Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 22

1282

Problem 22-4B (Concluded)

Supporting Footnotes

Note C

Note D

Beginning raw materials inventory …………………………..

Purchases of raw materials ……………………………………….

Less materials used in production** …………………………..

(240,000)

Note E

Beginning finished goods inventory …………………………..

$ 241,080

Cost of goods completed during the period ……………….

Less cost of goods sold during the period …………………

*Also equals 16,800 units @ $14.35 = $241,080

Note F

Beginning equipment …………………………..……………………

$ 720,000

Purchased in September …………………………………………..

Note G

Beginning accumulated depreciation …………………………

Depreciation expense ……………………………………………….

60,000

Note H

Beginning accounts payable ……………………………………..

$ 51,400

Purchases of raw materials ……………………………………….

Payments for raw materials ……………………………………….

Note I

NABAR MANUFACTURING

Budgeted Statement of Retained Earnings

For Three Months Ended September 30, 2017

Retained earnings, beginning ……………………. $60,580

Beginning receivables ………………………………………………

Credit sales ………………………………………………………………

Less collections ……………………………………………………….

1283

Problem 22-5B (60 minutes)

Part 1

H2O SPORTS

Merchandise Purchases Budgets

For April, May, and June

April

May

June

Budgeted sales for next month ………………………

Ratio of ending inventory to future sales ………..

Budgeted ending inventory …………………………..

Required units of available merchandise ………..

79,000

103,000

140,000

Less actual (or budgeted) beginning inventory …….

(40,000)

(9,000)

(13,000)

Budgeted purchases ……………………………………..

Budgeted sales for next month ………………………

Ratio of ending inventory to future sales ………..

Add budgeted sales ……………………………………….

110,000

Required units of available merchandise ………..

101,000

120,000

Less actual (or budgeted) beginning inventory …….

(9,000)

(11,000)

Budgeted purchases ……………………………………..

