CHAPTER 22 Budgeting

Ex. 22-19

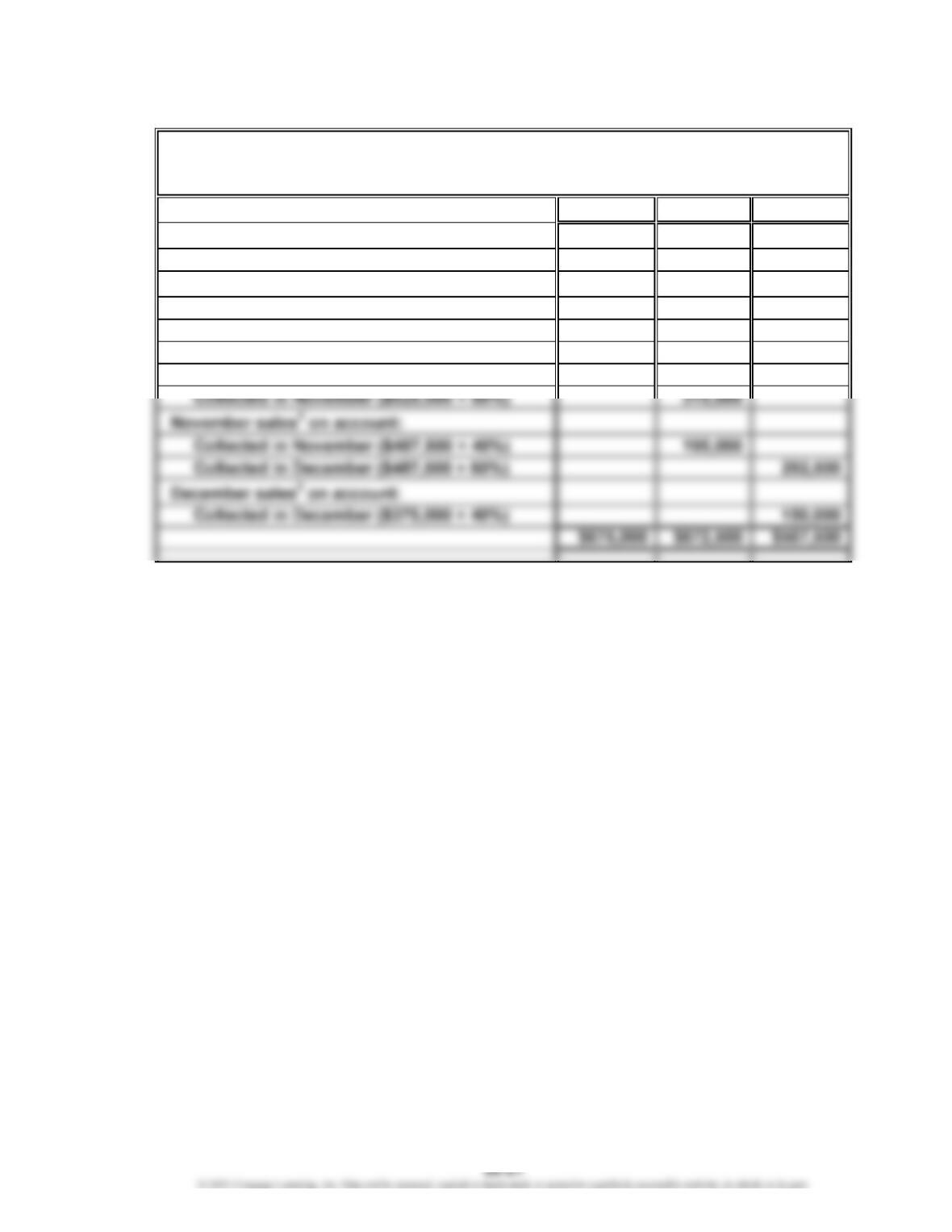

October November December

Receipts from cash sales:

Cash sales (25% × current month’s sales) $175,000 $162,500 $125,000

September sales on account:

Collected in October (Accounts Receivable

balance) 290,000

October sales

1

on account:

Collected in October ($525,000 × 40%) 210,000

1

$700,000 × 75% = $525,000

2

$650,000 × 75% = $487,500

3

$500,000 × 75% = $375,000

Office World Inc.

Schedule of Collections from Sales

For the Three Months Ending December 31

CHAPTER 22 Budgeting

Ex. 22-20

March April May

March expenses:

1

Paid in March ($52,600 × 60%) $31,560

Paid in April ($52,600 × 40%) $21,040

April expenses:

2

Paid in April ($59,400 × 60%) 35,640

Paid in May ($59,400 × 40%) $23,760

Oakwood Financial Inc.

Schedule of Cash Payments for Selling and Administrative Expenses

For the Three Months Ending May 31

CHAPTER 22 Budgeting

Ex. 22-21

January February March

1

$15,000 $ 26,430 $ 32,610

1

$15,000, given as Accrued Expenses Payable, January 1

$26,430 = ($91,600 – $3,000 – $500) × 30%

$32,610 = ($112,200 – $3,000 – $500) × 30%

2

$61,670 = ($91,600 – $3,000 – $500) × 70%

$76,090 = ($112,200 – $3,000 – $500) × 70%

$81,130 = ($119,400 – $3,000 – $500) × 70%

Ex. 22-22

20Y2 20Y3 20Y4 20Y5

Building $4,000,000 $6,000,000 $3,500,000

1

$10,000,000 × 35% = $3,500,000

2

$800,000 × 75% × 75% = $450,000

Capital Expenditures Budget

For the Four Years Ending December 31, 20Y2−20Y5

EastGate Physical Therapy Inc.

Schedule of Cash Payments for Operations

For the Three Months Ending March 31

Omicron Inc.

