Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

PERFORMANCE EVALUATION USING VARIANCES

1. Standards are performance goals. Manufacturing companies normally use standard cost for

each of the three following product costs:

a. Direct materials

2. Reporting by the “principle of exceptions” is the reporting of only variances (or

3. The two variances in direct materials cost are:

4. The offsetting variances might have been caused by the purchase of low-priced, inferior

5. a. The two variances in direct labor costs are:

6. No. Even though the assembly workers are covered by union contracts, direct labor cost variances

7. Standards can be very appropriate in repetitive service operations. Fast-food restaurants can

CHAPTER 22 (FIN MAN); CHAPTER 7 (MAN)

FROM STANDARD COSTS

DISCUSSION QUESTIONS

22-1

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

DISCUSSION QUESTIONS (Continued)

8. a. The variable factory overhead controllable variance results from incurring a total amount

of variable factory overhead cost greater or less than the amount budgeted for the level of

10. Nonfinancial performance measures provide managers additional measures beyond the dollar

22-2

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

PE 22–1A (FIN MAN); PE 7–1A (MAN)

a. Direct materials price –$10,800 [($33.25 – $34.00) × 14,400 gal.]

PE 22–1B (FIN MAN); PE 7–1B (MAN)

a. Direct materials price $2,250 [($3.00 – $2.50) × 4,500 lbs.]

PE 22–2A (FIN MAN); PE 7–2A (MAN)

a. Direct labor rate $8,850 [($30.50 – $30.00) × 17,700 hrs.]

PE 22–2B (FIN MAN); PE 7–2B (MAN)

a. Direct labor rate –$1,400 [($16.50 – $17.00) × 2,800 hrs.]

PRACTICE EXERCISES

22-3

PE 22–3A (FIN MAN); PE 7–3A (MAN)

PE 22–3B (FIN MAN); PE 7–3B (MAN)

PE 22–4A (FIN MAN); PE 7–4A (MAN)

PE 22–4B (FIN MAN); PE 7–4B (MAN)

Variable Factory Overhead

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

PE 22–5A (FIN MAN); PE 7–5A (MAN)

