1. The three major objectives of budgeting are (1) to establish specific goals for future

operations, (2) to execute plans to achieve the goals, and (3) to periodically compare

actual results with the goals.

2. If goals set by the budgets are viewed as unrealistic or unachievable, employees and

managers may become discouraged and may not be committed to the achievement of the

goals, resulting in the budget becoming less effective as a planning and control tool.

3. A budget that is set too loosely may fail to motivate managers and other employees to perform

efficiently. In addition, a loose budget may cause a “spend it or lose it” mentality, where excess

b

udget resources are spent in order to protect the budget from future reductions.

4. Conflicting goals can cause employees or department managers to act in their own self-

interests to the detriment of the organization’s objectives.

5. A static budget is most appropriate in situations where costs are not variable to an underlying

activity level. As a result, it is reasonable to plan spending on the basis of a fixed quantity of

resources for the year. This will occur in some administrative functions, such as human

resources, accounting, or public relations.

6. Computers not only speed up the budgeting process, but they also reduce the cost of budget

p

reparation when large quantities of data need to be processed. In addition, by using

computerized simulation models, management can determine the impact of various operating

alternatives on the master budget.

7. The production requirements must be carefully coordinated with the sales budget to ensure

that production and sales are kept in balance during the period. Ideally, manufacturing

operations should be maintained at 100% of capacity, with no idle time or overtime, and

there should be neither excessive inventories nor inventories insufficient to fill sales orders.

8. Purchases of direct materials should be closely coordinated with the production budget so

that inventory levels can be maintained within reasonable limits.

9. a. The cash budget contributes to effective cash planning. This involves advance planning

so that a cash shortage does not arise and excess cash is not permitted to remain “idle.”

b. The excess cash can be invested in readily marketable income-producing securities or

used to reduce loans.

10. The plans for financing the capital expenditures budget may affect the cash budget.

CHAPTER 22

BUDGETING

DISCUSSION QUESTIONS

22-1

CHAPTER 22 Budgeting

PE 21–1A

Variable cost:

Direct labor (7,500 hours × $16.00* per hour)…………………………………

…

$120,000

Fixed cost:

PE 21–1B

Variable cost:

Direct labor (600 hours × $14.50* per hour)……………………………………

…

$ 8,700

Fixed cost:

PE 22–2A

Expected units to be sold 240,000

PE 22–2B

Expected units to be sold 75,000

Plus desired ending inventory, December 31, 2016 2,700

MyLife Chronicles Inc.

Production Budget

For the Year Ending December 31, 2016

Magnolia Candle Inc.

Production Budget

For the Year Ending December 31, 2016

22-2

CHAPTER 22 Budgeting

PE 22–3A

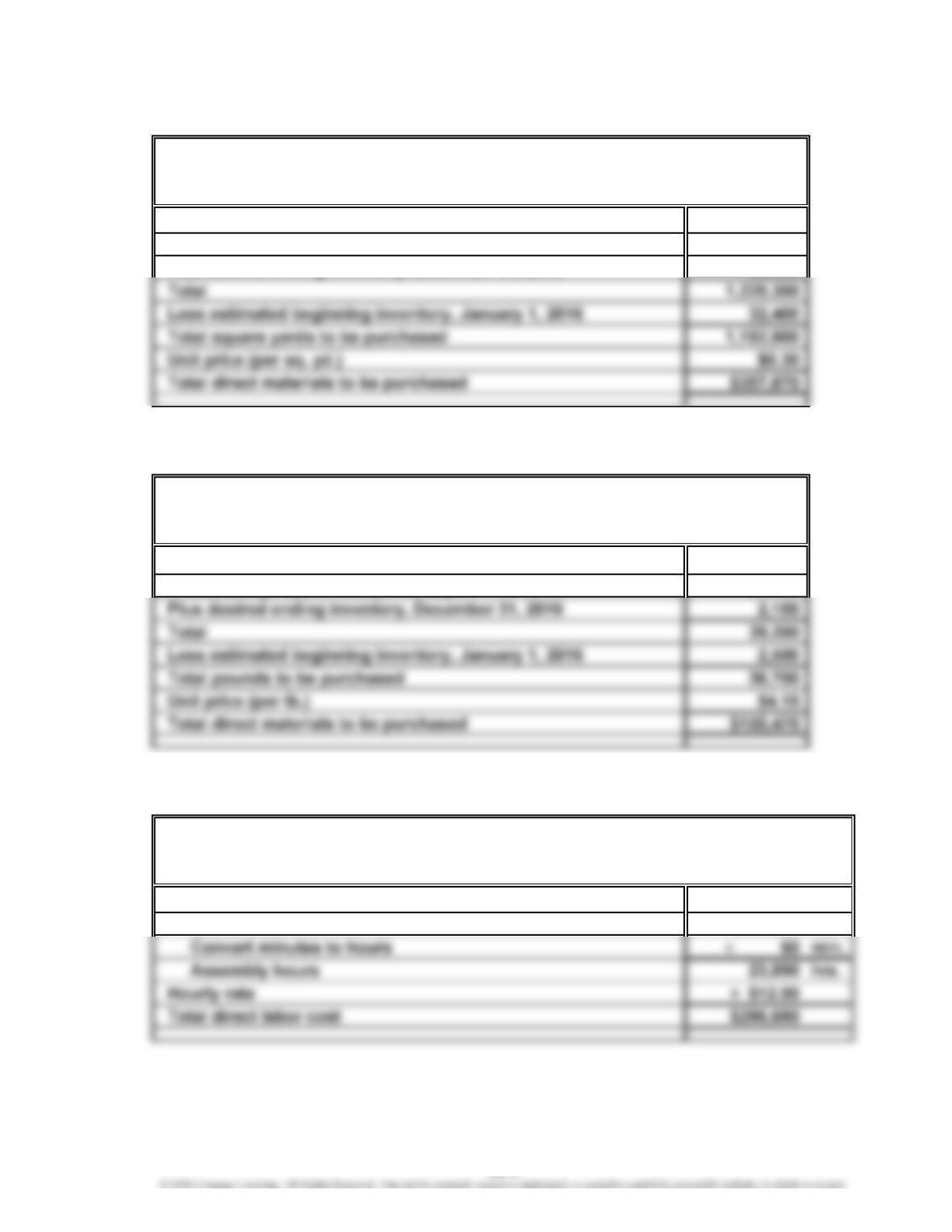

Square yards required for production:

Diaries (238,900 × 5 sq. yd.) 1,194,500

Plus desired ending inventory, December 31, 2016 30,800

PE 22–3B

Pounds of wax required for production:

Candles [(74,200 × 8 oz.) ÷ 16 oz.] 37,100

PE 22–4A

Hours required for assembly:

Diaries (238,900 × 6 min.) 1,433,400 min.

MyLife Chronicles Inc.

Direct Materials Purchases Budget

For the Year Ending December 31, 2016

Magnolia Candle Inc.

Direct Materials Purchases Budget

For the Year Ending December 31, 2016

MyLife Chronicles Inc.