1

CHAPTER 22 Budgeting

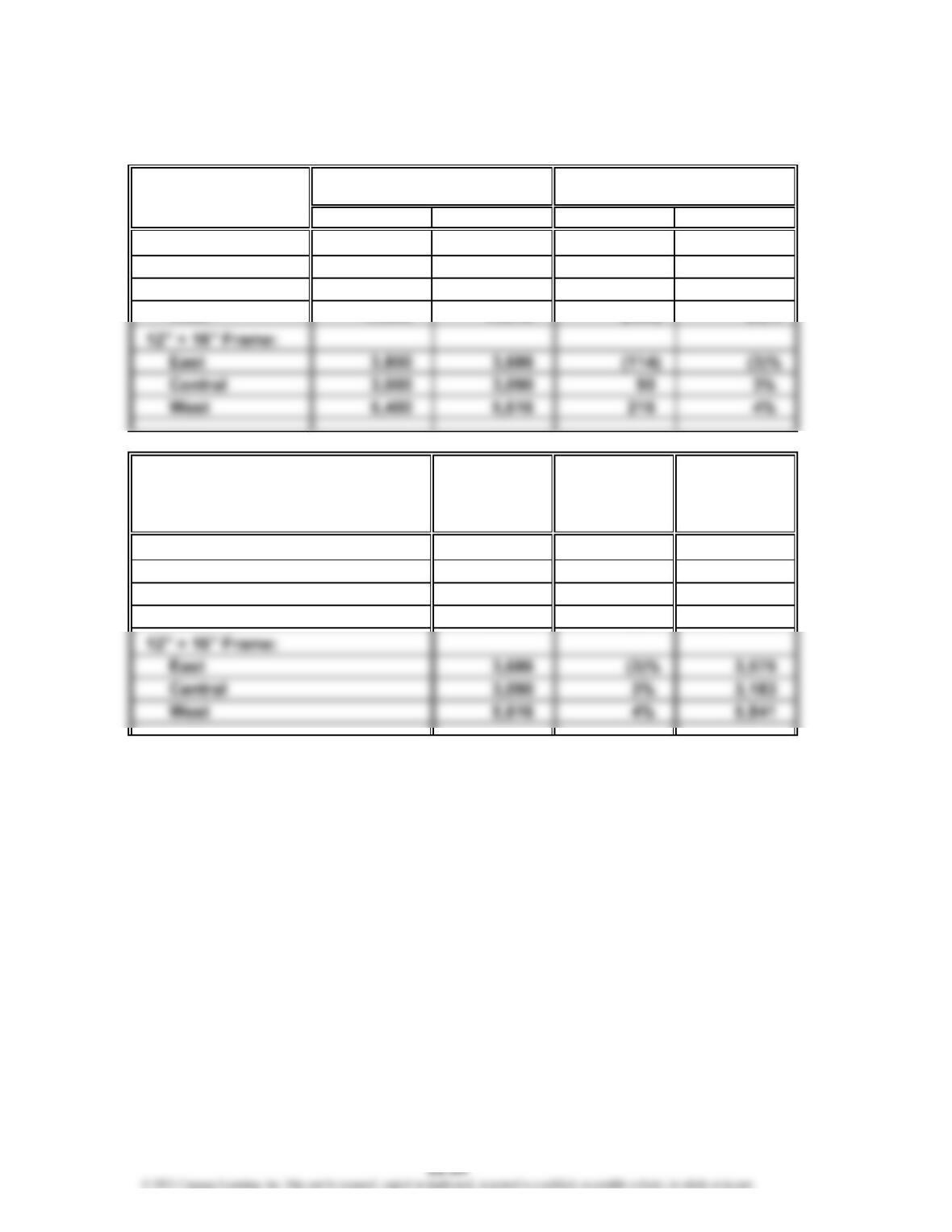

Prob. 22-1A

1.

Budget Actual Sales Amount Percent

8″ × 10″ Frame:

East 8,500 8,755 255 3%

Central 6,200 6,510 310 5%

2. 20Y7

20Y6 Percentage Budgeted

Actual Increase Units

Units (Decrease) (rounded)

8″ × 10″ Frame:

East 8,755 3% 9,018

Central 6,510 5% 6,836

West 12,348 (2)% 12,101

PROBLEMS

Increase (Decrease)

Actual Over BudgetUnit Sales, Year Ended 20Y6

CHAPTER 22 Budgeting

Prob. 22-1A (Concluded)

3.

Unit Sales Unit Selling

Volume Price Total Sales

8″ × 10″ Frame:

East 9,018 $17 $153,306

Central 6,836 17 116,212

West 12,101 17 205,717

Product and Area

Raphael Frame Company

For the Year Ending December 31, 20Y7

Sales Budget

CHAPTER 22 Budgeting

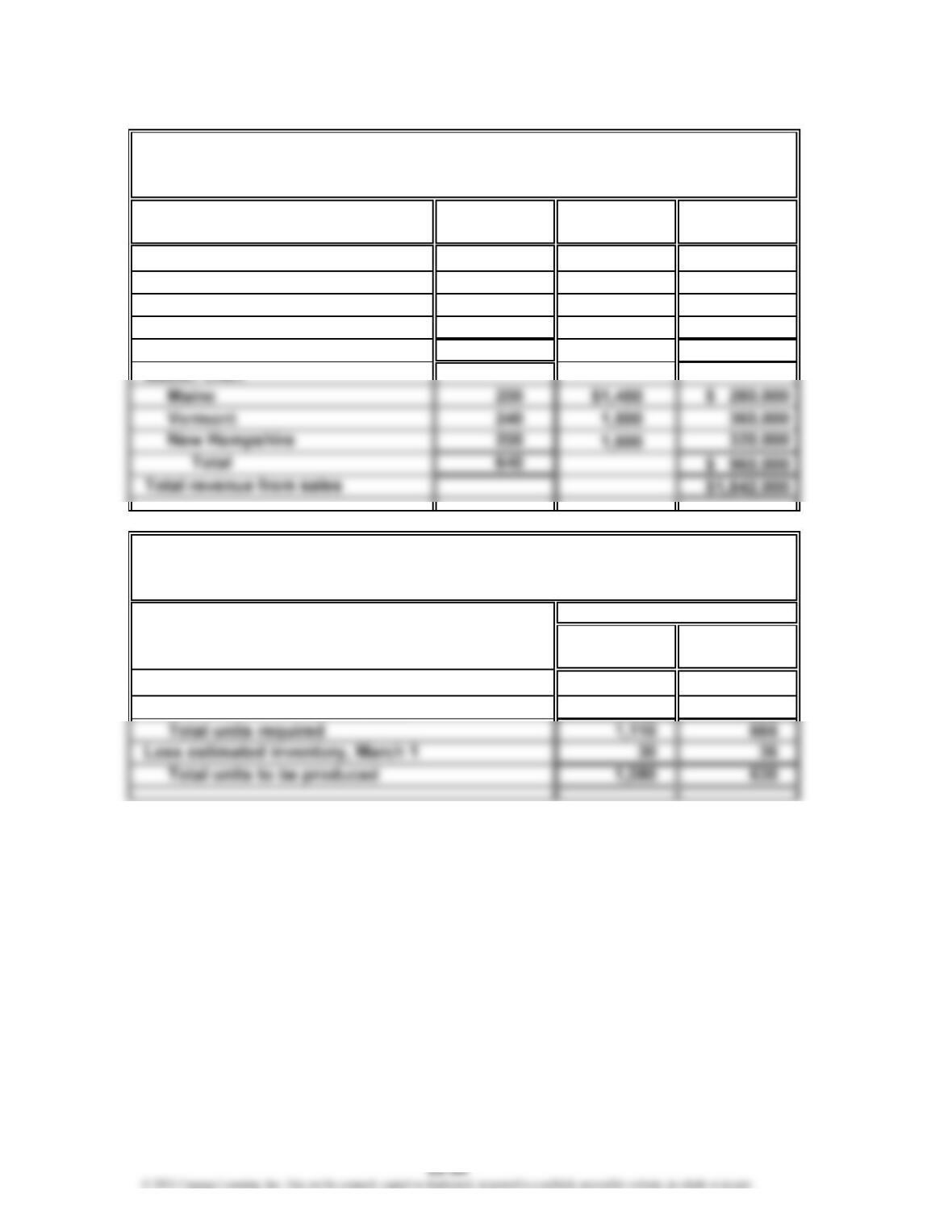

Prob. 22-2A

1.