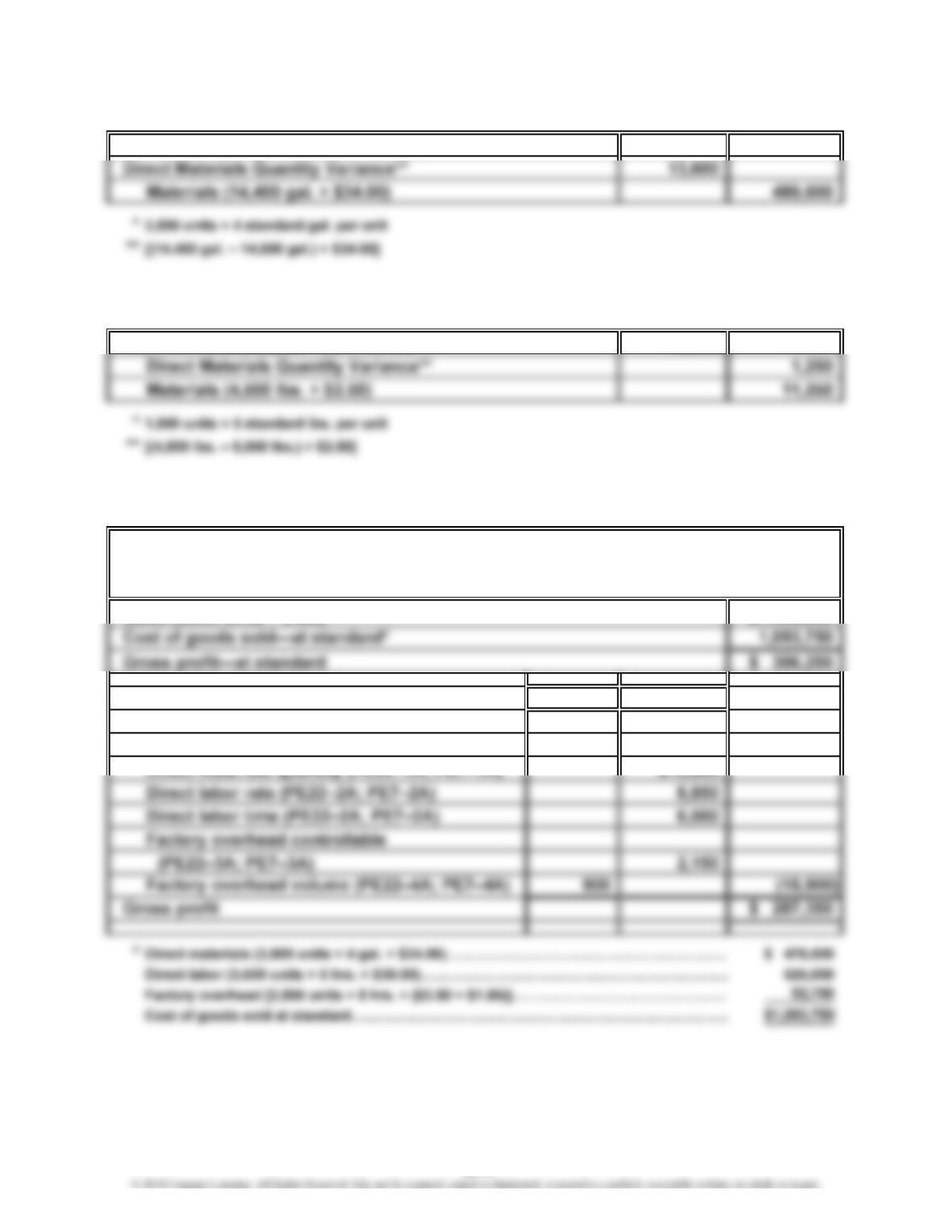

Work in Process (14,000* gal. × $34.00) 476,000

PE 22–5B (FIN MAN); PE 7–5B (MAN)

Work in Process (5,000* lbs. × $2.50) 12,500

PE 22–6A (FIN MAN); PE 7–6A (MAN)

Sales (3,500 units × $400) $1,400,000

Favorable Unfavorable

Less variances from standard cost:

Direct materials price (PE22–1A; PE7–1A) $10,800

GIOVANNI COMPANY

Income Statement Through Gross Profit

For the Year Ended December 31, 2014

22-5

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

PE 22–6B (FIN MAN); PE 7–6B (MAN)