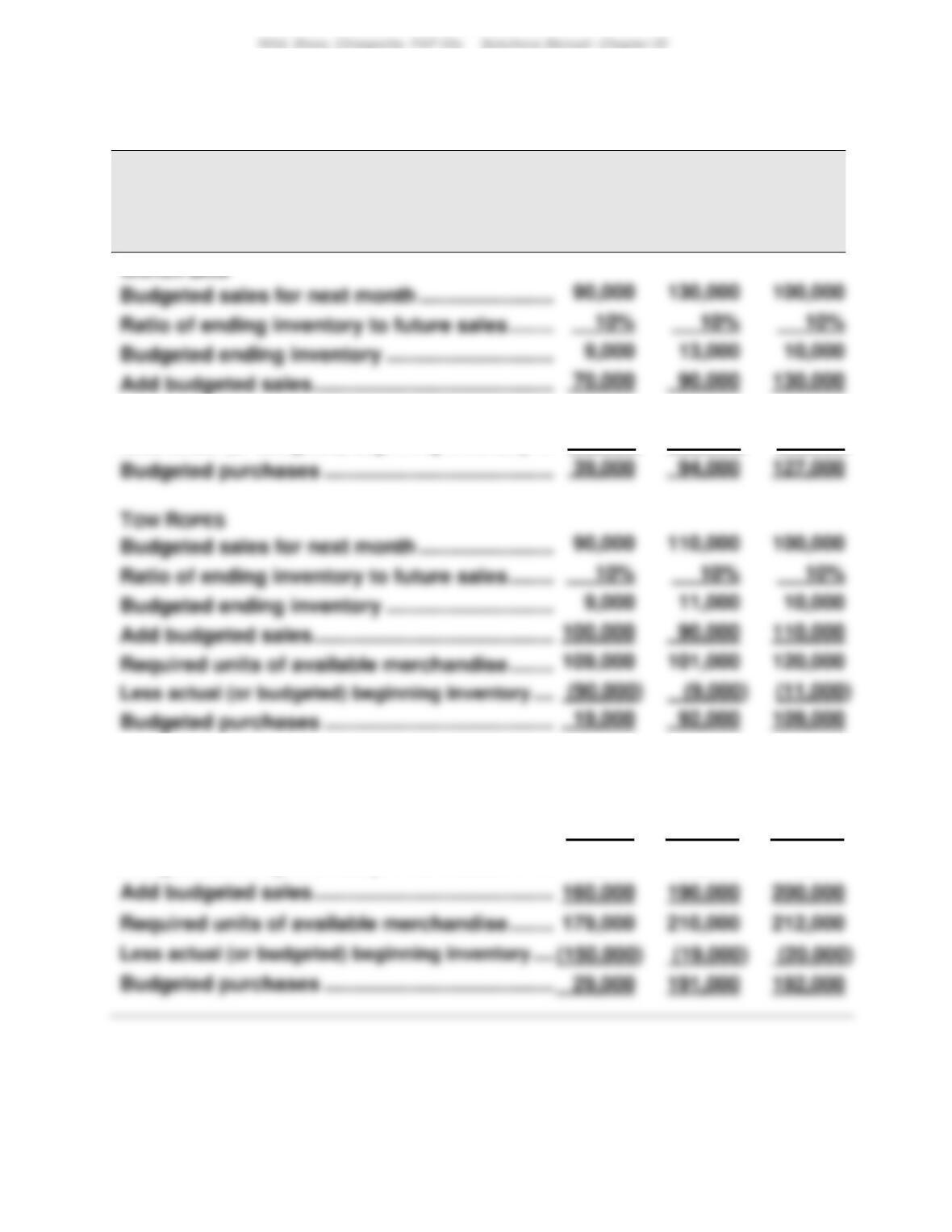

LIFE JACKETS

Budgeted sales for next month ………………………

190,000

200,000

120,000

Ratio of ending inventory to future sales ………..

10%

10%

10%

Budgeted ending inventory …………………………..

19,000

20,000

12,000

160,000

190,000

200,000

Required units of available merchandise ………..

179,000

210,000

212,000

Less actual (or budgeted) beginning inventory …….

1284

Problem 22-5B (Concluded)

Part 2. Analysis Component

Inventory levels might become too high for a number of reasons, including:

• Management may have simply lost sight of inventory levels, thereby

allowing them to reach inappropriately high levels.