Unit Sales Unit Selling

Volume Price Total Sales

Backyard Chef:

Maine 350 $ 800 $ 280,000

Vermont 400 825 330,000

New Hampshire 320 850 272,000

Total 1,070 $ 882,000

2.

Backyard Master

Chef Chef

Expected units to be sold 1,070 640

Plus desired inventory, March 31 40 26

For the Month Ending March 31

Units

Product and Area

Gourmet Grill Company

Sales Budget

For the Month Ending March 31

Gourmet Grill Company

Production Budget

CHAPTER 22 Budgeting

Prob. 22-2A (Continued)

3.

Stainless Burner

Grates Steel Subassemblies Shelves

(units) (lb.) (units) (units) Total

Required units for

production:

Backyard Chef 3,240 25,920 2,160 4,320

Total units to be

purchased 7,000 52,180 4,700 7,520

Unit price $16.00 $8.00 $120.00 $12.00

Total direct materials

to be purchased $112,000 $417,440 $564,000 $90,240 $1,183,680

1

1,080 × 3 grates = 3,240 grates

2

1,080 × 24 lb. = 25,920 lb.

3

1,080 × 2 subassemblies = 2,160 subassemblies

4

1,080 × 4 shelves = 4,320 shelves

5

630 × 6 grates = 3,780 grates

Gourmet Grill Company

Direct Materials Purchases Budget

For the Month Ending March 31

××××

12 34

56 78

CHAPTER 22 Budgeting

Prob. 22-2A (Concluded)

4.

Stamping Forming Assembly

Department Department Department Total

Hours required for production:

Backyard Chef

1

540 648 1,080

2

378 504 945

1

This line is computed as 1,080 Backyard Chef units from the production budget multiplied

by the hours per unit in each department estimated for the Backyard Chef.

