1243

Exercise 22-30 (10 minutes)

HECTOR COMPANY

Budgeted Cash Payments

For August and September

August

Sept.

Payments for:

Merchandise* ………………………………………………………………….

$14,400

$19,200

Rent expense ………………………………………………………………….

7,400

7,400

1244

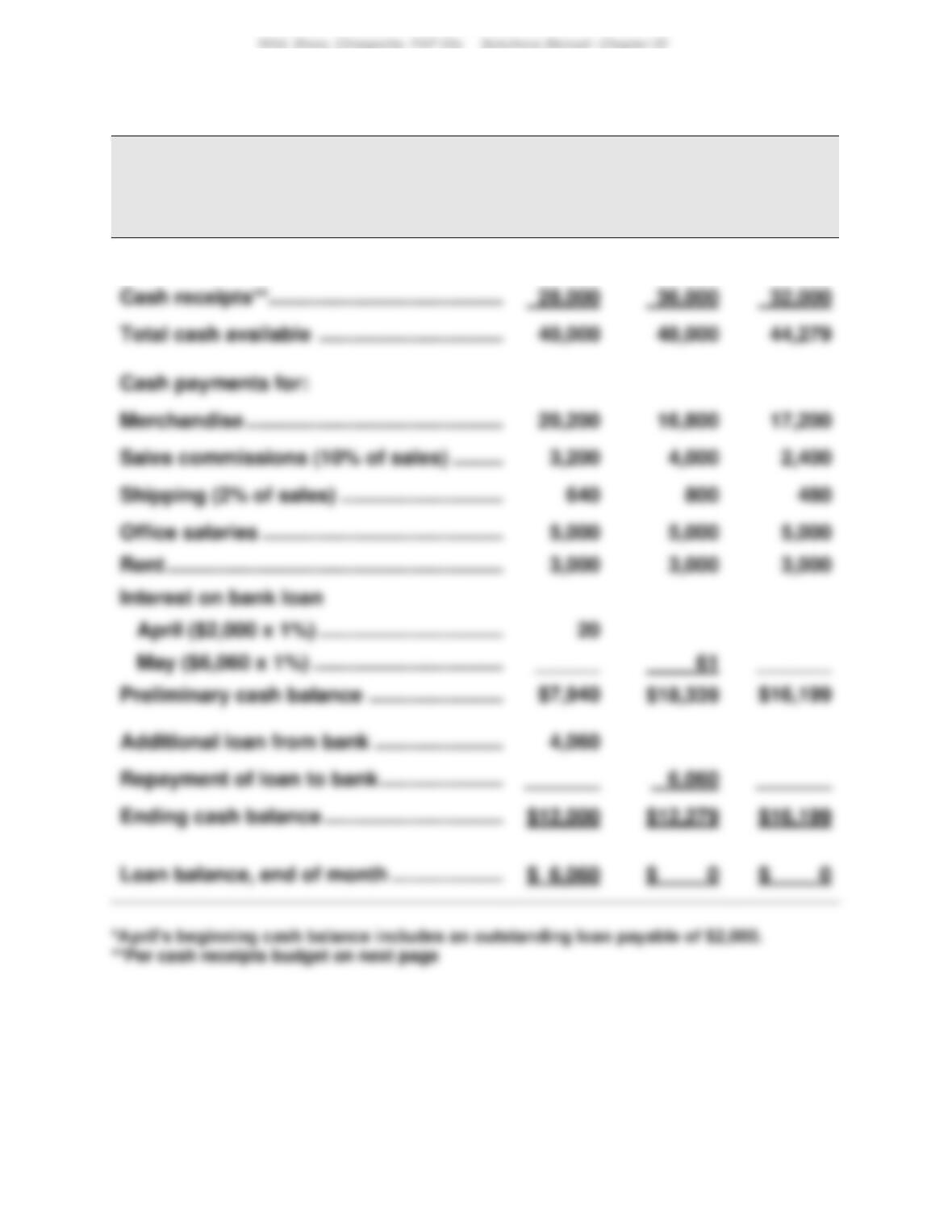

Exercise 22-31 (25 minutes)

CASTOR, INC.

Cash Budget

For April, May, and June

April

May

June

Beginning cash balance* ……………………….

$12,000

$12,000

$12,279

$18,339

Additional loan from bank ……………………..

1245

Exercise 22-31 (continued)

CASTOR, INC.

Cash Receipts Budget

For April, May, and June

April

May

June

Sales ……………………………………………………..

$32,000

$40,000

$24,000

Exercise 22-32 (30 minutes)

(1)

KELSEY

Cash Receipts Budget

For July, August, and September

July

August

Sept.

Sales ……………………………………………………..

