity:

Cream base: 1,500 cases × 102 ozs. = 153,000 ozs.

Natural oils: 1,500 cases × 31 ozs. = 46,500 ozs.

BottlesOilsBase

Cream Natural

22-61

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

COMPREHENSIVE PROBLEM 5 (Continued)

11. Direct Labor Rate Variance:

Actual rate………………………………………………

…

$18.20 $ 14.00

Standard rate……………………………………………

…

18.00 14.40

The Mixing Department has an unfavorable direct labor rate variance from

using a higher classification of labor. The higher labor classification costs an

Direct Labor Time Variance:

Actual time (hours)1……………………………………

…

487.5 140

Standard time

(

hours

)

2………………………………… 500 125

1Actual time:

Mixing: (1,500 units × 19.50 min.) ÷ 60 min. = 487.5 hrs.

Filling: (1,500 units × 5.60 min.) ÷ 60 min. = 140 hrs.

2Standard time:

Mixing: (1,500 units × 20.00 min.) ÷ 60 min. = 500 hrs.

Mixing Filling

Department Department

Filling

DepartmentDepartment

Mixing

22-62

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

COMPREHENSIVE PROBLEM 5 (Continued)

12. Factory Overhead Controllable Variance:

Actual variable overhead……………………………………………………

…

$305

13. Factory Overhead Volume Variance:

Normal volume (cases)………………………………………………………

…

1,600

Actual volume (cases)………………………………………………………

…

1,500

22-63

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

COMPREHENSIVE PROBLEM 5 (Concluded)

Actual costs 19,765.00 Applied costs 18,543.75

($19,460 + $305) [1,500 × ($12.1625 + $0.20)]

Balance (underapplied) 1,221.25

$5 U $1,216.25 U

Controllable Volume

Variance Variance

14. The production volume of 1,375 cases determined in part (5) was planned at the

beginning of August. The variances compare the actual cost and the standard

$1,221.25 U

Cost Variance

Total Factory Overhead

Alternative Computation of Overhead Variances

Factory Overhead

22-64

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

CP 22–1 (FIN MAN); CP 7–1 (MAN)

The use of ideal standards is a legitimate concern for Henry. It is likely that such

standards are too tight and do not include the necessary fatigue factors that are

likely in this type of operation. It seems as though Henry is arguing for practical

CP 22–2 (FIN MAN); CP 7–2 (MAN)

Although the Tungston Company performance measurement system uses both

financial and nonfinancial measures, there may still be some serious performance

CASES & PROJECTS

22-65

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

CP 22–3 (FIN MAN); CP 7–3 (MAN)

This is a case where there is strong evidence that the poor performance that is

(1) the materials price variance is very favorable; (2) the Fabrication Department’s

labor time variance is also very favorable. A possible explanation is that the

Purchasing Department found a low-price supplier. The low price translated into a

favorable variance. Unfortunately, it appears the company is “getting what it paid

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

CP 22–4 (FIN MAN); CP 7–4 (MAN)

The plant manager is placing pressure on the controller because the controllable

variance is very unfavorable. The claim is that these costs are not really variable at

all. This is a very difficult claim to accept. This is a small company, so it purchases

its power from the outside. The power and light bill is variable to the amount of

22-67

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

CP 22–5 (FIN MAN); CP 7–5 (MAN)

Use this activity to compare performance measures from different groups and their

selected cities.

The following are examples of performance measures from Worcester,

Massachusetts:

ECONOMIC DEVELOPMENT

Indicator Outcome Type Measured As

Growth of commercial and Performance Change in total assessed value

residential tax base over time

PUBLIC SAFETY

Indicator Outcome Type Measured As

Level of crime Performance Crime rate and clearance rate by type

of crime

Police community relations Performance Responses to annual citizen survey

questions, performance of personnel

All measured both citywide and by neighborhood

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

CP 22–5 (FIN MAN); CP 7–5 (MAN) (Continued)

IMPROVED MUNICIPAL SERVICES

Indicator Outcome Type Measured As

Cleanliness of streets Performance Responses to questions on the annual

citizen survey, objective resident ratings

waste collection

Library usage Performance Circulation per capita

Citizen involvement (citywide Performance % of eligible voters registered;

and by neighborhood) % of registered voters voting

EDUCATION

Indicator Outcome Type Measured As

Student and school achievement Performance MCAS test scores

Graduation rate Performance Percent graduating

Dropout rate Performance Percent dropouts

Employer satisfaction with Performance Employer survey

graduates

22-69

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

CP 22–5 (FIN MAN); CP 7–5 (MAN) (Concluded)

IMPROVED YOUTH SERVICES

Indicator Outcome Type Measured As

Presence of “at risk youth” Performance Responses to questions from the Youth

Risk Behavior Survey (includes

questions on drug and alcohol use

and violent behavior) by high school

Extent of juvenile crime Performance Juvenile crime rate, citywide and by