Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CHAPTER 22

RESPONSIBILITY ACCOUNTING

AND TRANSFER PRICING

Brief Learning

Exercises Topic Objectives Skills

B. Ex. 22.1 Contribution margin effects 22-5 Analysis

B. Ex. 22.2 Contribution margin vs. responsibility margin 22-2, 22-3 Analysis, judgment

B. Ex. 22.3 Responsibility center design 22-1, 22-2 Analysis, judgment

B. Ex. 22.4 Transfer Prices 22-6 Analysis

B. Ex. 22.5 Contribution margin ratios 22-2, 22-3 Analysis

B. Ex. 22.6 Identifying transfer prices 22-6 Analysis

B. Ex. 22.7 Tracing common costs 22-4 Analysis

B. Ex. 22.8 Common or traceable costs 22-1, 22-4 Analysis

B. Ex. 22.9 Responsibility accounting system 22-2 Analysis, judgment

B. Ex. 22.10 Evaluating responsibility center managers 22-4, 22-5 Analysis

Learning

Exercises Topic Objectives Skills

22.1 Accounting terminology

22-1, 22-4,

22-6

Analysis

22.2 Types of responsibility centers 22-1 Analysis, judgment

22.3 Classification of costs in an income statement 22-4 Analysis

22.4 Real World: Home Depot’s segments 22-1, 22-2 Analysis, research

22.5 Preparing a responsibility income statement 22-1–22-5 Analysis

22.6

Evaluation of responsibility centers and center

managers

22-1, 22-2 Analysis, judgment

22.7 Closing an unprofitable business unit

22-1–22-3,

Analysis

22.8 Cost-volume-profit analysis 22-1–22-4 Analysis

22.9 Transfer pricing

22-1, 22-2,

22-6

Analysis, judgment

22.10 Types of responsibility centers 22-1–22-3

Analysis,

communication,

judgment

22.11 Corporate costs; traceable or common 22-2, 22-4 Analysis, judgment

22.12 Transfer prices and responsibility margins

22-3, 22-5,

Analysis

22.13 Transfer price and international taxes 22-6 Analysis

22.14 Responsibility centers in a golf resort 22-1, 22-2 Analysis, judgment

22.15

Real World: Home Depot’s responsibility

centers

22-1–22-3

Analysis,

communication,

research

OVERVIEW OF BRIEF EXERCISES, EXERCISES, PROBLEMS, AND CRITICAL

THINKING CASES

Topic Skills

22.1 A,B

Preparing and using responsibility income

statements

22-3–22-5 Analysis, communication

22.2 A,B

Preparing and using responsibility income

statements

22-3–22-5 Analysis, communication

22.3 A,B

Preparing and using responsibility income

statements

22-3–22-5 Analysis

22.4 A,B

Preparing responsibility income statements

in a Responsibility accounting system

22-3–22-5

Analysis, communication,

judgment

22.5 A,B Analysis of responsibility income statements 22-3–22-5 Analysis

22.6 A,B Evaluating an unprofitable business center 22-3–22-5

Analysis, communication,

judgment

22.7 A,B Transfer pricing decisions 22-1, 22-6

Analysis, communication,

judgment

22.8 A,B Transfer pricing with external market prices 22-1, 22-6

Analysis, communication,

judgment

Critical Thinking Cases

22.1

Allocating fixed costs to responsibility

centers

22-1, 22-2,

22-4

Analysis, communication,

judgment

22.2 An ethical dilemma

22-1, 22-3,

22-6

Analysis, communication,

judgment

22.3 Hospital profit centers

22-1, 22-2,

22-5

Analysis, communication,

judgment

22.4

Real World: General Mills & Kirby

(Internet) Comparing responsibility centers

22-1–22-3

Analysis, communication,

judgment, research,

technology

22. 5

Real World: University of Minnesota

(Ethics, fraud & corporate governance)

22-1, 22-2

Analysis, communication,

judgment

Problems

Learning

Objectives

Sets A, B

DESCRIPTIONS OF PROBLEMS AND CRITICAL THINKING CASES

Problems (Sets A and B)

Chocolatiers Company/Fasteners, Inc. Easy

Students prepare responsibility income statements and determine the

product line in which it would be most advantageous to invest

advertising dollars.

