CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

Prob. 22–3A (FIN MAN); Prob. 7–3A (MAN) (Continued)

c.

Variable factory overhead controllable variance:

Actual variable factory overhead cost incurred…………

…

$16,680

Budgeted variable factory overhead for 3,000 hrs.* ……

…

16,500

V

ariance—unfavorable……………………………………

…

$180

Factory Overhead Cost Variance

**

22-41

V

…

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

Prob. 22–3A (FIN MAN); Prob. 7–3A (MAN) (Concluded)

Actual costs 29,480 Applied costs 28,500

($16,680 + $12,800) [3,000 × ($5.50 + $4.00)]

Balance (underapplied) 980

Alternative Computation of Overhead Variances

Factory Overhead

22-42

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

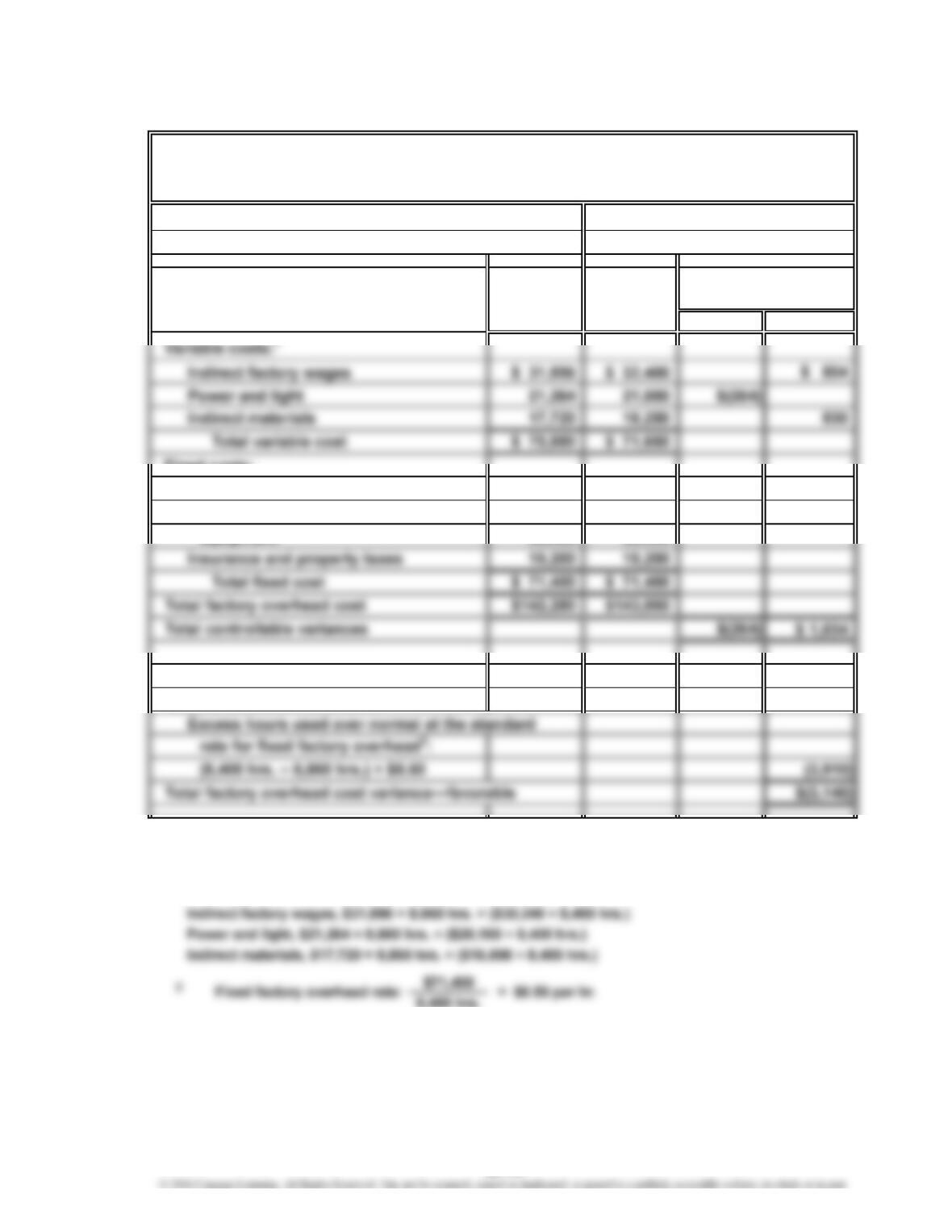

Prob. 22–4A (FIN MAN); Prob. 7–4A (MAN)

Normal capacity for the month 8,400

hrs.

Actual production for the month 8,860 hrs.