540 = 1,080 × 0.5; 648 = 1,080 × 0.6; 1,080 = 1,080 × 1.0

Gourmet Grill Company

Direct Labor Cost Budget

For the Month Ending March 31

CHAPTER 22 Budgeting

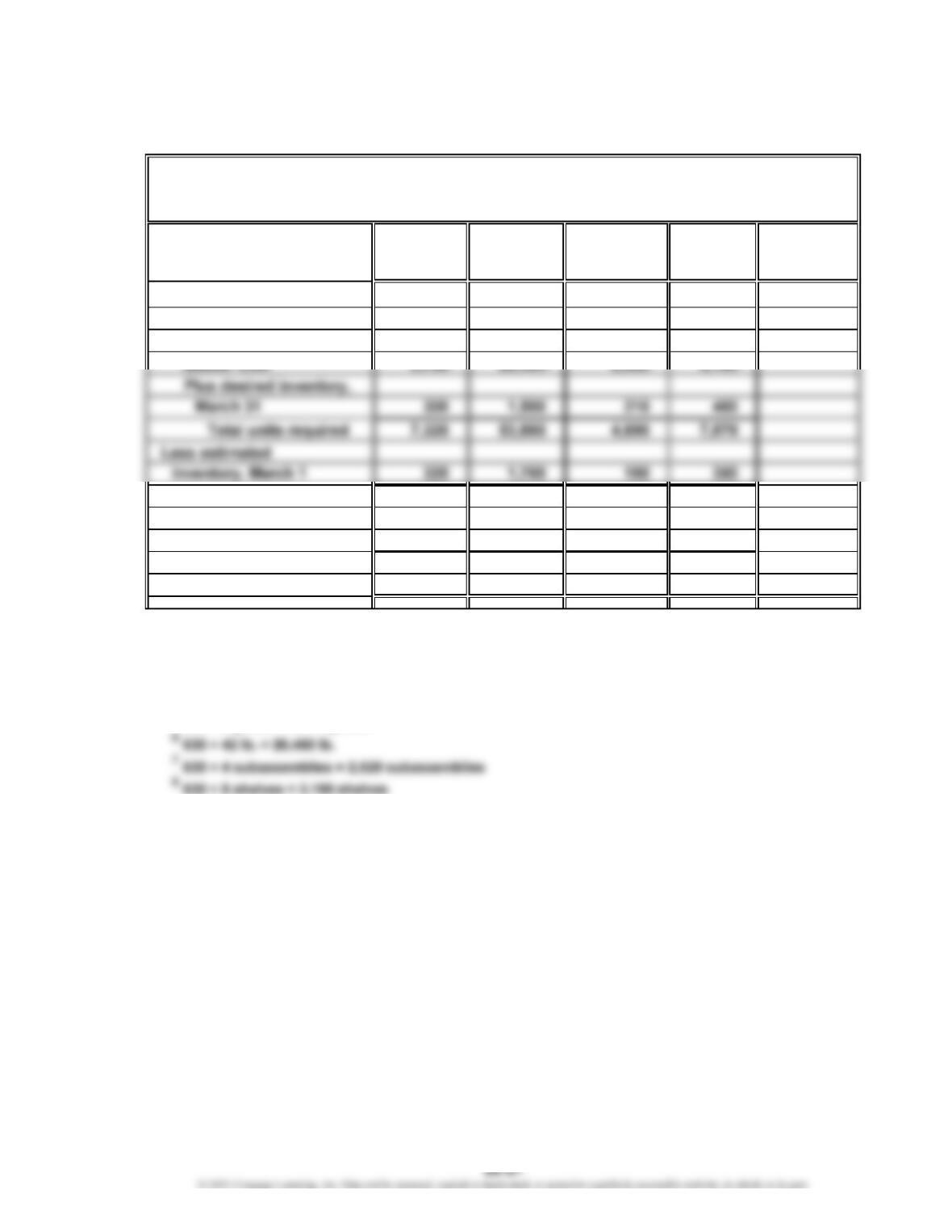

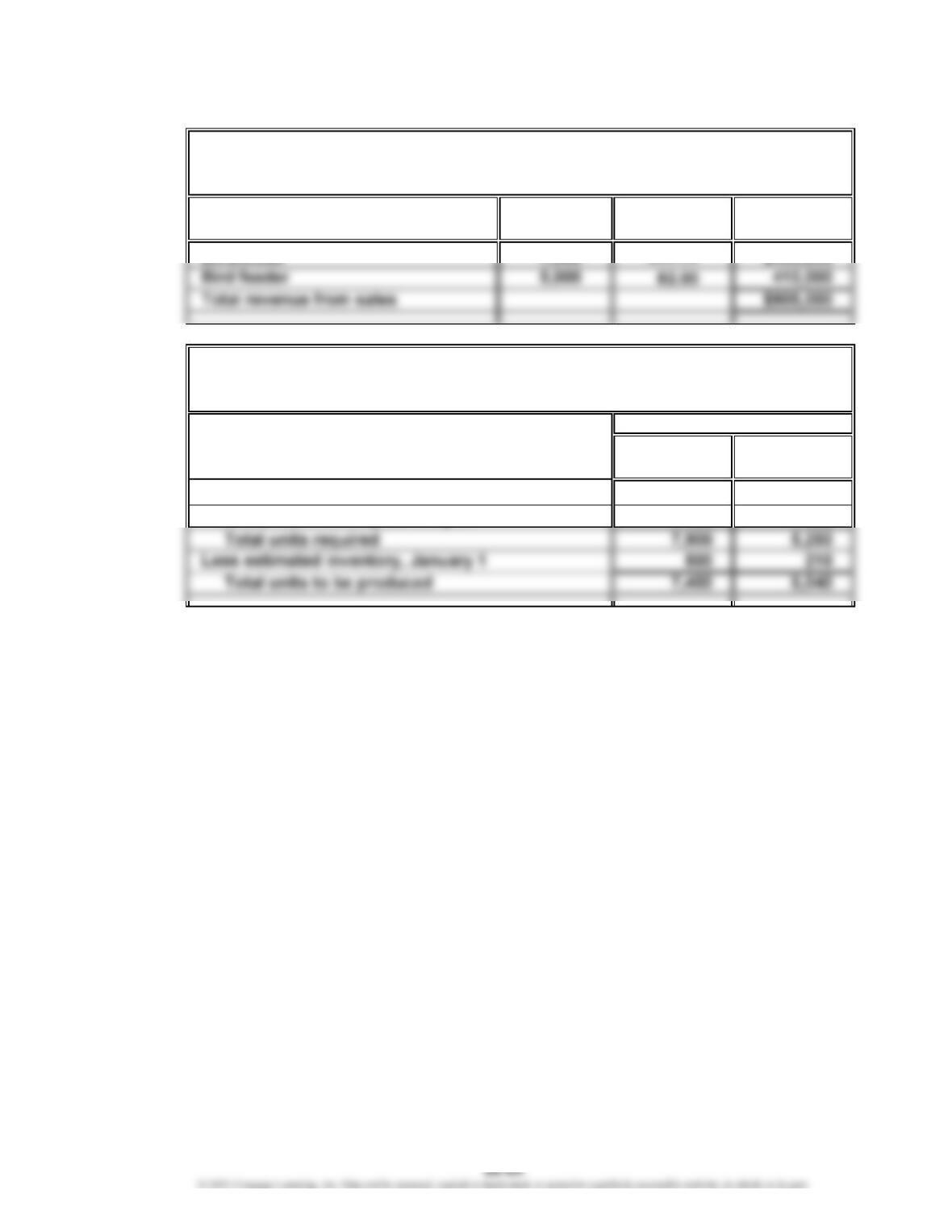

Prob. 22-3A

1.

Unit Sales Unit Selling

Volume Price Total Sales

2.

Bird- Bird

house Feeder

Expected units to be sold 7,500 5,000

Plus desired inventory, January 31 400 250

For the Month Ending January 31

Units

Birds and Beyond Inc.

Sales Budget

For the Month Ending January 31

Birds and Beyond Inc.

Production Budget

CHAPTER 22 Budgeting

Prob. 22-3A (Continued)

3.

Wood Plastic Total

Required units for production:

Birdhouse 5,920 3,700

Bird feeder 6,048 3,780

Plus desired inventory, January 31 220 340

1

7,400 × 0.80 ft. = 5,920 ft.

2

Birds and Beyond Inc.