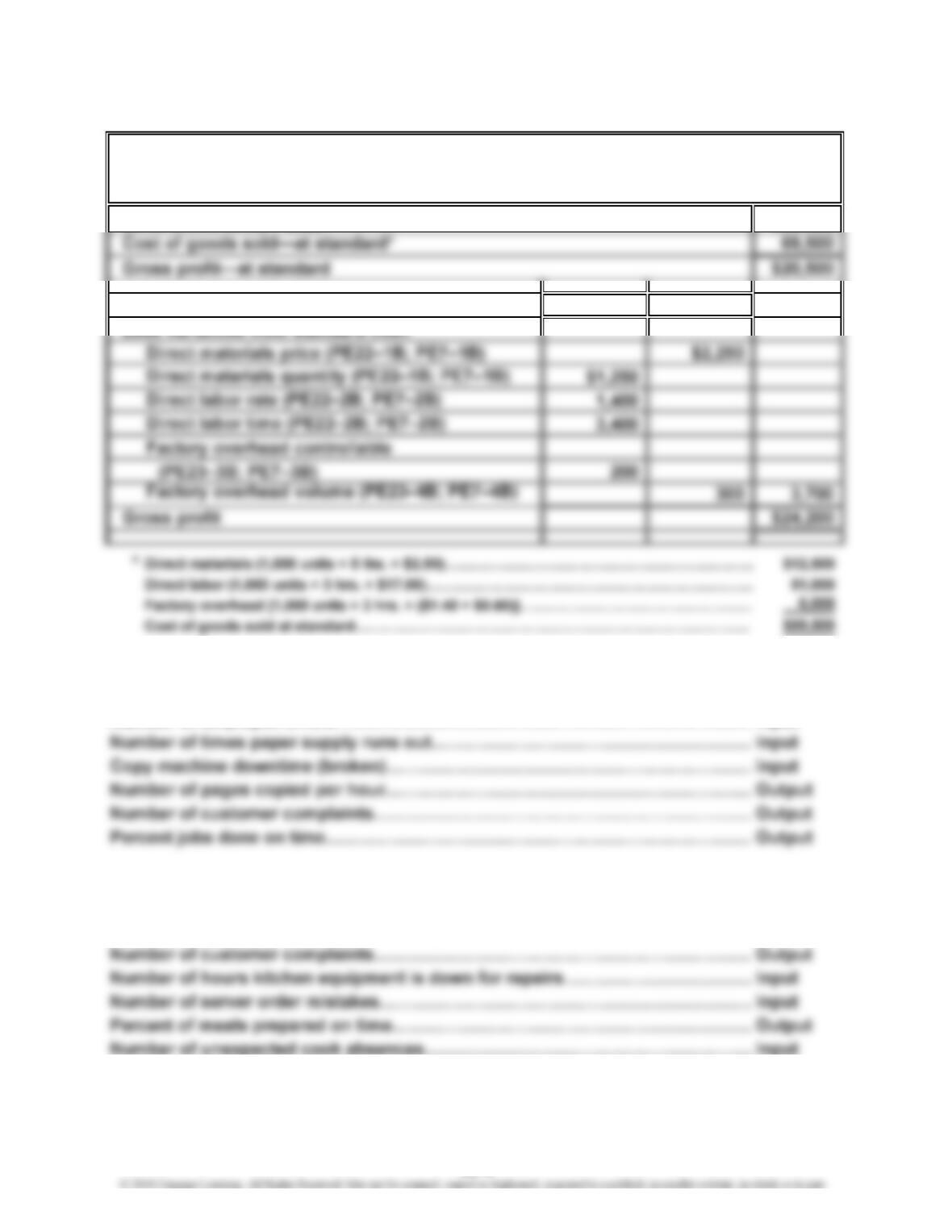

Sales (1,000 units × $90) $90,000

Favorable Unfavorable

PE 22–7A (FIN MAN); PE 7–7A (MAN)

Number of employee errors………………………………………………………………

…

Input

PE 22–7B (FIN MAN); PE 7–7B (MAN)

Number of times ingredients are missing……………………………………………… Input

DVORAK COMPANY

Income Statement Through Gross Profit

For the Year Ended December 31, 2014

22-6

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

Ex. 22–1 (FIN MAN); Ex. 7–1 (MAN)

