EXERCISE 22-13

(a)

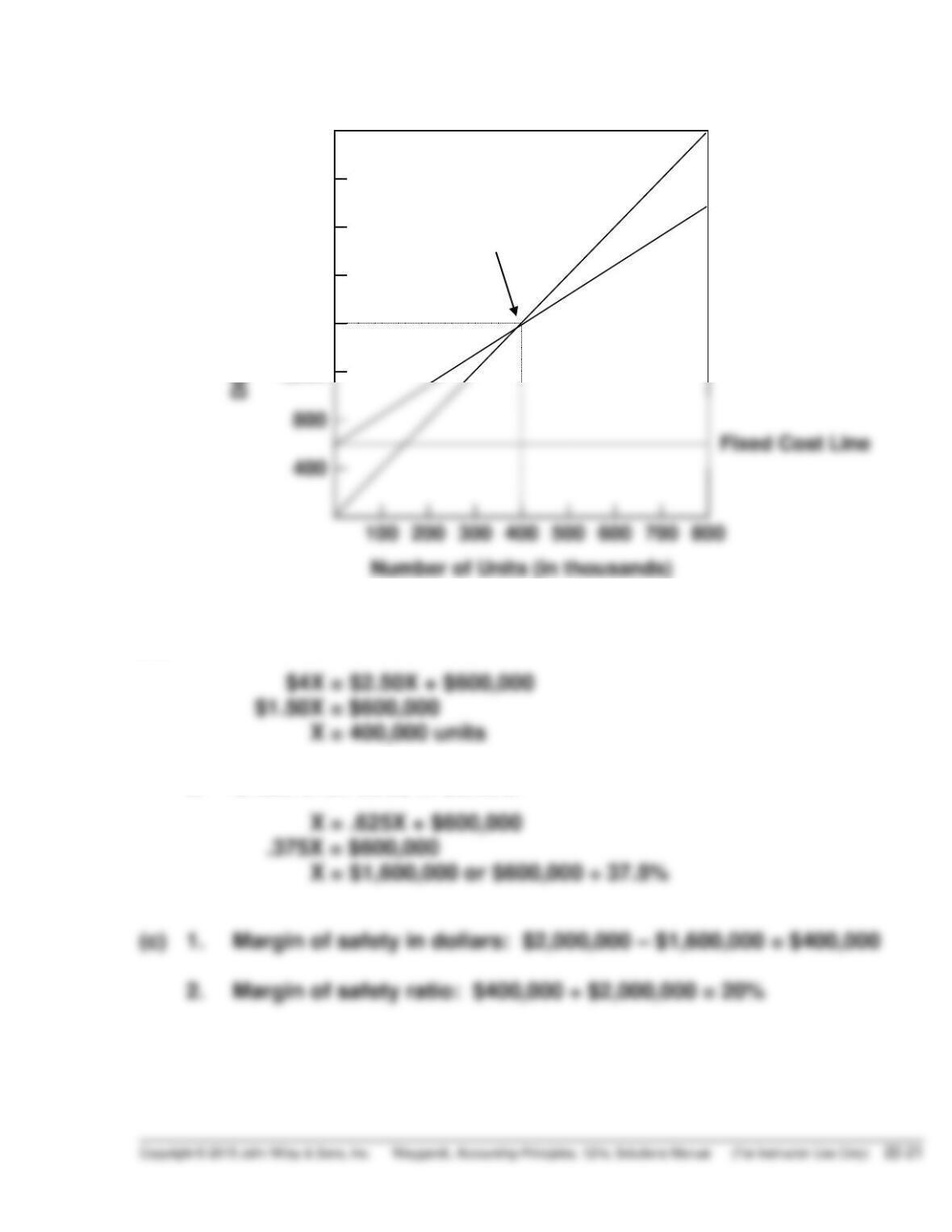

$3,200

Sales Line

Fixed Cost Line

2,800

2,400

Total Cost Line

Break-even Point

2,000

1,600

1,200

(b) 1. Break-even sales in units:

$4X = $2.50X + $600,000

2. Break-even sales in dollars:

X = .625X + $600,000

(c) 1. Margin of safety in dollars: $2,000,000 – $1,600,000 = $400,000

EXERCISE 22-14

(a) CAREY COMPANY

CVP Income Statement

For the Year Ended December 31, 2017

Total

Per Unit

Sales (60,000 X $26) ………………………………..