Direct Materials Purchases Budget

For the Month Ending January 31

12

34

CHAPTER 22 Budgeting

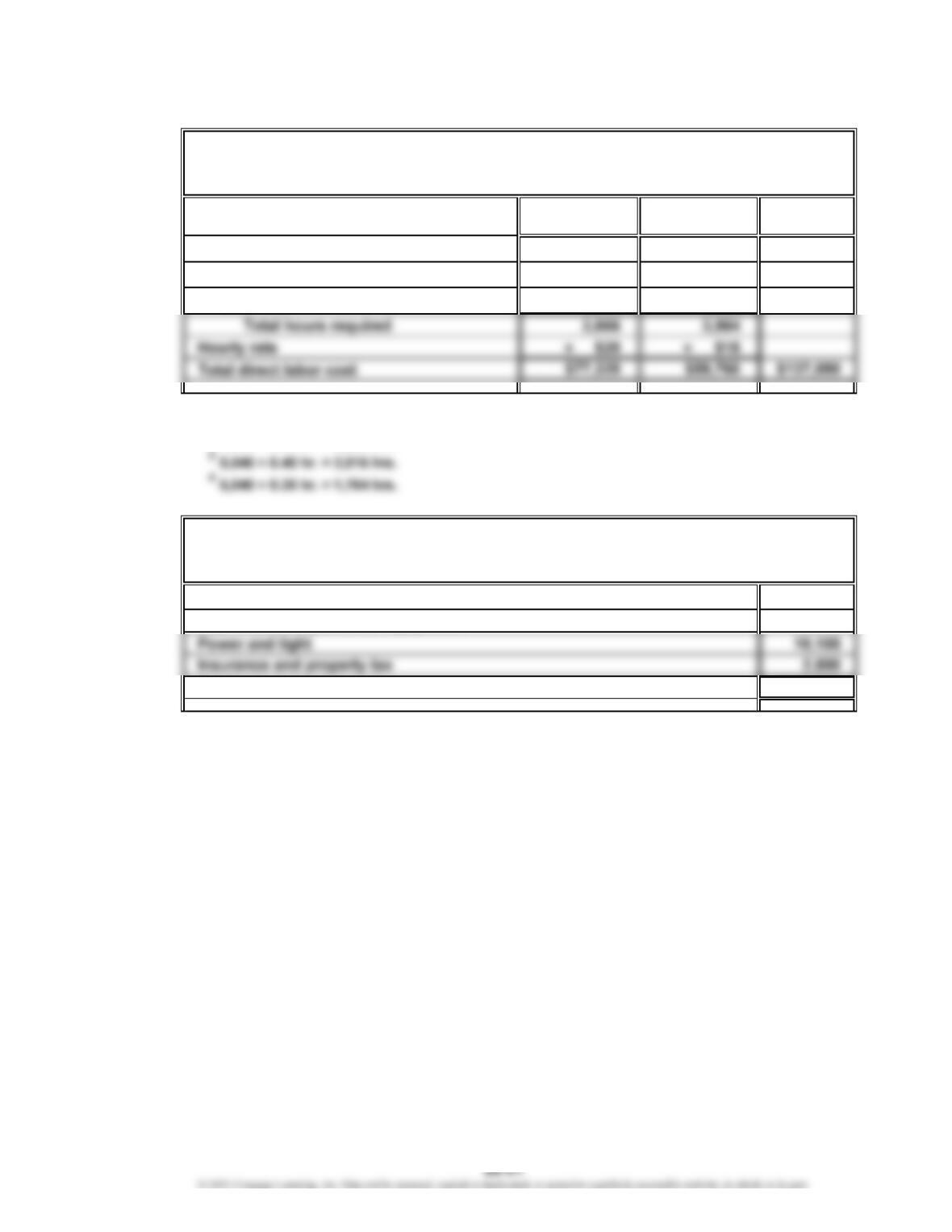

Prob. 22-3A (Continued)

4.

Fabrication Assembly

Department Department Total

Hours required for production:

Birdhouse 1,850 2,220

Bird feeder 2,016 1,764

1

7,400 × 0.25 hr. = 1,850 hrs.

2

7,400 × 0.30 hr. = 2,220 hrs.

5.

Indirect factory wages $ 92,000

Depreciation of plant and equipment 34,000

Total $138,900

Factory Overhead Cost Budget

For the Month Ending January 31

Birds and Beyond Inc.

Direct Labor Cost Budget

For the Month Ending January 31

Birds and Beyond Inc.

12

34

6.

Finished goods inventory, January 1

1

$ 22,400

Work in process inventory, January 1 $ 33,600

January 31

3

2,456

Cost of direct materials placed in

production $118,184

Direct labor 137,080

Factory overhead 138,900

Total manufacturing costs 394,164

Total work in process during period $427,764

1

Birdhouse (500 × $28)…………………………………………………………… $14,000

Bird feeder (210 × $40)…………………………………………………………

…

8,400

Finished goods inventory, January 1………………………………………

…

$22,400

…

…

Direct materials inventory, January 31………………………………………

…

$ 2,456

4

Birdhouse (400 × $28)…………………………………………………………… $11,200

Bird feeder (250 × $40)…………………………………………………………

…

10,000

Finished goods inventory, January 31………………………………………

…

$21,200

Cost of Goods Sold Budget

For the Month Ending January 31

Birds and Beyond Inc.

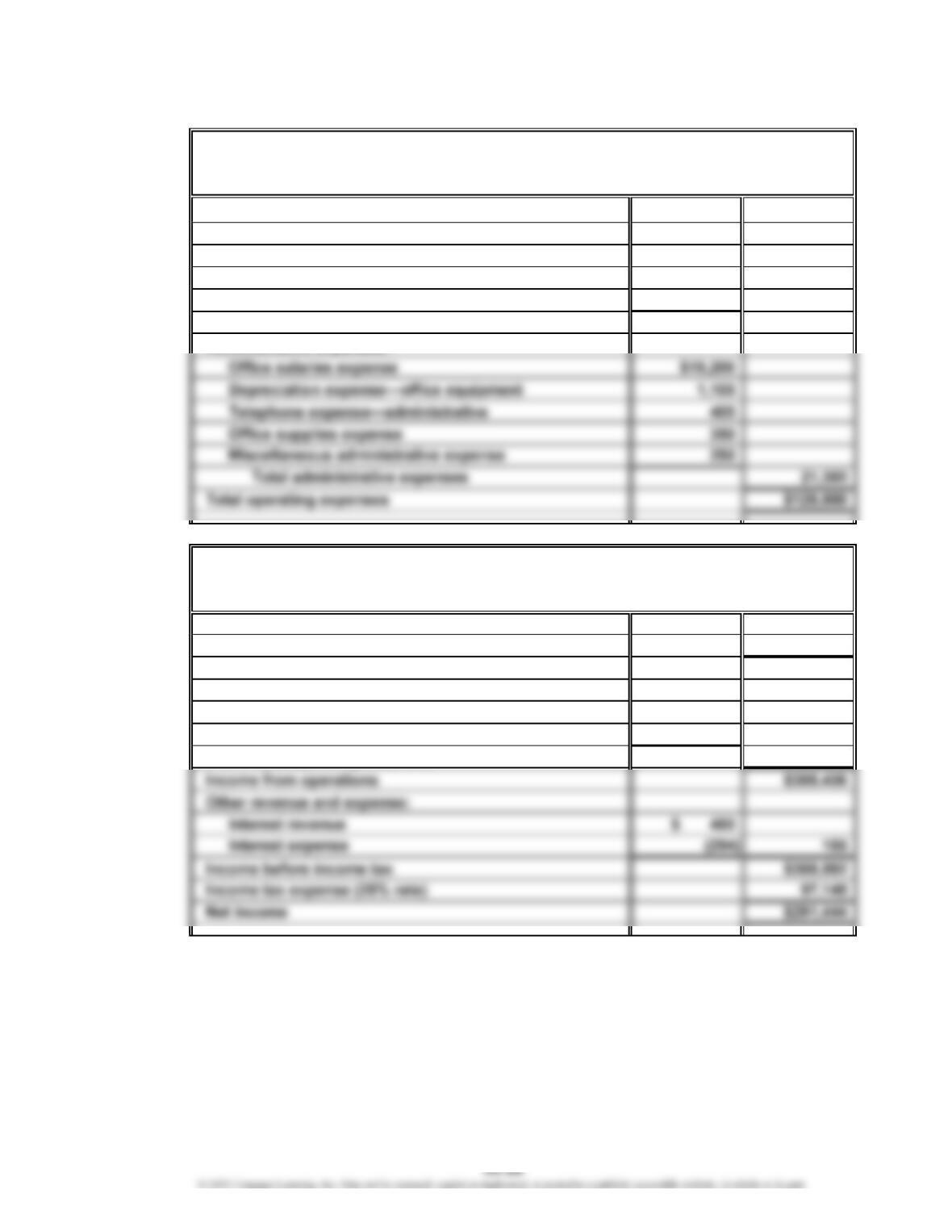

CHAPTER 22 Budgeting

Prob. 22-3A (Concluded)

7.