1285

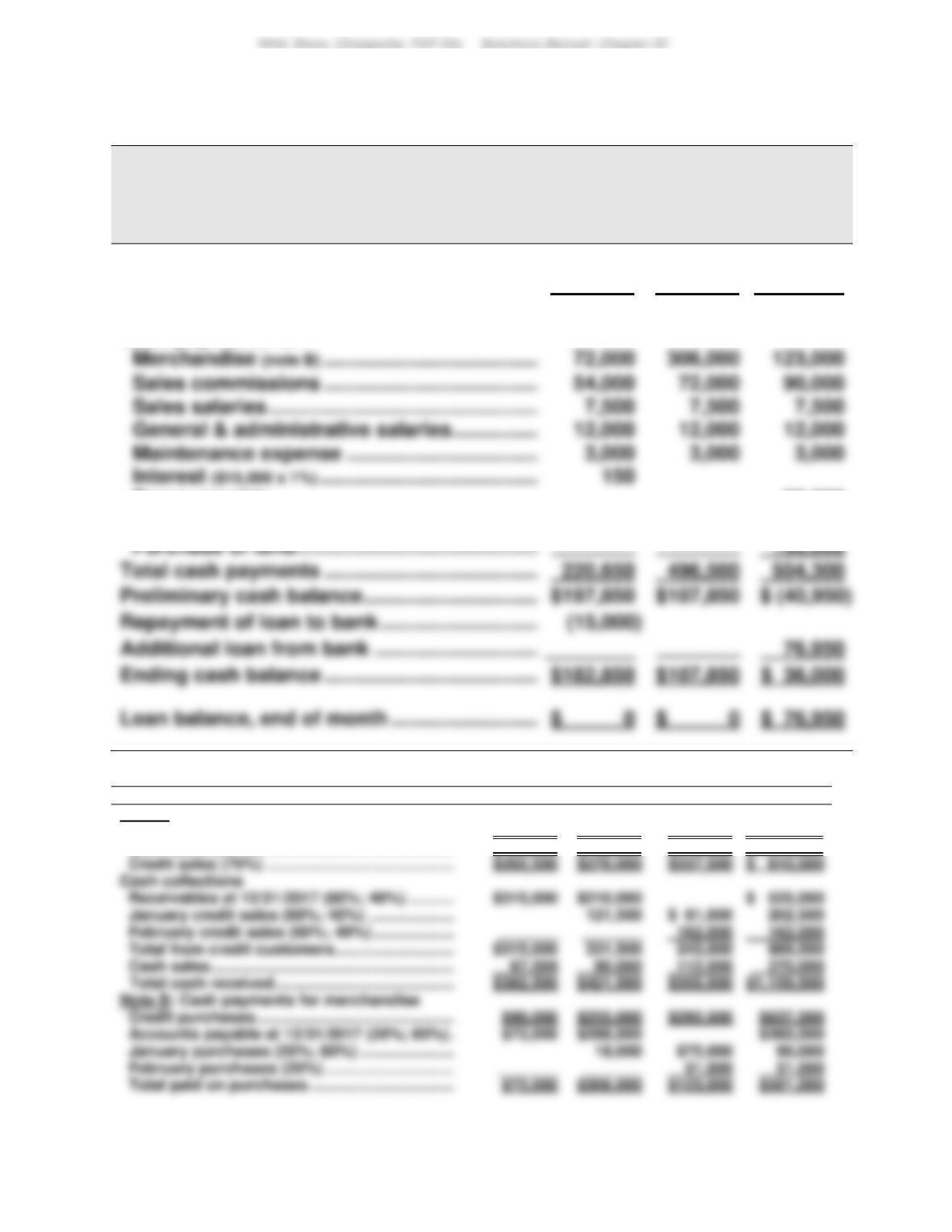

Problem 22-6B (50 minutes)

SONY STEREO

Cash Budgets

For April, May, and June

April

May

June

Beginning balance ……………………………………

$ 3,000

$ 53,000

$ 44,000

Cash receipts

Receipts from bank loan …………………………

Total cash available ………………………………….

Cash payments

Payments on accounts payable** ……………

80,000

188,000

186,000

Payroll ……………………………………………………

16,000

17,000

18,000

Other expenses ………………………………………

64,000

Interest on bank loan* …………………………..

Supporting calculations

Collections of credit sales*

March

April

May

June

March sales ($180,000)—[25%: 45%: 20%: 9%] …………..

$ 45,000

$ 81,000

$ 36,000

$ 16,200

April sales ($220,000)—[25%: 45%: 20%] …………………..

May sales ($300,000)—[25%: 45%] …………………………..

June sales ($380,000)—[25%] …………………………..

–

–

Payments on credit purchases**

March

April

May

June

March purchases ($100,000)—(0%: 80%: 20%) …………………………..

April purchases ($210,000)—(0%: 80%: 20%) …………………………..

May purchases ($180,000)—(0%: 80%) …………………………..

June purchases ($220,000)—(0%) …………………………..

–

–

1286

Problem 22-7B (70 minutes)