Direct Labor Cost Budget

For the Year Ending December 31, 2016

22-3

CHAPTER 22 Budgeting

PE 22–4B

PE 22–5A

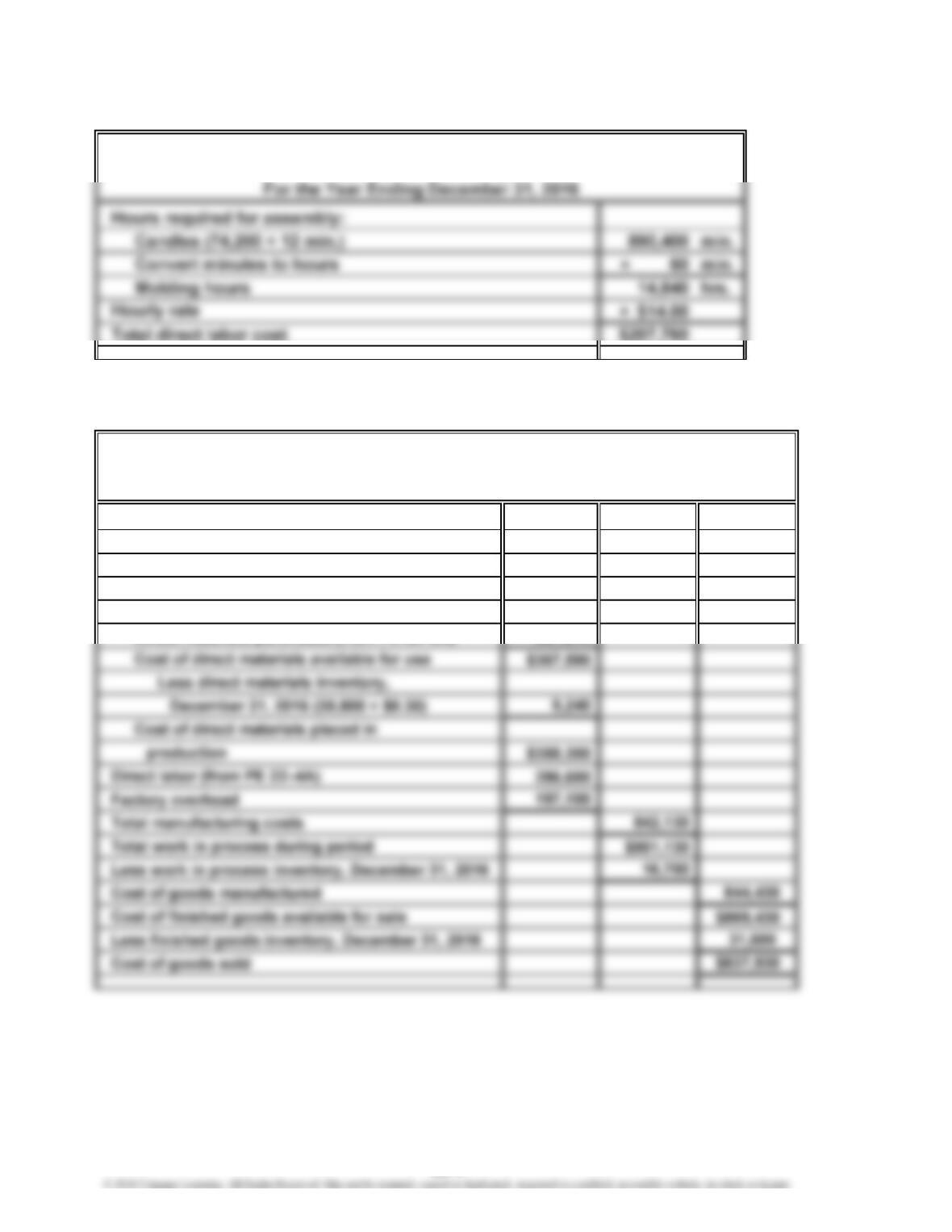

Finished goods inventory, January 1, 2016

Work in process inventory, January 1, 2016 $ 19,000

Direct materials:

Direct materials inventory, January 1, 2016

(32,400 × $0.30) $ 9,720

Direct materials purchases (from PE 22–3A) 357,870

Magnolia Candle Inc.

Direct Labor Cost Budget

MyLife Chronicles Inc.

Cost of Goods Sold Budget

For the Year Ending December 31, 2016

$ 25,000

22-4

PE 22–5B

Finished goods inventory, January 1, 2016 $ 9,800

Work in process inventory, January 1, 2016 $ 3,600

Direct materials:

Direct materials inventory, January 1, 2016

(2,500 × $4.10) $ 10,250

Direct materials purchases (from PE 22–3B) 150,470

Cost of direct materials available for use $160,720

PE 22–6A

July

Collections from June sales (70% × $170,000)……………………………………

…

$119,000

PE 22–6B

April

Payments for March purchases (90% × $11,900)…………………………………

…

$10,710

Magnolia Candle Inc.

Cost of Goods Sold Budget

For the Year Ending December 31, 2016

22-5

CHAPTER 22 Budgeting

Ex. 22–1

a.

September October November December

Estimated cash receipts from:

Part-time job $ 1,400 $1,400 $1,400 $1,400

Deposit 500

Rent 600 600 600 600

Food 235 235 235 235

Deposit 500

Total cash payments $ 5,520 $1,110 $1,110 $1,110

c. While Malloy’s budget might first appear satisfactory, Malloy must earn

enough cash in order to pay for the spring semester tuition. Her present budget

shows that she will be $700 short of the tuition amount ($3,700 – $3,000) by the

time she needs to pay her spring tuition. Thus, Malloy will likely need to

adjust the plan before the fall term even begins. Some possibilities would be to

rent a lower cost apartment or to get a roommate. Other considerations include

For the Four Months Ending December 31, 2016

KATHERINE MALLOY

Cash Budget

EXERCISES

22-6

CHAPTER 22 Budgeting

Ex. 22–2

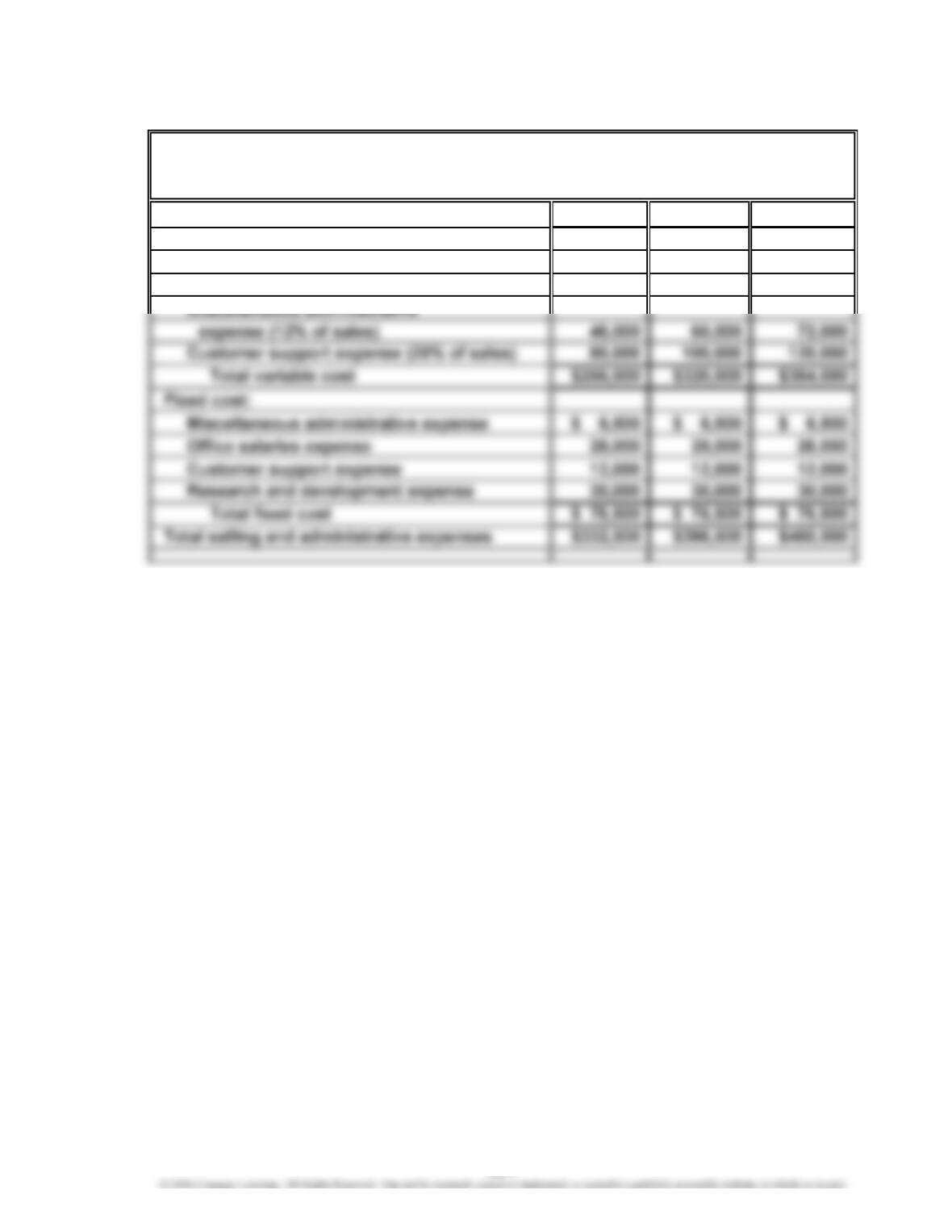

Total sales $400,000 $500,000 $600,000

Variable cost:

Sales commissions (14% of sales) $ 56,000 $ 70,000 $ 84,000

Advertising expense (18% of sales) 72,000 90,000 108,000

CLOUD PRODUCTIVITY INC.