$64,000

$80,000

$48,000

1246

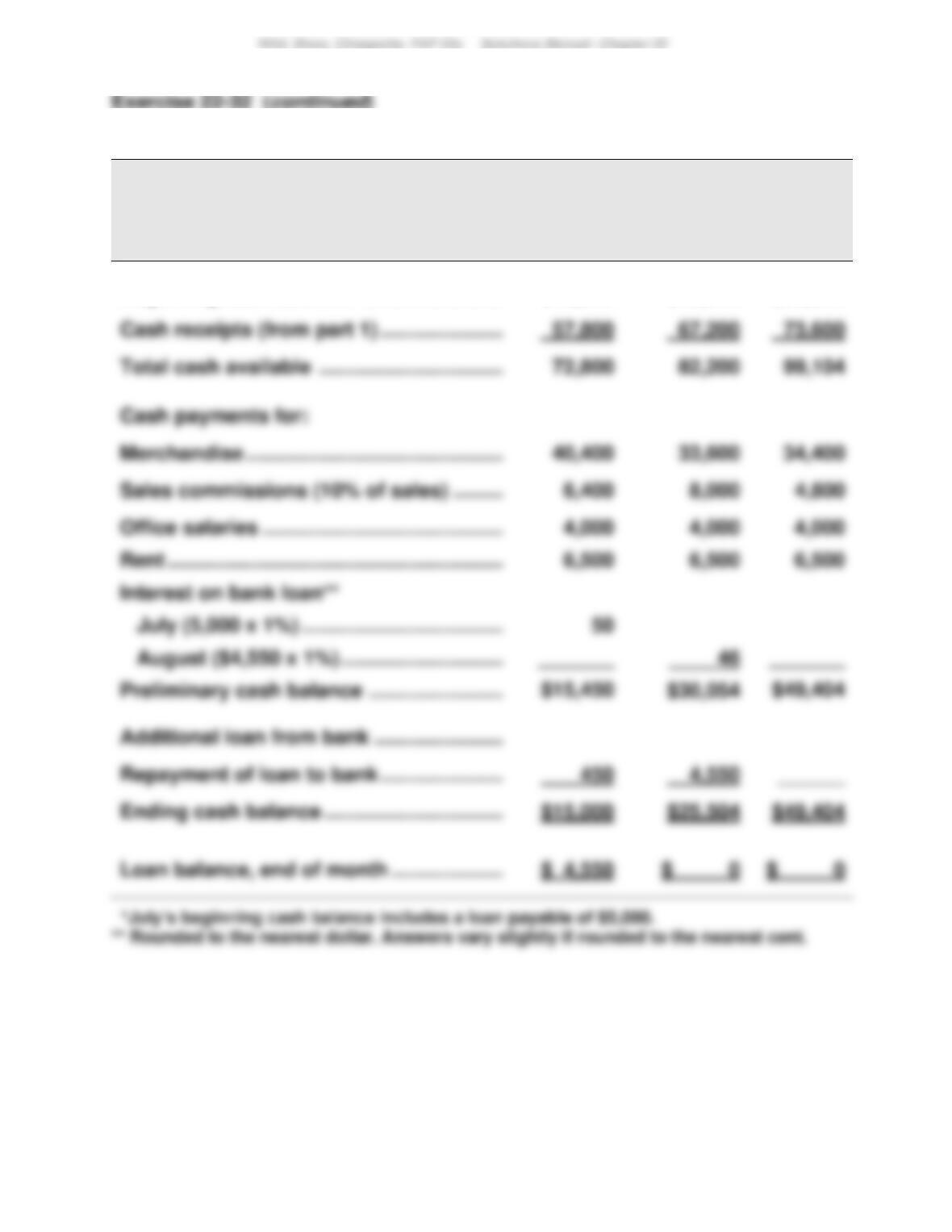

(2)

KELSEY

Cash Budget

For July, August, and September

July

August

Sept.

Beginning cash balance* ……………………….

$15,000

$15,000

$25,504

Cash payments for:

1247

Exercise 22-33 (15 minutes)

ZETROV COMPANY

Budgeted Balance Sheet

As of March 31

ASSETS

Cash ……………………………………………………………………..

$ 50,000

Accounts receivable ($140,000 x 70%) ………………………..

98,000

Total current assets ……………………………………………….

Less accumulated depreciation (note 1) ………………….

LIABILITIES AND EQUITY

Supporting calculations

(1) Accumulated depreciation

Beginning ……………………………………………………….

$46,000

Depreciation expense …………………………..

Ending ……………………………………………………….

$47,000

(2) Retained earnings

Beginning ……………………………………………………….

$ 8,000

Net income ……………………………………………………….

Ending ……………………………………………………….

$56,000

Tax rate ……………………………………………………

Exercise 22-34 (15 minutes)

FORTUNE, INC.

Budgeted Income Statement

For Quarter Ended March 31

Sales (note 1) ……………………………………………………………

$3,750,000

Cost of goods sold (note 2) ………………………………………

2,100,000

Supporting calculations

(1) Sales

Unit sales (45,000 + 55,000 + 50,000) ………….

Unit price …………………………………………………

$25

(2) Cost of goods sold

Unit sales (45,000 + 55,000 + 50,000) ………….

Unit cost…………………………………………………..

(3) Income tax expense

Pre-tax income …………………………………………

$ 397,375

1249

Exercise 22-35 (15 minutes)

RENDER CO. CPA

Activity-Based Budget

For Year Ending December 31, 2017

Budgeted

Hours

Budgeted

Price/hour

Budgeted

Cost

Data-entry ……………………………………………..

2,200

$10

$ 22,000

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 22

1250

PROBLEM SET A

Problem 22-1A (40 minutes)

Part 1

BLACK DIAMOND COMPANY

Production Budget (in units)

Third Quarter

Budgeted ending inventory (skis) …………………………………………………

3,500

Part 2

BLACK DIAMOND COMPANY

Direct Materials Budget (in lbs, except where noted)

Third Quarter

Materials (carbon fiber) needed for production (148,500 x 2) ……..

297,000

Direct materials cost per pound ………………………………………………..

1251

Problem 22-1A (concluded)

Part 3

BLACK DIAMOND COMPANY

Direct Labor Budget

Third Quarter

Units to be produced ………………………………………………………

148,500

Direct labor rate (per hour) ……………………………………………..

Part 4

BLACK DIAMOND COMPANY

Factory Overhead Budget

Third Quarter

Total labor hours needed ………………………………………………..

74,250

1252

Problem 22-2A (30 minutes)