Selling expenses:

Sales salaries expense $85,100

Advertising expense 17,600

Telephone expense—selling 1,000

Travel expense—selling 3,800

Total selling expenses $107,500

8.

Revenue from sales $905,000

Cost of goods sold 387,764

Gross profit $517,236

Operating expenses:

Selling expenses $107,500

Administrative expenses 21,300

Total operating expenses 128,800

Birds and Beyond Inc.

Birds and Beyond Inc.

Budgeted Income Statement

For the Month Ending January 31

Selling and Administrative Expenses Budget

For the Month Ending January 31

CHAPTER 22 Budgeting

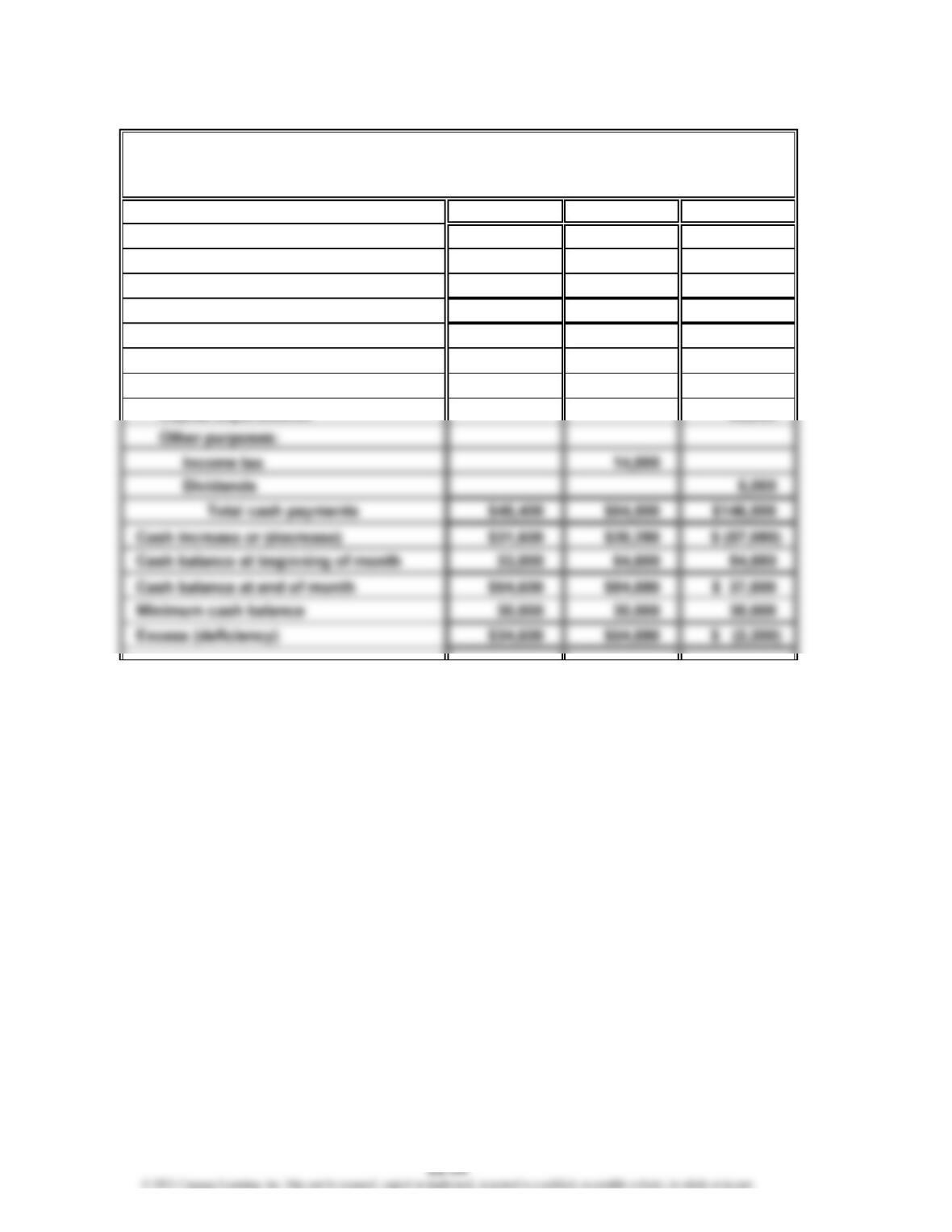

Prob. 22-4A

1.

May June July

Estimated cash receipts from:

Cash sales (10% of monthly sales) $ 8,600 $ 9,000 $ 9,500

Collection of accounts receivablea68,400 75,780 79,920

Total cash receipts $77,000 $84,780 $ 89,420

Estimated cash payments for:

Manufacturing costsb$30,400 $34,500 $ 39,500

Selling and administrative expenses 15,000 16,000 22,000

Sonoma Housewares Inc.

For the Three Months Ending July 31

Cash Budget

CHAPTER 22 Budgeting

Prob. 22-4A (Concluded)

Computations:

a

Collections of accounts receivable: May June July

March sales………………………………………

…

$18,000

April sales…………………………………………

…

50,400 $21,600

1

$60,000 × 30% = $18,000

2

$72,000 × 70% = $50,400

3

$72,000 × 30% = $21,600

b

Payments for manufacturing costs: May June July

Payment of accounts payable, beginning

of month balance

c

……………………………

…

$ 6,000 $ 6,100 $ 7,100

Pa

y

ment of current month’s cost

d

……………

…

24,400 28,400 32,400

Total……………………………………………

…

$30,400 $34,500 $39,500

2. The budget indicates that the minimum cash balance will not be maintained

in July. This is due to the capital expenditures requiring significant cash

outflows during this month. This situation can be corrected by borrowing

and/or by the sale of the marketable securities, if they are held for such

1

23

…

…

CHAPTER 22 Budgeting

Prob. 22-5A

1.

Sales1$1,000,000

Cost of goods sold:

Operating expenses:

Selling expenses:

Sales salaries and commissions5$136,000

Advertising 64,000

Miscellaneous sellin

g

ex

p

enses656,000

Total selling expenses $256,000

Income tax expense 30,000

Net income $ 96,600

1200,000 units × $5.00

2200,000 units × $1.10

3200,000 units × $0.65

4(200,000 units × $0.40) + $40,000 + $12,000

5(200,000 units × $0.45) + $46,000

Regina Soap Co.