Regal Flair Enterprises/Brown Enterprises Medium

Prepare a responsibility income statement and identify the business units

that will provide the most benefit from short-run product promotion and

from long-run expansion. Requires an understanding of the different

roles of contribution margin and responsibility margin in managerial

decisions.

Giant Chef Equipment Company/Glassware Company Medium

Prepare a responsibility income statement and use the data to perform

cost-volume-profit analysis.

Muscle Bound Company/Freeze, Inc. Strong

Prepare income statements at two successive levels of responsibility.

Also, compute the return on assets for two investment centers and use

data in several managerial decisions.

Butterfield, Inc./Sotheby, Inc. Strong

Given income statements at two levels of responsibility, students are

asked to make several decisions based upon the data and to explain the

“disappearance” of the common costs as the responsibility centers are

redefined. Also calls for a revised version of one responsibility

statement reflecting different sales levels.

Flywiz, Inc./Footware, Inc. Easy

Students are asked to evaluate a decision to close a seemingly

unprofitable unit of a business. However, upon closer examination, they

may discover that seasonality is distorting the data and that products of

the unprofitable unit support sales in the more profitable unit.

Below are brief descriptions of each problem and case. These descriptions are accompanied by the

estimated time (in minutes) required for completion and by a difficulty rating. The time estimates

assume use of the partially filled-in working papers.

22.1 A,B

20

22.4 A,B

60

30

22.3 A,B

30

22.2 A,B

22.6 A,B

15

22.5 A,B

45

Tots-To-Go/Eastrise Corporation Easy

Students are asked to evaluate a transfer price used by two responsibility

centers of a business. The manager of one center wants the transfer price

reduced. Students are to recognize that, regardless of the transfer price

used, the profit of the entire company remains the same. Students must

also consider opportunity costs and the way in which center managers

are evaluated.

Sparta and Associates/Westminster, Inc. Medium

Students investigate market-based transfer prices versus less than market

transfer prices. Students will see the loss in profits to the entire company

when divisions purchase from outside the company rather than

transferring within the company.

22.8 A,B

40

22.7 A,B

20

Critical Thinking Cases

Land’s End Hotel Medium

A conceptual (nonnumerical) case focusing upon the problems that often

arise from efforts to allocate common fixed costs among profit centers. A

practical problem, in that many businesses make such

allocations—perhaps without recognizing the pitfalls.

Osborn Diversified Products, Inc. Medium

A computer error results in the overstatement of a division manager’s

bonus. He needs the money because he has large medical bills and a

daughter in college. The only other person who may be aware of the

problem is another division manager who is angry with the company.

This is a good problem to assign to small groups or teams of students.

Hospital Profit Centers Medium

Students identify cost and profit centers for hospitals. Students consider

the ethical implications of having a type of surgery as a profit center.

General Mills and the Kirby Company Medium

Internet

Students are asked to visit the web pages of two companies and decide

how responsibility centers could be assigned within each. They are also

asked to think of examples of investment centers, profit centers, and cost

centers within each firm. Finally, they are asked what characteristics lead

to the differences in the responsibility center systems.

22.5 University Ethics 20 Medium

Ethics, Fraud & Corporate Governance

Students evaluate the ethical implications when a university views

students as a profit center.

22.2

40

22.1

35

22.4

30

22.3

30

SUGGESTED ANSWERS TO DISCUSSION QUESTIONS

1.

2.

3.

4.

5.

6.