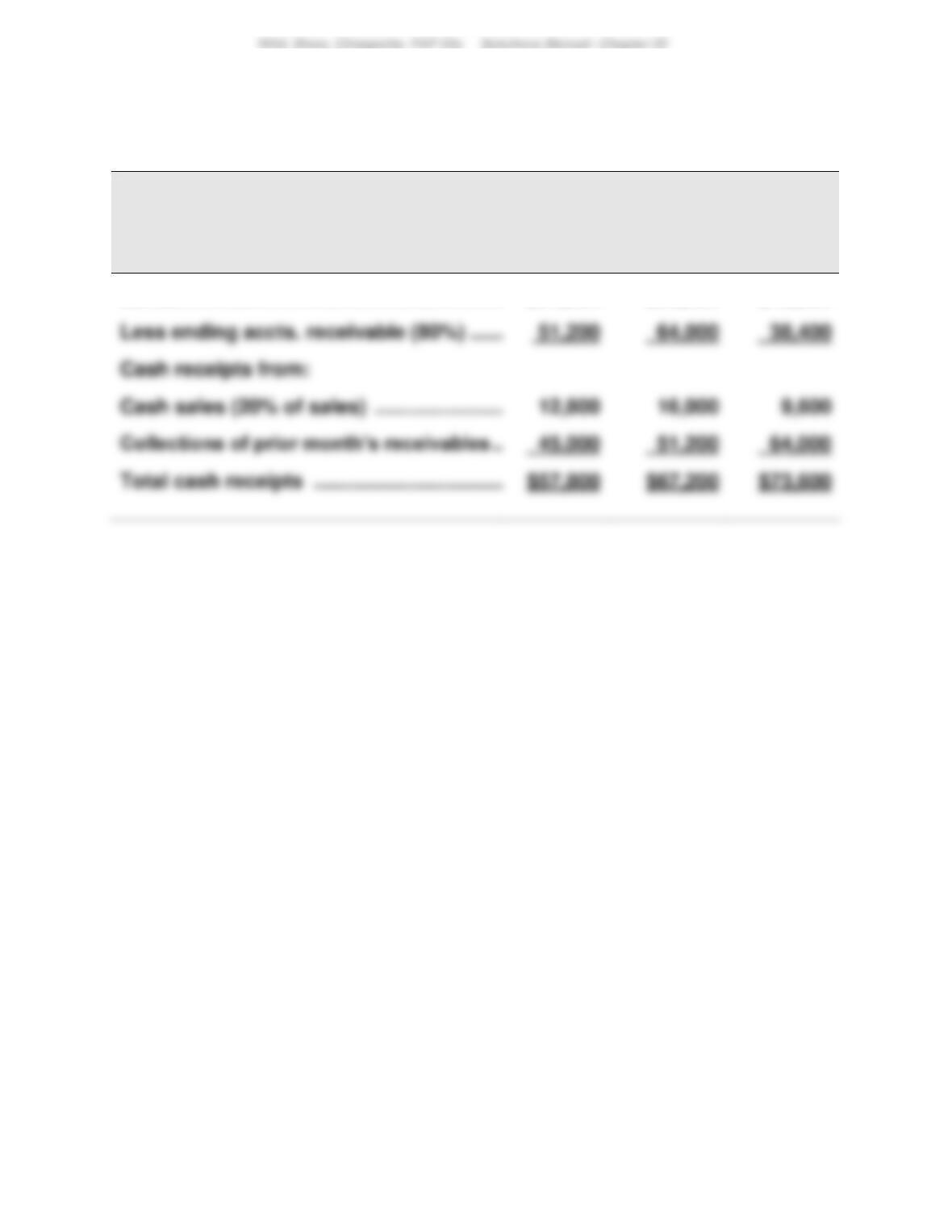

(1)

BUILT-TIGHT

Cash Receipts Budget

For July, August, and September

July

August

Sept.

Sales ……………………………………………………..

$64,000

$80,000

$48,000

1253

Problem 22-2A (continued)

(2)

BUILT-TIGHT

Cash Budget

For July, August, and September

July

August

Sept.

Beginning cash balance* ……………………….

$15,000

$15,000

$25,504

Cash receipts (from part 1) …………………….

57,800

67,200

73,600

Cash payments for:

Direct materials ……………………………………..

16,160

13,440

13,760

Direct labor ……………………………………………

4,040

3,360

3,440

Overhead ………………………………………………

20,200

16,800

17,200

Sales commissions (10% of sales) …………

6,400

8,000

4,800

$30,054

Repayment of loan to bank …………………….