Budget Actual Favorable Unfavorable

Fixed costs:

Supervisory salaries $ 20,000 $ 20,000

Depreciation of plant and

equipment 36,200 36,200

Net controllable variance—unfavorable $ 770

Volume variance—favorable:

1

The budgeted variable costs are determined by multiplying the 8,860 actual hours

by the variable overhead rate (the May budget divided by 8,400 hours for each

variable overhead cost). Thus,

TIGER EQUIPMENT INC.

Factory Overhead Cost Variance Report—Welding Department

For the Month Ended May 31

Variances

22-43

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

Prob. 22–4A (FIN MAN); Prob. 7–4A (MAN) (Concluded)

Actual costs 143,050 Applied costs* 146,190

[8,860 × ($8.00 + $8.50)]

Balance (overapplied) 3,140

Alternative Computation of Overhead Variances

Factory Overhead

22-44

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

Prob. 22–5A (FIN MAN); Prob. 7–5A (MAN)

1. Actual hours provided (5 × 40 hrs.)……………………………………………

…

200

Standard hours required for the original plan*………………………………

…

186

2. Actual hours provided (5 × 40 hrs.)……………………………………………

…

200

Standard hours required for the actual results*……………………………

…

226

…

…

3. Actual labor rate…………………………………………………………………… $40

Standard labor rate………………………………………………………………

…

32

…

4. The labor rate and time variances fail to consider the number of errors in the

code from programmer fatigue. A program that has many errors will require

5. Actual hours provided (6 × 40 hrs.)……………………………………………

…

240

…

…

*

6. Hiring an extra employee is less costly than the bonus by $320. The direct labor

cost variance for paying the bonus was $768 unfavorable, which is the sum of the

22-45

…

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

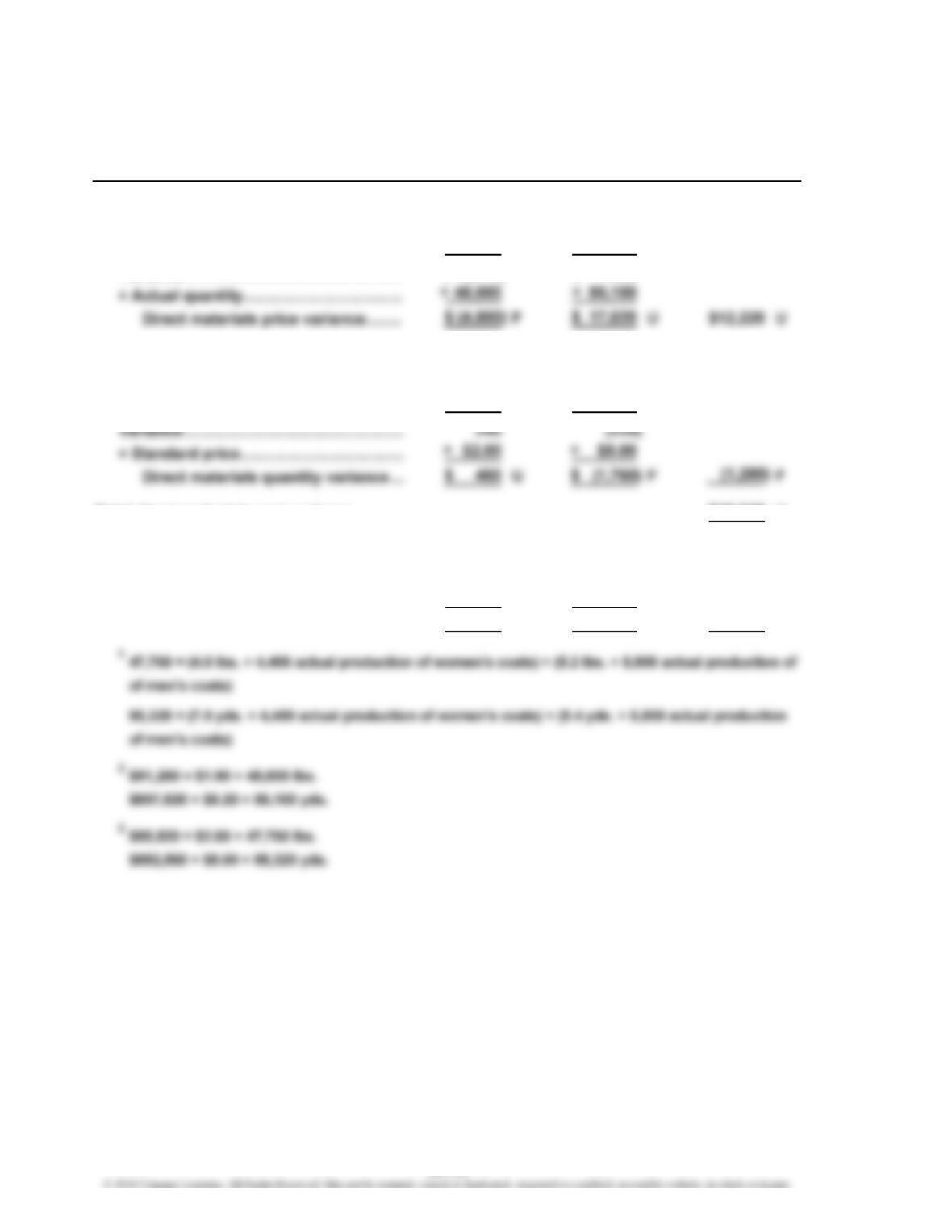

Prob. 22–1B (FIN MAN); Prob. 7–1B (MAN)

a.