$1,560,000

$26

(b) CAREY COMPANY

CVP Income Statement

For the Year Ended December 31, 2017

Total

Per Unit

Sales [(60,000 X 105%) X $24.50*] …………….

Variable costs (63,000 X $12.00**) …………….

$1,543,500

756,000

$24.50

12.00

*EXERCISE 22-15

(a)

Utility Expense

Months in

a year

X

Kilowatt

hours

X

Hourly

Charge

=

Variable

Utilities

*EXERCISE 22-15 (Continued)

Variable Costing

Labor:

Crate builders

$43,000

Material:

Wood

54,000

Variable Overhead:

Utilities

Nails

Total manufacturing costs

(b)

Absorption Costing

Labor:

Crate builders

$ 43,000

Material:

Wood

54,000

Variable overhead:

Utilities

Nails

Fixed overhead:

Utilities

18,000

Rent

Total manufacturing costs

(c) The entire difference in costs between the two methods is due to the

*EXERCISE 22-16

(a) MONTIER CORPORATION

Income Statement

For the Month Ended October 31, 2017

(Absorption Costing)

Sales (20,000 X $50) …………………………..………………… $1,000,000

Cost of goods sold (20,000 X $32*)……………………….. 640,000

(b) MONTIER CORPORATION

Income Statement

For the Month Ended October 31, 2017

(Variable Costing)