Budgeted Income Statement

For the Year Ending December 31, 20Y4

CHAPTER 22 Budgeting

Prob. 22-5A (Continued)

2.

Current assets:

Cash 1 $135,800

Prepaid expenses 2,600

Total current assets $414,700

Property, plant, and equipment:

Plant and equipment 2 $400,000

Less accumulated depreciation 3 196,200 203,800

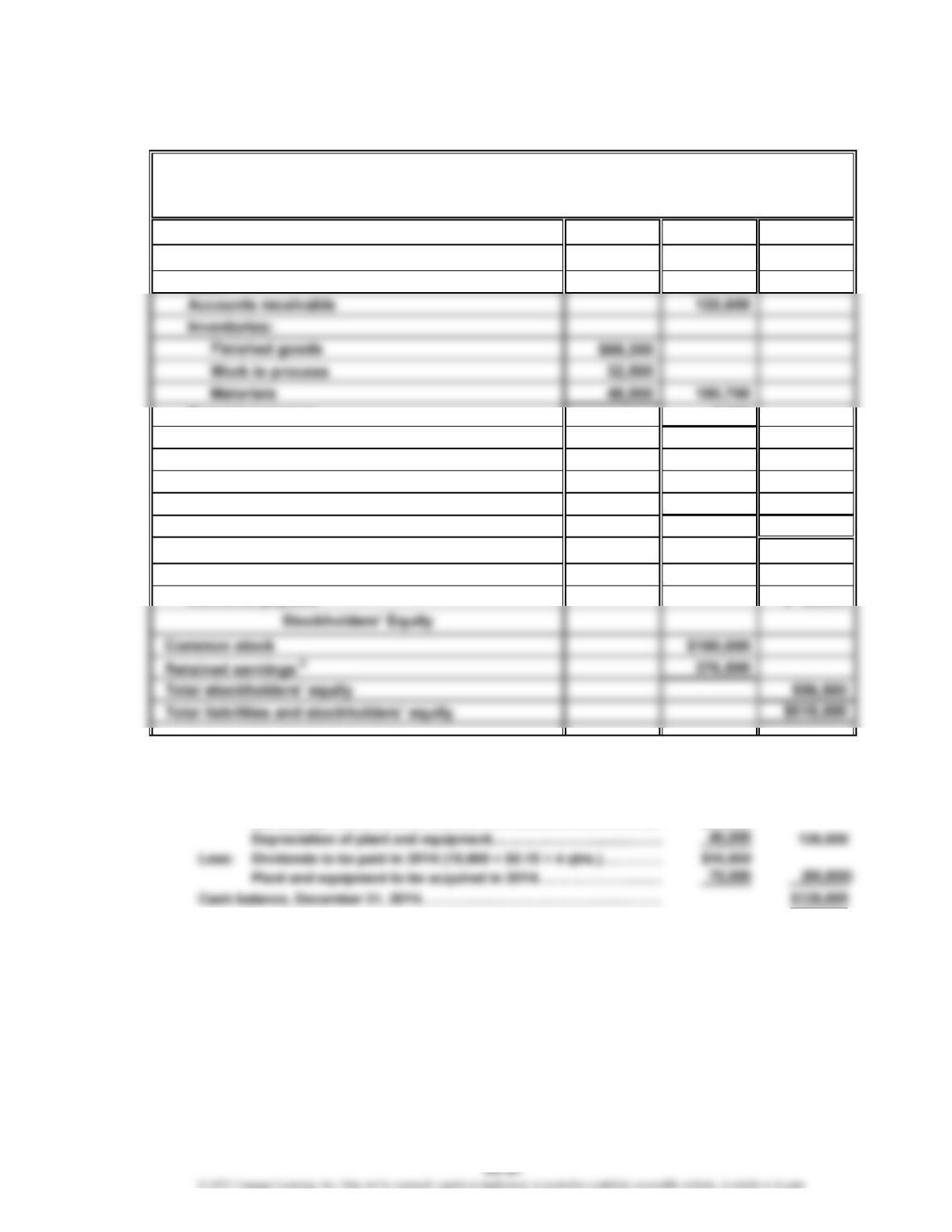

Total assets $618,500

Current liabilities:

1Cash balance, December 31, 20Y4:

Balance, January 1, 20Y4………………………………………………………

…

$ 85,000

Add: Cash from operations

Net income*……………………………………………………………

…

$96,600

…

*As per question: Balances of accounts receivable, prepaid expenses, and accounts payable

at the end of the year are not expected to differ significantly from the beginning balances.

Therefore, there is no need to adjust net income for changes to current assets and/or

current liabilities to arrive at the cash from operating activities.

Regina Soap Co.

Budgeted Balance Sheet

December 31, 20Y4

Assets

Liabilities

CHAPTER 22 Budgeting

Prob. 22-5A (Concluded)

2$325,000 + $75,000 = $400,000

3$156,200 + $40,000 = $196,200

4Retained earnings balance, December 31, 20Y4:

CHAPTER 22 Budgeting

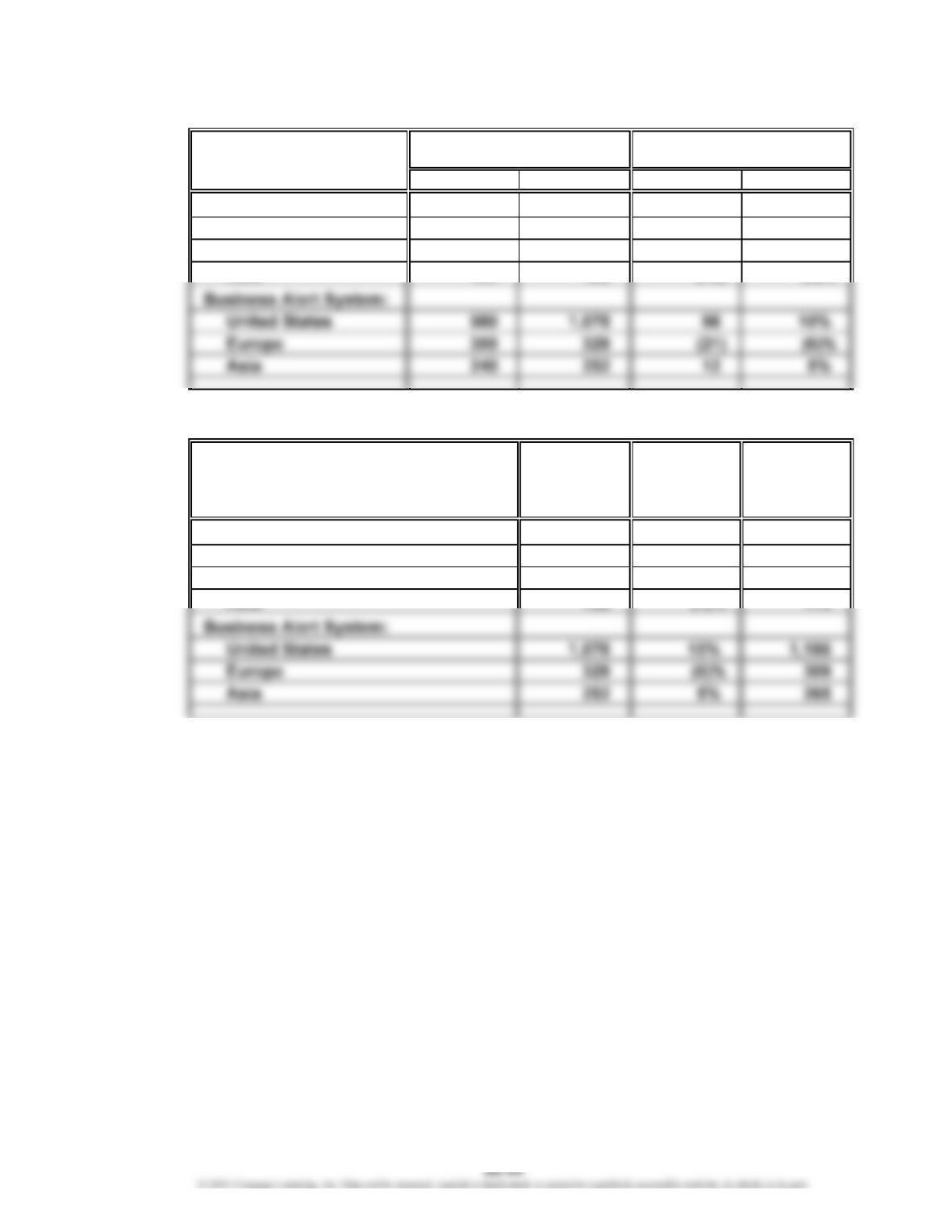

Prob. 22-1B

1.

Budget Actual Sales Amount Percent

Home Alert System:

United States 1,700 1,734 34 2%

Europe 580 609 29 5%

*

34 ÷ 1,700

2.

20Y9

20Y8 Percenta

g

eBud

g

eted

Actual Increase Units

Units

(

Decrease

)

(

rounded

)

Home Alert System:

United States 1,734 2% 1,769

Europe 609 5% 639

Increase (Decrease)

Unit Sales, Year Ended 20Y8 Actual Over Bud

g

et

*

CHAPTER 22 Budgeting

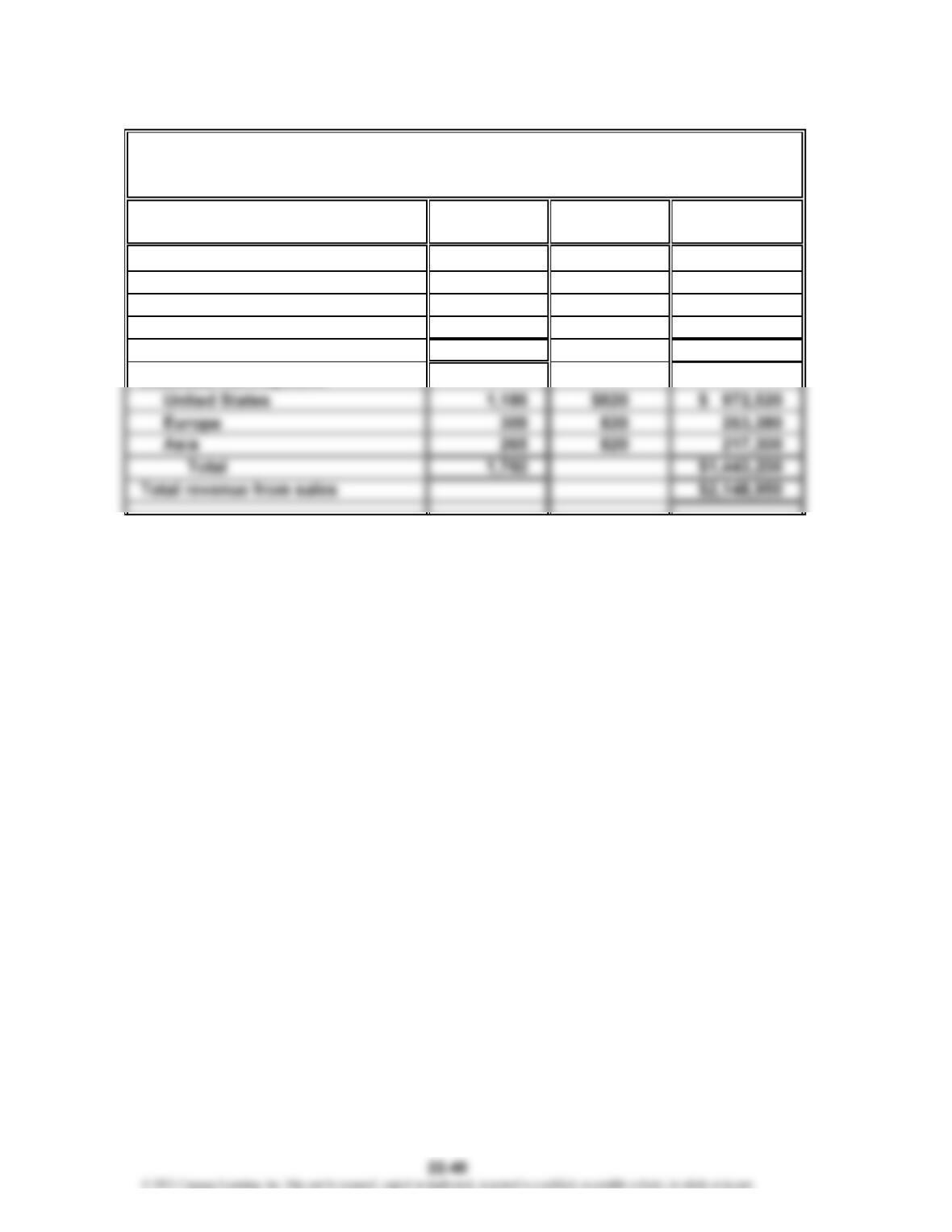

Prob. 22-1B (Concluded)

3.

Unit Sales Unit Selling

Volume Price Total Sales

Home Alert System:

United States 1,769 $250 $ 442,250

Europe 639 250 159,750

Asia 415 250 103,750

Total 2,823 $ 705,750

Product and Area

Sentinel Systems Inc.

For the Year Ending December 31, 20Y9

Sales Budget