Management makes use of accounting information about individual responsibility centers of the

A cost center is a part of the business that incurs cost but that does not directly generate

revenue. Examples include service departments such as the accounting, janitorial, laundry, or

Three types of transfer prices are market-based, cost-based, and negotiated. Market-based

Unless the costs of operating the service center can be traced directly to one or more of the

In a responsibility accounting system, the recording of revenue and costs should begin with the

Traceable fixed costs are fixed costs that arise because of the existence of a particular business

unit and that would be eliminated if that unit were closed. Common fixed costs are fixed costs

9.

10.

12

8.

The transfer price for a product will divide that product’s profits between different divisions.

This statement is not a logical criterion for closing departments. First, a business unit that has

any responsibility margin is contributing to the common fixed costs and profitability of the

11.

All the elements of responsibility margin—revenue, variable costs, and traceable fixed

costs—will be eliminated if a center is closed. Without considering other issues, this information

Controllable fixed costs and committed fixed costs are subclassifications of fixed costs

traceable to a responsibility center. The controllable fixed costs are those that are readily

Contribution margin is a measurement of performance that takes into consideration only

revenue and variable costs. Therefore, this measurement is useful in evaluating the probable

13.

14.

15.

A profit center is evaluated based upon its ability to generate profits. If cost is used as a transfer

price, the center has no opportunity to earn a profit on the products that it produces and transfers

Managers of responsibility centers are typically held accountable for costs or profits. In a cost

center the manager is held accountable for the costs incurred to meet the obligations of the center.

No. The costs relating to operations of the corporate headquarters cannot be traced to the revenue

of specific restaurants on a basis of cause and effect. With respect to the individual restaurants,

SOLUTIONS TO BRIEF EXERCISES

B. Ex. 22.1

B. Ex. 22.2

B. Ex. 22.3

B. Ex. 22.4

Department B. Short-run product promotion affects revenue and variable costs but

Divisions Two and Three make investment decisions and should be designated as

investment centers. Divisions One, Four, and Five sell their products in external

The contribution margin for the combo is $1.75 - ($0.89 + $0.37 + $0.42) = $0.07.

The small contribution margin for the combo likely implies a negative

The transfer price with an available competitive market should be $48. However, if

there is no external competitive market then a cost-based transfer price might

B. Ex. 22.9

B. Ex. 22.10

Disadvantages of allocating common costs are: 1) Because common fixed costs

do not change when a business center is eliminated, inclusion in the business

The three characteristics are: 1) preparing budgets prior to operations; 2)

SOLUTIONS TO EXERCISES

Ex. 22.1 a.

Ex. 22.2 a.

b.

c.

Ex. 22.3 a.

Traceable fixed costs

An individual video arcade within a chain of video arcades will be

Common fixed costs

A snack bar within one of the company’s arcades will most likely be

A particular game within one of the company’s arcades will most likely

Ex. 22.4

Ex. 22.5

Dollars

Percent of

Sales

Dollars

Percent of

Sales

Dollars

Percent of

Sales

$ 1,200,000 100% $ 900,000 100% $ 300,000 100%

540,000 45% 360,000 40% 180,000 60%

Sales

Variable costs

Contribution

Student responses will differ. Below are some suggested measures:

--Country level investment center measures:

• Capital budgeting (activities/growth in the investment center)

Entire Company

Routers Line

Hepras’ responsibility income statement is shown below:

HEPRAS INCORPORATED

Responsibility Income Statement

For the Current Month

Switches Line

Ethernet

a. 600,000$

180,000

420,000$

Store 1 Store 2

Net decrease expected in total monthly sales

Ex. 22.6

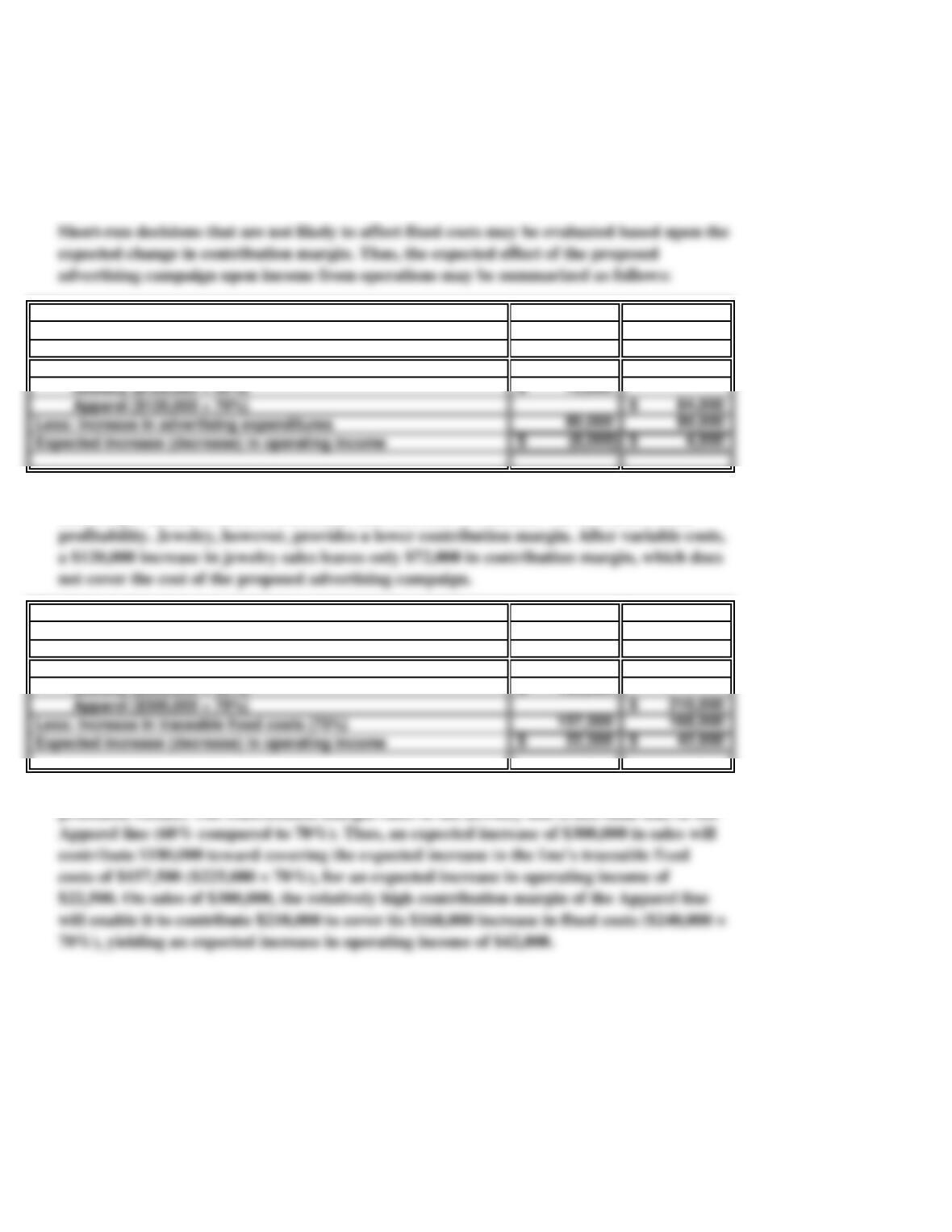

Store 3. The effect of an advertising campaign upon operating income is determined by

comparing the cost of the advertising ($15,000 per month) with the additional contribution

Store 1. The contribution that each store makes toward common costs and toward the

Store 2. The effectiveness of the store manager’s strategies are best evaluated by looking at the

relationship of revenue to expenses under the manager’s direct control. This relationship is

Ex. 22.7

Decrease in monthly sales from closing Store 3

Less: Increases in sales expected at Stores 1 and 2

($60,000 + $120,000)