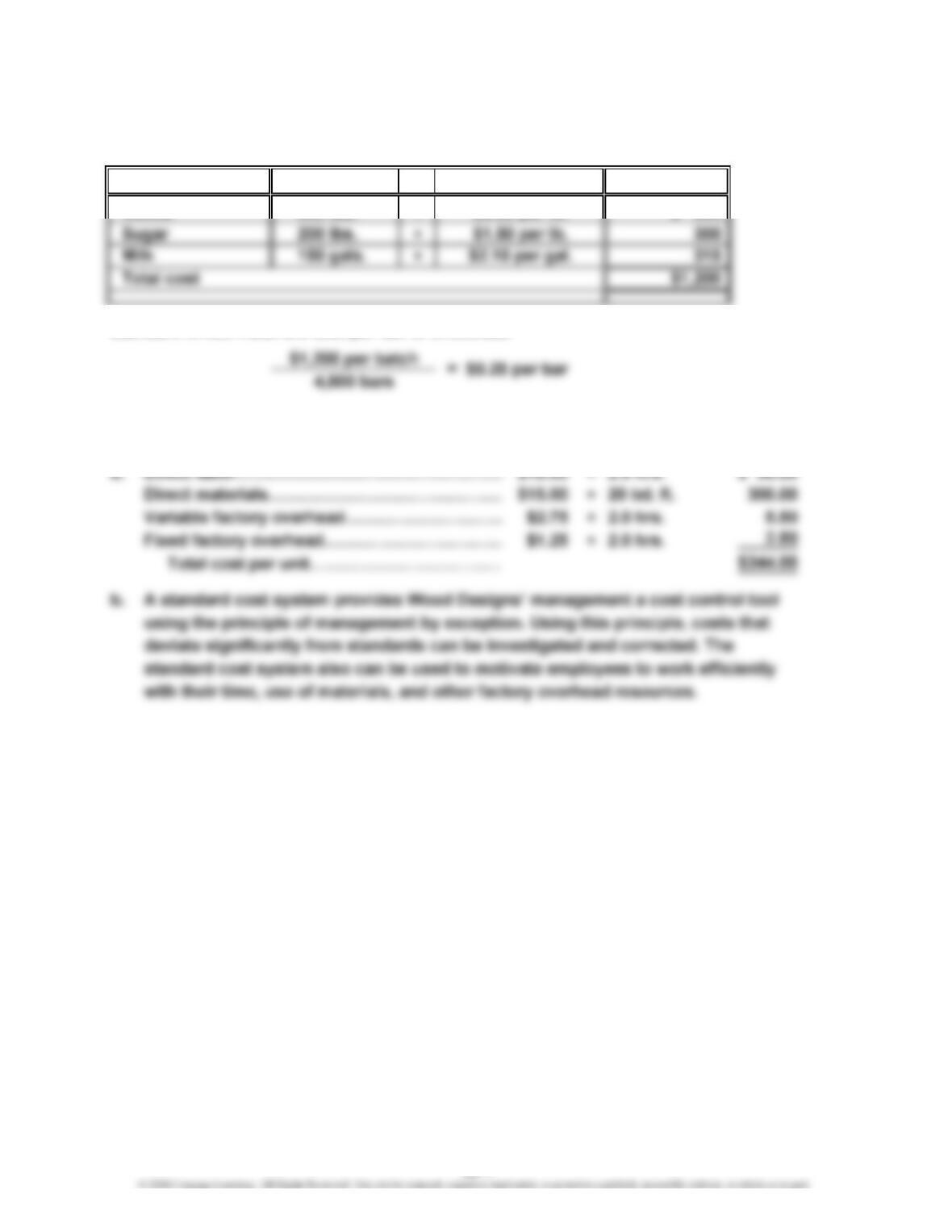

Quantity × Total

650 lbs. ×$ 585

Standard direct materials cost per bar of chocolate:

Ex. 22–2 (FIN MAN); Ex. 7–2 (MAN)

EXERCISES

Ingredient

Cocoa

Price

$0.90 per lb.

22-7

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

Ex. 22–3 (FIN MAN); Ex. 7–3 (MAN)

a.

Standard Cost at

Planned Volume

(600,000 Bottles)