Part 1

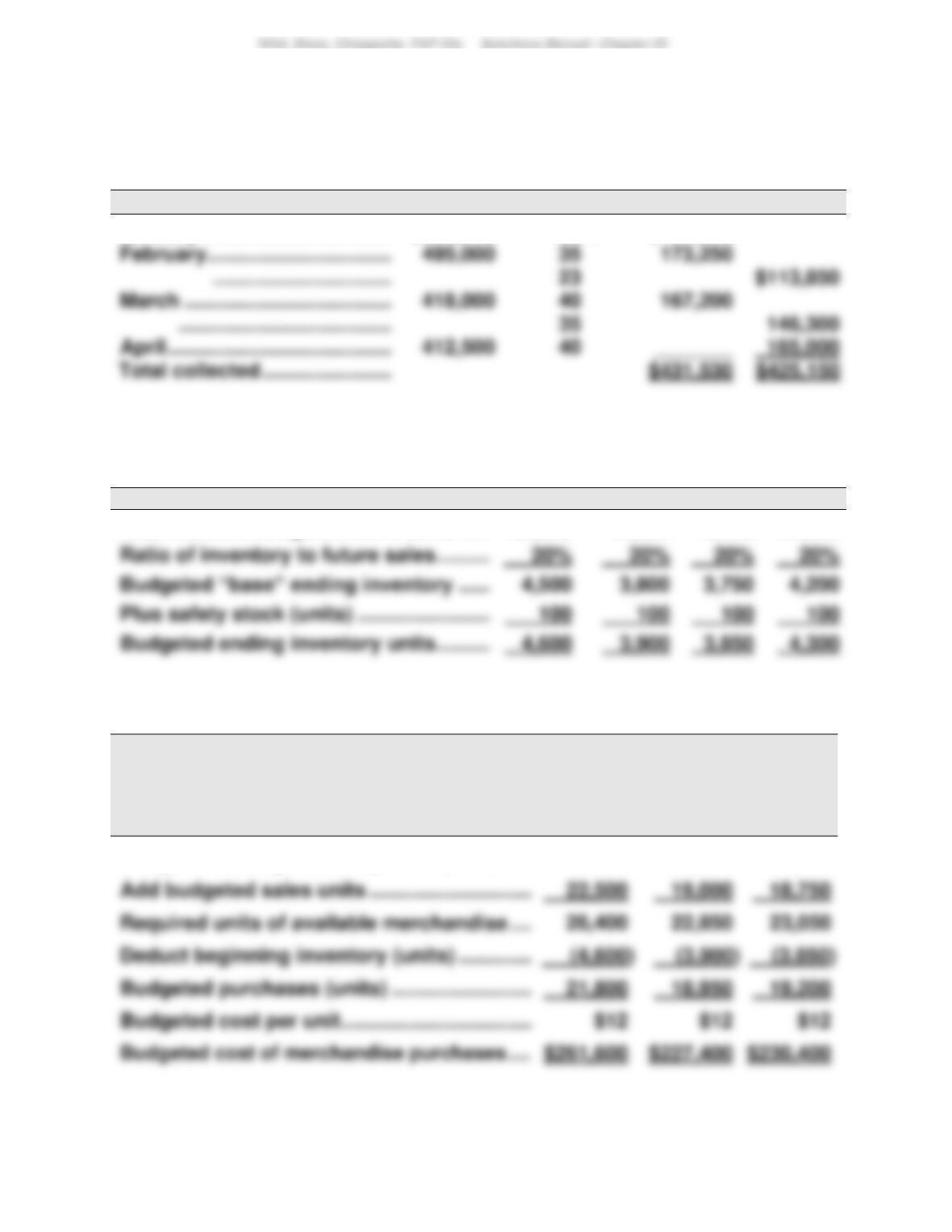

Cash collections of credit sales (accounts receivable)

From sales in

Total

% Collected

March

April

January …………………………..…..

$396,000

23%

$ 91,080

February ………………………………

173,250

March ………………………………….

167,200

Part 2

Budgeted ending inventories (in units)

January

February

March

April

Next month’s budgeted sales units ………..

22,500

19,000

18,750

21,000

Budgeted “base” ending inventory ………..

Part 3

CONNICK COMPANY

Merchandise Purchases Budgets

For February, March, and April

February

March

April

Budgeted ending inventory units (part 2) ………

3,900

3,850

4,300

Required units of available merchandise …….

Budgeted cost per unit ……………………………….

1287

Problem 22-7B (Continued)

