Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CHAPTER 22

SOLUTIONS TO PROBLEMS: SET B

PROBLEM 22-1B

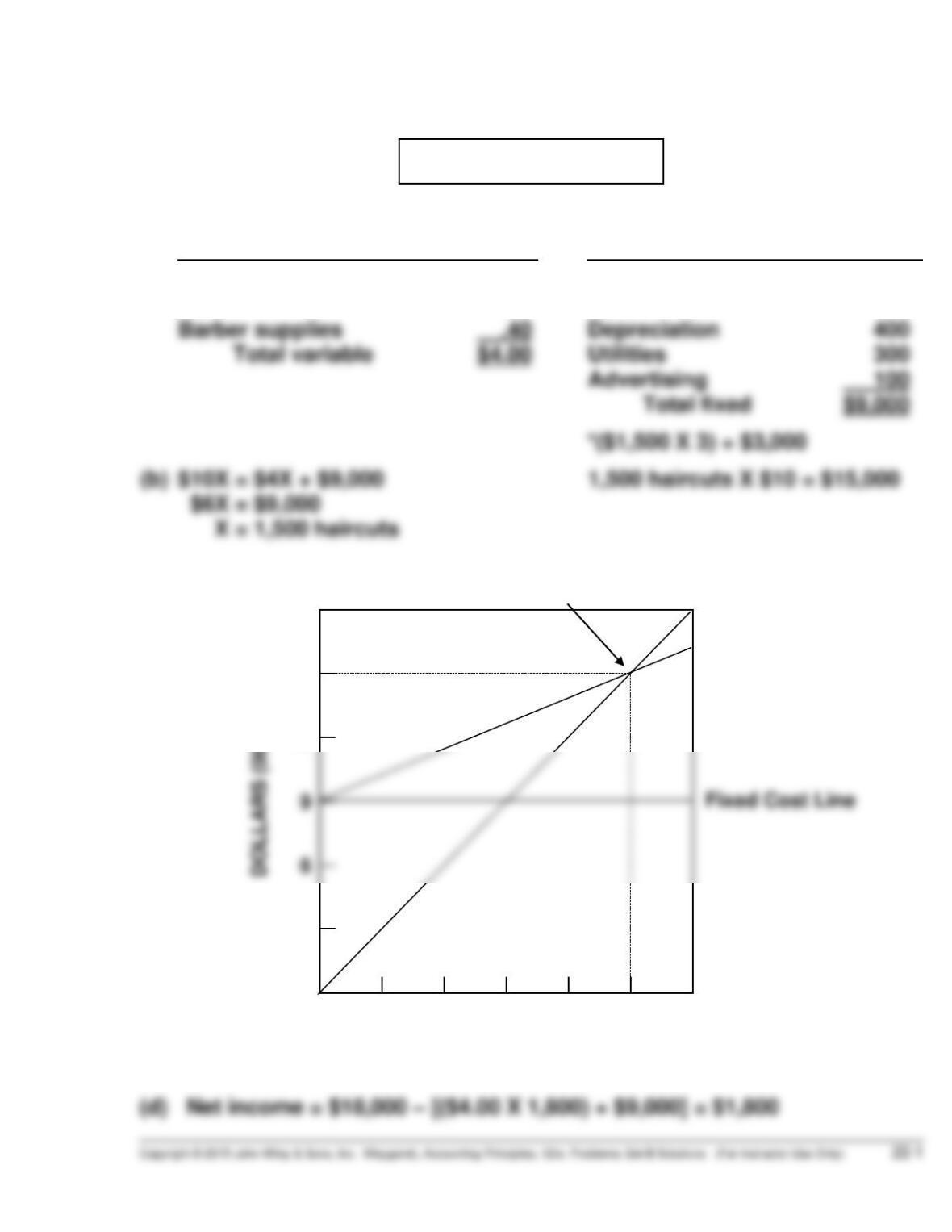

(a)

Variable costs (per haircut)

Fixed costs (per month)

Barbers’ commission $3.00

Rent .60

Barbers’ salaries $7,500*

Rent 700

(c)