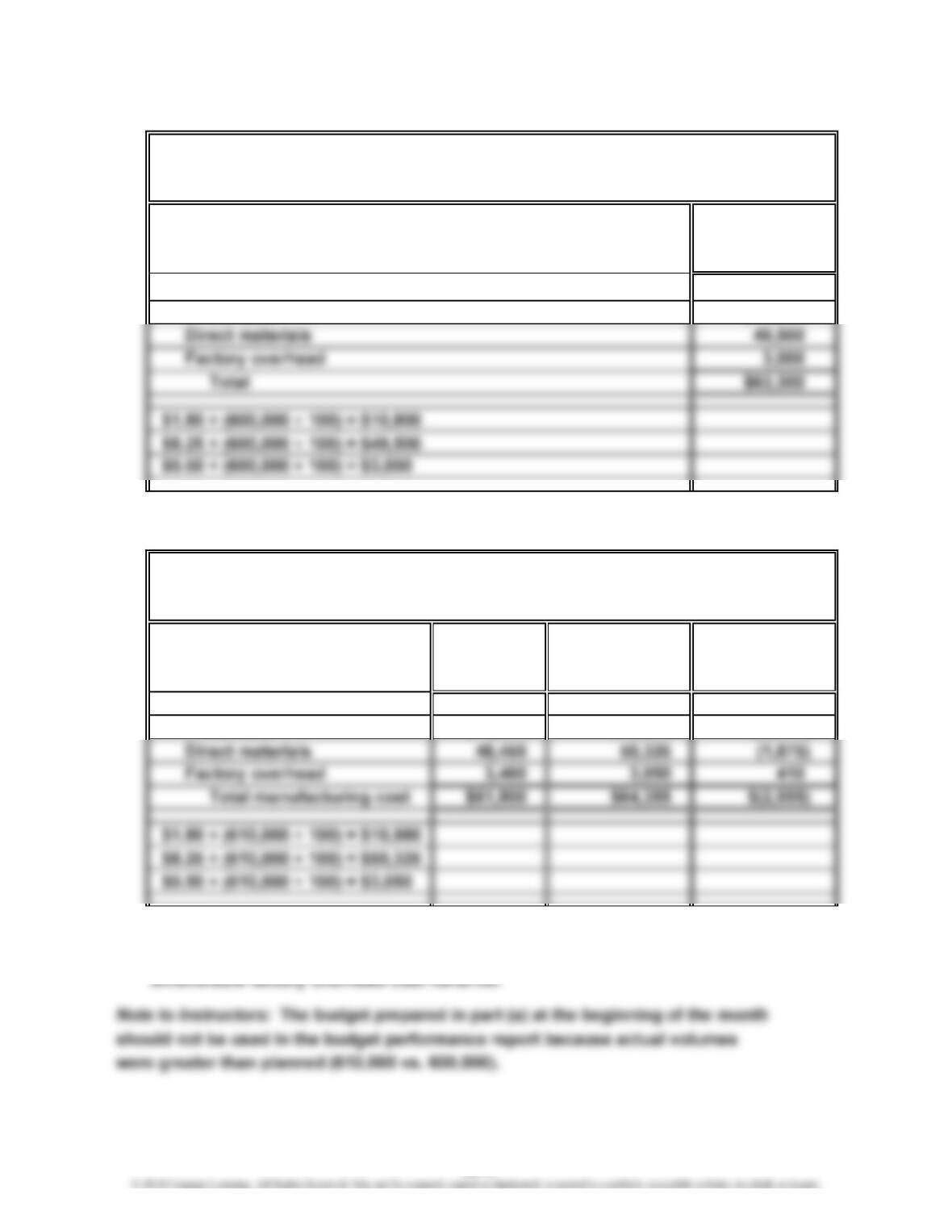

Manufacturing costs:

Direct labor $10,800

Note: The cost standards are expressed as “per 100 bottles.”

b.

Standard Cost at Cost Variance—

Actual Actual Volume (Favorable)

Costs (610,000 Bottles) Unfavorable

Manufacturing costs:

Direct labor $ 9,890 $10,980 $(1,090)

c. Time in a Bottle Company’s actual costs were $2,555 less than budgeted. Favorable

direct labor and direct material cost variances more than offset a small

For the Month Ended May 31, 2014

TIME IN A BOTTLE COMPANY

Manufacturing Costs—Budget Performance Report

TIME IN A BOTTLE COMPANY

Manufacturing Cost Budget

For the Month Ended May 31, 2014

22-8

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

Ex. 22–4 (FIN MAN); Ex. 7–4 (MAN)

a. Price variance:

Quantity variance:

Total direct materials cost variance:

b. The direct materials price variance should normally be reported to the

Purchasing Department, which may or may not be able to control this variance.

If materials of the same quality were purchased from another supplier at a price

Direct Materials

Cost Variance =

Direct Materials

Price Variance

Direct Materials

Quantity Variance

(Actual Price – Standard Price) × Actual Quantity

=

=

Direct Materials Price Variance +

Direct Materials Quantity Variance

(Actual Quantity – Standard Quantity) × Standard Price

22-9

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

Ex. 22–5 (FIN MAN); Ex. 7–5 (MAN)

Price variance:

Quantity variance:

Total direct materials cost variance:

(Actual Quantity – Standard Quantity) × Standard Price

=

Direct Materials

Price Variance

Direct Materials

Quantity Variance

=

Direct Materials Price Variance +

Direct Materials Quantity Variance

(Actual Price – Standard Price) × Actual Quantity

Direct Materials

Cost Variance =

22-10

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

Ex. 22–6 (FIN MAN); Ex. 7–6 (MAN)

Product finished………………………………………………………

…

1,400 units

Proof:

Direct Materials Price Variance = (Actual Price – Standard Price) × Actual Quantity

22-11

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

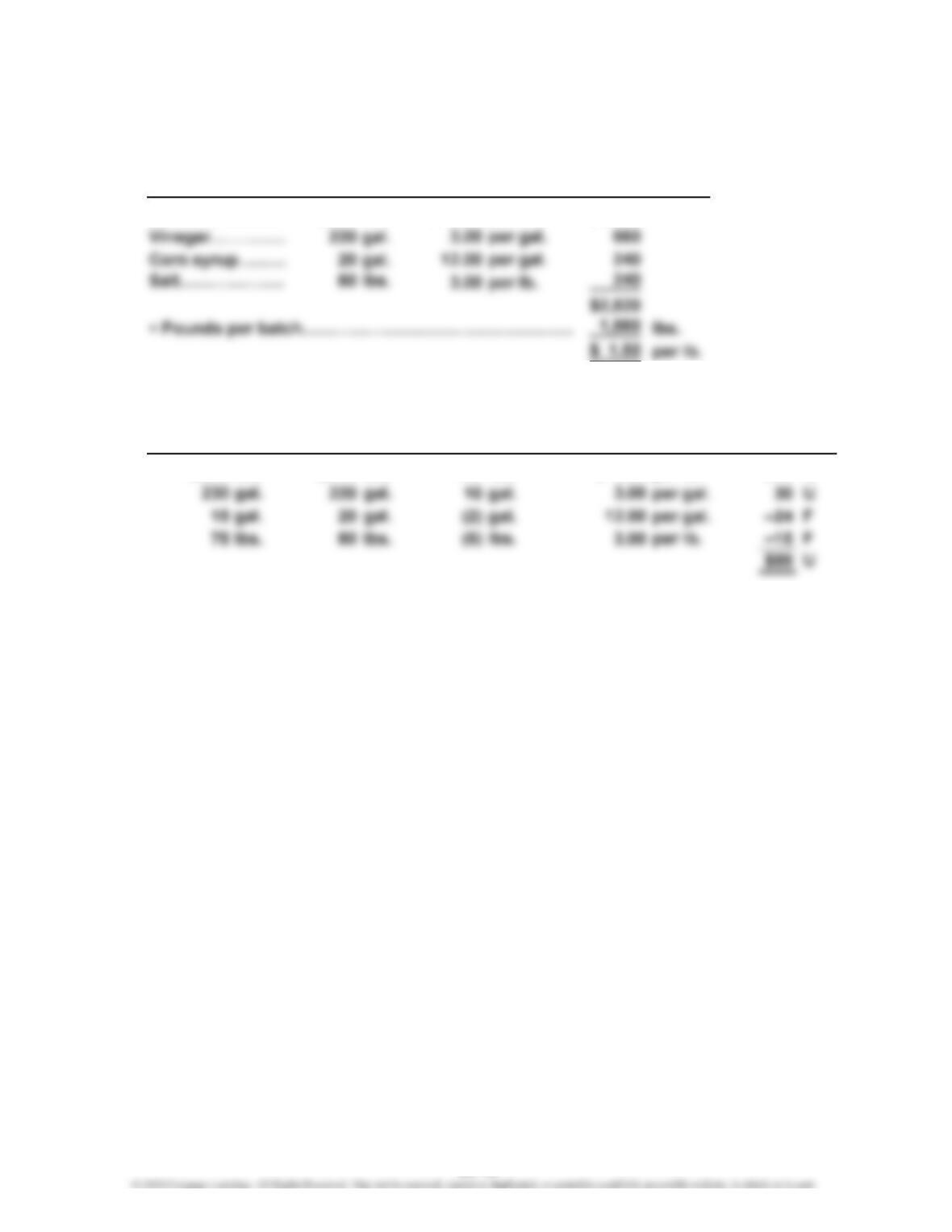

Ex. 22–7 (FIN MAN); Ex. 7–7 (MAN)

a.