(c) Under variable costing, all fixed manufacturing costs ($225,000) are

SOLUTIONS TO PROBLEMS

PROBLEM 22–1A

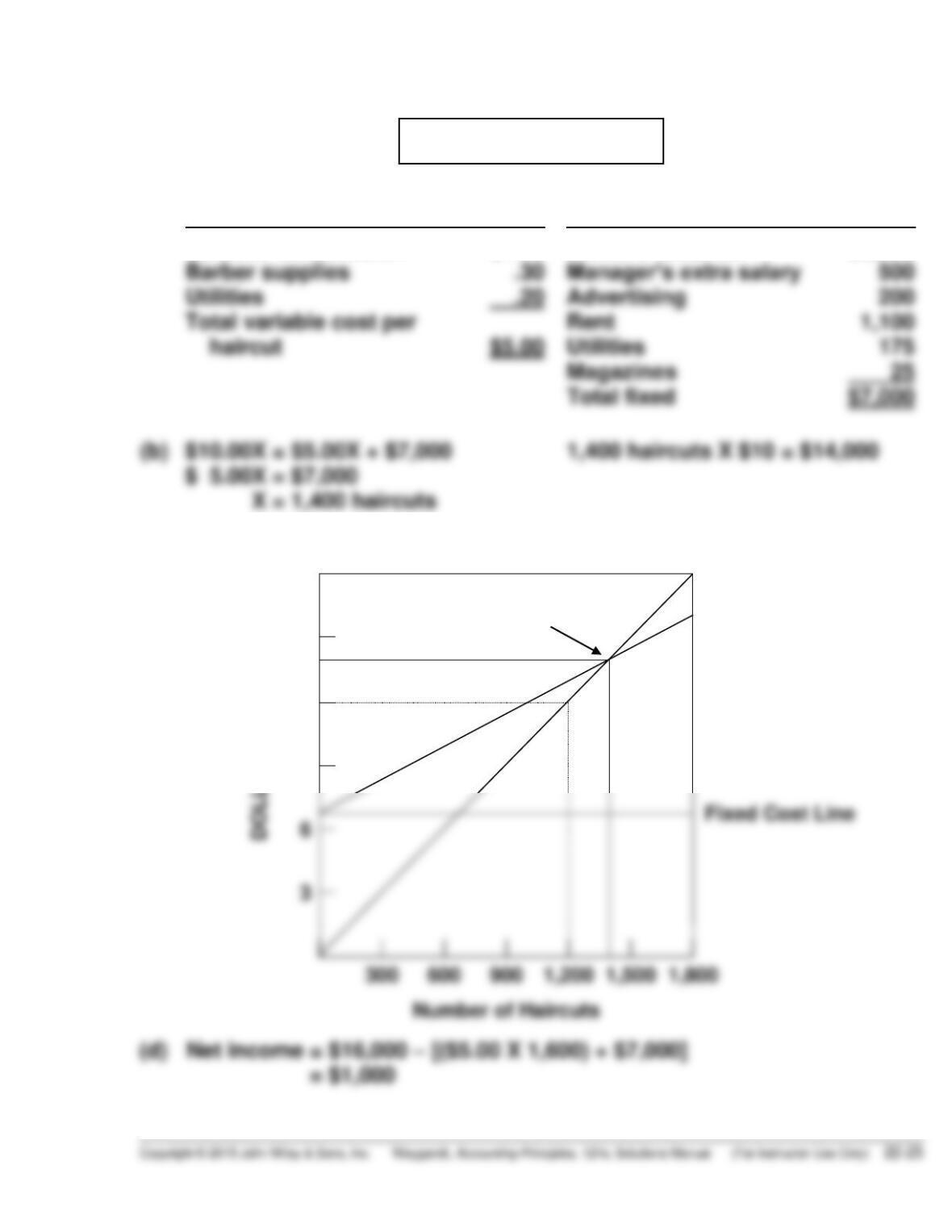

(a)

Variable costs (per haircut)

Fixed costs (per month)

Total fixed $7,000

Barbers’ commission $4.50

Barber supplies .30

Barbers’ salaries $5,000

Manager’s extra salary 500

(c)