Ex. 22.8

11,400$

11,100

13,500

Ex. 22.9

Ex. 22.10 (1)

Strategy 1: Advertise the name Drexel-Hall:

Expected increase (decrease) in monthly contribution margin:

Store 1: ($228,000 × 5% increase)

Store 2: ($222,000 × 5% increase)

The higher each division’s responsibility margin, the higher each division’s

profitability will be. Thus, since the managers are paid a bonus based on the

Profit center

Store 3: ($270,000 × 5% increase)

Strategy 2: Advertise low prices at Store 2:

Expected increase (decrease) in contribution margin:

Responsibility centers assist managers in evaluating the overall performance of

subunits of a business, and also help in creating future budgets and setting future

Sales Repairs

Department Department

180,000$ 24,000$

94,000 8,000

a.

Entire UK Mexican

Company Division Division

Sales

1,600,000£ 1,600,000£ 700,000£

Operating Expense

650,000 400,000 250,000

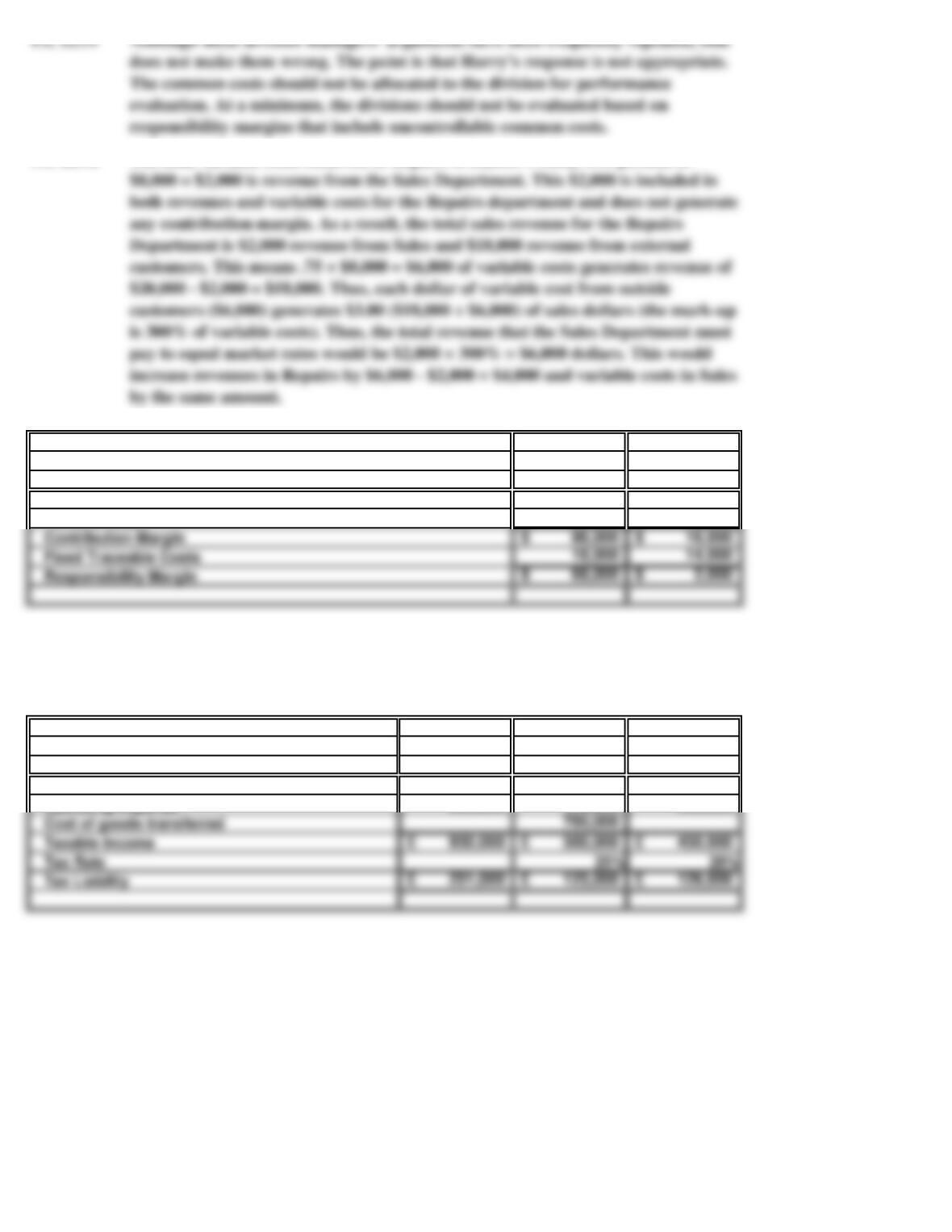

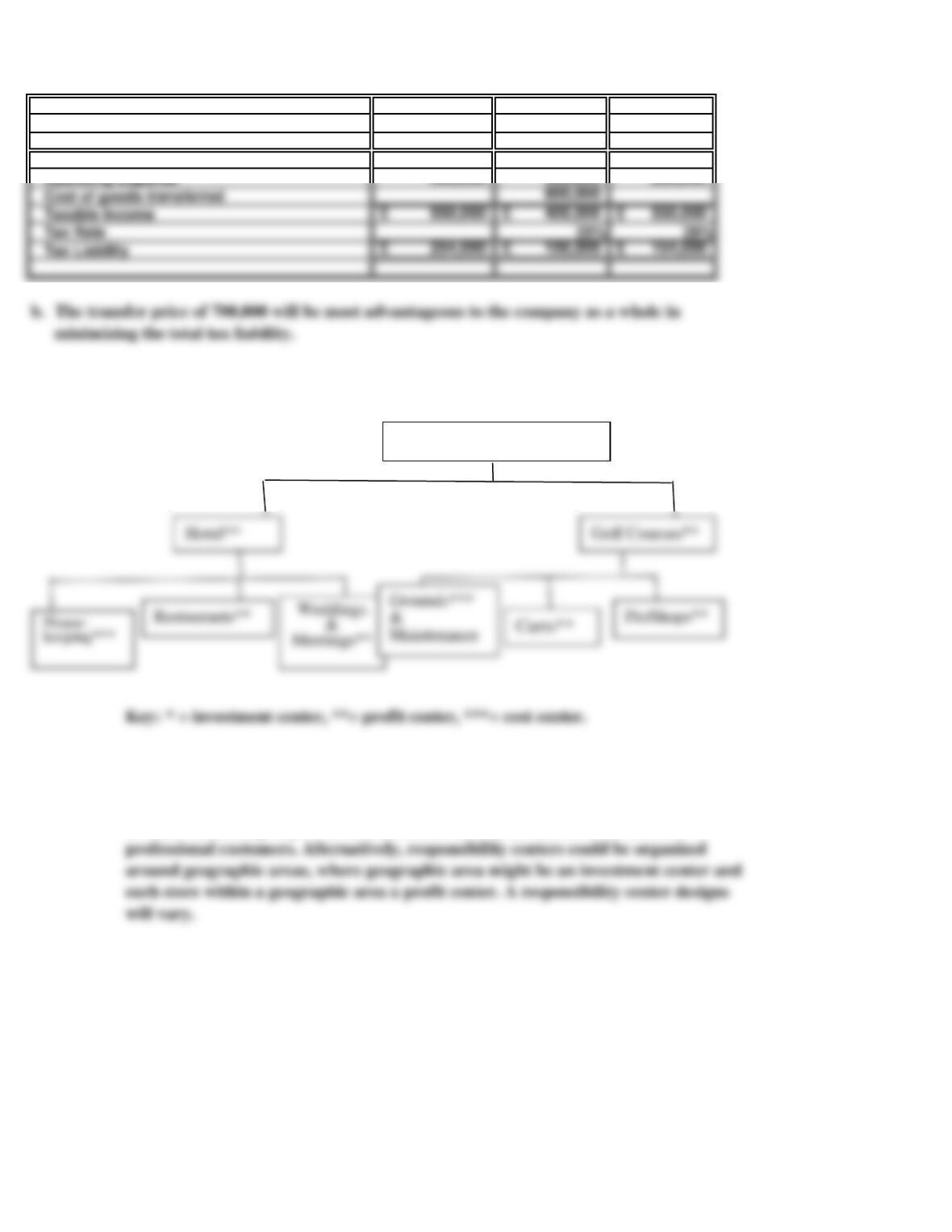

Using a transfer price of 700,000 British pounds, the tax liability for each division and for the

company as a whole are:

Ex. 22.13

The total variable costs incurred in Repairs is $8,000. Twenty-five percent of

Ex. 22.12

Variable Costs