Standard

Materials and

Labor Cost

b.

Price variance:

= ($5.10 per yd. – $5.00 per yd.) × 26,200 yds.

Direct Materials Cost Variance

Direct Materials

Price Variance

= (Actual Price – Standard Price) × Actual Quantity

22-46

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

Prob. 22–1B (FIN MAN); Prob. 7–1B (MAN) (Concluded)

c.

Rate variance:

= ($11.80 – $12.00) × 1,000 hrs.*

= –$200 Favorable

Direct Labor Cost Variance

(Actual Rate per Hour – Standard Rate per Hour)

× Actual Hours

Direct Labor

Rate Variance

=

22-47

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

Prob. 22–2B (FIN MAN); Prob. 7–2B (MAN)

1. a.

Direct Materials Variance

Price variance:

Actual price………………………………

…

$ 1.90 $ 8.20

Standard price……………………………

…

2.00 8.00

V

ariance……………………………………

…

$ (0.10) $ 0.20

Quantity variance:

Actual quantity used……………………

…

48,000 85,100

Standard quantity used

1

………………

…

47,760 85,320

V

…

…

Total direct materials cost variance………

…

$10,940 U

Alternatively, total direct materials cost variance:

Actual cost

2

………………………………

…

$91,200 $697,820

Standard cost

3

……………………………

…

95,520 682,560

Total direct materials cost variance

…

$ (4,320) F$ 15,260 U$10,940 U

Filler Liner Total

22-48

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

Prob. 22–2B (FIN MAN); Prob. 7–2B (MAN) (Concluded)

1. b.

Actual rate…………………………………

…

$ 14.10 $ 13.30

Standard rate………………………………

…

$ 14.00 $ 13.00

…

Direct labor rate variance……………

…

$182.50 U$ 840 U $1,022.50 U

Time variance:

…

…

Direct labor time variance……………

…

$910.00 U$(1,300) F(390) F

Total direct labor cost variance……………

…

$ 632.50 U

Alternatively, total direct labor cost variance:

Actual cost

2

………………………………… $25,732.50 $37,240.00

Standard cost

3

……………………………

…

24,640.00 37,700.00

2

$25,732.50 = 1,825 hrs. × $14.10

$37,240.00 = 2,800 hrs. × $13.30

2. The variance analyses should be based on the standard amounts at actual

volumes. The budget must flex with the volume changes. If the actual volume

22-49

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

Prob. 22–3B (FIN MAN); Prob. 7–3B (MAN)

a.

Price variance:

= ($6.50 per lb. – $6.40 per lb.) × 101,000 lbs.

= $10,100 Unfavorable

Quantity variance:

Direct Materials Cost Variance

= (Actual Price – Standard Price) × Actual Quantity

Direct Materials

Quantity Variance = (Actual Quantity – Standard Quantity) × Standard Price

Direct Materials

Price Variance

22-50

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

Prob. 22–3B (FIN MAN); Prob. 7–3B (MAN) (Continued)

b.

Rate variance:

= ($15.40 – $15.75) × 2,000 hrs.

= –$700 Favorable

Direct Labor Cost Variance

Direct Labor

Rate Variance

=(Actual Rate per Hour – Standard Rate per Hour)

× Actual Hours

22-51

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

Prob. 22–3B (FIN MAN); Prob. 7–3B (MAN) (Continued)

c.

Variable factory overhead controllable variance:

Actual variable factory overhead cost incurred…………

…

$8,200

Budgeted variable factory overhead for 2,080 hrs.* ……

…

8,320

V

ariance—favorable………………………………………

…

$(120)

Factory Overhead Cost Variance

**

22-52

V

…

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

Prob. 22–3B (FIN MAN); Prob. 7–3B (MAN) (Concluded)

Actual costs 20,200 Applied costs 20,800

($8,200 + $12,000) [2,080 × ($4.00 + $6.00)]

Balance (overapplied) (600)