Flexible Selling and Administrative Expenses Budget

For the Month Ending March 31, 2016

22-7

CHAPTER 22 Budgeting

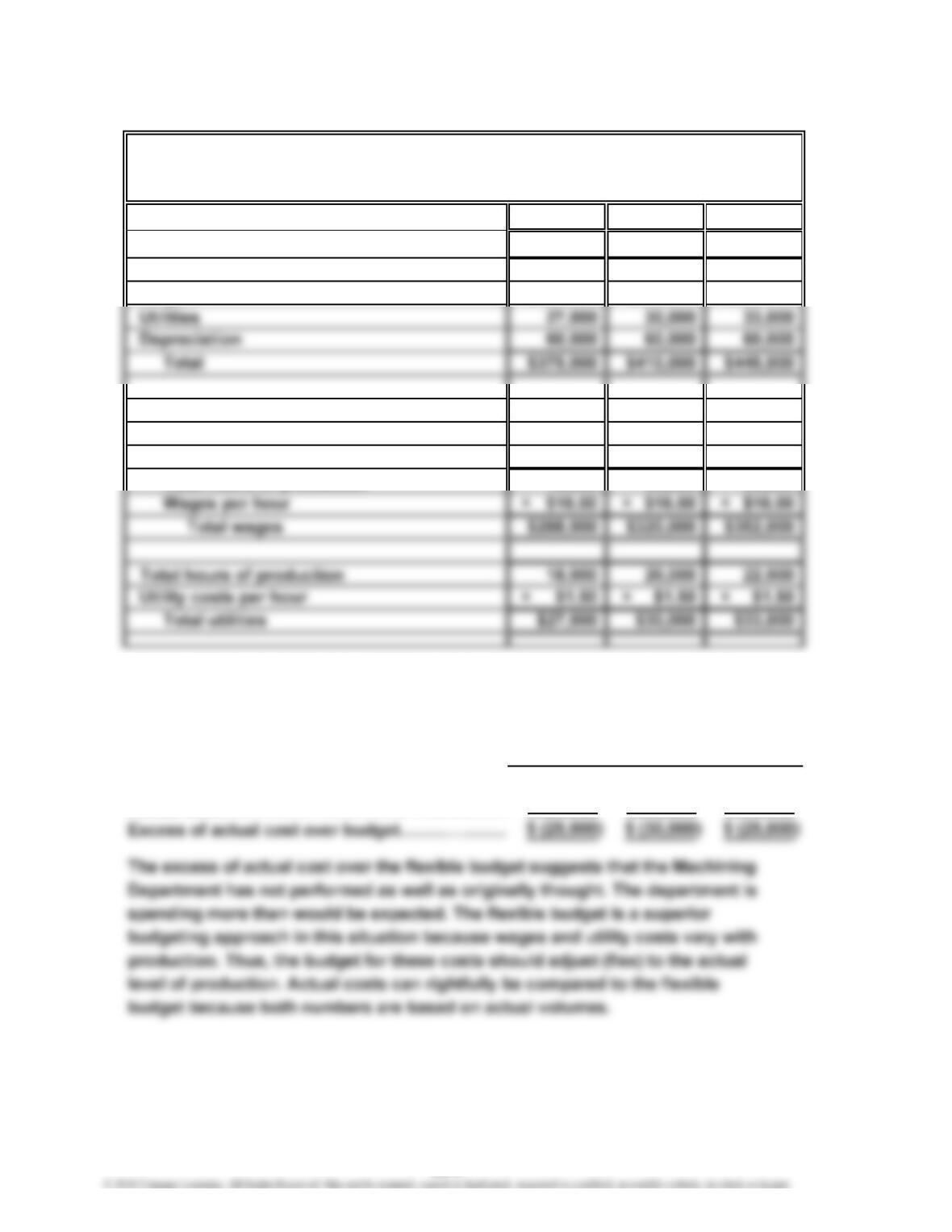

Ex. 22–3

a.

January February March

Units of production 90,000 100,000 110,000

Wages $288,000 $320,000 $352,000

Supporting calculations:

Units of production 90,000 100,000 110,000

Hours per unit 0.20 0.20 0.20

Total hours of production 18,000 20,000 22,000

Depreciation is a fixed cost, so it does not “flex” with changes in production.

Because it is the only fixed cost, the variable and fixed costs are not classified in

the budget.

b.

January February March

Total flexible budget………………………………

…

$375,000 $410,000 $445,000

Actual cost……………………………………………

…

400,000 440,000 470,000

RODRIGUEZ COMPANY—MACHINING DEPARTMENT

Flexible Production Budget

For the Three Months Ending March 31, 2016

×××

22-8

CHAPTER 22 Budgeting

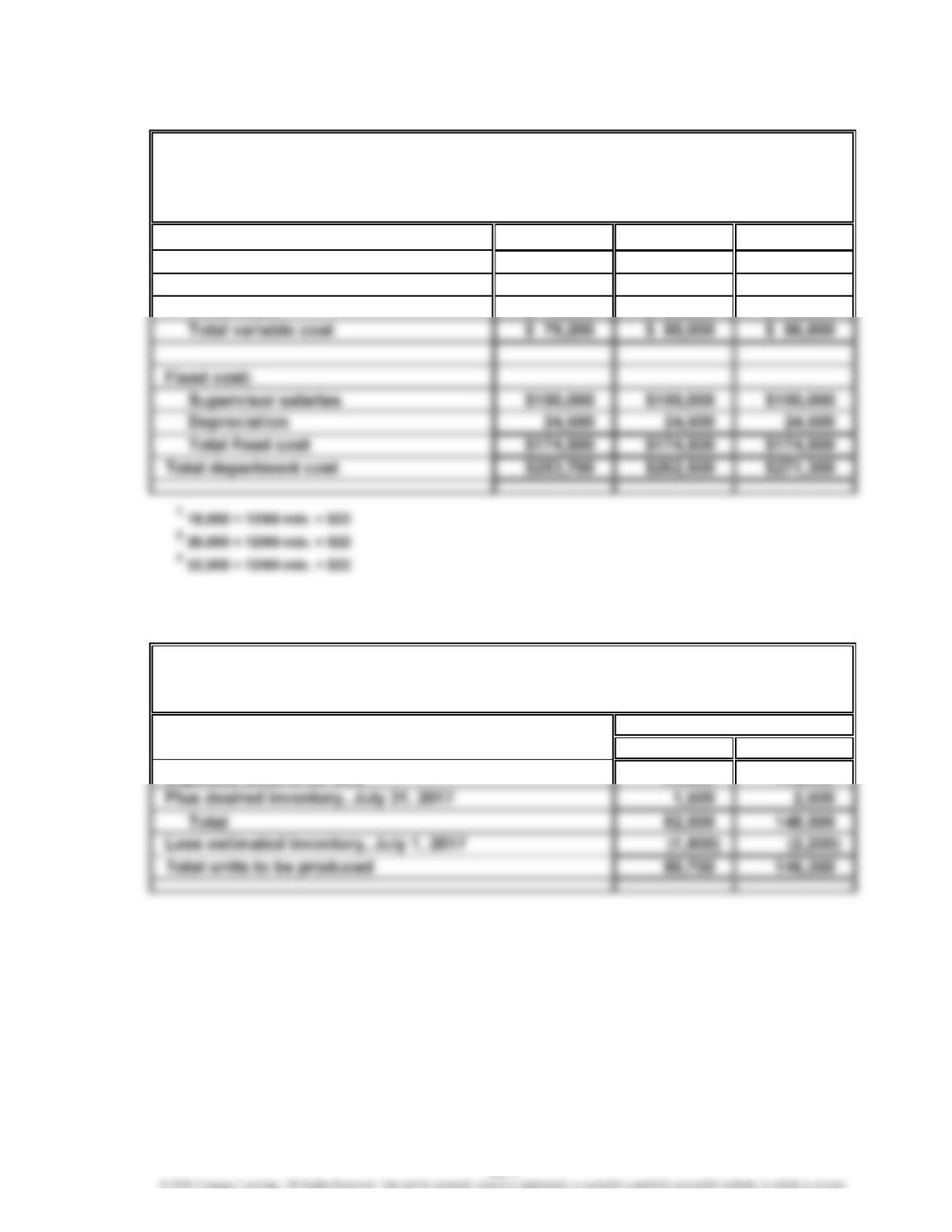

Ex. 22–4

Units of production 18,000 20,000 22,000

Variable cost:

Direct labor $ 79,200 $ 88,000 $ 96,800

Ex. 22–5

Small Scale Large Scale

Expected units to be sold 81,000 146,000

For the Month Ending July 31, 2017

Units

STEELCASE INC.—ASSEMBLY DEPARTMENT

Flexible Production Budget

(assumed data)

August 2016

TRUE TAB INC.