450

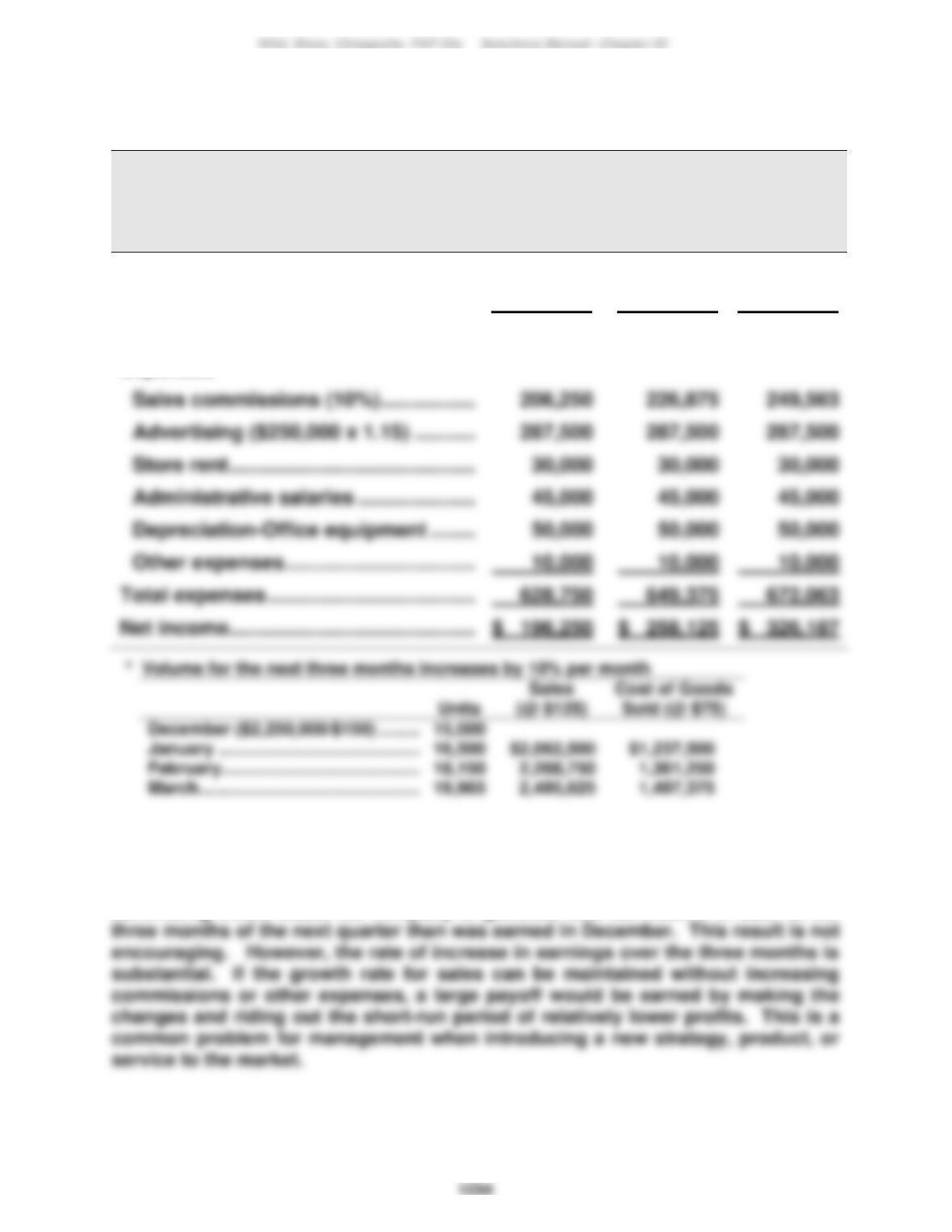

Problem 22-3A (50 minutes)

Part 1

MERLINE MANUFACTURING

Budgeted Income Statement

For Months of January, February, and March, 2018

January

February

March

Sales* ……………………………………………….

$2,062,500

$2,268,750

$2,495,625

Cost of goods sold* …………………………..

1,237,500

1,361,250

1,497,375

Gross profit ………………………………………

825,000

907,500

998,250

Expenses

287,500

287,500

287,500

Total expenses ………………………………….

Part 2: Analysis Component

The plan for increasing sales volume by reducing the price and increasing

advertising would cause the company to generate less net income in each of the

1255

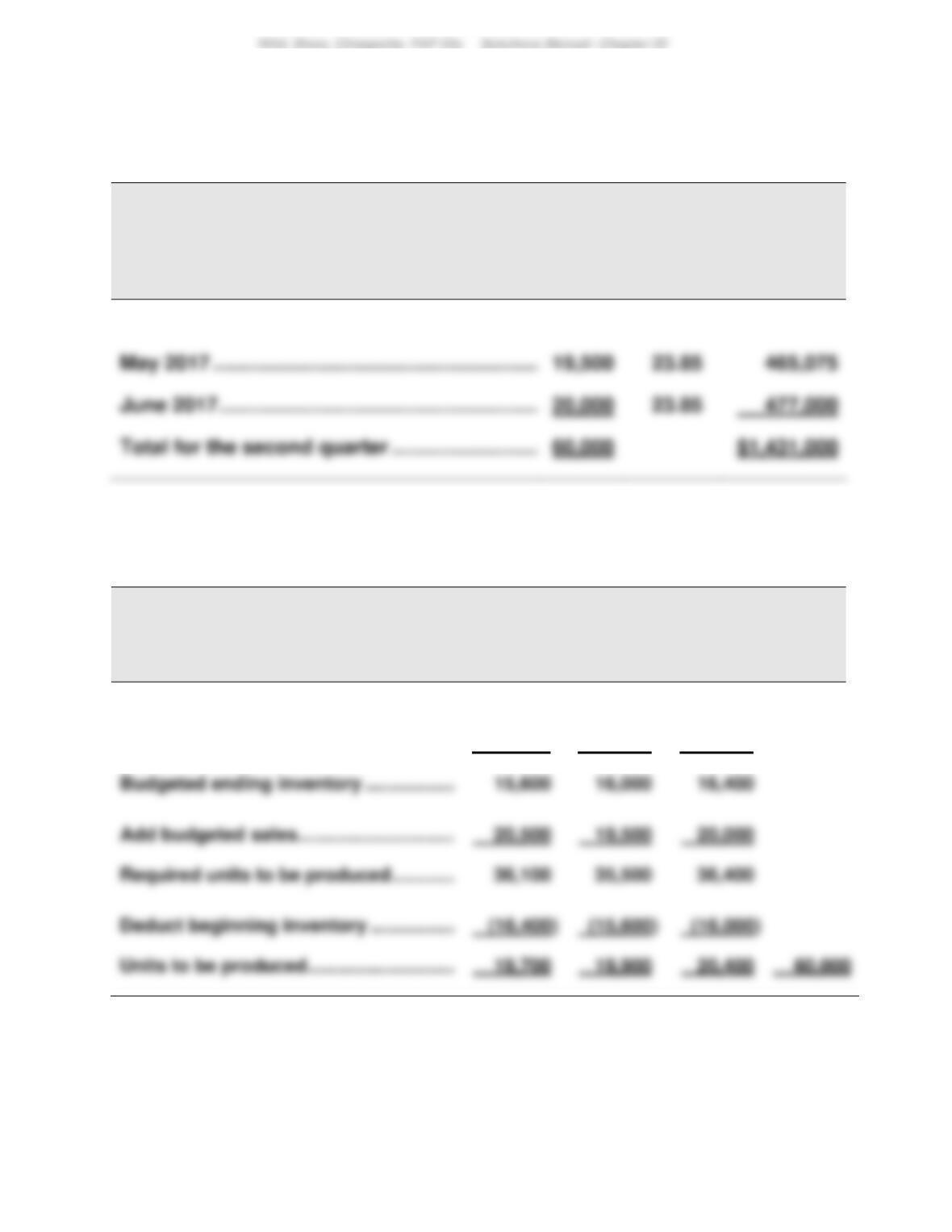

Problem 22-4A (130 minutes)

Part 1

ZIGBY MANUFACTURING

Sales Budgets

April, May, and June 2017

Budgeted

Units

Budgeted

Unit Price

Budgeted

Sales Dollars

April 2017 ……………………………………………………..

20,500

$23.85

$ 488,925

20,000

Part 2

ZIGBY MANUFACTURING

Production Budget

April, May, and June 2017

April

May

June

Total

Next month’s budgeted sales ……………

19,500

20,000

20,500

Ratio of inventory to future sales ………

x 80%

x 80%

x 80%

Add budgeted sales ………………………….