Actual Applied

Factory Factory

Overhead for Amount

Alternative Computation of Overhead Variances

Factory Overhead

Budgeted Factory

22-53

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

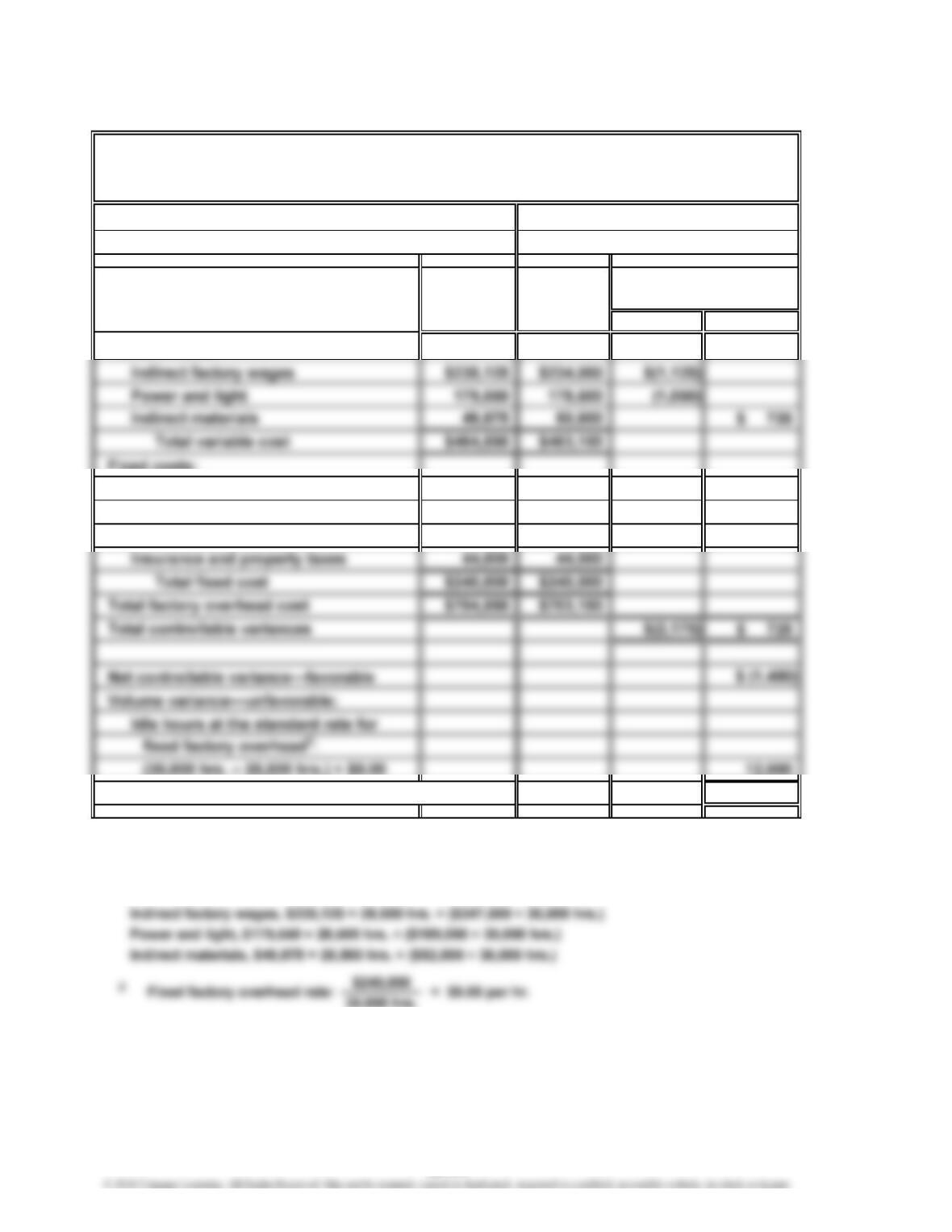

Prob. 22–4B (FIN MAN); Prob. 7–4B (MAN)

Normal capacity for the month 30,000

hrs.

Actual production for the month 28,500 hrs.

Budget Actual Favorable Unfavorable

Variable costs:

1

Fixed costs:

Supervisory salaries $126,000 $126,000

Depreciation of plant and

equipment 70,000 70,000

Total factory overhead cost variance—unfavorable $10,550

1

The budgeted variable costs are determined by multiplying 28,500 actual hours

by the variable overhead rate (the October budget divided by 30,000 hours for

each variable overhead cost). Thus,

FEELING BETTER MEDICAL INC.

Factory Overhead Cost Variance Report—Assembly Department

For the Month Ended October 31

Variances

22-54

CHAPTER 22 Performance Evaluation Using Variances from Standard Costs

Prob. 22–4B (FIN MAN); Prob. 7–4B (MAN) (Concluded)

Actual costs 703,100 Applied costs* 692,550

[28,500 × ($16.30 + $8.00)]

Balance (underapplied) 10,550

Actual Applied

Factory Factory

Overhead Overhead

Produced

Overhead for Amount

Alternative Computation of Overhead Variances

Factory Overhead

Budgeted Factory

22-55