Part 4

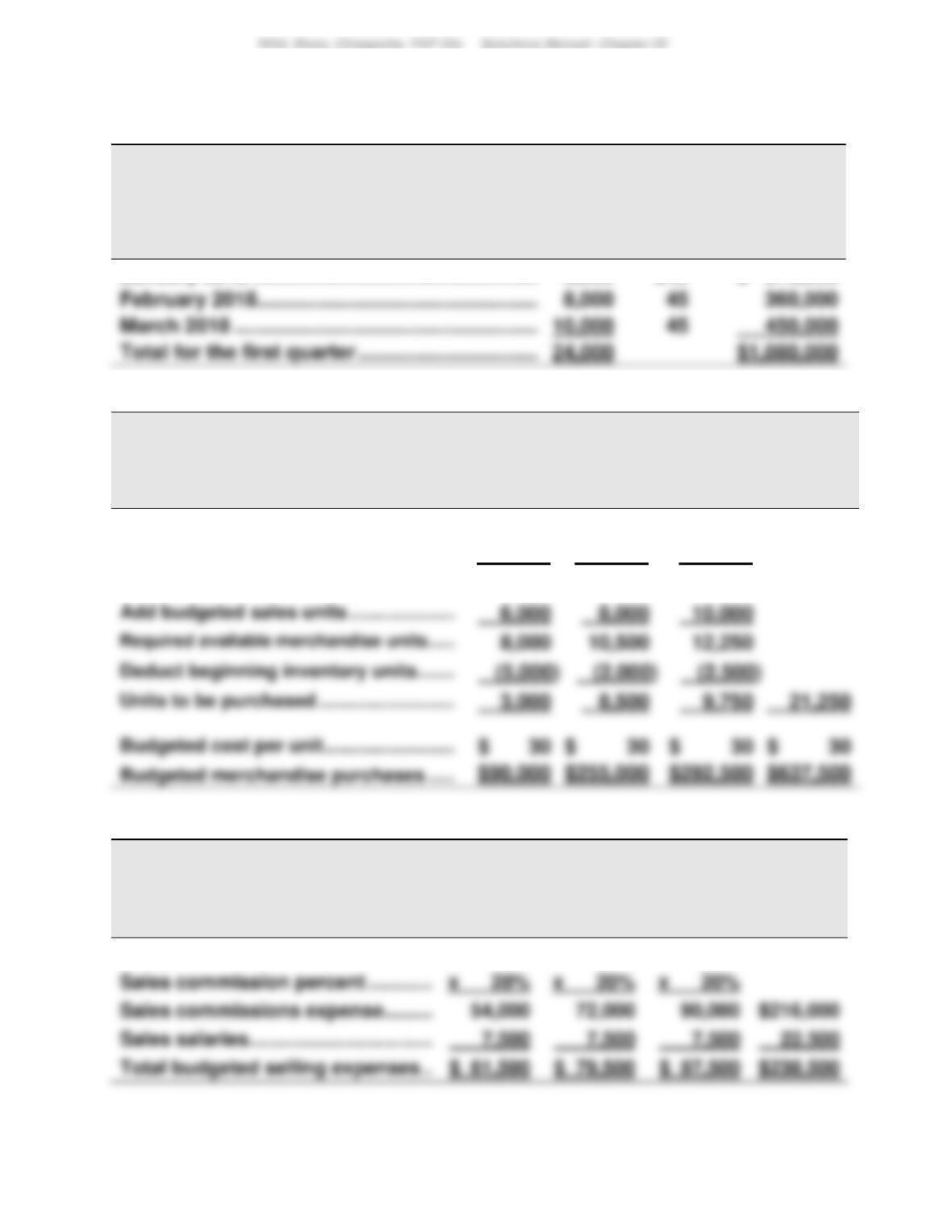

Cash payments on product purchases (for March and April)

From purchases in

Total

% Paid

March

April

February …………………………………

$261,600

70%

$183,120

March …………………………………….

30

70

30

Part 5

CONNICK COMPANY

Cash Budget

March and April

March

April

Beginning cash balance ………………………………………………….

$ 50,000

$ 58,070

Cash payments for:

Additional loan ……………………………………………………….

$ 58,070

$ 94,920

Part 6

Analysis Component: Information about the supply of cash in the near future

would be helpful to the management of Connick Company. A good cash

1288

Problem 22-8B (130 minutes)

Part 1

ISLE CORPORATION

Sales Budgets

January, February, and March 2018

Budgeted

Units

Budgeted

Unit Price

Budgeted

Total Dollars

January 2018 ……………………………………………….

6,000

$45

$ 270,000

February 2018………………………………………………

8,000

March 2018 ………………………………………………….

Part 2

ISLE CORPORATION

Merchandise Purchases Budgets

January, February, and March 2018

January

February

March

Total

Next month’s budgeted sales units …..

8,000

10,000

9,000

Ratio of inventory to future sales ………

x 25%

x 25%

x 25%

Budgeted ending inventory units ………

2,000

2,500

2,250

Deduct beginning inventory units ……..

(5,000)

Units to be purchased ………………………

Budgeted cost per unit ……………………..

Part 3

ISLE CORPORATION

Selling Expense Budgets

January, February, and March 2018

January

February

March

Total

Budgeted sales …………………………..

$270,000

$360,000

$450,000

Sales commission percent ………………

Sales commissions expense ……………

Sales salaries………………………………….

1289

Problem 22-8B (Continued)