Production Budget

123

22-9

CHAPTER 22 Budgeting

Ex. 22–6

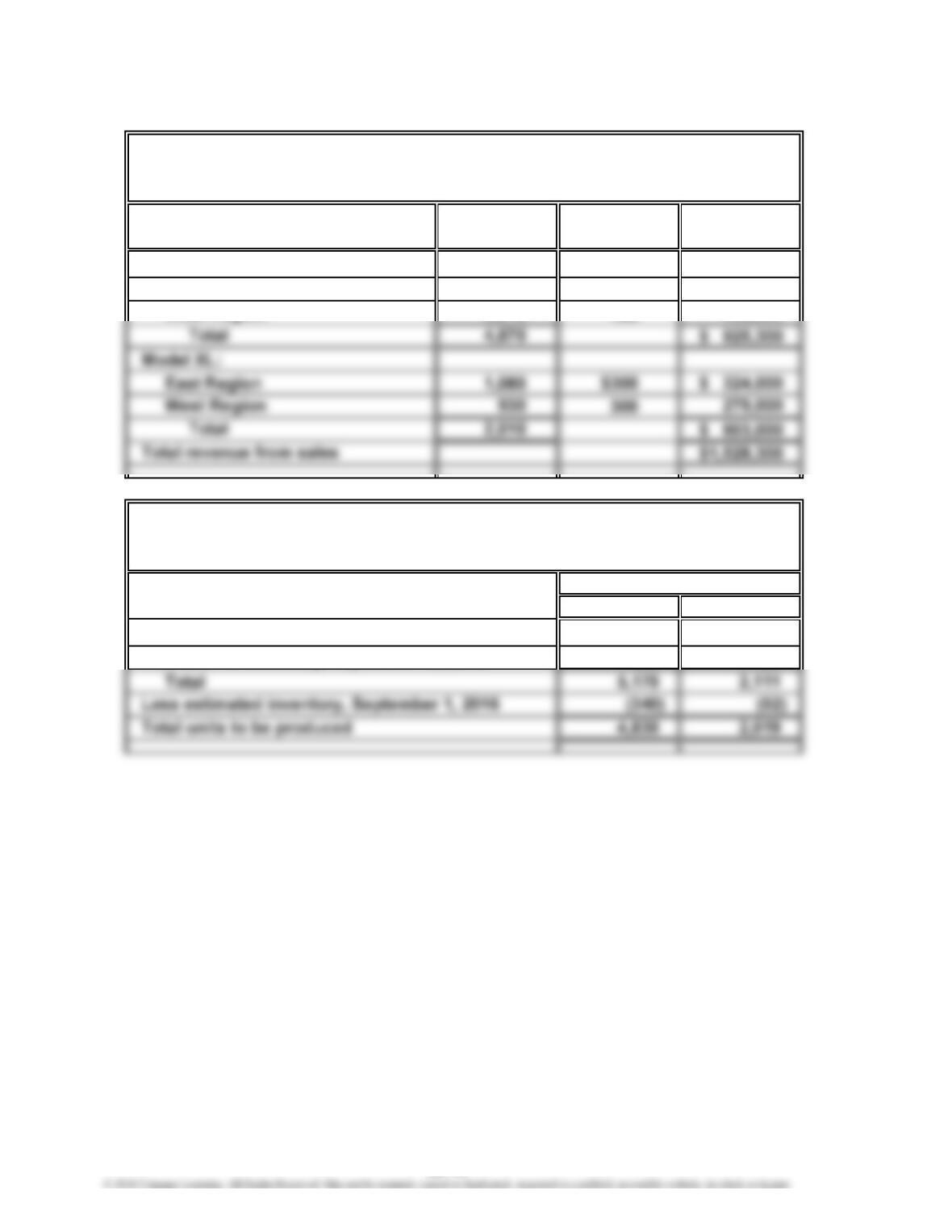

a.

Unit Sales Unit Selling

Volume Price Total Sales

Model DL:

East Region 2,560 $190 $ 486,400

West Region 2,310 190 438,900

b.

Model DL Model XL

Expected units to be sold 4,870 2,010

Plus desired inventory, September 30, 2016 300 101

For the Month Ending September 30, 2016

Units

Product and Area

SOUNDLAB INC.

Sales Budget

For the Month Ending September 30, 2016

SOUNDLAB INC.

Production Budget

22-10

CHAPTER 22 Budgeting

Ex. 22–7

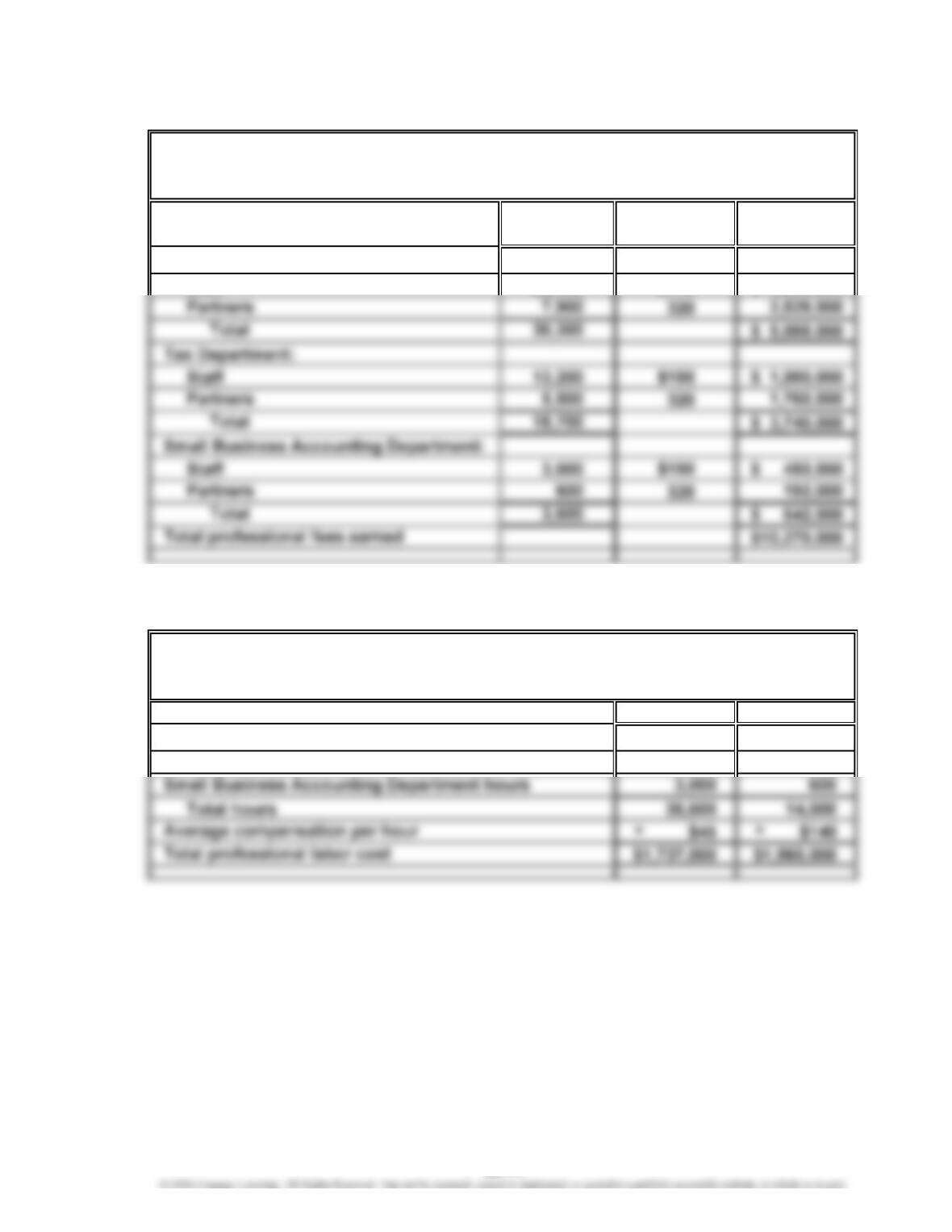

Billable Hourly Total

Hours Rate Revenue

Audit Department:

Staff 22,400 $150 $ 3,360,000

Ex. 22–8

Staff Partners

Audit Department hours 22,400 7,900

Tax Department hours 13,200 5,500

Professional Labor Cost Budget

For the Year Ending December 31, 2016

ROLLINS AND COHEN, CPAs

Professional Fees Earned Budget

For the Year Ending December 31, 2016

ROLLINS AND COHEN, CPAs

22-11

CHAPTER 22 Budgeting

Ex. 22–9

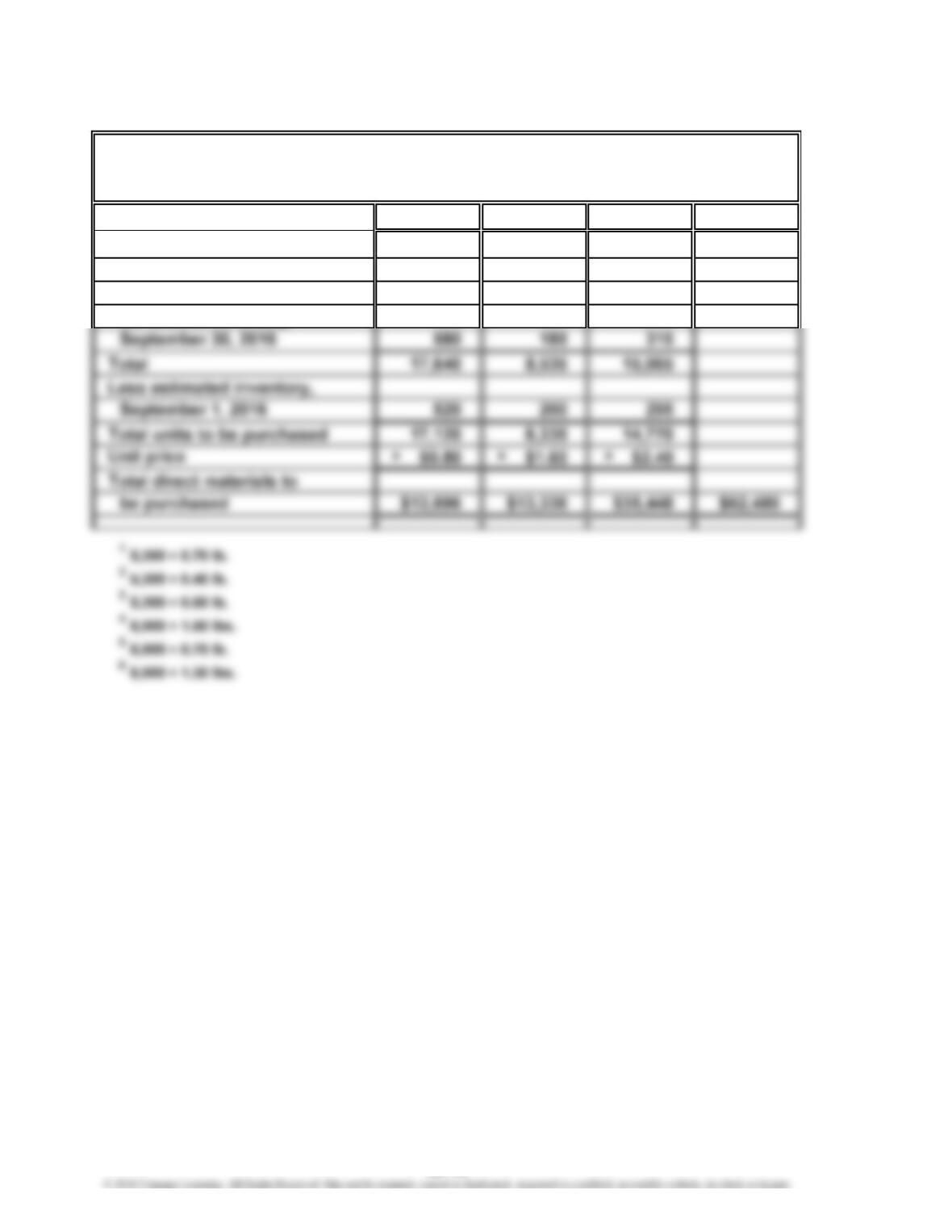

Dough Tomato Cheese Total

Units required for production:

12″ pizza 3,710 2,120 3,180

16″ pizza 13,350 6,230 11,570

Plus desired inventory,

ROMANO’S FROZEN PIZZA INC.

Direct Materials Purchases Budget

For the Month Ending September 30, 2016

12

45

3

6

22-12

CHAPTER 22 Budgeting

Ex. 22–10

Materials required for production:

Coke® 459 lbs. 153,000 btls. 306,000 ltrs.

COCA-COLA ENTERPRISES—WAKEFIELD PLANT

For the Month Ending May 31, 2016

(assumed data)

Direct Materials Purchases Budget

2-Liter Carbonated

Concentrate Bottles Water

*

22-13

CHAPTER 22 Budgeting

Ex. 22–11

Total

Pounds required for production:

Passenger tires 1,470,000 lbs. 210,000 lbs.

Truck tires 1,482,000 152,000

Plus desired inventory,

December 31, 2016 40,000 10,000

Steel belts: 19,000 units × 8 lbs. per unit = 152,000 lbs.