18

Break-even Point

Sales Line

15

Total Cost Line

12

3

300

600

900

1,200

1,500

1,800

Number of Haircuts

PROBLEM 22-2B

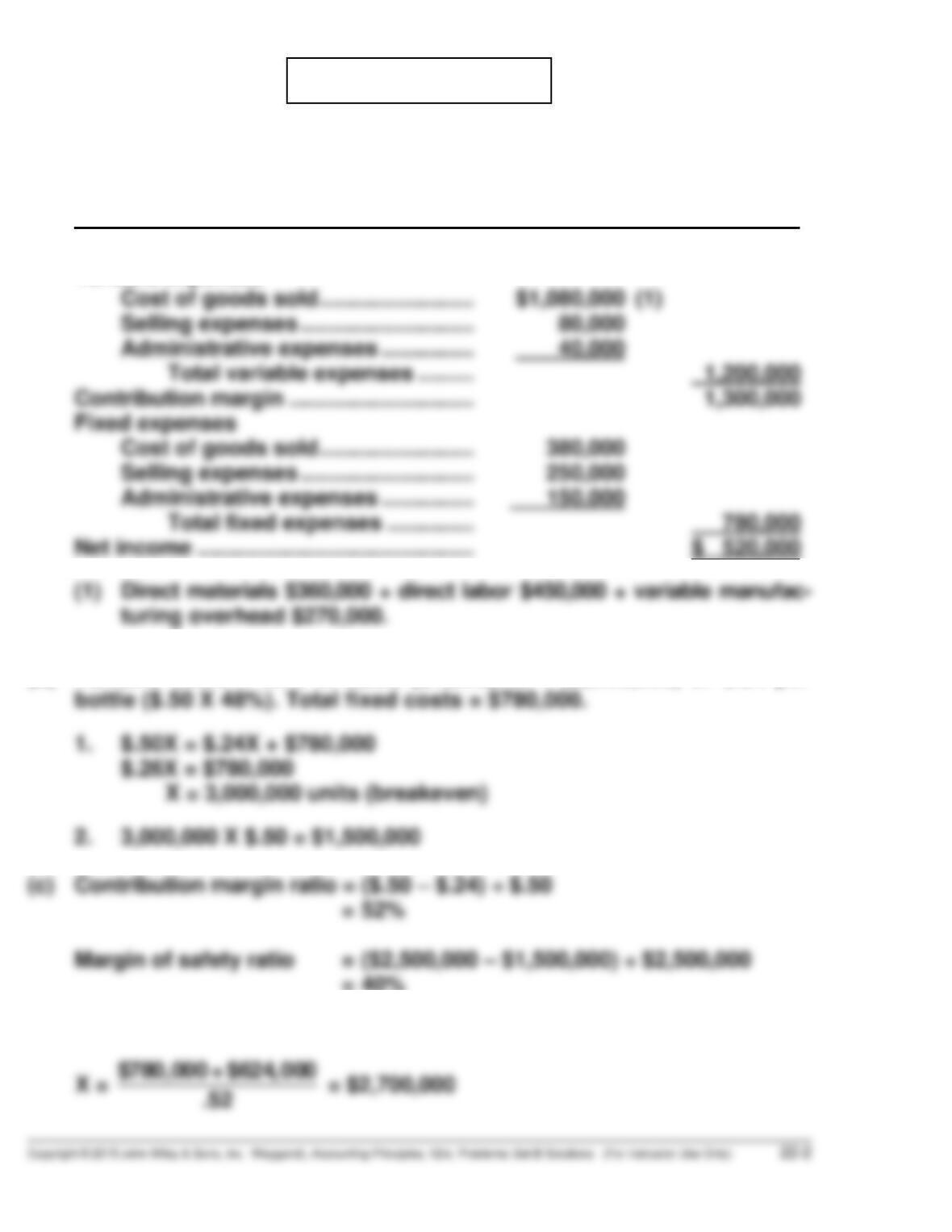

(a) ALL FRUTE COMPANY

CVP Income Statement (Estimated)

For the Year Ending December 31, 2016

Sales ....................................................... $2,500,000

Variable expenses

Cost of goods sold ......................... $1,080,000 (1)

Selling expenses ............................ 80,000

Administrative expenses ............... 40,000

(1) Direct materials $360,000 + direct labor $450,000 + variable manufac-

(b) Variable costs = 48% of sales ($1,200,000 ÷ $2,500,000) or $.24 per

bottle ($.50 X 48%). Total fixed costs = $780,000.