Part 4

ISLE CORPORATION

General and Administrative Expense Budgets

January, February, and March 2018

January

February

March

Total

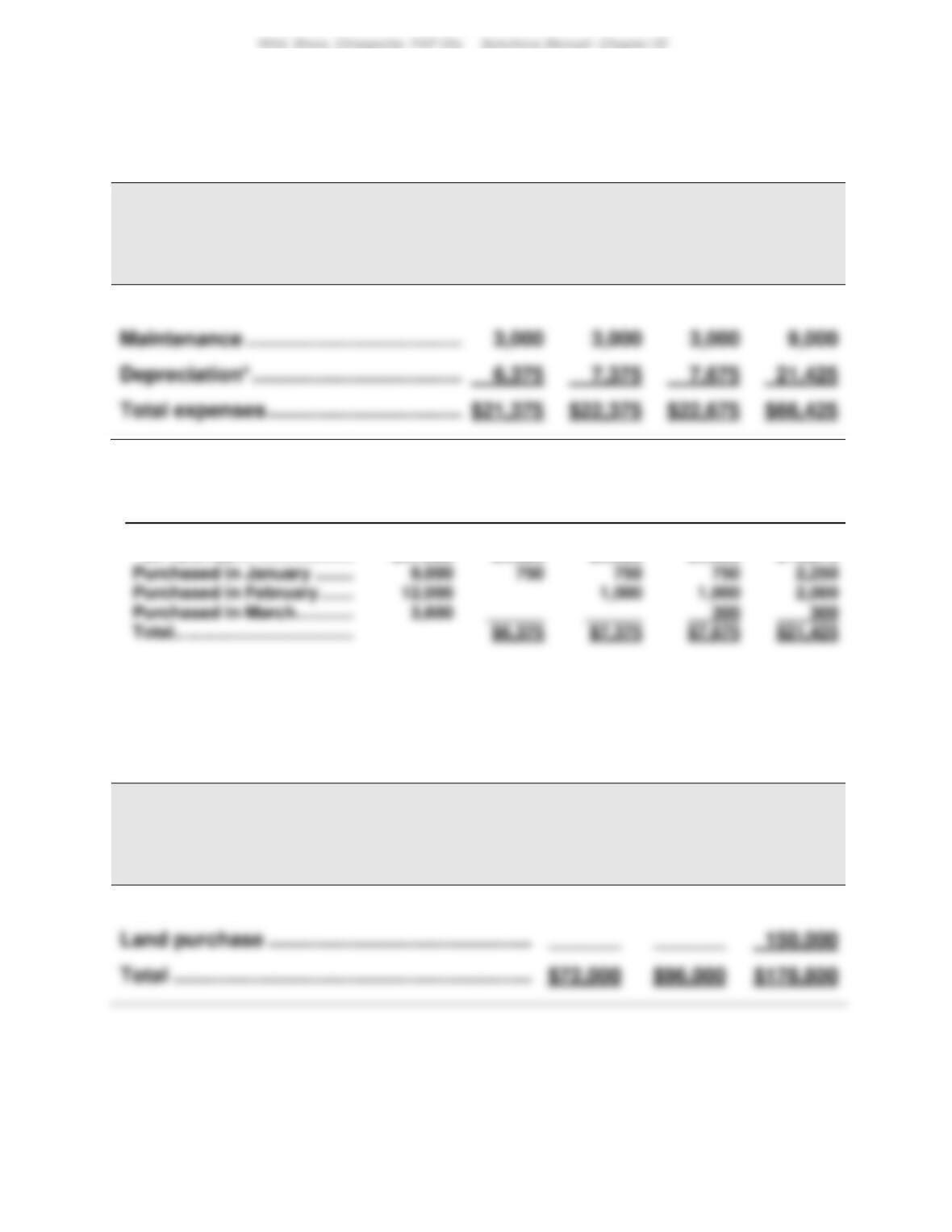

Salaries …………………………..…………………..

$12,000

$12,000

$12,000

$36,000

Depreciation* ……………………………………….

* Depreciation expense calculations

Annual

Amount

January

February

March

Total

Equipment owned

on 12/31/2017 ………………..

$67,500

$5,625

$5,625

$5,625

$16,875

2,250

12,000

Part 5

ISLE CORPORATION

Capital Expenditures Budgets

January, February, and March 2018

January

February

March

Equipment purchases …………………………………..

$72,000

$96,000

$ 28,800

1290

Problem 22-8B (Continued)

Part 6

ISLE CORPORATION

Cash Budgets

January, February, and March 2018

January

February

March

Beginning cash balance ………………………………..

$ 36,000

$182,850

$ 107,850

Cash receipts from customers (note A)…………….

382,500

421,500

355,500

Total cash available ………………………………………

418,500

604,350

463,350

Cash payments for:

306,000

123,000

Sales salaries …………………………..…………………

General & administrative salaries ………………..

12,000

12,000

12,000

Maintenance expense …………………………………

Taxes payable …………………………………………….

90,000

Purchases of equipment …………………………..

72,000

96,000

28,800

Purchase of land …………………………………………

76,950

Supporting calculations

January

February

March

Total

Note A: Cash receipts from customers

Total sales …………………………………………………

$270,000

$360,000

$450,000

$1,080,000

Cash sales (25%) ……………………………………….

$ 67,500

$ 90,000

$112,500

$ 270,000

Credit sales (75%) ……………………………………..

$202,500

$270,000

$337,500

$ 810,000

Cash collections

Receivables at 12/31/2017 (60%; 40%) ………..

$315,000

$210,000

$ 525,000

January credit sales (60%; 40%) ………………..

$ 81,000

Total from credit customers ……………………….

$315,000

Cash sales…………………………………………………

270,000

Total cash received ……………………………………

$382,500

$421,500

$355,500

$1,159,500

Credit purchases ……………………………………….

$255,000

$292,500

$637,500

Accounts payable at 12/31/2017 (20%; 80%) .

$288,000

$360,000

January purchases (20%; 80%) ………………….

1291

Problem 22-8B (Continued)

Part 7

ISLE CORPORATION

Budgeted Income Statement

For Three Months Ended March 31, 2018

Sales ……………………………………………………………………..