× =

Whole tomatoes

…

3,360 lbs. $ 0.50 per lb. $1,680

b.

– = × =

3,556 lbs. 3,360 lbs. 196 lbs. $ 0.50 per lb. $98 U

Materials

Quantity

Variance

Standard

Cost per

Batch

Standard

Quantity

Standard

Price

Batch K-54

Quantity for

Actual Standard

Quantity per

Batch

Quantity

Difference

Standard

Price

22-12

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

Ex. 22–8 (FIN MAN); Ex. 7–8 (MAN)

a. Rate variance:

Time variance:

Total direct labor cost variance:

b. The employees may have been less experienced workers who were paid less than

(Actual Direct Labor Hours – Standard Direct Labor Hours)

× Standard Rate per Hour

Direct Labor Rate Variance + Direct Labor Time Variance

(Actual Rate per Hour – Standard Rate per Hour)

× Actual Hours

=

Direct Labor

Rate Variance

Direct Labor

Time Variance

=

Direct Labor

Cost Variance =

22-13

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

Ex. 22–9 (FIN MAN); Ex. 7–9 (MAN)

a. Rate variance:

Time variance:

Total direct labor cost variance:

b. Debit to Work in Process: $12,800

Direct Labor

Rate Variance

Direct Labor

Time Variance

=

=

Direct Labor

Cost Variance =

Direct Labor Rate Variance + Direct Labor Time Variance

(Actual Rate per Hour – Standard Rate per Hour)

× Actual Hours

(Actual Direct Labor Hours – Standard Direct Labor Hours)

× Standard Rate per Hour

22-14

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

Ex. 22–10 (FIN MAN); Ex. 7–10 (MAN)

a. (1) Cutting Department

Rate variance:

Time variance:

Total direct labor cost variance:

=

(Actual Direct Labor Hours – Standard Direct Labor Hours)

× Standard Rate per Hour

Direct Labor

Time Variance

(Actual Rate per Hour – Standard Rate per Hour)

× Actual Hours

Direct Labor

Rate Variance =

22-15

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

Ex. 22–10 (FIN MAN); Ex. 7–10 (MAN) (Concluded)

(2) Sewing Department

Rate variance:

*0.40 hr. × 25,000 units

Total direct labor cost variance:

(Actual Rate per Hour – Standard Rate per Hour)

× Actual Hours

Direct Labor

Rate Variance =

Direct Labor

Cost Variance =

Direct Labor Rate Variance + Direct Labor Time Variance

22-16

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

Ex. 22–11 (FIN MAN); Ex. 7–11 (MAN)

b. Standard time used for the volume of admissions:

Total

Number of admissions…

…

140 350

c. Actual productive minutes available

(4 employees × 40 hrs. × 60 min.)………………………

…

9,600 minutes

Unscheduled Scheduled

22-17

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

Ex. 22–12 (FIN MAN); Ex. 7–12 (MAN)

a.

b. Actual pieces sorted = 41,220,000

Actual Pieces of Mail Sorted ÷

Standard Sorts per Minute ×

Standard Minutes per Hour =

Standard Number of Hours

Standard Sorts per Hour

(per employee)

22-18

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

Ex. 22–13 (FIN MAN); Ex. 7–13 (MAN)

Step 1: Determine the standard direct materials and direct labor per unit.

Standard direct materials quantity per unit:

Direct materials lbs. budgeted for June:

Standard pounds per unit:

Standard direct labor time per unit:

Direct labor hrs. budgeted for June:

Step 2: Using the standard quantity and time rates in step 1, determine the

standard costs for the actual June production.

Standard direct materials at actual volume:

Step 3: Determine the direct materials quantity and direct labor time variances,

assuming no direct materials price or direct labor rate variances.