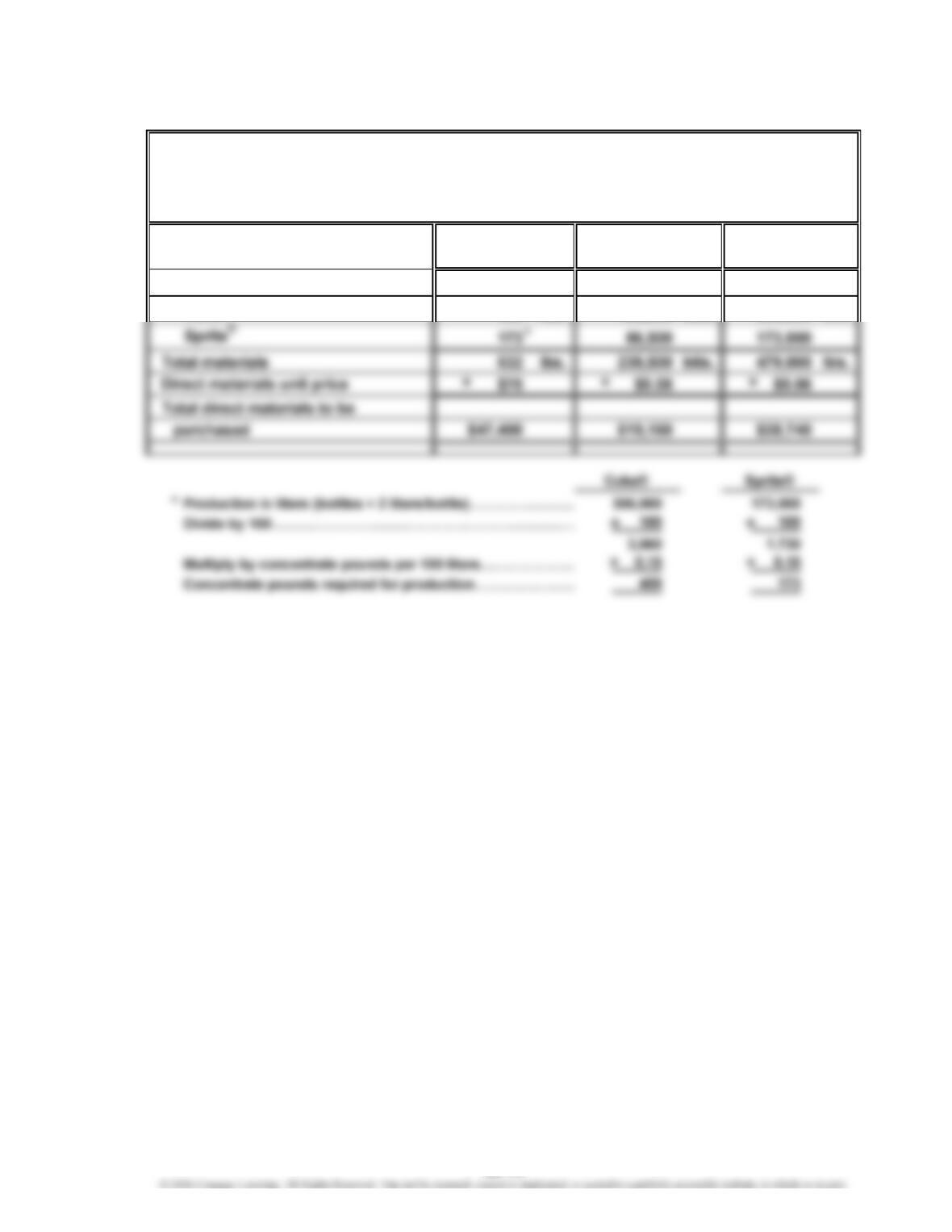

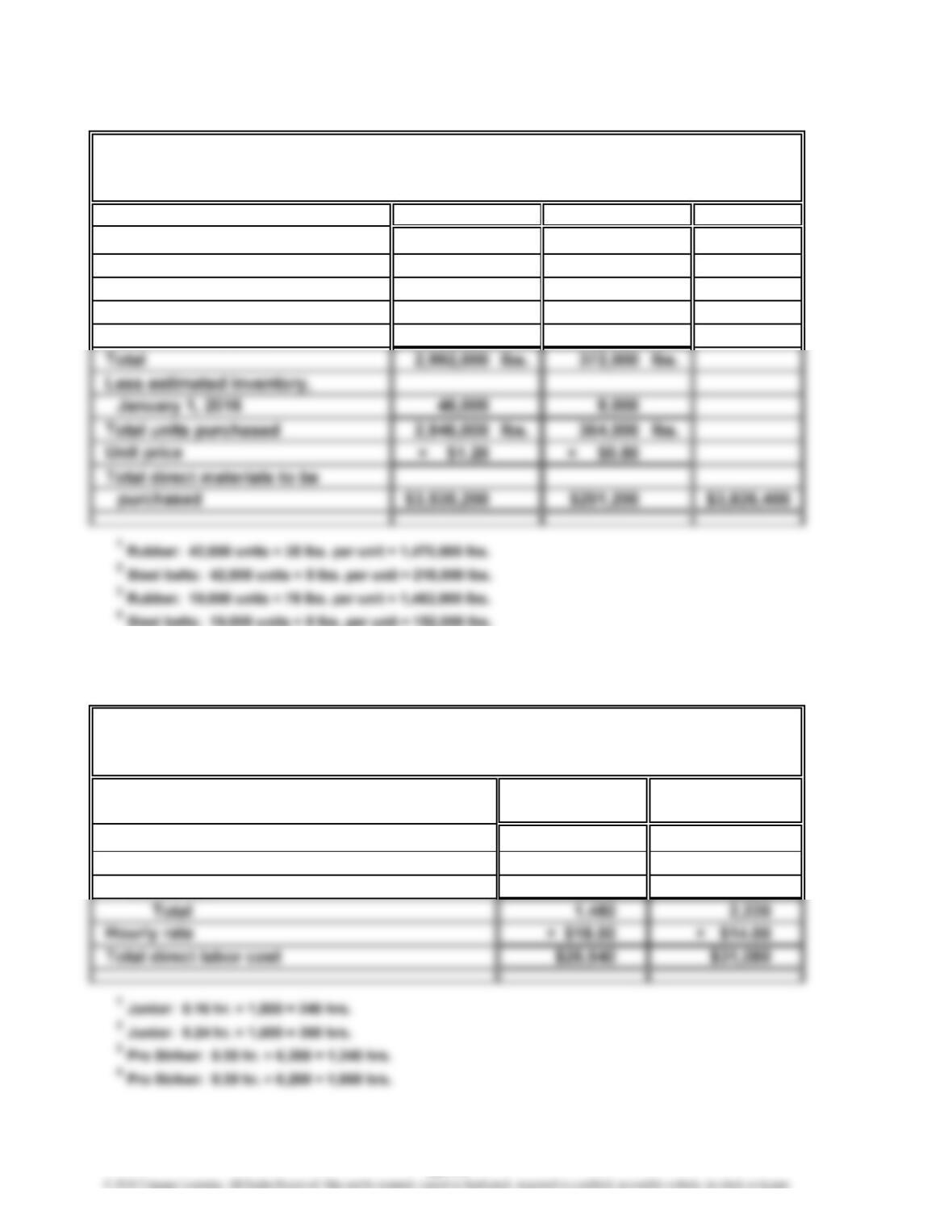

Ex. 22–12

Hours required for production:

Junior

Pro Striker

SAFETY GRIP COMPANY

Direct Materials Purchases Budget

For the Year Ending December 31, 2016

Rubber Steel Belts

240

1,240

360

1,860

Direct Labor Cost Budget

For the Month Ending July 31, 2016

ACE RACKET COMPANY

Department

Forming Assembly

Department

12

34

12

34

22-14

CHAPTER 22 Budgeting

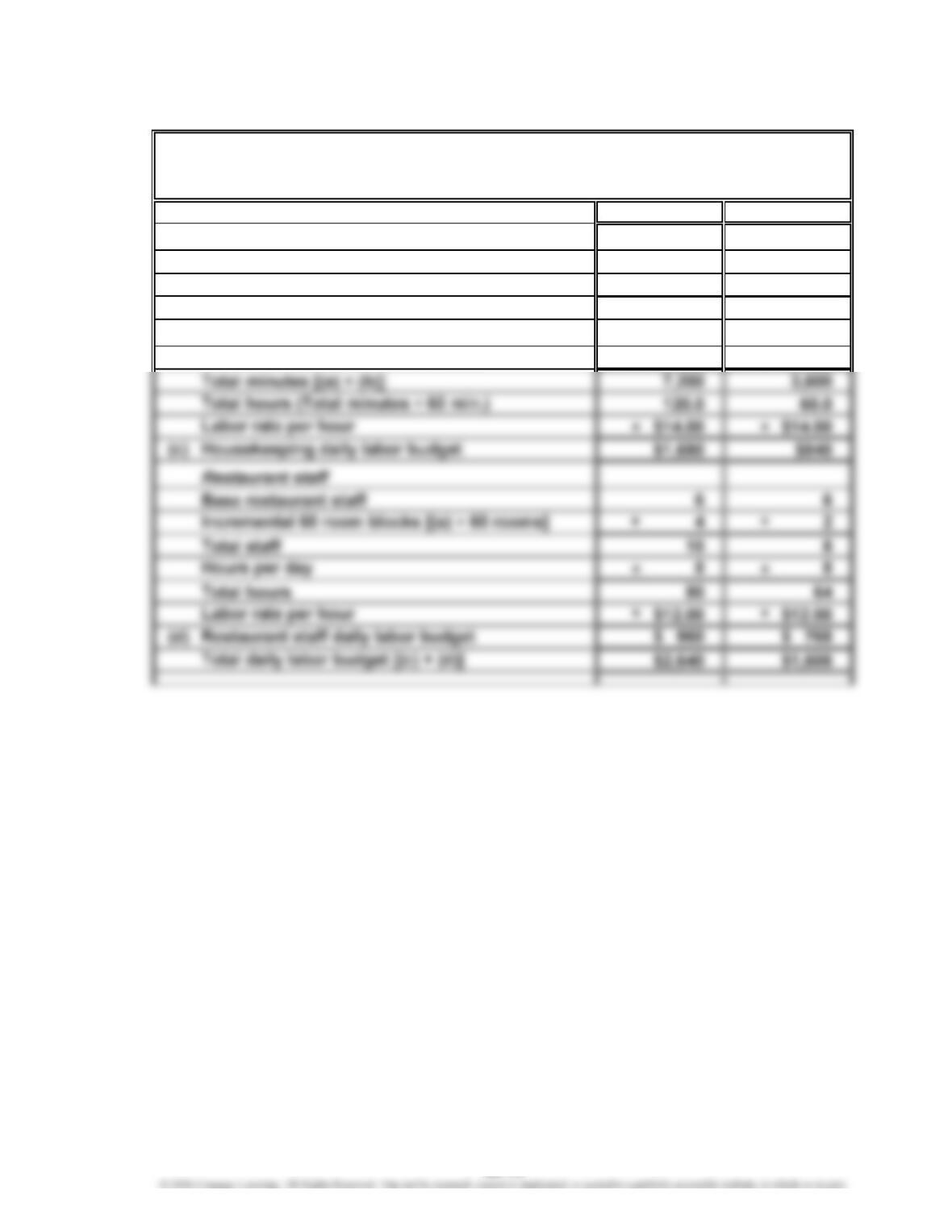

Ex. 22–13

Weekday Weekend Day

Room occupancy

Room capacity 300 300

Occupied percent (occupancy) 80% 40%

(a) Rooms occupied 240 120

Housekeeping

(b) Number of minutes to clean a room 30 30

AMBASSADOR SUITES INC.

Direct Labor Cost Budget

For a Weekday or a Weekend Day

××

××

22-15

CHAPTER 22 Budgeting

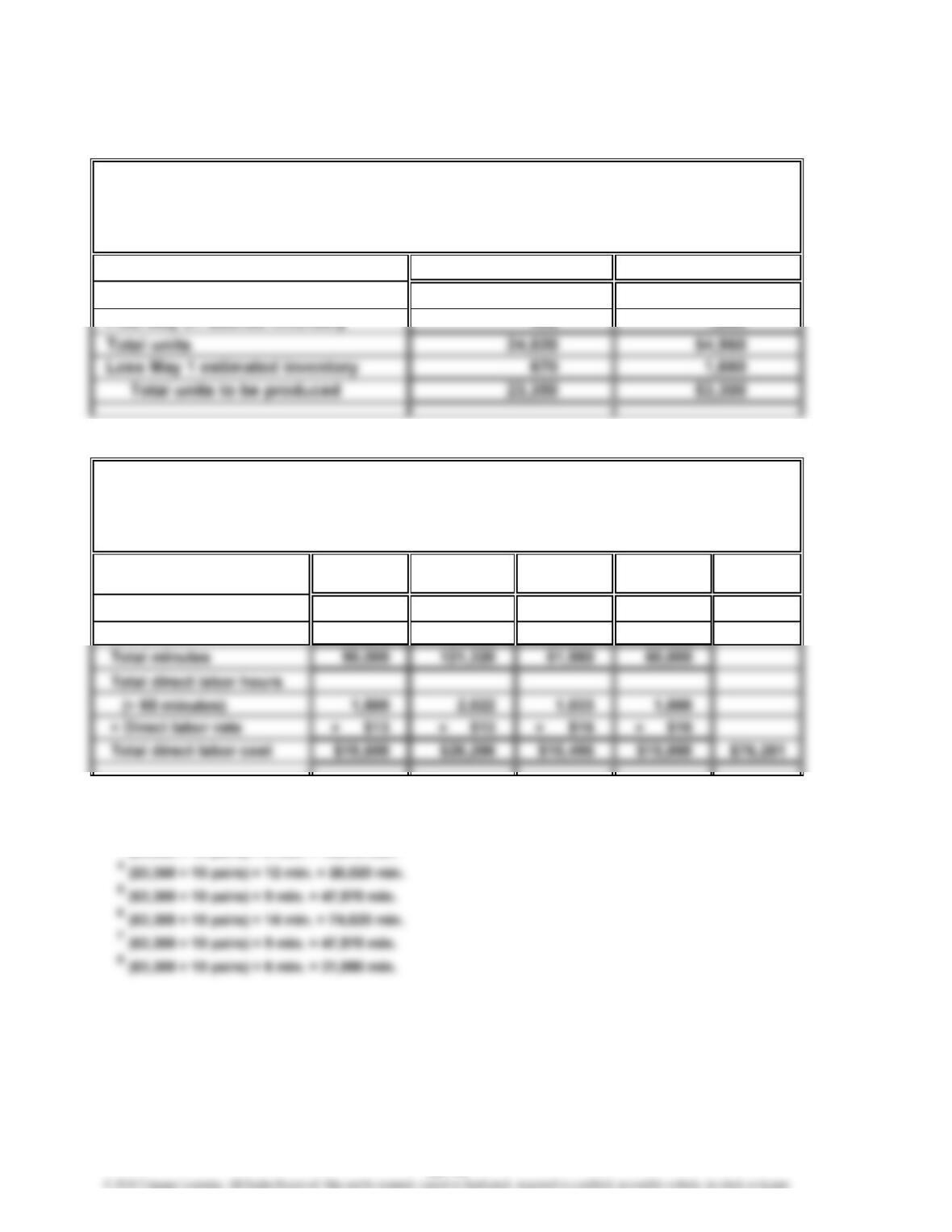

Ex. 22–14

a.