$1,080,000

Cost of goods sold (24,000 units @ $30) …………………

720,000

Gross profit …………………………………………………………..

360,000

$216,000

305,075

Income before taxes ………………………………………………

21,970

Part 8

ISLE CORPORATION

Budgeted Balance Sheet

March 31, 2018

ASSETS

Cash …………………………..……………………….

$ 36,000

Cash budget

Accounts receivable …………………………..

445,500

Note C

Note D

Total current assets …………………………..

549,000

Equipment …………………………………………..

$736,800

Note E

Less accumulated depreciation ……………

88,925

647,875

Note F

Capital budget

Total assets …………………………..…………….

$1,346,875

LIABILITIES AND EQUITY

Bank loan payable ……………………………….

Cash budget

Taxes payable (due 4/15/2018) ……………..

Income stmt.

Total liabilities ……………………………………..

595,420

Common stock …………………………………….

$472,500

Unchanged

Retained earnings ………………………………..

278,955

Note H

Total stockholders’ equity ……………………

1292

Problem 22-8B (Concluded)

Supporting Footnotes

Note C

Beginning receivables ……………………………………………………….

$ 525,000

Credit sales ………………………………………………………………………..

Less collections …………………………………………………………………

Note D

Beginning inventory ……………………………………………………….

$ 150,000

Purchases ………………………………………………………………………….

Less cost of goods sold ……………………………………………………..

*Also equals 2,250 units @ $30 = $67,500

Note E

Beginning equipment …………………………..…………………………..

$ 540,000

Purchased in January ……………………………………………………….

72,000

Purchased in February……………………………………………………….

Purchased in March ……………………………………………………….

28,800

Note F

Beginning accumulated depreciation …………………………..………

$ 67,500

Depreciation expense ……………………………………………………….

21,425

Note G

Beginning accounts payable ……………………………………………….

Purchases ………………………………………………………………………….

Payments …………………………………………………………………………..

Note H

Beginning retained earnings ……………………………………………….