Sales

Entire UK Mexican

Company Division Division

Sales 1,600,000£ 1,600,000£ 800,000£

Ex. 22.14

Ex. 22.15

Ex. 22.13 (continued): Using a transfer price of 800,000 British pounds, the tax liability for

each division and for the company as a whole are:

Student responses will vary, but here is one organizational design:

Home Depot’s Note 1 in Appendix A outlines a couple of different scenarios for

responsibility center organization. First, responsibility centers could be organized

around customer groups. The note mentions do-it-yourself, do-it-for me, and

Jasper Golf Resort*

SOLUTIONS TO PROBLEMS SET A

20 Minutes, Easy PROBLEM 22.1A

CHOCOLATIERS COMPANY

a. CHOCOLATIERS COMPANY

Responsibility Income Statement

For the Current Month

Entire Company Solid Chocolate Powdered Chocolate

Dollars Percent Dollars Percent Dollars Percent

Sales

1,500,000$ 100% 600,000$ 100% 900,000$ 100%

Variable costs 780,000 52% 240,000 40% 540,000 60%

b.

c.

According to the analysis in part a, the Powdered Chocolate product line is more profitable in terms

of dollars of responsibility margin that it contributes to the entire company.

When determining the profitability of any product line, common fixed costs should not be considered.

Due to the short term nature of such an advertising campaign, fixed production costs will most likely

30 Minutes, Medium PROBLEM 22.2A

REGAL FLAIR ENTERPRISES

a. Responsibility income statement:

Entire Company Jewelry Line Apparel Line

Dollars Percent Dollars Percent Dollars Percent

Sales

1,300,000$ 100% 900,000$ 100% 400,000$ 100%

Variable costs 480,000 37% 360,000 40% 120,000 30%

For the Current Month

Responsibility Income Statement

REGAL FLAIR ENTERPRISES

PROBLEM 22.2A

REGAL FLAIR ENTERPRISES (concluded)

b.

Jewelry Apparel

Expected increase in contribution margin:

c. Results of investment in each product line:

Jewelry Apparel

Expected increase in contribution margin:

Jewelry ($300,000 × 60%) 180,000$

Because of the relatively high contribution margin in the apparel segment, spending

$80,000 per month to achieve a monthly sales increase of $120,000 will increase overall

Thus, it would appear that an investment in the Apparel line would produce the most

Recommendations on increased advertising:

It appears that increasing advertising expenditures on apparel will increase the

profitability of the business, but spending the proposed amount to advertise jewelry would

reduce profitability.