Expected units to be sold

Plus May 31 desired inventory

b.

Outer-

Inseam seam Pockets Zipper Total

Dockers® 42,030 46,700 14,010 28,020

501 Jeans® 47,970 74,620 47,970 31,980

1

(23,350 ÷ 10 pairs) × 18 min. = 42,030 min.

2

(23,350 ÷ 10 pairs) × 20 min. = 46,700 min.

3

(23,350 ÷ 10 pairs) × 6 min. = 14,010 min.

LEVI STRAUSS & CO.

Production Budget

(assumed data)

May 2016

LEVI STRAUSS & CO.

Direct Labor Cost Budget

501 Jeans®

53,100

Dockers®

23,600

420

(assumed data)

May 2016

1,860

1234

5678

22-16

CHAPTER 22 Budgeting

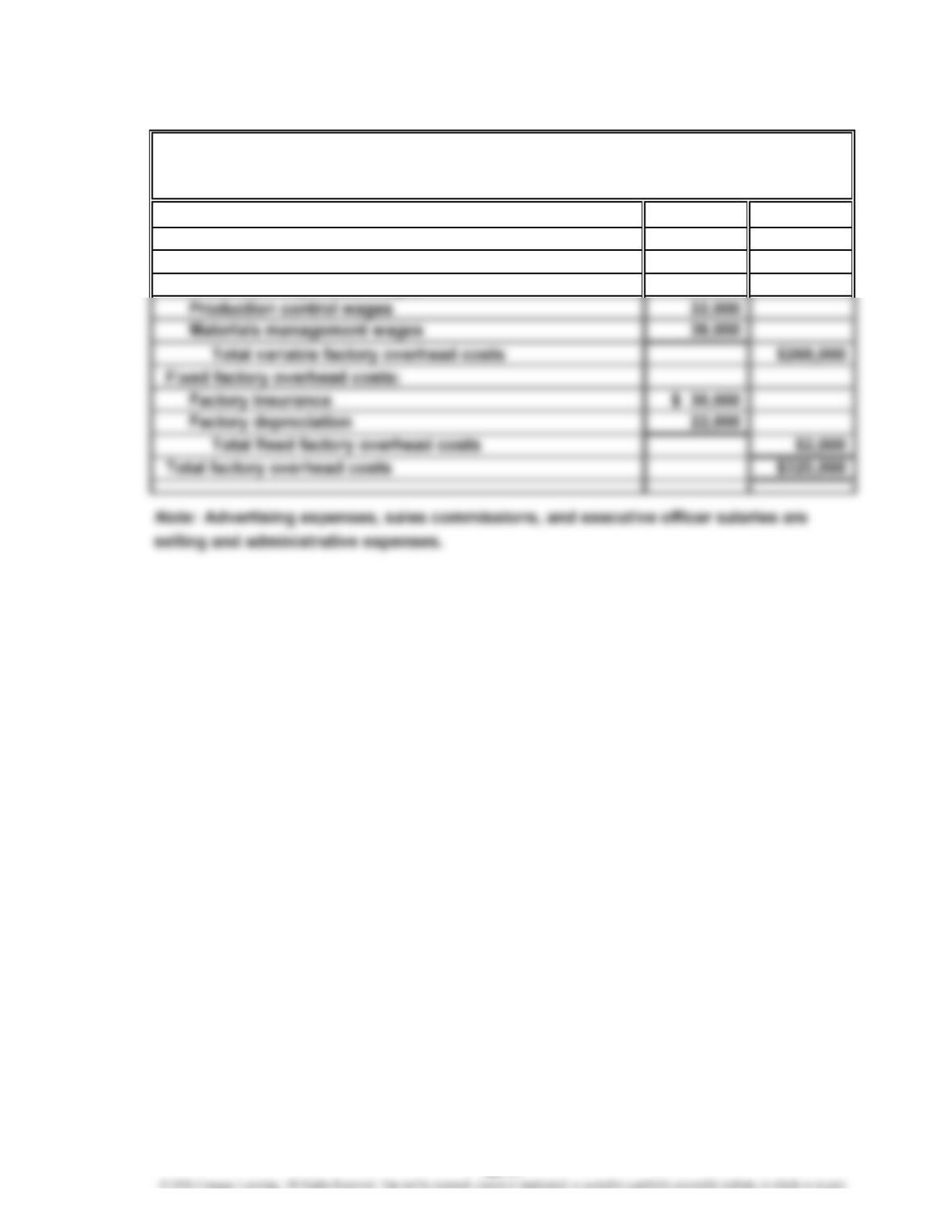

Ex. 22–15

Variable factory overhead costs:

Manufacturing supplies $ 14,000

Power and light 48,000

Production supervisor wages 135,000

SWEET TOOTH CANDY COMPANY

Factory Overhead Cost Budget

For the Month Ending August 31, 2016

22-17

CHAPTER 22 Budgeting

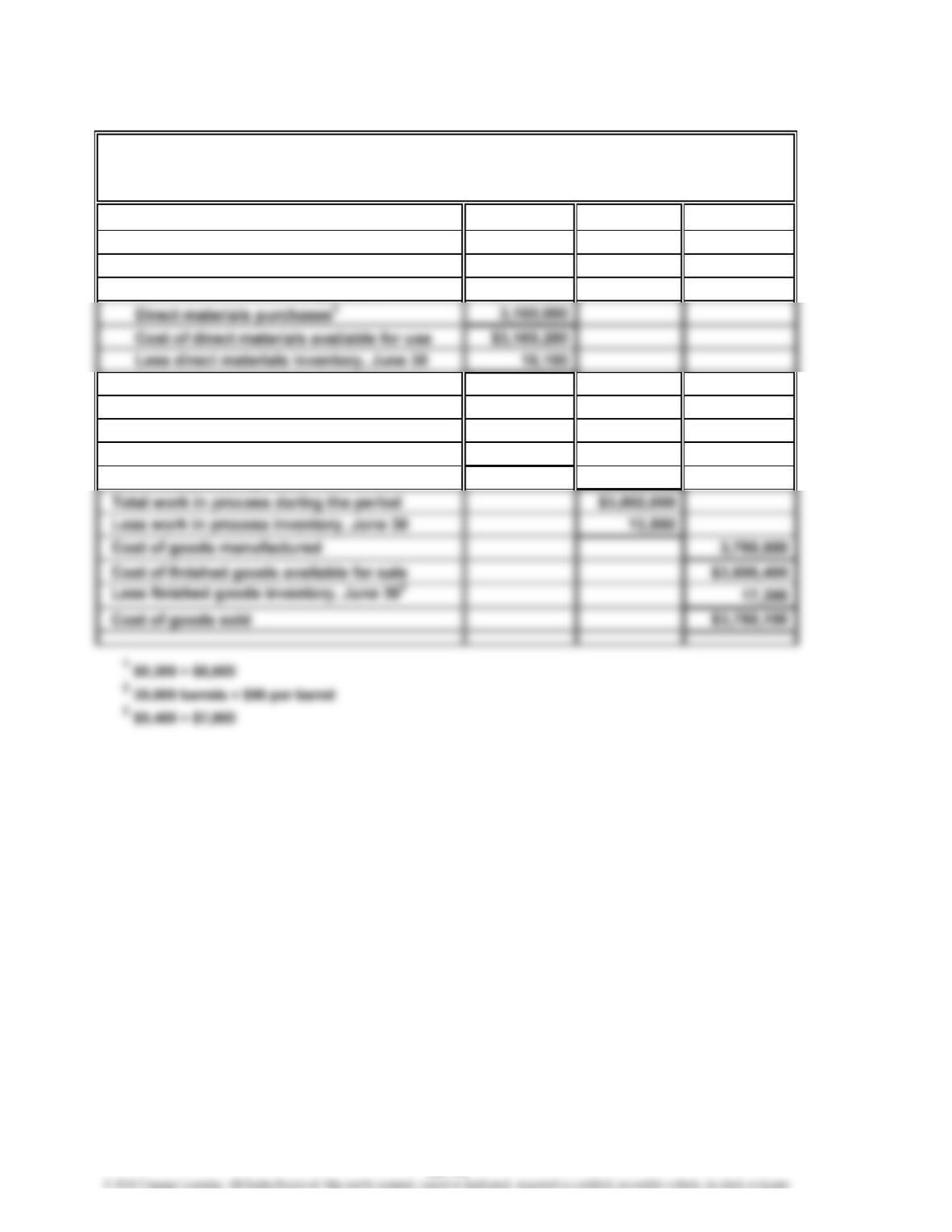

Ex. 22–16

Finished goods inventory, June 1

1

$ 16,900

Work in process inventory, June 1 $ 12,900

Direct materials:

Direct materials inventory, June 1 $ 15,200

Cost of direct materials placed in

production $3,149,100

Direct labor 240,000

Factory overhead 400,000

Total manufacturing costs 3,789,100

DELAWARE CHEMICAL COMPANY

Cost of Goods Sold Budget

For the Month Ending June 30, 2017

22-18

CHAPTER 22 Budgeting

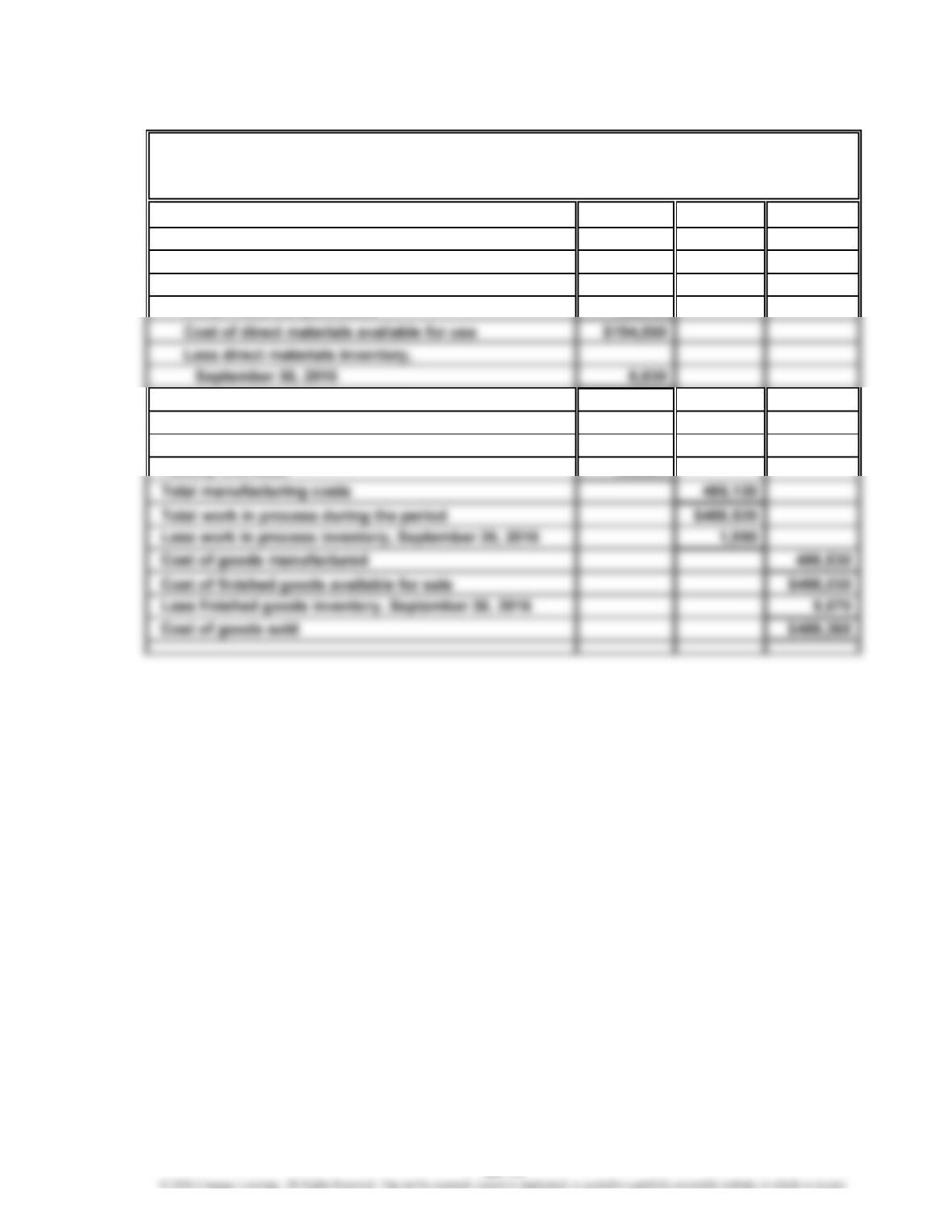

Ex. 22–17

Finished goods inventory, September 1, 2016 $ 11,500

Work in process inventory, September 1, 2016 $ 3,400

Direct materials:

Direct materials inventory, September 1, 2016 $ 6,440

Direct materials purchases 188,410

Cost of direct materials placed in

production $186,020

Direct labor 193,600

Factory overhead 105,500

MINGWARE CERAMICS INC.

Cost of Goods Sold Budget

For the Month Ending September 30, 2016

22-19

CHAPTER 22 Budgeting

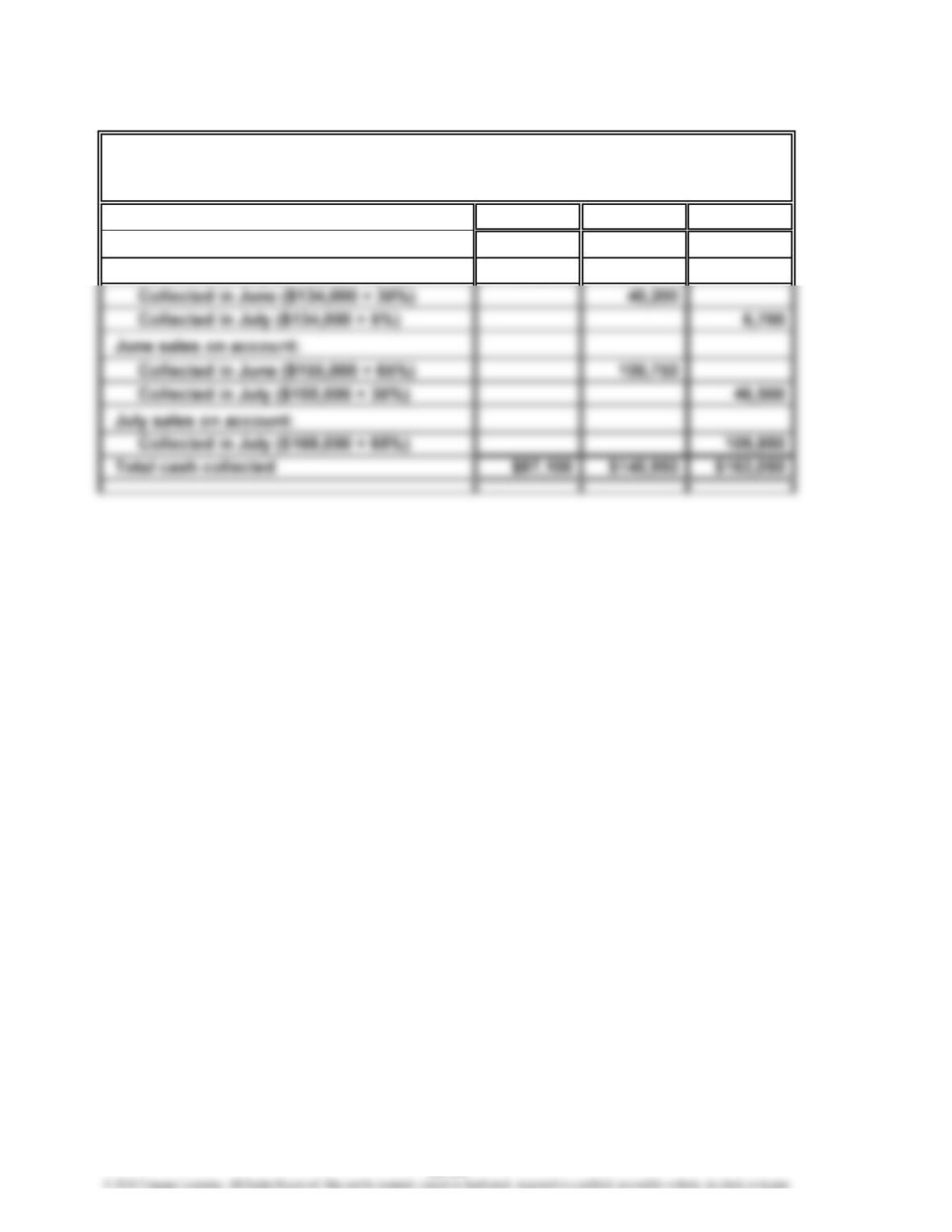

Ex. 22–18

May June July

May sales on account:

Collected in May ($134,000 × 65%) 87,100

PET PLACE SUPPLIES INC.

Schedule of Collections from Sales

For the Three Months Ending July 31, 2016

22-20