Deduct beginning inventory ……………..

1256

Problem 22-4A (continued)

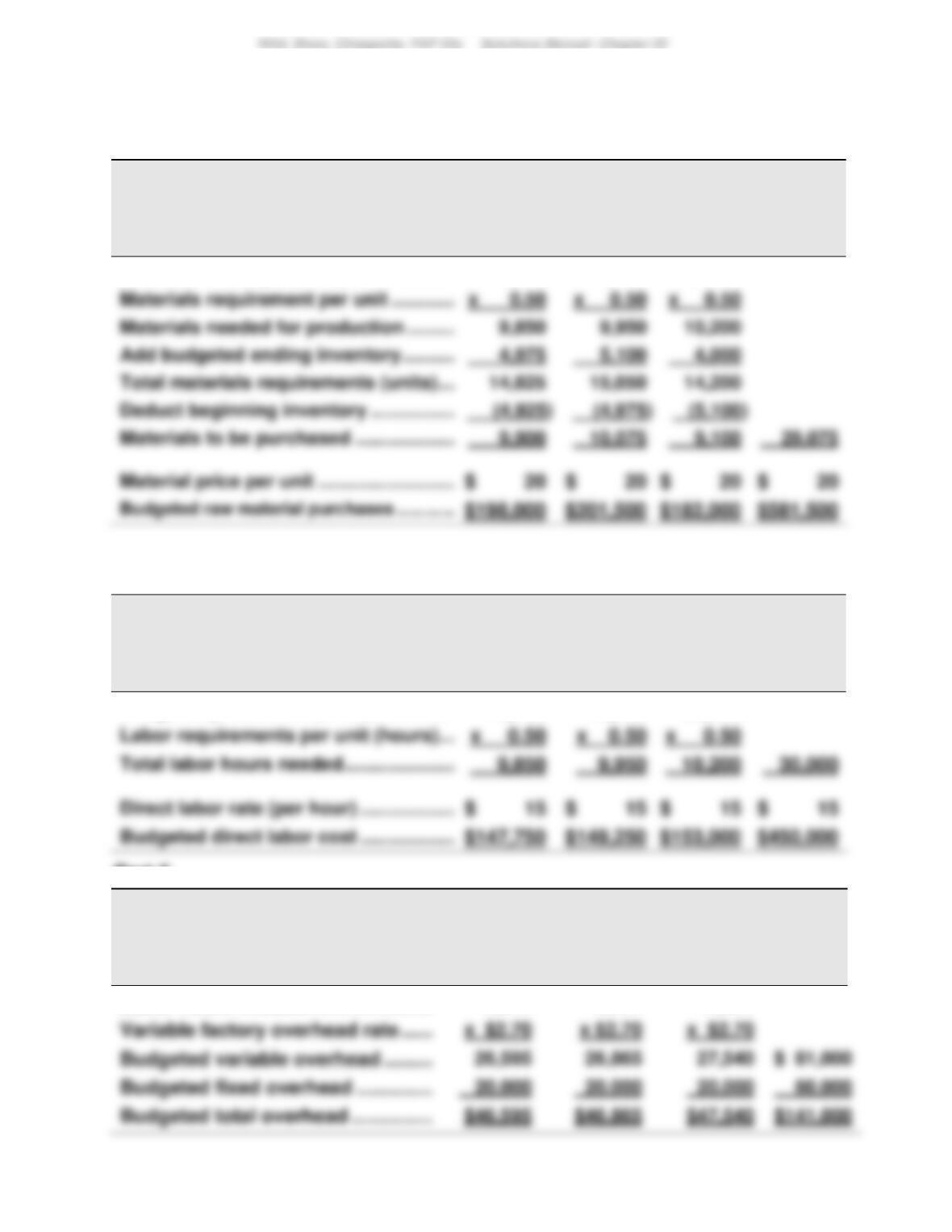

Part 3

ZIGBY MANUFACTURING

Raw Materials Budget

April, May, and June 2017

April

May

June

Total

Production budget (units) …………………

19,700

19,900

20,400

Add budgeted ending inventory ………..

Materials to be purchased ………………..

Material price per unit ………………………

$ 20

Part 4

ZIGBY MANUFACTURING

Direct Labor Budget

April, May, and June 2017

April

May

June

Total

Budgeted production (units) …………….

19,700

19,900

20,400

Labor requirements per unit (hours) ….

Total labor hours needed ………………….

Direct labor rate (per hour) ……………….

Budgeted direct labor cost ……………….

Part 5

ZIGBY MANUFACTURING

Factory Overhead Budget

April, May, and June 2017

April

May

June

Total

Labor hours needed ………………………..