(c) Contribution margin ratio = ($.50 – $.24) ÷ $.50

= 52%

(d) Required sales

PROBLEM 22-3B

(a) Sales were $1,800,000 and variable expenses were $1,170,000, which

means contribution margin was $630,000 and CM ratio was 35%. Fixed

expenses were $840,000. Therefore, the breakeven point in dollars is:

(b) 1. The effect of this alternative is to increase the selling price per unit

to $37.50 ($30 X 125%). Total sales become $2,250,000 (60,000 X

$37.50). Thus, the contribution margin ratio changes to 48%

[($2,250,000 – $1,170,000) ÷ $2,250,000]. The new breakeven point is:

2. The effects of this alternative are to change total fixed costs to

$660,000 ($840,000 – $180,000) and to change the contribution margin

to .30 [($1,800,000 – $1,170,000 – $90,000) ÷ $1,800,000]. The new

breakeven point is:

3. The effects of this alternative are: (1) variable and fixed cost of

goods sold become $675,000 each, (2) total variable costs become

$915,000 ($675,000 + $125,000 + $115,000), and (3) total fixed costs

are $1,095,000 ($675,000 + $355,000 + $65,000). The new breakeven

point is:

PROBLEM 22-4B

(a) Current break-even point: $30X = $12X + $216,000

(where X = pairs of shoes)

(b) Current margin of safety ratio =

(20,000 X $30) – (12,000 X $30)

(20,000 X $30)

= 40%

(c) COSTLESS SHOE STORE

CVP Income Statement

Current

New

Sales (20,000 X $30)

Variable expenses (20,000 X $12)

Contribution margin

$600,000

240,000

360,000

$648,000

288,000

360,000

(24,000 X $27)

(24,000 X $12)