30 Minutes, Medium PROBLEM 22.3A

GIANT CHEF EQUIPMENT COMPANY

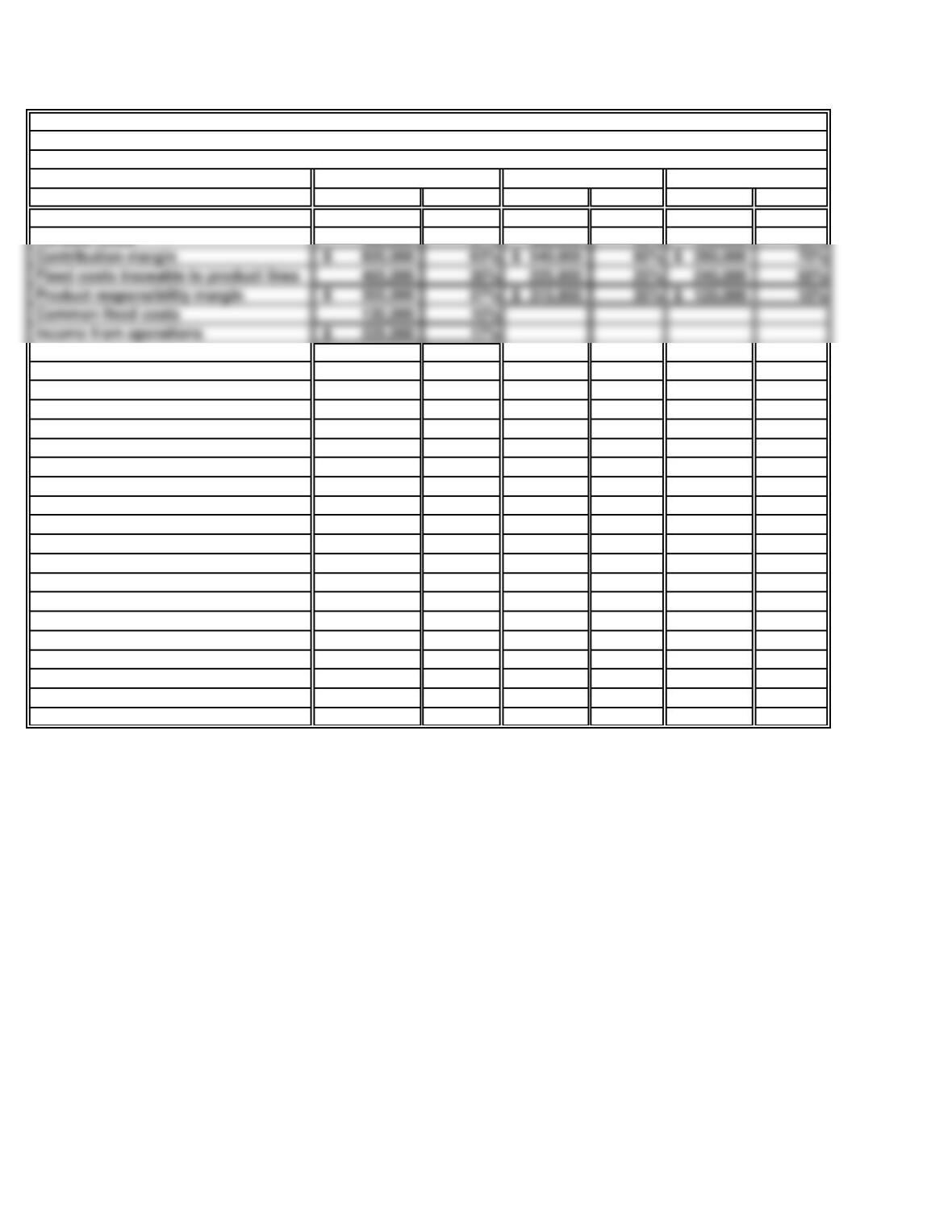

a. Responsibility income statement

Entire Company Commercial Sales Division Home Products Division

Dollars Percent Dollars Percent Dollars Percent

Sales

2,400,000$ 100.0 1,500,000$ 100.0 900,000$ 100.0

Variable costs 1,440,000 60.0 990,000 66.0 450,000 50.0

Contribution margin 960,000$ 40.0 510,000$ 34.0 450,000$ 50.0

GIANT CHEF EQUIPMENT COMPANY

Responsibility Income Statement

For June