9,850

9,950

10,200

Budgeted variable overhead ……………

27,540

1257

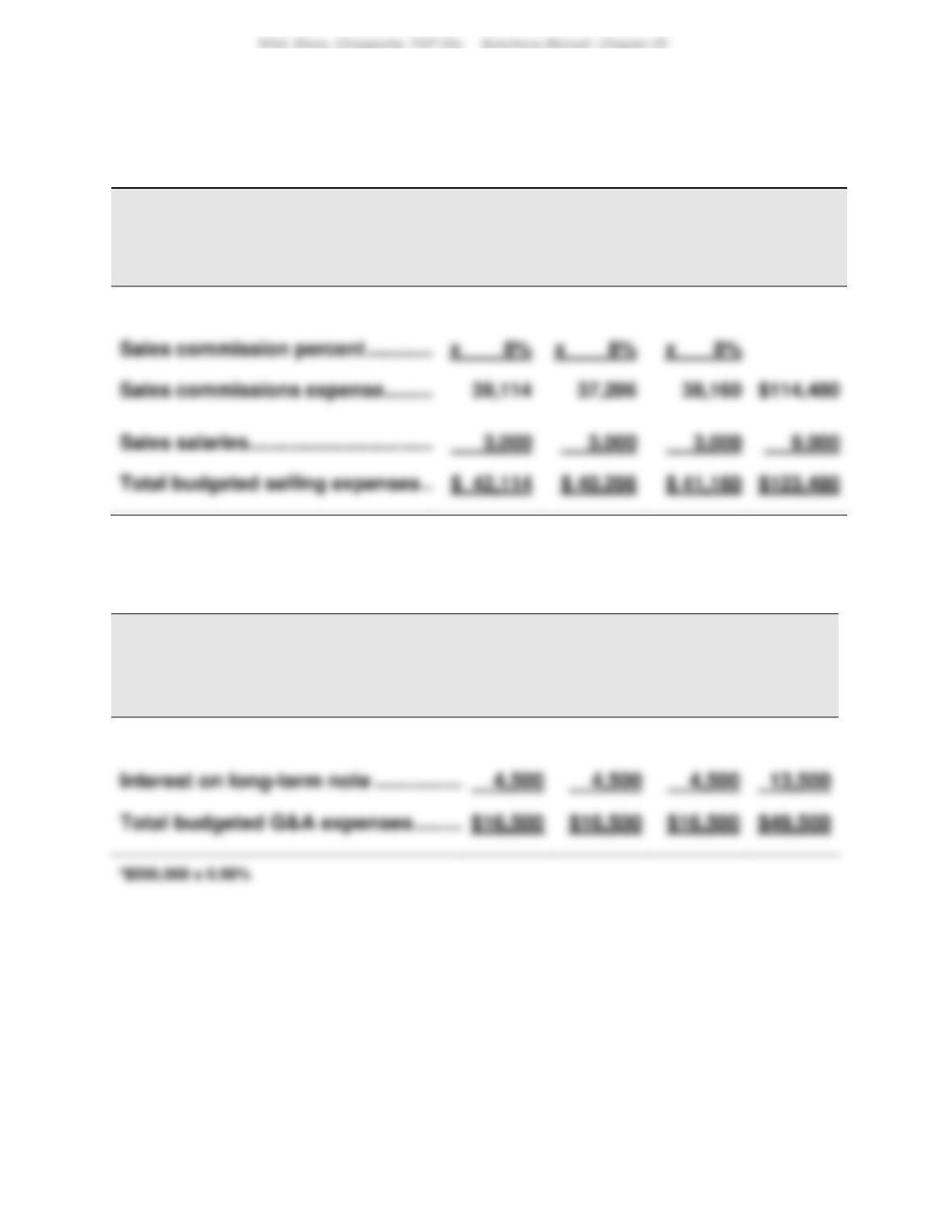

Problem 22-4A (continued)

Part 6

ZIGBY MANUFACTURING

Selling Expense Budgets

April, May, and June 2017

April

May

June

Total

Budgeted sales …………………………..

$488,925

$465,075

$477,000

Sales commission percent ………………

x 8%

Part 7

ZIGBY MANUFACTURING

General and Administrative Expense Budgets

April, May, and June 2017

April

May

June

Total

Salaries ……………………………………………….

$12,000

$12,000

$12,000

$36,000

1258

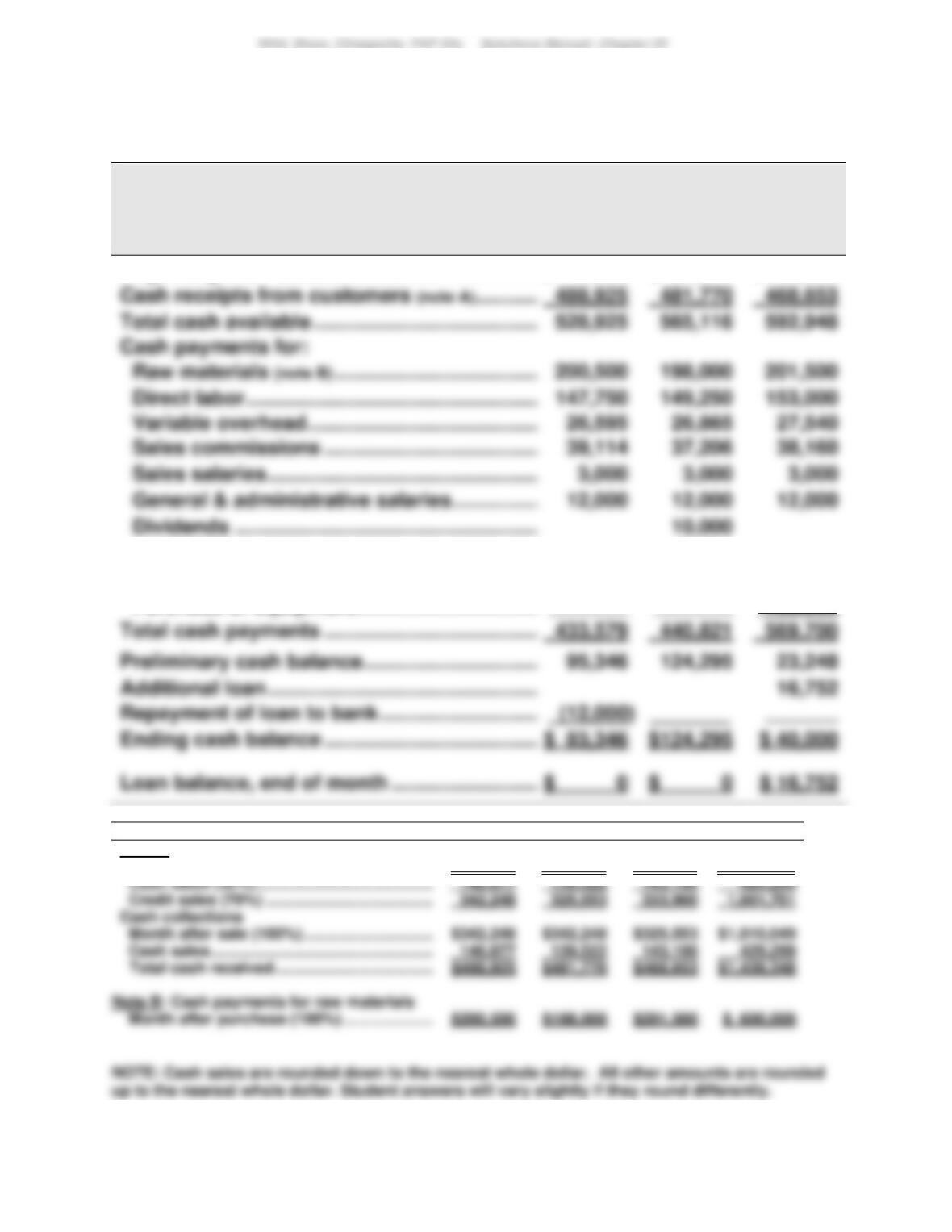

Problem 22-4A (Continued)

Part 8

ZIGBY MANUFACTURING

Cash Budgets

April, May, and June 2017

April

May

June

Beginning cash balance ………………………………..