Actual direct labor……………………………………………………………………… $24,500

(1,750 hrs. – 1,800 hrs.) × $14.00 = –$700 F

22-19

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

Ex. 22–14 (FIN MAN); Ex. 7–14 (MAN)

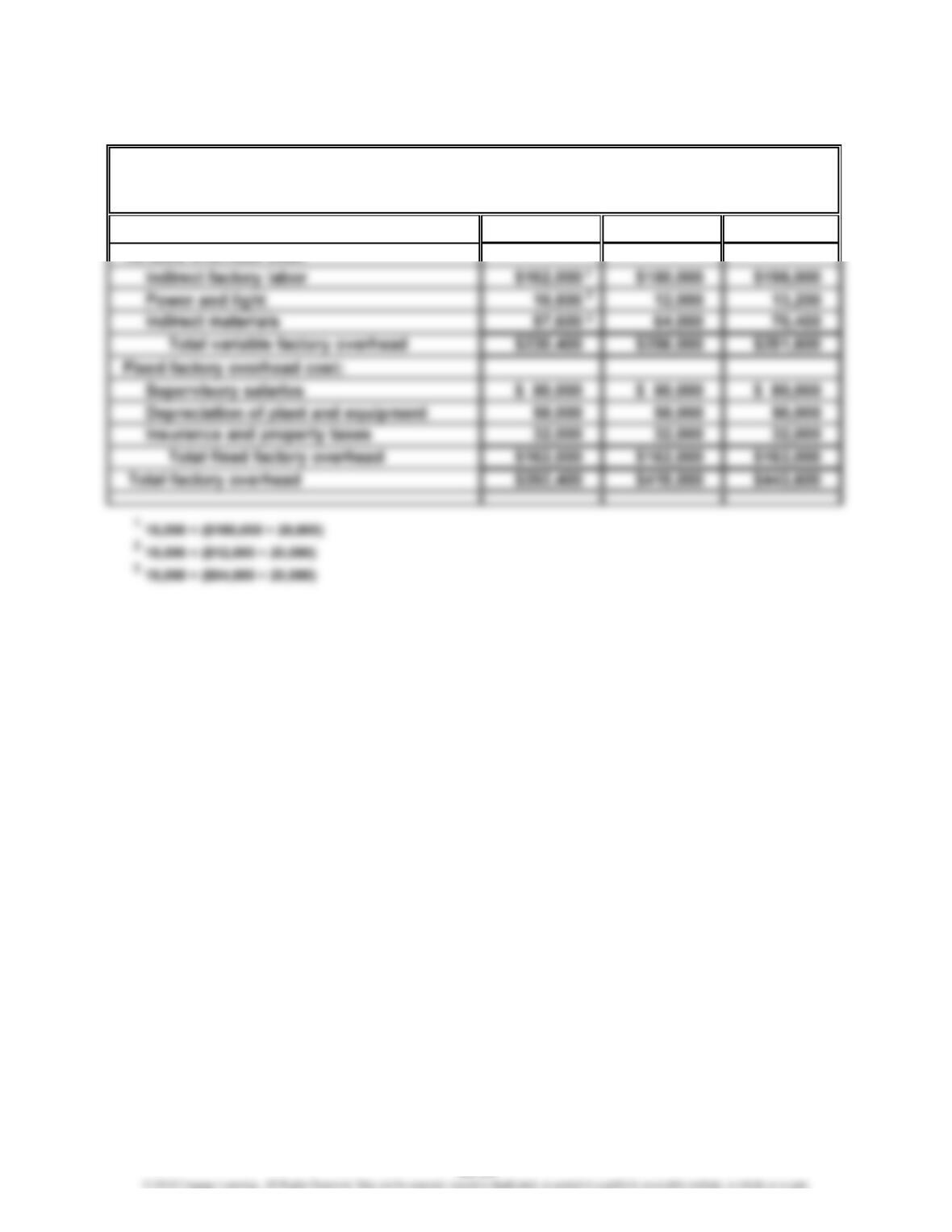

Direct labor hours 18,000 20,000 22,000

Variable overhead cost:

LENO MANUFACTURING COMPANY

Factory Overhead Cost Budget—Press Department

For the Month Ended November 30, 2014

22-20