18

Sales Line

6

15

Break-even Point

Total Cost Line

12

9

PROBLEM 22–2A

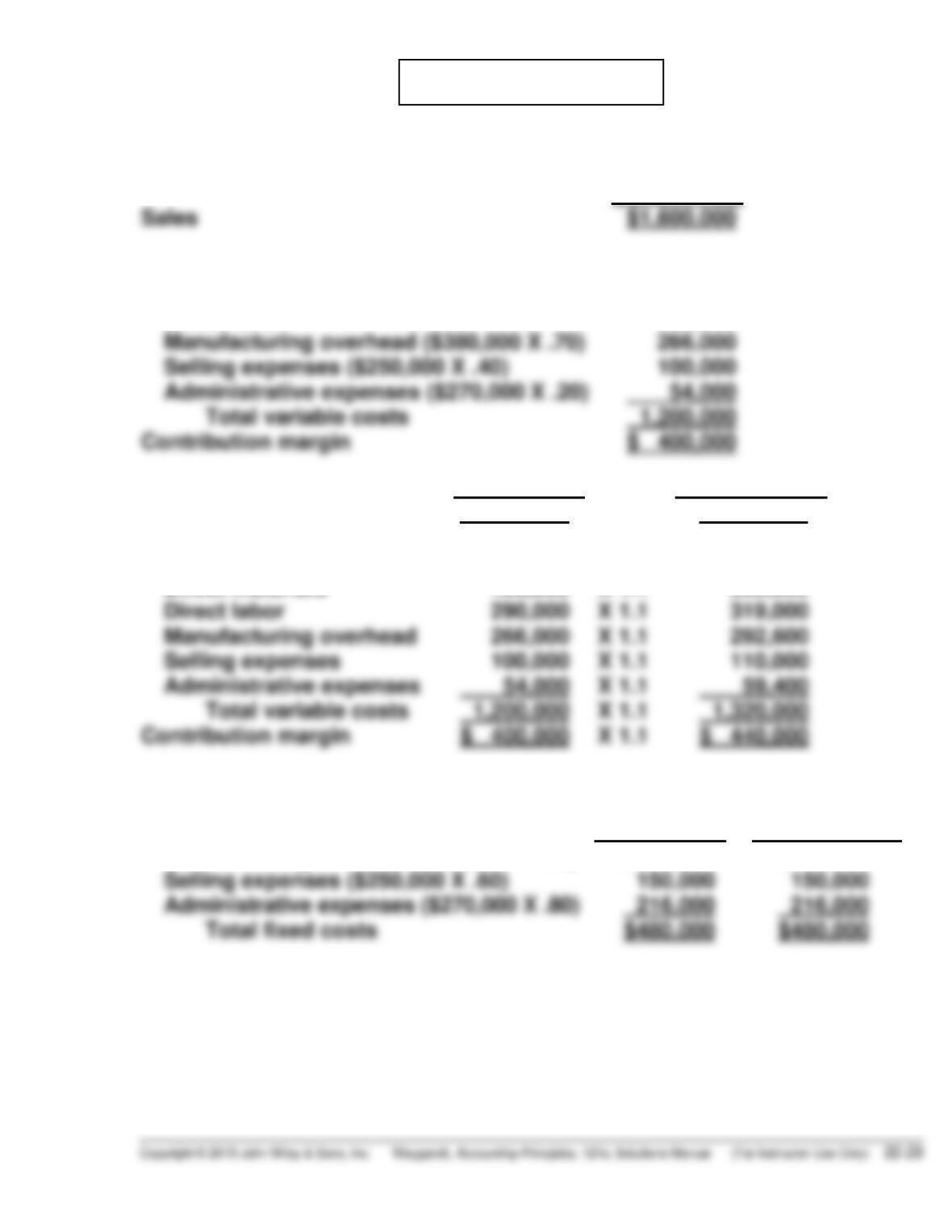

(a) JORGE COMPANY

CVP Income Statement (Estimated)

For the Year Ending December 31, 2017

Sales …………………………………………………….. $1,800,000

Variable expenses

Cost of goods sold ………………………….. $1,170,000 *

Selling expenses …………………………….. 70,000

(b) Variable costs = 70% of sales ($1,260,000 ÷ $1,800,000) or $.35 per

bottle ($.50 X 70%). Total fixed costs = $405,000.

1. $.50X = $.35X + $405,000

(c) Contribution margin ratio = ($.50 – $.35) ÷ $.50

= 30% (or 1 – .70)

PROBLEM 22–3A

(a) Sales were $2,500,000, variable expenses were $1,750,000 (70% of sales),

and fixed expenses were $850,000. Therefore, the break-even point in

dollars is:

(b) 1. The effect of this alternative is to increase the selling price per unit

to $6 ($5 X 120%). Total sales become $3,000,000 (500,000 X $6).

Thus, the contribution margin ratio changes to 42% [($3,000,000 –

$1,750,000) ÷ $3,000,000]. The new break-even point is:

Alternative 1 is the recommended course of action because it has a

lower break-even point.

PROBLEM 22–4A

(a) Current break-even point: $40X = $24X + $270,000

(where X = pairs of shoes)

(b) Current margin of safety ratio =

(20,000 X $40) – (16,875 X $40)

(20,000 X $40)

(24,000 X $38) – (21,000 X $38)

(24,000 X $38)

(c) BARGAIN SHOE STORE

CVP Income Statement

Current

New

Sales (20,000 X $40)

Variable expenses (20,000 X $24)

Contribution margin

$800,000

480,000

320,000

$912,000

576,000

336,000

(24,000 X $38)

(24,000 X $24)

PROBLEM 22–5A

(a)

(1)

Current Year

Variable costs

Direct materials

Direct labor

490,000

290,000

Current Year

Projected Year

Sales

Variable costs

Direct materials

Direct labor

$1,600,000

490,000

290,000

X 1.1

X 1.1

X 1.1

$1,760,000

539,000

319,000

(2)

Fixed Costs

Current Year

Projected year

Manufacturing overhead ($380,000 X .30)

$114,000

$114,000

PROBLEM 22-5A (Continued)

(b) Unit selling price = $1,600,000 ÷ 100,000 = $16

Unit variable cost = $1,200,000 ÷ 100,000 = $12

Break-even point in units

=

Fixed costs

÷

Unit contribution margin

120,000 units

=

$480,000

÷

$4

Fixed costs

÷

Contribution margin ratio

÷

.25

(c) Sales dollars

required for

=

(Fixed costs

+

Target net income)