$ 40,000

$ 83,346

$124,295

Loan interest ($12,000 x 1%) …………………………..

120

Long-term note interest ($500,000 x .0.9%) …………

Purchase of equipment ……………………………….

4,500

_______

4,500

_______

4,500

130,000

$124,295

Supporting calculations

April

May

June

Total

Note A: Cash receipts from customers

Total sales …………………………………………………

$488,925

$465,075

$477,000

$1,431,000

Cash sales (30%) ……………………………………….

Credit sales (70%) ……………………………………..

Cash collections

Month after sale (100%) …………………………..

$342,248

$342,248

$325,553

$1,010,049

Cash sales…………………………………………………

Total cash received ……………………………………

$488,925

$481,770

$468,653

$1,439,348

Month after purchase (100%) ……………………..

$200,500

$198,000

$201,500

1259

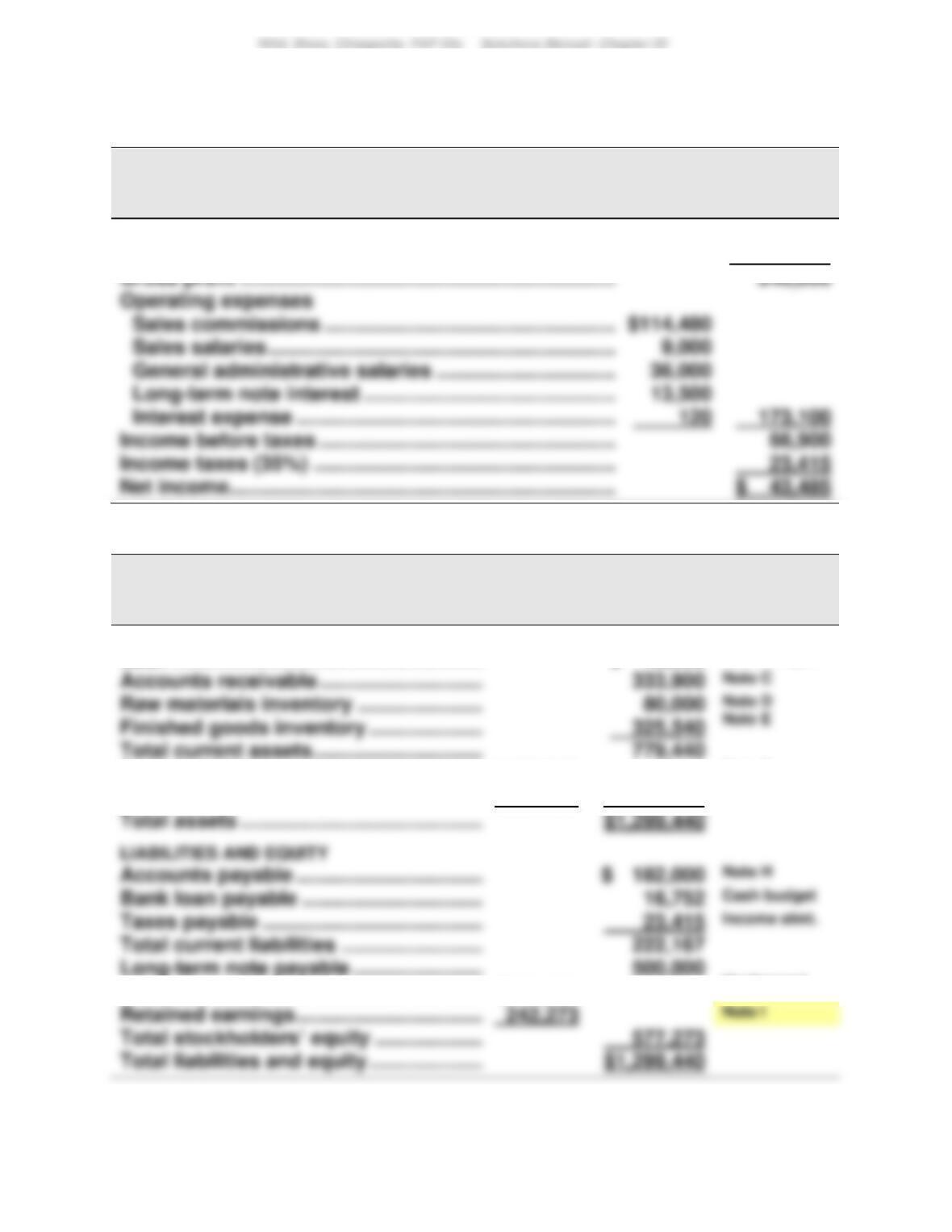

Problem 22-4A (Continued)

Part 9

ZIGBY MANUFACTURING

Budgeted Income Statement

For Three Months Ended June 30, 2017

Sales ……………………………………………………………………..

$1,431,000

Cost of goods sold (60,000 units @ $19.85) …………….

1,191,000

Gross profit …………………………………………………………..

$114,480

Income before taxes ………………………………………………

Part 10

ZIGBY MANUFACTURING

Budgeted Balance Sheet

June 30, 2017

ASSETS

Cash ……………………………………………………

$ 40,000

Cash budget

Accounts receivable …………………………..

Note C

Total current assets …………………………..

Equipment …………………………………………..

$730,000

Note F

Less accumulated depreciation ……………

210,000

520,000

Note G

Total assets …………………………………………

Accounts payable ………………………………..

Note H

Bank loan payable ……………………………….