Net income …………………………………………………………………………

32,955

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 22

1293

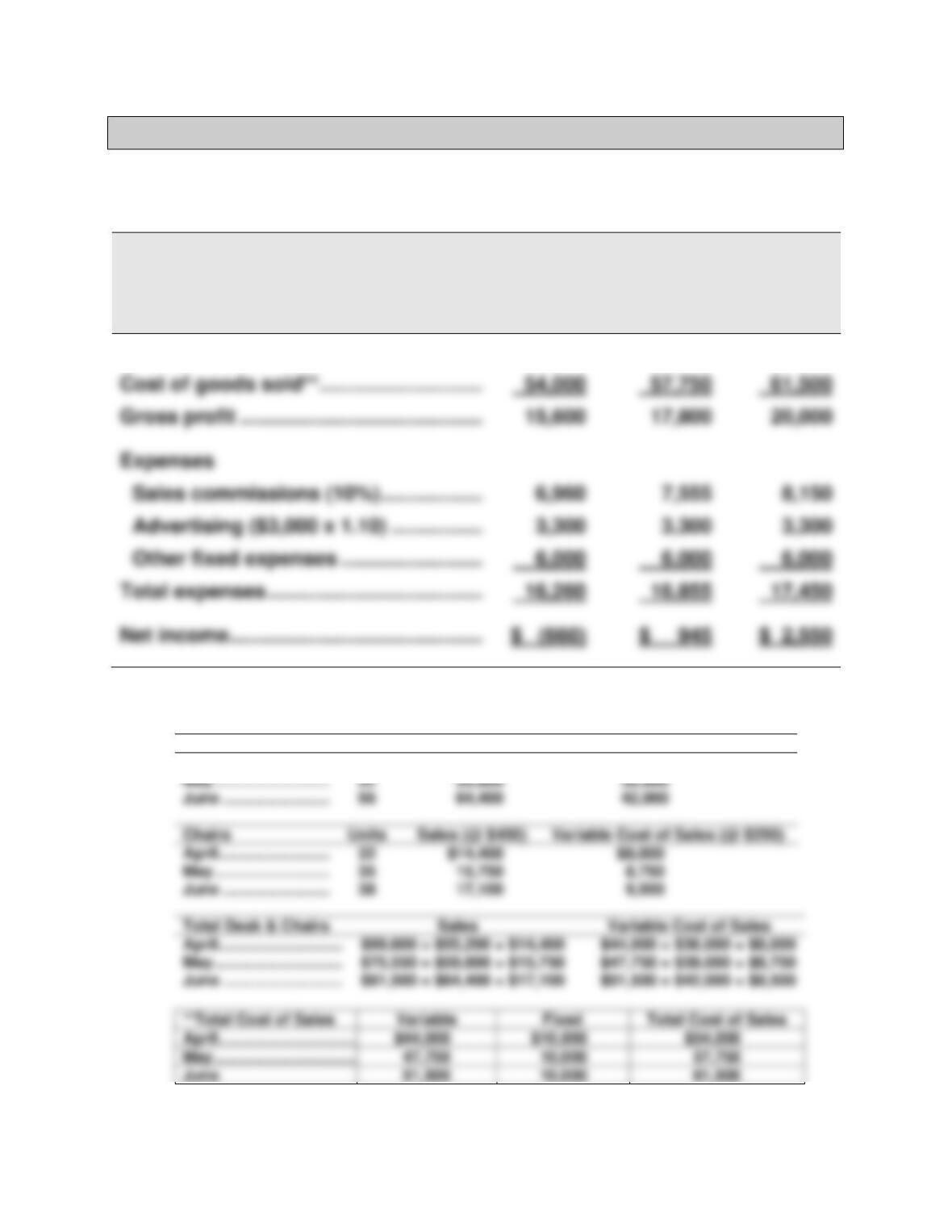

Serial Problem — SP 22

Serial Problem, Business Solutions (50 minutes)

Part 1

BUSINESS SOLUTIONS—Computer Furniture Segment

Budgeted Income Statements

For Months of April, May, and June

April

May

June

Sales* …………………………………………………

$69,600

$75,550

$81,500

*Results from per month volume increases for the next 3 months

Desks

Units

Sales (@ $1,150)

Variable Cost of Sales (@ $750)

April …………………………..

48

$55,200

$36,000

52

June …………………………..

56

Chairs

Units

Variable Cost of Sales (@ $250)

April …………………………..

32

$14,400

35

June …………………………..

38

April …………………………..

June …………………………..

April …………………………..

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 22

1294

Serial Problem, Business Solutions (Concluded)

Part 2

The plan for increasing sales volume by reducing the price and increasing

advertising would cause the company to generate a loss in the first month

Reporting in Action — BTN 22-1

1. Apple’s statement of cash flows would report cash paid for acquisitions

2. a. Cash paid for acquisitions of property, plant and equipment and

reported on the statement of cash flows for the year ended

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 22

1295

Comparative Analysis — BTN 22-2

1. 1. Apple and Google figures for the most recent 3 years—data available

from Appendix A—are shown below ($ millions):

Apple

Two Years

Prior

One Year

Prior

Current

Year

One

Year

Ahead

Two

Years

Ahead

Google

Two Years

Prior

One Year

Prior

Current

Year

One

Year

Ahead

Two

Years

Ahead

Sales

$55,519

$66,001

$74,989

_______

_______

2. Predictions will vary among students. Based on these three years,

Apple’s SGA/Sales ratio averages 6.35%, while Google’s averages

Sales

_______

_______

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 22

1296

Ethics Challenge — BTN 22-3

Report on “Use It or Lose It” Budgeting

Instructor note: There is no widely accepted solution to this problem. The key is for the student to

think about the problem and work to at least modify the negative behavioral consequences of this

practice.

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 22

Communicating in Practice — BTN 22-4

MEMORANDUM

TO: ____________________

FROM: ____________________

DATE: ____________________

SUBJECT: ____________________

The content of this memorandum will vary among students. The student

Taking It to the Net — BTN 22-5

1. The “e–budgets” Website lists a number of benefits such as accuracy, timeliness, ease of

sharing information, ease of updating, real-time comparison of actual performance vs.

estimates, and so on.

2. As a senior manager, my biggest concern would be security, particularly

when the system is easily accessible and usable. It would be important

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 22

1298

Teamwork in Action — BTN 22-6

There is no specific solution to this assignment. The instructor should

watch for proper development and identification of all reasonable costs.

Entrepreneurial Decision — BTN 22-7

1. Budgeting allows an organization to plan its activities better by

2. To expand their operations, Marilyn and Michelle will need financing.

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 22

1299

Hitting the Road — BTN 22-8

Instructor note: This problem is designed to (1) show that external factors are important

1. & 2.

The types of external factors identified by the student for consideration in

part (1), or selected as an explanatory factor for part (2), might include the

following:

• Location, such as near a convenient or busy traffic area.

Global Decision — BTN 22-9

1. The selling and administrative expenses budget is likely to be an

important budget in the master budgeting process at Samsung. In 2015,

2. General office expenses

3. The initial responsibility usually rests with a vice president or an