÷

Contribution margin ratio

target net

income

+

÷

=

÷

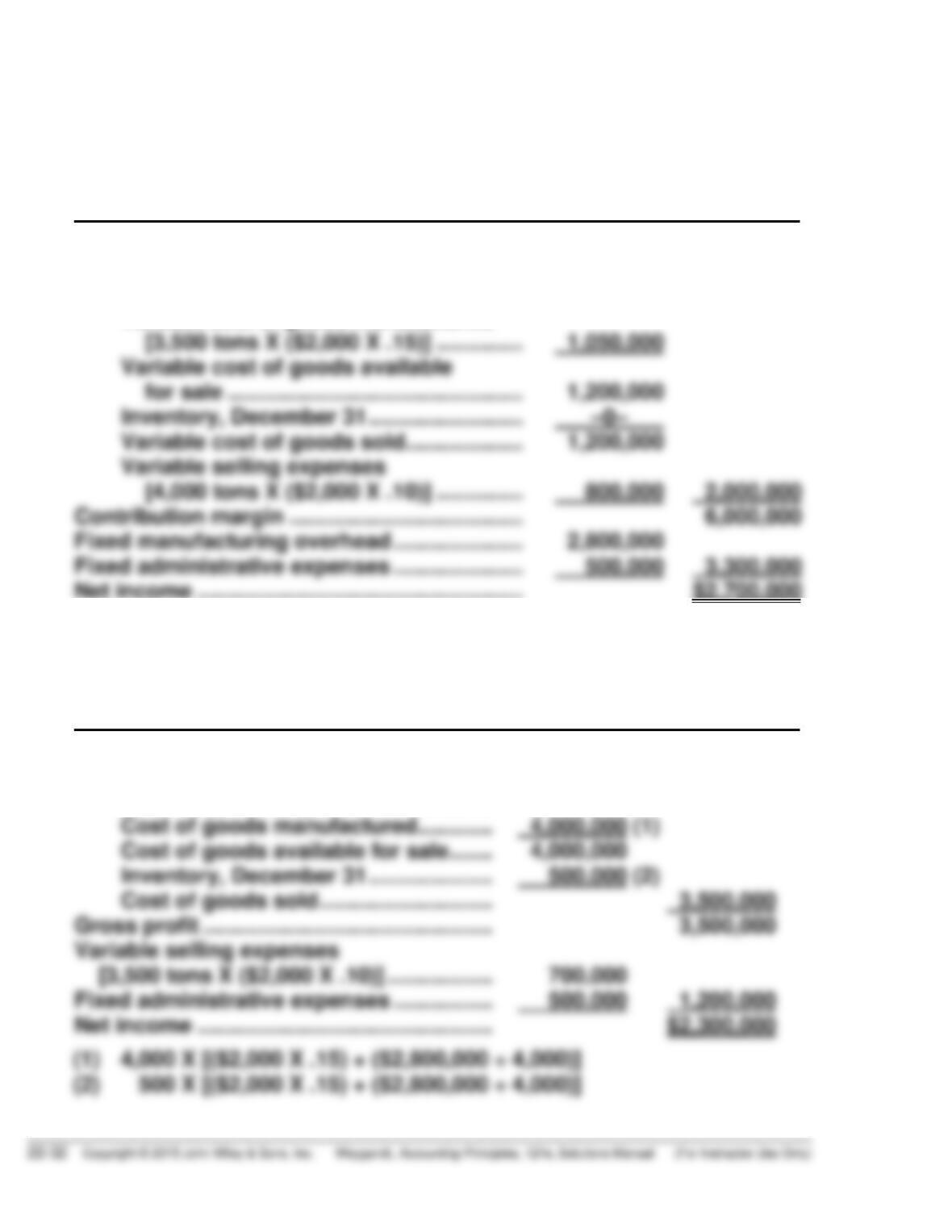

*PROBLEM 22–6A

(a) JACKSON COMPANY

Income Statement

For the Year Ended December 31, 2016

Variable Costing

Sales (3,500 tons X $2,000) …………………….

Variable cost of goods sold

Inventory, January 1 ……………………….

Variable cost of goods manufactured

$ –0–

$7,000,000

*PROBLEM 22-6A (Continued)

JACKSON COMPANY

Income Statement

For the Year Ended December 31, 2017

Variable Costing

Sales (4,000 tons X $2,000) ………………………

Variable cost of goods sold

Inventory, January 1 …………………………

Variable cost of goods manufactured

[3,500 tons X ($2,000 X .15)] …………..

$ 150,000

1,050,000

$8,000,000

(b) JACKSON COMPANY

Income Statement

For the Year Ended December 31, 2016

Absorption Costing

Sales (3,500 tons X $2,000) ………………….

Cost of goods sold

Inventory, January 1 …………………….

$ –0–

$7,000,000