Cash budget

Taxes payable ……………………………………..

23,415

Income stmt.

Total current liabilities …………………………

Common stock …………………………………….

$335,000

Unchanged

Retained earnings ………………………………..

242,273

Note I

577,273

1260

Problem 22-4A (Concluded)

Supporting Footnotes

Note C

Beginning receivables ………………………………………………

$ 342,248

Credit sales ………………………………………………………………

1,001,701

Less collections ……………………………………………………….

Note D

Beginning raw materials inventory …………………………..

$ 98,500

Purchases of raw materials ……………………………………….

Less materials used in production** …………………………..

(600,000)

Note E

Beginning finished goods inventory …………………………..

$ 325,540

Cost of goods completed during the period ……………….

Less cost of goods sold during the period …………………

(1,191,000)

*Also equals 16,400 units @ $19.85 = $325,540

Note F

Beginning equipment ………………………………………………..

$ 600,000

Purchased in June ……………………………………………………

130,000

Note G

Beginning accumulated depreciation …………………………

$ 150,000

Depreciation expense ……………………………………………….

60,000

Note H

Beginning accounts payable ……………………………………..

$ 200,500

Purchases of raw materials ……………………………………….

Payments for raw materials ……………………………………….

(600,000)

Note I

ZIGBY MANUFACTURING

Budgeted Statement of Retained Earnings

For Three Months Ended June 30, 2017

Retained earnings, beginning ……………………. $208,788

1261

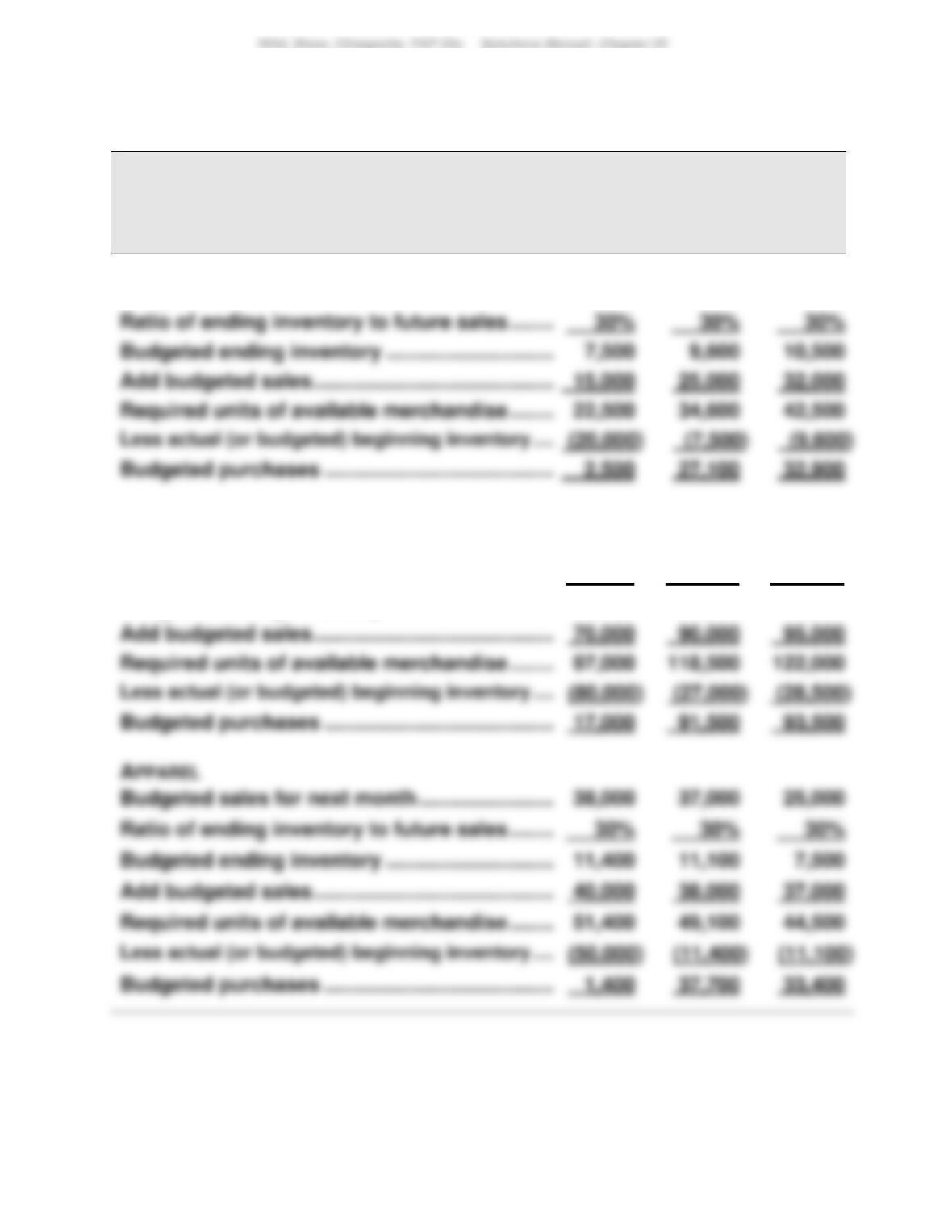

Problem 22-5A (60 minutes)

Part 1

KEGGLER’S SUPPLY

Merchandise Purchases Budgets

For March, April, and May

March

April

May

FOOTWEAR

Budgeted sales for next month ………………………

25,000

32,000

35,000

Budgeted ending inventory …………………………..

10,500

Required units of available merchandise ………..

22,500

34,600

42,500

Budgeted purchases ……………………………………..

SPORTS EQUIPMENT

Budgeted sales for next month ………………………

90,000

95,000

90,000

Ratio of ending inventory to future sales ………..

30%

30%

30%

Budgeted ending inventory …………………………..

27,000

28,500

27,000

Required units of available merchandise ………..

97,000

Budgeted purchases ……………………………………..

1262

Problem 22-5A (Continued)

Part 2. Analysis Component

Inventory levels might become too high for a number of reasons, including:

• Management may have simply lost sight of inventory levels, thereby

allowing them to reach inappropriately high levels.