PROBLEM 22-5B

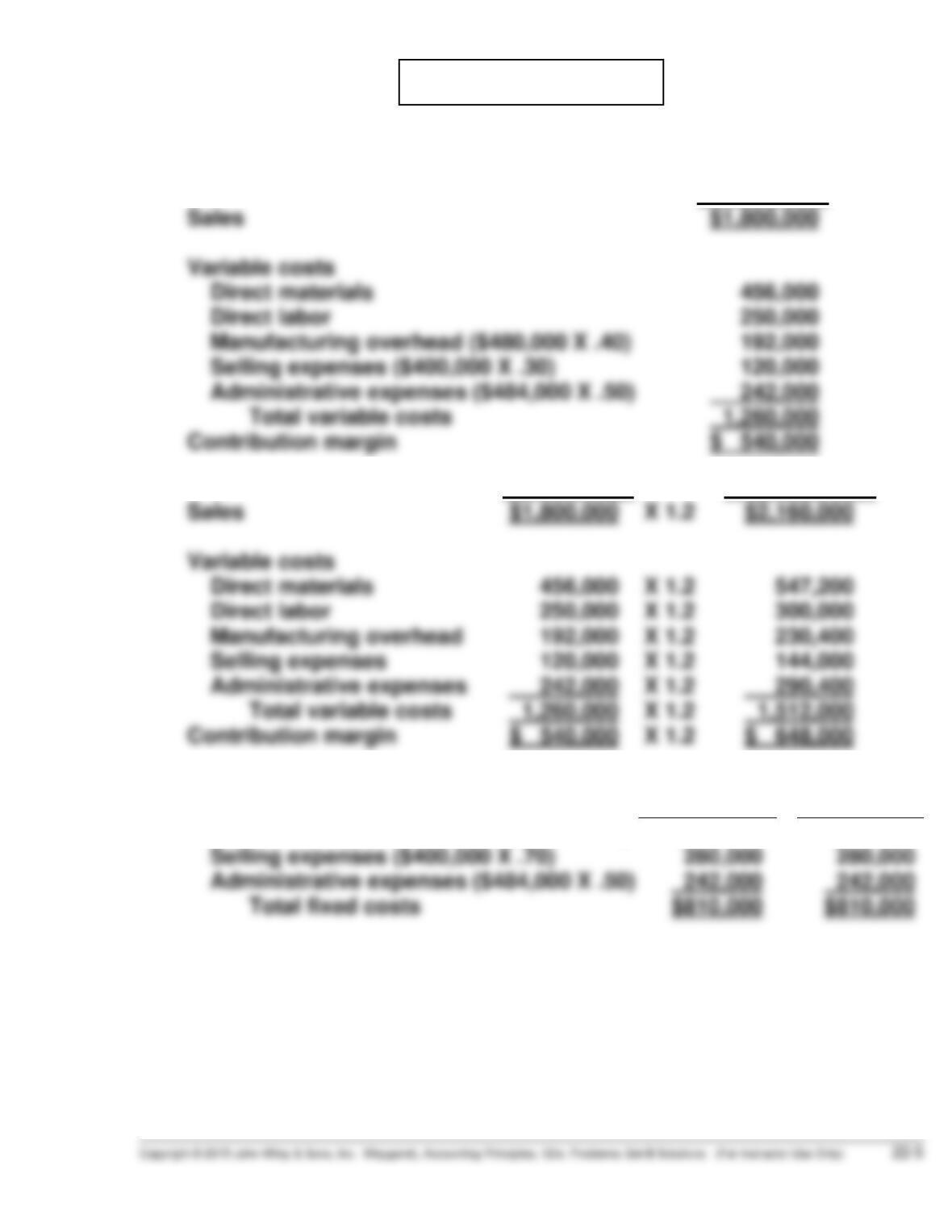

(a)

(1)

Current Year

Sales

Variable costs

Direct materials

Direct labor

$1,800,000

456,000

250,000

Current Year

Projected Year

Sales

Variable costs

Direct materials

Direct labor

$1,800,000

456,000

250,000

X 1.2

X 1.2

X 1.2

$2,160,000

547,200

300,000

(2)

Current

Projected

Fixed Costs

Year

Year

Manufacturing overhead ($480,000 X .60)

$288,000

$288,000

PROBLEM 22-5B (Continued)

(b) Unit selling price = $1,800,000 ÷ 100,000 = $18.00

Unit variable cost = $1,260,000 ÷ 100,000 = $12.60

(c) Sales dollars

required for

=

(Fixed costs

+

Target net income)

÷

Contribution margin ratio

target net income

(e)

(1)

Sales

Variable costs

Direct materials

Direct labor ($250,000 – $100,000)

$1,800,000

456,000

150,000

PROBLEM 22-5B (Continued)

(3) Break-even point in dollars = $754,000 ÷ .32 = $2,356,250

Fixed costs

The break-even point in dollars declined from $2,700,000 to $2,356,250.

This means that overall the company’s risk has declined because it

doesn’t have to generate as much in sales. The two changes actually

*PROBLEM 22-6B

(a) FAB COMPANY

Income Statement

For the Year Ended December 31, 2016

Variable Costing

Sales (400,000 yards X $2.50) ......................

Variable cost of goods sold

Inventory, January 1 .............................

Variable cost of goods manufactured

$ –0–

$1,000,000

*PROBLEM 22-6B (Continued)

FAB COMPANY

Income Statement

For the Year Ended December 31, 2017

Variable Costing

Sales (500,000 yards X $2.50) ..........................

Variable cost of goods sold

Inventory, January 1 .................................

Variable cost of goods manufactured

$ 75,000

$1,250,000

(b) FAB COMPANY

Income Statement

For the Year Ended December 31, 2016

Absorption Costing

Sales (400,000 yards X $2.50) ........................

Cost of goods sold

Inventory, January 1 ...............................

Cost of goods manufactured .................

$ –0–

775,000

(1)

$1,000,000

*PROBLEM 22-6B (Continued)

FAB COMPANY

Income Statement

For the Year Ended December 31, 2017

Absorption Costing

Sales (500,000 yards X $2.50) ..............

Cost of goods sold

Inventory, January 1 .....................

Cost of goods manufactured ........

Cost of goods available for sale ...

Inventory, December 31 ................

$ 155,000

700,000

855,000

–0–

(1)

$1,250,000

(c) The variable costing and the absorption costing income from opera-

tions can be reconciled as follows:

2016

2017

Variable costing net income

Fixed manufacturing overhead

$100,000

$250,000

(1)In 2016, with absorption costing $320,000

$400,000 X 400,000 units sold

500,000 units manufactured

of

the fixed manufacturing overhead is expensed as part of cost of goods sold, and $80,000

*PROBLEM 22-6B (Continued)

(d) Income parallels sales under variable costing as seen in the increase

in net income in 2017 when 100,000 additional units were sold. In